Page 1

Submitted by:

Group 2

Aditya Mahadev Prakash 1311144

B Kiran Maruthi 1311154

Aditi Nehete 1311178

Sharad Chandran R 1311199

Swati Ramteke 1311189

COMPETITION

&

STRATEGY TELECOMMUNICATION INDUSTRY ANALYSIS

Page 2

2

Table of Contents 1. Introduction .......................................................................................................................................... 4

2. Evolution of Telecom Industry in India ................................................................................................. 4

3. Porter’s Five Forces Model ................................................................................................................... 6

3.1 Threat of New Entrants ..................................................................................................................... 6

3.1.1 Barriers to Entry ........................................................................................................................... 6

I. Economies of Scale .......................................................................................................................... 6

II. Differentiation ................................................................................................................................. 7

III. Brand Identity ................................................................................................................................. 7

IV. Switching Cost ................................................................................................................................ 7

V. Access to Distribution Channel ....................................................................................................... 8

VI. Capital Requirement ...................................................................................................................... 8

VII. Access to Technology .................................................................................................................... 8

VIII. Access to Raw Materials .............................................................................................................. 8

IX. Government Protection ................................................................................................................. 8

3.2 Industry Rivalry ................................................................................................................................. 9

I. Number of Competitors ................................................................................................................ 9

II. Industry Growth .......................................................................................................................... 10

III. Fixed costs ................................................................................................................................... 11

IV. Exit barriers .................................................................................................................................. 11

V. Switching Costs, Product Differentiation .................................................................................... 12

3.3 Bargaining Power of the Suppliers .................................................................................................. 12

I. Number of suppliers ................................................................................................................... 12

II. Availability of substitutes ............................................................................................................ 12

III. Switching costs ............................................................................................................................ 12

IV. Supplier’s threat of forward integration ..................................................................................... 13

V. Industry’s threat of backward integration .................................................................................. 13

VI. Industry’s importance to supplier ............................................................................................... 13

3.4 Bargaining Power of the Buyers ............................................................................................................ 13

3.4.1 Analyzing Customer Sensitivity: ..................................................................................................... 13

I. Product Differentiation ............................................................................................................... 13

II. Competition between Buyers ..................................................................................................... 14

Page 3

3

3.4.2 Analyzing Relative Buying Power: .................................................................................................. 14

I. Size and Concentration of Buyers relative to products .............................................................. 14

II. Buyers Switching Costs ............................................................................................................... 14

III. Buyers information ...................................................................................................................... 14

IV. Buyers ability to backward integrate ........................................................................................... 15

3.5 Threat of Substitutes ....................................................................................................................... 15

4. Growth ................................................................................................................................................ 16

5. Future Trends ...................................................................................................................................... 16

6. Summary ............................................................................................................................................. 16

7. Appendix ............................................................................................................................................. 17

8. References .......................................................................................................................................... 23

Page 4

4

1. Introduction

Telecom Industry is split into the following three segments

Mobile (Wireless): Comprises establishments operating and maintaining switching and transmission

facilities to provide direct communications via airwaves

Fixed Line (Wireline): Consists of companies that operate and maintain switching and transmission

facilities to provide direct communications through landlines, microwave or a combination of

landlines and satellite link-ups

Internet Services: Includes internet service providers (ISPs) that offer broadband internet

connections through consumer and corporate channels

2. Evolution of Telecom Industry in India

The telecom sector was formally introduced in India in 1881.However the actual evolution of the

telecom industry started in 1985 after the Indian Government set up the Department of

Telecommunications (DoT).In 1986, Mahanagar Telephone Nigam Limited (MTNL) and Videsh Sanchar

Nigam Limited (VSNL) were carved out of DoT to run the telecom services of metro

cities(Delhi and Mumbai) and international long distance operations respectively.1

The entire evolution of the telecom industry can be classified into three distinct phases.

Phase I- Pre-Liberalization Era (1980-89)

Phase II- Post Liberalization Era (1990-99)

Phase III- Post 2000

Until the late 90s the Government of India held a monopoly on all types of communications – as a result

of the Telegraph Act of 1885. Increased demand for telephones in India in the 90’s forced the

government to open doors to privatization and liberalization. Post-liberalization Indian telecom market

became one of the most liberalized markets in the world with private participation in almost all of its

segments.

1VanitaKohli (14 June 2006). The Indian Media Business. SAGE. pp. 189–. ISBN 978-0-7619-3469-1.

Page 5

5

In 1997, the government set up TRAI (Telecom Regulatory Authority of India) to provide autonomy in

deciding tariffs and policy making. The New Telecom Policy (NTP-1999) provided the much needed

impetus to the growth and liberalization of the industry. The policy introduced the concept of

telecommunication for all and its vision was to expand the telecommunication facilities to all the villages

in India. International players entered the market through joint ventures with state owned telecom

companies. Foreign firms were eligible to 49% of the total stake, but were just involved in technology

transfer, and not policy making. The government corporatized the operations wing of DoT on 1 October

2000 as Bharat Sanchar Nigam Limited (BSNL).

After March 2002 the government increased the allowable stake to 74% for foreign companies. As a

result, the service fees finally reduced and the call costs reduced greatly enabling every common

middle-class family in India to afford a cell phone. Nearly 32 million handsets were sold in India. Many

private operators, such as Reliance Communications, Tata Indicom, Vodafone, Airtel, Idea etc.,

successfully entered the high potential Indian telecom market.

In March ’98 there were only 0.88 million mobile subscribers in India with half of them from the Mumbai

and Delhi circles. NTP ’99 helped the mobile services take off in ’99-2000 adding 0.7 million customers to

its base. By 2003 the additions touched 6.6 million.

The implementation of Calling Party Pays (CPP) where incoming calls were made free and launch of

services by Reliance brought more low usage customers to mobile telephony. In 2004-05 with 52.2m

customers, the total mobile subscriber base overtook the total fixed line subscriber base. Since then the

industry has been adding more than 4m mobile subscribers every month.2

India has opted for the use of both GSM (global system for mobile communications) and CDMA (code-

division multiple access) technologies in the mobile sector. Along with landline and mobile phones,

some companies also provide the WLL service. The mobile tariffs in India have also become lowest in the

world.

2 State of the Industry, Telecom Industry Report- Crisil, India

Page 6

6

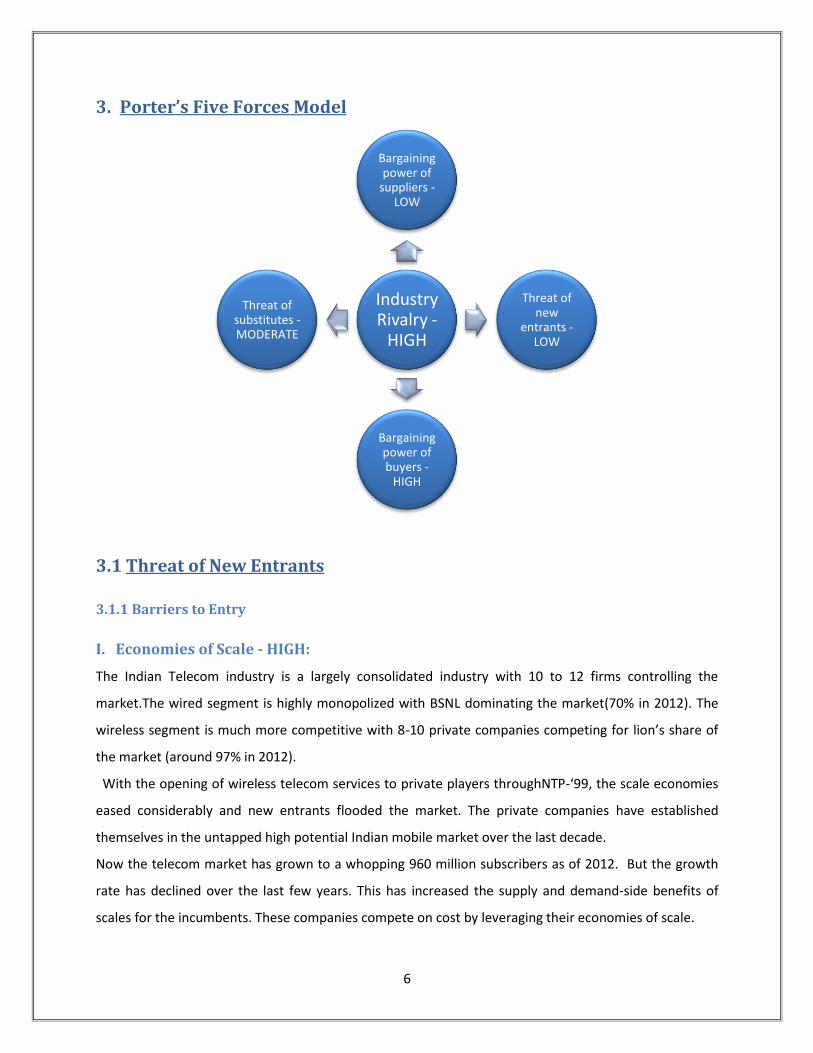

3. Porter’s Five Forces Model

3.1 Threat of New Entrants

3.1.1 Barriers to Entry

I. Economies of Scale - HIGH:

The Indian Telecom industry is a largely consolidated industry with 10 to 12 firms controlling the

market.The wired segment is highly monopolized with BSNL dominating the market(70% in 2012). The

wireless segment is much more competitive with 8-10 private companies competing for lion’s share of

the market (around 97% in 2012).

With the opening of wireless telecom services to private players throughNTP-‘99, the scale economies

eased considerably and new entrants flooded the market. The private companies have established

themselves in the untapped high potential Indian mobile market over the last decade.

Now the telecom market has grown to a whopping 960 million subscribers as of 2012. But the growth

rate has declined over the last few years. This has increased the supply and demand-side benefits of

scales for the incumbents. These companies compete on cost by leveraging their economies of scale.

Industry Rivalry -

HIGH

Bargaining power of

suppliers -LOW

Threat of new

entrants - LOW

Bargaining power of buyers -

HIGH

Threat of substitutes - MODERATE

Page 7

7

The low initial returns, nation-wide coverage by well-established players, declining Average Revenue per

User (ARPU- average 65% decline in last 5 years) and declining tariff rates(97% decline from 1999-2012)

are some of the scale economies that discourage new entrants.However the scale economies are more

influential in the wired segment than in the wireless segment because of the monopolistic power

exercised by the government-run BSNL.

So, in general, new entrants face unfavorable economies of scale.

II. Differentiation - LOW:

All the telecom service operators today provide the same basic services like voice, SMS and internet

capabilities. As such, the industry is largely driven by cost-competition. Attractive cost packages, high

quality and reliability of service and high accessibility differentiates the companies in the minds of the

customer. Hence there is no product differentiation in terms of the variety of features offered.

Low differentiation, in turn, leads to increased rivalry and lowers profitability and attractiveness of the

industry as a whole.

III. Brand Identity - MEDIUM:

Indian telecom sector is dominated by well-established companies with high brand image like Airtel

Idea, Vodafone etc. Brand image in telecom is built by reliability, accessibility and quality of service. A

new entrant would have to incur high infrastructure and advertising costs along with low pricing to build

a brand image. Also the incumbents can retaliate by further price cuts, providing availability of services

in new areas etc. However in the last 5 years, new entrants like Uninor and Tata Docomo have managed

to gain a substantial customer base through aggressive marketing and innovative pricing strategies.

So the incumbents exercise a moderate amount of power through their ‘Brand Pull’.

IV. Switching Cost - LOW:

The switching costs are relatively low in the telecom sector. Typically, the setup costs for wired services

are more than wireless sector because of the labor and material involved. Now, the Mobile number

portability facility for mobile users has reduced the switching costs to practically zero.

Thus overall switching cost is low.

Page 8

8

V. Access to Distribution Channel - HIGH:

India is a geographically diverse country that makes distribution a critical function. Since the market is

now huge (tele-density is 73.3% as of 2012), the incumbents have a huge advantage having already

setup their distribution channels all over the country. Since the distributors are small-time retailers and

distributors, they do not have much bargaining power and are more than satisfied to work with well-

established incumbents. So the costs for a new entrant to find new distribution channels are very high.

VI. Capital Requirement - HIGH:

A new entrant has to consider the following while entering the telecom sector

Extremely high infrastructure costs like communication equipment ,mobile towers

Spectrum License fee.

Cost of acquiring distribution channels

Marketing costs

So the incumbents have a huge cost advantage.

VII. Access to Technology – SLIGHTLY HIGH:

Technology is much more of a factor in the cellular segment than the wired segment. With rapidly

evolving cellular technologies like 3G and 4G, The incumbent firms can adapt more easily to the

changing technologies at a lower cost, since they already have the basic infrastructure in place. However

this is not a huge advantage as access to technology is readily available.

VIII. Access to Raw Materials – MODERATE:

In wired telecom sector, there is no advantage for the incumbents over new players as the access to

raw materials are easily available. SIM cards and Spectrum bandwidth are only raw materials in the

wireless sector. SIM cards are obtained from local manufacturers and are easily available at the same

cost. So access to raw materials is not a factor.

IX. Government Protection - HIGH:

Spectrum availability is a constraint for wireless sector. Spectrum allocations are done through auctions

by the government. Issues of interoperability with changing bandwidth, seamless integration of various

services and lobbying by powerful incumbents are major issues. Thus, spectrum availability poses a huge

barrier to entry, increasing the industry attractiveness.

The entry barriers are HIGH for entry into the Indian telecom industry.

Page 9

9

3.2 Industry Rivalry

There is intense rivalry in the industry due to emergence of new firms leading to price cuts. The

competition has become cut-throat. Due to almost equal size of rivals and nearly same customer base,

there is intense competition to attract customer with lower tariffs and more exciting services which

tends to drive industry profitability down. Apart from low profits, there are high exit barriers and high

fixed costs which are explained below:

I. Number of Competitors: High

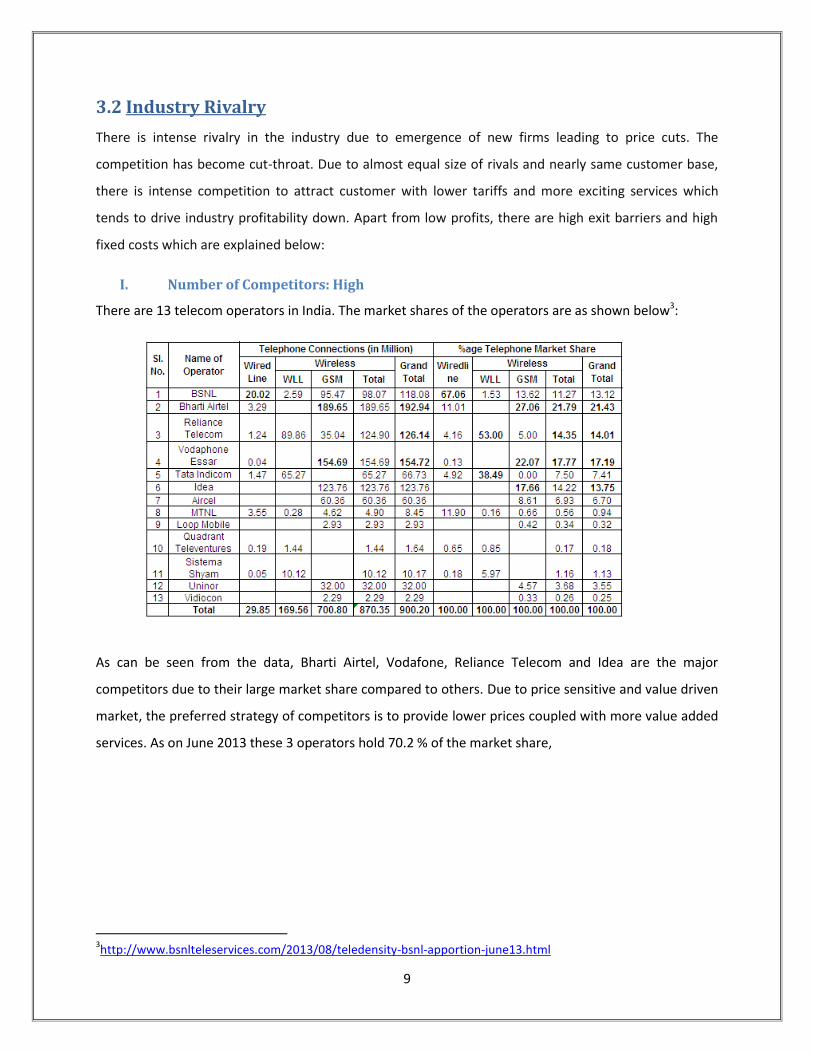

There are 13 telecom operators in India. The market shares of the operators are as shown below3:

As can be seen from the data, Bharti Airtel, Vodafone, Reliance Telecom and Idea are the major

competitors due to their large market share compared to others. Due to price sensitive and value driven

market, the preferred strategy of competitors is to provide lower prices coupled with more value added

services. As on June 2013 these 3 operators hold 70.2 % of the market share,

3http://www.bsnlteleservices.com/2013/08/teledensity-bsnl-apportion-june13.html

Page 10

10

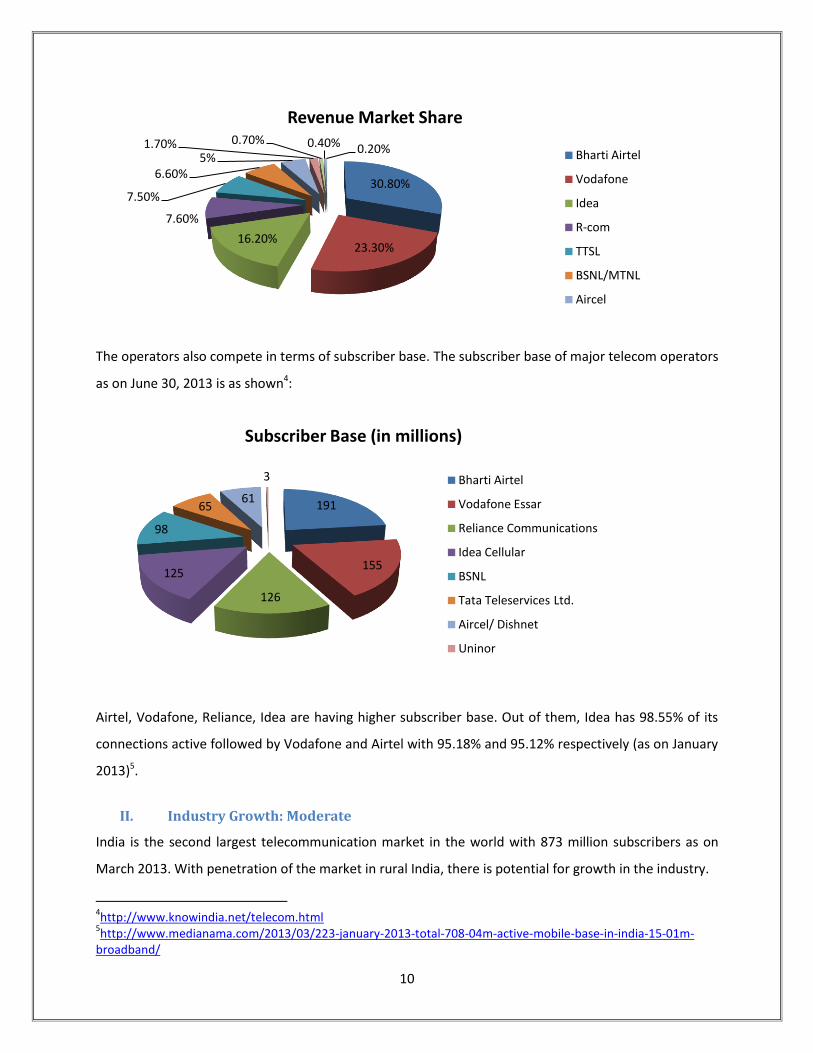

The operators also compete in terms of subscriber base. The subscriber base of major telecom operators

as on June 30, 2013 is as shown4:

Airtel, Vodafone, Reliance, Idea are having higher subscriber base. Out of them, Idea has 98.55% of its

connections active followed by Vodafone and Airtel with 95.18% and 95.12% respectively (as on January

2013)5.

II. Industry Growth: Moderate

India is the second largest telecommunication market in the world with 873 million subscribers as on

March 2013. With penetration of the market in rural India, there is potential for growth in the industry.

4http://www.knowindia.net/telecom.html

5http://www.medianama.com/2013/03/223-january-2013-total-708-04m-active-mobile-base-in-india-15-01m-

broadband/

30.80%

23.30% 16.20%

7.60%

7.50%

6.60% 5%

1.70% 0.70% 0.40% 0.20%

Revenue Market Share

Bharti Airtel

Vodafone

Idea

R-com

TTSL

BSNL/MTNL

Aircel

191

155

126

125

98

65 61

3

Subscriber Base (in millions)

Bharti Airtel

Vodafone Essar

Reliance Communications

Idea Cellular

BSNL

Tata Teleservices Ltd.

Aircel/ Dishnet

Uninor

Page 11

11

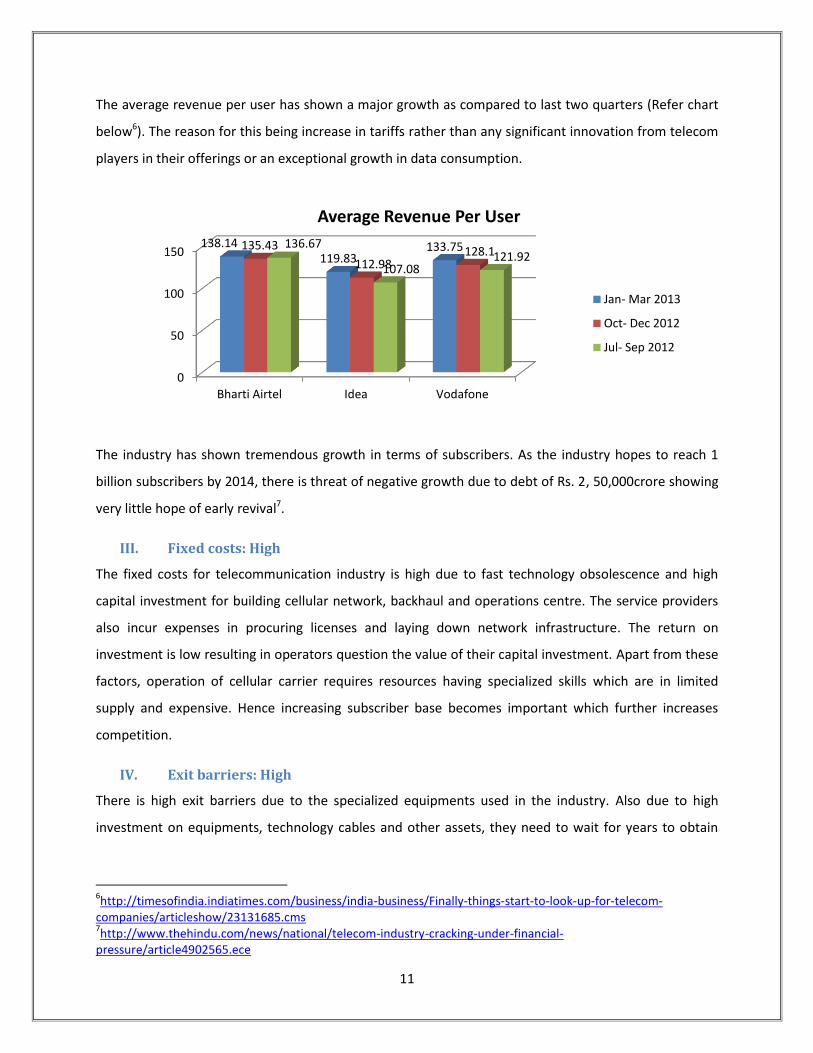

The average revenue per user has shown a major growth as compared to last two quarters (Refer chart

below6). The reason for this being increase in tariffs rather than any significant innovation from telecom

players in their offerings or an exceptional growth in data consumption.

The industry has shown tremendous growth in terms of subscribers. As the industry hopes to reach 1

billion subscribers by 2014, there is threat of negative growth due to debt of Rs. 2, 50,000crore showing

very little hope of early revival7.

III. Fixed costs: High

The fixed costs for telecommunication industry is high due to fast technology obsolescence and high

capital investment for building cellular network, backhaul and operations centre. The service providers

also incur expenses in procuring licenses and laying down network infrastructure. The return on

investment is low resulting in operators question the value of their capital investment. Apart from these

factors, operation of cellular carrier requires resources having specialized skills which are in limited

supply and expensive. Hence increasing subscriber base becomes important which further increases

competition.

IV. Exit barriers: High

There is high exit barriers due to the specialized equipments used in the industry. Also due to high

investment on equipments, technology cables and other assets, they need to wait for years to obtain

6http://timesofindia.indiatimes.com/business/india-business/Finally-things-start-to-look-up-for-telecom-

companies/articleshow/23131685.cms 7http://www.thehindu.com/news/national/telecom-industry-cracking-under-financial-

pressure/article4902565.ece

0

50

100

150

Bharti Airtel Idea Vodafone

138.14 119.83

133.75 135.43

112.98 128.1

136.67

107.08 121.92

Average Revenue Per User

Jan- Mar 2013

Oct- Dec 2012

Jul- Sep 2012

Page 12

12

return on investment. Thus due to sunk costs and no exit regulations in India, there is increase in

competition.

V. Switching Costs, Product Differentiation: Low

As the number of operators is large, there are low switching costs resulting in higher rivalry. There is no

differentiation among the service providers with innovations also easily imitable hence there is minimal

customer loyalty making industry rivalry more significant.

Thus overall there is HIGH rivalry in the industry.

3.3 Bargaining Power of the Suppliers

Suppliers for Telecos are

Telecom infrastructure providers (e.g. tower industry)

Telecom equipment manufacturers (e.g. network routers, transmission lines)

Government which allocates spectrum

Bargaining power of suppliers arises from the fact that telecos compete for equipment, labour and

spectrum in input markets. In both output and input markets transactions create value, and the extent

of profitability division decides their relative economic power.

I. Number of suppliers

The list of infrastructure and equipment providers is provided in the Appendix.

Cellular tower industry can been divided into two segments; one independent of telecom service

providers and the other segment is of the telecom service provider itself. Equipment manufacturing

industry has few significant players.

II. Availability of substitutes

As seen from the table of suppliers, telecom firms have substitutes in terms of different companies

offering the same service. Hence, telecos have an option to switch. In terms of substitutes to technology

related to towers and telecom equipment, as of now there are no substitutes.

III. Switching costs: Low

There are quite a few network providers & equipment manufacturers. Also, input markets have been

commoditized over time. Hence, switching costs are low.

Page 13

13

IV. Supplier’s threat of forward integration: Moderate

Suppliers can forward integrate given that they have access to infrastructure and logistics, but

establishing brand identity will be a challenge. Hence there is intermediate supplier’s threat of forward

integration.

V. Industry’s threat of backward integration: High

Large telecos can buy out network providers and backward integrate. This has happened in the case of

cellular towers where big players acquired major stake in existing suppliers. They have also shared their

resources in input markets to decrease costs.

VI. Industry’s importance to supplier: High

Suppliers form the core of telecommunication industry. Without cellular towers, transmission lines,

switches, modems, routers and spectrum (allocated government) service providers cannot carry out

their functions. Hence industry thrives on suppliers’ products and service.

3.4 Bargaining Power of the Buyers As of May 2012, the total number of telecom subscribers in India is 960 million with a growth rate of

0.84% per month. Buyers, in the telecommunication industry can be classified as8:

1. Residential or Individual Customers

2. Enterprise or Business Customers

Residential Customers refer to individual subscribers, whereas Enterprise Customers are the large

business firms like any IT firm or a bank et al.

3.4.1 Analyzing Customer Sensitivity:

I. Product Differentiation

The Telecom service providers, Telephone and Data services do not vary much, except for the signal

strength in specific geographical locations. Moreover, the government regulations apply to all the

providers.

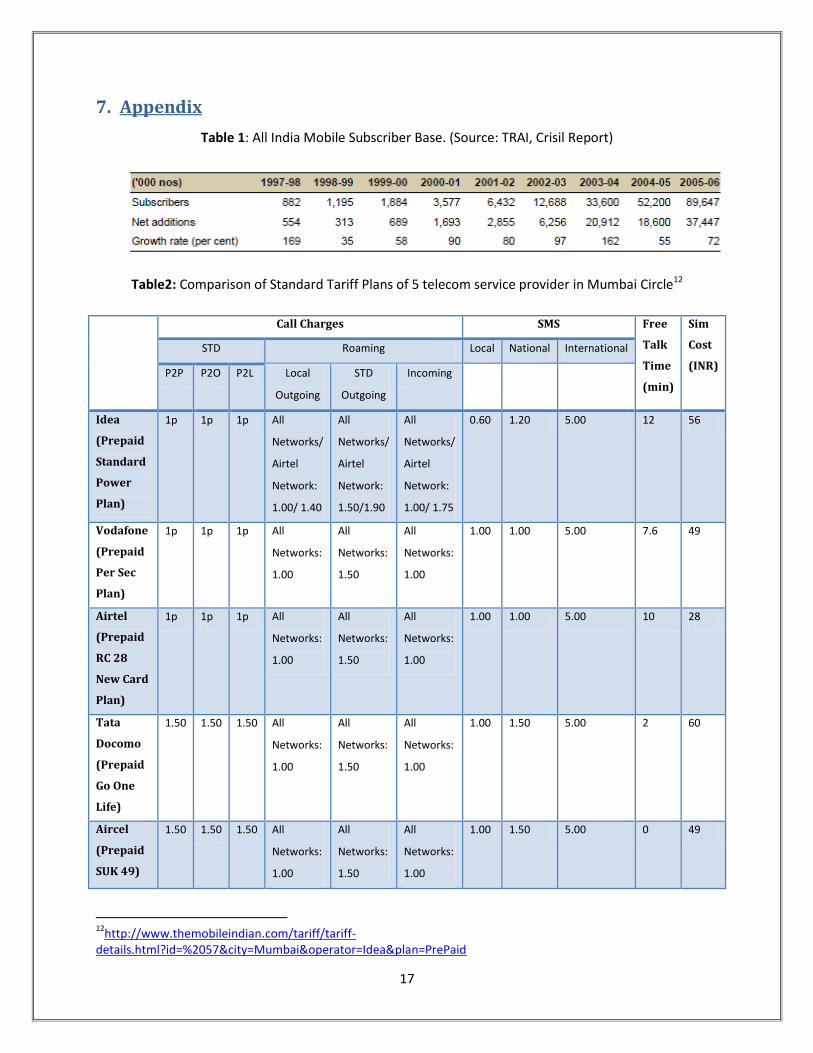

The Tariff table (Table 2 in appendix) compares the tariff plans of various telecom service providers. The

tariff rates are relatively similar. However, the customers can definitely switch over to any other service

provider which provides higher reliability and signal strength in their corresponding geographical area.

8http://www.investopedia.com/features/industryhandbook/telecom.asp

Page 14

14

Since the product differentiation is very minimal, switching costs are low for the residential customers.

The enterprise or business customers, like bank or IT firms requires bulk and customized services. In

their case, bargaining power as well as switching costs goes high.

II. Competition between Buyers

The residential customers don’t have any internal competition. However, the enterprise customer

segment generate, especially banks who render services to telecom operators in return and supplement

a major part of the provider’s revenue, have a upper hand in bargaining on the prices incurred on them.

3.4.2 Analyzing Relative Buying Power:

I. Size and Concentration of Buyers relative to products: MEDIUM

In the first segment, the size is large while the concentration of consumption per individual is relatively

lower. Buyer power is thus low. On the other hand, the enterprise customer segment has large size as

well as large concentration in term of consumption. They exercise a higher buyer power. The overall

buying power is thus medium.

II. Buyers Switching Costs: LOW

As stated in Product Differentiation, the switching costs are low.

The Mobile Number Portability (MNP)9 is convenient and affordable. Due to these reasons, the number

of MNP requests has gone up from 54 million subscribers to 59 million subscribers10 by the end of July

2012. Thus, switching costs are low.

Another indicator of Low Switching Cost is the Churn Rate.

Due to fierce competition, Telecom industry has the highest customer churn rate. This proves that the

high churn rate is due to the ease of switching among the service providers.

Thus the overall switching cost for customers is very low.

III. Buyers information: HIGH

Due to the explosion of social networking and internet advertising these days, the customers are aware

of all the available options. They can compare the tariff plans online and then decide which plan to

9http://www.mnpindia.in/number-portability.aspx

10 www.trai.gov.in

Page 15

15

choose. Blogs and other online dashboards provide various discussion threads wherein every user

shares his/her experience with the service provider. Using these resources, the customer does

background check on many attributes like roaming charges, signal strength, seasonal offers, network

reliability and quality of service before deciding on a particular operator. Hence, high buyer information

corresponds to high buyer power.

IV. Buyers ability to backward integrate: LOW

There are no intermediaries between the service provider and the customer. Hence, the ability to

backward integrate is low. This, in turn corresponds to lower buyer power.

Thus, overall Bargaining Power of the Buyers is HIGH.

3.5 Threat of Substitutes

The threat of substitutes in the telecom industry is moderate. Products and services from non-

traditional telecom industries pose serious substitution threats. Cable TV and satellite operators now

compete for buyers. The cable guys, with their own direct lines into homes, offer broadband internet

services, and satellite links can substitute for high-speed business networking needs. Railways and

energy utility companies are laying miles of high-capacity telecom network alongside their own track

and pipeline assets. Another substitute, the internet is becoming a viable vehicle for cut-rate voice calls.

Delivered by ISPs - "internet telephony" could take a big bite out of telecom companies' core voice

revenues. VoIP Applications like Skype offers video chat and call services over the internet, whereas

apps like Whatsapp offer free messaging services. India is a latecomer to the VoIP revolution. Currently,

Indian laws only allow VoIP calls to a telephone in India under strict conditions. However, they allow

such calls between computers within the country’s borders and between a computer in India and a

telephone (fixed or wireless) outside India.

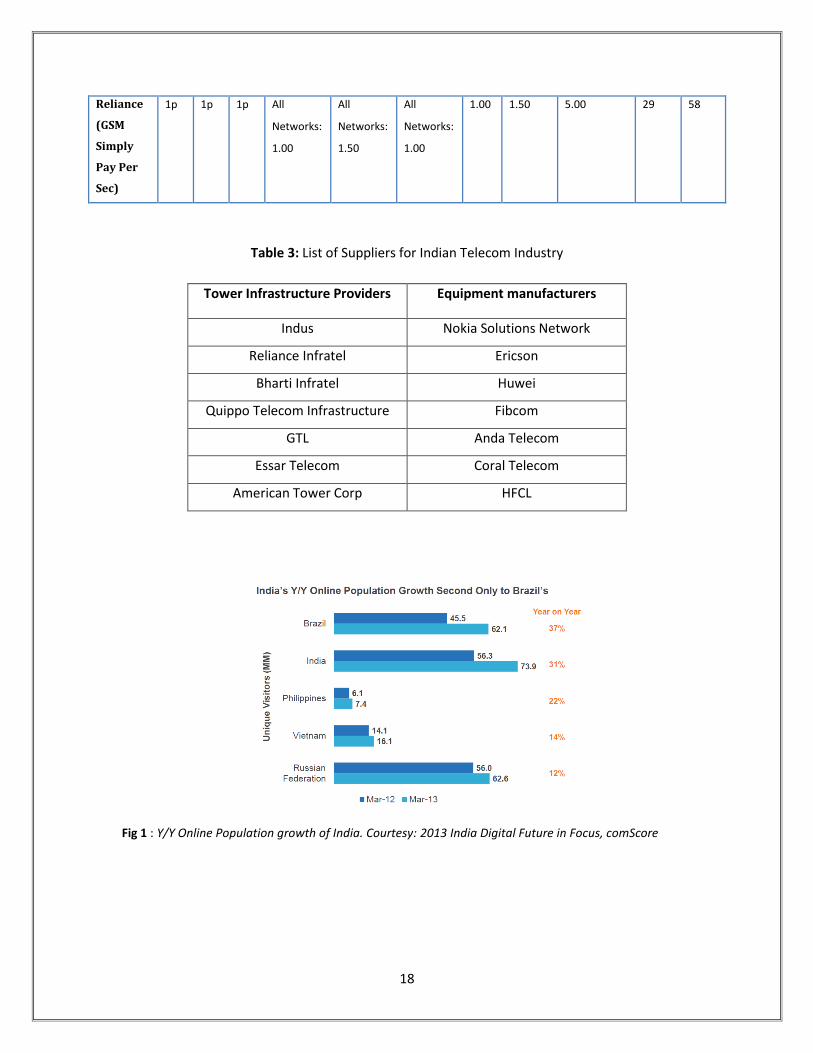

India has now the world’s third largest internet using population11 with nearly 74 million Internet users,

a 31% increase over March 2012. The Telecom Regulatory Authority of India (TRAI) pegged the number

of Internet subscribers in India at 164.81 million as of March 31, 2013, with seven out of eight accessing

the Internet from their mobile phones. This is good news for the mobile phone internet providers as

well as bad news due to the threat of VoIP software.

11

http://www.thehindu.com/sci-tech/technology/internet/india-is-now-worlds-third-largest-internet-user-after-us-china/article5053115.ece

Page 16

16

Therefore the overall Threat of Substitutes is MODERATE.

4. Growth

Revenue from wireless and wireline increased at a CAGR of 11.9 % to $40.8 billion over FY07-12.

Wireless subscriptions had increased at a CAGR of 34 % to 864.7 million over a 6 year period from

2006 to 2012

Mobile telephone density increased more than 5 times from 13.5% in 2006 to 70.9% in 2013

GSM services contribute the most to wireless segment with 88.1% share (June 2012); CDMA takes

the remaining.

Bharti Airtel is the market leader. The top five players – Bharti Airtel, Vodafone, Reliance, Idea, and

BSNL – contribute to about 79% of the total subscribers

5. Future Trends

Expansion to rural markets will be key to future growth

Broadband Wireless Access (BWA) technologies like WiMax have been successful in US and hence

expected to grow in India

Rising investments in telecom sector is a great sign for the industry

Outsourcing of non-core activities is expected to increase even more

6. Summary

The impact of each of the forces indicates that the Indian telecom industry is a moderately attractive

industry. Its strengths are low bargaining powers of suppliers and high barriers to entry. The weakness is

the high bargaining power of suppliers. The attractiveness index of this industry is 3.2(refer appendix)

which is neither too high nor too low.

Page 17

17

7. Appendix

Table 1: All India Mobile Subscriber Base. (Source: TRAI, Crisil Report)

Table2: Comparison of Standard Tariff Plans of 5 telecom service provider in Mumbai Circle12

Call Charges SMS Free

Talk

Time

(min)

Sim

Cost

(INR)

STD Roaming Local National International

P2P P2O P2L Local

Outgoing

STD

Outgoing

Incoming

Idea

(Prepaid

Standard

Power

Plan)

1p 1p 1p All

Networks/

Airtel

Network:

1.00/ 1.40

All

Networks/

Airtel

Network:

1.50/1.90

All

Networks/

Airtel

Network:

1.00/ 1.75

0.60 1.20 5.00 12 56

Vodafone

(Prepaid

Per Sec

Plan)

1p 1p 1p All

Networks:

1.00

All

Networks:

1.50

All

Networks:

1.00

1.00 1.00 5.00 7.6 49

Airtel

(Prepaid

RC 28

New Card

Plan)

1p 1p 1p All

Networks:

1.00

All

Networks:

1.50

All

Networks:

1.00

1.00 1.00 5.00 10 28

Tata

Docomo

(Prepaid

Go One

Life)

1.50 1.50 1.50 All

Networks:

1.00

All

Networks:

1.50

All

Networks:

1.00

1.00 1.50 5.00 2 60

Aircel

(Prepaid

SUK 49)

1.50 1.50 1.50 All

Networks:

1.00

All

Networks:

1.50

All

Networks:

1.00

1.00 1.50 5.00 0 49

12

http://www.themobileindian.com/tariff/tariff-details.html?id=%2057&city=Mumbai&operator=Idea&plan=PrePaid

Page 18

18

Reliance

(GSM

Simply

Pay Per

Sec)

1p 1p 1p All

Networks:

1.00

All

Networks:

1.50

All

Networks:

1.00

1.00 1.50 5.00 29 58

Table 3: List of Suppliers for Indian Telecom Industry

Tower Infrastructure Providers Equipment manufacturers

Indus Nokia Solutions Network

Reliance Infratel Ericson

Bharti Infratel Huwei

Quippo Telecom Infrastructure Fibcom

GTL Anda Telecom

Essar Telecom Coral Telecom

American Tower Corp HFCL

Fig 1 : Y/Y Online Population growth of India. Courtesy: 2013 India Digital Future in Focus, comScore

Page 19

19

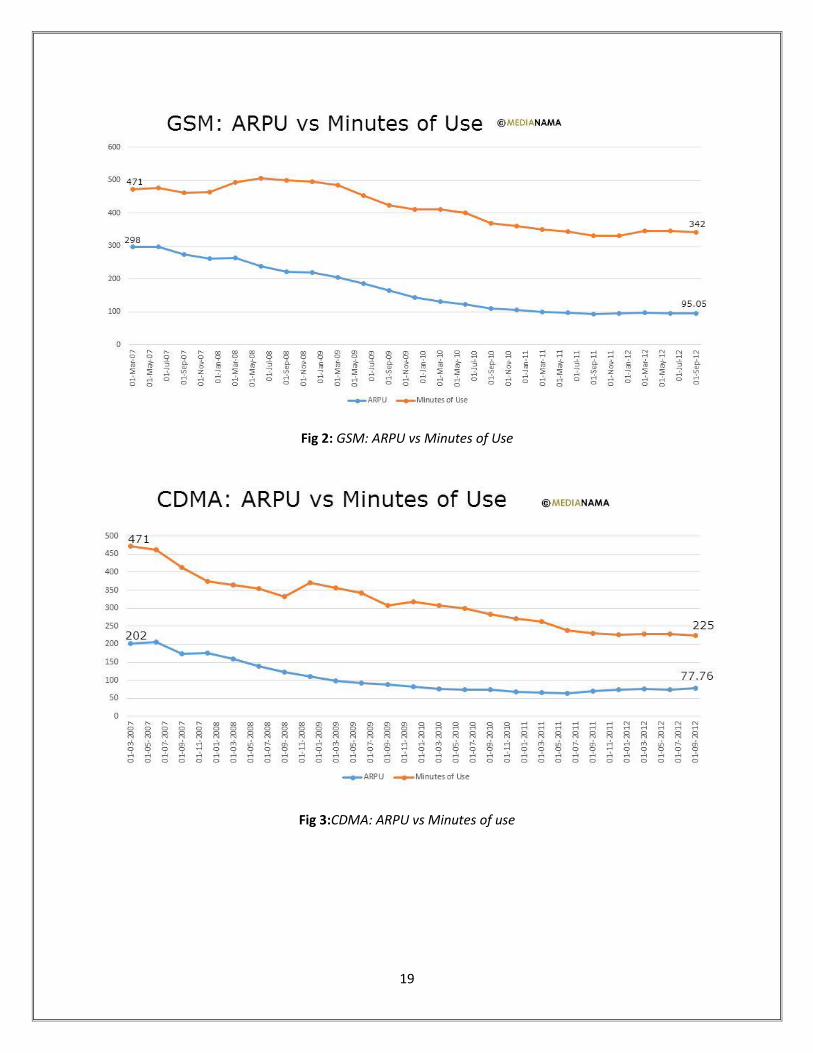

Fig 2: GSM: ARPU vs Minutes of Use

Fig 3:CDMA: ARPU vs Minutes of use

Page 20

20

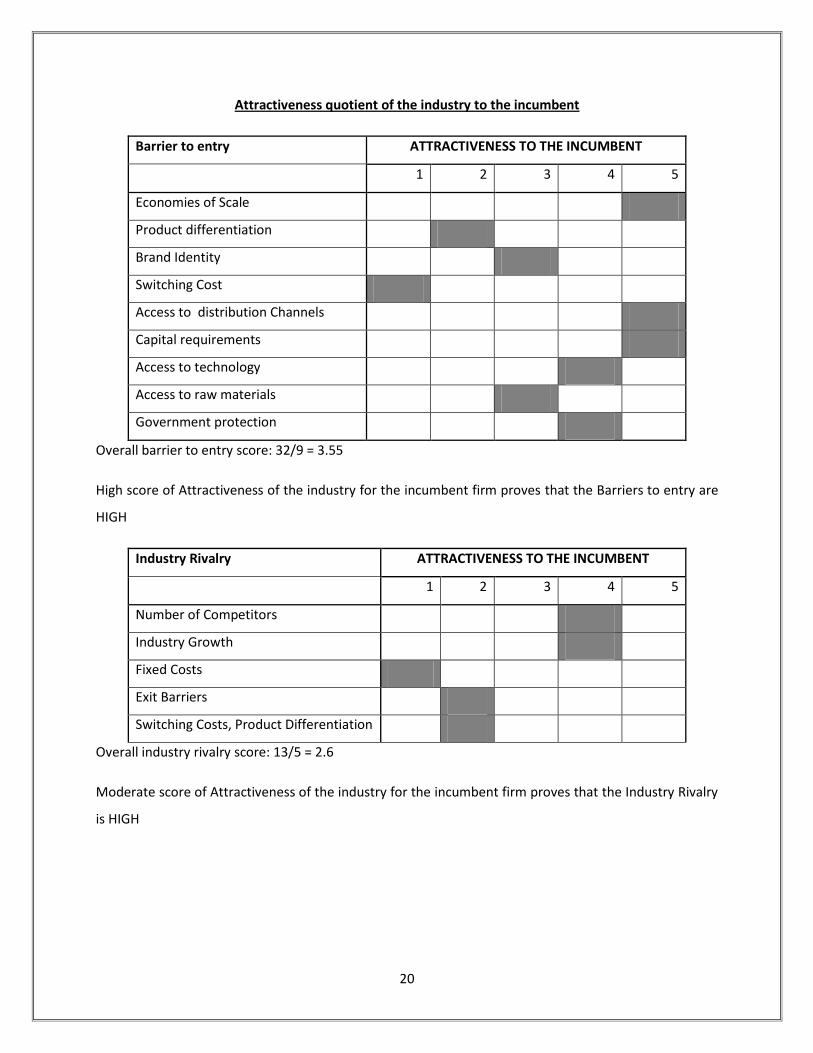

Attractiveness quotient of the industry to the incumbent

Barrier to entry ATTRACTIVENESS TO THE INCUMBENT

1 2 3 4 5

Economies of Scale

Product differentiation

Brand Identity

Switching Cost

Access to distribution Channels

Capital requirements

Access to technology

Access to raw materials

Government protection

Overall barrier to entry score: 32/9 = 3.55

High score of Attractiveness of the industry for the incumbent firm proves that the Barriers to entry are

HIGH

Industry Rivalry ATTRACTIVENESS TO THE INCUMBENT

1 2 3 4 5

Number of Competitors

Industry Growth

Fixed Costs

Exit Barriers

Switching Costs, Product Differentiation

Overall industry rivalry score: 13/5 = 2.6

Moderate score of Attractiveness of the industry for the incumbent firm proves that the Industry Rivalry

is HIGH

Page 21

21

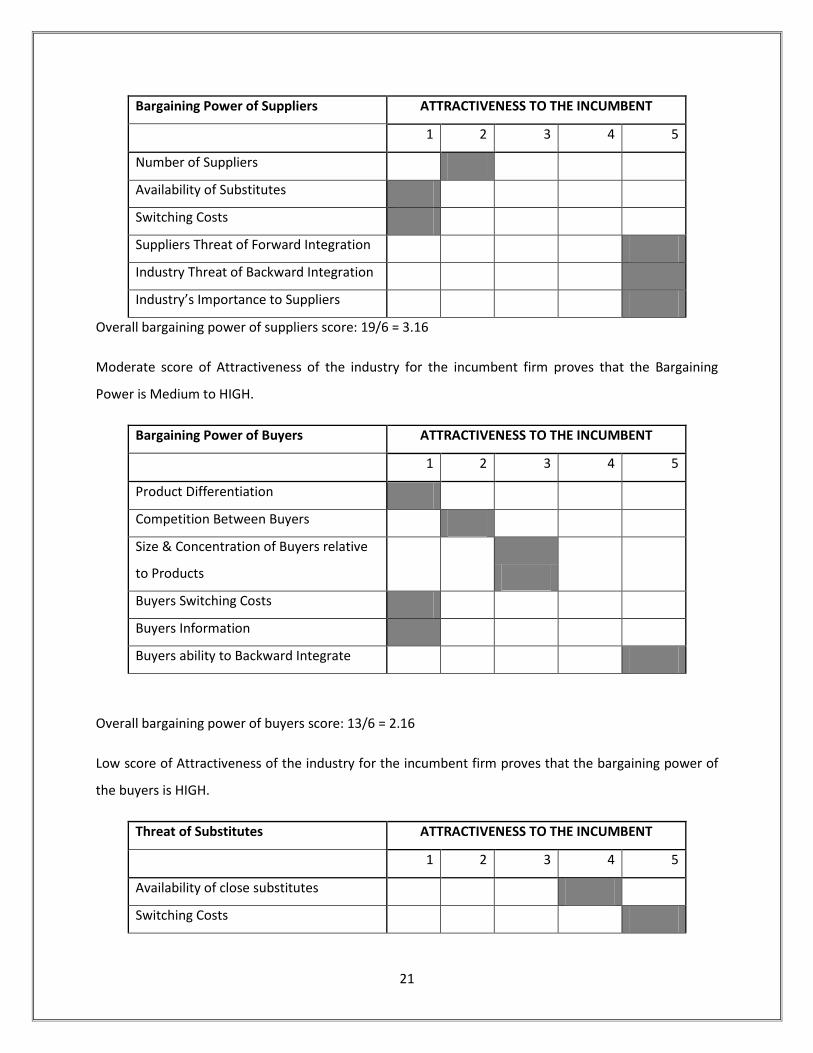

Bargaining Power of Suppliers ATTRACTIVENESS TO THE INCUMBENT

1 2 3 4 5

Number of Suppliers

Availability of Substitutes

Switching Costs

Suppliers Threat of Forward Integration

Industry Threat of Backward Integration

Industry’s Importance to Suppliers

Overall bargaining power of suppliers score: 19/6 = 3.16

Moderate score of Attractiveness of the industry for the incumbent firm proves that the Bargaining

Power is Medium to HIGH.

Bargaining Power of Buyers ATTRACTIVENESS TO THE INCUMBENT

1 2 3 4 5

Product Differentiation

Competition Between Buyers

Size & Concentration of Buyers relative

to Products

Buyers Switching Costs

Buyers Information

Buyers ability to Backward Integrate

Overall bargaining power of buyers score: 13/6 = 2.16

Low score of Attractiveness of the industry for the incumbent firm proves that the bargaining power of

the buyers is HIGH.

Threat of Substitutes ATTRACTIVENESS TO THE INCUMBENT

1 2 3 4 5

Availability of close substitutes

Switching Costs

Page 22

22

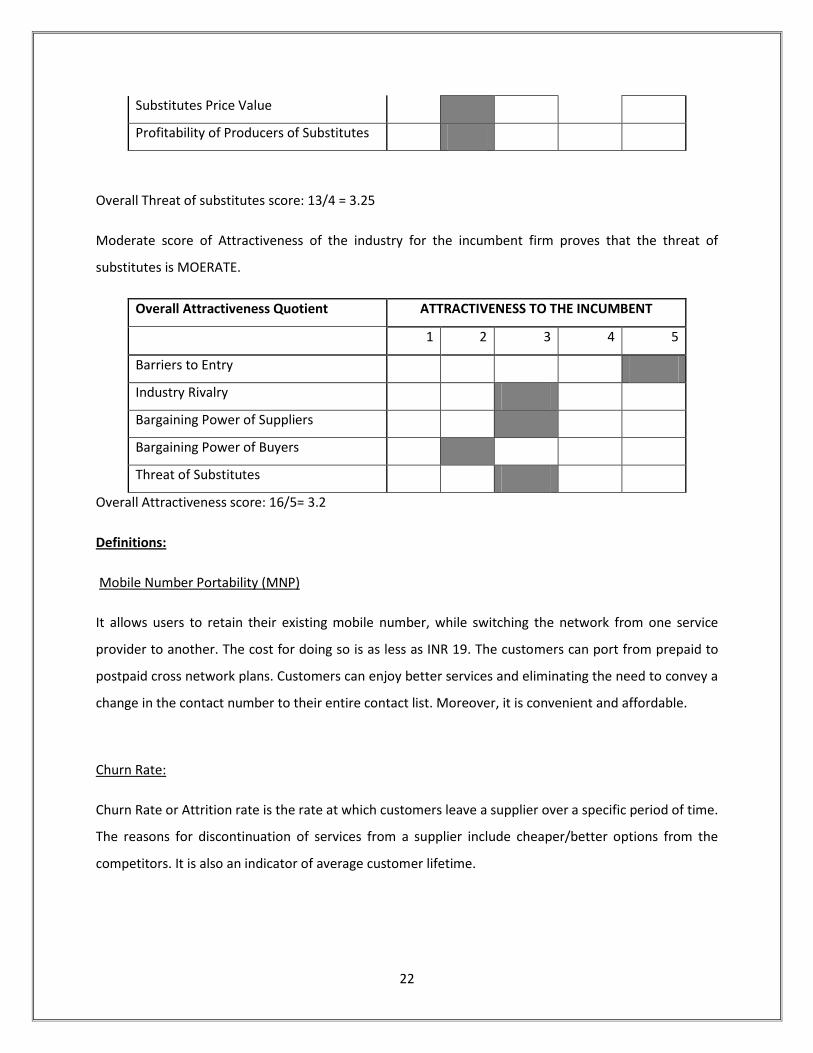

Substitutes Price Value

Profitability of Producers of Substitutes

Overall Threat of substitutes score: 13/4 = 3.25

Moderate score of Attractiveness of the industry for the incumbent firm proves that the threat of

substitutes is MOERATE.

Overall Attractiveness Quotient ATTRACTIVENESS TO THE INCUMBENT

1 2 3 4 5

Barriers to Entry

Industry Rivalry

Bargaining Power of Suppliers

Bargaining Power of Buyers

Threat of Substitutes

Overall Attractiveness score: 16/5= 3.2

Definitions:

Mobile Number Portability (MNP)

It allows users to retain their existing mobile number, while switching the network from one service

provider to another. The cost for doing so is as less as INR 19. The customers can port from prepaid to

postpaid cross network plans. Customers can enjoy better services and eliminating the need to convey a

change in the contact number to their entire contact list. Moreover, it is convenient and affordable.

Churn Rate:

Churn Rate or Attrition rate is the rate at which customers leave a supplier over a specific period of time.

The reasons for discontinuation of services from a supplier include cheaper/better options from the

competitors. It is also an indicator of average customer lifetime.

Page 23

23

8. References http://www.dnb.co.in/IndianTelecomIndustry/OverviewTI.asp

http://www.slideshare.net/zinnov/indian-telecom-market-overview

http://research.ijcaonline.org/ncaete/number3/mpginmc1098.pdf

http://www.livemint.com/Industry/9JEh45TZDJ1HU1xae9YRTJ/What-lies-ahead-for-Indias-telecom-

industry.html

http://www.comviva.com/media/BEsectortelecom.pdf

http://www.equitymaster.com/research-it/sector-info/telecom/Telecom-Sector-Analysis-Report.asp

http://www.ibef.org/download/telecommunication-august-2013.pdf

http://www.ideasmakemarket.com/2013/08/aug-entry6-analysis-of-indian.html

http://www.medianama.com/2013/04/223-india-mobile-arpu-minutes-cdma-gsm-2/