Technical Innovation for Expanding Technical Innovation for Expanding Outreach: Outreach: Mobile Phone Banking in the Mobile Phone Banking in the Philippines Philippines MELIZA H. AGABIN MELIZA H. AGABIN Deputy Chief of Party, MABS Program Deputy Chief of Party, MABS Program Presented at the 3 Presented at the 3 rd rd African Microfinance Conference African Microfinance Conference Kampala, Uganda Kampala, Uganda August 20-24, 2007 August 20-24, 2007

Transcript

Technical Innovation for Expanding Technical Innovation for Expanding Outreach: Outreach:

Mobile Phone Banking in the Mobile Phone Banking in the PhilippinesPhilippines

MELIZA H. AGABINMELIZA H. AGABIN

Deputy Chief of Party, MABS ProgramDeputy Chief of Party, MABS ProgramPresented at the 3Presented at the 3rdrd African Microfinance Conference African Microfinance Conference

Kampala, UgandaKampala, Uganda

August 20-24, 2007August 20-24, 2007

Philippines Location:

Microenterprise Access to Banking Services (MABS)

Program

The program assists banks

to develop the capability

to profitably provide

financial services to

microenterprises through

technical assistance and

training.

Rural Banks in the Philippines

• Wide network coverage: 760 rural

banks; over 2,000 branches

• Over 50 year history

• US$2 billion in assets

• Over 5 million deposit accounts

• Over 1 million borrowers

MABS Partner Rural BanksAs of June 2007

• MABS works with 90 rural banks through

337 branches

• Over 165,000 active microenterprise

borrowers

• Over 390,000 new micro borrowers

served since 1998

• Over 410,000 new micro deposit accounts

Challenges

• Reaching deeper into rural areas

without costly investments in

infrastructure

• Reducing costs of servicing

• Avoiding security risks from robbery,

holdup

• Reducing costs to clients

Challenges for Rural Banks to reach Rural Clients

High Transaction Costs−Transportation Cost−Loss of business opportunity−Security risk

Technology Technology Solution: Mobile Solution: Mobile Phone BankingPhone Banking

Technology Solution:Mobile Phone Banking

To extend low-cost banking services to existing clients and un-banked individuals especially in rural areas.

WHY CHOOSE THIS TECHNOLOGY?

Why Choose this Technology?

External Drivers:

Rapid expansion of mobile phone outreach

Nationwide coverage

Enhanced Mobile Phone Services

Falling cost of technology

Increased competition Ability to offer banking services at very

Motivation Reduce cost and increase efficiency of loan

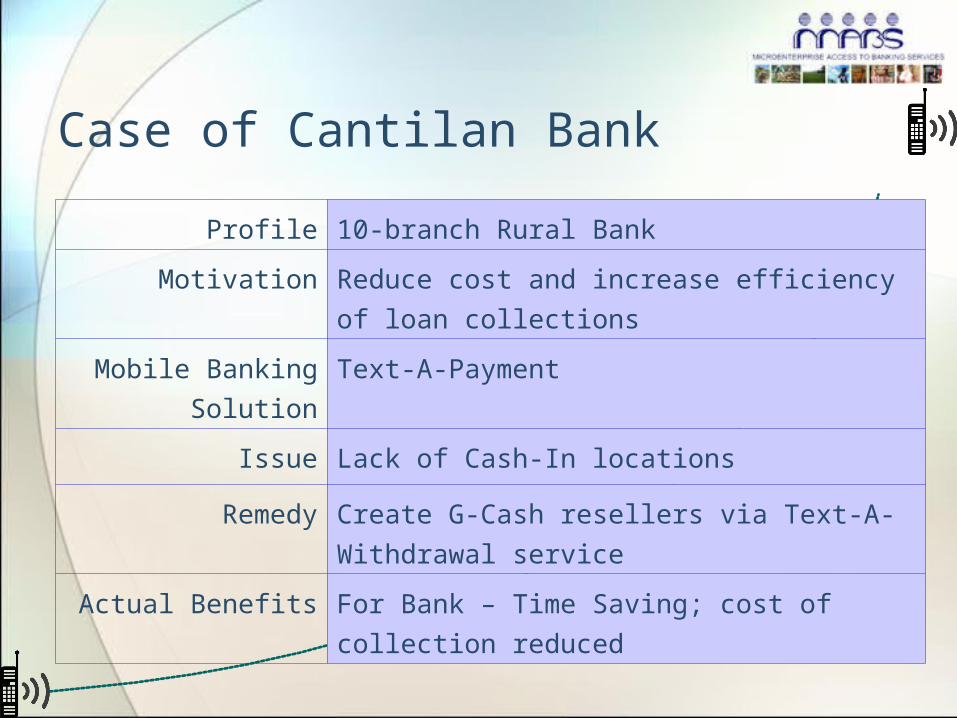

collections

Mobile Banking

Solution

Text-A-Payment

Issue Lack of Cash-In locations

Remedy Create G-Cash resellers via Text-A-

Withdrawal service

Actual Benefits For Bank – Time Saving; cost of collection

reduced

Case of Bangko Kabayan

Issue Lack of Cash-In locations

Remedy Create G-Cash resellers

via Text-A-Withdrawal

service

Actual

Benefits

Expand outreach;

Reduced transaction

costs; convenient for

clients

Profile 9-branch Rural Bank

Motivation Expand outreach to rural areas

Mobile Banking

Solution

Text-A-Payment

Case of 1st Valley Bank

Profile 16-branch Rural Bank

Motivatio

n

Increase deposit base and offer bill

collection services

Mobile

Banking

Solution

-Partnered with an electric

cooperative

-Offering customers Text-A-BillPay

service

-M-Payment services for local

merchants

Actual

Benefits

Able to remotely accept bills

payment; Increase Deposit Balance;

Merchants become new bank

depositors

What Users Say…

What Users Say…

Main Challenges

Lack of Re-sellers (Cash-in outlets)Introduced TEXT-A-SWELDO (salary) service

• Banks pay employee salaries and bonuses

with G-Cash.−Created a critical mass of people carrying G-Cash in

their mobile phones, using the technology, and familiar with different services and benefits

−Employees help with promotions.

Main Challenges

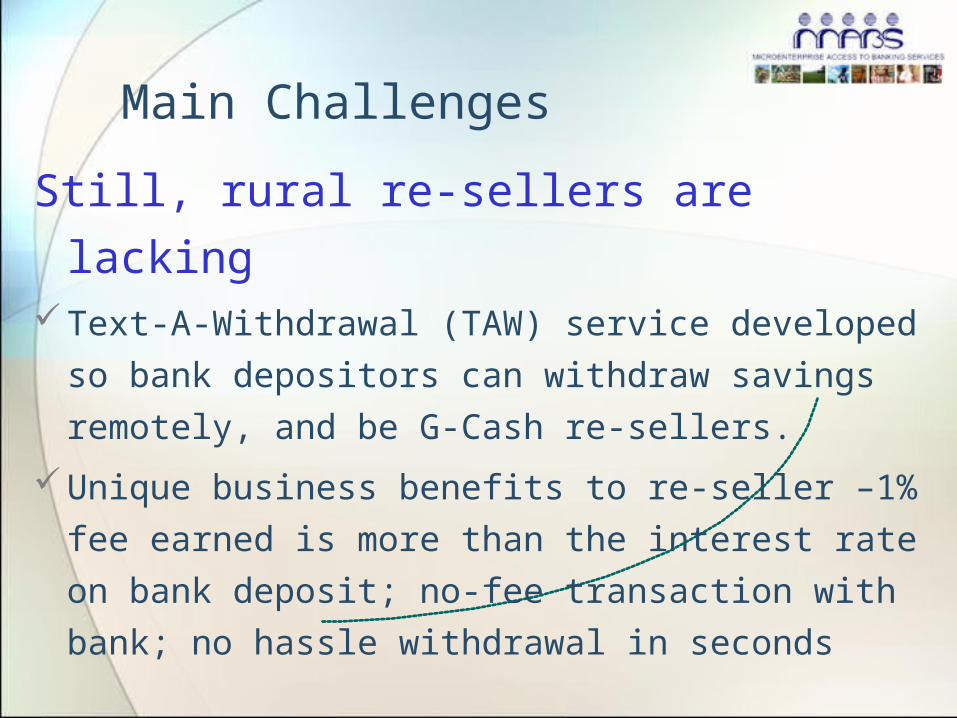

Still, rural re-sellers are lackingText-A-Withdrawal (TAW) service developed so

bank depositors can withdraw savings

remotely, and be G-Cash re-sellers.

Unique business benefits to re-seller –1% fee

earned is more than the interest rate on bank

deposit; no-fee transaction with bank; no

hassle withdrawal in seconds

Main Challenges

Marketing to convince more people to embrace

the technology and use the services.

• Eco-system rollout: MABS work with rural banks to

train and accredit merchants and shops to accept G-

Cash in payment for goods and services.

• Telecom co-branding with partner rural banks for

marketing materials

• Telecom support for merchandizing materials, like

tarpaulins and standees promoting G-Cash services.

Main Challenges

Training and reaching more users, overcoming

initial fear of USE technology and SECURITY of

their money.

• Whether it is the bank, the merchant, the end

user, presenting the unique benefits helped.

• Globe offered 10% discount on pre-paid

airtime load using G-cash; opportunity to

earn; frequency of use establishes G-Cash

security, ease and convenience.

Updates and Updates and Future DirectionFuture Direction

Volume of Transactions Through Accredited Rural Banks (as of June 2007):Accredited Rural Banks 37

Accredited Bank-Branches 287

# of Employees (Receiving salaries & benefits

through Text-A-Sweldo (TAS)

2,484

# G-Cash Transactions (cumulative) 110,000

Amount G-Cash Transactions – in Pesos

- in USD

PhP380

M

USD 7.6

M

Ecosystem Roll-out (# of merchants-

accredited by rural banks)

145

New Developments and Future Directions of Mobile Phone Banking and Mobile Commerce• Text-A-BillPay (through rural banks) has been

piloted and ready for rollout

• Activating more G-Cash Resellers to serve Text-A-Payment clients

• Continuous development of G-Cash Ecosystem in the rural areas to increase the use of e-money especially in commercial applications

• Continuous Pilot testing of the other mobile banking services to model cost effective ways of reaching more and more people in areas farther away from the bank.

New Developments and Future Directions of Mobile Phone Banking and Mobile Commerce• Developed a Mobile Banking Website

(www.mobilephonebanking.rbap.org) as information portal particularly for rural banks, its clients, money senders, and the cyberworld in general

• Continuous Support and Training-Workshop on Mobile Phone Banking

• Text-A-Credit (line) manuals and procedures –development on-going

• Development of mobile phone banking system to automate G-Cash transactions

This is the road we’ve traveled so rural banks can reach more people farther away, faster, cheaper, and more efficiently.

Text-A-Remittance (Cash-in/ Cash-

out)

Text-A-Withdrawal (debit system)

Text-A-Payment

(loan collection)

Text-A-Deposit

Text-A-Sweldo

Text-A-Credit(Line)

Text-A-Bills Payment

We are Here!

TEXT A MONEY REMITTANCE

TEXT A SWELDO

TEXT A PAYMENT

TEXT A DEPOSIT

TEXT A WITHDRAWAL

And this is the roadmap a bank in a remote area in Mindanao Region is following.

The goal is to turn the rural folks’ mobilephones into a virtual ATM.