39

The 40 th Quarterly C-Suite Survey: Federal Election, Interest Rates, Oil Prices and Trade September 28, 2015 Sponsored by: Published and broadcast by:

The 40th Quarterly C-Suite Survey:Federal Election, Interest Rates, Oil Prices and Trade

September 28, 2015

Sponsored by:

Published and broadcast by:

2222

Introduction

Methodology: telephone interviews with 152 C-Suite executives fromROB1000 companies between August 24th and September 18th, 2015.

This survey quarter’s survey asked the C-Suite about:

The state of the Canadian economy Monetary and fiscal policy responses to the recession Opinion about the Federal Election: what the parties and leaders should be

discussing Attitudes to foreign markets, trade promotion & supply management

3

Key Findings

Recent C-Suite surveys signaled concern about the broader impact ofthe downturn in the oil & gas sector.

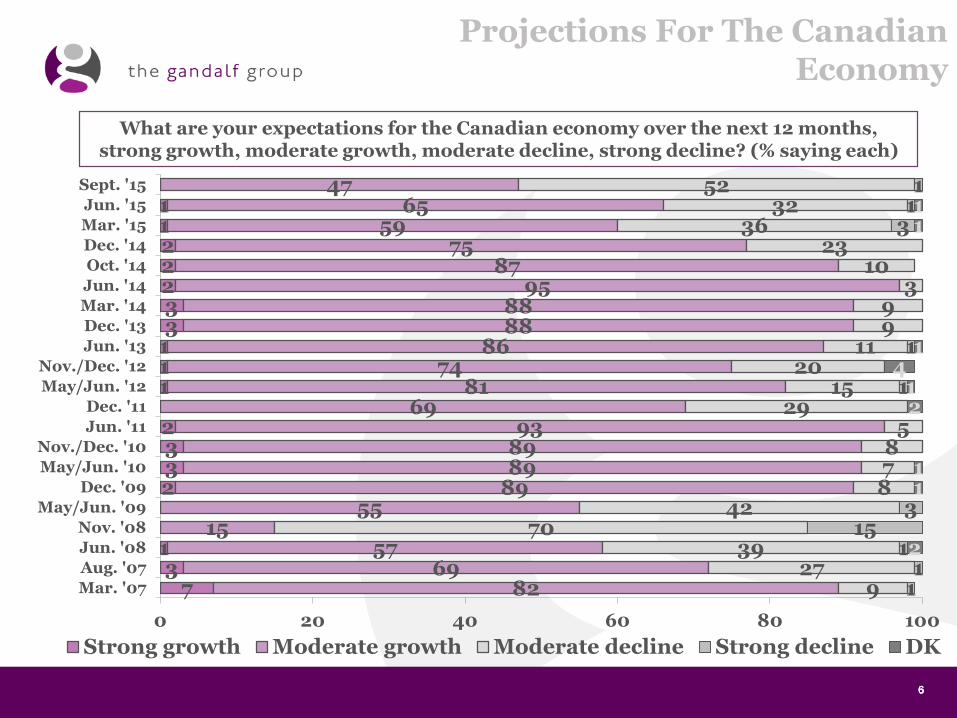

However this quarter we see a pronounced lack of confidence in theeconomy, with a 20-point drop in the number of executives who expectCanada’s economy to grow.

This is undoubtedly tied to the oil and gas sector. Far fewer thisquarter are predicting the benchmark North American price for oil willreturn to $70 or higher in the next 12 months.

Four in ten agreed that Canada is not only in a technical recession but one that will last through to the end of 2015.

Other executives – whether they agreed or disagreed that Canada is in a technical recession – are still dissatisfied with current growth rates and any economic growth will be grudging going forward.

4

Key Findings

The C-Suite thinks the economy is far and away the biggest issue thatleaders and parties should be prioritizing in this election.

There is good support for monetary or fiscal stimulus to help grow theeconomy.

Few expressed opposition to the Bank of Canada’s recent rate cut.

There is modest concern that a new government would reverse recenttax cuts.

Where there is more debate is on the question of whether the federalgovernment should exercise spending restraint with a view tobalancing the budget.

Those who take this view were more likely to favour using monetarypolicy over fiscal policy to assist the economy. However nearly half ofthe C-Suite believes restraint should not be the order of the day andthat spending on stimulus or infrastructure is in order.

5

Assessments of the Economy

Oil prices have been depressed since the beginning of 2015, yet theoutlook for Canada’s economy is worse now than it was in surveysconducted in the first two quarters of 2015.

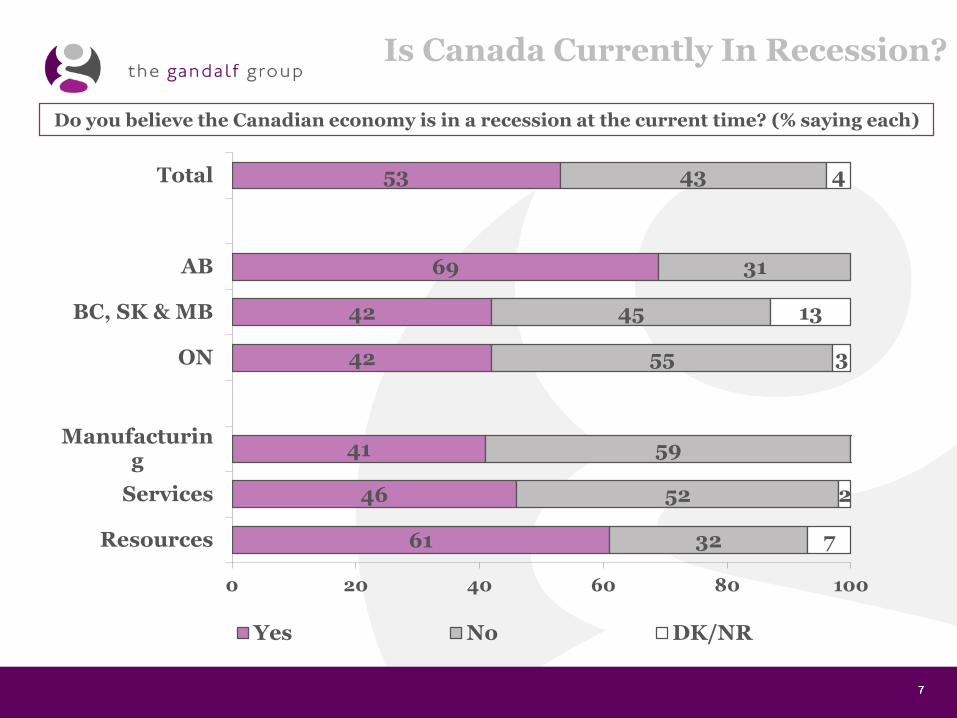

There is no consensus as to whether Canada is in recession.

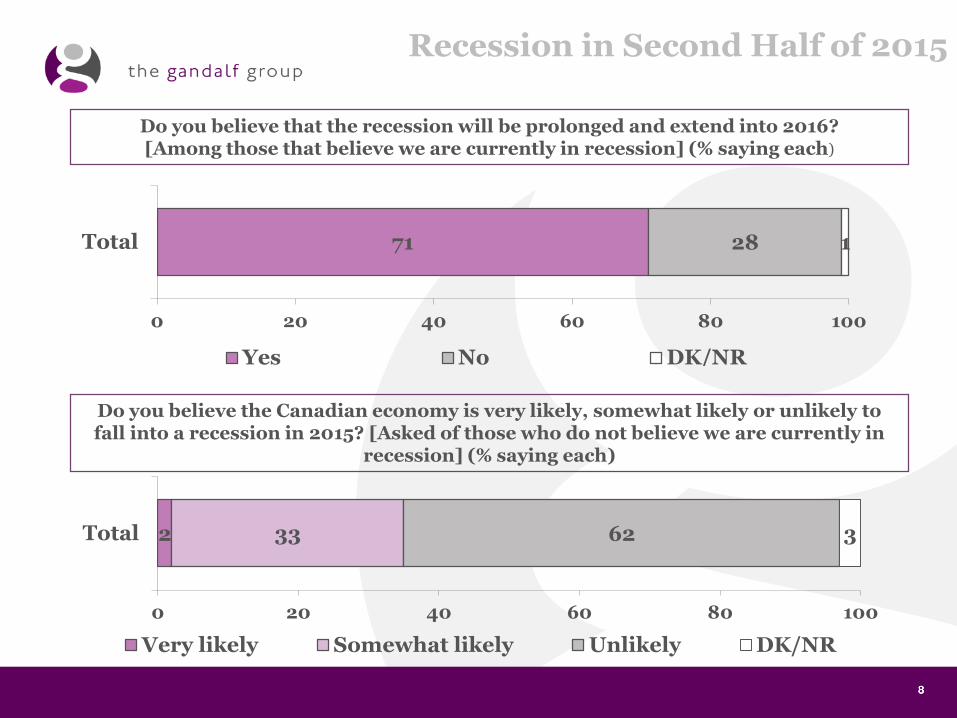

Fifty-three percent of the C-Suite believes Canada is in a recession. Most whosaid Canada is in recession agreed it will extend into 2016, but some believethe economy will rebound.

Many disagree with the premise that the contraction in Canada’s economy islimited to the oil and gas sector. However those who believe the economy isgrowing were more likely to agree the contraction is confined to oil & gas.

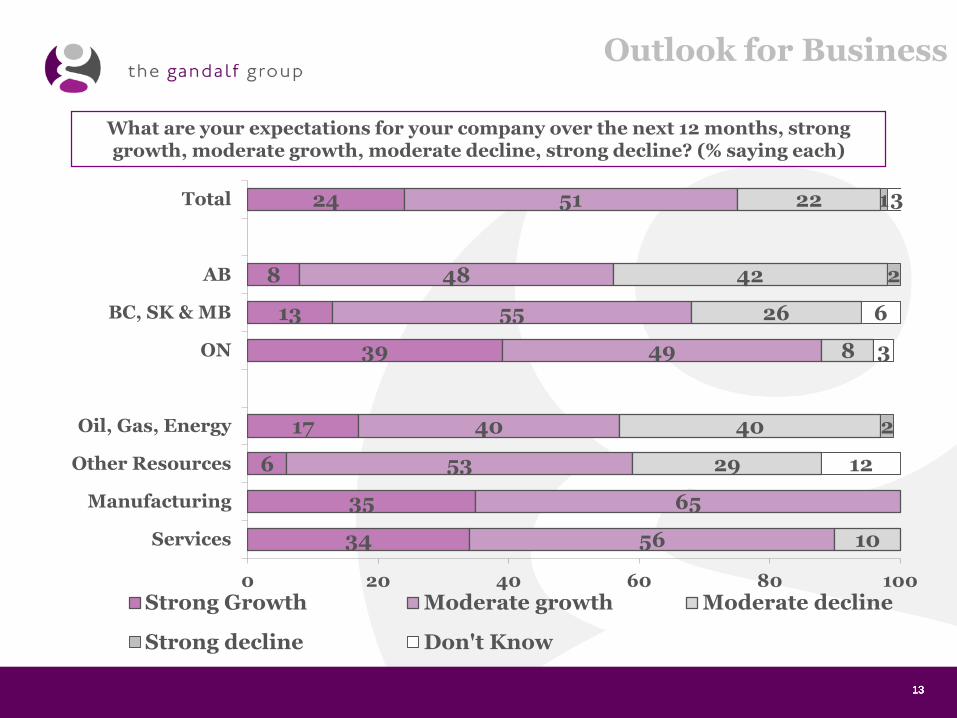

Most executives still expect their business will grow over the next 12 mos., butthe number has declined slightly – as many as one in five now expects theirbusiness will not grow over the next 12 mos.

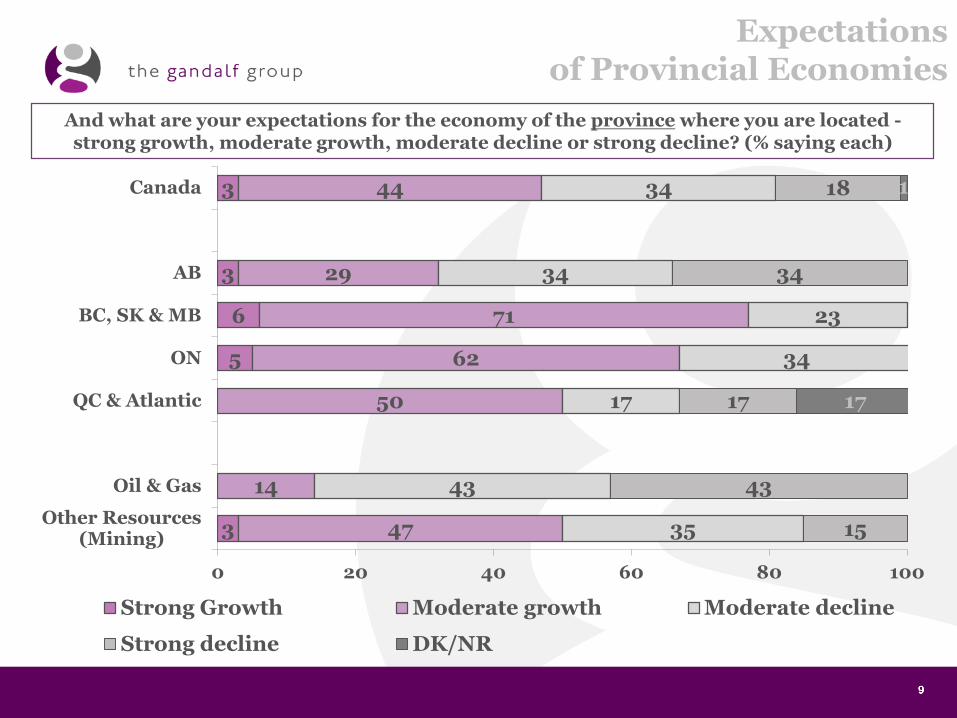

The outlook is most pessimistic in Alberta and among resources/oil & gascos.; and relatively positive in Ontario.

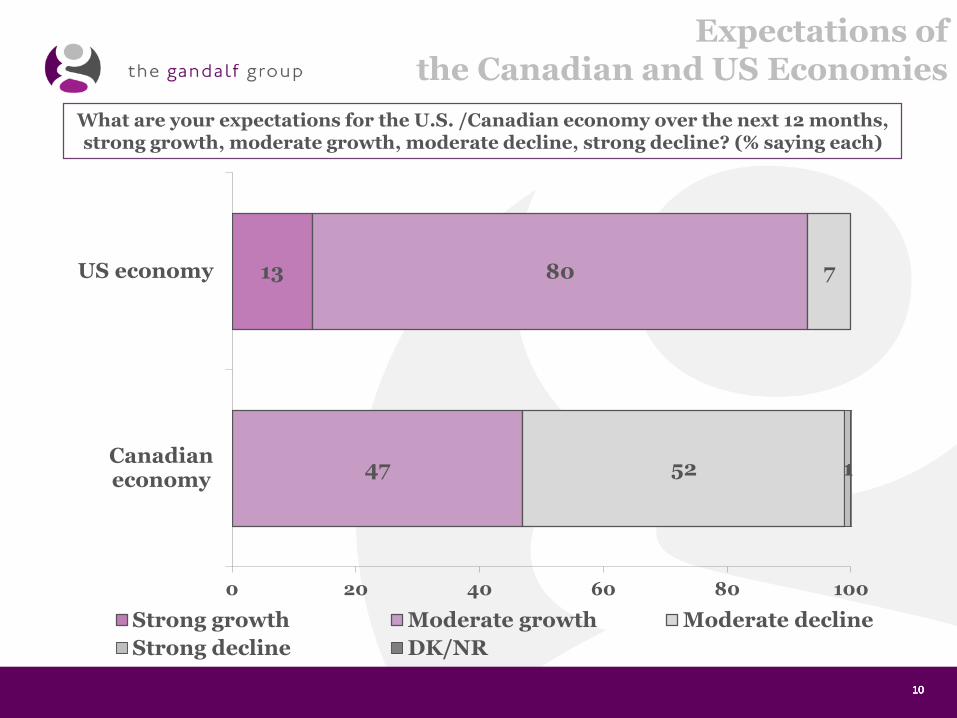

The outlook for the US economy is far better than the outlook for Canada’s.

6666

Projections For The Canadian Economy

What are your expectations for the Canadian economy over the next 12 months, strong growth, moderate growth, moderate decline, strong decline? (% saying each)

73

1

2332

1113322211

8269

5715

5589898993

6981

7486

8888

9587

7559

6547

927

3970

42878

529

1520

1199

310

2336

3252

11

115

3

1

1

311

2

11

21

41

11

0 20 40 60 80 100

Mar. '07

Aug. '07

Jun. '08

Nov. '08

May/Jun. '09

Dec. '09

May/Jun. '10

Nov./Dec. '10

Jun. '11

Dec. '11

May/Jun. '12

Nov./Dec. '12

Jun. '13

Dec. '13

Mar. '14

Jun. '14

Oct. '14

Dec. '14

Mar. '15

Jun. '15

Sept. '15

Strong growth Moderate growth Moderate decline Strong decline DK

7777

Is Canada Currently In Recession?

53

69

42

42

41

46

61

43

31

45

55

59

52

32

4

13

3

2

7

0 20 40 60 80 100

Total

AB

BC, SK & MB

ON

Manufacturing

Services

Resources

Yes No DK/NR

Do you believe the Canadian economy is in a recession at the current time? (% saying each)

8888

Recession in Second Half of 2015

71 28 1

0 20 40 60 80 100

Total

Yes No DK/NR

Do you believe that the recession will be prolonged and extend into 2016?[Among those that believe we are currently in recession] (% saying each)

2 33 62 3

0 20 40 60 80 100

Total

Very likely Somewhat likely Unlikely DK/NR

Do you believe the Canadian economy is very likely, somewhat likely or unlikely to fall into a recession in 2015? [Asked of those who do not believe we are currently in

recession] (% saying each)

9999

Expectationsof Provincial Economies

3

3

6

5

3

44

29

71

62

50

14

47

34

34

23

34

17

43

35

18

34

17

43

15

1

17

0 20 40 60 80 100

Canada

AB

BC, SK & MB

ON

QC & Atlantic

Oil & Gas

Other Resources(Mining)

Strong Growth Moderate growth Moderate decline

Strong decline DK/NR

And what are your expectations for the economy of the province where you are located -strong growth, moderate growth, moderate decline or strong decline? (% saying each)

10101010

Expectations ofthe Canadian and US Economies

13 80

47

7

52 1

0 20 40 60 80 100

US economy

Canadianeconomy

Strong growth Moderate growth Moderate decline

Strong decline DK/NR

What are your expectations for the U.S. /Canadian economy over the next 12 months, strong growth, moderate growth, moderate decline, strong decline? (% saying each)

11111111

Contraction is Confined to Oil & Gas

42

64

23

56

35

75

2

2

1

0 20 40 60 80 100

Total

Economy isnot in

recession

Economy is inrecession

Agree Disagree DK/NR

Would you agree or disagree with the following statement? “The economic contraction in the Canadian economy is exclusively in the energy sector, while the

rest of the economy is growing.” (% saying each)

12

Growth for Businesses

Most executives with ROB1000 companies still expect their businesseswill grow. That number has declined only slightly since last quarter.

23% said their business will not grow over the next 12 mos. – up 4 pointssince last quarter.

24

8

13

39

17

6

35

34

51

48

55

49

40

53

65

56

22

42

26

8

40

29

10

1

2

2

3

6

3

12

0 20 40 60 80 100

Total

AB

BC, SK & MB

ON

Oil, Gas, Energy

Other Resources

Manufacturing

Services

Strong Growth Moderate growth Moderate decline

Strong decline Don't Know

13131313

Outlook for Business

What are your expectations for your company over the next 12 months, strong growth, moderate growth, moderate decline, strong decline? (% saying each)

14

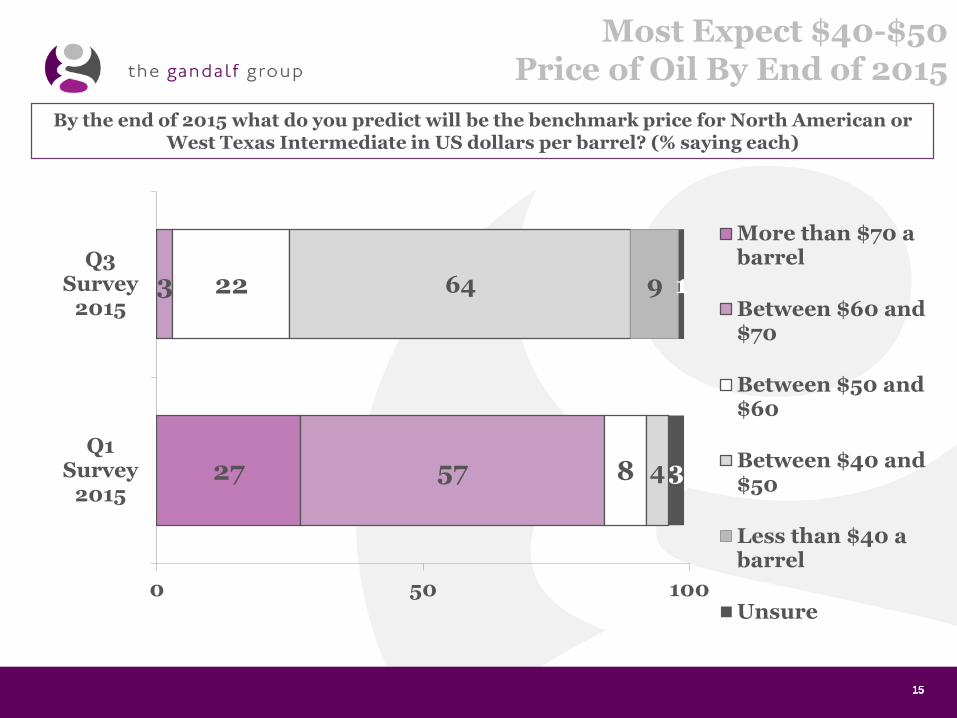

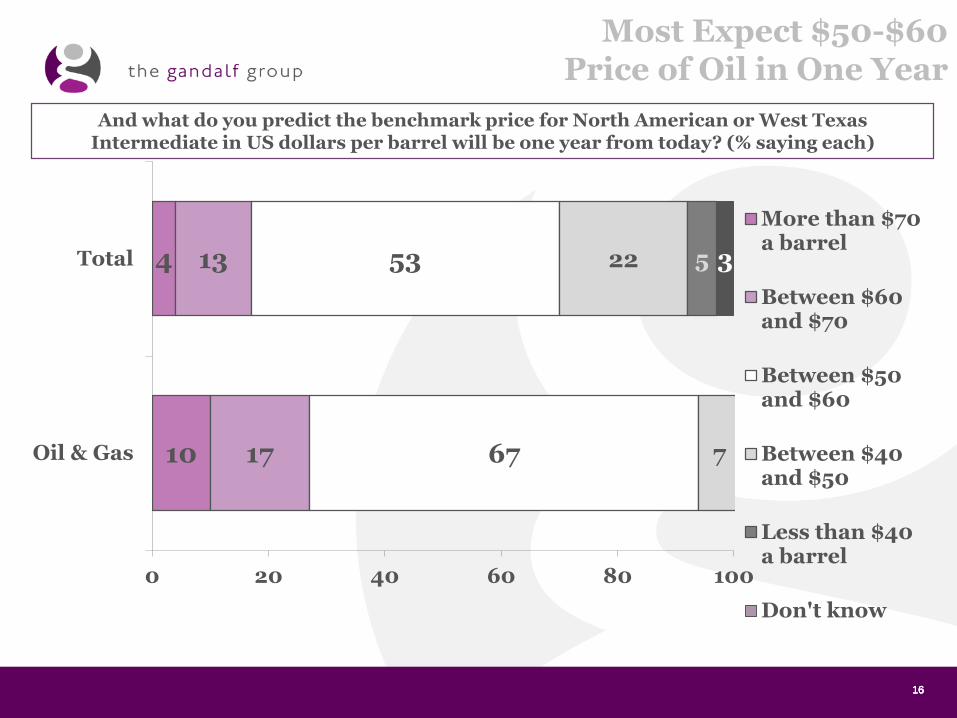

Expectations for Oil Prices

Explaining much of the slide in opinion about the economy is the clearsense that oil prices will remain depressed into 2016.

Last quarter most executives believed the price for WTI crude would exceedUS$60 a barrel.

Now virtually none expect this, and most expect prices to stay below $50 abarrel until the end of the year:

• only 25% expect prices to exceed $50 a barrel;

• among oil & gas executives 31% expect prices to exceed $50.

The outlook is only somewhat better for 2016 – but few expect oil toreturn to prices of 2015.

Most believe prices will be below $60 in a year’s time;

17% expect prices could exceed $60 in a year.

Oil & gas executives are somewhat more likely to predict WTI oil pricesreaching $60 or $70.

15151515

Most Expect $40-$50 Price of Oil By End of 2015

27

3

57

22

8

64

4

9 1

3

0 50 100

Q3Survey

2015

Q1Survey

2015

More than $70 abarrel

Between $60 and$70

Between $50 and$60

Between $40 and$50

Less than $40 abarrel

Unsure

By the end of 2015 what do you predict will be the benchmark price for North American or West Texas Intermediate in US dollars per barrel? (% saying each)

16161616

Most Expect $50-$60 Price of Oil in One Year

And what do you predict the benchmark price for North American or West Texas Intermediate in US dollars per barrel will be one year from today? (% saying each)

4

10

13

17

53

67

22

7

5 3

0 20 40 60 80 100

Total

Oil & Gas

More than $70a barrel

Between $60and $70

Between $50and $60

Between $40and $50

Less than $40a barrel

Don't know

17

Low Oil Prices

Very few companies in any region in Canada said they stand to benefitif oil prices stay at current levels until the end of 2015:

40% said there would be no impact or a neutral impact on their business

39% said it would have a very or somewhat negative impact.

18181818

Impact if Oil Prices Stay at Current Levels Until the end of 2015

5

2

3

6

15

6

19

14

40

23

42

57

28

38

29

22

11

31

3

2

1

3

0 20 40 60 80 100

Total

AB

BC, SK & MB

ON

Very positive Somewhat positive Neutral

Somewhat negative Very negative DK/NR

Since the price of oil has dropped significantly over the past year, what would be the impact on your company if oil prices stay at current levels until the end of 2015? Would it be a

positive for your company or negative for your company or neutral? (% saying each)

19

Monetary & Fiscal Policy

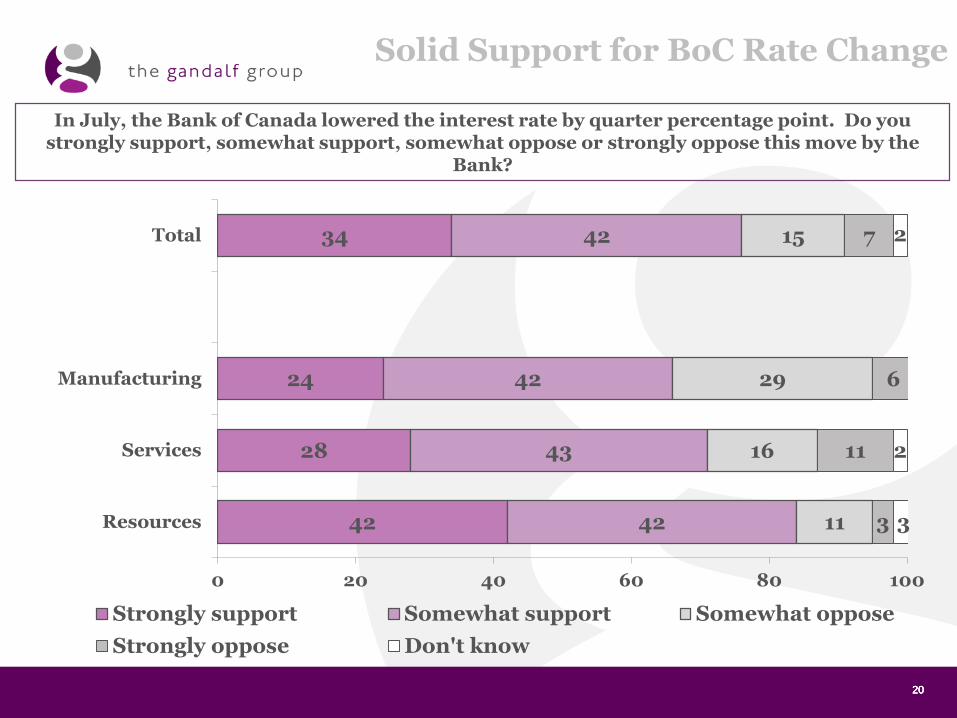

Three quarters of executives support the Bank of Canada’s recent(July) cut to the prime lending rate. In our March 2015 survey onlyhalf said they supported the idea of an additional rate cut.

Support is highest among Resources sector executives, and opposition to thisis mostly not strong opposition.

There is very little difference between executives who think the country is inrecession and those who think it is growing: 72% of those who said theeconomy is growing supported the rate cut. A sign perhaps of how any growththat Canada is experiencing is likely to be moderate growth.

20202020

Solid Support for BoC Rate Change

34

24

28

42

42

42

43

42

15

29

16

11

7

6

11

3

2

2

3

0 20 40 60 80 100

Total

Manufacturing

Services

Resources

Strongly support Somewhat support Somewhat oppose

Strongly oppose Don't know

In July, the Bank of Canada lowered the interest rate by quarter percentage point. Do you strongly support, somewhat support, somewhat oppose or strongly oppose this move by the

Bank?

21212121

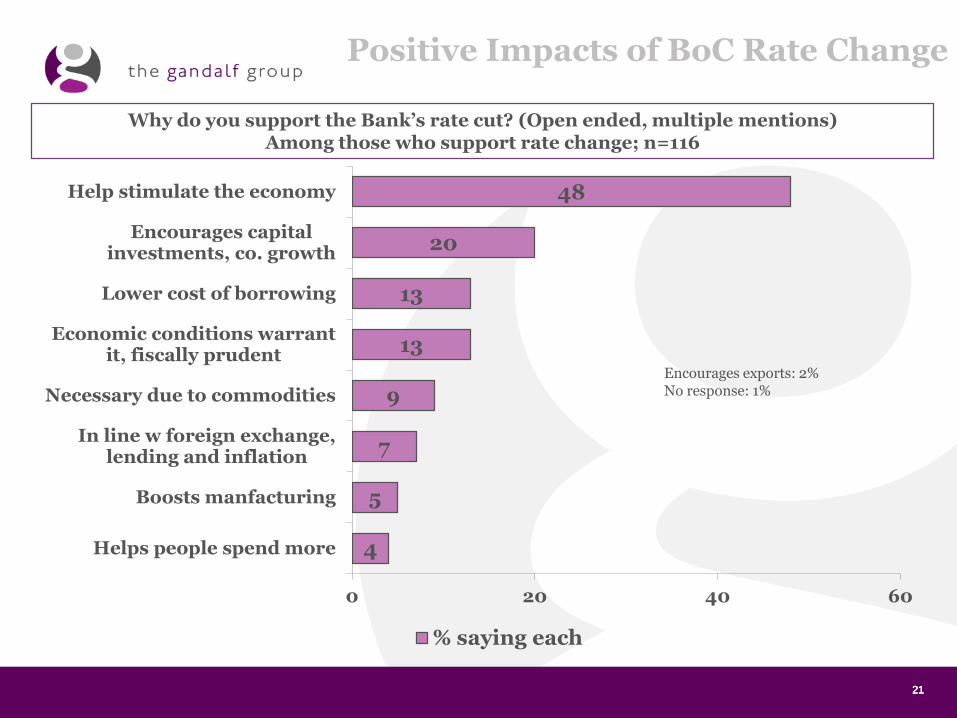

Positive Impacts of BoC Rate Change

48

20

13

13

9

7

5

4

0 20 40 60

Help stimulate the economy

Encourages capitalinvestments, co. growth

Lower cost of borrowing

Economic conditions warrantit, fiscally prudent

Necessary due to commodities

In line w foreign exchange,lending and inflation

Boosts manfacturing

Helps people spend more

% saying each

Why do you support the Bank’s rate cut? (Open ended, multiple mentions) Among those who support rate change; n=116

Encourages exports: 2%No response: 1%

22222222

Negative Impacts of BoC Rate Change

33

33

27

24

12

0 10 20 30 40

Not effective long term

Devalues dollar

Encourages high debtlevels, hurts savers

Real estate bubble

Discouragesinvestment/saving

% saying each

What most concerns you about a rate cut? (Open ended, multiple mentions) Among those who oppose rate change; n=33

Other mentions include:

Negative impacts on pensioners: 6%

Negative impacts on financial/banking industry: 6%

23

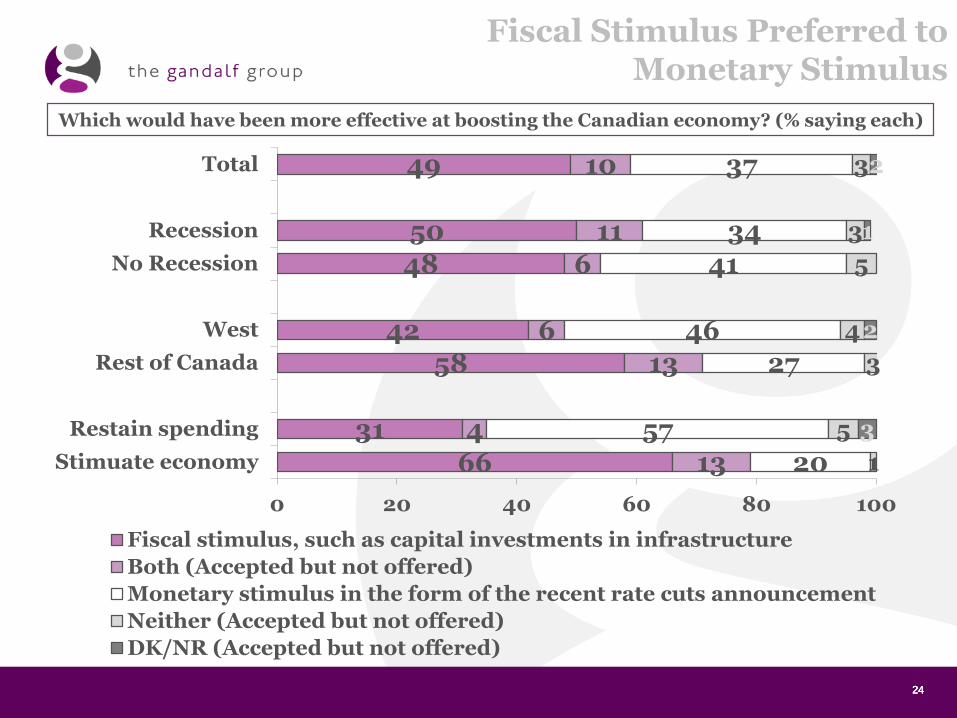

Monetary & Fiscal Policy

Executives tend to believe fiscal stimulus would be more effective atboosting the economy than monetary policy measures.

In a forced choice, 37% said monetary policy would be more effective, while49% said fiscal policy would be more effective.

In Ontario, Quebec and Atlantic Canada there is a strong preference for fiscalpolicy measures such as infrastructure.

Those who favour fiscal restraint (rather than fiscal stimulus) tend to believemonetary policy is more effective than fiscal policy measures when it comesto boosting the economy.

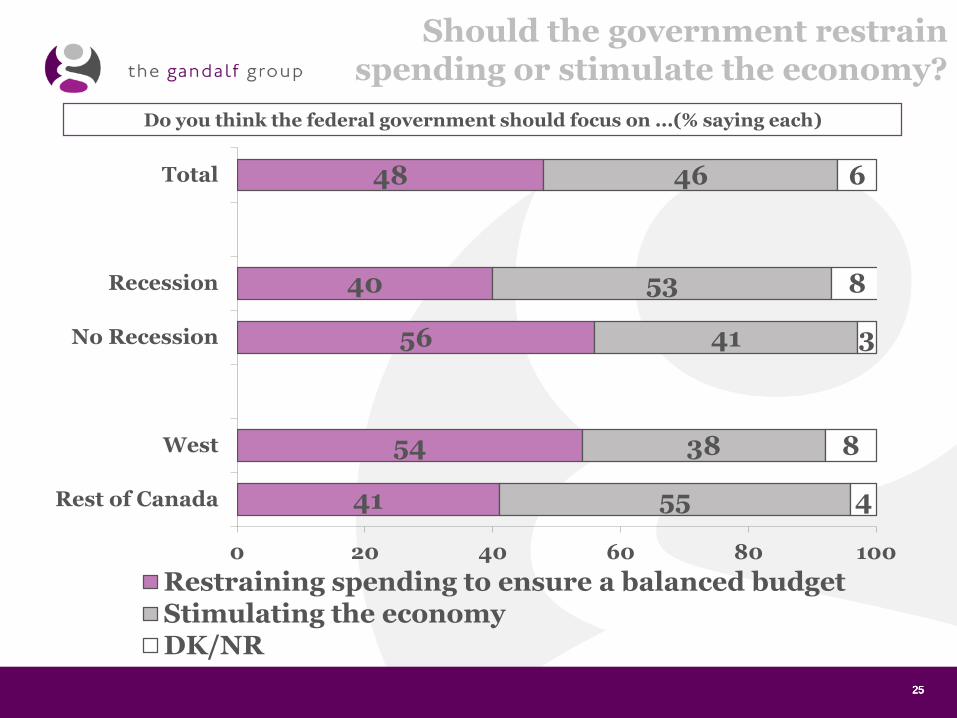

Respondents were split on whether the federal government shouldrestrain spending to run a balance budget or stimulating the economy.

In a forced choice: roughly half said government should restrain spending toensure a balanced budget; and half said the government should stimulate theeconomy instead.

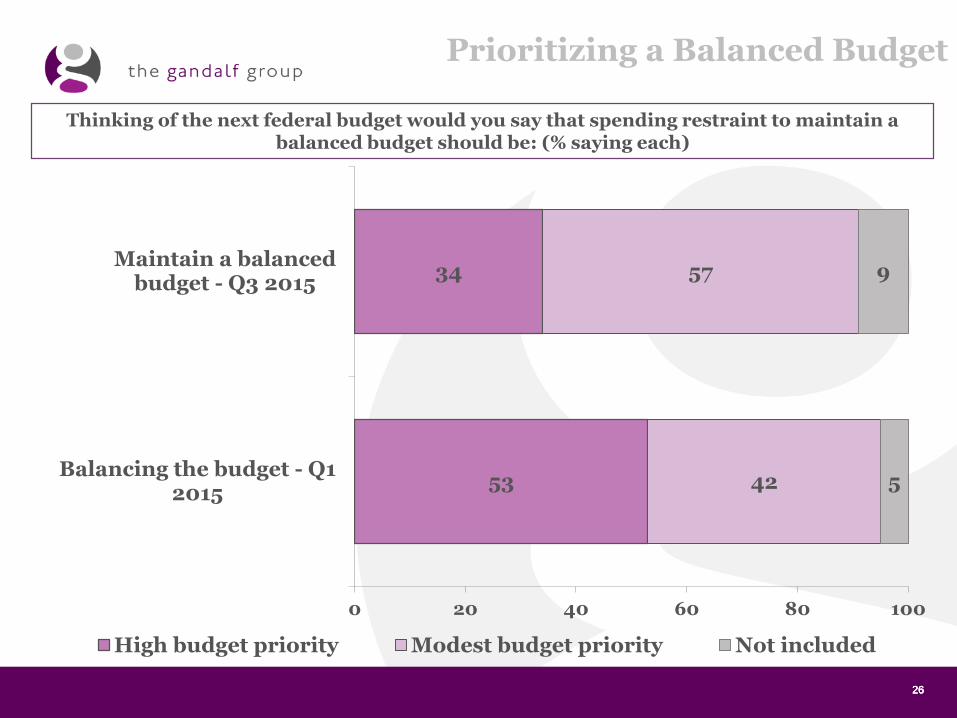

One third of executives said spending restraint to maintain a balancedbudget should be a high priority, down from 53% saying so in oursurvey in the first quarter of 2015.

24242424

Fiscal Stimulus Preferred to Monetary Stimulus

49

50

48

42

58

31

66

10

11

6

6

13

4

13

37

34

41

46

27

57

20

3

3

5

4

3

5

1

2

1

2

3

0 20 40 60 80 100

Total

Recession

No Recession

West

Rest of Canada

Restain spending

Stimuate economy

Fiscal stimulus, such as capital investments in infrastructure

Both (Accepted but not offered)

Monetary stimulus in the form of the recent rate cuts announcement

Neither (Accepted but not offered)

DK/NR (Accepted but not offered)

Which would have been more effective at boosting the Canadian economy? (% saying each)

25252525

Should the government restrain spending or stimulate the economy?

48

40

56

54

41

46

53

41

38

55

6

8

3

8

4

0 20 40 60 80 100

Total

Recession

No Recession

West

Rest of Canada

Restraining spending to ensure a balanced budgetStimulating the economyDK/NR

Do you think the federal government should focus on ...(% saying each)

26262626

Prioritizing a Balanced Budget

34

53

57

42

9

5

0 20 40 60 80 100

Maintain a balancedbudget - Q3 2015

Balancing the budget - Q12015

High budget priority Modest budget priority Not included

Thinking of the next federal budget would you say that spending restraint to maintain a balanced budget should be: (% saying each)

27

The Federal Election

Most executives said that the economy is the most important issue thatleaders and parties should be discussing in this election.

When asked what issues leaders and parties are not discussing weheard a range of issues.

No single issue such as the economy predominates, suggesting that theeconomy has been an important focus of debate so far.

Among the issues mentioned are employment and labour market concerns(as well as education), the environment, health care, defense, and issuesrelating to Aboriginal land and agreements.

28282828

The Economy is Most Important Issue in Federal Election

53

14

9

0 10 20 30 40 50 60

Economy (generalmention)

Economicgrowth/stimulus

Responsible fiscalspending

% saying each

What issue should be the most important issue that leaders and parties should be discussing in this election? (Open ended)

Other mentions include:

Energy: 3%Economy – employment/ job creation: 3%Economic diversification: 2%Economy – debt/deficit: 2%Immigration: 2%Infrastructure: 2%Good leadership: 2%Tax reform: 2%Don’t know/ No response: 3%

29292929

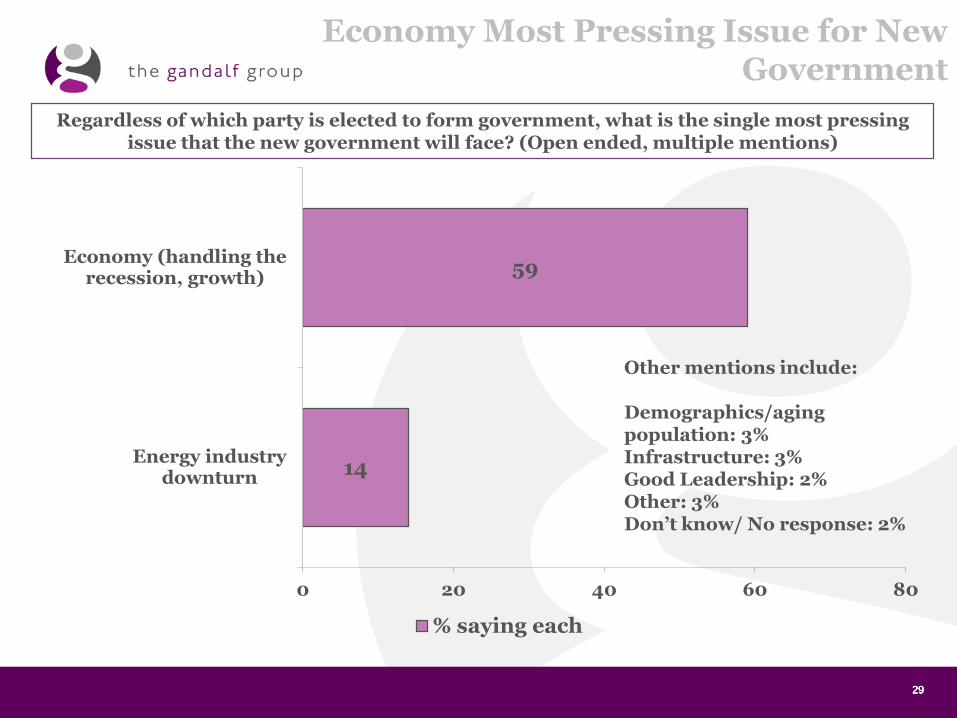

Economy Most Pressing Issue for New Government

59

14

0 20 40 60 80

Economy (handling therecession, growth)

Energy industrydownturn

% saying each

Regardless of which party is elected to form government, what is the single most pressing issue that the new government will face? (Open ended, multiple mentions)

Other mentions include:

Demographics/aging population: 3%Infrastructure: 3%Good Leadership: 2%Other: 3%Don’t know/ No response: 2%

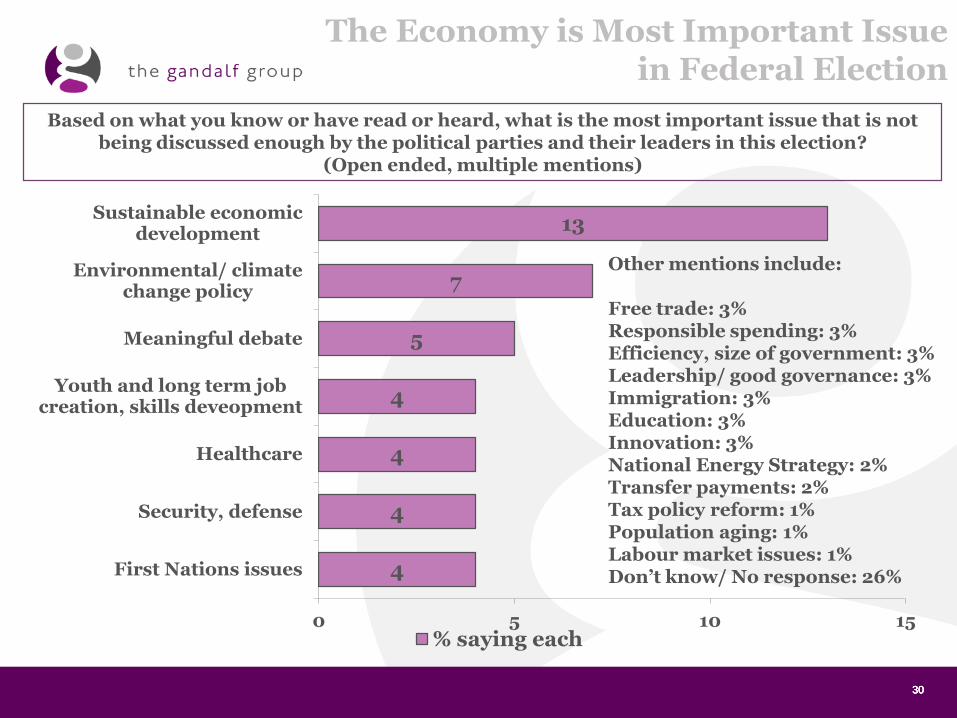

30303030

The Economy is Most Important Issue in Federal Election

13

7

5

4

4

4

4

0 5 10 15

Sustainable economicdevelopment

Environmental/ climatechange policy

Meaningful debate

Youth and long term jobcreation, skills deveopment

Healthcare

Security, defense

First Nations issues

% saying each

Based on what you know or have read or heard, what is the most important issue that is not being discussed enough by the political parties and their leaders in this election?

(Open ended, multiple mentions)

Other mentions include:

Free trade: 3%Responsible spending: 3%Efficiency, size of government: 3%Leadership/ good governance: 3%Immigration: 3%Education: 3%Innovation: 3%National Energy Strategy: 2%Transfer payments: 2%Tax policy reform: 1%Population aging: 1%Labour market issues: 1%Don’t know/ No response: 26%

31

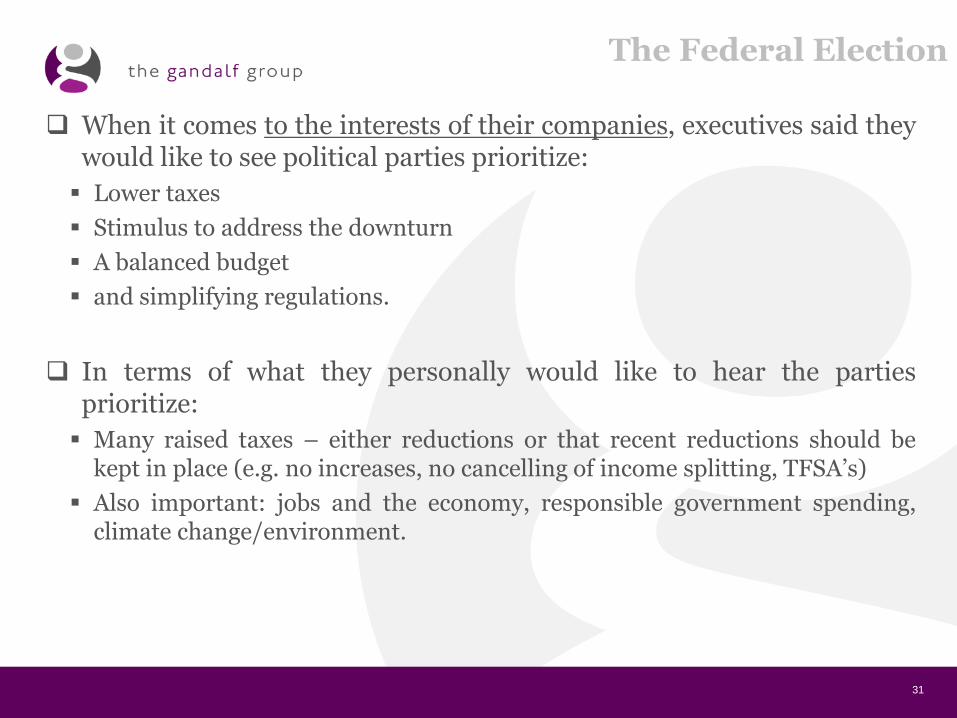

The Federal Election

When it comes to the interests of their companies, executives said theywould like to see political parties prioritize:

Lower taxes

Stimulus to address the downturn

A balanced budget

and simplifying regulations.

In terms of what they personally would like to hear the partiesprioritize:

Many raised taxes – either reductions or that recent reductions should bekept in place (e.g. no increases, no cancelling of income splitting, TFSA’s)

Also important: jobs and the economy, responsible government spending,climate change/environment.

32323232

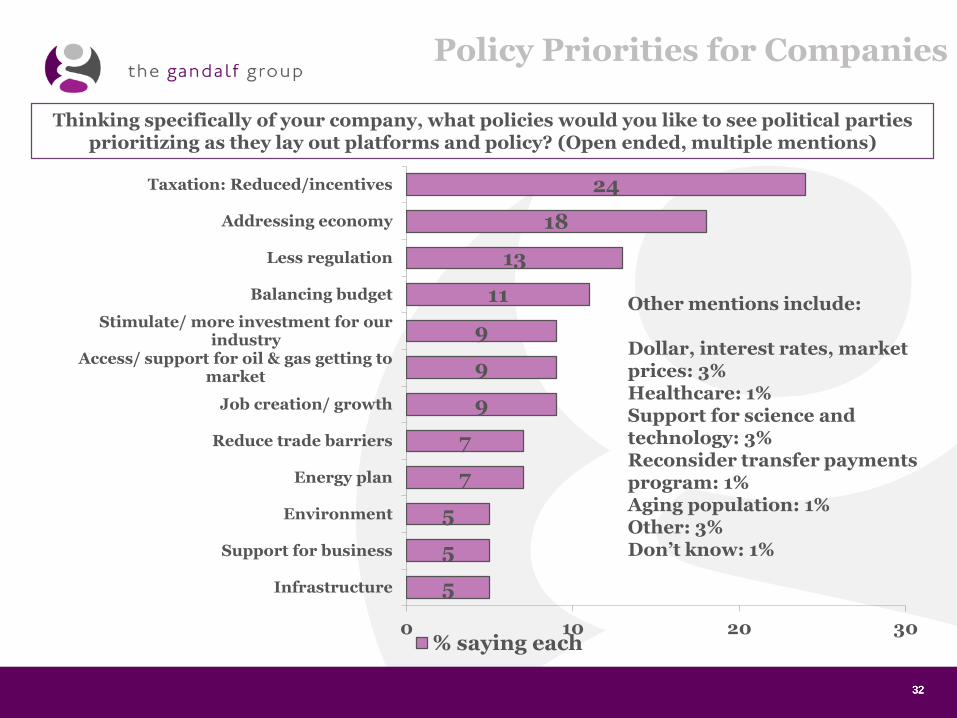

Policy Priorities for Companies

24

18

13

11

9

9

9

7

7

5

5

5

0 10 20 30

Taxation: Reduced/incentives

Addressing economy

Less regulation

Balancing budget

Stimulate/ more investment for ourindustry

Access/ support for oil & gas getting tomarket

Job creation/ growth

Reduce trade barriers

Energy plan

Environment

Support for business

Infrastructure

% saying each

Thinking specifically of your company, what policies would you like to see political parties prioritizing as they lay out platforms and policy? (Open ended, multiple mentions)

Other mentions include:

Dollar, interest rates, market prices: 3%Healthcare: 1%Support for science and technology: 3%Reconsider transfer payments program: 1%Aging population: 1%Other: 3%Don’t know: 1%

33333333

Personal Policy Priorities for Executives

26

13

12

11

8

8

7

4

0 10 20 30

Taxes/Stable tax rates

Balancing budget

Economic growth

Job creation

Healthcare

Immigration

Climate change/environment

Energy plan

% saying each

And now thinking not about your company but your own personal concerns or perspective, are there other policies you would like to see political parties prioritizing as they lay out

platforms and policy? (Open ended, multiple mentions)

Other mentions include:

Infrastructure: 3%Transportation/ transit infrastructure: 3%Investments in R&D: 3%Defense/ security: 3%Improved relationships with First Nations: 3%Foreign policy: 3%Housing: 2%Homelessness and poverty: 2%Education: 3%Household debt: 2%

34

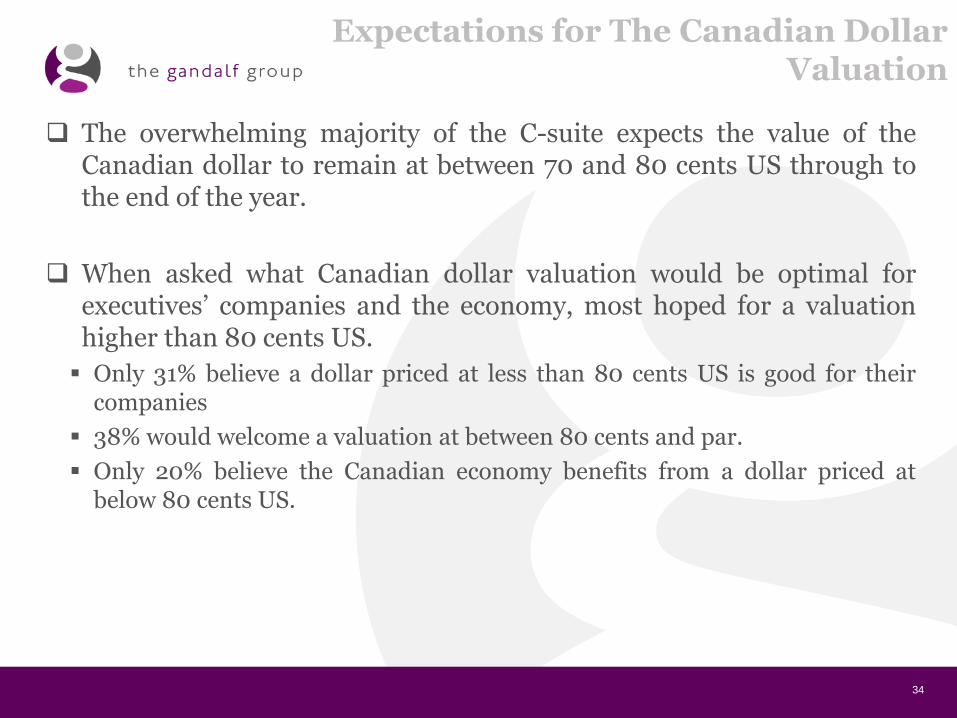

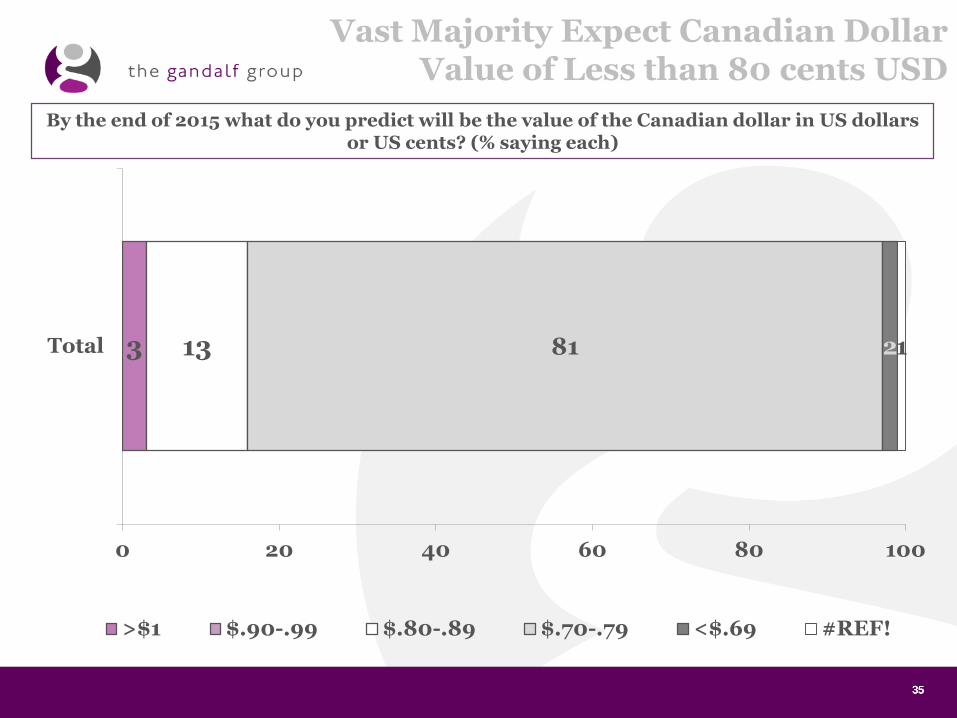

Expectations for The Canadian Dollar Valuation

The overwhelming majority of the C-suite expects the value of theCanadian dollar to remain at between 70 and 80 cents US through tothe end of the year.

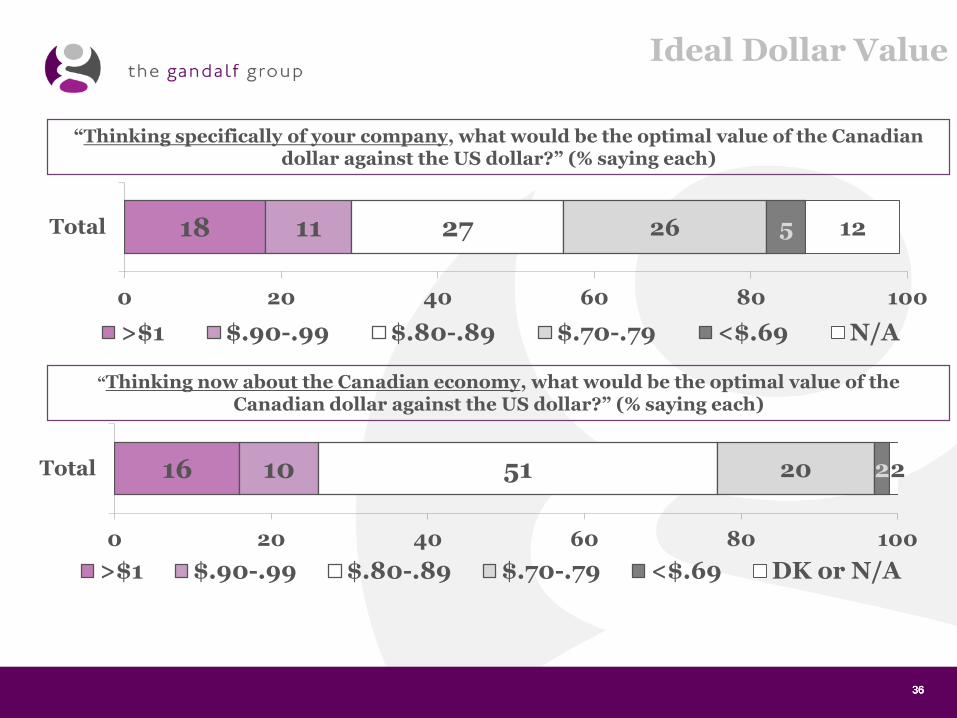

When asked what Canadian dollar valuation would be optimal forexecutives’ companies and the economy, most hoped for a valuationhigher than 80 cents US.

Only 31% believe a dollar priced at less than 80 cents US is good for theircompanies

38% would welcome a valuation at between 80 cents and par.

Only 20% believe the Canadian economy benefits from a dollar priced atbelow 80 cents US.

35353535

Vast Majority Expect Canadian Dollar Value of Less than 80 cents USD

By the end of 2015 what do you predict will be the value of the Canadian dollar in US dollars or US cents? (% saying each)

3 13 81 21

0 20 40 60 80 100

Total

>$1 $.90-.99 $.80-.89 $.70-.79 <$.69 #REF!

36363636

Ideal Dollar Value

18 11 27 26 5 12

0 20 40 60 80 100

Total

>$1 $.90-.99 $.80-.89 $.70-.79 <$.69 N/A

“Thinking now about the Canadian economy, what would be the optimal value of the Canadian dollar against the US dollar?” (% saying each)

16 10 51 20 22

0 20 40 60 80 100

Total

>$1 $.90-.99 $.80-.89 $.70-.79 <$.69 DK or N/A

“Thinking specifically of your company, what would be the optimal value of the Canadian dollar against the US dollar?” (% saying each)

37

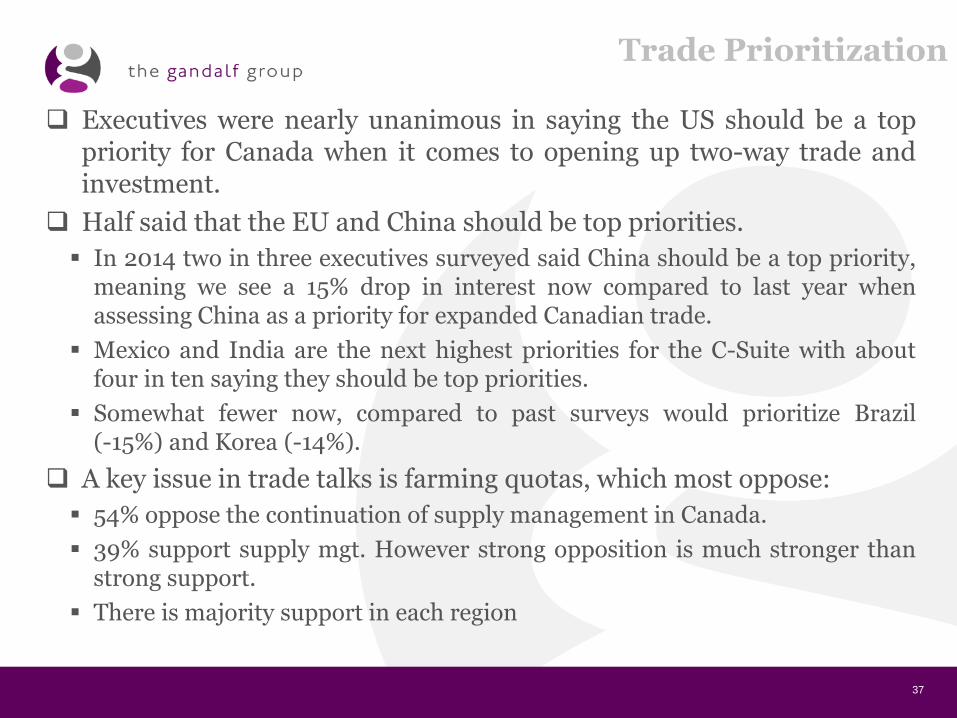

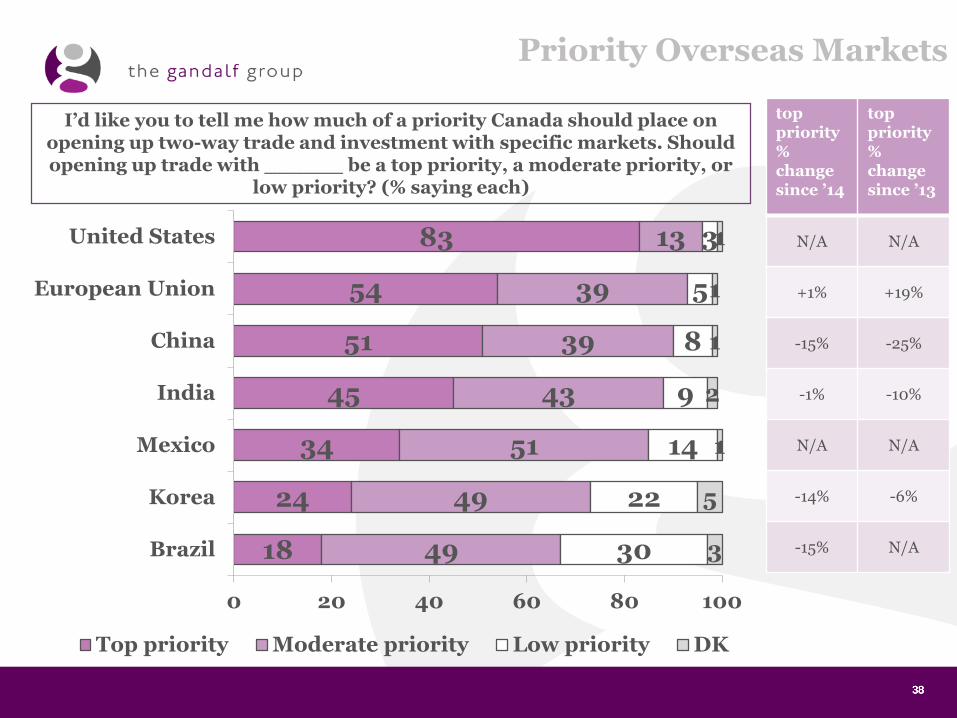

Trade Prioritization

Executives were nearly unanimous in saying the US should be a toppriority for Canada when it comes to opening up two-way trade andinvestment.

Half said that the EU and China should be top priorities.

In 2014 two in three executives surveyed said China should be a top priority,meaning we see a 15% drop in interest now compared to last year whenassessing China as a priority for expanded Canadian trade.

Mexico and India are the next highest priorities for the C-Suite with aboutfour in ten saying they should be top priorities.

Somewhat fewer now, compared to past surveys would prioritize Brazil(-15%) and Korea (-14%).

A key issue in trade talks is farming quotas, which most oppose:

54% oppose the continuation of supply management in Canada.

39% support supply mgt. However strong opposition is much stronger thanstrong support.

There is majority support in each region

38383838

Priority Overseas Markets

83

54

51

45

34

24

18

13

39

39

43

51

49

49

3

5

8

9

14

22

30

1

1

1

2

1

5

3

0 20 40 60 80 100

United States

European Union

China

India

Mexico

Korea

Brazil

Top priority Moderate priority Low priority DK

I’d like you to tell me how much of a priority Canada should place on opening up two-way trade and investment with specific markets. Should opening up trade with ______ be a top priority, a moderate priority, or

low priority? (% saying each)

top priority % changesince ’14

top priority % changesince ’13

N/A N/A

+1% +19%

-15% -25%

-1% -10%

N/A N/A

-14% -6%

-15% N/A

39393939

Supply Management

9 30 24 30 8Total

Strongly support Somewhat support Somewhat oppose

Strongly oppose DK/NR

Do you support or oppose the continuation of supply management in Canada? This is the policy that controls the price of agricultural products and agrifood through marketing

boards and limits imports with tariffs. (if support/oppose) Would that be: (% saying each)