73

NAVIGATING THE NEW NORMAL David A. Rosenberg October 2012 TM

| Date post: | 18-Apr-2015 |

| Category: |

Documents |

| Upload: | annawitkowski88 |

| View: | 38,150 times |

| Download: | 4 times |

NAVIGATING THE NEW NORMAL

David A. Rosenberg

October 2012

TM

WHAT, ME WORRY?

1

Note:

Source: The Atlantic, April 2012 2

Yes, I am

more worried

than I look!

LET’S PLAY “RISK”

The staff also reported on potential risks to financial stability, including those owing to the developments in Europe and to the current environment of low interest rates.

The staff viewed the uncertainty around the forecast for economic activity as elevated and the risks skewed to the downside, largely reflecting concerns about the situation in Europe and the possibility of a more severe tightening in U.S. fiscal policy than anticipated.

In addition, participants still saw significant downside risks to the outlook for economic growth. Prominent among these risks were a possible intensification of strains in the euro zone, with potential spillovers to U.S. financial markets and institutions and thus to the broader U.S. economy; a larger-than-expected U.S. fiscal tightening; and the possibility of a further slowdown in global economic growth.

However, participants also observed that significant risks related to the euro-area banking and fiscal crisis remained, and that a number of important issues would have to be resolved in order to achieve further progress toward a comprehensive solution to the crisis.

Moreover, while the sovereign and banking crisis in Europe had eased some recently, members still saw strains in global financial conditions as posing significant downside risks to the economic outlook. The possibility of a larger-than-expected fiscal tightening in the United States and slower global growth were also seen as downside risks.

The Minutes from the September 12 - 13, 2012 Federal Open Market Committee Meeting, released on October 4, 2012

3

4

U.S. GOVERNMENT SPENDING $1.50 FOR EVERY $1.00 IN REVENUE

United States: Net Outlays/Net Receipts

Note:

Shaded bar and represents the OMB estimate

Source: Office of Management and Budget, U.S. Treasury

(ratio)

5

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09 12

Deficit

Surplus

Unheard of

outside of WWII

CENTRAL BANKS RADICALLY EXPANDED THEIR BALANCE SHEETS

Note:

Source: Haver Analytics

U.S., U.K., ECB, and Japan Central Bank Assets as Percent of Combined GDP

6

(percent)

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

26.0%

2006 2007 2008 2009 2010 2011 2012

Unprecedented!

CALL IT THE WILE E. COYOTE ECONOMY

7

3.7%

3.3% 3.3%

4.5%

1.7% 1.7%

3.0%

1.4%

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

5%

61 Q1 70 Q4 75 Q1 82 Q4 91 Q1 01 Q4 Avg. Current

Last Quarter of Recession

5.0%

8.2%

9.2%

7.6%

3.8%4.0%

6.3%

3.1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

61 Q1 70 Q4 75 Q1 82 Q4 91 Q1 01 Q4 Avg. Current

Last Quarter of Recession

A SUB-PAR U.S. ECONOMIC RECOVERY

Note:

Source: Bureau of Economic Analysis, Bureau of Labour Statistics

United States: 12 Quarters After A Recession Ends

Real GDP per capita (annualized percent change)

Nominal GDP per capita (annualized percent change)

8

9

-4.0

0.0

4.0

8.0

12.0

16.0

20.0

58 63 68 73 78 83 88 93 98 03 08

Debt deleveraging

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Down 43%!

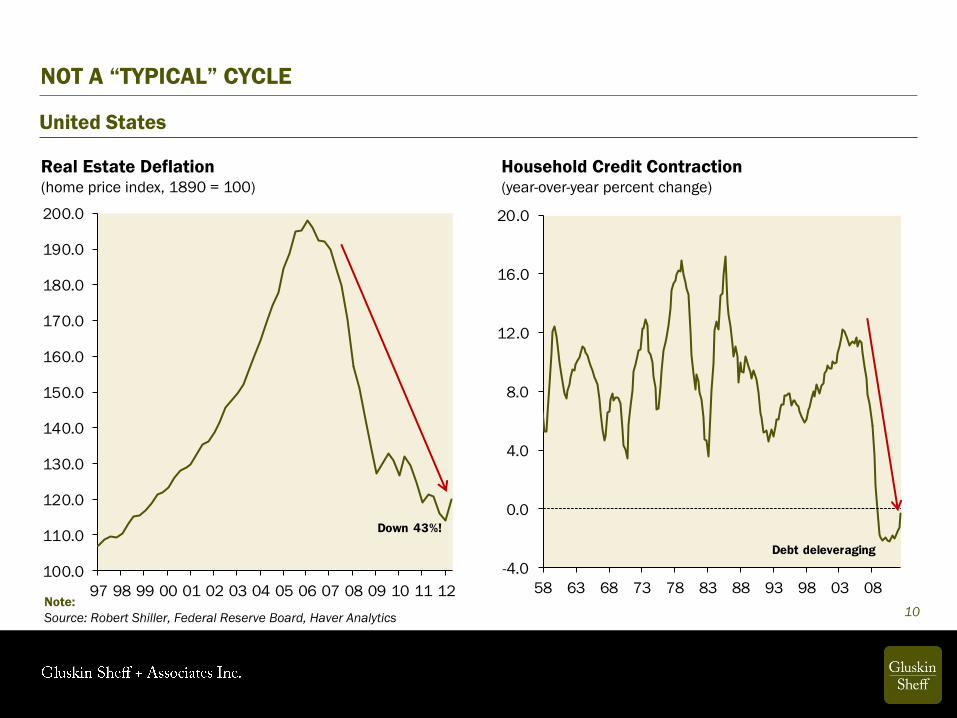

Real Estate Deflation (home price index, 1890 = 100)

NOT A “TYPICAL” CYCLE

Note:

Source: Robert Shiller, Federal Reserve Board, Haver Analytics

United States

Household Credit Contraction (year-over-year percent change)

10

-4

-2

0

2

4

6

8

10

12

14

16

57 60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08 11

(five-year percent change at an annual rate)

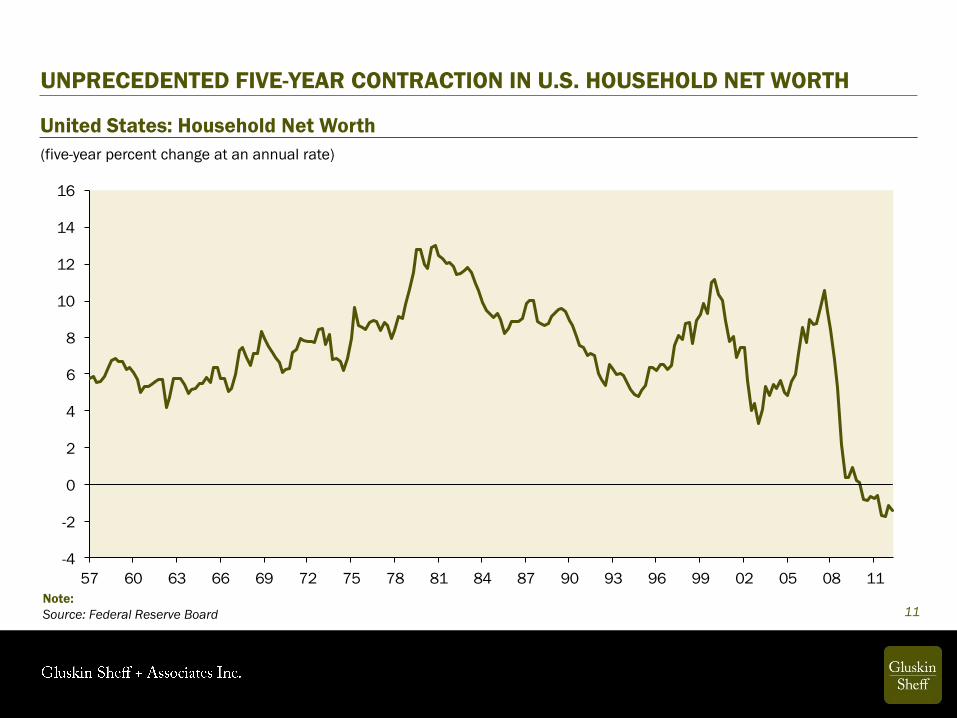

UNPRECEDENTED FIVE-YEAR CONTRACTION IN U.S. HOUSEHOLD NET WORTH

Note:

Source: Federal Reserve Board

United States: Household Net Worth

11

11

12

13

14

15

16

17

18

19

20

21

22

23

'72 '77 '82 '87 '92 '97 '02 '07 '12

60

70

80

90

100

110

120

130

140

'72 '77 '82 '87 '92 '97 '02 '07 '12

STILL MORE TO GO BEFORE THE HOUSEHOLD BALANCE SHEET IS REPAIRED

Note:

Source: Federal Reserve Board

United States

Household Debt-to-Income Ratio Household Debt-to-Asset Ratio

Pre-bubble average Pre-bubble average

(percent)

12

Findings from McKinsey & Company:

“While we cannot say for certain whether

these sectors will deleverage, we do know

that nearly every significant financial crisis in

the post-World War II period was followed by

a lengthy and painful period of

deleveraging. These episodes lasted on

average six to seven years, with total debt

as a percentage of GDP declining by

roughly 25 percent. GDP contracted in the

initial years of deleveraging but rebounded

in the later years. If history is a guide,

therefore, we would expect a significant

period of deleveraging to come, which will

dampen GDP growth.”

MCKINSEY ON FINANCE: PERSPECTIVE ON CORPORATE FINANCE & STRATEGY

13

LIFE AFTER THE CREDIT COLLAPSE -- FAT TAIL RISK

14

Distribution of Outcomes before the Credit Collapse

Distribution of Outcomes after the Credit Collapse

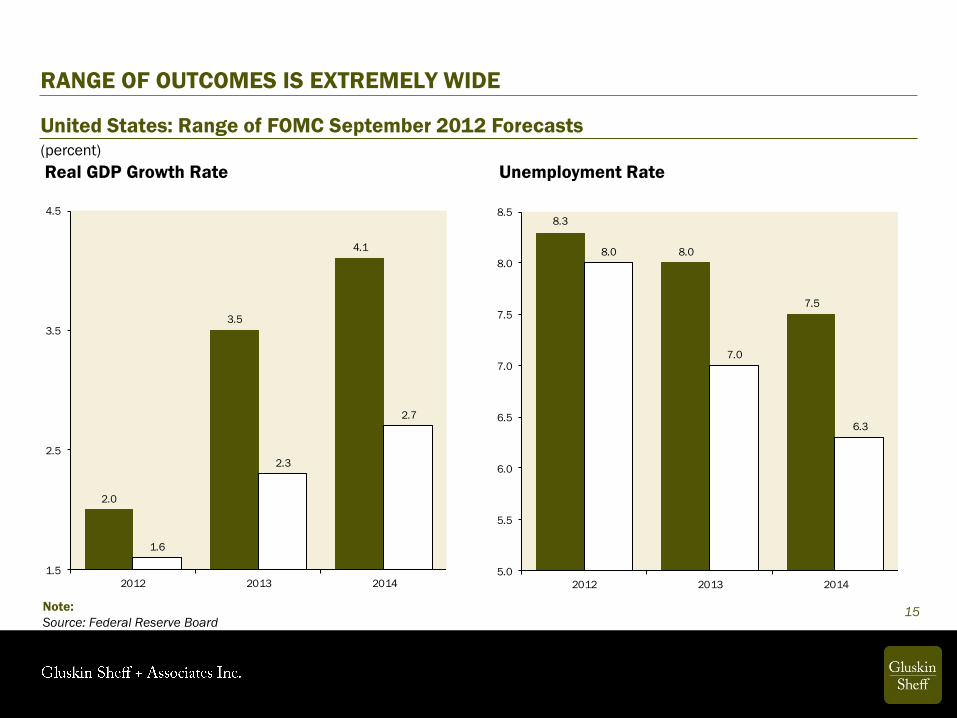

RANGE OF OUTCOMES IS EXTREMELY WIDE

Note:

Source: Federal Reserve Board

United States: Range of FOMC September 2012 Forecasts

Real GDP Growth Rate Unemployment Rate

15

2.0

3.5

4.1

1.6

2.3

2.7

1.5

2.5

3.5

4.5

2012 2013 2014

8.3

8.0

7.5

8.0

7.0

6.3

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

2012 2013 2014

(percent)

WHAT HAVE WE LEARNED IN 2,604 YEARS?

“The budget should be balanced, the Treasury should be

refilled, public debt should be reduced, the arrogance of

officialdom should be tempered and controlled, and the

assistance to foreign lands should be curtailed lest

Rome become bankrupt. People must again learn

to work, instead of living on public assistance.”

Cicero - 55 BC

16

64

69 7072

74 74 7473

70 7072

7375

7675

73

80

91

98

102

106

55

65

75

85

95

105

115

'92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

THE WORLD IS AWASH IN DEBT

Notes:

Shaded bars represent OECD estimates

Source: OECD

OECD: Gross General Government Debt-to-GDP Ratio

(percent of nominal GDP)

17

18

0%

10%

20%

30%

40%

50%

60%

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

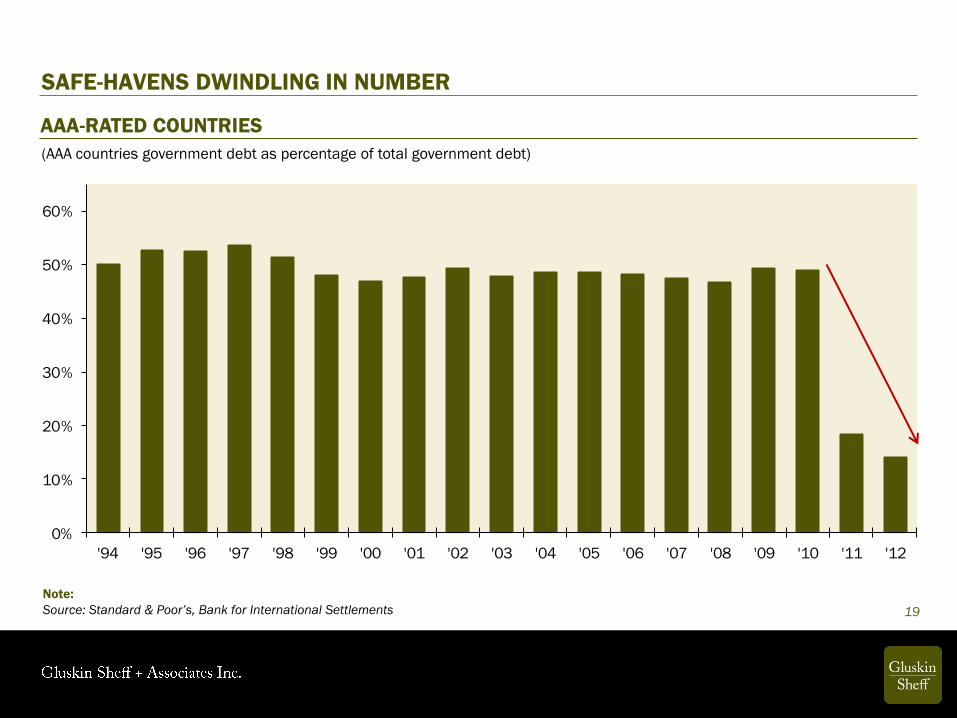

SAFE-HAVENS DWINDLING IN NUMBER

Note:

Source: Standard & Poor’s, Bank for International Settlements 19

AAA-RATED COUNTRIES

(AAA countries government debt as percentage of total government debt)

0

100

200

300

400

500

600

700

800

TOO MUCH DEBT AT ALL LEVELS

Note:

Source: Haver Analytics

* Q1 data are not available, using the last available data

Domestic Debt Outstanding as a % of adjusted GDP (Q1 2012)

20

IS THIS REALLY THE END?

21

Note:

Source: The Economist, November 26, 2011

INTEREST RATES DIVERGE IN THE EUROZONE TO THE PRE-EMU LEVELS

Notes:

Source: Bloomberg

10-Year Government Bond Yield

(percent)

22

19.2

8.7

5.85.0 4.9

2.4 2.21.7 1.3

0

5

10

15

20

25

Greece Portugal Spain Ireland Italy Belgium France Netherlands Germany

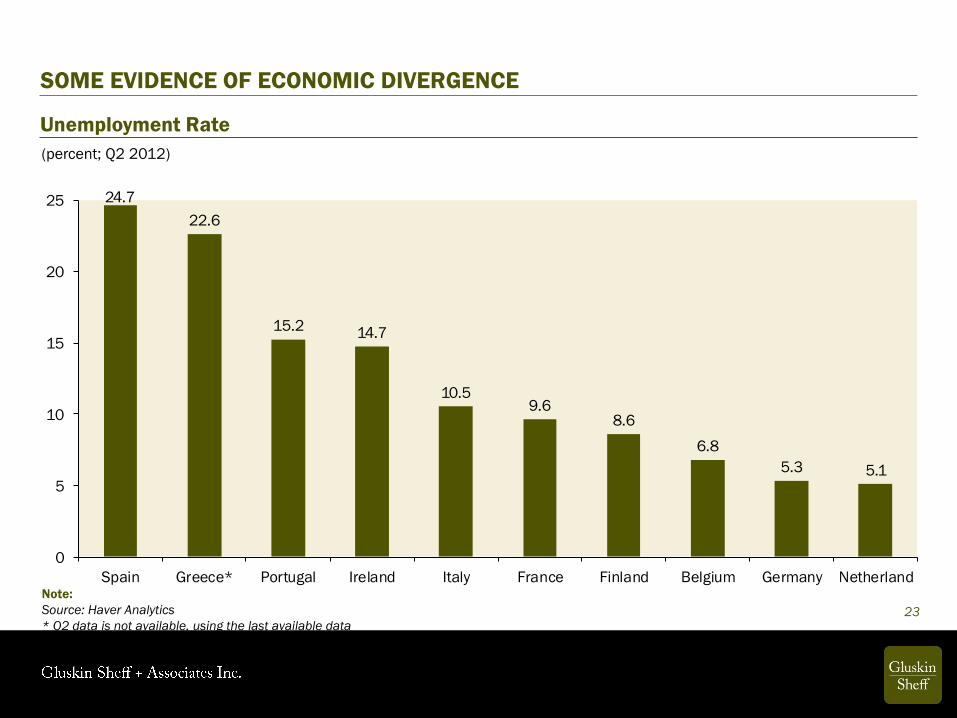

24.7

22.6

15.214.7

10.59.6

8.6

6.8

5.3 5.1

0

5

10

15

20

25

Spain Greece* Portugal Ireland Italy France Finland Belgium Germany NetherlandNote:

Source: Haver Analytics

* Q2 data is not available, using the last available data

Unemployment Rate

(percent; Q2 2012)

SOME EVIDENCE OF ECONOMIC DIVERGENCE

23

1.0

0.3 0.2

-0.3-0.6

-1.3

-2.6-3.2

-6.3-7

-6

-5

-4

-3

-2

-1

0

1

2

3

Germany France Finland Belgium Netherland Spain Italy Portugal Greece

MORE EVIDENCE OF ECONOMIC DIVERGENCE

Year-over-Year GDP Growth Rate

Notes:

Source: Haver Analytics, Gluskin Sheff

(percent; Q2 2012)

24

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

'07 '08 '09 '10 '11 '12

-6

-5

-4

-3

-2

-1

0

1

2

3

4

'07 '08 '09 '10 '11 '12

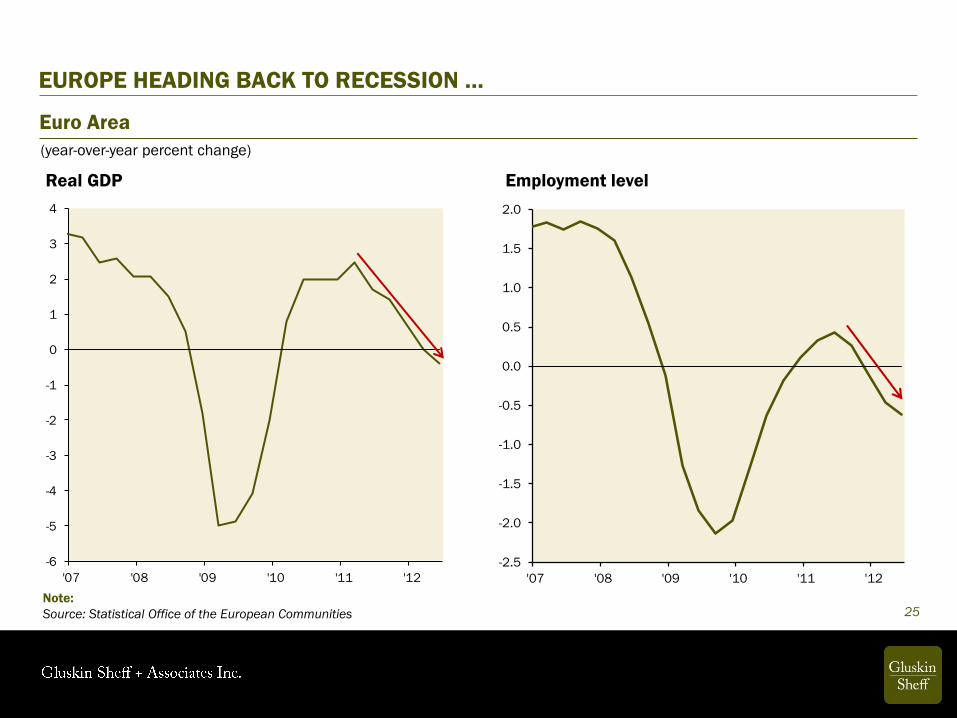

EUROPE HEADING BACK TO RECESSION …

Note:

Source: Statistical Office of the European Communities

Euro Area

25

Real GDP Employment level

(year-over-year percent change)

… AND LIKELY TO REMAIN THAT WAY FOR SOME TIME

Note:

Source: OECD, Haver Analytics

Euro Area: Leading Indicator

(year-over-year percent change)

26

-6

-4

-2

0

2

4

6

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

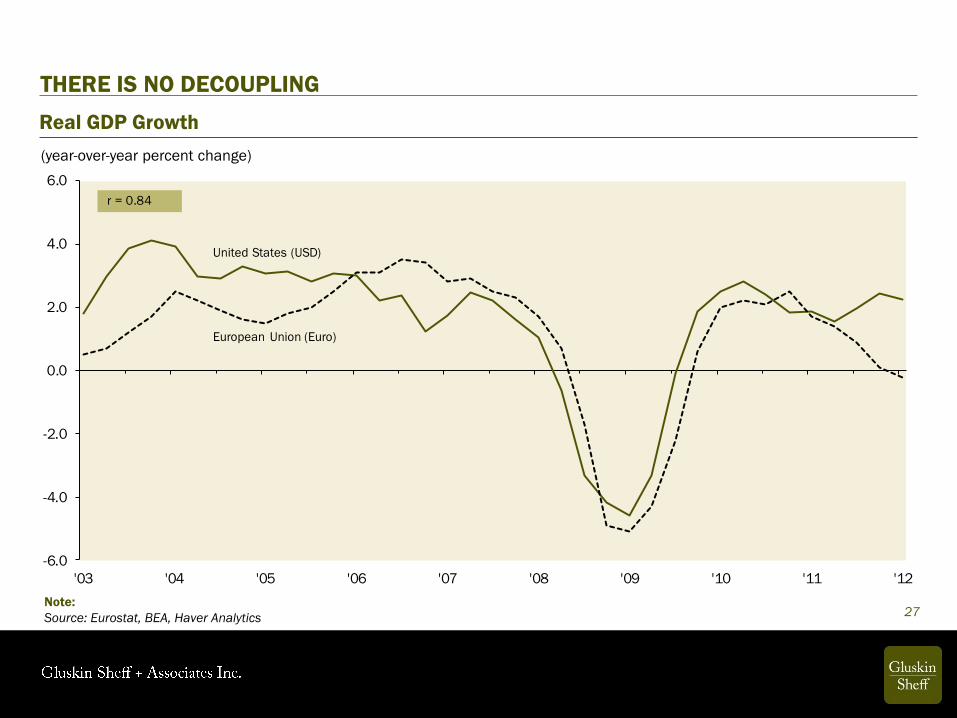

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12

r = 0.84

United States (USD)

European Union (Euro)

THERE IS NO DECOUPLING

Note:

Source: Eurostat, BEA, Haver Analytics

Real GDP Growth

27

(year-over-year percent change)

-40

-30

-20

-10

0

10

20

30

40

50

'07 '08 '09 '10 '11 '12

-40

-30

-20

-10

0

10

20

30

40

50

60

'07 '08 '09 '10 '11 '12

EUROPEAN RECESSION ALREADY CAUSING ASIAN EXPORTS TO DECLINE

Note:

Source: China Customs, Korea Custom Services, Haver Analytics

Exports

Korea China

28

(year-over-year percent change)

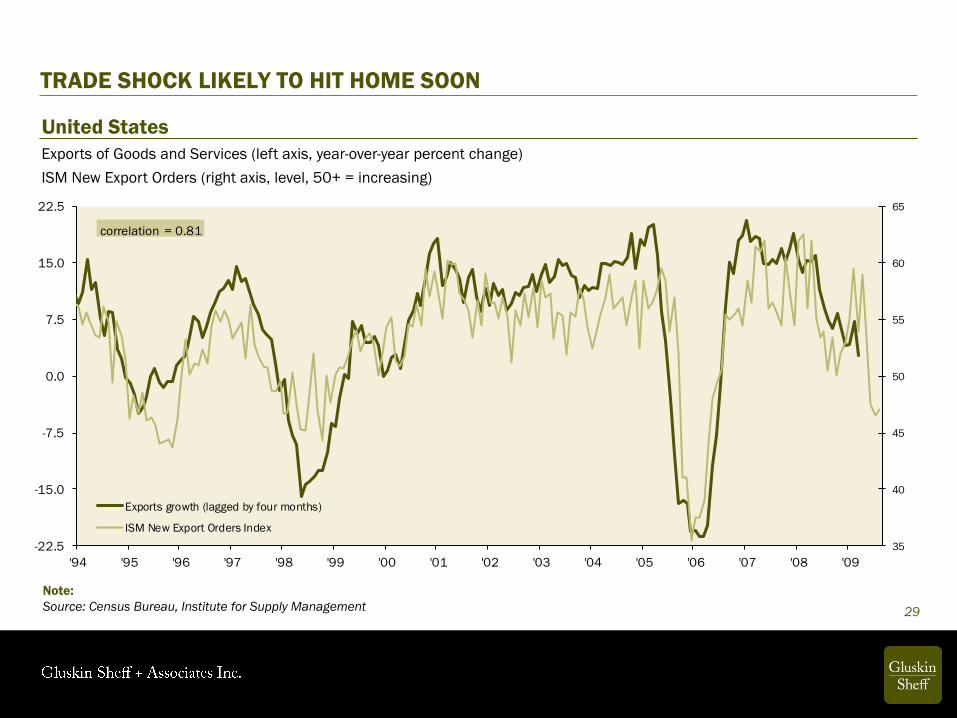

TRADE SHOCK LIKELY TO HIT HOME SOON

Exports of Goods and Services (left axis, year-over-year percent change)

United States

Note:

Source: Census Bureau, Institute for Supply Management

ISM New Export Orders (right axis, level, 50+ = increasing)

29

35

40

45

50

55

60

65

-22.5

-15.0

-7.5

0.0

7.5

15.0

22.5

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09

Exports growth (lagged by four months)

ISM New Export Orders Index

correlation = 0.81

30

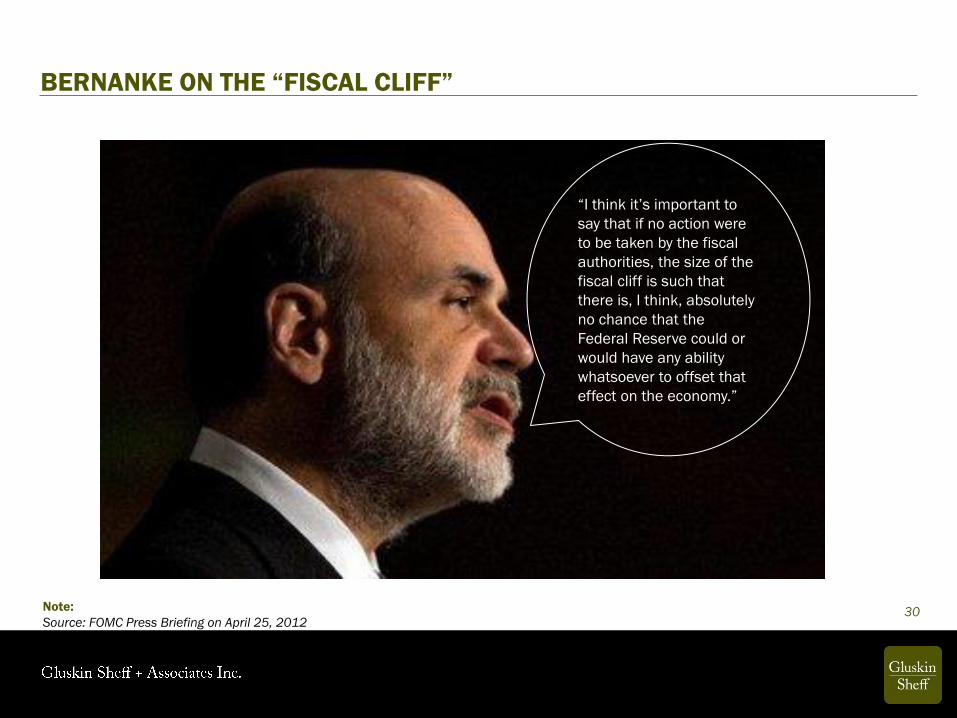

“I think it’s important to

say that if no action were

to be taken by the fiscal

authorities, the size of the

fiscal cliff is such that

there is, I think, absolutely

no chance that the

Federal Reserve could or

would have any ability

whatsoever to offset that

effect on the economy.”

BERNANKE ON THE “FISCAL CLIFF”

Note:

Source: FOMC Press Briefing on April 25, 2012

-7%

-5%

-3%

-1%

2%

4%

57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11 13

Record Drag!Net Fiscal

Drag

Net Fiscal

Stimulus

THE FISCAL CLIFF

Notes:

2013 is based on CBO estimates of the fiscal balance

Source: CBO, Haver Analytics

Change in Primary Fiscal Balance to GDP Ratio

31

(percentage points)

5

7

9

11

13

15

17

19

21

'70 '75 '80 '85 '90 '95 '00 '05 '10 '15 '20

25

35

45

55

65

75

85

95

105

115

'70 '75 '80 '85 '90 '95 '00 '05 '10 '15 '20

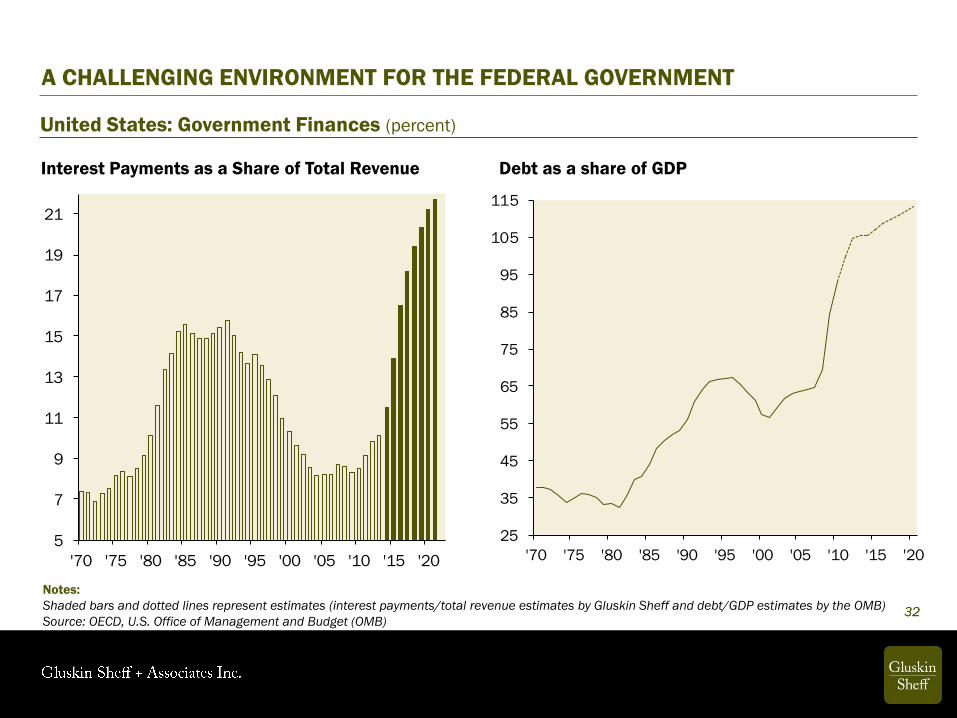

A CHALLENGING ENVIRONMENT FOR THE FEDERAL GOVERNMENT

Notes:

Shaded bars and dotted lines represent estimates (interest payments/total revenue estimates by Gluskin Sheff and debt/GDP estimates by the OMB)

Source: OECD, U.S. Office of Management and Budget (OMB)

United States: Government Finances (percent)

Interest Payments as a Share of Total Revenue Debt as a share of GDP

32 32

-6

-4

-2

0

2

4

6

8

10

'06 '07 '08 '09 '10 '11 '12

-40

-30

-20

-10

0

10

20

30

'93 '95 '97 '99 '01 '03 '05 '07 '09 '11

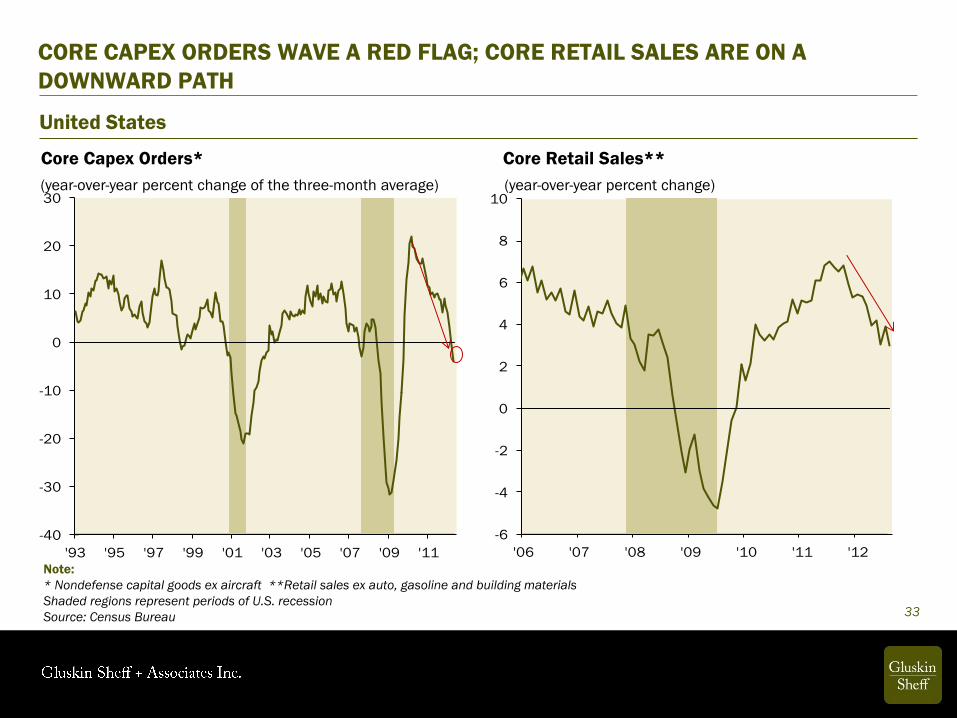

CORE CAPEX ORDERS WAVE A RED FLAG; CORE RETAIL SALES ARE ON A

DOWNWARD PATH

Note:

* Nondefense capital goods ex aircraft **Retail sales ex auto, gasoline and building materials

Shaded regions represent periods of U.S. recession

Source: Census Bureau

United States

Core Capex Orders*

33

(year-over-year percent change of the three-month average)

Core Retail Sales**

(year-over-year percent change)

Note:

Source: Time Magazine (June 13, 2005) 34

400

800

1,200

1,600

2,000

2,400

2,800

'59 '69 '79 '89 '99 '09

500

550

600

650

700

750

800

Jan/10 Jul/10 Jan/11 Jul/11 Jan/12 Jul/12

Short-term View

HOUSING RECOVERY IN PERSPECTIVE

Note:

Source: Census Bureau, Haver Analytics

United States: Housing Starts

Long-term View

35

(thousands)

260

280

300

320

340

360

380

Aug/10 Feb/11 Aug/11 Feb/12

200

400

600

800

1,000

1,200

1,400

'62 '72 '82 '92 '02 '12

Short-term View

DITTO …

Note:

Source: Census Bureau, Haver Analytics

United States: New Home Sales

Long-term View

36

(thousands)

2

3

4

5

6

7

8

'47 '52 '57 '62 '67 '72 '77 '82 '87 '92 '97 '02 '07 '12

HOUSING DOWN TO A 2% SHARE OF GDP

Note:

Shaded regions represent periods of U.S. recession

Source: Bureau of Economic Analysis

United States: Housing Share of GDP

(year-over-year percent change)

37

4.2

3.93.9

3.3

3.02.9

2.5

2.75

2.0

2.5

3.0

3.5

4.0

4.5

4.14.0

3.9

3.5

2.7

2.5

2.7

2.2

1.85

1.8

2.3

2.8

3.3

3.8

4.3

THE (SLIDING) EVOLUTION OF THE FED'S GDP FORECAST

Note:

Source: Bloomberg

United States: Federal Reserve GDP Forecast

2012 2013

38

(percent)

HELICOPTER BEN BERNANKE ….

39

0.5

1.0

1.5

2.0

2.5

3.0

05 06 07 08 09 10 11 12

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

05 06 07 08 09 10 11 12

Fed Funds Rate (percent)

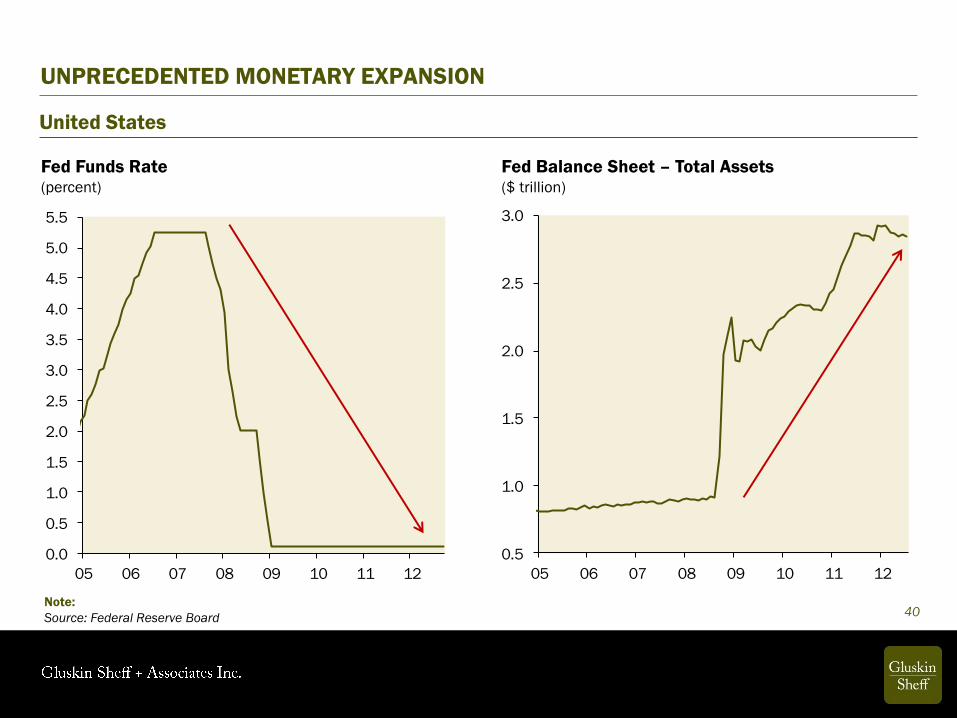

UNPRECEDENTED MONETARY EXPANSION

Note:

Source: Federal Reserve Board

United States

Fed Balance Sheet – Total Assets ($ trillion)

40

RATES ON HOLD FOR ANOTHER THREE YEARS

FOMC meeting – June 22, 2011

The Committee continues to anticipate that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run -- are likely to warrant exceptionally low levels for the federal funds rate for an extended period.

FOMC meeting – August 9, 2011

The Committee currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run -- are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.

FOMC meeting – January 25, 2012

In particular, the Committee decided today to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions -- including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through late 2014.

FOMC meeting – September 13, 2012

In particular, the Committee also decided today to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that exceptionally low levels for the federal funds rate are likely to be warranted at least through mid-2015.

41

Note:

Source: Minutes from FOMC meetings

88%

75%

64% 64%

58%

40% 39%

25%

Fed Policy Core CPI

Inflation

CPI Inflation Core PPI

Inflation

PPI Inflation Budget Deficits CRB Index Oil Prices

WHAT CORRELATES WITH BOND YIELDS

Note:

Source: Haver Analytics

United States

(correlation: percent)

42

0

2

4

6

8

10

12

14

16

18

20

'55 '60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10

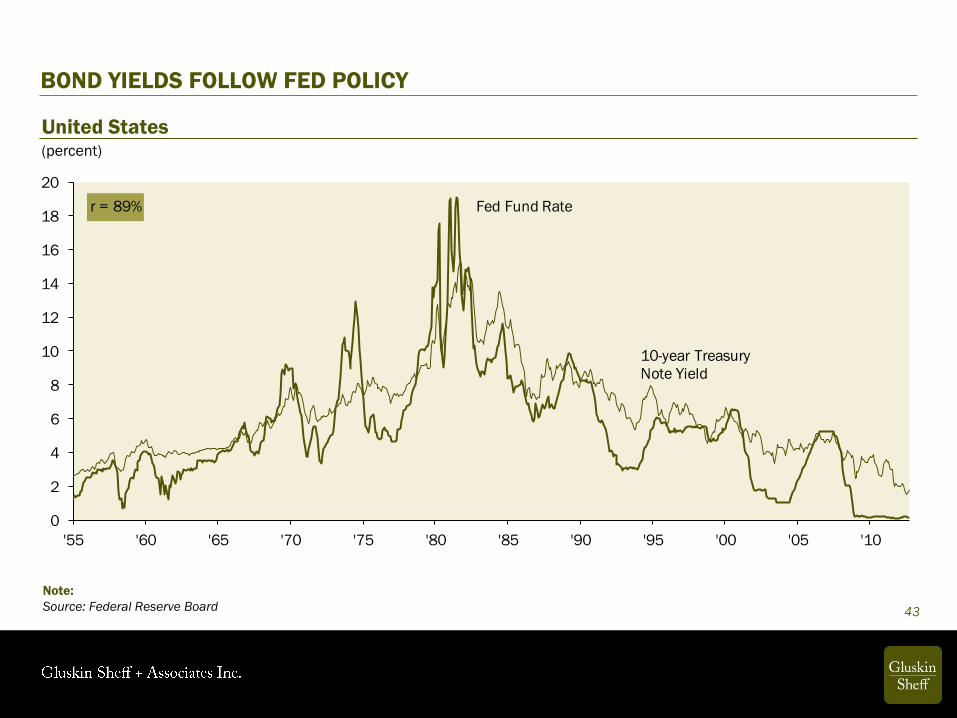

Fed Fund Rater = 89%

10-year Treasury

Note Yield

BOND YIELDS FOLLOW FED POLICY

United States

Note:

Source: Federal Reserve Board 43

(percent)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Fed Funds

Rate

2Y 5Y 10Y 20Y 30Y

+270bps

A Year Ago

?

Today

Historical Avg

A SUPER STEEP U.S. YIELD CURVE: HOW WILL IT FLATTEN?

Note:

Source: Federal Reserve Board

United States: Treasury Yield Curve

Average for Past 30 Years Today (October 2012)

44

(percent)

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Fed Funds

Rate

2Y 5Y 10Y 20Y 30Y

+160bps

Note:

Source: Wall Street Journal, January 3, 2011 45

WHAT THE FED HAS DONE BEYOND INTEREST RATES ─ MULTIPLE QEs

QE1 (December 2008 to March 2010):

• $1.25 trillion of mortgage-backed securities

• $300 billion of long-term Treasuries

• $200 billion of Agency debt

QE2 (November 2010 to June 2011):

• $600 billion of longer-term Treasury securities

Operation Twist (September 2011 to present):

• The Fed bought over $500 billion of long-term Treasury securities and sold an equal amount of short-term Treasury securities

QE3 (September 2012 to ??):

• The Fed will purchase additional Agency mortgage-backed securities at a pace of $40 billion per month, until it is satisfied with the economy’s progress.

46 Note:

Source: Federal Reserve Board

HE SAID WHAT??

“We do think that these policies can bring interest rates down, not just treasury rates but a whole range of rates including mortgage rates and rates for corporate bonds and other types of important interest rates. It also affects stock prices. It affects other prices, home prices, for example.

So looking at all the different channels of effect, we think it does have an impact on the economy. It will have impact on the labor market but again, the way I would describe it is a meaningful effect, a significant effect, but not a panacea, not a solution for the whole issue.”

Ben Bernanke, at the Post-FOMC Meeting Press Conference, September 13, 2012.

47

0.7

0.9

1.1

1.3

1.5

1.7

'03 '04 '05 '06 '07 '08 '09 '10 '11 '121.55

1.60

1.65

1.70

1.75

1.80

1.85

1.90

1.95

2.00

'03 '04 '05 '06 '07 '08 '09 '10 '11

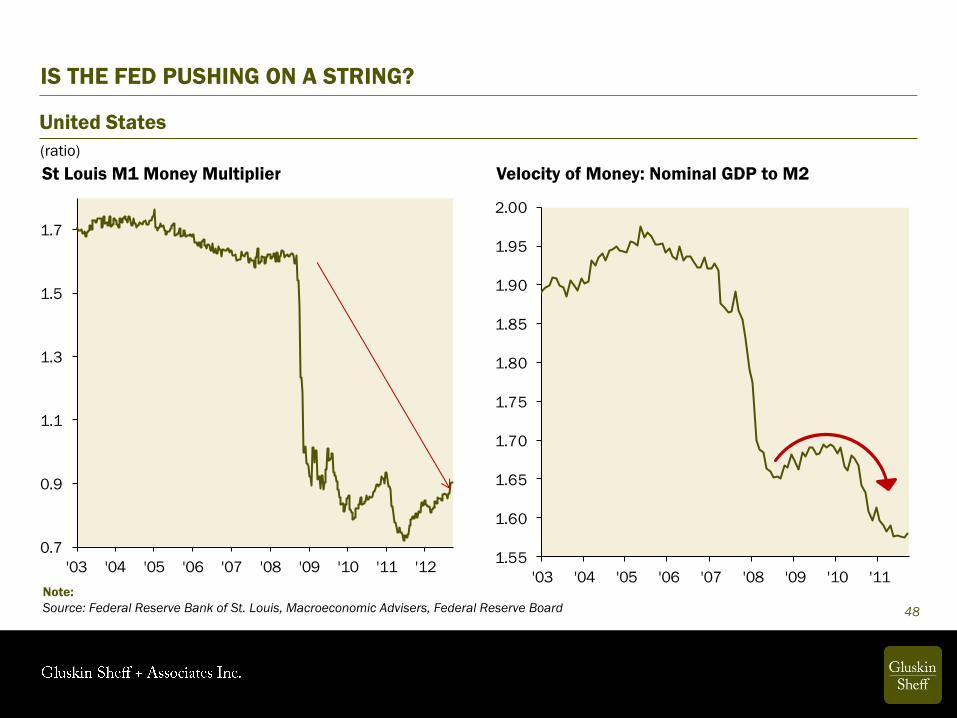

IS THE FED PUSHING ON A STRING?

Note:

Source: Federal Reserve Bank of St. Louis, Macroeconomic Advisers, Federal Reserve Board

United States

Velocity of Money: Nominal GDP to M2

48

St Louis M1 Money Multiplier

(ratio)

250

500

750

1000

1250

1500

1750

'99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

600

700

800

900

1000

1100

1200

1300

1400

1500

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

FED LIQUIDITY BOTTLED UP ON BALANCE SHEETS

Note:

Source: Federal Reserve Board

United States

All Commercial Banks’ Cash Assets Nonfinancial Corps’ Cash and Cash Equivalents

49

($ billions)

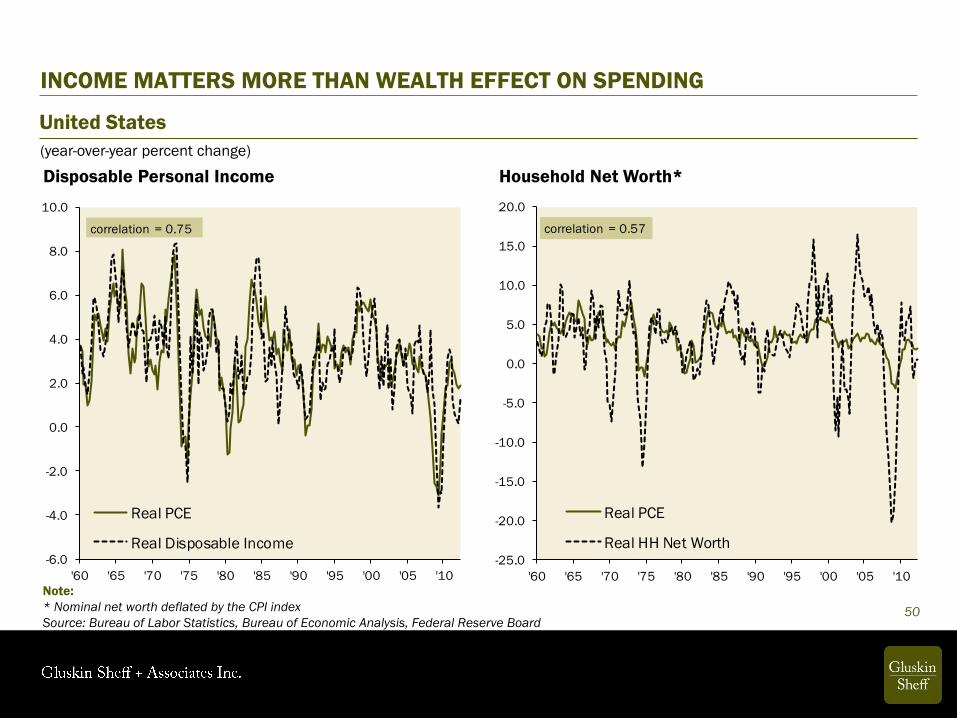

INCOME MATTERS MORE THAN WEALTH EFFECT ON SPENDING

Note:

* Nominal net worth deflated by the CPI index

Source: Bureau of Labor Statistics, Bureau of Economic Analysis, Federal Reserve Board

United States

Household Net Worth* Disposable Personal Income

50

(year-over-year percent change)

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

'60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10

Real PCE

Real HH Net Worth

correlation = 0.57

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

'60 '65 '70 '75 '80 '85 '90 '95 '00 '05 '10

Real PCE

Real Disposable Income

correlation = 0.75

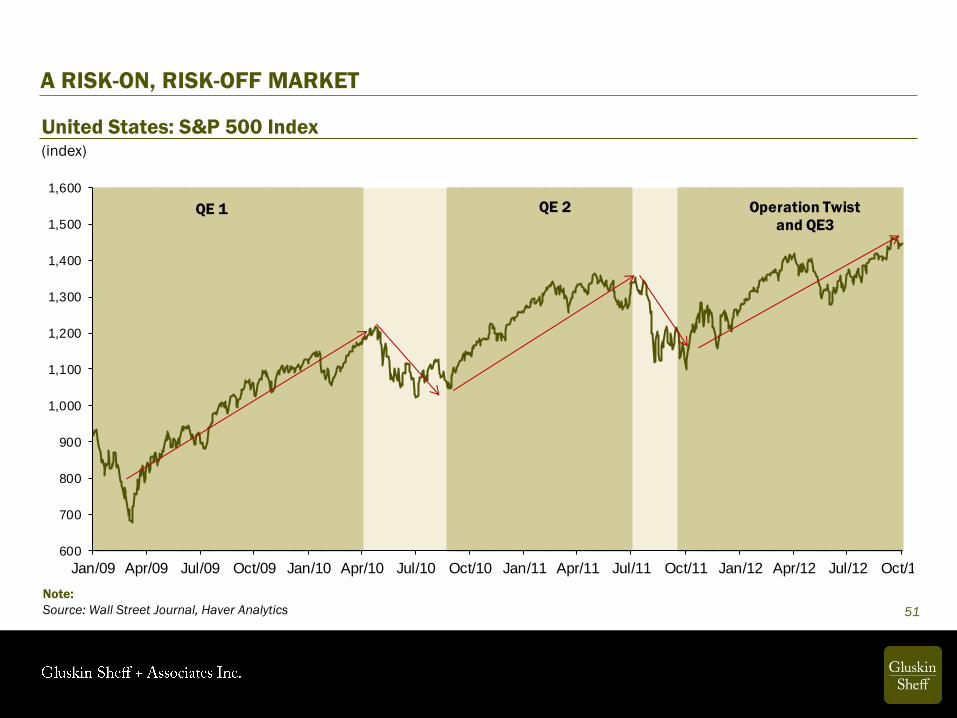

A RISK-ON, RISK-OFF MARKET

United States: S&P 500 Index

Note:

Source: Wall Street Journal, Haver Analytics 51

(index)

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

Jan/09 Apr/09 Jul/09 Oct/09 Jan/10 Apr/10 Jul/10 Oct/10 Jan/11 Apr/11 Jul/11 Oct/11 Jan/12 Apr/12 Jul/12 Oct/12

QE 1 QE 2 Operation Twist

and QE3

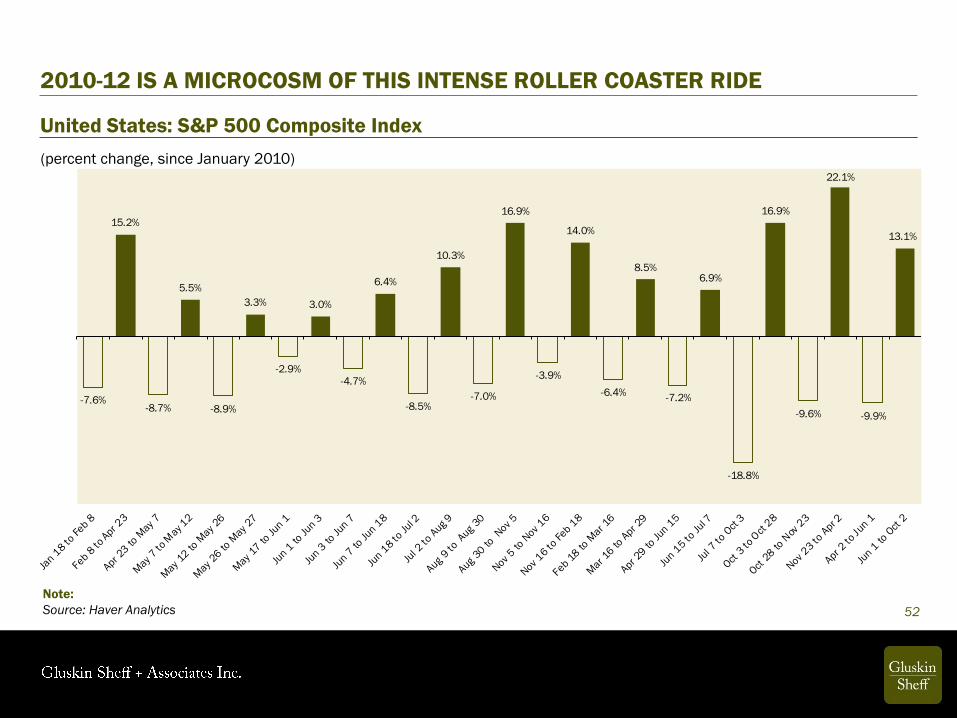

-7.6%

15.2%

-8.7%

5.5%

-8.9%

3.3%

-2.9%

3.0%

-4.7%

6.4%

-8.5%

10.3%

-7.0%

16.9%

-3.9%

14.0%

-6.4%

8.5%

-7.2%

6.9%

-18.8%

16.9%

-9.6%

22.1%

-9.9%

13.1%

(percent change, since January 2010)

2010-12 IS A MICROCOSM OF THIS INTENSE ROLLER COASTER RIDE

Note:

Source: Haver Analytics

United States: S&P 500 Composite Index

52

BEARISH FUNDAMENTALS BUT BULLISH MARKETS

Note:

Source: Barron’s (September 3, 2012) 53

-30

-20

-10

0

10

20

30

40

50

60

70

-25

-20

-15

-10

-5

0

5

10

15

20

S&P 500 Sales Per Share

REVENUE AND PROFIT GROWTH ALMOST VANISHED

Note:

* Corporate profits after tax with inventory valuation adjustment and capital consumption adjustment

Source: Standard & Poor’s, Bureau of Economic Analysis, Gluskin Sheff

United States

Corporate Profits*

54

(year-over-year percent change)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Oct/08 Apr/09 Oct/09 Apr/10 Oct/10 Apr/11 Oct/11 Apr/12

QE1

announced

QE2

announced

OT

announced

QE3

announced

(percent)

THE FED’S INFLATION REACTION FUNCTION HAS CHANGED

Note:

Source: Bloomberg, Gluskin Sheff

United States: 10-Year TIPS Breakeven Rate

55

FED POLICY GEARED TOWARDS DOLLAR WEAKNESS AND HIGHER GOLD PRICE

Note:

Source: Bloomberg

United States

The DXY Dollar Index

56

(index)

Gold Price

($/troy oz)

78.5

79.5

80.5

81.5

82.5

83.5

84.5

Apr/12 May/12 Jun/12 Jul/12 Aug/12 Sep/12

1,540

1,580

1,620

1,660

1,700

1,740

1,780

Apr/12 May/12 Jun/12 Jul/12 Aug/12 Sep/12

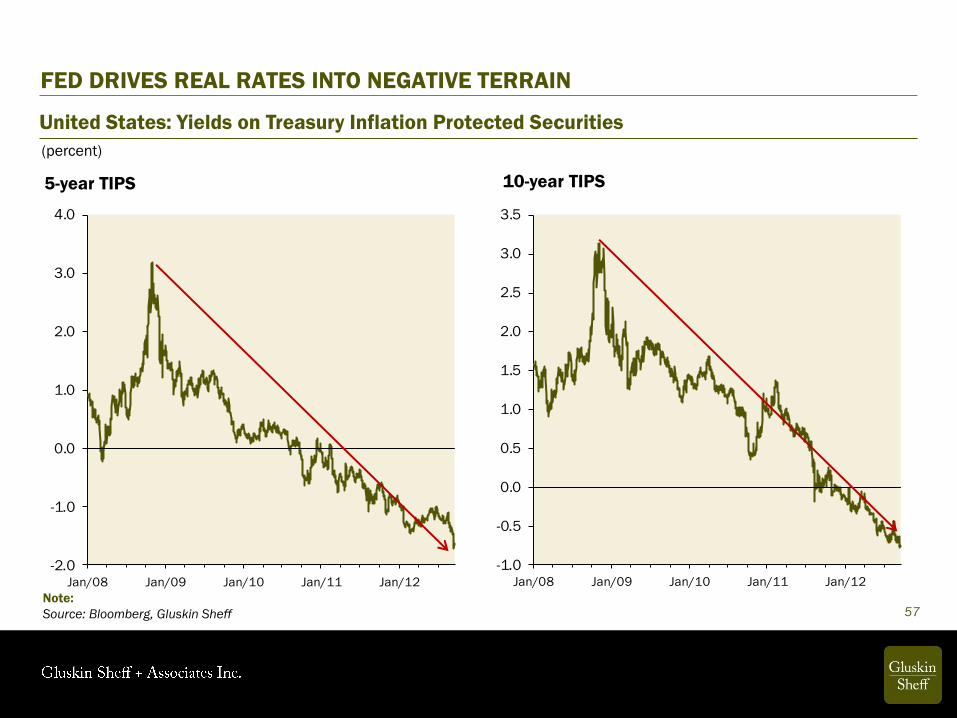

FED DRIVES REAL RATES INTO NEGATIVE TERRAIN

Note:

Source: Bloomberg, Gluskin Sheff

United States: Yields on Treasury Inflation Protected Securities

5-year TIPS

57

10-year TIPS

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Jan/08 Jan/09 Jan/10 Jan/11 Jan/12

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan/08 Jan/09 Jan/10 Jan/11 Jan/12

(percent)

ARGUABLY THE MOST COMPELLING ARGUMENT FOR EQUITIES

Note:

Source: Standard & Poor’s, Federal Reserve Board, Haver Analytics

United States: S&P 500 Dividend Yield and Five-year T-note Yield

Yield Levels

58

(percent)

Spread

(basis points)

0

1

2

3

4

5

6

Jan/02 Jan/04 Jan/06 Jan/08 Jan/10 Jan/12

Five-year T-note Yield

S&P 500 Dividend Yield

-1,200

-1,000

-800

-600

-400

-200

0

200

400

'53 '58 '63 '68 '73 '78 '83 '88 '93 '98 '03 '08

Widest since

1958!

S&P 500 Dividend Yield -

Five-year Treasury Yield

Spread

900.0

1000.0

1100.0

1200.0

1300.0

1400.0

1500.0

Jan/06 Jan/07 Jan/08 Jan/09 Jan/10 Jan/11 Jan/12

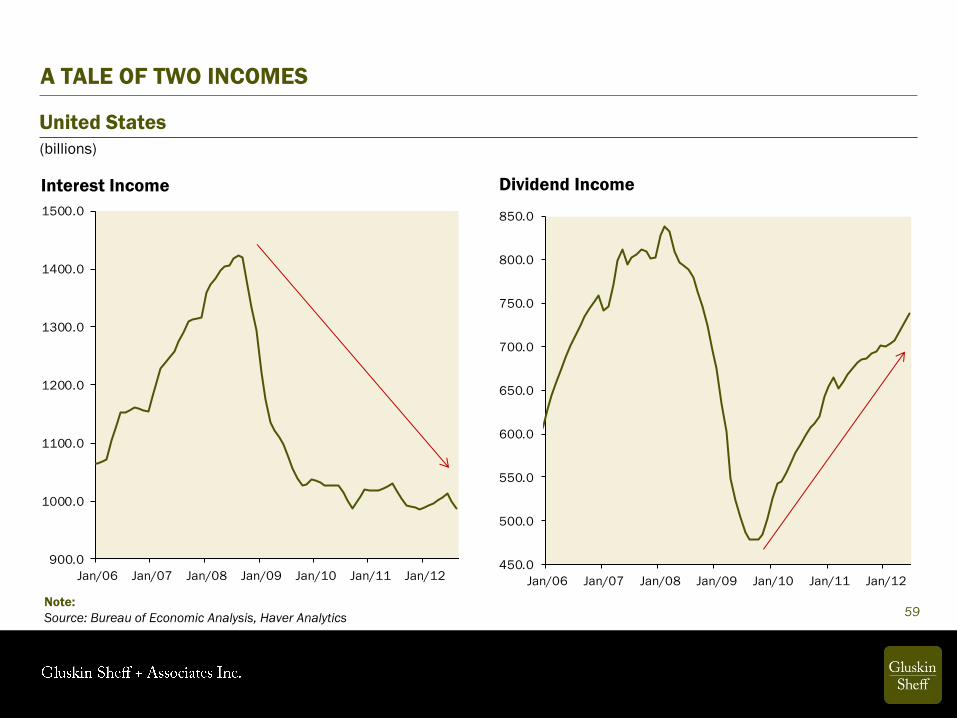

Interest Income

A TALE OF TWO INCOMES

Note:

Source: Bureau of Economic Analysis, Haver Analytics

United States

Dividend Income

59

(billions)

450.0

500.0

550.0

600.0

650.0

700.0

750.0

800.0

850.0

Jan/06 Jan/07 Jan/08 Jan/09 Jan/10 Jan/11 Jan/12

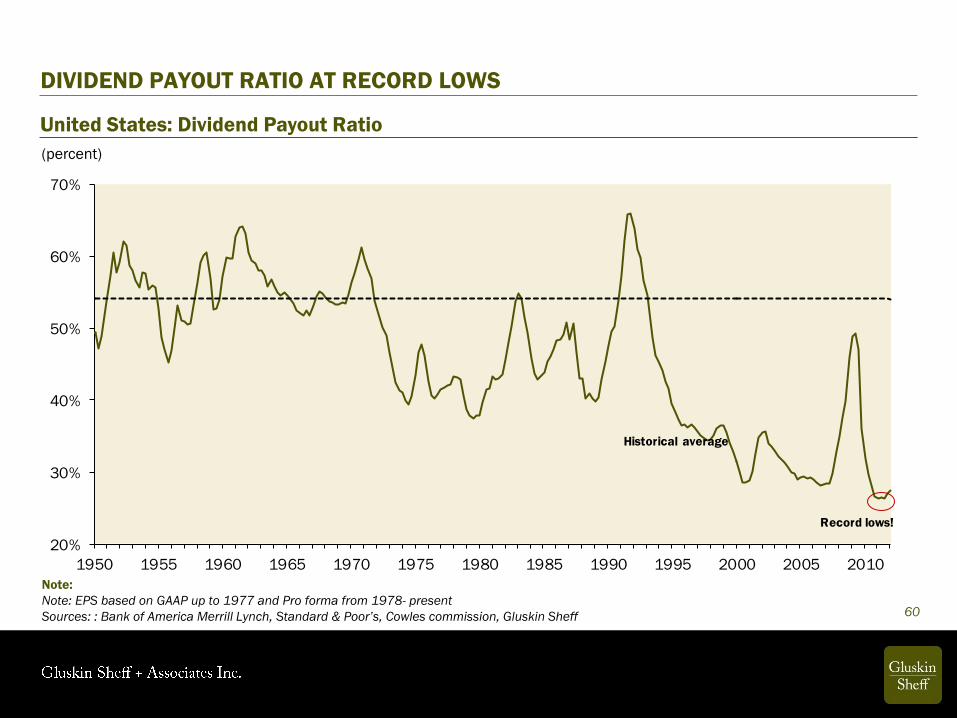

20%

30%

40%

50%

60%

70%

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Historical average

Record lows!

Note:

Note: EPS based on GAAP up to 1977 and Pro forma from 1978- present

Sources: : Bank of America Merrill Lynch, Standard & Poor’s, Cowles commission, Gluskin Sheff

United States: Dividend Payout Ratio

(percent)

DIVIDEND PAYOUT RATIO AT RECORD LOWS

60

0

100

200

300

400

500

600

700

800

900

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Pre-Bubble Average

3

4

5

6

7

8

9

10

11

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

CORPORATE BOND YIELDS LOW IN ABSOLUTE TERMS BUT HIGH IN RELATIVE

TERMS

Note:

Source: Bank of America Merrill Lynch

United States: BBB-rated Corporate Bond Yield and Spread off Treasury

Yield

61

(percent)

Spread

(basis points)

(percent)

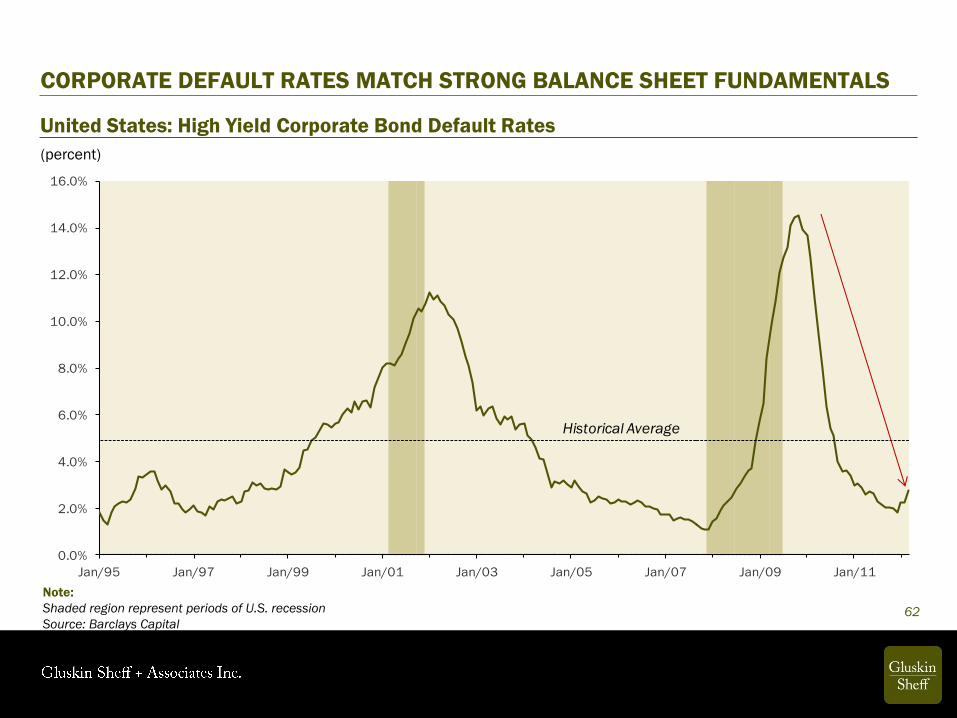

CORPORATE DEFAULT RATES MATCH STRONG BALANCE SHEET FUNDAMENTALS

Note:

Shaded region represent periods of U.S. recession

Source: Barclays Capital

United States: High Yield Corporate Bond Default Rates

62

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Jan/95 Jan/97 Jan/99 Jan/01 Jan/03 Jan/05 Jan/07 Jan/09 Jan/11

Historical Average

50

55

60

65

70

75

80

'70 '74 '78 '82 '86 '90 '94 '98 '02 '06 '10

15

20

25

30

35

40

45

50

55

60

'70 '74 '78 '82 '86 '90 '94 '98 '02 '06 '10

CORPORATE SECTOR FINANCES IN GOOD SHAPE

Note:

Source: Federal Reserve Board

United States: Nonfarm Nonfinancial Corporate Business (percent)

Liquid Assets to Short-term Debt Ratio Long-term Debt to Credit Market Debt Ratio

63

64

35 37

46 4853

46

32 3326 27

44

5547

42

29 27

21 2014

17

18 1824

30

26

21

2325

33 34 31 30 31 36

48 47 4639

2620

2527

2 3 2 2 2 2 3 3 4 4 4 4 5 6

0

10

20

30

40

50

60

70

80

90

100

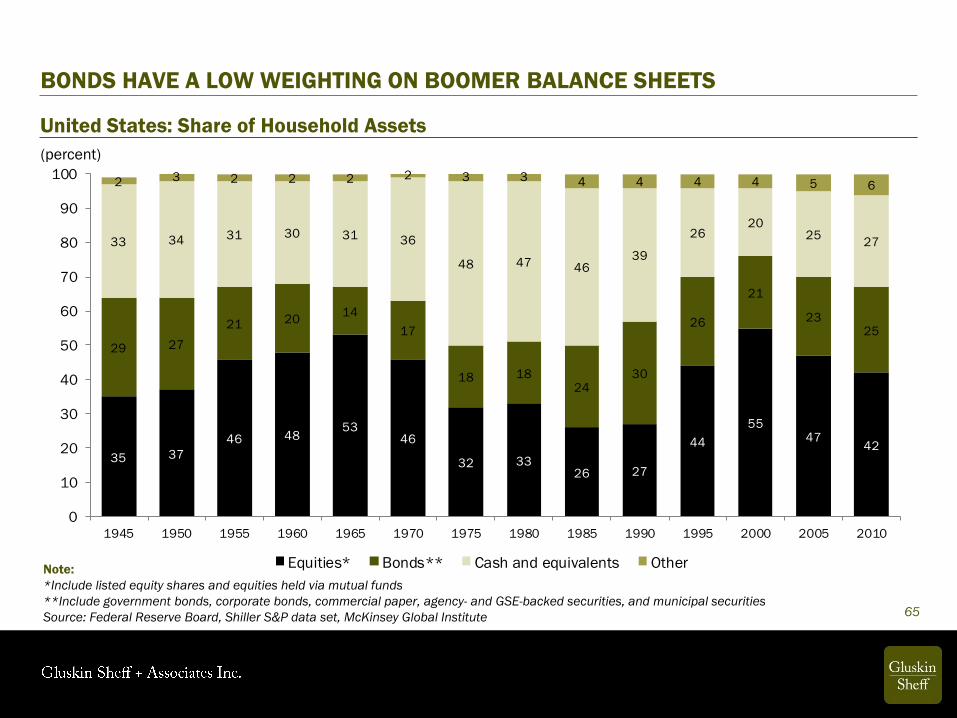

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Equities* Bonds** Cash and equivalents Other

(percent)

BONDS HAVE A LOW WEIGHTING ON BOOMER BALANCE SHEETS

Note:

*Include listed equity shares and equities held via mutual funds

**Include government bonds, corporate bonds, commercial paper, agency- and GSE-backed securities, and municipal securities

Source: Federal Reserve Board, Shiller S&P data set, McKinsey Global Institute

United States: Share of Household Assets

65

-200

-150

-100

-50

0

50

100

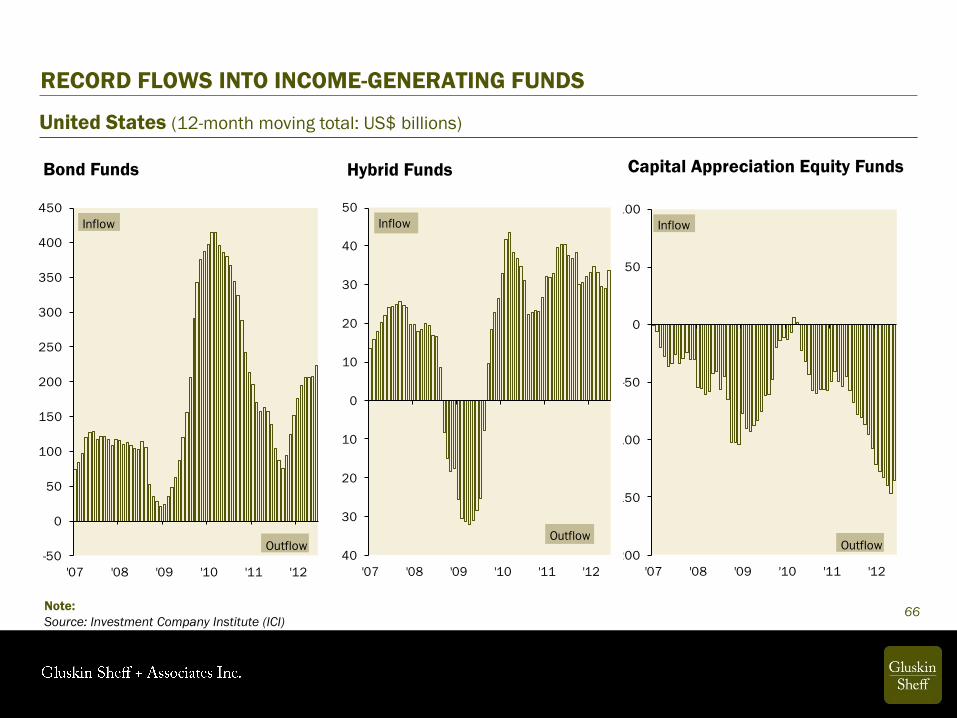

'07 '08 '09 '10 '11 '12

Inflow

Outflow

RECORD FLOWS INTO INCOME-GENERATING FUNDS

Note:

Source: Investment Company Institute (ICI)

United States (12-month moving total: US$ billions)

66

Capital Appreciation Equity Funds Hybrid Funds

-40

-30

-20

-10

0

10

20

30

40

50

'07 '08 '09 '10 '11 '12

Inflow

Outflow

-50

0

50

100

150

200

250

300

350

400

450

'07 '08 '09 '10 '11 '12

Inflow

Outflow

Bond Funds

67

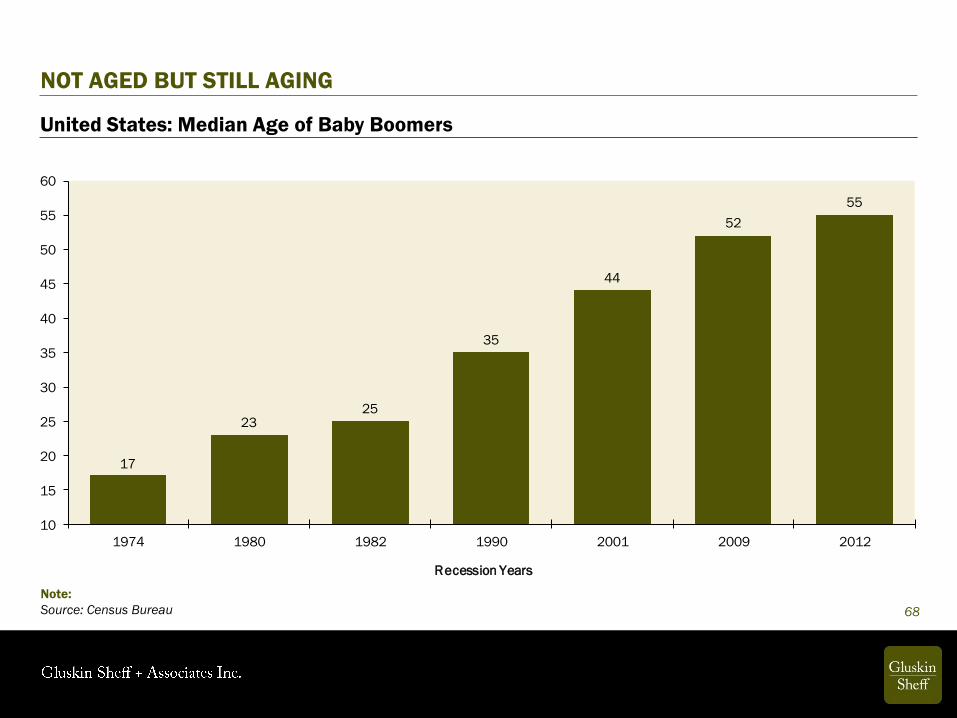

17

2325

35

44

52

55

10

15

20

25

30

35

40

45

50

55

60

1974 1980 1982 1990 2001 2009 2012

Recession Years

NOT AGED BUT STILL AGING

Note:

Source: Census Bureau

United States: Median Age of Baby Boomers

68

32%

33%

34%

35%

36%

37%

38%

39%

40%

'80 '90 '00 '10

Capital appreciation crowd

DEALING WITH DEMOGRAPHICS

Notes:

Dashed lines represent forecast

Source: Census Bureau

United States: Share of Total Population

Age 25-49 (percent)

Age 50-74 (percent)

69

20%

21%

22%

23%

24%

25%

26%

27%

28%

29%

30%

'80 '90 '00 '10

Capital preservation crowd

0%

5%

10%

15%

20%

25%

30%

35%

40%

REITs "Dogs" of the

dow

U.S.

preferreds

High yield

bonds

Dow utilities High dividend

paying TSXstocks

Invest. grade

corp bonds

Muni bonds 10-year strip 30-year strip Canadian

provincialbonds

10-year T-

note

Note:

Source: Bloomberg, Haver Analytics

Total Returns of Different Asset Classes

HAPPY RETURNS IN INCOME STRATEGIES

70

(year-over-year percent change, as of September)

INVESTMENT STRATEGY: SAFETY AND INCOME AT A REASONABLE PRICE (S.I.R.P)

1. Focus on safe yield: High-quality corporates (non- cyclical, high cash reserves, minimal

refinancing needs). Corporate balance sheets are in very good shape.

2. Equities: focus on reliable dividend growth/yield; preferred shares (“income” orientation).

3. Whether it be credit or equities, focus on companies with low debt/equity ratios and high

liquid asset ratios – balance sheet quality is even more important than usual. Avoid highly

leveraged companies.

4. Even hard assets that provide an income stream work well in a deflationary environment

(ie, oil and gas royalties, REITs, etc…).

5. Focus on sectors or companies with these micro characteristics: low fixed costs, high

variable cost, high barriers to entry/some sort of oligopolistic features, a relatively high

level of demand inelasticity (utilities, staples, health care — these sectors are also unloved and under

owned by institutional portfolio managers).

6. Alternative assets: allocate significant portion of asset mix to strategies that are not reliant on rising equity

markets and where volatility can be used to advantage.

7. Precious metals: A hedge against the reflationary policies aimed at defusing deflationary risks — money

printing, rolling currency depreciations, heightened trade frictions, and government procurement policies

71

DISCLAIMER

The information, opinions, and other materials contained in this presentation is the

property of Gluskin Sheff + Associates Inc. and may not be reproduced in any way, in

whole or in part, without express authorization of the copyright holder in writing. The

statements and statistics contained herein have been prepared by Gluskin Sheff +

Associates Inc. based on information from sources considered to be reliable. We make

no representation or warranty, express or implied, as to its accuracy or completeness.

This publication is for the information of investors and business persons and does not

constitute an offer to sell or a solicitation to buy securities.

72