24

1 TGP DART Update Meeting New York, NY May 18, 2017

Agenda

Welcome and Introductions Erin Mortimer

Regulatory Update Gene Nowak

KM Update Sherri Glazebrook

Operations/Scheduling Update Cathy Soape Hutton

Brian Merchant

Commercial Update Coralie Sculley

DART

Contract Updates Sherry Noack

Nominations Debbie Vasquez

Discussion and Feedback All

2

TRANSPORTATION SERVICES ORGANIZATIONAL

STRUCTURE

3

WEARs DSRs

NAESB / KM Update

• Passport – EPNG/Mojave

• October 1, 2017

• Last of 4 major system conversions – 5 ½ years

• Ongoing upgrades to DART

• Limited resources due to focus on conversions and related regression testing

• 2018 will be a year of various improvements that have been backlogged over the years

• NAESB – GEH (Gas Electric Harmonization)

• FERC Order 809 requested NAESB to continue looking for way to have faster

scheduling and confirmation processes

• KM actively participated in a series of GEH forums and NAESB standards meetings

• Default level of confirmations was narrowly defeated

• NAESB Version 3.1 will be published in 3rd Quarter 2017 – no major changes

• INGAA Educational Seminar to FERC Staff – Feb 2017

• Scheduling and Moving Gas Through a Pipeline

• Design, Scheduling and Flexibility

4

Winter Look Back Summary

Peak Day was ~10.1 Bcfd on Jan 7, 2017 - Deliveries

Peak Day was ~1.7 Bcfd on Jan 8, 2017 – Storage (withdrawal)

Peak Day was ~1.8 Bcfd on Jan 7, 2017 – Power Plant Load

Winter OFO count

2016/2017 Zones 5 & 6 - 28 vs 21 in 2015/2016

11 OFO’s were directed at power plants (Dec/Jan) vs 8 in 2015/16

2016/2017 All other zones - 16 vs 6 in 2015/2016

Storage Inventories down from 2015/16

44% lower than the levels for 2015/16

2% higher than 2014/15

System Challenges

Less supply coming in from Dracut/Distrigas

Short Term Unit/Pipeline Issues — Managed without cutting In-Path Services at Timely

Continuous communication between Commercial, Scheduling and Gas Control Groups

5

Winter Days - (%) Restricted Restriction

Point

Highly Utilized

TGP Paths

Percentage

Days Restricted

(November -

March)

Percentage

Days Restricted

(November -

March)

Percentage

Days Restricted

(November -

March)

Percentage

Days Restricted

(November -

March)

2013/2014 2014/2015 2015/2016 2016/2017

Sta. 200/204 30.46% 22.52% 64.47% 68.87%

Sta. 245 100% 100% 100.00% 99.33%

Sta. 261 30.46% 32.45% 68.42% 27.81%

Sta. 267 2.65% 5.29% 30.92% 55.63%

MLV 273 0.00% 0.00% 0.00% 17.22%

Sta. 315 BH 100% 100% 76.32% 96.69%

Sta. 321 94.70% 94.71% 86.18% 92.72%

MLV 336 50.33% 73.51% 57.24% 30.46%

MLV 355 BH 70.20% 5.96% 9.21% 5.30%

Sta. 1 BH 50.99% 11.26% 84.21% 0.00%

Sta. 9 BH 0.00% 0.00% 0.00% 43.71%

Mahwah 49.67% 64.24% 92.76% 88.08%

Rivervale 80.79% 80.79% 66.45% 80.79%

7

Summer Preview

Demand to remain strong across the system

Capacity Utilization on the 200/300 Line in Northeast should remain high

Marcellus and Utica Production to remain at High Levels

Southbound Flows

Volumes through Station 87 should remain in the 2.0-2.2 Bcf/d as maintenance activities are completed

Exports to Mexico and Canada to remain strong

Storage Field Levels

Northern Storage levels down from last year; better able to manage maintenance activities and handle market area supply swings

Bear Creek Storage levels higher than last year; better able to handle higher power demand in the South

High level of system maintenance, repair, rebuild activity

GETTING READY FOR WINTER

DART SCHEDULING TOOLS

No delivery nominations allowed to Dracut

No receipt nominations allowed at Mendon until ID1 (compared to EPSQ volumes)

No delivery nominations allowed at Wright/Shelton until ID1 (compared to EPSQ volumes)

Invalid nominations not allowed

Limitations of Storage Services/Linepack Services

No meter bounces allowed at power plants downstream (may be invoked)

New restriction locations as needed

Imbalance Warnings

Monthly OFOs

Daily OFOs

Hourly OFOs – new screens coming

Additional segment capacities posted to the EBB

8

Forward-Looking Statements /

Non-GAAP Financial Measures

This presentation includes forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and

Section 21E of the Securities and Exchange Act of 1934. These forward-looking statements are identified as any statement that does not relate

strictly to historical or current facts. In particular, statements, express or implied, concerning future actions, conditions or events, future operating

results or the ability to generate revenues, income or cash flow or to pay dividends are forward-looking statements. Forward-looking statements

are not guarantees of performance. They involve risks, uncertainties and assumptions. Future actions, conditions or events and future results of

operations of Kinder Morgan, Inc. may differ materially from those expressed in these forward-looking statements. Many of the factors that will

determine these results are beyond Kinder Morgan's ability to control or predict. These statements are necessarily based upon various

assumptions involving judgments with respect to the future, including, among others, the timing and extent of changes in the supply of and

demand for the products we transport and handle; national, international, regional and local economic, competitive and regulatory conditions and

developments; the timing and success of business development efforts; technological developments; condition of capital and credit markets;

inflation rates; interest rates; the political and economic stability of oil producing nations; energy markets; weather conditions; environmental

conditions; business, regulatory and legal decisions; terrorism, including cyber-attacks; and other uncertainties. There is no assurance that any of

the actions, events or results of the forward-looking statements will occur, or if any of them do, what impact they will have on our results of

operations or financial condition. Because of these uncertainties, you are cautioned not to put undue reliance on any forward-looking statement.

Please read "Risk Factors" and "Information Regarding Forward-Looking Statements" in our most recent Annual Report on Form 10-K and our

subsequently filed Exchange Act reports, which are available through the SEC’s EDGAR system at www.sec.gov and on our website at

www.kindermorgan.com.

We use non-generally accepted accounting principles (“non-GAAP”) financial measures in this presentation. These non-GAAP measures should

not be considered as alternatives to GAAP financial measures.

9

Natural Gas Pipelines Segment Outlook

Well-positioned connecting key natural gas resources with major demand centers

Growing Footprint:

Own or operate largest natural gas

network in North America

— ~70,000 miles of pipeline

— ~70 Bcf/d of capacity

— ~690 Bcf of storage capacity

Moving ~40% of U.S. natural gas

consumption

Connected to every important natural

gas resources play in the U.S.

Project Backlog:

$3.4 billion of identified growth projects

over next four years (2017-2020)(a),

including:

— LNG liquefaction (Elba Island, GA)

— Transport projects supporting LNG

liquefaction

— Expansions to Mexico border

— TGP North-South projects __________________________

(a) Includes KM share of non-wholly owned projects. Includes

projects currently under construction. 10

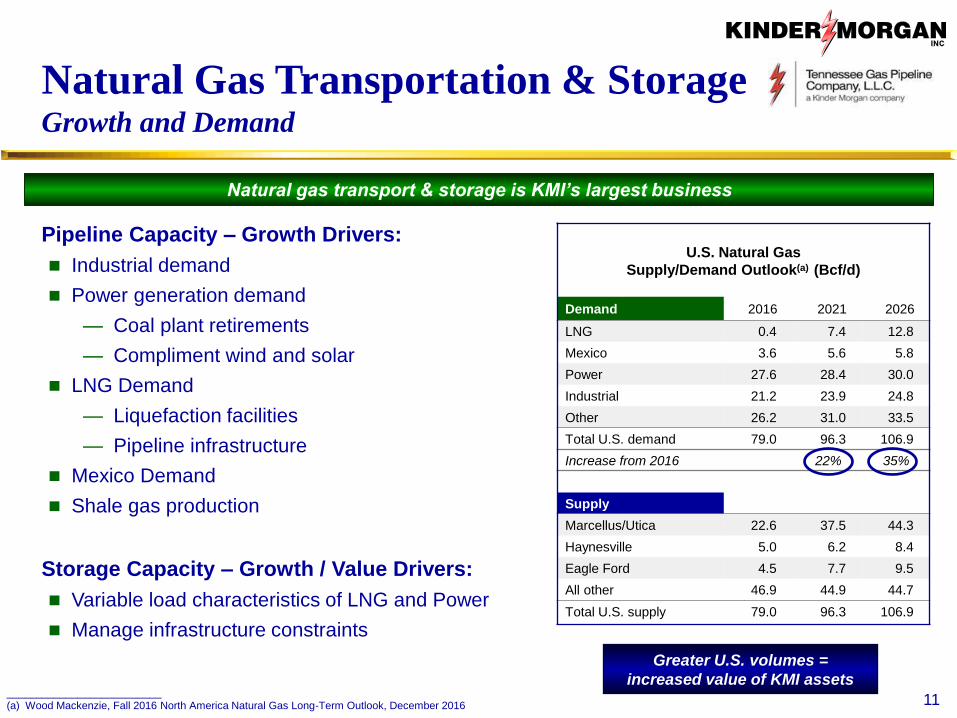

11

Natural gas transport & storage is KMI’s largest business

U.S. Natural Gas

Supply/Demand Outlook(a) (Bcf/d)

Demand 2016 2021 2026

LNG 0.4 7.4 12.8

Mexico 3.6 5.6 5.8

Power 27.6 28.4 30.0

Industrial 21.2 23.9 24.8

Other 26.2 31.0 33.5

Total U.S. demand 79.0 96.3 106.9

Increase from 2016 22% 35%

Supply

Marcellus/Utica 22.6 37.5 44.3

Haynesville 5.0 6.2 8.4

Eagle Ford 4.5 7.7 9.5

All other 46.9 44.9 44.7

Total U.S. supply 79.0 96.3 106.9

Greater U.S. volumes =

increased value of KMI assets

Natural Gas Transportation & Storage Growth and Demand

Pipeline Capacity – Growth Drivers:

Industrial demand

Power generation demand

— Coal plant retirements

— Compliment wind and solar

LNG Demand

— Liquefaction facilities

— Pipeline infrastructure

Mexico Demand

Shale gas production

Storage Capacity – Growth / Value Drivers:

Variable load characteristics of LNG and Power

Manage infrastructure constraints

__________________________

(a) Wood Mackenzie, Fall 2016 North America Natural Gas Long-Term Outlook, December 2016

Northeast shale production expected

to double by 2026(a)

— 40% of all U.S. natural gas production

— North–to–South transport continues to

grow, even with higher costs

KM Opportunity

— TGP: First mover in the Marcellus/Utica

• ~ 4.5 Bcf/d combined Northeast receipts

• ~ 11 Bcf/d of Northeast receipt capacity

• ~ 2 Bcf/d transported from North-to-South

— 938 MDth/d of expansion projects in

development to support NE supply growth

— Total program capital ~ $1.2 Billion

Drivers of Future Growth Marcellus/Utica

__________________________

(a) ICF – Gas Transport in a Changing Market Environment 4/20/17 and KM analysis.

KM Asset KM Project/Transportation

Contracted

Capacity

(MDth/d)

In-Service

Date

KM Capital

($MM)

TGP Broad Run Flexibility 590 In-Service

$736.1

TGP Broad Run Expansion 200 6/2018

TGP Susquehanna West 143 11/2017 $143

TGP Orion 135 6/2018 $129.3

NGPL Gulf Coast Southbound (via REX) 460 10/2018 $212

12

Forecast

Sta 87

Supply-Push Dth/d In-Service

Broad Run Expansion 200,000 Jun-2018

Susquehanna West 145,000 Nov-2017

Orion 135,000 Jun-2018

Market-Pull Dth/d In-Service

SW Louisiana Supply 900,000 Q1-2018

Lone Star 300,000 Jan-2019

Connecticut Expansion 72,100 Nov-2017

Triad 180,000 Jun-2018

Development Project Updates

13

Sta 219

Sta 17

Sta 534

Sta 313

Sta 47

Sta 40

Market-Driven Project

o Demand growth in Connecticut

Capacity: 72,100 Dth/d

Customers: Southern Connecticut,

Connecticut Natural,

Yankee

Projected In-service: November 2017

Project Scope:

o 13.46 miles of pipeline loop

o Acquisition of Thompsonville Lateral

Project Status:

o FERC certificate received March 11, 201

o FERC issued Notice to Proceed for tree

clearing & full construction April 12, 2017

o MA 401 Permit final and unappeable as of

April 24, 2017

14

Connecticut Expansion Project

The Importance of Fossil Fuels …and the Recent, Modest Growth of Renewable Energy

Fossil Fuels

Have accounted for >80% of total U.S. energy consumption

over the last 100+ years(a)

Generating ~67% of U.S. electricity (Q3-2016)(b)

Over 99% of U.S. light vehicles today run on gasoline or

diesel (>250 million cars and trucks)(c)

Approximately 66% of global textile production comes from

synthetic fibers derived from fossil fuels(d)

__________________________

(a) EIA, Monthly Energy Review, April 2016

(b) EIA, Monthly Energy Review, December 2016

(c) Goldman Sachs, Start Me Up v2.0

(d) Textile Exchange, Preferred Fiber and Materials Market Report, July 2016 15

Coal

Petroleum

Natural Gas

Nuclear Hydroelectric

Other Renewable

Wood

0%

20%

40%

60%

80%

100%

201519751935189518551815

Share of U.S. Energy Consumption by Major Energy Source, 1776-2015

Renewables

Accounted for only ~15% of U.S. generation i(Q3-2016)(a)

— About half is hydropower which is not expected to grow

Renewable energy cannot be stored effectively at scale

— Wind and Solar are intermittent and require reliable

complimentary sources for balancing and backup

— Natural gas has primarily fulfilled this role

Natural Gas Critical to Climate Goals Opposition to Natural Gas is Misplaced

16

Monthly Energy Review(a) 1993 2007 2015

U.S. Population ~260 million ~301 million ~321 million

Real GDP ~$9.5 trillion ~$14.9 trillion ~$16.3 trillion

Power sector CO2 emissions 1.92 GT 2.42 GT 1.91 GT

Power generation (GWh) 3,197,191 4,156,745 4,077,601

Coal 53% 49% 33%

Natural Gas 13% 22% 33%

Nuclear 19% 19% 20%

Solar/Wind <1% <1% 5%

__________________________

(a) EIA, Monthly Energy Review, December 2016.

(b) EPA, U.S. Greenhouse Gas Inventory Report, April 2016.

Natural gas is the cleanest burning fossil fuel with significantly lower

emissions than coal or fuel oil

Switching from coal to natural gas has driven a reduction in the nation’s

power sector CO2 emissions

U.S. methane emissions decreased 6% from 1990 to 2014(b) despite a 46%

increase in natural gas production(a) over the same period

Pipeline Development Environment Attack on Fossil Fuels Focused on Pipelines

17

NGO Opposition

Well funded and organized

— National, regional and local

— Challenging every step in process

Refining tactics

— Widespread misinformation

— Consistently linked to production and exports

— Delaying construction

— Focus on state resource agencies

State Permitting Challenges

Interdependency of permits and delegation of authority

Agency concern with “second guessing”

Requirements vary significantly by state

Impacts

— Costly and time consuming

— Uncertainty and delays in obtaining permits

— More stringent requirements

It’s Changing How We Develop Projects

Project Planning

— Extended timelines – from filing to in-service

— Thorough risk identification & planning

— Early Stakeholder engagement

— Safety and security

Relationship with Customers

— Stronger partnerships

— Earlier engagement

— Setting expectations

— Combined outreach and communication

Contracting

— Recognition of risks

— Risk allocation

— Account for potential schedule impacts

18

DART Modifications - Contracts In Progress/Upcoming

Request Description Status

Re-release Indicator Testing – planned implementation in June

Capacity Release Offer Upload

In discussion – plan to

start working on this in 3rd

or 4th quarter

Other Upcoming Capacity Release Enhancements Ability to release 100% of primary available quantity with the click of a button Ability to copy an offer with one click instead of two

Automatically delete the zero when clicking in the Max Offer Quantity box instead of manually deleting Add more filters to the All Offers/Awards screen Offer an un-editable format for the Capacity Release Award Audit Report in addition to the Excel format

19

20

DART Modifications – Noms/Confs In Progress/Upcoming

Request Description Status Fixing nomination validation and MDQ Utilization screen for specific overlapping nomination scenario In progress - 3rd Quarter

Confirmations for subsequent cycles In progress - 3rd Quarter

Ability to edit/modify submitted nomination batch Submitted

Contract Path Tab – Add row # Submitted Enhance Subscription to Critical Notices for subcategory options Upcoming

21

DART – Nominations

22

UDP Level Confirmation

Denotes confirmation party

Auto Match – On/Off

23

Tips for Buy/Sell transactions between UDPs at the same meter

Auto match - OFF

Nominations may duplicate if UDPs at a single meter use different confirmation methods (Auto match function on/off) AND buy and sell from each other.

UDP

A

UDP B

(as shipper)

UDP

C

UDP B

(as shipper)

Sell 1,000 Buy 1,000

Sell 1,000 Buy 1,000

Blue – manually entered Red – auto generated

Auto match - ON

Auto match - ON

Auto match - ON

Sell 1,000 Buy 1,000

*Possible duplicate nominations

Discussion And Feedback