51

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | roberta-hutchinson |

| View: | 219 times |

| Download: | 0 times |

© 2001 Openwave Systems Inc.

MARKET SCENARIOS

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Base Market Model Case

Probable Storm Perfect Storm <$400M

Probable Wave Perfect Wave >$800M

© 2001 Openwave Systems Inc.

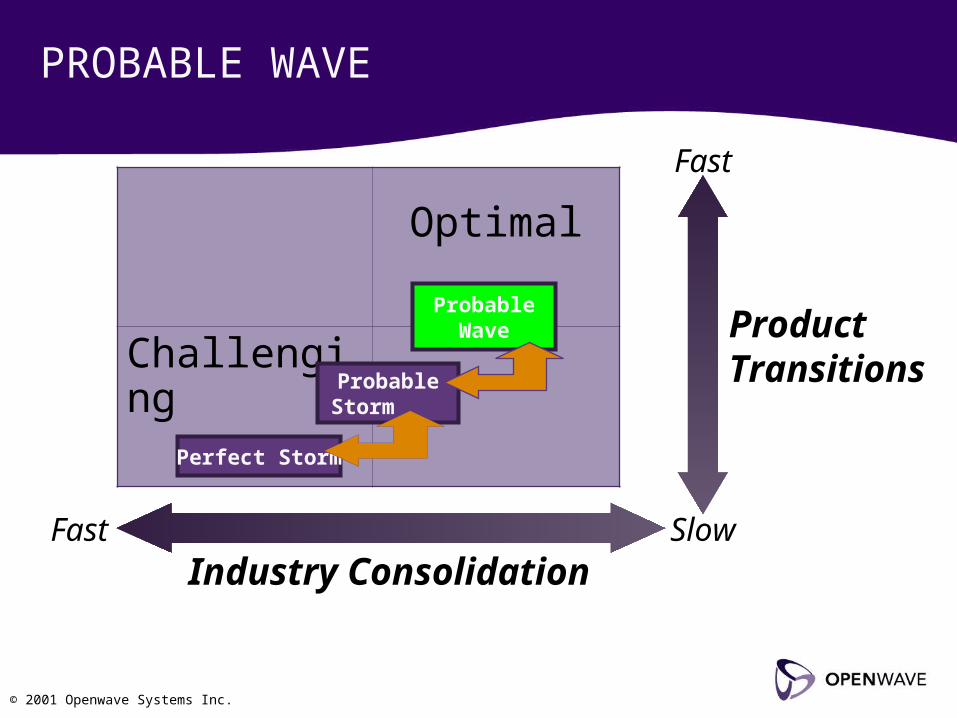

PROBABLE WAVE

Optimal

Challenging

Slow

Fast

ProductTransitions

FastIndustry Consolidation

Perfect Storm

ProbableStorm

ProbableWave

© 2001 Openwave Systems Inc.

PROBABLE STORM

Optimal

Challenging

Slow

Fast

ProductTransitions

FastIndustry Consolidation

Assumes: Market Share Constant / ASP Constant

Perfect Storm

Scenario 1

Probable Wave

ProbableStorm

© 2001 Openwave Systems Inc.

OPENWAVE MISSION

Deliver the Services OS™ software

platform that enables

communication service providers

to rapidly create profitable

Internet-based services.

© 2001 Openwave Systems Inc.

ANNUAL REVENUE GROWTH

$0

$100

$200

$300

$400

$500

1997 1998 1999 2000 2001

Mill

ion

s

© 2001 Openwave Systems Inc.

ANNUAL REVENUE GROWTH

$0

$100

$200

$300

$400

$500

1997 1998 1999 2000 2001

Mill

ion

s

85% GM

25¢/share

85% GM

25¢/share

© 2001 Openwave Systems Inc.

GEOGRAPHIC REVENUE DIVERSITY

June, 2001 September, 2001

Source: Openwave

Americas

EMEA

Japan andAsia-Pacific

ROW

38% 35%

27%

Americas

EMEA

Japan andAsia-Pacific

ROW

30% 35%

35%

© 2001 Openwave Systems Inc.

SUBSCRIBER GROWTH

1,000M+

189M

125M

906M

25.7M

420M

Mobile Internet Messaging

Active Subscribers

Subs Served by Our Customers

Worldwide Subscribers

Sources: Messaging Online (Year End 2000 Report), Radacati, EMC, CSFB, Operator Press Releases, Openwave Estimates, Morgan Stanley Dean Witter PC Industry Overview March 2001

# Seats Activated

# PCs

# Seats Licensed# Subscribers Licensed40M

+4.1M +5.9M

© 2001 Openwave Systems Inc.

COMPANY FACTS

2,000+Employees

© 2001 Openwave Systems Inc.

FINANCIAL PERFORMANCE

$117

$144.7$130.0

$109.7

Dec Mar Jun Sep

2001 2002

© 2001 Openwave Systems Inc.

FINANCIAL PERFORMANCE

$XXX $YYY

$144.7$130.0

$109.7

Dec Mar Jun Sep Dec

2001

85% GM

(4.6)% Profit Ops

(0.03)¢

85% GM

(4.6)% Profit Ops

(0.03)¢

2002

© 2001 Openwave Systems Inc.

AGENDA

Industry ModelIndustry Model

Japan’s Success

Global Market

Openwave Technology

© 2001 Openwave Systems Inc.

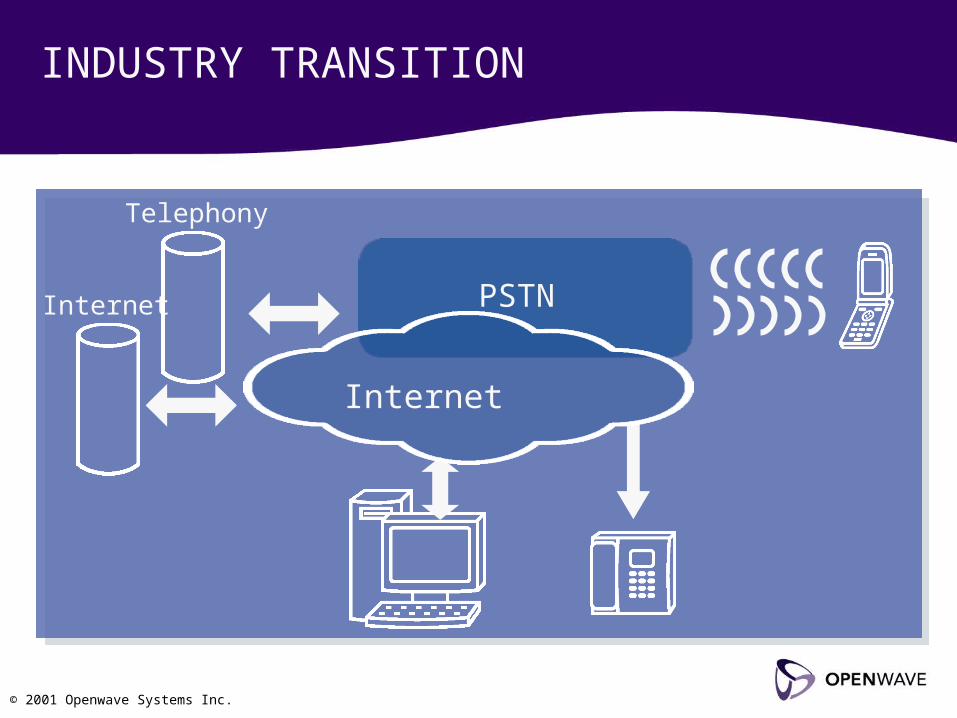

INDUSTRY TRANSITION

Internet

Telephony

PSTN

Internet

© 2001 Openwave Systems Inc.

# of Subscribers

INDUSTRY BUSINESS MODEL

# of Subscribers ProfitabilityNew ServicesVoice

Cost

© 2001 Openwave Systems Inc.

Content

INDUSTRY

ENTERPRISE

SME

SOHO

CONSUMER

Carrier Data Center

Telephony

Internet

Openwave

De

vice

Pro

du

cts

De

velo

per P

rod

ucts

Communication Services

Platform Services

Mobile Services Infrastructure

Customer Service

Ecosystem Partners

© 2001 Openwave Systems Inc.

ContentENTERPRISE

SME

SOHO

CONSUMER

Telephony

Internet

Carrier Data Center

Openwave

INDUSTRY SITUATION

Carrier Data CenterData Back Office

Voice

© 2001 Openwave Systems Inc.

ContentENTERPRISE

SME

SOHO

CONSUMER

Telephony

Internet

Carrier Data Center

Openwave

ENTERPRISE

ENTERPRISE

© 2001 Openwave Systems Inc.

AGENDA

Industry Model

Japan’s SuccessJapan’s Success

Global Market

Openwave Technology

© 2001 Openwave Systems Inc.

MARKET MODEL

ContentENTERPRISE

SME

SOHO

CONSUMER

Carrier Data Center

Telephony

Internet

Openwave

© 2001 Openwave Systems Inc.

0

0

0

0

SUCCESS FACTORS

1Internet

1

© 2001 Openwave Systems Inc.

ContentENTERPRISE

SME

SOHO

CONSUMER

Carrier Data Center

Telephony

Internet

Openwave

INDUSTRY SITUATION

© 2001 Openwave Systems Inc.

INDUSTRY PRIMITIVES AND MARKET MODEL: 12% INCREASE IN HANDSET SALES…

Summary

Total Handset Sales 1999 2000 2001 2002 2003 2004 2005 2006

Analog 0 14,553,708 7,490,937 5,368,588 3,121,895 1,915,078 754,731 440,383

2G

CDMA 0 53,997,112 52,239,189 53,315,311 61,064,964 68,446,559 53,644,559 30,127,607TDMA 0 42,008,987 39,232,331 42,171,544 45,297,200 40,859,986 29,673,696 18,909,950

GSM 0 265,055,824 272,589,870 270,655,591 296,522,525 302,705,668 252,800,052 205,573,904PDC 0 27,633,205 24,152,131 22,494,314 24,074,505 23,055,686 20,609,444 14,442,265

2.5GGPRS 0 0 5,481,861 37,998,235 67,679,935 129,950,961 168,612,154 240,027,862

CDMA 1xRTT 0 0 384,307 1,619,178 9,151,907 21,669,048 39,595,176 66,621,499HSCSD 0 0 6,009,276 16,584,902 6,073,003 4,135,375 607,972 391,968

EDGE 0 0 0 1,662,054 3,328,151 7,649,370 9,523,453 13,794,6343G

CDMA 2000 0 0 0 59,040 1,135,026 2,146,069 4,420,467 7,470,454WCDMA 0 0 299,654 6,188,250 13,468,094 38,465,334 74,837,554 147,243,745

Total Digital 0 388,695,128 400,388,619 452,748,420 527,795,311 639,084,054 654,324,527 744,603,887

Total 0 403,248,836 407,879,556 458,117,008 530,917,205 640,999,133 655,079,258 745,044,2710 0 0 0 0 0 0 0

Consistent With Current Analyst Expectations

© 2001 Openwave Systems Inc.

HANDSETS

© 2001 Openwave Systems Inc.

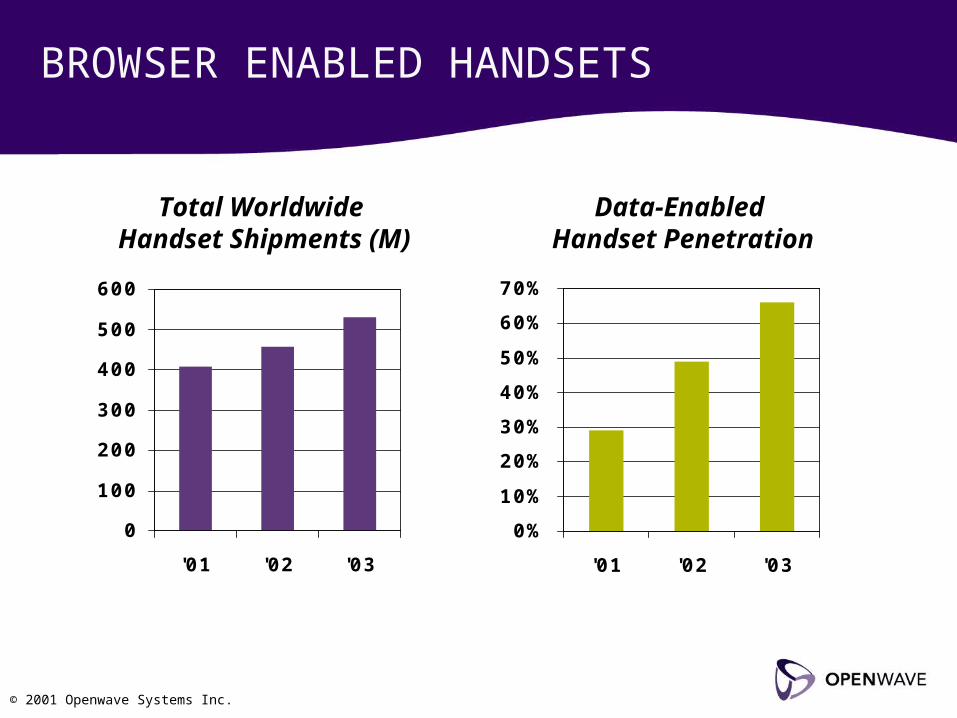

BROWSER ENABLED HANDSETS

0

100

200

300

400

500

600

'01 '02 '03

0%

10%

20%

30%

40%

50%

60%

70%

'01 '02 '03

Total Worldwide Handset Shipments (M)

Data-Enabled Handset Penetration

© 2001 Openwave Systems Inc.

ContentENTERPRISE

SME

SOHO

CONSUMER

Carrier Data Center

Telephony

Internet

Openwave

INDUSTRY SITUATION

Internet

© 2001 Openwave Systems Inc.

2.5G NETWORKS

Source: EMC, Openwave Analysis

69242

1480

52 258

3 25

Total # CSPs with 2.5G Footprint

1xRTT

GPRSIn Service(Commercial)

139 CSPs 605M Subs100%

GPRS

1xRTT

In Deployment(In Process ofRolling Out)

© 2001 Openwave Systems Inc.

ContentENTERPRISE

SME

SOHO

CONSUMER

Carrier Data Center

Telephony

Internet

Openwave

INDUSTRY SITUATION

New Services

$15/month

$30/month

© 2001 Openwave Systems Inc.

“Moore’s Law”

2-way and Global

Network

Secure and Private

Accessible

COMMUNITY STRUCTURE

© 2001 Openwave Systems Inc.

AGENDA

Industry Model

Japan’s Success

Global MarketGlobal Market

Openwave Technology

© 2001 Openwave Systems Inc.

INDUSTRY STANDARDS

Optical Standards

SecurityStandards

PresentationStandards

IP StandardsMessagingStandards

IP StandardsMessagingStandards

PresentationStandards

SecurityStandards

Optical Standards

Transport Communication Entertainment Commerce Imaging

© 2001 Openwave Systems Inc.

MOBILE INTERNET GROWTH

© 2001 Openwave Systems Inc.

CONTENT

Entertainment

Useful Information

Melodies/Images

Gourmet/Recipes

Shopping/Living

Travel/Traffic/Maps

Credit Card/Securities/Insurance

MobileBanking

News/Weather/

Information

Games/Fortunetelling

© 2001 Openwave Systems Inc.

DEMOGRAPHICS

20-2424%

25-2920%

30-3412%

35-398%

Over 3927%

Under 207%

Unknown2%

© 2001 Openwave Systems Inc.

MARKET SCENARIOS

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Pessimistic Base Case Optimistic

Handset Replacement Cycles

Next Gen. Network Rollout

Availability of Data Enabled Handsets

Rate of Service Adoption Among

2

1

3

4

Base Market Model Case

Probable Storm Perfect Storm <$400M

Probable Wave Perfect Wave >$800M

© 2001 Openwave Systems Inc.

PROBABLE WAVE

Optimal

Challenging

Slow

Fast

ProductTransitions

FastIndustry Consolidation

Perfect Storm

ProbableStorm

ProbableWave

© 2001 Openwave Systems Inc.

PROBABLE STORM

Optimal

Challenging

Slow

Fast

ProductTransitions

FastIndustry Consolidation

Assumes: Market Share Constant / ASP Constant

Perfect Storm

Scenario 1

Probable Wave

ProbableStorm

© 2001 Openwave Systems Inc.

PROBABLE STORM – CY2002

124m 139m 181m 216m 226mMobile Data Subs

Key Drivers Perfect Storm• Replacement rates

fall (US) or stagnate • Significant delays in

NG infrastructure. US falls further behind Europe.

• Failure by vendors to increase number of browser enabled handsets

• Data adoption continues to be slow.

• Nokia stalls M-Services in Europe

Probable Storm• Replacement picks

up as confidence recovers and new models are shipped

• Continued delays in NG rollout. Greatest impact in US

• Data capable hand-sets become more pervasive

• Compelling content continues to be lacking, pushing back adoption by 2 quarters. .

• Europe sees continued use of SMS, causing delays in micro-browser uptake of up to 1 yr

Base Case• Gradual recovery in

handset replacement in all regions ‘02-06.

• Rollout of 2.5G in APAC and Europe in ‘01. US follows ’02. S. America, Asia, Middle East/ Africa ‘03-04

• All 2.5G+ handsets data enabled. Increases in % of new 2G handsets data enabled.

• Among users with data enabled handsets, steady growth in adoption to 60% by 2006 in US, APAC, W.Europe.

• Moderate growth in less developed regions

Probable Wave• Handset replacement

begins to pick up gradually from ‘02

• 2.5G and 3G networks continue present rollout path. 2001 APAC and W.Europe. 2002 US, 2002-3 ROW

• Increase in micro-browser enabled 2G handsets as consumer demand emerges.

• M-Services achieves early success and availability of rich content increases (e.g. Java).

• Data uptake outside Japan accelerates

Perfect Wave• Replacement rates return

to ’99/’00 level. Ongoing growth in Middle East/Africa and C.Asia

• 2.5G rollout accelerates from ’02. Seen in increased share of handset sales.

• Vendors rapidly increase availability of data enabled handsets.

• M-Services takes off in EU. CSPs “get” the concept of ecosystem development. Data uptake accelerates.

• Transition to Japan type penetration rates in Europe, US, Asia

90% C.I.99% C.I.

* Subs defined as at least 1 use per month

CY2001 – 84M

© 2001 Openwave Systems Inc.

COMMUNITY STRUCTURE

Open Community Messaging

© 2001 Openwave Systems Inc.

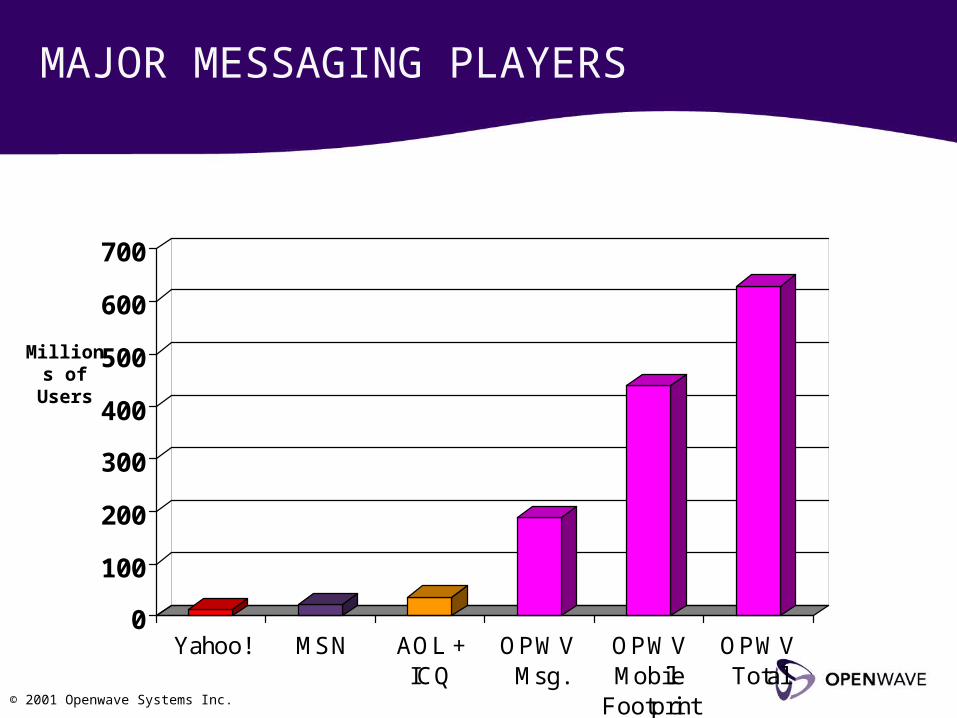

MAJOR MESSAGING PLAYERS

0

100

200

300

400

500

600

700

Yahoo! MSN AOL +ICQ

OPWV Msg.

OPWVMobile

Footprint

OPWVTotal

Millions of Users

© 2001 Openwave Systems Inc.

GLOBAL MARKET GROWTH

United StatesUnited States

DevelopmentDevelopment

EuropeEurope

DeploymentDeployment

Asia-PacificAsia-Pacific

JapanJapan

ExpansionExpansion

© 2001 Openwave Systems Inc.

AGENDA

Industry Model

Japan’s Success

Global Market

Openwave TechnologyOpenwave Technology

© 2001 Openwave Systems Inc.

COMPONENTS

Customer Service

Communication Services

Platform Services

Mobile Services Infrastructure

Mobile Access Gateway /Mobile Services Platform

Dev

ice

Pro

du

cts

Mo

bil

eB

row

se

rD

ev

ice

A

pp

lic

ati

on

s

Develo

per P

rod

ucts

WA

P P

us

h

Lib

rary

SD

K

MobileEmail

UnifiedMessaging

InstantMessaging

MultimediaMessaging

CommerceBroker

SyncManager

Provisioning Manager

DownloadFun

Mobile Messaging Gateway

Ecosystem Partners

Channel Alliances Strategic Alliances Developer AlliancesProduct andTechnology Alliances

Professional Services Customer Support

© 2001 Openwave Systems Inc.

PLATFORM

Mobile Services PlatformClie

nt

Ap

plic

atio

ns Communication Suite

Customer Life Cycle Management

Develo

per

Allian

ces

Strategic Alliances

© 2001 Openwave Systems Inc.

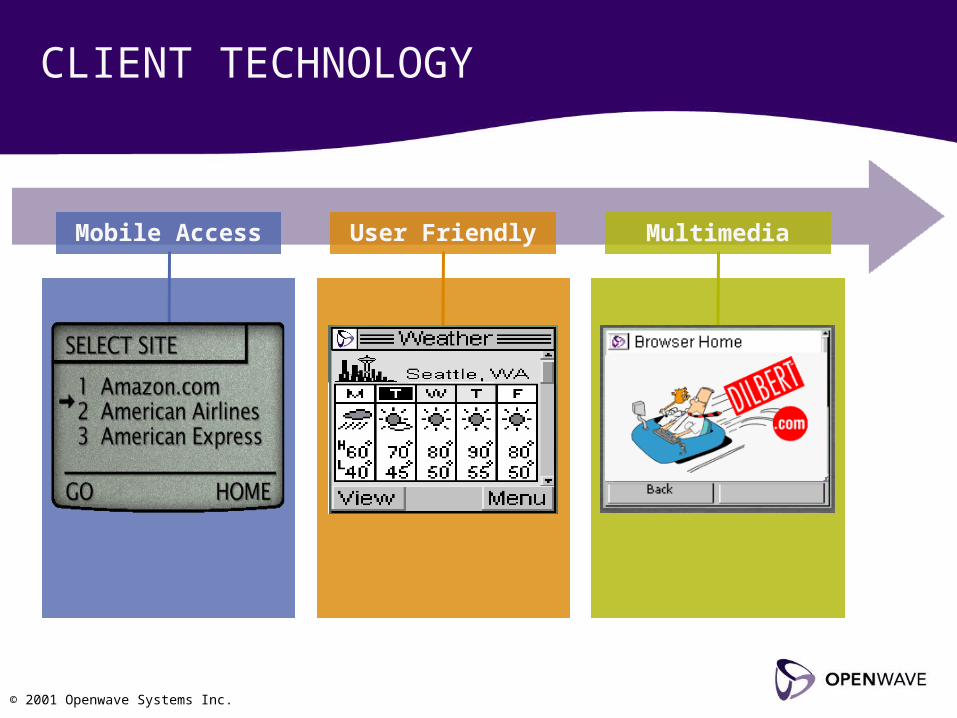

CLIENT TECHNOLOGY

Mobile Access MultimediaUser Friendly

© 2001 Openwave Systems Inc.

UNIFIED MESSAGING

TUI

“You have 3 urgent Voicemail Messages, 6 new Emails…”

Address Book

Notification

Calendar

Messaging

© 2001 Openwave Systems Inc.

INSTANT MESSAGING

WAP Client

SMS Client

DesktopIM Client

Mobile –Embedded Client

© 2001 Openwave Systems Inc.

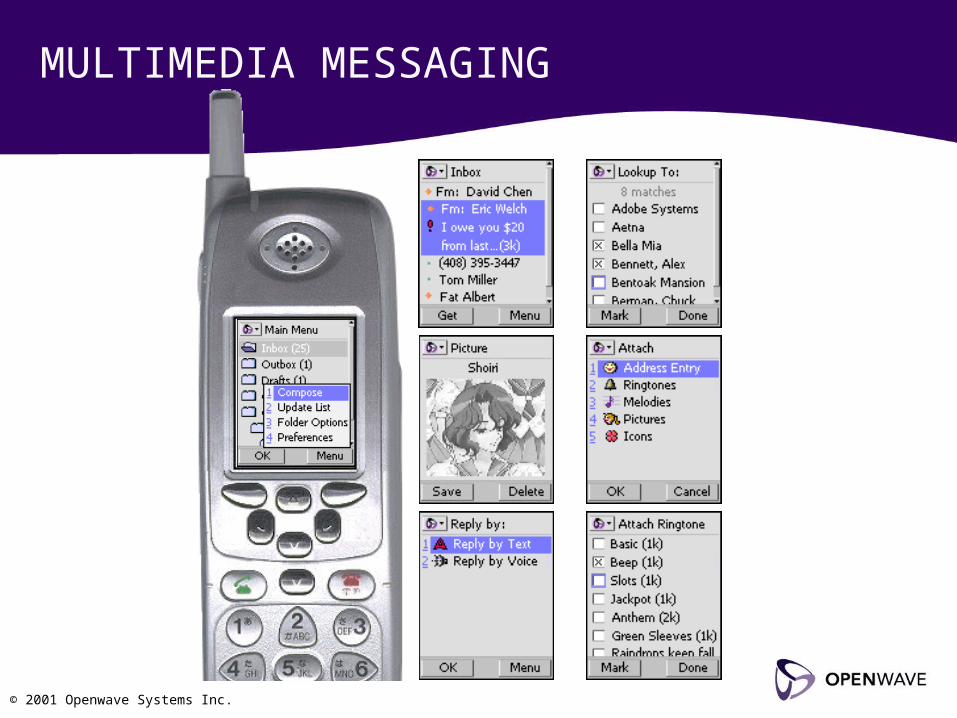

MULTIMEDIA MESSAGING

© 2001 Openwave Systems Inc.

ASIA’S SUCCESS…

© 2001 Openwave Systems Inc.

… COMING TO REST OF WORLD

THANK YOU!