Assetz Capital Page 1 PLEASE NOTE The information contained in this credit report has been provided by the applicant who has declared it complete and correct. Assetz Capital has not conducted an audit and provides no warranty as to the accuracy of the information. Assetz Capital gives no recommendation or advice in relation to this loan application and investors should seek their own advice before bidding. Techflow Flexibles (Holdings) Ltd TERM LOAN AMOUNT SECURITY VALUE LTV 5 Years £1,800,000 £2,400,000 75% INTEREST CAPITAL Paid Monthly Paid Monthly SECURITY Debenture over Techflow Flexibles (Holdings) Ltd. Debenture over Techflow Flexibles Ltd. Inter-company guarantee between Techflow Flexibles (Holdings) Ltd and Techflow Flexibles Ltd. 1st Legal Charge over the land and property at 4 Bassington Drive, Bassington Industrial Estate, Cramlington, Northumberland, NE23 8AS. Personal guarantee for £250,000 from Kenneth Beattie.

Transcript

A s s e t z C a p i t a l

Page 1

PLEASE NOTE

The information contained in this credit report has been provided by the applicant who has

declared it complete and correct. Assetz Capital has not conducted an audit and provides no

warranty as to the accuracy of the information. Assetz Capital gives no recommendation or advice

in relation to this loan application and investors should seek their own advice before bidding.

Techflow Flexibles (Holdings) Ltd

TERM LOAN AMOUNT SECURITY VALUE LTV

5 Years £1,800,000 £2,400,000 75%

INTEREST CAPITAL

Paid Monthly Paid Monthly

SECURITY

Debenture over Techflow Flexibles (Holdings) Ltd. Debenture over Techflow Flexibles Ltd.

Inter-company guarantee between Techflow Flexibles (Holdings) Ltd and Techflow Flexibles Ltd. 1st Legal Charge over the land and property at 4 Bassington Drive, Bassington Industrial Estate,

Cramlington, Northumberland, NE23 8AS. Personal guarantee for £250,000 from Kenneth Beattie.

A s s e t z C a p i t a l

Page 2

1 BORROWER

1.1 Background

This is a company operating in the oil and gas sector and has been trading very well (see

financial summary below). They specialise in the design, manufacture and supply of hoses to

the Oil and Gas Exploration and Production industries. The hoses are used in a variety of

different applications, such as – fire water mains, cement hoses, rig supply hoses etc.

The trading company has been in existence for over 11 years. The holding company over 5

years.

The directors are Ken Beattie & Bryan Beattie. Ken’s father (also Ken) & Ken’s Uncle (Bryan)

started business (“K & B Beattie”) in the sector around 40 years ago. Originally an

engineering business using CNC machines and lathes to produce machined metal products

for their customers. In the 1980’s considerable work was undertaken for customers in

Aberdeen in relation to specialist diving equipment. They moved into manufacture of high

pressure diving hoses. They sold out in 2000 for £10M. Subsequent to this, they established

a new business (“TechDrill”) in 2002. This business manufactured manifolds and couplings

primarily for the oil & gas sector. This business was sold for £24M in 2011.

Alongside Techdrill they established Techflow Flexibles in 2006. The business has been built

up to a turnover regularly in excess of £20Mpa now. They had a division in China that was

being used to produce goods. However, they recognised that the Chinese product was

sometimes viewed as of inferior product quality. They also noted that the products they

provide are predominantly for new oil platforms etc. and they wished to diversify to be able

to provide a “repairs & maintenance” offering, rather than simply supporting new

exploration. To this end, they have recently sold off their stake in the Chinese operation

having spent the last few years undertaking significant research and development to enable

them to serve the repairs & maintenance side of the sector. Over the last few years they

have spent over £8M on new equipment in the UK and research & development.

They now carry various valuable certifications, including the following:

• API 7K Rotary Drilling & Mud hoses Type Approved to DNV-OS-E101 & ABS CDS

• API 7K Cement Hoses Type Approved to DNV-OS-E101 & ABS CDS

• API 7K Hydraulic Tensioner Hoses Approved to DNV-OS-E101 & ABS CDS

• API 16C Flexibles Choke & Kill Lines

• API 17K Bonded Flexible Pipe

(“API” = American Petroleum Institute)

… which are now enabling them to secure new contracts on maintenance projects. This is very

good news for Techflow as the maintenance side of the sector is considerably larger and

A s s e t z C a p i t a l

Page 3

presents much more opportunity (as well as being something that cannot be “turned off” if

demand dictates – such as new exploration projects).

As an example, Saudi Aramco (the national petroleum and natural gas company of Saudi

Arabia) has over 17km of pipes that need to be replaced on a rolling programme over the next

10 years. These pipes are currently made of steel. However, the steel corrodes over time and

creates leaks in the system. These are currently being patched on a reactionary basis. Techflow

have developed a steel reinforced thermoplastic pipe (“RTP”) (effectively of rubber

construction with spiral wrapped steel reinforcement) which is easy to substitute the existing

steel and has a much longer expected lifespan (approximately 10 years v the current 1 to 2

years – before they potentially start leaking). In addition, they are much more flexible, smaller

and lighter – easier to handle.

The certifications above are coveted and these, coupled with the existing and new contracts

coming on line, have made Techflow an attractive acquisition target. The directors have

advised they have had an approach to sell the business. The offer at this stage is c$66M USD.

They are continuing discussions with the potential purchasers. However, this is considered

some time off and indeed is by no means certain at this time.

1.2 Structure

Techflow Flexibles (Holdings) Ltd is the top company with shares owned 50/50 by Bryan &

• External Secured lay down / storage area = 50,000 sq ft

• Overhead crane facilities with multiple 10 Tonne capacity.

Offshore services include:

• Project Management

A s s e t z C a p i t a l

Page 5

• Hose Design & Configuration

• Hose Manufacture

• Research & Development

• FHA Management Services

• Inspection & Repair Service

1.5 Market

The marketplace is enormous and breaks down into many different segments /

requirements. Techflow provide a wide variety of products, some of which are listed below:

• High Pressure Drilling Hoses

• Drag Chain Hoses

• Fire Resistant Hydraulic BOP Hoses

• Firewater Mains Hoses

• Industrial & Rig Supply Hoses

• Specialist Heat-Trace Hoses

• Fire Resistant Hydraulic Quick Release Couplings

• Hose Loading Stations

• Breakaway Couplings

To give some perspective to this, the renewal of 17km of steel pipework for Saudi Aramco

alone will cost in the region of £1.7Bn. Each new oil platform will spend over £1M in hoses,

pipes and ancillary products – all of which need regular replacement too.

1.6 Suppliers

Steel wire is generally sourced from Bekaert. They have other options but have a good

working relationship with Bekaert and therefore choose not to spread around supply

requirements.

Rubber products are supplied by 2 or 3 sources both domestically and internationally.

1.7 Customers

Techflow has a wide variety of clients including: BP, Total, Maersk, Seadrill, Bentec, Samsung

Heavy Industries, Statoil, Daewoo Shipbuilding, Petrobas and Keppel Fels. The client base is

wide and varied – predominantly blue chip quality.

1.8 Competition and Strategy

Techflow’s most proficient competitor is considered to be Contitech. Contitech is an

international company offering a very wide variety of products and services, although their

key offerings are in drive belts and hoses. Techflow consider them good, but they are quite

A s s e t z C a p i t a l

Page 6

inflexible in their approach and they are not offering RTP. They are also comparatively

expensive.

Pipelife does offer the RTP system. They are also an international company and focus

predominantly of pipe products. Two of the key technical staff at Pipelife are now with

Techflow.

Copper State Rubber, based in Arizona, US, are considered to produce an inferior product to

Techflow’s RTP product. They are also unable to provide the analysis and data Techflow can

offer as part of their services.

2 PROPOSAL

2.1 The proposal is to re-finance the premises from which they trade to repay existing debt with

HSBC (£595,000) and the rest will be used in part to acquire some specialist equipment in

relation to their trade, along with reimbursing themselves for some of the considerable R&D

spend they have undertaken in the last couple of years. In the financial reporting period to

31/12/15, they spent c£3.47M on research and development. This exercise will inject cash

to be used as part of the growth funding of the business as turnover grows again.

2.2 The request is for a 5-year commitment on a 1+19 amortising profile. The interest only

period at the outset will offset some of the transaction costs. The following low repayment

rate will allow them to preserve cash generated for ongoing R&D spending and to fund the

re-growth in turnover of the business which they have allowed to reduce while they have

focussed on securing their additional accreditations.

2.3 It is fair to say the directors have spent large sums of cash on R&D and also clearing

substantial funding lines over the last couple of years. This has left them short of cash and

the net loan proceeds will assist with reinstating a suitable level of working capital from

which to grow the business again.

3 CONDITIONS AND COVENANTS

3.1 Conditions Precedent

a) Satisfactory AML/KYC checks in respect of the Borrowers / Directors / Shareholders.

(COMPLETE).

b) Clear credit searches against the Borrowers / Directors / Shareholders.

(COMPLETE).

c) Satisfactory completion of all stated security requirements.

(IN PROGRESS WITH SOLICITORS).

A s s e t z C a p i t a l

Page 7

d) A formal, independent valuation addressed to Assetz Capital Trust Company Limited

and its Lenders from time to time by a RICS qualified valuer confirming market values

of the property. Expected minimum market value of £2,400,000 (based on vacant

possession value and an assumed 180-day restricted sale period).

(COMPLETE).

e) Loan to value not to exceed 75% value (as measured against the Vacant Possession

Value – 180-day restricted sale period).

(COMPLETE).

f) Satisfactory insurance cover with Assetz Capital noted as first loss payee.

(IN PROGRESS WITH SOLICITORS).

g) 6 months’ copies of the business and personal bank statements revealing satisfactory

conduct.

(COMPLETE).

h) Assetz Capital due diligence to be satisfied that loan can be serviced.

(COMPLETE).

3.2 Covenants

a) Annual accounts to be provided to Assetz Capital within 180 days of the period end to which they relate.

b) Monthly management accounts comprising of profit & loss, balance sheet and cash flow statements to be provided to Assetz Capital within 30 days of the period end to which they relate.

c) Debt Servicing – EBITDA to All Debt Service Liability for each Quarter must be at least 1.25:1. To be tested Quarterly on a Rolling 12-month basis.

d) Interest Cover – EBITDA to All Interest Cost for each quarter must be at least 1.50:1. To be tested quarterly on a rolling 12-month basis.

e) Maximum Loan to value (as measured against the Vacant Possession Value – 180-day sale period) not to exceed 75% on each valuation date.

f) Dividends in any annual period not to exceed £0 without the prior written consent of Assetz Capital SME Ltd.

g) Expenditure on research & development in any annual period not to exceed £100,000 without the prior written consent of Assetz Capital SME Ltd.

h) Repayments of the loan from Marine as proposed per the 5 year projections

(produced Jan 17 – Revision 0) not to be accelerated. Repayments to be regulated by

* Please note the 2015 period was actually a 16-month period generating turnover of

£34,068.974 and EBITDA of £4,509,072. The figures used above are the annualised figures to

afford a like-for-like comparison.

The 2014 & 2015 periods (now to 31st December) demonstrate the level of business Techflow

can readily attract. The 2016 figures reflect the period in which management took a deliberate

decision to withdraw from higher volume / lower margin work and focus on a lower volume

of more profitable contracts. This has also enabled them the capacity to focus on their

research and development activities and successfully attract the new accreditations (which

will give rise to securing more lucrative work going forward).

Despite the halving of turnover, the underlying profit percentage is up, primarily as a result of

the higher gross margin on work taken on. The intention is to continue in this manner, and

also lift turnover in future periods whilst maintaining margin levels. The customers have

projected forward for 5 years and the following data completes the projected picture (albeit

could not be included in the tabulation above due to space constraints):

• 2019 – Turnover £33,652,000; EBITDA £5,671,000

• 2020 – Turnover £36,957,000; EBITDA £6,816,000

• 2021 – Turnover £40,243,000; EBITDA £7,747,000

The customers have advised that there is adequate capacity within the existing buildings to

accommodate the above levels of business.

Since producing the 5 year projections, the customer has revised (upwards) their expected

turnover for 2017 to £24,925,454 (up c£2m). This is based on confirmed monthly orders for

£15,475,454 and pending orders of £9,460,000 already accumulated for 2017. These numbers

confirm turnover is already set to climb from the 2016 period.

It can be seen above that the company can service the debt proposed and would exceed the

proposed 1.25x covenant (even based on the historic 2016 period). The debt servicing

obligation equates to £1,262,000pa and incorporates this proposed loan along with all other

facilities (primarily 1 large asset finance agreement and a few small ones soon to run off).

A s s e t z C a p i t a l

Page 9

Please note, there is little corporation tax payable (indeed the 2017 & 2018 periods are

expected to feature net refunds from HMR&C). This is as a result of the research &

development undertaken and the successful reclaiming of relief in that respect.

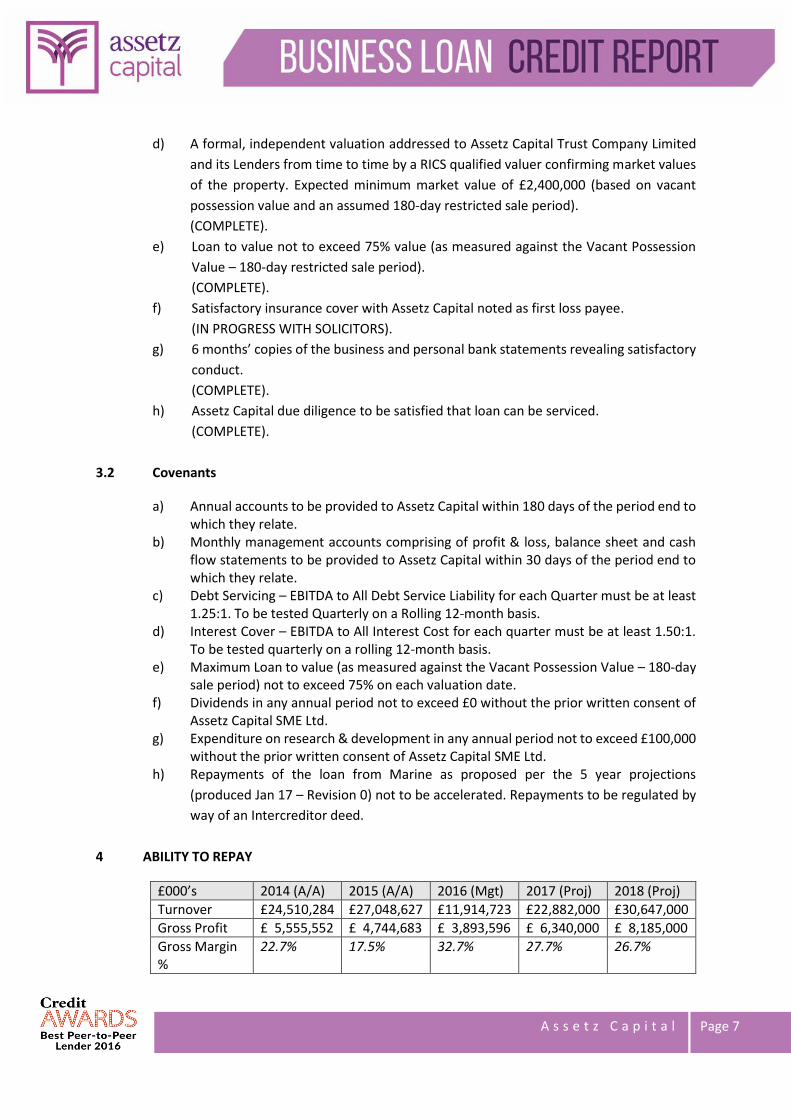

5 FINANCE ASSESMENT INCLUDING SERVICEABILITY FROM PAST AND FUTURE PERFORMANCE

Debt servicing based on profitability has been demonstrated above. In addition to this, an analysis

based on cash generation has been undertaken below.

In 2016, there was a little over £4.5M of cash generated from operating activities. This would be

a little unusual based on the reduced turnover. However, reflective of a collect-in of debtor

balances in the main. The funds were used to clear approximately £3.3M of external funding as

well as c£1.3M of inter-company loans.

Turning to the 2017 figures, there is an expected net cashflow (before financing capital and

interest repayments) of £1,980,000. This figure includes the proceeds of sale of the Chinese

operation and the proceeds of this funding request. If we strip this back, there would be negative

cash generation of £1,169,000. On the face of it, this might be concerning. However, it is entirely

understandable as turnover increases and debtors balances will naturally increase and consume

cash pending receipt of payment from customers under trade terms. There is an expectation that

debtors balances will climb by some c£5M+ in the period. This consumption of cash is offset in

part by an increase in supplier terms, reduction in stocks, retained cash profits and the

aforementioned funds coming in.

2018 is expected to see net cash flow of c£4M before financing and a surplus of c£2.765M after

financing. The net cash flow before financing compares with the forecast EBITDA of c£4.662M and

indicates a slow down in cash consumption by balance sheet assets such as debtors and stock.

Net worth is stated as £12,471,586 per the 2015 audited accounts. However, this includes an

“intangibles” figure of £7,584,775 and as such one might prudently consider the net worth to be

a little under £5M if one excludes the “intangibles” value. That said, the intangibles reflect the

value in the patents and patents pending in relation to a number of the products they produce

and manufacturing processes employed. These would likely be of some reasonable value to a

competitor who wished to obtain them and use them.

Bank Statements

Bank statements have been provided for the business as well as the personal bank statements for

the guarantor.

A s s e t z C a p i t a l

Page 10

The business bank statements for the holding entity and the trading do not feature any unpaid

items. They are generally well-conducted. There is the occasional modest overnight overdrawn

position. However, this is always cleared the next morning.

There was a large influx of cash in December as a result of the re-finance of machinery to release

additional cash. The repayments on this facility have been included in the debt servicing above.

There were £30,000 regular payments to HMR&C which looked unusual and warranted further

investigation. It transpires that the customers had a large research & development allowance

claim in and the customers were reluctant to pay out the calculated corporation tax on their

profits, knowing that they were entitled not to pay it. As a compromise, HMR&C agreed to accept

the nominal £30,000 payments until they had reviewed the claim and settled it. This has since

been settled and the amounts are no longer payable.

The personal bank statements for the guarantor do feature 2 modest unpaid items. I have inquired

as to why this occurred as there is a good level of income going through the personal account. It

seems the guarantor has been undertaking some sizeable home improvements and this has

caused a lot more personal expenditure than usual to go through the account – and the unpaid

items were as a result of an oversight in relation to the extra expenditure through the account.

6 SECURITY

6.1 The following security shall be provided:

a) Debenture over Techflow Flexibles (Holdings) Ltd.

b) Debenture over Techflow Flexibles Ltd.

c) Inter-company guarantee between Techflow Flexibles (Holdings) Ltd and Techflow Flexibles

Ltd.

d) 1st Legal Charge over the land and property at 4 Bassington Drive, Bassington Industrial

Estate, Cramlington, Northumberland, NE23 8AS.

e) Personal guarantee for £250,000 from Kenneth Beattie.

A valuation report has been commissioned / received and the following key figures have been provided:

• £2,750,000 = Market Value assuming Vacant Possession

• £2,400,000 = Market Value assuming Vacant Possession (and a 180-day restricted sale period)

• £370,000 = Market Rent (equates to £2 per sq ft) Key commentary is as follows:

• The property is located on the Bassington Industrial Estate in Cramlington in the north east of England, approximately 10 miles north of Newcastle. It is very close to the A19

A s s e t z C a p i t a l

Page 11

& A1(M) and as such has good transport links. In addition, it is c6 miles from Newcastle International Airport.

• The site is c13 acres in size and the property comprises a large industrial complex arranged in two buildings which have been refurbished. The industrial accommodation is of steel frame construction with brick elevations which have been overclad with profile metal sheeting beneath a pitched roof with an asbestos sheet covering. To the west of the site is a car park and area of grassed expansion land. Site coverage is c32% at present.

• The estimated useful economic life of the building is stated as 25 years.

• The location is not considered to be in a floodplain and the risk of flooding is considered negligible.

• An Energy Performance Certificate was prepared on 28th June 2012 and rated the building as a “D” rating. As such it would not currently fall foul of the upcoming Minimum Energy Efficiency Standards (effective 1st April 2018) whereby a property with a rating of “F” or worse must have energy efficiency improvements made before it can be leased.

• The valuer comments that “despite the wider economic and political uncertainty, industrial occupier take-up has continued to remain strong”. He goes on to say that “generally the stock of industrial premises on the market in the North-East region is relatively low and in particular for freehold opportunities for which there is a considerable appetite. Currently demand remains for modern units, which are now available in very limited numbers and consequently there is now a significant disparity between rental and capital values for modern and older second hand space. Cramlington continues to be a popular industrial location given the town’s excellent communication links being situated close to the junction of the A1 and A19. Up until the past 10 years there had been limited new development in Cramlington however those new developments which have taken place have proved extremely popular.”

• The valuer states “The main production facility has an eaves height of approximately 4.43m which is relatively low and would limit occupier demand to manufacturing occupiers. The facility is large at c.185,000 sq ft and while demand for units of this size is relatively “thin” we are aware of a number of existing requirements for this type of asset in and around Cramlington. In the event the property was offered to the market at present we believe there would be reasonable levels of demand.”

Our funding will represent 75% of the vacant possession value (assuming the restricted 180-day sale period). Further comfort is derived from the personal guarantee from Ken Beattie.

7 RISK AND MITIGANTS

7.1 Sector Risk

The business is very much dependent on the oil and gas sector and as such, fluctuations in the

performance of the wider sector can have a great impact on a business like this, especially if

their activities are tied to the exploratory side of the sector and the installation of new

facilities for the extraction of oil. It is for this reason that the business has invested heavily in

research & development and diversified its offering such that it is now serving the existing

markets on more of a “repairs & maintenance” front than the new / exploratory operations.

A s s e t z C a p i t a l

Page 12

This puts the company in a much stronger position as it has the capabilities to serve new &

existing facilities and significantly reduces exposure to any cyclical patterns in the oil & gas

sector.

7.2 Currency Risk

Given the company trades with partners in a number of locations around the world, there are

often occasions when large payments are made in currency. The business chooses to hedge

against currency movements from time to time to mitigate against exchange rate loss.

7.3 Property Risk

The valuer has indicated that the roof is made of asbestos and considers that renewal will be

required over the medium term. The customers have confirmed that they have implemented

and continue a regular maintenance programme on the whole building. They envisage the

lifetime of the roof to be substantial. Upon a visit to the site and inspection of the properties,

it is confirmed there were no signs of any leaks to the roof (it was a wet day).

As part of the legal process, we shall seek a copy of the asbestos register to ensure that the

asbestos has been examined, considered safe and / or being managed appropriately.

The eaves height of the main production facility is low at 4.43m and this will restrict the

market for the unit. That said, the valuer has indicated there is current demand from occupiers

that the building would satisfy.

The valuer has stated that whilst the site coverage is low at c32% there is a limited level of

external yard space. This was raised with the borrowers and they advised that they could

readily re-configure the parking allocation on the property so as to free up more storage /

yard space as required.

7.4 Exit Risk

Considering capacity for full repayment, there are a number of potential exit routes:

• Trade Sale

There is already interest in the business as alluded to above. The principals have

successfully achieved trade sales in the past.

• Re-finance to another lender at the end of the loan term

The debt at maturity of the 5-year term should equate to 68% of the vacant

possession value (assuming a 180 day sale period) or c59% of the market value.

This should be a level supported by a number of lenders. Alternatively, an invoice

A s s e t z C a p i t a l

Page 13

finance provider should be able to release sufficient cash against the debtor book

to fully repay the facility.

• Re-finance with Assetz Capital

Assuming satisfactory conduct during the 5 year term, it is quite reasonable to

consider that Assetz Capital would consider a proposal for a further 5 year term.

• Recourse to security

As a last resort, recourse to security is expected to achieve full repayment. There

would be the property, the personal guarantee and a reasonable expectation of

some collect-out of the debtor book as caught under the Debenture.

![Assetz Marq Bangalore[[9019196393]]New Launch Whitefield](https://static.documents.pub/doc/80x56/56816698550346895dda82f7/assetz-marq-bangalore9019196393new-launch-whitefield.jpg)