34

THAICOM Public Company Limited GS & SCBS Thailand Corporate Day June 19, 2015

| Date post: | 02-May-2018 |

| Category: |

Documents |

| Upload: | truongxuyen |

| View: | 215 times |

| Download: | 1 times |

THAICOM Public Company Limited

GS & SCBS Thailand Corporate DayJune 19, 2015

2

Agenda

• Thaicom…Who We Are

• Financial Highlights

• Industry Outlook & Moving Forward

3

Who We Are

4

Our Company

• Thaicom Public Company Limited (formerly known as Shin Satellite) was founded on 7th November 1991, as part of Intouch Holdings Public Company Limited (formerly known as Shin Corp.)

• His Majesty King Bhumibol Adulyadej of Thailand graciously named the first national communications satellite, “THAICOM” which stands for “Thai Communications”.

5

Shareholding StructureAspen Holdings Ltd. (Temasek Holdings)

41.62%

IPSTAR Global Service Ltd. 100.00%

Spacecode Llc. 70.00%

IPSTAR New Zealand Co., Ltd. 100.00%

1) Holding Company

2) Listed Company on the Stock Exchange of Thailand

* As of 2 April 2015

IPSTAR Japan Co., Ltd. 100.00%

IPSTAR International Pte Ltd. 100.00%

STAR Nucleus Co., Ltd. 100.00%

IPSTAR Co., Ltd. 100.00%

IPSTAR Australia Pty Ltd. 100.00%

TC Broadcasting co., Ltd. 99.99%

International Satellite Co., Ltd. 100.00%

Intouch Holdings Plc. 1),2)

Advanced Info Service Plc .2)

Thaicom Plc. 2)

ITV Plc.

I.T. Applications and Services Co., Ltd.

Satellite Services

Shenington Investments Pte Ltd. 51.00%

Lao Telecom Co., Ltd. 49.00% DTV Service Co., Ltd. 99. 99%

CS LoxInfo Plc. 2) 42.07%

Cambodian DTV Network Ltd. 100.00%

AD Venture Public Co., Ltd. 99.99%

Teleinfo Media Plc. 99.99%

Telephone Network services Internet Services and Media

40.45%

Orion Satellite Systems Pty Ltd. 100.00%

41.14% 52.92% 99.99%

6

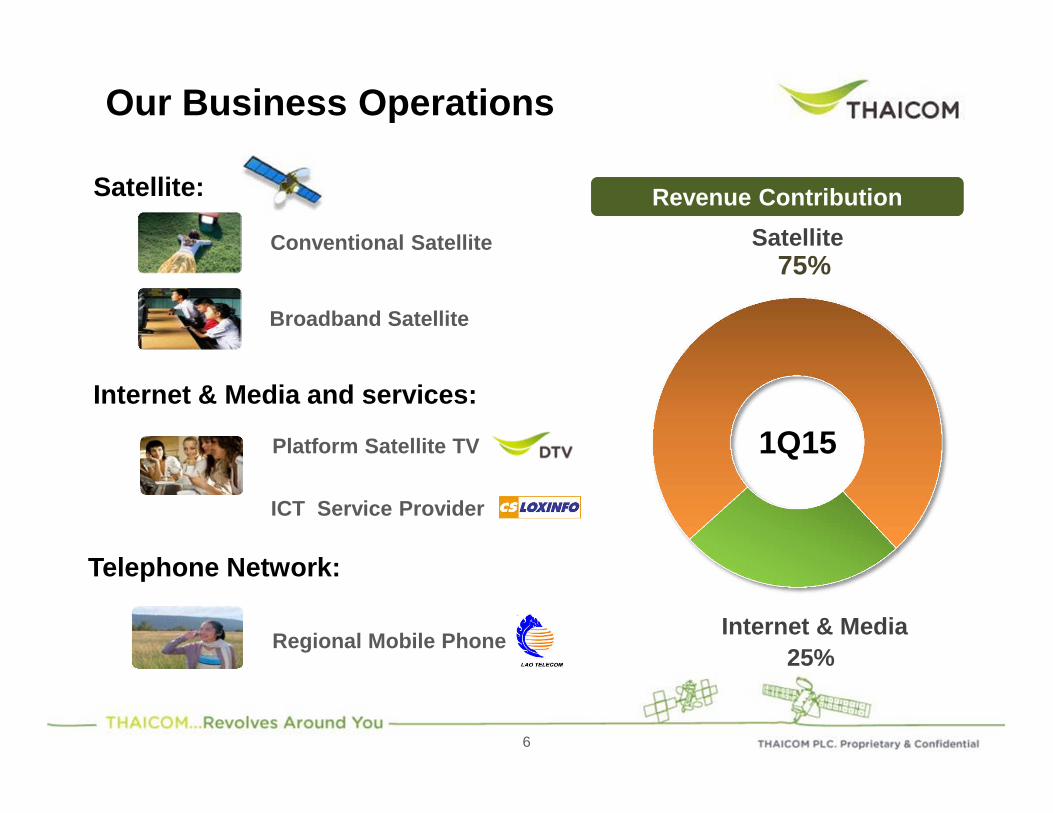

Our Business Operations

Broadband Satellite

Conventional Satellite

Regional Mobile Phone

Platform Satellite TV

Satellite:

Telephone Network:

Internet & Media and services:

Revenue ContributionRevenue Contribution

Satellite75%

Internet & Media25%

1Q15

ICT Service Provider

7

THAICOM 4 (IPSTAR)

Our Satellite Fleet

Concession License

Launched 2005 2006 2014 2014 Target 1H’16

Type of Satellite Broadband Conventional Conventional

Fee20.5%

(Sep 2016 = 22.5% onwards)5.25%

Contract Life (Yr) 30 yr (2021) 20 yr (2032)

Satellite Life (Yr) 15 14 18 18 18

Utilization rate* 57% ~100% ~67% ~50%

THAICOM 1ALaunched: 1993De-orbited: 2010

THAICOM 2Launched: 1994De-orbited: 2010

THAICOM 3Launched: 1997De-orbited: 2006

THAICOM 5 THAICOM 6 THAICOM 7

UpcomingIn-orbitDe-orbited

*As of March 31, 2015

THAICOM 8

8

Our Capacity

3,439

2,819

2,539

2,175

1,5751,411

992 968

633 612436

331 330

ViaSat Eutelsat EchoStar/Hughes

Intelsat SES InmarSat Thaicom2016

Thaicom2014

Telesat Yahsat JSAT ABS ChinaSatCom

Satellite Operators' Bandwidth Capacity (Estimated)

Est

imat

ed C

apac

ityE

quiv

alen

t (T

PE

)

Note:* Thaicom's capacity Y2014 includes THAICOM 4 , THAICOM 5, THAICOM 6 and THAICOM 7 satellites** Thaicom's capacity Y2016 includes THAICOM 4 , THAICOM 5, THAICOM 6, THAICOM 7 and THAICOM 8 satellites*** Other satellite operators' capacities (estimated) are as of July 2014**** TPE = 36MHz transponder equivalent

Largest Satellite Operator in Asia Pacific (7 th Globally)Largest Satellite Operator in Asia Pacific (7 th Globally)

9

TC4 (Ku)

TC5 (C,Ku)

Our Satellite Footprints

50.5E 78.5E 120E119.5ECoverage Area

TC4

TC5

Remarks: *TPE = 36 MHz transponder equivalents

TC6 (C,Ku)

TC7 (C)

TC6

TC7

TC8

TC4 TC5 TC6 TC7 TC8

119.5°E 78.5°E 78.5°E 120°E 78.5°EC Ku C Ku C Ku C Ku C Ku

Indochina - - -

SEA - - - - - - -

South Asia - - - - - -

North Asia - - - - - - - -

Australasia - - - - - - -

ME, Africa - - - - - - -

Total TPE* 881 40 33 14 24

TC8 (Ku)

Broadband Satellite Capacity

=TC4 = 881 TPE*

TC5 = 40 TPE*

10

Covering More than

120 COUNTRIES

Hosting

738 (110 HD)SATELLITE TV CHANNELS

Asia’s “Hot Bird” for Satellite TV

No.1 in Thailand and Indochina

A key player in South AsiaSource : Thaicom PLC, 1Q15

17.5 Million viewers or

73% of total TV HOUSEHOLDS

Source : Nielsen

Our Broadcast Services

Number of Satellite TV channels on Thaicom @78.5E

416 442567 592 628

1123

74 110 110

2011 2012 2013 2014 Q1 2015

SD channel HD channel

1Q15

11

PRESENCE in10+ COUNTRIES in Asia Pacific

5,000 small-cell 3G sites in Japan

17,000 corporate/banking and mobile backhaul sites in India

80,000 broadband users in Australia and New Zealand

37,000 schools and government project sites in Thailand and Malaysia

The World’s first High Throughput Satellite (HTS)

Our Broadband Services

12

Financial Highlights

900

1,100

1,300

1,500

1,700

1,900

- 5

10 15 20 25 30 35 40 45

4-Jan

-124-M

ar-12

4-May-12

4-Jul-

124-S

ep-12

4-Nov-12

4-Jan

-134-M

ar-13

4-May-13

4-Jul-

134-S

ep-13

4-Nov-13

4-Jan

-144-M

ar-14

4-May-14

4-Jul-

144-S

ep-14

4-Nov-14

4-Jan

-154-M

ar-15

4-May-15

THCOM SET Index

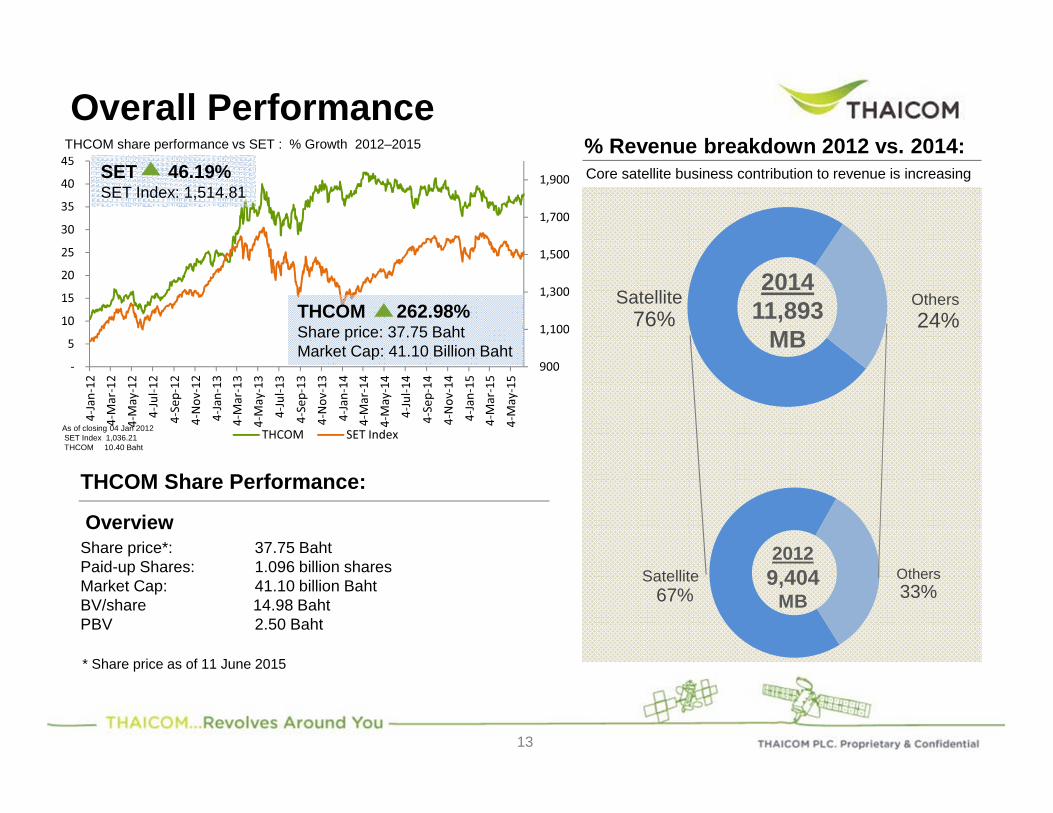

Overall PerformanceTHCOM share performance vs SET : % Growth 2012–2015

THCOM Share Performance:

Overview

* Share price as of 11 June 2015

Core satellite business contribution to revenue is increasing

% Revenue breakdown 2012 vs. 2014:

Satellite76%

Others24%

201411,893

MB

Share price*: 37.75 Baht Paid-up Shares: 1.096 billion shares Market Cap: 41.10 billion Baht BV/share 14.98 Baht PBV 2.50 Baht

Satellite67%

Others33%

20129,404

MB

SET 46.19%SET Index: 1,514.81

THCOM 262.98%Share price: 37.75 BahtMarket Cap: 41.10 Billion Baht

As of closing 04 Jan 2012 SET Index 1,036.21 THCOM 10.40 Baht

13

14

Others

Revenue Breakdown by Country

oIndonesiaoMalaysiaoPhilippineoKoreaoNew ZealandoCambodiaoVietnamoSouth AsiaoMiddle East/Africa & Pacific

Thailand62%

Australia11%

Other8%

Myanmar8%

Japan6%

India3%

China2%

1Q153,074MB

15

6,309 6,964 8,784

2,309

3,095 3,028 3,109

765

9,404 9,992 11,893

3,074

2012 2013 2014 1Q15

other

Satellite Revenue

174 1,128

1,601

540 371

231

545 1,128

1,832

540

6%

11%

15%18%

0%2%4%6%8%10%12%14%16%18%20%

2012 2013 2014 1Q15

Net profit

Net profit Margin

Consolidated Sales & Services RevenuesUnit: MB

Bottom Line Grew Significantly from Satellite Performance

Revenue grew continuously with CAGR of 8% (2012-2014).

Normalized Net profit and marginUnit: MB

* Excludes Impairment of M-fone and Watta total 371 MB** Excludes Impairment of TMC of 231 MB

Drastically improved in Normalized Net Profit and Margin with CAGR of 50% (2012-2104).

**

*

16

6,279 6,964

8,784

2,309

2012 2013 2014 1Q15

BroadbandConventional

3,328 3,373

4,577

1,191

53%

48%

52% 52%

30%

35%

40%

45%

50%

55%

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 1Q15

Satellite EBITDA

EBITDA Margin

Satellite RevenuesUnit: MB

Satellite EBITDAUnit: MB

Strong Satellite Performances with Improving Margin

EBITDA grew with CAGR of 11% (2012-2014).

FY2013, EBITDA Margin dropped to 48% due to cost of interim satellite.

Revenues continuously grew with CAGR of 12% (2012-2014).

46%

54% 51%

49%

49%

51%

55%45%

17

Asset, 27,437

Cash,3,819

Interest bearing debt,

10,497

Liabilities, 3,955

Equity, 16,804

Financial Position Remains Strong

Unit: MB

* Restated

Unit: MB

1. Interest-bearing Debt / Equity2. Excludes Cash and Current Investment3. Excludes Interest-Bearing Debt4. Cash and Current Investment(B/E)

D/E Ratio at 0.62x 1 Strong cash from operation

2

4

3

Consolidated CF 1Q14* 1Q15

CF from Operating 1,042 867

CF from Investing (442) (132)

CF from Financing (351) (590)

Ending Cash 2,530 2,915

18

0.40 0.45

0.65

56%62%

70%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

2012 2013 2014

DPS (Baht) Dividend Payout ratio

Delivering Consistent Dividend Growth

Dividend payout policy is NOT less than 40% of stand-alone Net Profit.

Dividend paid for the past 3 years exceeded the policy with payout ratio of 56%, 62%, and 70% respectively.

19

Industry Outlook & Moving Forward

20

0

200

400

600

800

1000

1200

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Global Ultra HD via Satellite ChannelsChannels

�Nearly 1,000 Ultra HD channels in 2025

�Over 180 channels are from Asia Pacific

�CAGR 52% from 2015 to 2025

Source: NSR

Higher Bandwidth Required for Broadcast Services

Audio-Video Adoption in USA Households

52% CAGR 2015-2025

�Ultra HD to reach 70% of USA households by 2019

Source: http://dusil.com/, Visual Unity

Global Industry Trend

21

Global Industry TrendExponential Growth of Broadband Demand

� Annual global IP traffic will pass

the zettabyte threshold (1,000 exabytes) by 2016

� Video content to account for

79% of total IP traffic in 2018

Video Content

Source: Cisco VNI

0

200

400

600

800

1,000

1,200

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Gbp

s

Distribution DTHContribution & OUTV Telephony & CarrierEnterprise Data Broadband AccessCommercial Mobility Gov/Mil

Enterprise Data

Broadband Access

Global HTS Bandwidth Demand by Application

� Over 1,000 Gbps bandwidth demand for Global HTS in 2023

� With 6.6 million satellite broadband subscribers in 2023

Global IP Traffic

Source: NSR

Remark: HTS – High Throughput Satellite

22

Domestic Industry Trend

� Ku-band channels to grow

160% in the next 15 years

� By 2030, all channels will be HD

Source : Thaicom PLC (2010-Q1’15); Value Partner (2015-2030)

Source : Nielsen

Source: NSR and Thaicom PLC, (Thailand Q1’15)

198283

73

0

200

400

600

800

1000

352 412

217

138

412650

911

198

356

490

824866

911

2010 2015 2020 2025 2030

4%CAGR, 2015-2030

17%CAGR, 2010-2015

Forecasted Ku-band channel in Thailand

SD

HD

Ku-band channel on THAICOM @78.5E

HD

SD

CABSAT Households

from 16.0 M to 17.5 M

15.1MSatellite homes

2.4MCablehomes

73%

8%

24%

40%

41%

South Asia

Thailand

Western Europe

North America

East Asia

DTH HD channel DTH Total channel

DTH HD Channel Penetration, 2015

Thaicom 21%

Increased CABSAT Households with Strong HD Growth

Remark: CABSAT – Cable and Satellite

23

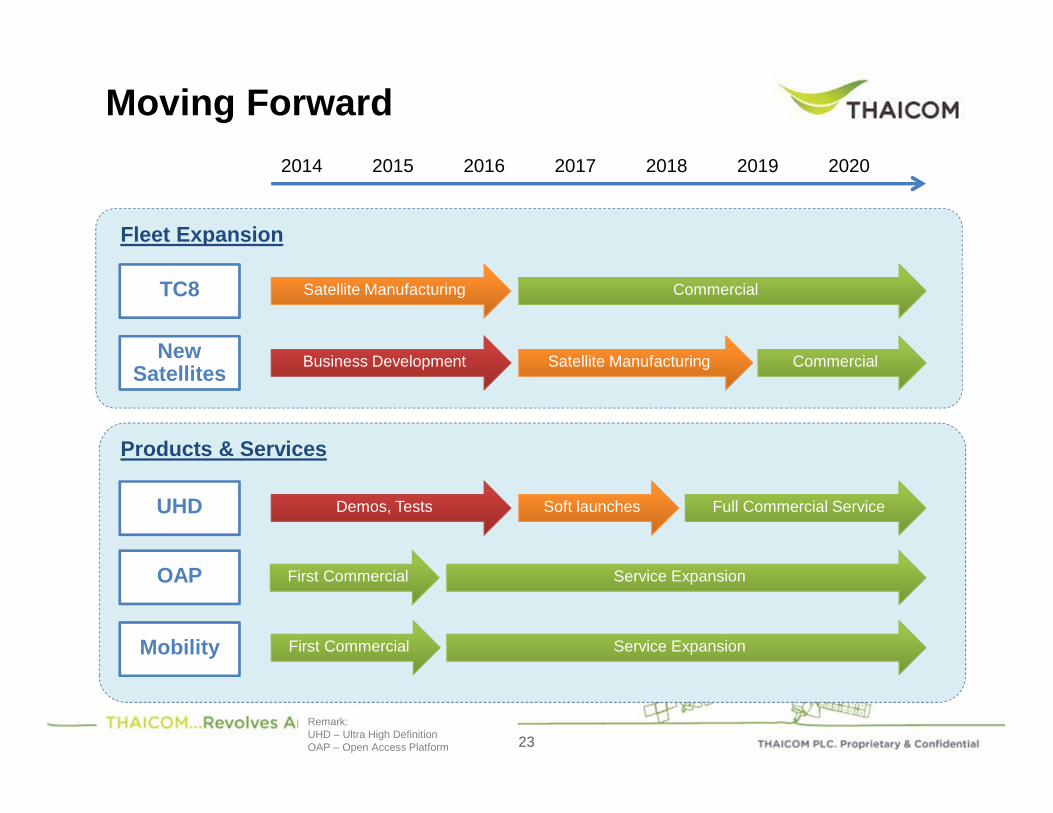

Moving Forward

2014 2015 2016 2017 2018 2019 2020

Fleet Expansion

TC8

New Satellites

Satellite Manufacturing Commercial

Business Development CommercialSatellite Manufacturing

Products & Services

UHD Demos, Tests Full Commercial ServiceSoft launches

OAP First Commercial Service Expansion

Mobility First Commercial Service Expansion

Remark: UHD – Ultra High DefinitionOAP – Open Access Platform

24

Thank You

25

Appendix

26

Myanmar China Nepal India Pakistan

Sweden

Somaliland

Egypt Thailand

Malaysia Indonesia Australia New Zealand

Philippines

Cambodia

Laos

Vietnam

Japan Korea

Israel

Maldives

Our Customers in 20+ Countries

Our Services: Broadcast

27

28

Conventional SatelliteKey Market Segments

29

Broadcast Service Diagram

TV Station/Teleport-Production-Compression-Uplink, etc.

Repeater Station (Analogue & Digital TV)

Direct-to-Home (DTH)

Cable TV

THAICOM (Conventional)

Our Services: Broadband

30

31

IPSTAR Key Market Segment

Telco Backhaul & Enterprise“Cellular Backhaul”“Rural Telephony”

“Corporate Networks”

Telco Backhaul & Enterprise“Cellular Backhaul”“Rural Telephony”

“Corporate Networks”

Government/ USO* Program

“e-Government”“Distance Learning”“National Broadband

Network”“Emergency

Communications”

Government/ USO* Program

“e-Government”“Distance Learning”“National Broadband

Network”“Emergency

Communications”

Mobility“Satcom-on-the-move”“In-flight Entertainment

& Connectivity”“Maritime”

Mobility“Satcom-on-the-move”“In-flight Entertainment

& Connectivity”“Maritime”

Remarks: *Universal Service Obligation

32

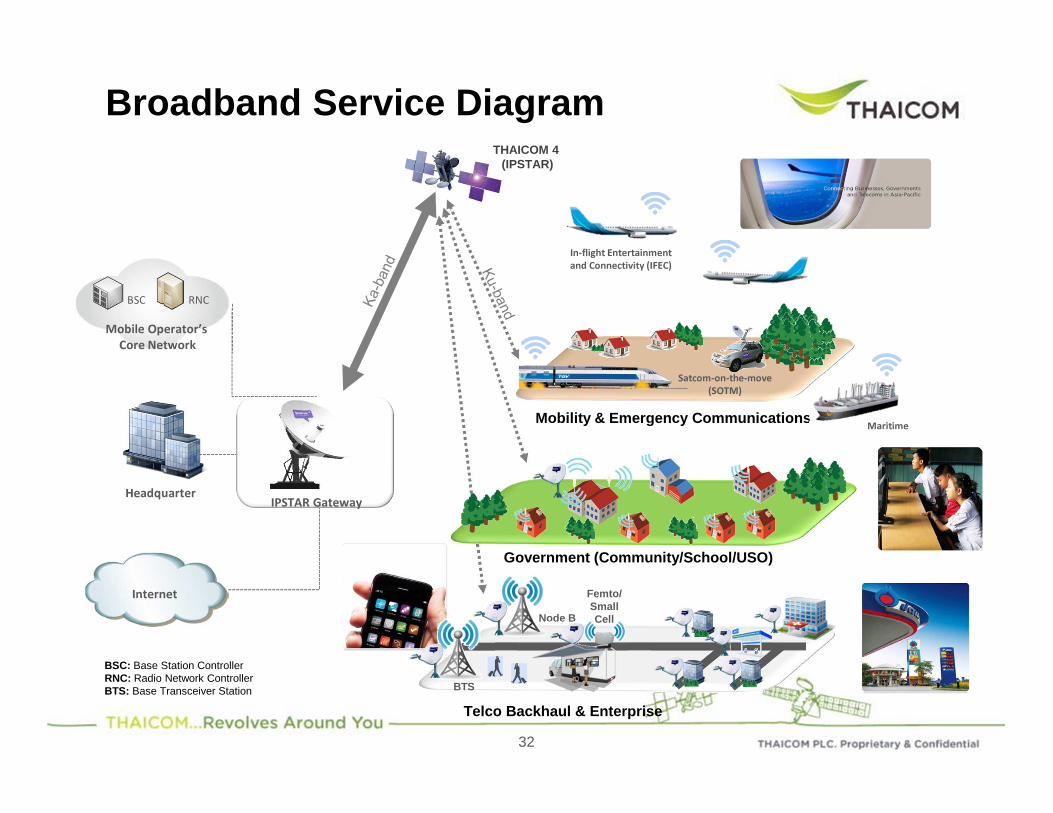

Broadband Service Diagram

BSC RNC

Mobile Operator’s Core Network

IPSTAR GatewayHeadquarter

Internet

THAICOM 4 (IPSTAR)

BSC: Base Station ControllerRNC: Radio Network ControllerBTS: Base Transceiver Station

Mobility & Emergency Communications

Government (Community/School/USO)

In-flight Entertainment and Connectivity (IFEC)

Telco Backhaul & Enterprise

Node B

Femto/SmallCell

Maritime

Satcom-on-the-move (SOTM)

BTS

33

“Best CEO Award”for Listed Companies 2014

by Investment Analysts Association (IAA)

A- with Stable Outlook

A-

Awards & Distinctions: Thailand

Excellent CG Scoring

2014

“ESG 100 Award”2014

by Thaipat Institute

33

34

“Satellite Executive of the Year ” in the Asia-Pacific by the Asia-Pacific Satellite

Communications Council (APSCC)

“Excellence Awards”Corporate Social Responsibility

from Via Satellite, USA

Awards & Distinctions: InternationalRank #10 in Global Top Fixed Satellite Service Operators

Rank #3 in terms of Revenue per Satellite

Top 50 ASEAN CG Scorecard

34