24

The 2017 USS Actuarial valuation 23 January 2018 © 2017 Willis Towers Watson. All rights reserved. Helping you understand the valuation

The 2017 USS Actuarial valuation

23 January 2018

© 2017 Willis Towers Watson. All rights reserved.

Helping you understand the valuation

Who we are

2

And what role do we have in the USS valuation

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

• firm of actuaries &

benefit consultants

• We do not advise USS

or other industry

stakeholder groups

Ellie Boston

• PhD from Birmingham

(applied mathematics)

• Qualified Actuary

• 9 years in the industry

Our role: is to help you understand the valuation process, some of the

technical language and answer your questions

How does a DB pension scheme work?

Benefits paid

ContributionsInvestment returns

Money goes in The Fund builds up Benefits promised

Annual income

Tax-free cash

Family benefits

3© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

4

What is an actuarial valuation?

An actuarial valuation involves:

estimating the present value of the cost of paying

benefits promised to scheme members (for example,

the scheme’s liabilities) and comparing with the value

of the scheme’s assets

determining a rate of future contributions to provide

appropriate security for members’ benefits Liabilities

Assets

The valuation process should help to answer the following questions:

Is there enough money in the scheme to cover benefits earned to date?

How much needs to be paid into the scheme in order to make up any deficit?

How much risk does the trustee wish to take?

4© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

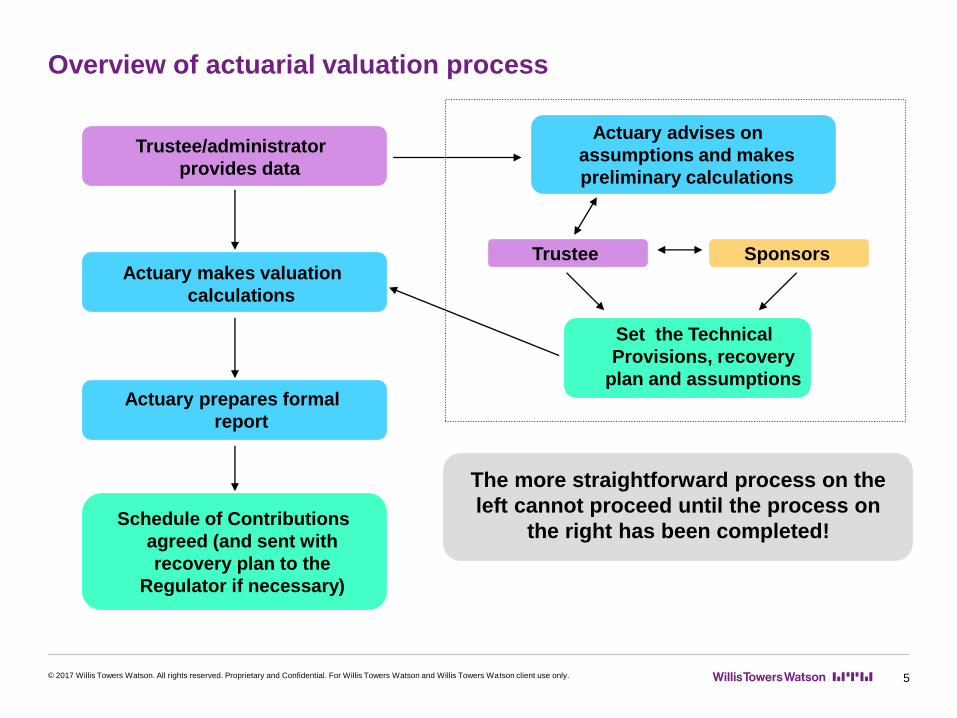

Overview of actuarial valuation process

5

The more straightforward process on the

left cannot proceed until the process on

the right has been completed!

Trustee/administrator

provides data

Actuary makes valuation

calculations

Actuary prepares formal

report

Schedule of Contributions

agreed (and sent with

recovery plan to the

Regulator if necessary)

Actuary advises on

assumptions and makes

preliminary calculations

Trustee Sponsors

Set the Technical

Provisions, recovery

plan and assumptions

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

What is an actuarial valuation

0

20

40

60

80

100

120

0 10 20 30 40 50 60 70 80

£ m

illi

on

Year

Undiscounted projected cashflows

Pensioners Deferred pensioners Actives

These calculations are produced by building a model of

the Scheme’s demographic and financial future that

takes into account:

up-to-date membership data from the Scheme’s administrator

the Scheme’s benefit structure

assumptions for demographic factors (eg mortality) and

financial factors (eg pension increases)

6

0

20

40

60

80

100

120

0 10 20 30 40 50 60 70 80

£ m

illi

on

Year

Discounted projected cashflows

Pensioners Deferred pensioners Actives

1Project future payments from the Scheme

(the ‘projected liability cashflows’)

2Discount the projected liability cashflows to a

present value at the valuation date

3Add up all of the discounted cashflow values to

calculate the ‘technical provisions’ or liabilities

Each future year’s cashflow is converted to a

present value at the valuation date by

discounting it.

For example, if the Scheme’s investments are

assumed to return 5% pa then £100m due to be

paid in 10 years’ time has a present value at the

valuation date of £61m

“At the valuation date, what amount of assets would be needed so that accrued

benefits can be paid as they fall due?”

Actuaries also talk about “ best estimate” and “ self sufficiency” as well

Stakeholders: Trustees

7© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

‘What they must do

Act in line with the trust deed and trust law

Act in the best interests of the

Scheme beneficiaries

Act impartiallyAct prudently, responsibly

and honestly

General responsibility under the Law

Stakeholders: The Pensions Regulator’s objectives

Protecting benefits – occupational schemes and personal pensions

Reducing the risk of schemes drawing on the Pension Protection Fund

Promoting good administration

Minimising any adverse impact on the sustainable growth of an employer

Mark BoyleChair of the Pensions Regulator

since April 2014

8© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

The Regulator – more detail

9

What the Regulator requires (some excerpts)

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Technical provisions should represent a target reserve to hold against a scheme’s future

liabilities calculated using assumptions that have been chosen prudently, taking into

account the degree to which the employer covenant can support a range of likely adverse

outcomes.

Source: tPR – code of practice para 117

A recovery plan should be appropriate. Its structure is fundamental. …. When setting the plan

structure trustees should recognise that the time taken for the scheme to meet its technical

provisions represents a period over which the trustees and employer may have agreed to accept

a risk level higher than that of the technical provisions. The level of risk accepted should depend

on the overall funding and security arrangements agreed.

Source: tPR – code of practice para 140 & 141

Trustees should understand the size and likelihood of risk (for both the scheme and

employer over time) inherent in a proposed investment strategy. Risk should be assessed

relative to the employer’s ability to support the likely adverse outcomes identified.

Source: tPR – code of practice para 117

Stakeholder: Pension Protection Fund (PPF)

The PPF compensation is almost always lower than the benefits

members were originally promised from their employer’s scheme.

People not yet drawing a pension receive 90% of what they were

promised.

Pensions are subject to an upper limit depending on age.

Pension increases will be lower for most people.

The compensation

When the company becomes insolvent, the PPF takes over the

assets of the scheme. Usually, this is not enough to pay out all

the compensation, so the difference is made up by a levy on all

pension schemes eligible for entry into the PPF.

PPF levies

The PPF was set up in 2005 to pay compensation to members of

defined benefit pension schemes when:

the company is insolvent, and

the scheme does not have enough money to buy annuities with an

insurer.

What is it?

10© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Stakeholders: employers

11© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

To support and fund the scheme (pay contributions and comply with the

Rules)

To provide a good quality pension scheme enabling staff to retire

To ensure that the cost profile remains within an acceptable range:

HE funding

Globally mobile student population

Different employers have different pressures, yet they all pay the same rate

Balance the needs for cash for different uses

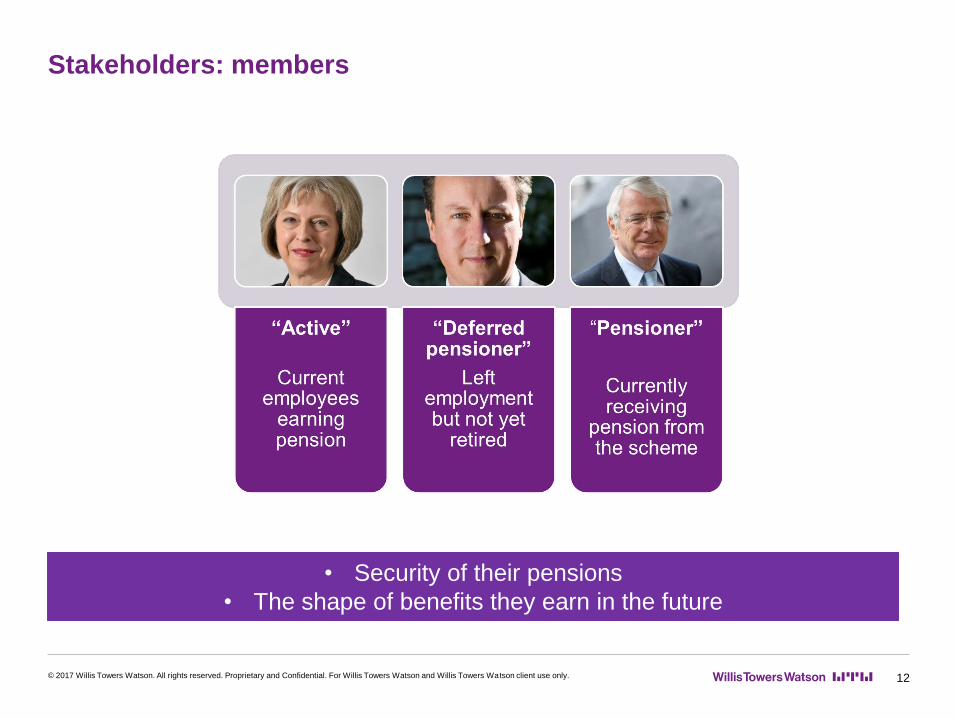

Stakeholders: members

12© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

• Security of their pensions

• The shape of benefits they earn in the future

Investment performance: what’s the issue

13

Equity markets

Returns have been positive over the last three years

So why is there a deficit?

Gilt yields

Have fallen dramatically since 2014

Index linked gilts are more relevant for USS: 3% fall

Generally speaking pensions are like long term index linked gilts

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

It’s not just about bond yields

14

Investment strategy is about balancing risk and return

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

By how much will USS investment returns beat gilt returns in the long run?

By the same amount as 2014: 1.15%

By less than 2014?

By more than 2014? (e.g. 1.41% as per the preliminary results or higher gilts

+1.85% per First Actuarial)

How prudent would you be?

What will the Regulator accept given its guidance?

USS final assumptions < 1.41% USS does not mechanistically use a gilts + approach but has used a

fundamental building block approach. Measuring as “ gilts +” gives a yard

stick to compare assumptions

UK mortality improvements – recent trends

15

Rapid increase in life expectancy

since the 1980s

Rapid decline in annual death

numbers since the 1980s

(England & Wales)

65

70

75

80

85

Males Females

Source: ONS National Life Tables

Cohort effect

In the UK, we know that different birth year groups

(cohorts) have experienced different changes in

longevity over time due to social, medical and

economic factors

Recent mortality shock

Since 2011, mortality improvements have stalled

and death numbers have increased sharply.

Is this a blip or the start of a new trend?

Source: ONS, England and Wales death registrations

460,000

480,000

500,000

520,000

540,000

560,000

580,000

600,000

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

USS valuation results

16

…so far

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Preliminary Revised

Liabilities £65.1bn £67.5bn

Assets £60.0bn £60.0bn

Deficit £5.1bn £7.5bn

Joint future

service cost

30.5% ~33.5%

Self sufficiency: deficit of £22.6bn. This means USS needs £82.6bn if it were to “stand

alone” and almost never ask employers for future deficit payments

Best estimate: surplus £8.3bn

USS has more than 50/50 chance of paying benefits from existing assets but

not enough assets to be certain “enough”

Future contributions need to increase to maintain that “certainty”

Why has the cost of future service increased so much

17

As well as the deficit

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Bond prices

“Pensions are like bonds”

Over the last 3 years bond prices have increased by

40%

You’d expect the future service cost to increase by

the same amount (roughly)

…and it has (23.9% to 30.5%)

If you believe investment returns are lower going forward, you need to save

more now to deliver the same in the future

What if the future is brighter than expected

18© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Let’s assume that investment returns are better than expected: say we return to 2014 market

conditions

Pensioners, deferred and active members all receive their benefits when the fall due

The level of risk in future is within that which can be supported by employers

There is no call on the PPF

But benefits have been reformed further than they needed to have been

What if USS assumptions are true

19© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Let’s assume that investment returns are as expected: USS have made the “right”

assumptions

Pensioners, deferred and active members all receive their benefits when the fall due

The level of risk in future is within that which can be supported by employers

There is no call on the PPF

But benefits have been reformed

What if the future is bleaker

20© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Let’s assume that yields do not revert as USS assume: the contribution rate for future service

could be a further 6% higher and the deficit is a further £4bn higher

Can the sector afford this? Or would only some institutions afford it

What would happen to those that could not?

Would all members get their benefits or would the PPF be involved (PPF benefits are smaller than

USS benefits)

Nobody knows what the future holds

21

Pensions are long term promises

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Unexpected things can occur that mean the future is different to expectations:

Brexit: unexpected referendum result

The last General Election (not the expected outcome!)

Political weakness in Spain, Germany and Ireland

Improvements in longevity: historically underestimated and not tailing off. Closely related to

future advances in medical care & treatment. This is complex in itself as it is a mix of research

and affordability of treatment

Bond yields are a key driver, but who knows when and if they will increase

Beware of “certainties”: they are almost always uncertain!

What does the future hold for the UK HE sector in a “ global” market?

Very many uncertainties and the Regulatory framework urges caution and

prudence to protect what has been built up already

How is the private sector reacting?

22

…. That operate within the same Regulatory framework

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Private sector have typically reformed but those schemes are now closing.

These schemes share the same Regulatory framework as USS.

The (reformed) public sector schemes continue to offer defined benefit.

Questions

23© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

?

Limitations

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only. 24

This document has been prepared for your sole and exclusive use and on the basis agreed with you. It was not

prepared for use by any other party and may not address their needs, concerns or objectives. As such this document

should not be disclosed to any third party other than in accordance with the terms of engagement agreed with you, or

with our specific written consent.. Unless otherwise specifically agreed in writing we assume no responsibility, duty of

care or liability to any third party who may gain access to a copy of this document and any such reliance that they may

place on it is entirely at their own risk.

This presentation was prepared for the University of Kent under the terms of our engagement with you. It may not be

suitable for use in any other context or for any other purpose and we accept no responsibility for any such use.

The assumptions made about future economic and demographic conditions are precisely that; they are assumptions,

and not predictions or guarantees. They provide, we believe, a reasonable basis on which the Company can formulate

their policy, but they must be aware that there are uncertainties and risks involved in any course of action. There is no

guarantee that the assumptions made will be borne out in practice, and the expectation is that in actuality the

Scheme’s experience will, from time to time, be better or worse than that assumed.

We have relied on information provided to us by third parties. Whilst reasonable care has been taken to gauge the

reliability of this information, this material carried no guarantee of accuracy or completeness and Willis Towers Watson

cannot be held accountable for the misrepresentation of data by third parties involved.

Towers Watson Limited is authorised and regulated by the Financial Conduct Authority