Ten Rules of Wealth Building Ten Rules of Wealth Building All Teachers Should Know All Teachers Should Know Justus Morgan Justus Morgan Financial Planner, CFP Financial Planner, CFP ® , EA , EA Financial Service Group, Financial Service Group, Inc. Inc. Money Smart Week Wisconsin Lambeau Field October 10, 2007 Dr. Norman Cloutier Dr. Norman Cloutier Professor of Economics Professor of Economics Director, UW-Parkside Center for Director, UW-Parkside Center for Economic Education Economic Education

Transcript

Ten Rules of Wealth Building Ten Rules of Wealth Building All Teachers Should KnowAll Teachers Should Know

Justus MorganJustus MorganFinancial Planner, CFPFinancial Planner, CFP®®, EA, EA

Financial Service Group, Inc.Financial Service Group, Inc.

Money Smart Week Wisconsin

Lambeau Field October 10, 2007Dr. Norman CloutierDr. Norman Cloutier

Professor of EconomicsProfessor of EconomicsDirector, UW-Parkside Center for Director, UW-Parkside Center for Economic EducationEconomic Education

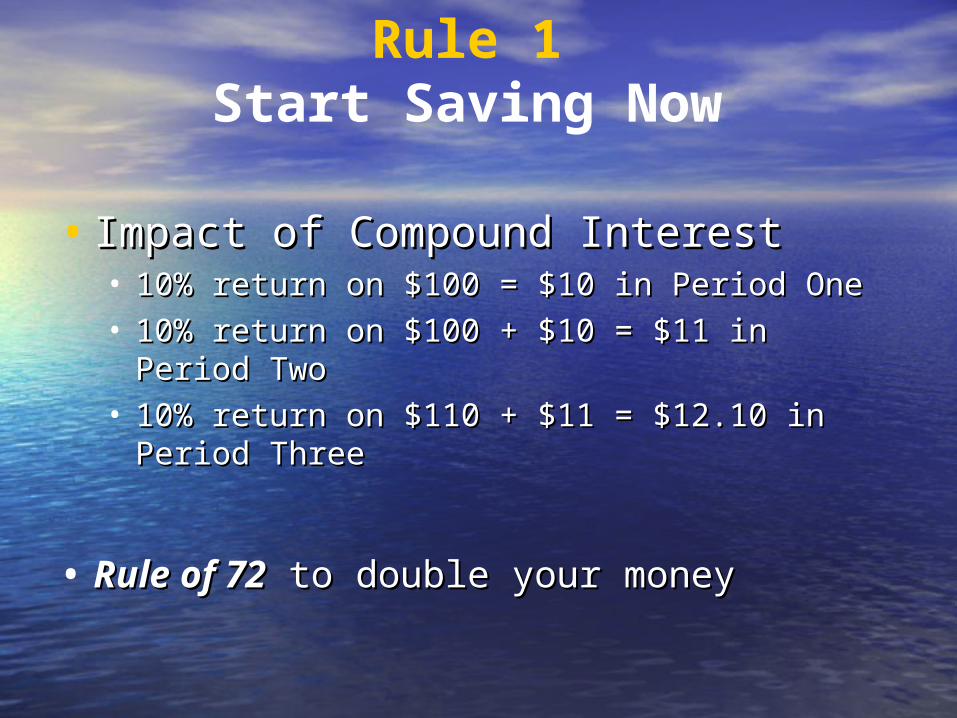

• Impact of Compound InterestImpact of Compound Interest• 10% return on $100 = $10 in Period One10% return on $100 = $10 in Period One• 10% return on $100 + $10 = $11 in Period Two10% return on $100 + $10 = $11 in Period Two• 10% return on $110 + $11 = $12.10 in Period 10% return on $110 + $11 = $12.10 in Period

ThreeThree

• Rule of 72Rule of 72 to double your money to double your money

Rule 1Start Saving Now

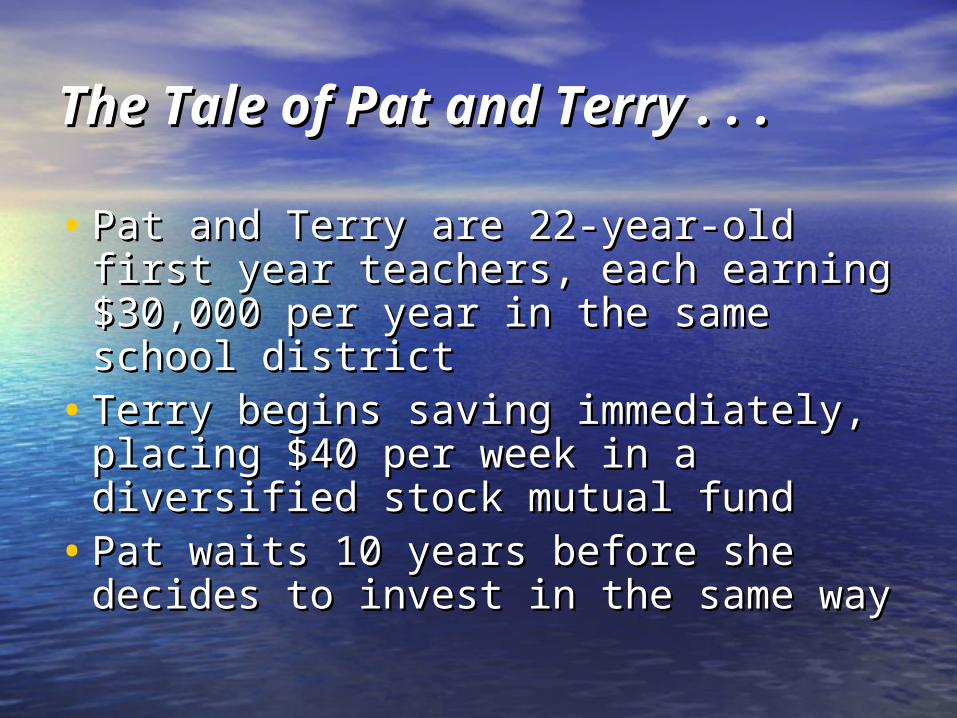

The Tale of Pat and Terry . . The Tale of Pat and Terry . . ..

• Pat and Terry are 22-year-old first Pat and Terry are 22-year-old first year teachers, each earning $30,000 year teachers, each earning $30,000 per year in the same school districtper year in the same school district

• Terry begins saving immediately, Terry begins saving immediately, placing $40 per week in a diversified placing $40 per week in a diversified stock mutual fundstock mutual fund

• Pat waits 10 years before she Pat waits 10 years before she decides to invest in the same waydecides to invest in the same way

Terry’s 1Terry’s 1stst 10 years . . . 10 years . . .

Beginning Addition to EndingYear Balance Principal Return Balance

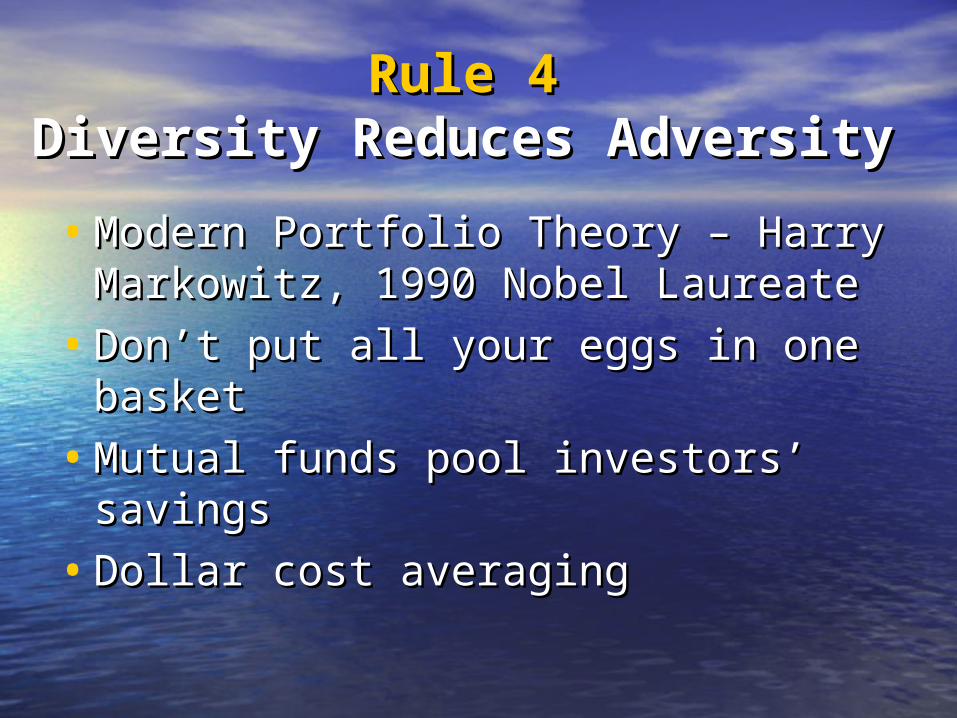

• Modern Portfolio Theory – Harry Modern Portfolio Theory – Harry Markowitz, 1990 Nobel LaureateMarkowitz, 1990 Nobel Laureate

• Don’t put all your eggs in one basketDon’t put all your eggs in one basket

• Mutual funds pool investors’ savings Mutual funds pool investors’ savings

• Dollar cost averagingDollar cost averaging

Learning, Earning and Investing

#7 What Are Mutual Funds? #12 Building Wealth Over the Long TermNational Standards in Economics

Marginal costs and benefitsEconomic institutions Interest rates

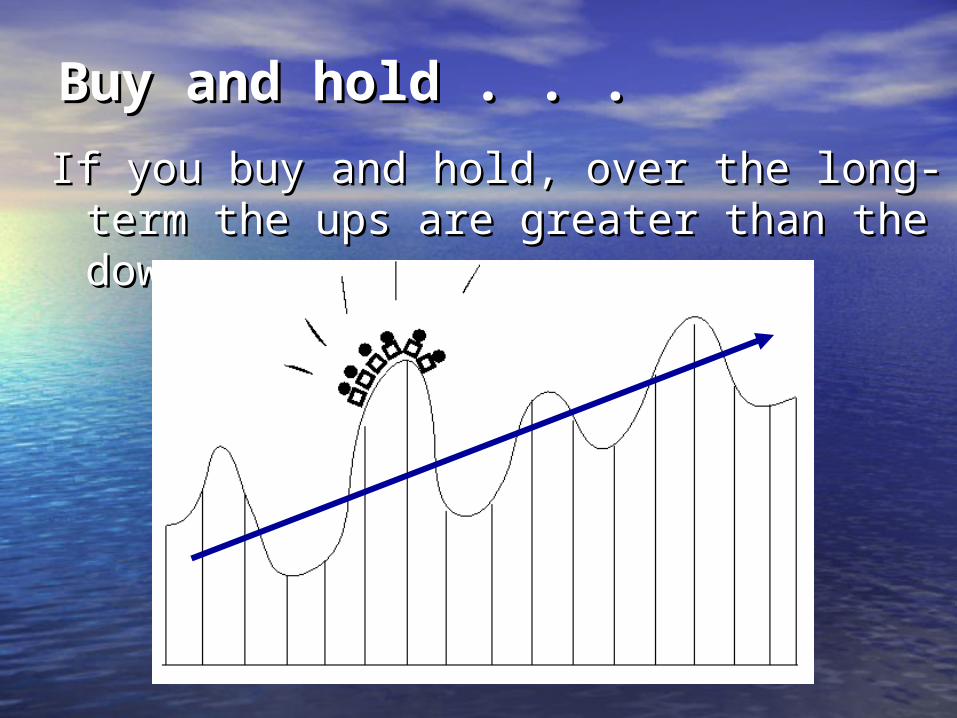

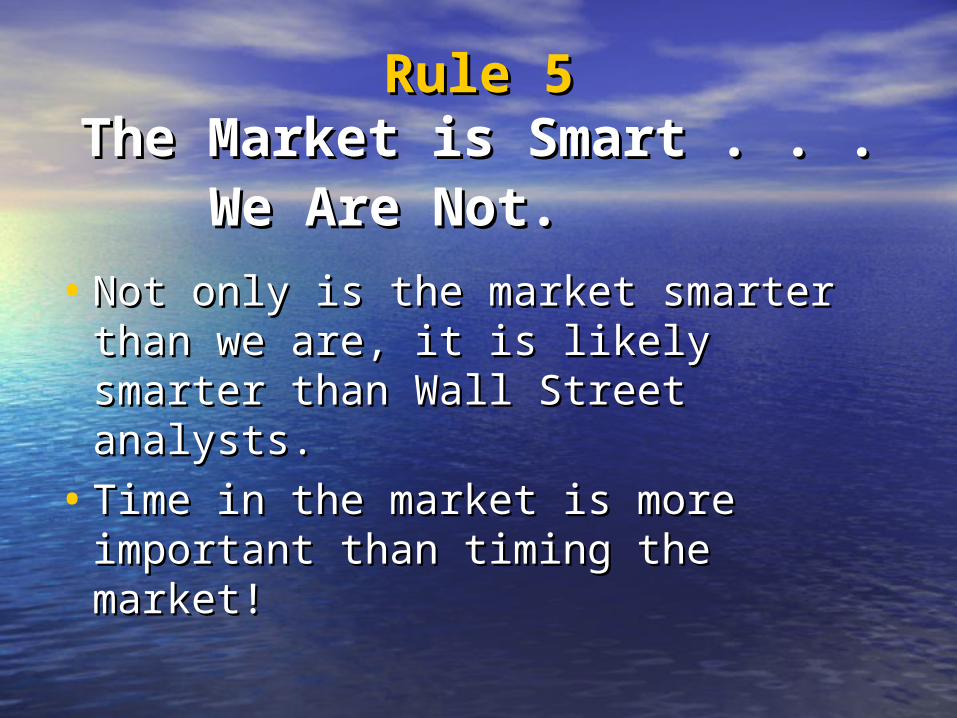

Rule 5Rule 5The Market is Smart . . .The Market is Smart . . .

• Not only is the market smarter than Not only is the market smarter than we are, it is likely smarter than Wall we are, it is likely smarter than Wall Street analysts.Street analysts.

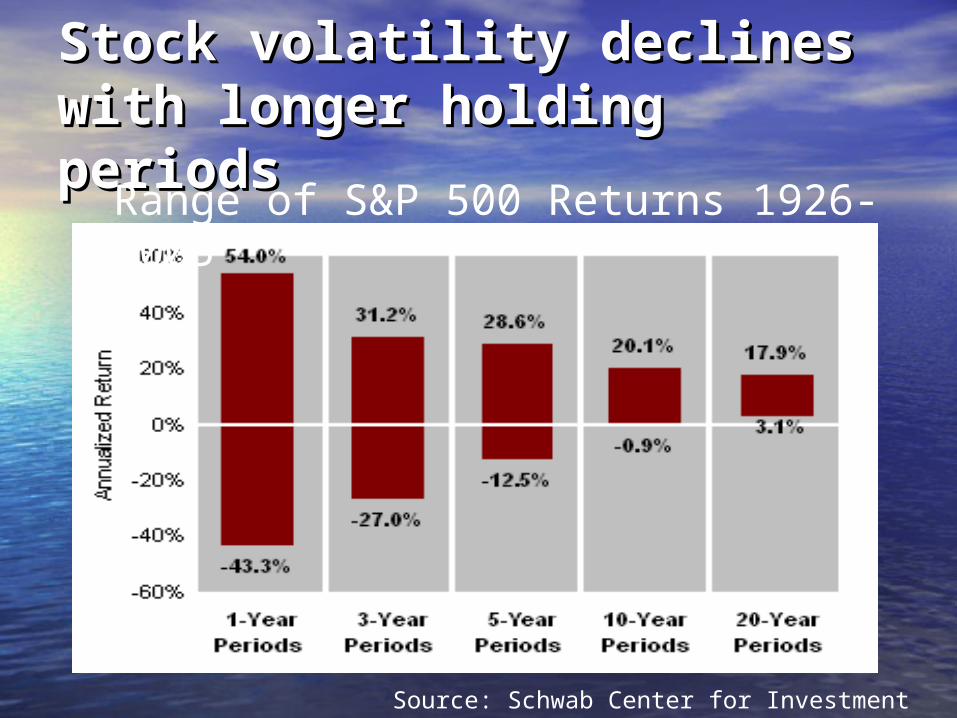

• Time in the market is more important Time in the market is more important than timing the market!than timing the market!

We Are Not.We Are Not.

Implication of Implication of Rule 5Rule 5 . . . . . .

• Use Index FundsUse Index Funds

• Reasons to use index funds:Reasons to use index funds:– Simplify investingSimplify investing– Cost-efficientCost-efficient– Returns outperform average mutual Returns outperform average mutual

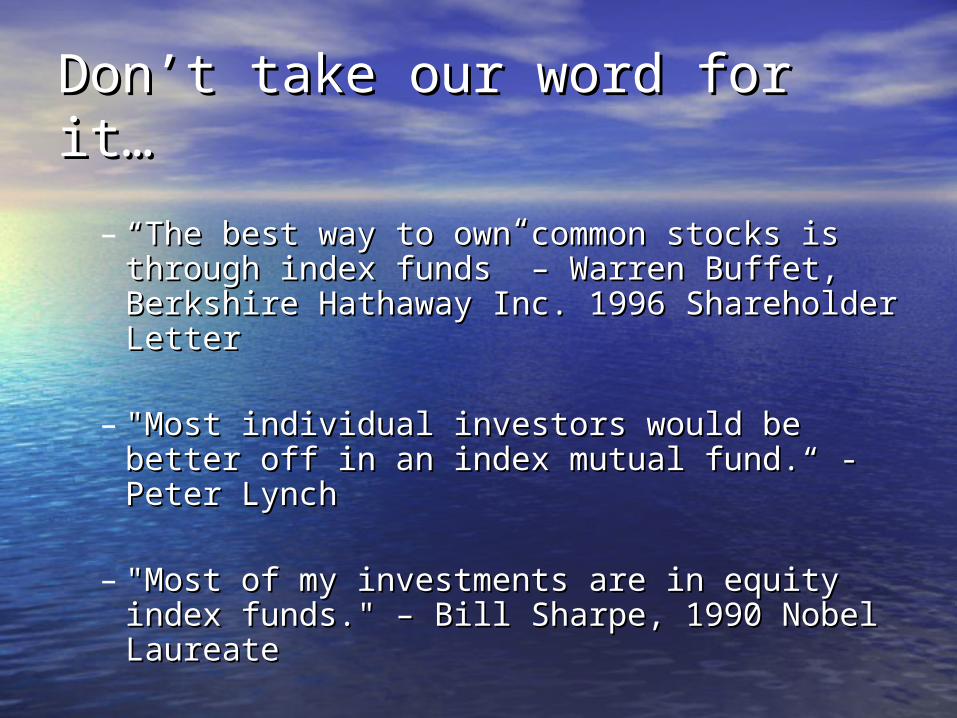

Don’t take our word for it…Don’t take our word for it…

– ““The best way to own common stocks is The best way to own common stocks is through index funds” – Warren Buffet, through index funds” – Warren Buffet, Berkshire Hathaway Inc. 1996 Shareholder Berkshire Hathaway Inc. 1996 Shareholder Letter Letter

– "Most individual investors would be better "Most individual investors would be better off in an index mutual fund.“ - Peter Lynchoff in an index mutual fund.“ - Peter Lynch

– "Most of my investments are in equity "Most of my investments are in equity index funds." – Bill Sharpe, 1990 Nobel index funds." – Bill Sharpe, 1990 Nobel LaureateLaureate

Learning, Earning and Investing

#7 What Are Mutual Funds? National Standards in Economics

Marginal costs and benefits

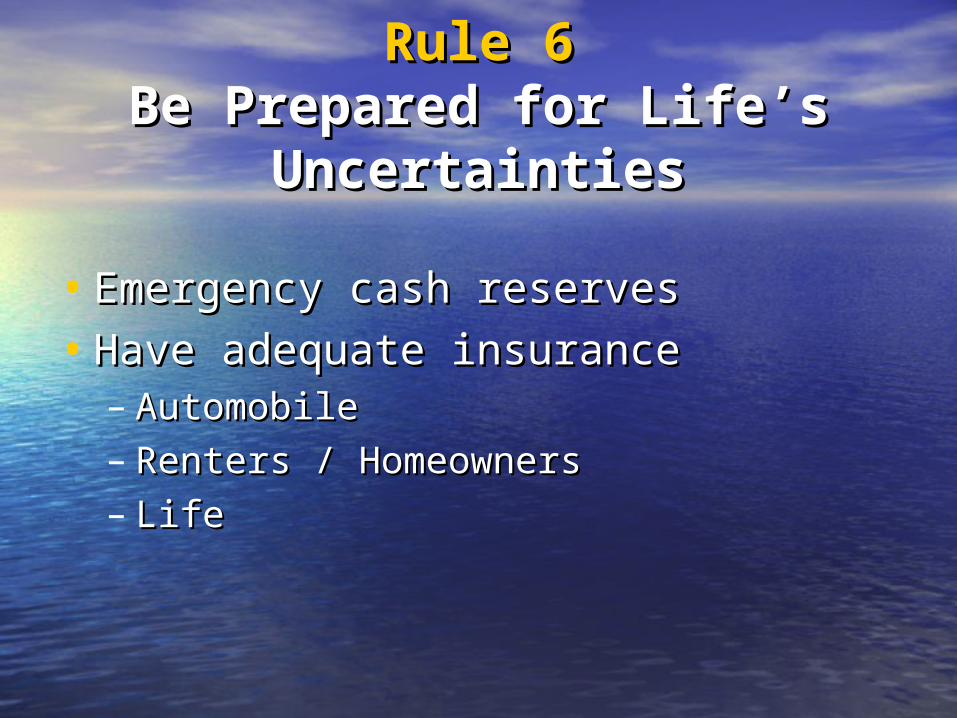

Rule 6Rule 6Be Prepared for Life’s Be Prepared for Life’s

#7 What Are Mutual Funds? #14 Credit: Your Best friend or Your

Worst Enemy? National Standards in Economics

Marginal costs and benefits

Impact of Earning Master’s DegreeImpact of Earning Master’s Degree

• Increased wage earningsIncreased wage earnings– 16% more with 5 years of service16% more with 5 years of service– 26% more with 14 years of service26% more with 14 years of service

• Increased pension benefitsIncreased pension benefits– $5,600 more per year with MA+24 vs. BA$5,600 more per year with MA+24 vs. BA– Increased benefit lasts for rest of your lifeIncreased benefit lasts for rest of your life

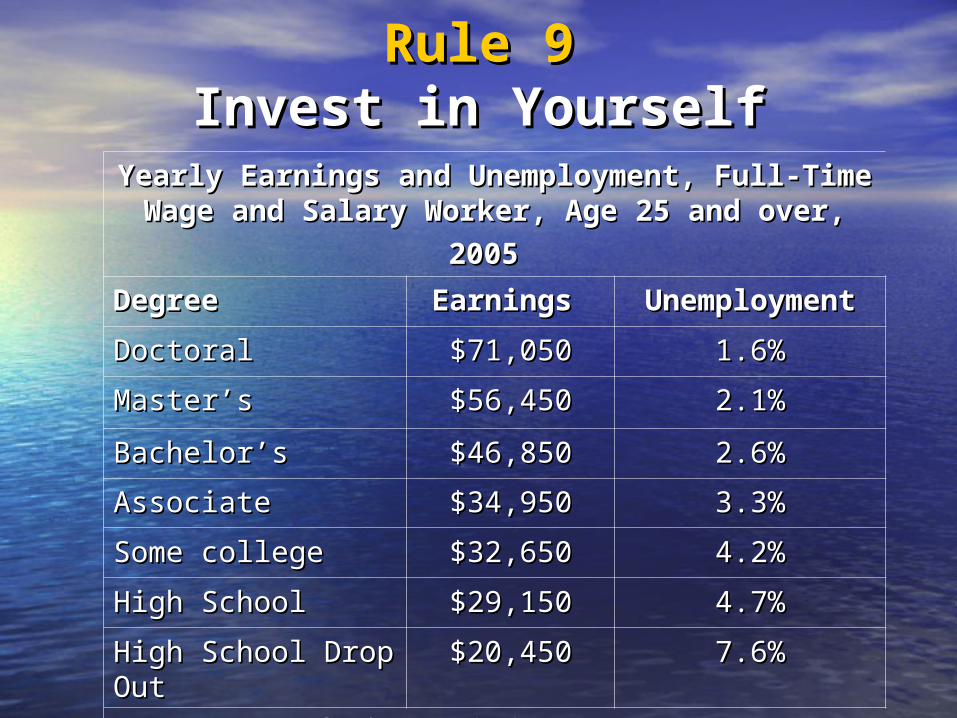

Rule 9Rule 9Invest in YourselfInvest in Yourself

Rule 9Rule 9Invest in YourselfInvest in Yourself

Yearly Earnings and Unemployment, Full-Yearly Earnings and Unemployment, Full-Time Wage and Salary Worker, Age 25 and Time Wage and Salary Worker, Age 25 and