40

TEE International Limited Corporate Profile 2016

| Date post: | 14-Feb-2017 |

| Category: |

Documents |

| Upload: | pua-zai-wei |

| View: | 227 times |

| Download: | 1 times |

TEE International Limited

Corporate Profile 2016

This presentation should be read in conjunction with TEE International Limited’s (the “Company”) Audited Full Year Financial

Statements for the period ended 31 May 2016 annual report released via SGXNET on 9 September 2016. The information contained

in this presentation has not been independently verified. No representation or warranty express or implied is made as to, and no

reliance should be placed on, the fairness, accuracy, completeness or correctness of such information or opinions contained herein.

The information contained in this document should be considered in the context of the circumstances prevailing at the time and

has not been, and will not be, updated to reflect material developments which may occur after the date of the presentation.

Neither the Company nor any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or

otherwise) for any loss howsoever arising, whether directly or indirectly, from any use, reliance or distribution of this presentation or its

contents or otherwise arising in connection with this presentation.

Certain statements in this presentation may constitute “forward-looking statements”, including forward-looking financial information.

Such forward-looking statements and financial information involve known and unknown risks, uncertainties and other factors which

may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any

future results, performance or achievements expressed or implied by such forward-looking statements and financial information.

Such forward-looking statements and financial information are based on numerous assumptions regarding the Company’s present

and future business strategies and the environment in which the Company will operate in the future. Because these statements and

financial information reflect the Company’s current views concerning future events, these statements and financial information

necessarily involve risks, uncertainties and assumptions. Actual future performance could differ materially from these forward-looking

statements and financial information. The Company expressly disclaims any obligation or undertaking to release publicly any

updates or revisions to any forward-looking statement or financial information contained in this presentation to reflect any change in

the Company’s expectations with regard thereto or any change in events, conditions or circumstances on which any such

statement or information is based, subject to compliance with all applicable laws and regulations and/or the rules of the SGX-ST

and/or any other regulatory or supervisory body or agency. You are cautioned not to place undue reliance on these forward-

looking statements, which are based on the current view of management on future events.

This presentation includes market and industry data and forecast that have been obtained from internal survey, reports and studies,

where appropriate, as well as market research, publicly available information and industry publications. Industry publications,

surveys and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but

there can be no assurance as to the accuracy or completeness of such included information. While the Company has taken

reasonable steps to ensure that the information is extracted accurately and in its proper context, the Company has not

independently verified any of the data from third party sources or ascertained the underlying economic assumptions relied upon

therein.

Business Overview

Company Profile

4

Founded in 1991, TEE International Limited builds on

our core engineering origins to evolve into a

dynamic group with business interests in engineering,

real estate and infrastructure, which spans

across 7 countries in Asia-Pacific.

1991 – 1995 Established as general

Electrical contractors

1996 – 2000 Expanded engineering

business into Malaysia &

Thailand

2001 – 2005 Listed on SGX SESDAQ with

a market cap of

S$16M & moved into

facilities mgmt business

in Thailand

2006 – 2010 Diversified into real

estate development in

Singapore & Thailand and

upgraded to

SGX Mainboard

2011 – 2016 Extended into other

regional markets –

Hong Kong, New Zealand,

Australia.

Diversified into

infrastructure business –

wastewater treatment

in Thailand & powerplant in

Philippines

Expanded into short-term

accommodation business

Issued bonus warrants

Listed real estate

subsidiary – TEE Land

Limited

Listed associated

companies – CMC

Infocomm Limited &

Chewathai PCL

Regionalisation and Diversification Focus

Mo

vin

g u

p t

he

Va

lue

Ch

ain

TEE Group at a Glance

5

TEE International Limited Listed on SGX Mainboard

• TEE Land Limited 63.18% owned

subsidiary listed on SGX Mainboard

• Regional real estate developer

ENGINEERING REAL ESTATE INFRASTRUCTURE

• Integrated engineering solutions

provider

• Specialises in M&E engineering and Building & Construction

• Invests in infrastructure assets & businesses relating to Water, Power & Infocommunications

Strategic focus for growth

6

Regional total solutions provider in Asia-Pacific

Focus on building business excellence

Partner of choice that delivers value

Our Goals

Integrated

Platform

Engineering

Infrastructure Real Estate

Business synergies from core

engineering fundamentals

Our

Regional

Footprint

Strengthening foothold in

overseas market

Building on business

excellence for growth

Human Capital

Value Creation

Business Quality

GROWTH

Singapore Malaysia

Thailand Philippines

Hong Kong Australia

New Zealand

Regional Footprint

7

Thailand

• 11 real estate

developments

• Facilities

management

• Invested & manages 2

wastewater

treatment plants

Thailand

Malaysia

Malaysia

• Construction of water

treatment plant

• Flagship mixed

development project

in Cyberjaya

Singapore

Singapore

• 70% of S$372M order book

• 24 real estate development

• Expanding into Waste-to-Energy

business

Australia

New Zealand

Australia • Owns 2 boutique

hotels in Sydney

New Zealand

• Owns 1 workers’ short

term accommodation &

1 guesthouse in

Christchurch

Philippines

Philippines

• Invested in a 25MW

power plant

Hong Kong

Hong Kong

• Engineering works for

The Parisian, Macao

Engineering Business

9

Suite of Engineering Capabilities

Builders Architectural Civil & Structure Mechanical &

Electrical

BCA CW01 Work Head A1 Grading

BCA ME15 Work Head L6 Grading

BCA ME01 Work Head L6 Grading

BCA ME05 Work Head L6 Grading

BCA CR06 Work Head L6 Grading

10

Engineering Business

Mission Critical Projects

Remodelling of NUH

Upgrading & fitting-out of existing MRT

stations

Upgrading & fitting-out of

shopping complex

Upgrading & fitting-out of institutions of

higher learning

Upgrading & fitting-out of commercial

banks

Focus on Rebuilding Projects

Building & Construction Division

11

Focus on Mega Integrated M&E and Special Services

Projects

Mechanical & Electrical Division

Asia Square

Tower One

Procter & Gamble

Singapore

Innovation Centre

Marina Bay

Sand Integrated

Resorts

Changi Airport Group

Marina One

Development

Engineering Business

Major ongoing engineering projects

12

Marina One Contract Value:

S$142.2M

Changi Airport Group Contract Value: S$177M*

*Cumulative figure of contracts awarded

Tampines Hub Contract Value: S$33.0M

Frasers Tower Contract Value:

S$43.9M

MDIS – Educity@Iskandar Contract Value: S$70.0M

AXA Tower Contract Value: ~S$90.0M

Outstanding

Order Book:

S$316M As at 31 Aug 16

Kedah WTP Contract Value: S$15.6M

Engineering Order Book Trend & Outlook

13

23 31 34 33 55

35

150

256

198

235 214 215

360

455

316

0

50

100

150

200

250

300

350

400

450

500

SG

D ‘m

il

ORDER BOOK

• Bidding for large-scale and sizable projects

• Expansion of Changi Airport (Changi

East development) presents

opportunities due to strong track

record

• Higher demand for public sector

projects i.e. institutions, healthcare

facilities that requires complex

engineering solutions

• Continue to scale up the engineering

business

Real Estate Business

Real Estate Regional Presence

15

Thailand

Malaysia

Singapore

New Zealand

THAILAND

11 Chewathai RBF 2

Chewathai Interchange

Chewathai Residence Bang Pho

Hallmark Chaengwattana

Hallmark Ngamwongwan

Chewathai Ratchaprarop

The Surawong

Chewathai Ramkhamhaeng

Chewathai RBF 1

Chewathai Petchkasem 27

Chewarom Rangsit – Don Meaung

MALAYSIA

1 Third Avenue, Cyberjaya

SINGAPORE

23 Cantiz @ Rambai

The Thomson Duplex

31 &31A Dunsfold

448 @ East Coast

91 Marshall

Aura 83

The Peak @ Cairnhill I

223@ Mountbatten

The Boutiq

TEE Building

Palacio

Sky Green

Rezi 26

Hilbre28

Rezi 3Two

Newest

Floraville,Flora Vista, FloraView

Trio

Hexacube

183 LONGHAUS

Harvey Ave

Geylang Lor 35

241 Pasir Panjang Road

AUSTRALIA

2 Quality Hotel CKS Sydney Airport

Larmont Sydney

NEW ZEALAND

2 Workotel @ Riccarton

Thistle Guesthouse

Australia

Real Estate Developments & Outlook

16

Mixed development (former Longhouse)

Residential units over 75% sold

Commercial units not launched

Hilbre28 along Hillside Drive close to 60%

sold to date

• Focus on identifying well-located freehold properties and land to acquire in Singapore

and the region

• Continue to grow the portfolio of investment

properties for recurring income

• Take on more majority-owned development projects

11

29.7

40.3

60.2

33.7

-0.7

2.9

9.2 10

14.7

1.5 3.9

11.9 9.9

7.3

-10

0

10

20

30

40

50

60

70

SG

D (

mil)

Revenue Share of Results of Associates Net Profit

FY2012 FY2013 FY2014 FY2015 FY2016

Real Estate Portfolio

17

RBF 1 - Chewathai Rezi3Two 91 Marshall Workotel

Third Avenue Chewathai

Interchange Quality CKS Sydney

Airport Hotel

Chewathai

Petchkasem 27

Infrastructure Business

Growing the Infrastructure Business

19

•Natural progression for TEE given our background in M&E

•Moving up the value chain to own the assets

•Focus on Water, Power & Infocommunications segment

Play in the NICHE space

Having the

MARKET

Knowledge

• Need to expand overseas, given the limited scope and

breadth in Singapore

• Leverage on our TEE network or work through a strong local

partner

• We play in a space that the big established infra players

cannot enter

• To move their needle, the “Bigger Boys” look at projects

>US$75M

• So we actively hunt for projects in the range of < US$75M

EXPERTISE to

undertake

these Infra

projects

Infrastructure Business Outlook

20

Power Sector in Philippines

• Strong Pipeline by private sector with

5.2 GW of committed generation capacity

under development

• 13 million number of Filipinos still living with

out power large capacity are still needed

to meet the demand-supply gap

• Government has plans to increase the

domestic electrification rate to 90% by

2017, private investment will be required

to support addition to capacity

• Expected aggregate investment

opportunity of about US $25 billion until

2030.

Water Sector in Thailand

• Water resources in Southeast Asia are

under strain from rapid urbanisation and

industrialisation

• Water pollution in Thailand is one of the

severe environmental problems.

• Bangkok Metropolitan Administration is

determined to reduce the amount of

wastewater pollution

• GETCO is currently one of the leading

wastewater treatment companies in

Thailand with total capacity of 350 million

litres per day.

• Leverage on capabilities to operate and

maintain other wastewater treatment

plants under the Bangkok Metropolitan

Administration.

Current Infrastructure Projects

21

Water

Global Environmental

Technology Co. Limited

(GETCO) Description

Investment

(49% ownership) S$5M

IRR 21.7%

Capacity 350,000 m3 per day

Competitive Advantages

Leading player in

Thailand

One of largest waste water treatment companies in Thailand with a capacity

of 350 million litres of waste water treated every day.

Diversified sources of

income

Provides wastewater treatment from multiple entities and sectors, ranging from

commercial, industrial and residential communities.

First underground waste

water treatment plant

Operates first underground waste water treatment plant in Bang Sue.

Underground waste water treatment plants generally provides advantages

such as efficient land usage as well as environment preservation.

Key Statistics

Current Infrastructure Projects

22

Power

Key Statistics Powersource Philippines

Distributed Power Holdings Description

Investment

(21% ownership)

S$ 4.2 million

IRR 14%

Capacity 25MW

Competitive Advantages

Strategic Partnership Facility is embedded into Lafarge cement plant. Lafarge Philippines is part of

the Lafarge Group, which is world leader in building materials and major player

in cement provider. One of the key partners include the country chairman for

Jardine Matheson Group in Philippines.

Secured Power

purchase Agreement

Secured a 25 year PPA with Illigan Light and Power Inc, which is the twelve

largest private distribution utility in Philippines. This allows TEE to attain

guaranteed cash flow in the entire 25 year horizon, which will limit our

downside

Participation of

renowned Japanese

Company Nippon Koei

Japan’s Number 1 International Engineering Consultant Nippon Koei has

entered into the strategic partnership in 2015. Nippon Koei has acquired equity

stake in power plant.

Key Achievements and

Developments in FY2016

Key Achievements in FY2016

24

Largest Rebuilding

Contract

AXA Tower

Gaining Foothold With

Changi Airport Group

Changi East Development

Broadening Infrastructure

Engineering Base

Wastewater Treatment

Plant in Kedah

Multiple Growth Platforms

New Heights Attained Robust Partnership Foundation for Future

Recent Developments

25

• Total unfulfilled order book of S$316M

• New contract from repeat customer (CAG)

• New large-scale project to provide A&A works for existing office tower

Engineering

• Strategic partnership of Nippon Koei Co., Ltd. and its investment into Philippines Distributed Power Holdings, Inc.

• Expanding into Waste-to-Energy segment

Infrastructure

• Associated company Chewathai Public Company Limited listed on SET in April 2016

• New land acquisitions in Singapore and Thailand

• Steady sales for our developments

Real Estate

Into the Horizon

Evolution of E&C

27

Large Scale

New Projects

Fast Turnaround

Rebuilding Projects

Infrastructure

Engineering Engineering

Strategy

Key Projects

• Marina One

• Marina Bay Sands

• Asia Square

• Frasers Tower

• AXA Building

• Centre Point

• PSB Academy

• Kedah Water Plant

• Changi East

Development

Offering diverse set of Engineering Solutions

Rationale

Long Visibility &

Significant addition

to order book

Fast Turnaround –

Aids in Cash Flow

Infrastructure is a

focus for

Government

Geared Up for Growth

28

Year: 2001

Total Market Capitalisation:

SGD 16m

Employees: 160

Countries Ventured: 2

Revenue: S$50m

Significant Growth Since 2002

Year : 2016

Total Market Capitalisation:

SGD 110m

Employees: 450

Countries Ventured: 7

Revenue: S$250m +

Strategic Diversification

29

100%

Revenue Segment

Engineering

Early Years to 2011

95%

5%

Revenue Segment

Engineering

Real Estate

From 2012

65%

34%

1% Revenue Segment

Engineering

Real Estate

Infrastructure

2016 and

Beyond

Strategic Diversification

Into the Horizon

30

Horizon The Into

Visible Profit Streams

PowerPlant

coming online

Engineering Order

Book at S$372m

Sales from

Cyberjaya

Future Tenders

Expanding into

Waste to Energy

Infrastructure &

Engineering new

Business

Investment Merits

Investment Merits

32

Established & Proven Track Record

Integrated Business Platform with

Synergies to Create Value

Established Regional Network

Long Term Partnerships with Regional

Local Reputable Partners

Dedicated & Experienced

Management Team

1

2

3

4

5

Financial Snapshot

Financial Snapshot of FY2016

34

0

50

100

150

200

250

300

82% since 2012

Source: Bloomberg

Strong track record of 10 years Revenue

growth at 14% CAGR S$’Mil

FY16

Revenue

S$261m

Growth

From

FY15

20%

Revenue

35

-15

-10

-5

0

5

10

15

20

25

-15

-10

-5

0

5

10

15

20

25

FY2005 FY2006 FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 2016

Net Income

Strong track record of 10 years Net Income

growth at 13.4% CAGR

Resilient against

slowed GDP growth

Source: Bloomberg

% S$’Mil

Financial Snapshot of FY2016

Revenue by BU

36

0

50

100

150

200

250

300

FY2012 FY2013 FY2014 FY2015 FY2016

[VALUE]

(92%)

[VALUE]

(85%) [VALUE]

(79%) [VALUE]

(70%)

[VALUE]

(85%)

[VALUE] (8%)

[VALUE] (14%)

[VALUE] (20%) [VALUE] (28%)

[VALUE] (13%)

[VALUE] (1%) [VALUE] (1%)

[VALUE] (1%)

[VALUE] (1%) [VALUE] (8%)

[VALUE] (1%)

S$

’mil

Engineering Real Estate Infrastructure Corporate & Others

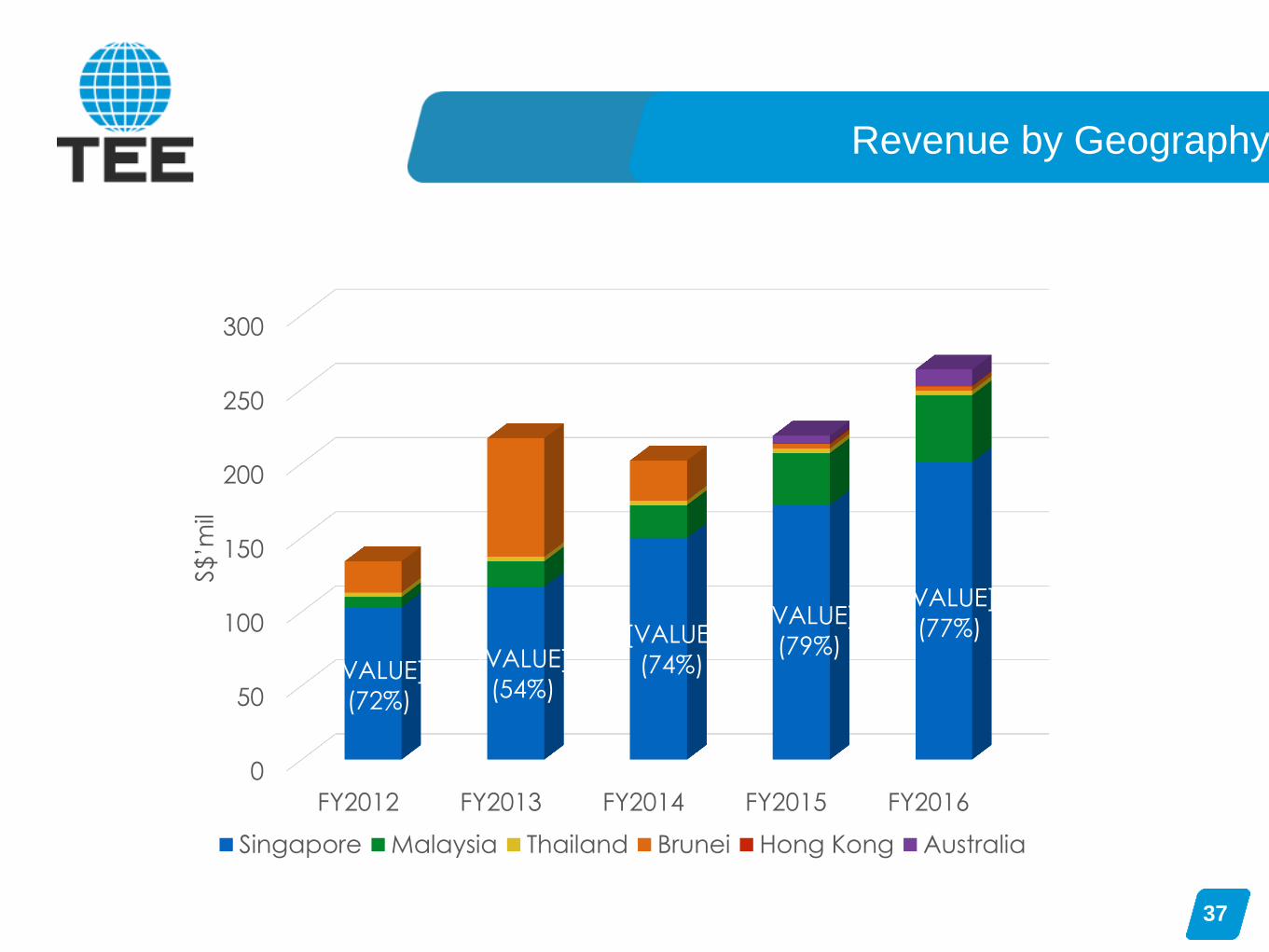

Revenue by Geography

37

0

50

100

150

200

250

300

FY2012 FY2013 FY2014 FY2015 FY2016

[VALUE]

(72%)

[VALUE]

(54%)

[VALUE]

(74%)

[VALUE]

(79%)

[VALUE]

(77%)

S$

’mil

Singapore Malaysia Thailand Brunei Hong Kong Australia

Profit & Loss Highlights

38

(S$‘000) FY2016 FY2015

Revenue 261,706 217,895

Gross Profit 29,855 35,862

Gross Profit Margin 11% 16%

Profit for the Year 10,719 12,882

Profit Margin 4% 6%

Finance Expenses 8,793 7,037

EBITDA 23,844 23,079

Interest Cover Ratio 2.2 times 2.8 times

Balance Sheet Highlights

39

(S$‘000) As at 31 May

2016 As at 31 May 2015

Total Assets 592,951 557,575

Total Liabilities 423,916 395,389

Secured Debt 198,721 177,366

Total Debt 271,358 256,677

Total Equity 169,035 162,186

Secured Debt to

Total Assets 0.34 times 0.32 times

Thank you

![TEE Certification Process v1 - GlobalPlatform · [TEE EM] GPD_TEN_045 : GlobalPlatform TEE Security Target Template . Public [TEE ST] GPD_SPE_050 : GlobalPlatform TEE Common Automated](https://static.documents.pub/doc/80x56/6027a08e90016542ee50485b/tee-certification-process-v1-globalplatform-tee-em-gpdten045-globalplatform.jpg)