38

ENERGY DEMOCRACY BEYOND UTILITY 2.0 TO John Farrell February 5, 2015

| Date post: | 14-Jul-2015 |

| Category: |

Presentations & Public Speaking |

| Upload: | john-farrell |

| View: | 755 times |

| Download: | 1 times |

E N E R G Y D E M O C R A C YB E Y O N D U T I L I T Y 2 . 0 T O

John Farrell February 5, 2015

T H E P R E L U D E

Per capita electricity useAverage annual retail electricity pricesInterstate transmission spendingWind and solar power capacity

c1900 199019801970 2000 2010

Sources: World Bank, EIA, US Census, SEIA, LBNL

“GOLDEN AGE”

• Regulated monopolies • Profits from sales • Profits from new

power plants • “bigger is better”

SHOCK & COMPETITION STABILITY DEREGULATION

• PURPA allows non-‐utility generation

• Prices rise • Sales slow • Competition starts

• Prices fall • Demand rises

• Independent producers rise, as do interstate transactions

• Feds open wholesale market

• States adopt renewable standards and net metering

• Some states introduce competition for generation and retail sales

• Wind+Solar go exponential

• Demand flattens

TRANSITION

• States offer “decoupling”

• States adopt energy efficiency standards

RULE CHANGES

MARKET CHANGES

T H E U . S . E L E C T R I C I T Y T I M E L I N E

Today’s turmoil isn’t the first change in the U.S.

electricity system

Per capita electricity useAverage annual retail electricity pricesInterstate transmission spendingWind and solar power capacity

c1900 199019801970 2000 2010

Sources: World Bank, EIA, US Census, SEIA, LBNL

• Regulated monopolies • Profits from sales • Profits from new

power plants • “bigger is better”

SHOCK & COMPETITION STABILITY DEREGULATION

• PURPA allows non-‐utility generation

• Prices rise • Sales slow • Competition starts

• Prices fall • Demand rises

• Independent producers rise, as do interstate transactions

• Feds open wholesale market

• States adopt renewable standards and net metering

• Some states introduce competition for generation and retail sales

• Wind+Solar go exponential

• Demand flattens

TRANSITION

• States offer “decoupling”

• States adopt energy efficiency standards

RULE CHANGES

MARKET CHANGES

“GOLDEN AGE”

T H E U . S . E L E C T R I C I T Y T I M E L I N E

Per capita electricity useAverage annual retail electricity pricesInterstate transmission spendingWind and solar power capacity

1980 2000 2010

Sources: World Bank, EIA, US Census, SEIA, LBNL

“GOLDEN AGE”

• Regulated monopolies • Profits from sales • Profits from new

power plants • “bigger is better”

SHOCK & COMPETITION STABILITY DEREGULATION

• PURPA allows non-‐utility generation

• Prices rise • Sales slow • Competition starts

• Prices fall • Demand rises

• Independent producers rise, as do interstate transactions

• Feds open wholesale market

• States adopt renewable standards and net metering

• Some states introduce competition for generation and retail sales

• Wind+Solar go exponential

• Demand flattens

TRANSITION

• States offer “decoupling”

• States adopt energy efficiency standards

RULE CHANGES

MARKET CHANGES

T H E U . S . E L E C T R I C I T Y T I M E L I N E

c1900 19901970

Per capita electricity useAverage annual retail electricity pricesInterstate transmission spendingWind and solar power capacity

c1900 19801970 2000 2010

Sources: World Bank, EIA, US Census, SEIA, LBNL

“GOLDEN AGE”

• Regulated monopolies • Profits from sales • Profits from new

power plants • “bigger is better”

SHOCK & COMPETITION STABILITY DEREGULATION

• PURPA allows non-‐utility generation

• Prices rise • Sales slow • Competition starts

• Prices fall • Demand rises

• Independent producers rise, as do interstate transactions

• Feds open wholesale market

• States adopt renewable standards and net metering

• Some states introduce competition for generation and retail sales

• Wind+Solar go exponential

• Demand flattens

TRANSITION

• States offer “decoupling”

• States adopt energy efficiency standards

RULE CHANGES

MARKET CHANGES

T H E U . S . E L E C T R I C I T Y T I M E L I N E

1990

T H E U . S . E L E C T R I C I T Y T I M E L I N E

Per capita electricity useAverage annual retail electricity pricesInterstate transmission spendingWind and solar power capacity

c1900 19901970 2000 2010

Sources: World Bank, EIA, US Census, SEIA, LBNL

“GOLDEN AGE”

• Regulated monopolies • Profits from sales • Profits from new

power plants • “bigger is better”

SHOCK & COMPETITION STABILITY DEREGULATION

• PURPA allows non-‐utility generation

• Prices rise • Sales slow • Competition starts

• Prices fall • Demand rises

• Independent producers rise, as do interstate transactions

• Feds open wholesale market

• States adopt renewable standards and net metering

• Some states introduce competition for generation and retail sales

• Wind+Solar go exponential

• Demand flattens

TRANSITION

• States offer “decoupling”

• States adopt energy efficiency standards

RULE CHANGES

MARKET CHANGES

1980

T H E P R E S E N T ( S T R E S S E S )

3.2

3.3

3.4

3.5

3.6

3.7

3.8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

P E A K

S TA G N A N T R E TA I L S A L E S

trillion kilowatt-hours

R I S I N G P E A K D E M A N D

75%

100%

125%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Eastern Interconnection

ERCOT (Texas)

Western Interconnection

CombinedSource: EIA, 2014

Summer Peak Demand by Grid Balancing Regions (2002 = 100%)

$0

$3,000

$6,000

$9,000

$12,000

1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Wind

SolarSource: Lawrence Berkeley Labs

FA L L I N G R E N E W A B L E E N E R G Y C O S T S

U.S. Installed Cost of Wind and Solar Power ($/kilowatt)

R I S I N G R E N E W A B L E E N E R G Y C A PA C I T Y

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Wind

Solar

Geothermal

Installed Wind and Solar Power Capacity (Megawatts)

Source: SEIA, Lawrence Berkeley Labs

R I S I N G R E N E W A B L E E N E R G Y S H A R EU.S. Power Plant Capacity Additions, 2003 through 1st Half of 2014

Source: EIA

0%

25%

50%

75%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014H

Fossil fuel Renewable

R I S I N G R E N E W A B L E E N E R G Y ( A N D D G ) S H A R EU.S. Power Plant Capacity Additions, 2003 through 1st Half of 2014

Source: EIA

0%

25%

50%

75%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014H

21.5%19.2%

5.8%3.1%2.3%

0.6%

18.3%12.4%

6.1%6.2%3.8%2.3%

1.8%

1.3%1.1%

0.5%0.3%0.1%

12.7%

6.7%56.4%

37.1%31.9%

60.9%52.8%

53%

31.7%

15.5%

3.3%3.1%

43.5%

44.5%

28%

44.3%

37.4%

23.3%28.8%40.8%

57%

75%

90.4%92.9%

9.8%4.6%

16.3%

5.9%3.7%2.2%

Coal Gas Wind Small solar Big solar

R I S I N G R E N E W A B L E E N E R G Y ( A N D D G ) S H A R EU.S. Power Plant Capacity Additions, 2003 through 1st Half of 2014

Source: EIA

0%

25%

50%

75%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014H

21.5%19.2%

5.8%3.1%2.3%

0.6%

18.3%12.4%

6.1%6.2%3.8%2.3%

1.8%

1.3%1.1%

0.5%0.3%0.1%

12.7%

6.7%56.4%

37.1%31.9%

60.9%52.8%

53%

31.7%

15.5%

3.3%3.1%

43.5%

44.5%

28%

44.3%

37.4%

23.3%28.8%40.8%

57%

75%

90.4%92.9%

9.8%4.6%

16.3%

5.9%3.7%2.2%

Coal Gas Wind Small solar Big solar

Tota

l GW

Ad

ded

0

15

30

45

60

Total GW added

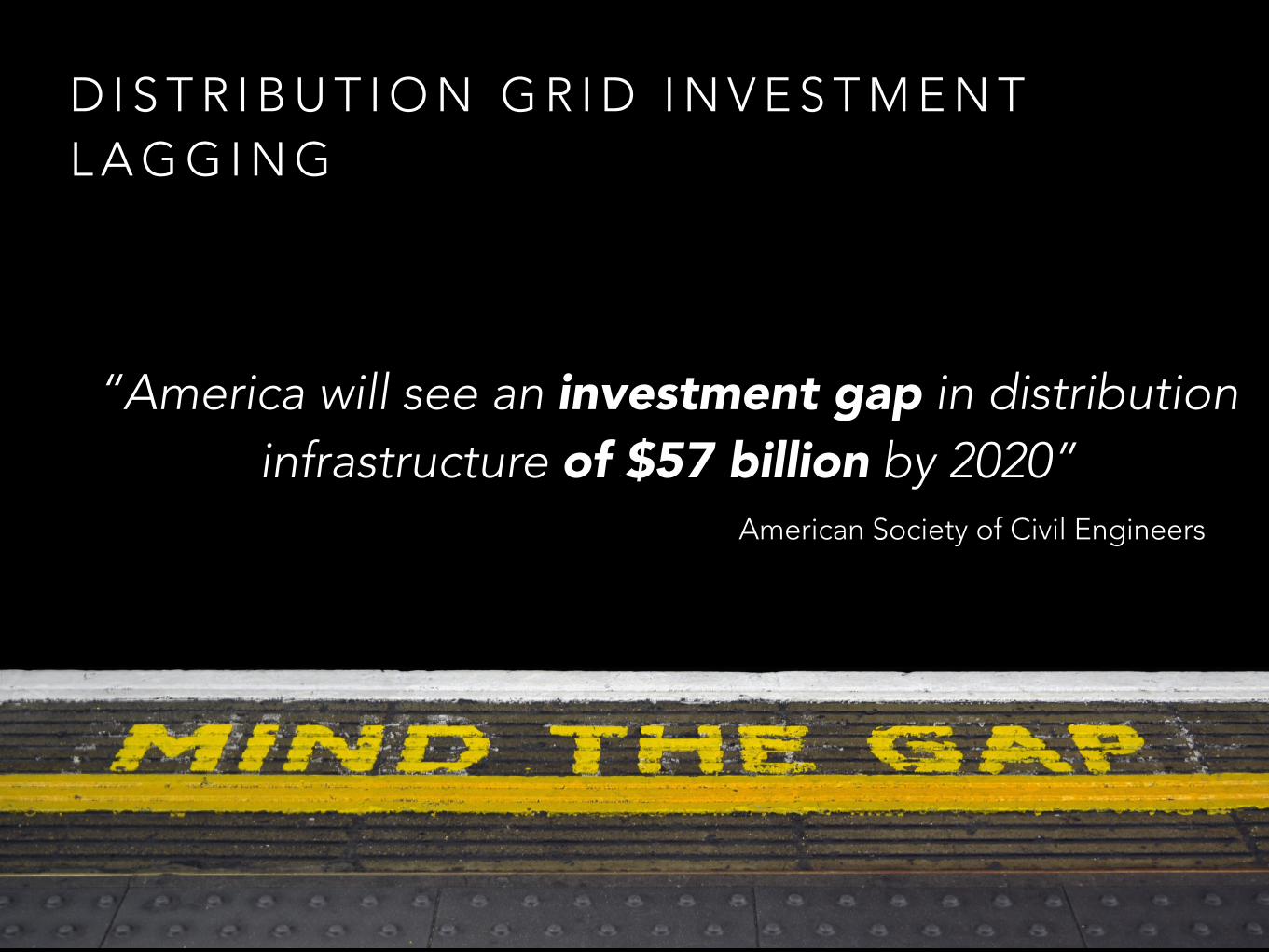

D I S T R I B U T I O N G R I D I N V E S T M E N T L A G G I N G

American Society of Civil Engineers

“America will see an investment gap in distribution infrastructure of $57 billion by 2020”

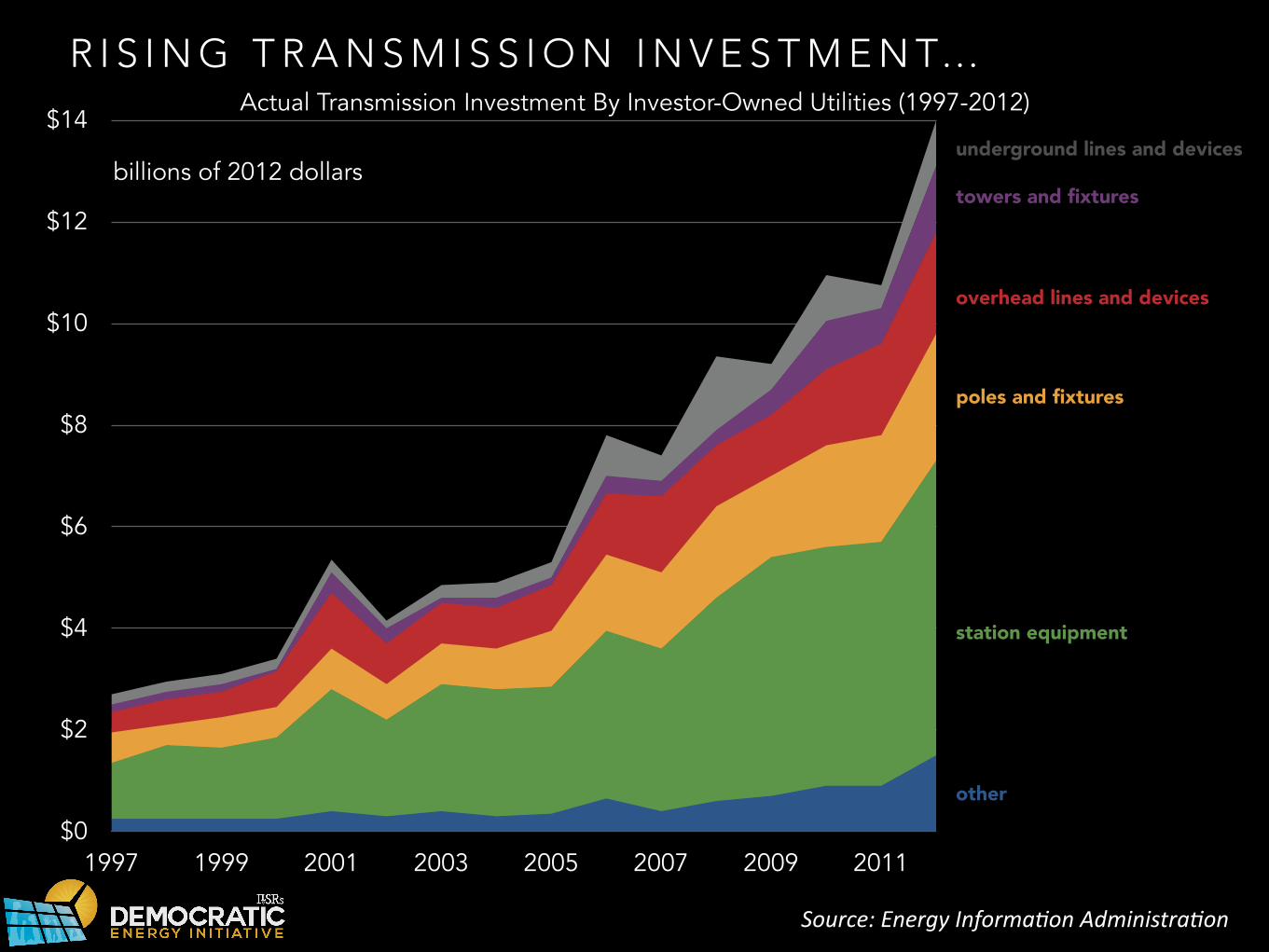

R I S I N G T R A N S M I S S I O N I N V E S T M E N T…

station equipment

$0

$2

$4

$6

$8

$10

$12

$14

1997 1999 2001 2003 2005 2007 2009 2011

billions of 2012 dollars

Source: Energy InformaCon AdministraCon

underground lines and devices

towers and fixtures

overhead lines and devices

poles and fixtures

other

Actual Transmission Investment By Investor-Owned Utilities (1997-2012)

T H E P R E S E N T ( R U L E S )

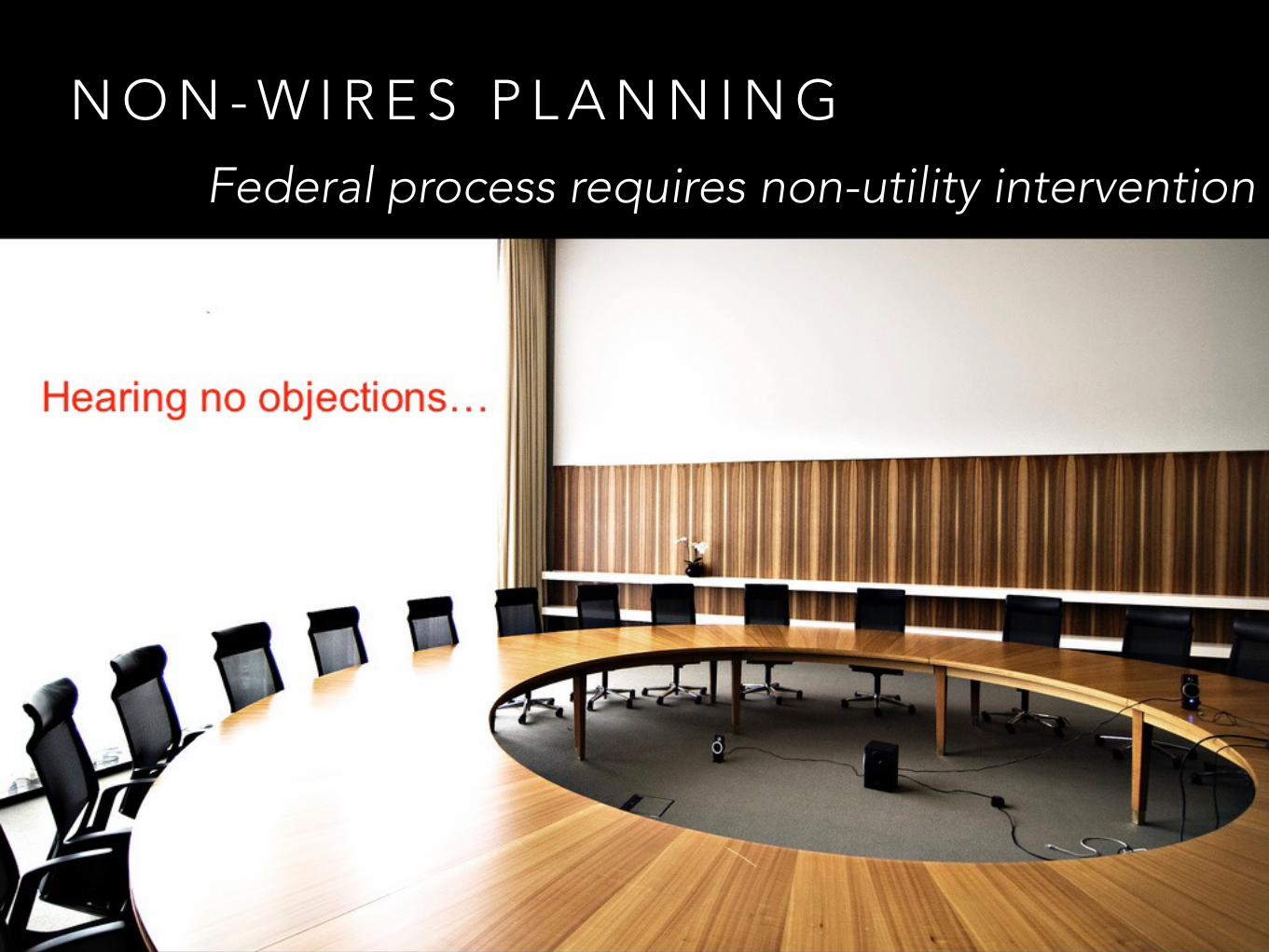

N O N - W I R E S P L A N N I N G

Federal process requires non-utility intervention

V E R M O N T E N E R G Y E F F I C I E N C Y P R O G R A M S AV I N G S

Ener

gy E

ffici

ency

Ben

efits

, 201

0 ($

/MW

h)

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

Avoided energy,

capacity and transmission

Avoided distribuIon, line losses, reserves

Risk benefits, other adders, water

O&M, other fuel savings, low-‐income adders

Greenhouse gas

emissions

State-level criteria NOT considered

by federal regulators

Adapted from: Public Utilities Fortnightly

http://www.fortnightly.com/fortnightly/2013/04/looking-beyond-transmission

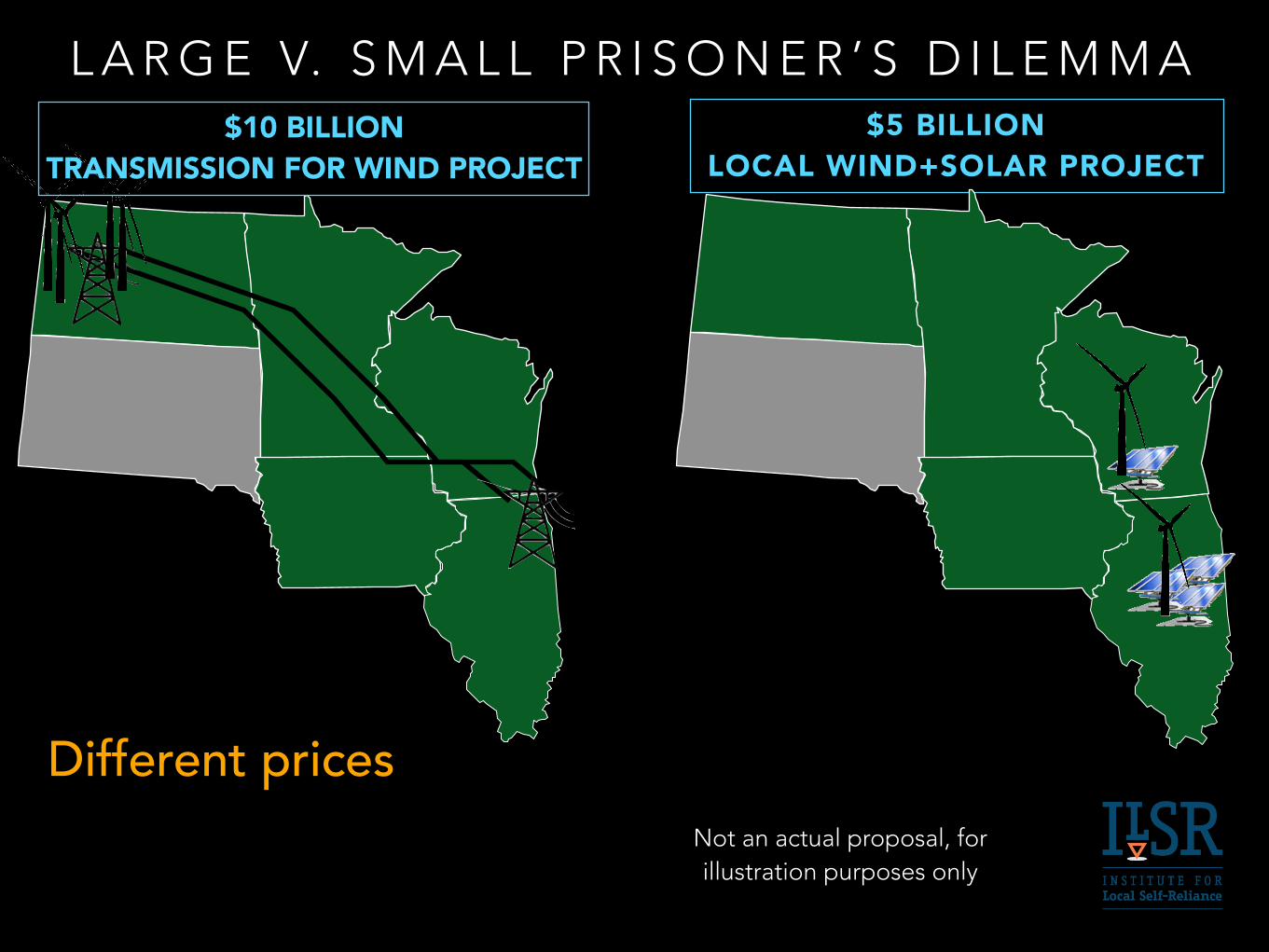

L A R G E V. S M A L L P R I S O N E R ’ S D I L E M M A

Not an actual proposal, for illustration purposes only

Two ways to deliver regional reliability and

energy

$5 BILLION LOCAL WIND+SOLAR PROJECT

$10 BILLION TRANSMISSION FOR WIND PROJECT

Not an actual proposal, for illustration purposes only

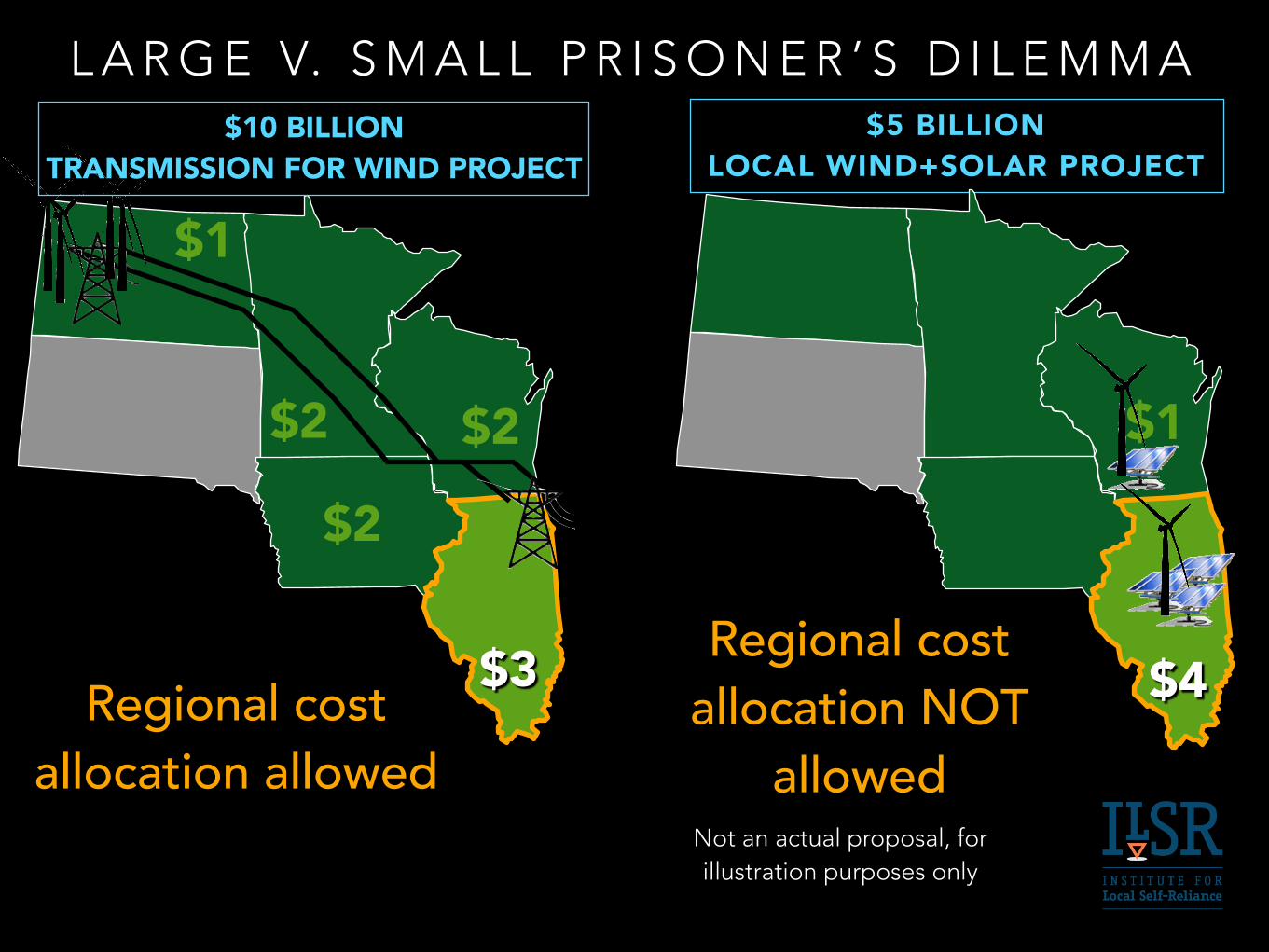

L A R G E V. S M A L L P R I S O N E R ’ S D I L E M M A

Different prices

$5 BILLION LOCAL WIND+SOLAR PROJECT

$1

$4

$1

$2 $2

$3

$2

$10 BILLION TRANSMISSION FOR WIND PROJECT

Not an actual proposal, for illustration purposes only

L A R G E V. S M A L L P R I S O N E R ’ S D I L E M M A

Regional cost allocation allowed

Regional cost allocation NOT

allowed

$5 BILLION LOCAL WIND+SOLAR PROJECT

$1

$4

$1

$2 $2

$3

$2

State chooses transmission because it pays less

$10 BILLION TRANSMISSION FOR WIND PROJECT

Not an actual proposal, for illustration purposes only

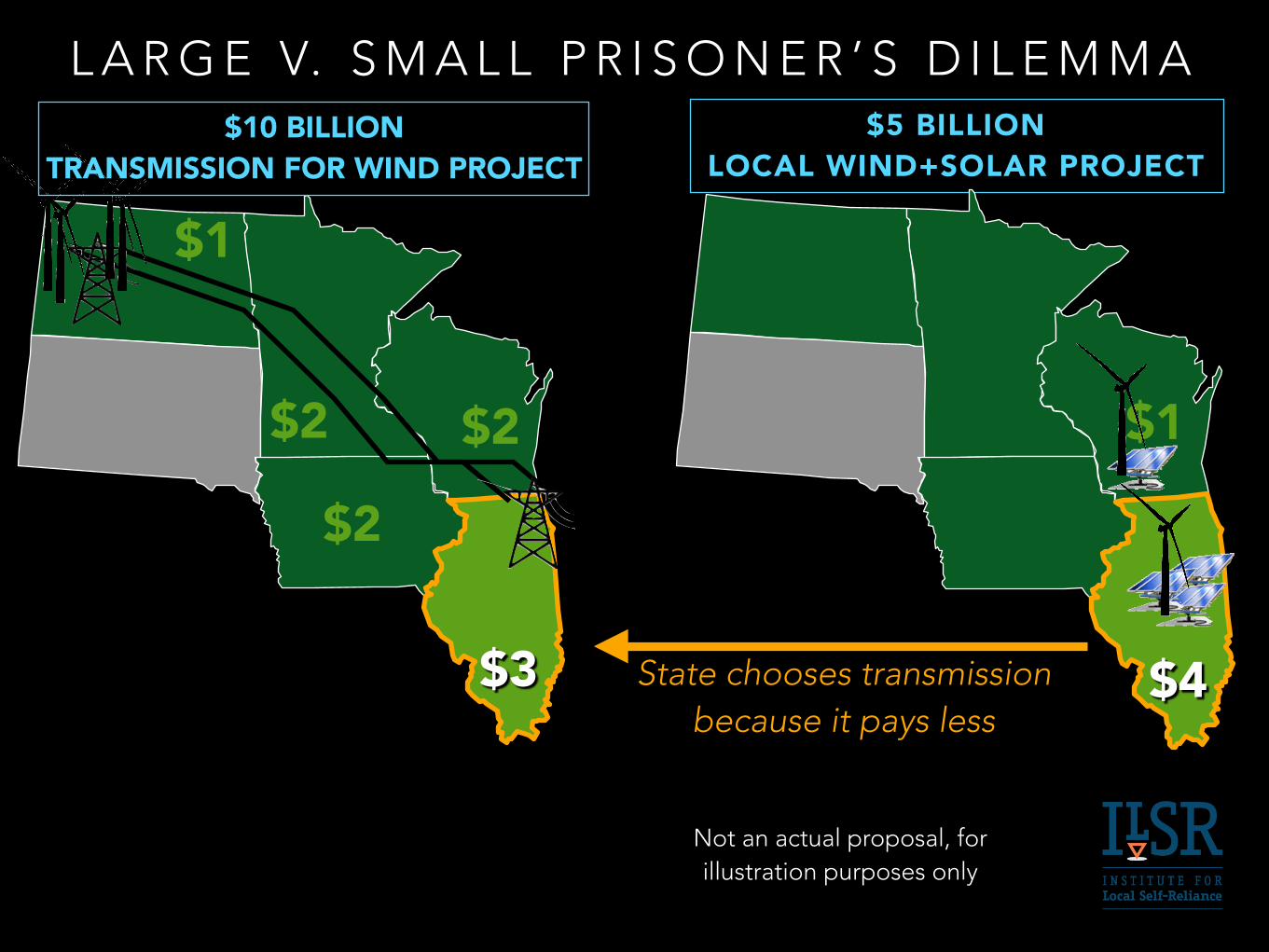

L A R G E V. S M A L L P R I S O N E R ’ S D I L E M M A

L A R G E V. S M A L L P R I S O N E R ’ S D I L E M M A$5 BILLION

LOCAL WIND+SOLAR PROJECT

$1

$4

$1

$2 $2

$3

$2

State chooses transmission because it pays less

Region pays twice as much for same reliability and clean

energy benefit

$10 BILLION TRANSMISSION FOR WIND PROJECT

Not an actual proposal, for illustration purposes only

B A L K A N I Z E D B U S I N E S S M O D E L S

T H E P R E S E N T ( R E S U LT S )

W O R S E N I N G U T I L I T Y C R E D I T R AT I N G S

0%

25%

50%

75%

100%

1970 1980 1990 2000 2011Source: Peter Kind

AAA

AA+ AA AA-

A+ A A-

BBB+ BBB

BBB-

A+ A A-

AA+ AA AA-

BBB+ BBB

BBB+ BBB

BBB+ BBB

A+ A A-

A+ A A-

A+ A A-

AA+ AA AA-

BBB-BBB-BBB-

$ 4 8 B I L L I O N AT S TA K E

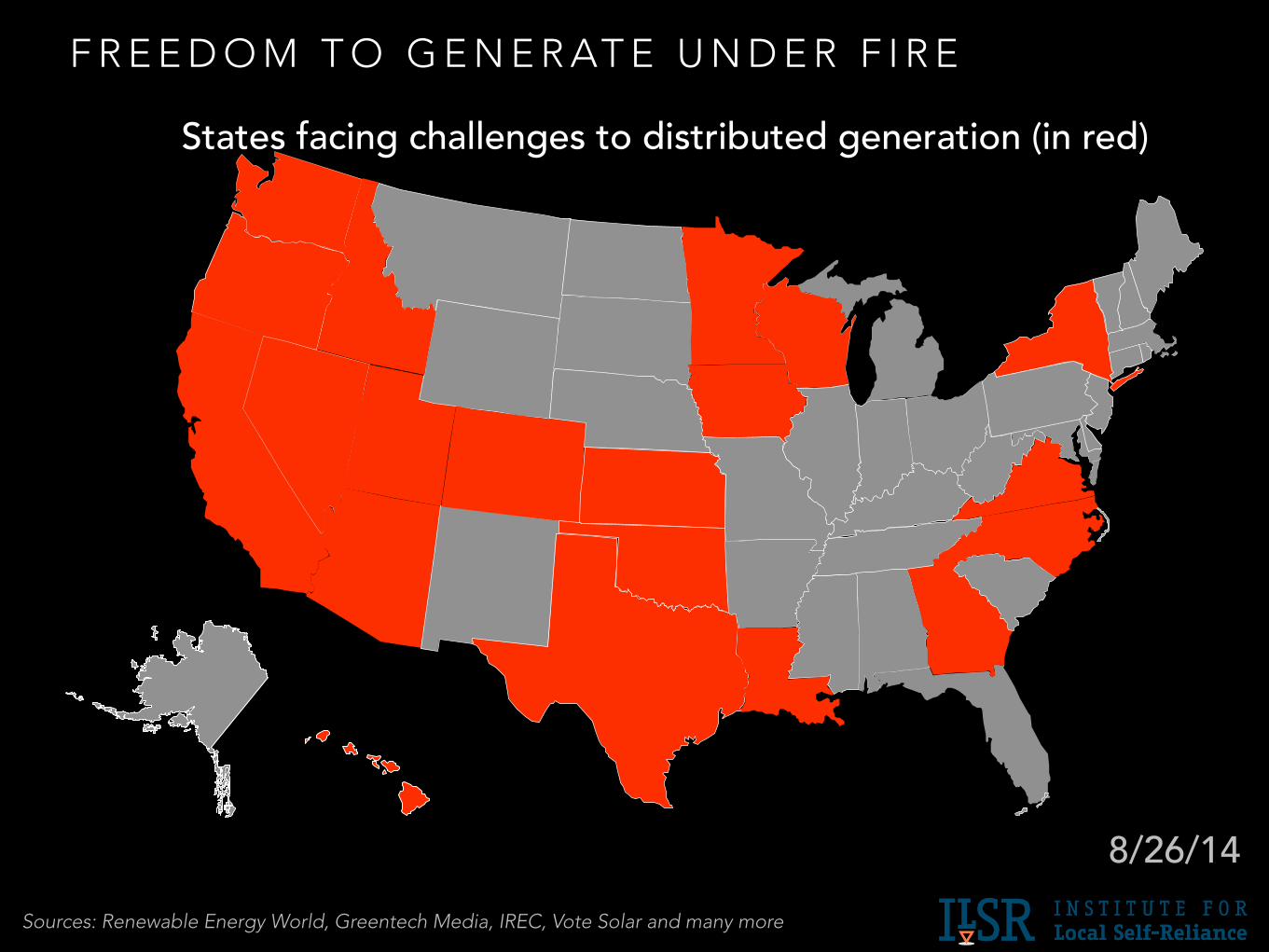

F R E E D O M T O G E N E R AT E U N D E R F I R E

States facing challenges to distributed generation (in red)

Sources: Renewable Energy World, Greentech Media, IREC, Vote Solar and many more

8/26/14

T H E F U T U R E

S TAT E S P I O N E E R I N G U T I L I T Y 2 . 0

LOW-CARBONEFFICIENTFLEXIBLE LOW-CARBONEFFICIENTFLEXIBLE

“Utility 2.0” principles or “pillars”

Utility 2.0

ELECTRICITY SYSTEM

EQUITABLELOCALLOW-

CARBONEFFICIENTFLEXIBLE LOW-CARBONEFFICIENTFLEXIBLE LOCAL EQUITABLE

“Utility 2.0” pillars

With $48 billion at stake, 2 more

principles needed

EQUITABLELOCALLOW-

CARBONEFFICIENTFLEXIBLE LOW-CARBONEFFICIENTFLEXIBLE LOCAL EQUITABLE

FIVE PILLARS OF ENERGY DEMOCRACY

“Utility 2.0” pillars

$48 billion

“Utility 3.0”

EQUITABLELOCALLOW-

CARBONEFFICIENTFLEXIBLE

DEMAND RESPONSE MARKET

ANCILLARY SERVICES MARKET

E N E R G Y S T O R A G E

R O O F T O P S O L A R

F E E D - I N TA R I F F

N E T M E T E R I N G

VIRTUAL NET METERING, E.G. COMMUNITY SOLAR

ENERGY STORAGE

RENEWABLE ENERGY STANDARD

E N E R G Y S T O R A G E ENERGY STORAGE

ON-BILL REPAYMENT

ELECTRIC VEHICLES

W/ DG SET-ASIDE

LOW-CARBONEFFICIENTFLEXIBLE LOCAL EQUITABLE

POLICIESTECHNOLOGY

LEGEND

FIVE PILLARS OF ENERGY DEMOCRACY

INDEPENDENT LOCAL GRID OPERATOR

REAL-TIME PRICING

SIMPLE ENERGY

MANAGE-MENT

“Utility 2.0” pillars

E N E R G Y D E M O C R A C Y I N A C T I O N

INDEPENDENTLOCAL GRID

MANAGER

= super efficient buildings

www.ilsr.org

D O W N L O A D T H E F U L L R E P O R T

R E A D M O R E

@johnffarrell