Page 1

CMP (Rs) 115.00

Target Price (Rs) 129.00

ISIN: INE904H01010

Mar 1st

, 2013

TECPRO SYSTEMS LIMITED Result Update: Q3 FY13

HOLDHOLDHOLDHOLD

Stock Data

Sector Industrial Machinery

BSE Code 533266

Face Value 10.00

52wk. High / Low (Rs.) 207.65/114.00

Volume (2wk. Avg ) 3139.00

Market Cap ( Rs in mn ) 5804.51

Annual Estimated Results (A*: Actual / E*: Estimated)

Years FY12A FY13E FY14E

Net Sales 25296.62 24100.54 26124.99

EBITDA 4049.23 3693.57 4035.79

Net Profit 1249.29 375.86 392.60

EPS 24.75 7.45 7.78

P/E 4.65 15.44 14.78

Shareholding Pattern (%)

1 Year Comparative Graph

BSE SENSEX TECPRO SYSTEMS LTD

SYNOPSIS

Tecpro started as a material handling company in 2001 and has become a prominent player in Engineering, Procurement and Construction (EPC) of handling systems.

Tecpro Systems received an order worth Rs. 139.8 crore from The West Bengal Power Development Corporation Ltd.

Tecpro Systems received an order worth Rs. 146.6 crore from Damodar Valley Corporation for the supply of Coal Handling Plant Package for BTPS ‘A’

Tecpro Systems received an International order worth US $17.4 million from SK Engineering & Construction, South Korea for Paco Power Plant (2X160 MW) in Panama.

Tecpro Systems has considered and decided to acquire 100% paid up share capital of Tecpro Ispat Private Ltd.

Tecpro Systems Ltd has received order worth Rs. 267.3 crore from Kanti Bijlee Utpadan Nigam Ltd a subsidiary of NTPC Ltd.

Tecpro Systems order book position as on 31st Dec, 2012 stood at about Rs. 47.2 billion.

Net Sales and Operating Profit of the company are expected to grow at a CAGR of 10% and 9% over 2011 to 2014E respectively.

Peer Groups CMP Market Cap EPS P/E (x) P/BV(x) Dividend

Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%)

Tecpro Systems Ltd 115.00 5804.51 24.75 4.65 0.77 30.00

Cummins India Ltd 490.60 136174.50 25.98 18.91 6.66 550.00

Elecon Engineering Ltd 34.05 3157.30 6.49 5.24 0.71 90.00

Austin Engineering Ltd 49.50 172.20 10.81 4.58 0.34 25.00

Page 2

Investment Highlights

Results updates- Q3 FY13,

Tecpro Systems Ltd is a leading Engineering

Procurement and Construction Company providing

comprehensive range of services in Coal handling

and Ash handling, BoP packages for Power Sector &

Material Handling to Steel, Cement, Ports, Mining &

other industries in Infrastructure sector, reported

its financial results for the quarter ended 31st Dec,

2012.

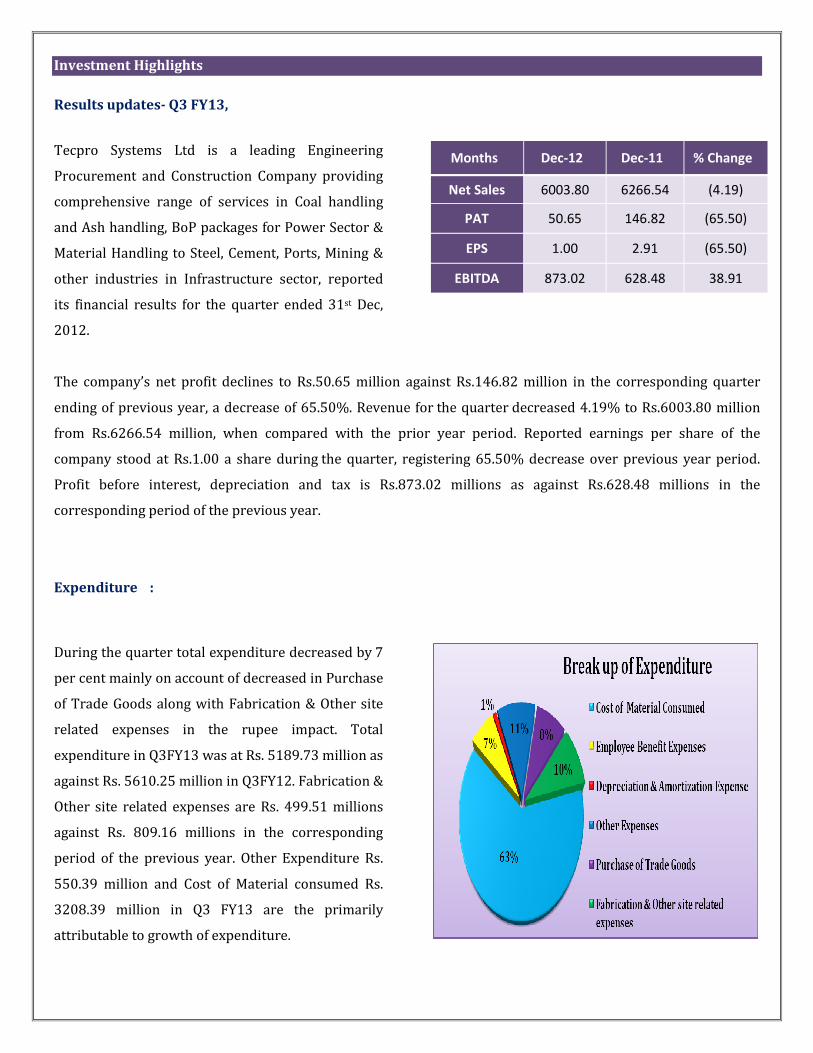

Months Dec-12 Dec-11 % Change

Net Sales 6003.80 6266.54 (4.19)

PAT 50.65 146.82 (65.50)

EPS 1.00 2.91 (65.50)

EBITDA 873.02 628.48 38.91

The company’s net profit declines to Rs.50.65 million against Rs.146.82 million in the corresponding quarter

ending of previous year, a decrease of 65.50%. Revenue for the quarter decreased 4.19% to Rs.6003.80 million

from Rs.6266.54 million, when compared with the prior year period. Reported earnings per share of the

company stood at Rs.1.00 a share during the quarter, registering 65.50% decrease over previous year period.

Profit before interest, depreciation and tax is Rs.873.02 millions as against Rs.628.48 millions in the

corresponding period of the previous year.

Expenditure :

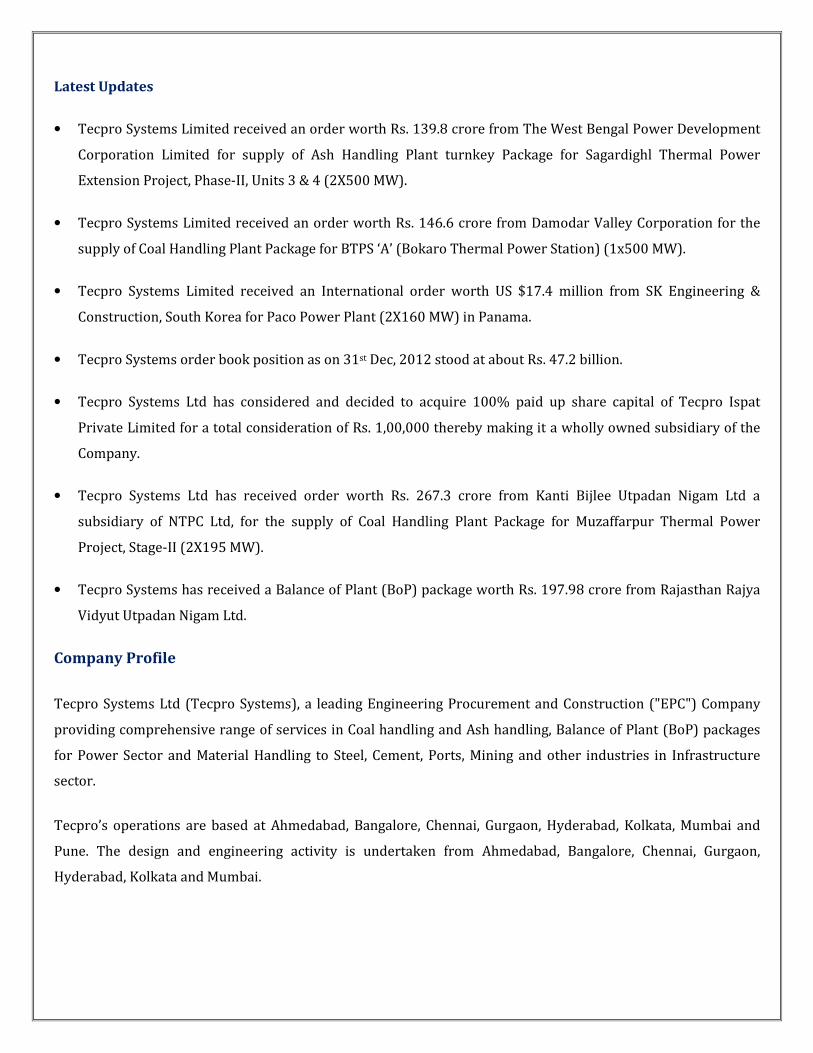

During the quarter total expenditure decreased by 7

per cent mainly on account of decreased in Purchase

of Trade Goods along with Fabrication & Other site

related expenses in the rupee impact. Total

expenditure in Q3FY13 was at Rs. 5189.73 million as

against Rs. 5610.25 million in Q3FY12. Fabrication &

Other site related expenses are Rs. 499.51 millions

against Rs. 809.16 millions in the corresponding

period of the previous year. Other Expenditure Rs.

550.39 million and Cost of Material consumed Rs.

3208.39 million in Q3 FY13 are the primarily

attributable to growth of expenditure.

Page 3

Latest Updates

• Tecpro Systems Limited received an order worth Rs. 139.8 crore from The West Bengal Power Development

Corporation Limited for supply of Ash Handling Plant turnkey Package for Sagardighl Thermal Power

Extension Project, Phase-II, Units 3 & 4 (2X500 MW).

• Tecpro Systems Limited received an order worth Rs. 146.6 crore from Damodar Valley Corporation for the

supply of Coal Handling Plant Package for BTPS ‘A’ (Bokaro Thermal Power Station) (1x500 MW).

• Tecpro Systems Limited received an International order worth US $17.4 million from SK Engineering &

Construction, South Korea for Paco Power Plant (2X160 MW) in Panama.

• Tecpro Systems order book position as on 31st Dec, 2012 stood at about Rs. 47.2 billion.

• Tecpro Systems Ltd has considered and decided to acquire 100% paid up share capital of Tecpro Ispat

Private Limited for a total consideration of Rs. 1,00,000 thereby making it a wholly owned subsidiary of the

Company.

• Tecpro Systems Ltd has received order worth Rs. 267.3 crore from Kanti Bijlee Utpadan Nigam Ltd a

subsidiary of NTPC Ltd, for the supply of Coal Handling Plant Package for Muzaffarpur Thermal Power

Project, Stage-II (2X195 MW).

• Tecpro Systems has received a Balance of Plant (BoP) package worth Rs. 197.98 crore from Rajasthan Rajya

Vidyut Utpadan Nigam Ltd.

Company Profile

Tecpro Systems Ltd (Tecpro Systems), a leading Engineering Procurement and Construction ("EPC") Company

providing comprehensive range of services in Coal handling and Ash handling, Balance of Plant (BoP) packages

for Power Sector and Material Handling to Steel, Cement, Ports, Mining and other industries in Infrastructure

sector.

Tecpro’s operations are based at Ahmedabad, Bangalore, Chennai, Gurgaon, Hyderabad, Kolkata, Mumbai and

Pune. The design and engineering activity is undertaken from Ahmedabad, Bangalore, Chennai, Gurgaon,

Hyderabad, Kolkata and Mumbai.

Page 4

Products Range

Material Handling Systems

• Turnkey Projects

Coal handling plants Conveying systems Crushing and Screening systems

• Equipment

Crushers Screens Feeders

• Technology

The company entered into collaboration and license agreements with 8 companies in relation to our material

handling operations.

� FAM Magdeburger Förderanlagen und Baumaschinen GmbH, Germany

� Siebtechnik GmbH

� Hein, Lehmann Trenn-Und Fördertechnik GmbH, Germany

� Won Duck Industrial Machinery Co. Ltd.

� Krusnohorske Strojirny Komorany a.s.

� MVW Lechtenberg und Beteiligungsgesellschaft GmbH

� Advanced Conveyor Technologies Inc. USA

Ash Handling Systems

• Turnkey Projects

� Bottom Ash Handling Systems Fly Ash Handling Systems HCSD

• Technology

The company has entered into collaboration and license agreements with 3 companies in relation to our ash

handling operations.

� GEA EGI Contracting/Engineering Company Limited

� Xiamen Longking Bulk Materials Science and Engineering Company Limited^^

� Pneuplan Oy

EPC Power

The EPC Power Division of Tecpro Systems Ltd takes care of EPC contracting of Power plants of various types

as follows:

� Coal based power plants (single/ multi fuels like indigenous Coal of all grades, Dolochar, Coal fines/

washery rejects - with Naphtha, CNG/ LNG and biomass as support fuels and imported coal from

Indonesia/ South Africa/ Australia)

� Waste heat recovery based power plants utilizing blast furnace / coke oven gas & cement kiln gas

Page 5

� Small/ Mini hydro electric power projects – turbines of Pelton, Francis & Kaplan types

� Municipal solid waste with most renowned technologies like mass burning & RDF technologies

� Tecpro provides State-of-the-art Design & engineering/ Project management/ Procurement/

Construction management.

� Tecpro’s scope of work/ services include concept to commissioning on complete EPC basis or BOP –

EPC basis of power projects.

Pollution Control

The Pollution Control Division of Tecpro Systems Ltd provides product as well as turnkey solutions from

concept to commissioning in the areas of Dust control, Noise Abetment systems etc as follows:

• Dust extraction & suppression system

• Scrubbers

• Cyclone separators

• Ventilation & Air dilution system.

• Industrial silencers for fans and steam vent applications

• Acoustic enclosures for fans and other machines

• Industrial fans and blowers

• Air intake systems

Subsidiary Companies

� Tecpro Energy Limited

� Tecpro Trema Limited

� Ajmer Waste Processing Company Private Limited

� Bikaner Waste Processing Company Private Limited

� Tecpro Systems (Singapore) Pte. Limited

� Eversun Energy Private Limited

� Ambika Projects (India) Private Limited

� PT Tecpro Systems Indonesia

Customer Relationship

• Material Handling

Page 6

• Ash Handling

• Balance of Plant

• Waste Heat Recovery

Page 7

Financial Highlight

Balance sheet as at March31st, 2012

(A*- Actual, E* -Estimations & Rs. In Millions)

Particulars March (Rs.in.mn) FY12A FY13E FY14E

EQUITY AND LIABILITIES:

Shareholders’ Funds:

a) Share Capital 504.74 504.74 504.74

b) Reserves and Surplus 7139.97 7445.75 7838.35

1. Net worth (a+b) 7644.71 7950.49 8343.09

Non-Current Liabilities:

Long-term borrowings 994.97 1293.46 1552.15

Deferred Tax Liabilities [Net] 1.14 1.23 1.29

Other Long Term Liabilities 1744.99 1570.49 1476.26

Trade Payables 903.25 1156.16 1375.83

Long Term Provisions 42.64 53.30 60.23

2. Total Non-Current Liabilities 3686.99 4074.64 4465.77

Current Liabilities:

Short-term borrowings 12011.42 15614.85 18425.52

Trade Payables 14167.59 18134.52 21580.07

Other Current Liabilities 3248.08 3930.18 4441.10

Short Term Provisions 408.25 375.59 360.57

3. Total Current Liabilities 29835.34 38055.13 44807.26

Total Liabilities ( 1+2+3 ) 41167.04 50080.26 57616.11

ASSETS:

Non-Current Assets:

Fixed Assets:

Tangible Assets 2351.79 3033.81 3579.89

Intangible Assets 41.71 58.39 72.99

Capital work-in-progress 315.70 366.21 402.83

a) Total Fixed Assets 2709.20 3458.42 4055.72

b) Other non-current assets 1342.56 1382.84 1410.49

c) Non Current Investments 215.53 183.20 166.71

d) Trade Receivables 6800.64 7752.73 8295.42

e) Long Term Loans and Advances 468.12 608.56 712.01

1. Total Non-Current Assets 11536.05 13385.74 14640.36

Current Assets:

Current Investments 1.04 1.09 1.14

Inventories 2312.46 3029.32 3695.77

Trade Receivables 16517.88 20099.05 23314.90

Cash and Bank Balances 2285.04 2353.59 2400.66

Short Term Loans and Advances 1980.57 2455.91 2799.73

Other Current Assets 6534.00 8755.56 10763.55

2. Total Current Assets 29630.99 36694.52 42975.75

Total Assets ( 1+2 ) 41167.04 50080.26 57616.11

Page 8

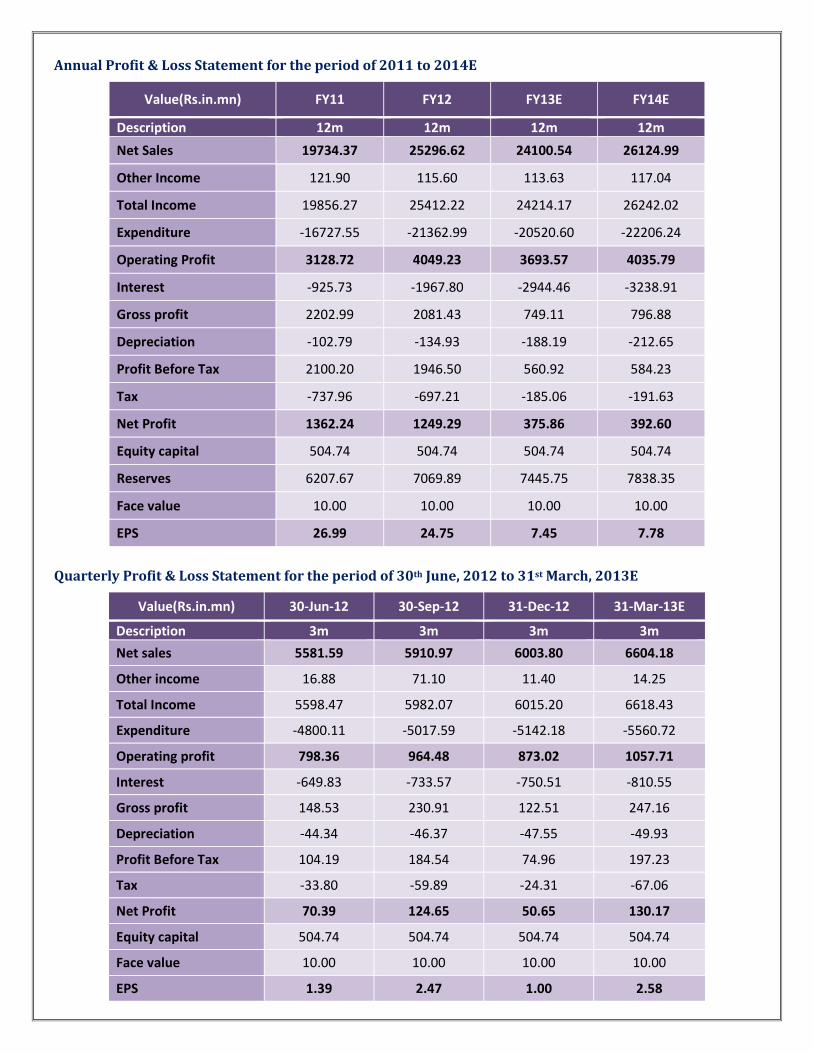

Annual Profit & Loss Statement for the period of 2011 to 2014E

Value(Rs.in.mn) FY11 FY12 FY13E FY14E

Description 12m 12m 12m 12m

Net Sales 19734.37 25296.62 24100.54 26124.99

Other Income 121.90 115.60 113.63 117.04

Total Income 19856.27 25412.22 24214.17 26242.02

Expenditure -16727.55 -21362.99 -20520.60 -22206.24

Operating Profit 3128.72 4049.23 3693.57 4035.79

Interest -925.73 -1967.80 -2944.46 -3238.91

Gross profit 2202.99 2081.43 749.11 796.88

Depreciation -102.79 -134.93 -188.19 -212.65

Profit Before Tax 2100.20 1946.50 560.92 584.23

Tax -737.96 -697.21 -185.06 -191.63

Net Profit 1362.24 1249.29 375.86 392.60

Equity capital 504.74 504.74 504.74 504.74

Reserves 6207.67 7069.89 7445.75 7838.35

Face value 10.00 10.00 10.00 10.00

EPS 26.99 24.75 7.45 7.78

Quarterly Profit & Loss Statement for the period of 30th June, 2012 to 31st March, 2013E

Value(Rs.in.mn) 30-Jun-12 30-Sep-12 31-Dec-12 31-Mar-13E

Description 3m 3m 3m 3m

Net sales 5581.59 5910.97 6003.80 6604.18

Other income 16.88 71.10 11.40 14.25

Total Income 5598.47 5982.07 6015.20 6618.43

Expenditure -4800.11 -5017.59 -5142.18 -5560.72

Operating profit 798.36 964.48 873.02 1057.71

Interest -649.83 -733.57 -750.51 -810.55

Gross profit 148.53 230.91 122.51 247.16

Depreciation -44.34 -46.37 -47.55 -49.93

Profit Before Tax 104.19 184.54 74.96 197.23

Tax -33.80 -59.89 -24.31 -67.06

Net Profit 70.39 124.65 50.65 130.17

Equity capital 504.74 504.74 504.74 504.74

Face value 10.00 10.00 10.00 10.00

EPS 1.39 2.47 1.00 2.58

Page 9

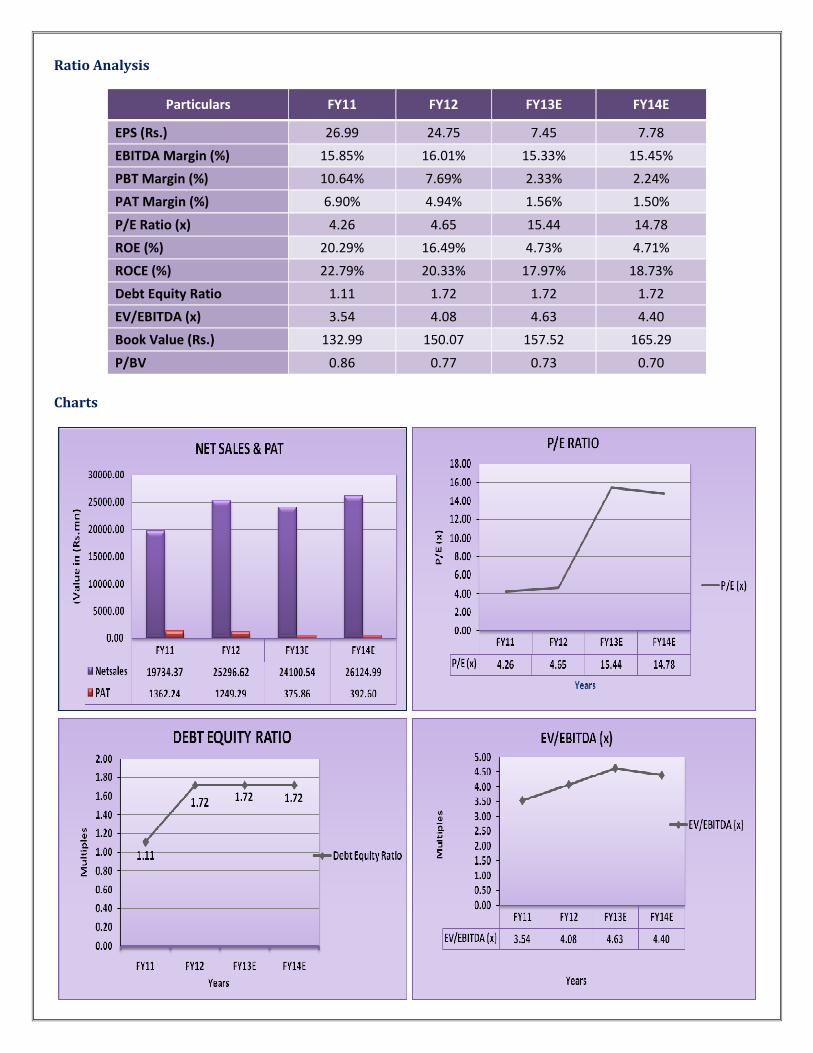

Ratio Analysis

Particulars FY11 FY12 FY13E FY14E

EPS (Rs.) 26.99 24.75 7.45 7.78

EBITDA Margin (%) 15.85% 16.01% 15.33% 15.45%

PBT Margin (%) 10.64% 7.69% 2.33% 2.24%

PAT Margin (%) 6.90% 4.94% 1.56% 1.50%

P/E Ratio (x) 4.26 4.65 15.44 14.78

ROE (%) 20.29% 16.49% 4.73% 4.71%

ROCE (%) 22.79% 20.33% 17.97% 18.73%

Debt Equity Ratio 1.11 1.72 1.72 1.72

EV/EBITDA (x) 3.54 4.08 4.63 4.40

Book Value (Rs.) 132.99 150.07 157.52 165.29

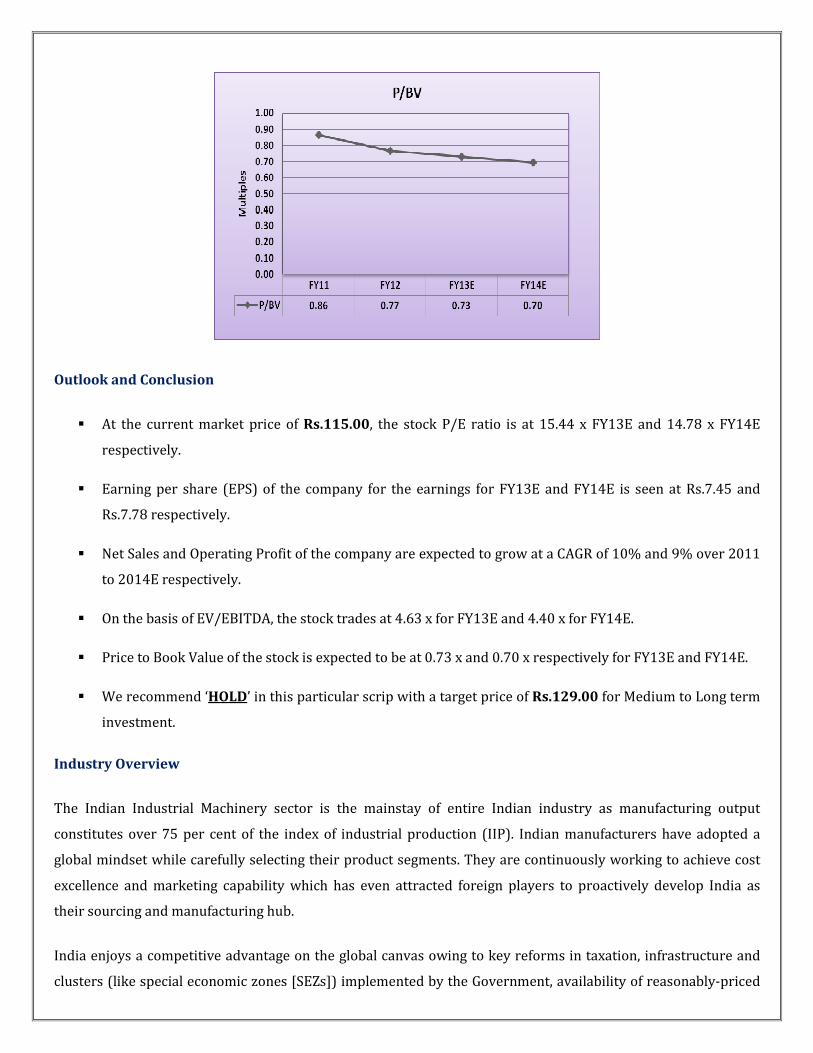

P/BV 0.86 0.77 0.73 0.70

Charts

Page 10

Outlook and Conclusion

� At the current market price of Rs.115.00, the stock P/E ratio is at 15.44 x FY13E and 14.78 x FY14E

respectively.

� Earning per share (EPS) of the company for the earnings for FY13E and FY14E is seen at Rs.7.45 and

Rs.7.78 respectively.

� Net Sales and Operating Profit of the company are expected to grow at a CAGR of 10% and 9% over 2011

to 2014E respectively.

� On the basis of EV/EBITDA, the stock trades at 4.63 x for FY13E and 4.40 x for FY14E.

� Price to Book Value of the stock is expected to be at 0.73 x and 0.70 x respectively for FY13E and FY14E.

� We recommend ‘HOLD’ in this particular scrip with a target price of Rs.129.00 for Medium to Long term

investment.

Industry Overview

The Indian Industrial Machinery sector is the mainstay of entire Indian industry as manufacturing output

constitutes over 75 per cent of the index of industrial production (IIP). Indian manufacturers have adopted a

global mindset while carefully selecting their product segments. They are continuously working to achieve cost

excellence and marketing capability which has even attracted foreign players to proactively develop India as

their sourcing and manufacturing hub.

India enjoys a competitive advantage on the global canvas owing to key reforms in taxation, infrastructure and

clusters (like special economic zones [SEZs]) implemented by the Government, availability of reasonably-priced

Page 11

skilled labor workforce and a positive eco-system. Moreover, the global trend to manufacture and source

products in low-cost countries has gained pace in the past decade, particularly in skill-intensive industries, and

India has been able to leverage on the opportunity to its best.

Growth Trend

The HSBC India Manufacturing Purchasing Managers' Index (PMI) - a measure of factory production -was at 56.6

in February 2012. The latest reading indicated a marked expansion of the Indian manufacturing sector which

was spurred by new orders (that touched a 10-month high) and a rise in new export business for the month.

The Indian manufacturing sector also showed moderate overall business sentiment in October-December 2011

quarter, as per the Industrial Outlook Survey conducted by the Reserve Bank of India (RBI) for the quarter. The

business expectation index (BEI), which acts as a barometer of the overall health of the manufacturing sector,

stood at 110.1 for the assessment quarter while RBI expects it at 117.2 for the January-March 2012 quarter.

The IIP for the Mining, Manufacturing and Electricity sectors for the month of December 2011 stood at 136.2,

190.7 and 149.8 respectively wherein manufacturing grew by 1.8 per cent. In terms of industries, 15 out of the

22 industry groups (as per 2-digit NIC-2004) in the manufacturing sector have shown positive growth during the

reported month.

Key Developments and Investments

• Shanghai Electric, China's biggest power equipment company, is all set to establish a manufacturing

facility in India. The company is in advanced stages of negotiations with French power major Alstom for a

joint venture facility that would manufacture boilers for power projects

• Detroit-headquartered automaker Ford Motor Co will make India its manufacturing hub for small, low-

cost cars that would cater to markets in Africa and the Asia-Pacific region. The company will set up a

plant in northwest India in 2014 that would entail an investment of US$ 1 billion and would have an

annual capacity of 2, 40, 000 units. Ford's existing manufacturing unit in Chengalpattu is undergoing

enhancements and is expected to be in full production mode by the end of 2012.

• Germany-based Hummel AG Group's subsidiary Hummel Connector Systems is establishing a

manufacturing facility at Neelambur, near Coimbatore, entailing an investment of €3,00, 000 (US$

3,94,360.03). Hummel produces cable glands, circular connectors, industrial enclosures, touch panels and

electronics for medical, measurement and control technology

• In order to price its new offering competitively, Japanese bike-maker Yamaha is planning to manufacture

its soon-to-arrive 250cc sports bike locally in India

• Japan-based electronics and durables giant Toshiba has commenced local manufacturing of selected TV

models in limited numbers at a facility in Dehra Dun. In order to ramp up its volumes across various

categories, the company is conducting a feasibility study to go-in for local manufacturing in a bigger way

Page 12

Government Initiatives

The Indian Government is laying intense focus on developing the manufacturing sector. It has set itself a target to

ensure that 25 per cent share of gross domestic product (GDP) growth comes from manufacturing by 2022 and

eventually creating 100 million job opportunities to make the growth inclusive.

Mr. Talleen Kumar, Joint Secretary, Department of Industrial Policy and Promotion, Ministry of Commerce and

Industry, Government of India, has stated that there are five more National Manufacturing Investment Zones

(NMIZs) which are being proposed apart from seven of them which are ready for execution in the Delhi Mumbai

Industrial Corridor.

The Indian Government has also invited Italian industry to get involved in the proposed NMIZs. Mr. Anand

Sharma, Commerce, Industry and Textiles Minister, India, has had a meeting with Italy's Foreign Minister Mr.

Guilio Terzi di Sant' Agata recently. India and Italy have Joint Working Groups (JWG) which give their

recommendations about infrastructure, manufacturing, innovation and science, information technology and

pharmaceuticals. More JWGs on tourism, hospitality and agro-processing are being considered.

The Government has also made certain recommendations for the manufacturing policy that would be unveiled

during the announcement of 12th five year plan. The proposed manufacturing policy enlists the following

recommendations:

• Make amendments in duty structure to ensure equal opportunities to local manufacturers. In this regard,

Government has proposed to impose 19 per cent duty on imported equipment for mega power projects.

The cabinet has also agreed to give preference to indigenously manufactured electronic products (step-

up value addition between 25-45 per cent in five years) in Government procurement

• Public sector enterprises (PSEs) should focus on areas that hold national importance, but look

commercially unfeasible to the private sector because of the heavy investments and risks involved. For

instance: aircraft production

• Ensure flexibility for entry and exit of public investment in the process of industrial growth by endorsing

a single holding structure or new PSEs. The model is proposed to be a combination of a sovereign wealth

fund, a single holding structure and the Government acting as a venture capitalist

Road Ahead

According to a joint report titled 'Made in India-the Next Big Manufacturing Export Story', prepared by industry

body CII and McKinsey, manufacturing exports from India could increase from US$ 40 billion in 2002 to about

US$ 300 billion by 2015. This would make India rake-in a share of approximately 3.5 per cent in the world

manufacturing trade.

Page 13

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation for the purchase or sale

of any financial instrument or as an official confirmation of any transaction. The information contained herein is

from publicly available data or other sources believed to be reliable but do not represent that it is accurate or

complete and it should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s affiliates shall

not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the

information contained in this report. This document is provide for assistance only and is not intended to be and must

not alone be taken as the basis for an investment decision.

Page 14

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

B.Anil Kumar Diversified

A.Nagaraju Cement, Reality & Infra, Oil & Gas

Ashish.Kushwaha IT, Consumer Durable & Banking

K. Jagadhishwari Devi Diversified

Abdul Khabeer Diversified

A.Ravi Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com

![PDF3A92 - environmentclearance.nic.inenvironmentclearance.nic.in/writereaddata/Online/TOR/27_Sep_2017...CPP- [45 MW to 159 MW (50 MW Coal & Dolochar Mix based and 109 WHRB] of M/S](https://static.documents.pub/doc/80x56/5abc18b57f8b9a441d8da596/pdf3a92-45-mw-to-159-mw-50-mw-coal-dolochar-mix-based-and-109-whrb-of-ms-rashmi.jpg)

![TECPRO SYSTEMS LIMITED · limited (“tecpro systems”, “our company” or “the issuer”) aggregating rs. [l] (the “offer”). the offer comprises a fresh issue of up to 6,250,000](https://static.documents.pub/doc/80x56/5f4cb5ab09b5fa18f7094081/tecpro-systems-limited-aoetecpro-systemsa-aoeour-companya-or-aoethe-issuera.jpg)