Page 1

The7thIndonesiaJapanJointScientificSymposium

(IJJSS2016)Chiba,20‐24November2016

67

Topic:SocioeconomicsRelations

TheResponseOfPublicInPalangkaRayaToBankMuamalatIndonesia(BMI)PalangkaRayaBranch

AliSadikin,SE,MSI1

HeadofMagisteronIslamicEconomics,GraduateProgram,StateIslamicInstitute(IAIN)ofPalangkaRaya,Jl.G.ObosKomplekIslamicCenterNo.24,PalangkaRaya73112,

Indonesia

AbstractThemainconceptsonIslamicbankingaretheprincipleofjusticeandnotchargeinterestsystem.ThroughtheprohibitionofinterestinIslamsothatIslamiceconomicsexpertsinagreement that re‐organization of Islamic banking should be implemented based onpartnerships (shirkah) and profit sharing (mudarabah). In other review, thecharacterizedofsocio‐culturalconditionsaswellasreligiousofpublicinPalangkaRayathose are the number of Muslim as majority and the level of religious life (based onresearcherobservations),thosethingsassumedhaveaninfluencetopublicresponseonfactorsofproduct,service,socialization,benefitandsocialsetting.Authorcollectsdatausedquestionnairesandinterviewmethods, toanalyzethepublicresponseandpublicperceptiontotheexistenceofBankMuamalatIndonesia.Theaimsofthisresearchare(1)tofindthepublicresponsetotheexistenceofBankMuamalat;(2) to find and analyze the public response toward Bank Muamalat Indonesia usedscoringmethodtothequestionary.Based on the result of this research discovered that for the most part of public ofPalangka Raya (respondents) accept and respond positively to the existence of BankMuamalat Indonesia (BMI) Palangka Raya Branch. At the aspects of product, service,benefit and setting social are in accordance as expected (adequate). While, publicresponse (respondents) at the aspect of socialization is still less and needs to beimproved

Keywords

PublicResponse,BankMuamalatIndonesia

1Telp.Fax:+625363222105.Phone:+6285248046845.E‐mailaddress:[email protected]

Page 2

68

TheResponseOfPublicInPalangkaRayaToBankMuamalatIndonesia(BMI)PalangkaRayaBranch

1. Background

Islamic economics development in accordance with the progress of Islamic

financial institutionsas theprimemoverof financial institution.Asoneof thehighest

Moslemcitizensintheworld,itwasquiteunfortunatethatIslamicfinancialinstitutions

newly flourished in the late 1990s, after recommendation ofMajelis Ulama Indonesia

(IndonesianCouncilofUlama)wasreleasedintheworkshoponbankintereston18‐20

August1990. Indonesiawas leftbehindcomparedtoMiddleEastcountries,evenfrom

Malaysia.

Attheeraof1940s,theconceptofIslamicbankhademerged.Bankingsystemin

Islamic economics based on profit and loss sharing concept. The general principle is

anyonewhowanttoearntheoutcomefromsavings,shouldbewillingtotakerisks,the

bank will also share the company’s losses if they want the outcome of their capital

gains.2 Mit Ghamr Lokal Saving Bank was the first modern Islamic bank in Mesir. In

ManilaalsoestablishedPhilipineAmanahBankin1973andDubaiIslamicBankin1975,

placedinDubai.3

Aftergoingthroughalongprocessthoughabitlate,attheendof1991,precisely

on 1st November 1991 was the signing of the Deed of Establishment of PT Bank

MuamalatIndonesia.4Thenon1stMay1992,Islamicfinancialinstitutions,suchasBank

MuamalatIndonesia,BankPerkreditanRakyatShariahandAsuransiTakafulstartedto

operate. Along with the emergence of those Islamic financial institutions, an Islamic

financial institution also established in Palangka Raya that is Bank Muamalat.

ContemporaryMoslemscholarshavebeenformulatedIslamicbankingproducts,which

2Muhammad, 2001, Bank Syari’ah: Analisis Kekuatan, Peluang, Kelemahan dan Ancaman, Ekonosia, Kampus

FakultasEkonomiUII,Yogyakarta.3M.Syafi’iAntonio,BankIslamdariTeorikePraktek,Jakarta:GemaInsaniPress,2001,p.18andp.25.4Syamsul Anwar, Permasalahan Produk‐produk Bank Syari’ah: Studi tentang Bai Muajjal (P3M, IAIN Sunan

Kalijaga,1995),p.17.

Page 3

69

have been adjusted to the concepts of muamalat contained in fiqih books by ulama5,

sourcedfromAl‐Qur’anandHadith.

Characteristic of those financial institutions above, showed from the products

offeredthatassumedbeabletogivesenseoffairnessandmoreIslamic.Thosefinancial

institutions have implemented their products in line with qawaid al fiqhiyah6 so that

expected will be able to meet Moslem’s desire, especially to transact with no riba

(usury)orinterestwhichhasbeenapolemic.

ThepeculiarityofIslamicbankisitusedanapproachwhichprioritizesenseof

justice,andforbidsaninterest.ThroughtheprohibitionofinterestinIslam,theexperts

of themoderneconomyagree that re‐organization inbankingshouldbe implemented

basedonpartnerships(shirkah)andprofitsharing(mudarabah).7Replacedaninterest

mechanism, some ulama believe that in an individual project funding, the best

instrumentisprofitsharing.

However,astheresultofafieldobservation,inpracticeitshouldberecognized

that the transaction of muamalat activities often incompatible with the concepts of

Islam,ashappenedinPalangkaRaya.Alotoftransactionpracticesonmuamalatwhich

incompatiblewith revelation. Inmuamalat cases, some people rarely heed the norms

andethicsthatregulatedinAl‐Qur’anandHadith,whereasalmosteveryoneknowsthe

prohibitionofriba(usury).Itsindicationcanbeviewedfromthelossamongcommunity

or business institutions. For example in this case is habit of public in Palangka Raya,

especiallyaroundauthor’sneighborhoodwhostillborrowingmoney(debt)totheloan

sharkswhileborrowingmoneytoIslamicbank.Sometradersprefertoborrowfundto

aninvestorwhoarepreparingafundbutaskingforinterest(usury)inarow.8

5Ulama is an expert on Islamic law. In this paper, ulama identified as an expert in Islamic economics who

participateactivelyintheimplementationoftheconceptsofIslamicvaluestotheoperationalofIslamicbanking,whichisbeingdevelopednowadays. 6RulesoffiqihortheprinciplesofIslamiclaw.

7Nejatullah Siddiqi,KemitraanUsahadanBagiHasildalamHukum Islam, (Jakarta: Dana Bhakti Prima Yasa,1992),p.1.

8Basedonauthor’sobservationtopeoplewhoinvolveddebtswithloansharksstyle.

Page 4

70

Actually,itisarealitythatMoslemcommunityinPalangkaRayaobeytherules

of Islam in field of ibadah (worship/ibadah mahdah), But unfortunately Tuan Guru

(ulamainPalangkaRaya)seemdonotchangetoomuchonreligiouslifeofMoslemsin

muamalataspect.

Inthecontextofmutualbenefit inbusiness,BankMuamalatexiststoservethe

community, especially in Palangka Raya as well as Central Kalimantan. In one side,

product of BankMuamalat is needed by people to be business partners and develop

business. But in another side, operational of Bank Muamalat still experiences many

obstacles to implement itsproducts.Thiscasecausednotonlybymaterialregulations

(itssubstance)informaconceptof itsproducts,butalsoinfluencedbyexternalfactor

thatisbehaviourofstakeholdersofmuamalatingeneral.Thesethingsgreatlyaffectsthe

responseofpublicinPalangkaRayatoBankMuamalatIndonesia(BMI)PalangkaRaya

Branch.

2. LiteratureReview

TheresearchbyAshanulIn’am(1996)on”PerformanceAnalysisofBMT”more

oriented to ”want to know or examine” the hyphotesis about opportunities and

obstacles facedbyBMT in theeconomicempowermentofpeople through itsbusiness

strategiesconsistingofsiteselection,pricesandservices.ThisresearchstatesthatBMT

hashighopportunitytocarryoutitsmissionandempowersmallbusiness.

OtherresearchonHowBMTgivecredittocustomerwithnointerestsystemby

Yustikosari (1996) oriented to credit with mudharabah system practiced by BMI

withoutbindingthecustomerthroughcontractualsystemascustomerorcreditorand

debtor, but both in balanced position, that is as partners. He also concluded that the

existenceofBankMuamalatIndonesiaismoreindependentthanconventionalbank.

This superiority, is a characteristic from Islamic bank and distinguish it from

non‐Islamicfinancialinstitutionsystem.AsstatedbyAbd.Adhim(1998)inhisresearch

oncomparativebetweenBankPerkreditanRakyat(BPR)withProfitSharingsystemand

Page 5

71

BankPerkreditanRakyatwithinterestsystem(conventional).Theresultofthisresearch

concludes that profit sharing system has positive double values. It means that BPR

through profit sharing system not only plays its role as financial institution but also

implementsIslammissionthatisAmarMa’rufNahiMunkar.

Ininternationalscale,bankerandIslamiceconomistalsohavedoneresearchon

various aspects related to Islamic banking. Comparative study did byAbdul GaderA.,

andGahrani S., on “IslamicandCommercialBankingRole inEconomicDevelopment:A

ComparativeFinancialEvaluation”in1990thatcomparedthreeIslamicbanks(Bahrain

IslamicBank,FaisalIslamicBank,inBahrainandDarAlmalAlIslamicwithnon‐Islamic

bank(NationCommercialBankinSaudiArabiaandSaudiAmericanBank).Theresultof

thisresearchshowsthat:1)IslamicBanktendstomaintainahigherratiobetweencash

and deposit than non‐Islamic bank; 2) Percentage of equity capital (equity) to total

assets inIslamicbankishigherthantraditionalbankthatoperatedinsameregion;3)

Islamic Bank shows higher profit ratio than traditional bank that operated in same

country; 4) IslamicBank ismoreefficient thancommercialbankwhichprovedby the

ratioofnon‐interestexpensewithgrossrevenue(Metwally,1995:149).

AnwarIgbalQureshi(1973:113)inhisbook“IslamandtheTheoryofInterest”

explainsspecificallyaboutIslamandcredit.HestatesthatIslamicbankingisconsistent

to Islamic doctrine wisely avoids things that harm for one side, and also put capital

ownerandtraderinsamelevel,andcombinetheirinterests.Ifthereissomeonewhohas

fundwithout experience or skill that needed to run a business, and also another one

whodoesnothas fundbutskill thatneededbyIslamicbusiness institution,asseen in

Islamicbankingpracticethatcombinesthosebothintereststhroughfundfromthefirst

person and skill from the rest would be permitted because profitable if combined to

businessinstitutioninordertogetprofitproportionally.

Anita Rahmawati, in 1999/2000 through her dissertation: Controversy on

Validity Status ofMurabahah in Islamic Banking: Study of Product Implementation of

Page 6

72

BMI Semarang Branch. In this research, main theme is focused to controversy of a

product of Islamic bank that is murabahah. This research is not too different with

research by Syamsul Anwar, because the productbaibi samanajil in the principle is

developed frommurabahah. But, this research has more value because this is field

researchwhichisinBMISemarangBranch.Itsdifferencewithresearchbyauthoristhis

doesnotlookfortheresponseofpublic(muamalatbehavior)totheproduct,aswellas

thedifferenceofresearchlocation.

Based on those researches above show explicitly the positive dynamics on

growthrateandsystemofoperationalizationofIslamicbanking.Inaddition,thesystem

that has been implemented by Islamic bank and Islamic financial institutionswith no

interest is respondedpositively by public. It caused by an assumption that interest is

prohibitedandcontainstheelementofexploitation.

3. ResearchMethods

Thisresearchusesdescriptiveanalysismethodthatdrawsandexplainsaboutthe

responseofpublicinPalangkaRayatoBankMuamalatIndonesia(BMI)PalangkaRaya

BranchandtheresponseofpublicinPalangkaRayatothefactorsofproduct,services,

socialization,benefitandsocialsettingofpublicofPalangkaRaya informof tableand

percentage.

Data of this research collected through: questionnaire, interview and

documentation.Throughthosemethodsvaliddatawouldbecollectedthatrelatedtothe

problemofresearch.

4. TheResultsofResearch

a. ResponseofPublictoBankMuamalatIndonesia

DatacollectingasonemethodofthisresearchhasdoneduringMarchtoApril

2006. Data collecting methods that choosed are questionnaire used checklist. The

questionnaire spread to respondents consists of: (1) Bank Mualamat practitioners,

eithermanagementoremployee,(2)customers;(3)publicfigure/tuanguru(ulama)(4)

Page 7

73

publicnon‐customer.ForrespondentwhonotknowingaboutBankMualamatwillgetan

explanation,especially fornon‐customerrespondent.Theresultof this researchabout

the response of public in PalangkaRaya toBankMualamat Indonesia (BMI)Palangka

RayaBranchcanbeviewedonthetablesbelow:

a. Basedonrespondentknowledge

Table1.1.ResponseofPublicBasedOnKnowledge

OpinionofRespondent Frequency PercentageKnow 12 8%

Justknow 74 49.3%

Knowlittle 35

23.3%

Donotknow 29 19.3%

Total 150 100%

Source:ResultDataofQuestionnaires

Fromthetable1.1.knownthat12respondents(8%)statedtheyknowaboutthe

concept of Bank Mualamat. 74 respondents (49%) stated they just know about the

concept of Bank Mualamat. Whereas 23,3% stated they know a little thing about the

concept of BankMualamat. And 29 from 150 respondents (19,3%) stated they do not

know about the concept of Bank Mualamat. From this research as the table above

concludes thatmostly people inPalangkaRayahave littleknowledgeon the concept of

BankMualamat.Basedonthatrespondentslittleknowledgesothatneededaproactive

effort fromBankMualamat to informandexplain topublicabout theconceptofBank

Muamalat.

b. BasedonSourceofInformation

Table1.2.ResponseofPublicBasedOnSourceofInformation

Respondent’sOpinion Frequency PercentageMassmedia 59 39,3%

Advertisement 0 0

Page 8

74

Friend/relation 47 31,3%

Others 44 29,3%

Total 150 100%

Source:ResultDataofQuestionnaires

Source:ResultDataofQuestionnaires

Table1.2.ResponseofPublicBasedOnSourceofInformation

Groupingbasedonsourceofinformationdisplayedabove(table1.2.)hasshown

59 respondents (39,3%) stated that they got information about BankMuamalat from

massmedia. No respondent (0%) has gotten information about BankMuamalat from

advertisement. 47 respondents (31,3%) got information from friend/relation. 44

respondents(29,3%)gotinformationaboutBankMuamalatfromothermediasuchas

socialgathering,associationsandothers.

Based on result of research about source of information that people get about

Bank Mualamat Indonesia, mass media plays big role to socialize Bank Mualamat

Indonesia (BMI) Palangka Raya Branch. Therefore, mass media is very effective to

improvepeople’sknowledgeinPalangkaRaya.

Furthermore, friend/relation and other media also play effective role to give

information about Bank Mualamat. However, if explored further, people will give

informationaboutanything(includingbank)iftheyfeelsatisfiedfromthatthing.Based

on those facts, so management of Bank Muamalat should prioritize customer

satisfaction.

c. BasedonTypesofRespondent

0

10

20

30

40

50

60

70

1 2 3 4

Series1

Page 9

75

Table1.3.TypesofRespondentofResearch

Respondent’sOpinion Frequency Percentage

BankMualamat’sEmployee 12 8%

Customer 68 45,3%

Non‐Customer 62 41,3%

PublicFigure 8 5,3%

Total 150 100%

Source:DatafromResultoftheQuestionnaires

Source:ResultDataofQuestionnaires

Informationaboveintable1.3.showsageneraldescriptionofrespondentbased

onitstypes,thatmajorityofrespondentsofBankMuamalatPalangkaRayaBranchare

both customer (45,3%) and non‐customer (41,3%). The next frequency came from

employee of Bank Muamalat (8%) and public figure (5,3%). Based on types of

respondentthatshowmajorityofrespondentsarecustomerandnon‐customer.

b. PublicResponsetoProduct,Service,Socialization,BenefitandSocialSetting

As in the data of public response on BankMuamalat, data of public response

about (1) product; (2) service; (3) socialization; (4) benefit (5); and social setting

collected through questionnaire instrument in collecting. Data collecting could be

describedasfollows:

a. PublicResponsetotheaspectofProduct

Result data of research about public response on product of Bank Muamalat

0

10

20

30

40

50

60

70

1 2 3 4

Series1

Page 10

76

composed to 5 categories; strongly disagree, disagree, doubtful, agree, and strongly

agree.Resultofresearchasinthetable1.4.below:

Table1.4.PublicResponsetotheAspectofProduct

Respondent’sOpinion Frequency Percentage

Stronglydisagree 2 1,3%

Disagree 3 2,0%

Doubtful 32 21,2%

Agree 85 56,7%

StronglyAgree 28 18,7%

Total 150 100%

Source:ResultoftheQuestionnaire

Based on the result of research above, canbe known thatmostly respondents

agree with the product of Bank Muamalat (56,7 %), followed by doubtful (21,2%),

stronglyagree (18,7%), disagree (2,0%)and stronglydisagree (1,3%)as the last. The

conclusionismostlyrespondentagreewiththeproductofBankMuamalat.Forfurther

detailscanbeviewedinpiechartbelow:

Source:ResultDataofResearch

b. PublicResponsetotheaspectofService

Result data of research on public response about service aspect of Bank

Muamalatcomposedto5categories;verylow,low,normal,highandveryhigh,thatcan

beviewedinthetable1.5.asfollows:

Strongly Disagree

Disagree

Doubtful

Agree

Strongly Agree

Page 11

77

Table1.5.PublicResponsetotheAspectofServiceInBankMualamat

Respondent’sOpinion Frequency Percentage

Verylow 3 2,0%Low 13 8,7%Normal 47 31,3%High 68 45,3%Veryhigh 19 12,7%Total 150 100%

Source:ResultoftheQuestionnaire

Based on result data of research above, can be known that mostly

respondentsrate“high”forserviceaspect(45,3%),andtherest31,3%ratenormal,

12,7%rateveryhigh,8,7%ratelowand2%rateverylowforthequalityofservice

aspect. The conclusion is mostly respondents agree with service model of Bank

Muamalatasoneof thefactorsofconsiderationbycustomer.Forfurtherdetailscan

beviewedinpiechartbelow:

Source:Datafromquestionnairec. PublicResponsetotheaspectofSocialization

Socialization aspect is an important aspect tomake BankMuamalat Indonesia

(BMI) known by public. Socialization aspect that has been implemented by Bank

MualamatIndonesia(BMI)PalangkaRayaBranchevidentlygetslowratingfrompublic

in Palangka Raya. It means that product of Bank Muamalat Indonesia Palangka Raya

Branchisnotmuchknownbypeople.

Respondent’sstatementstotheaspectofsocializationcanbeviewedfrompublic

awareness on Bank Muamalat Indonesia (BMI) Palangka Raya Branch. Those

Very low

Low

Normal

High

Very high

Page 12

78

statementscomposedinthetable1.6.below:

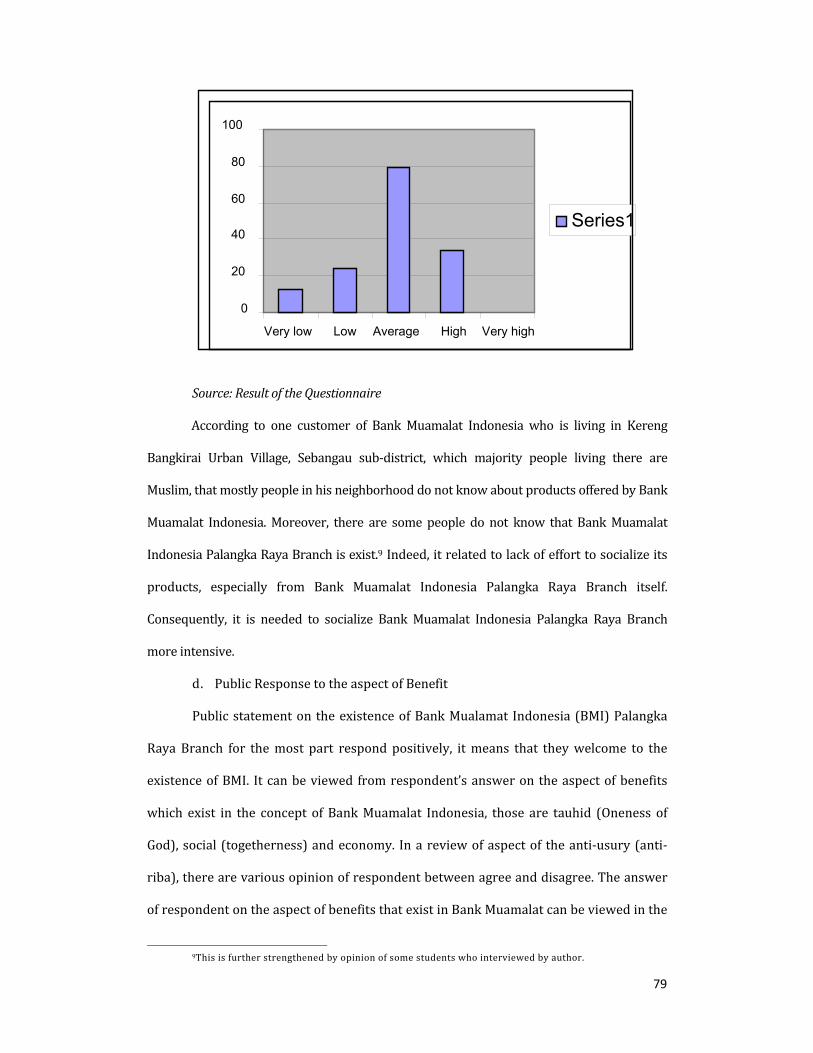

Table1.6. PublicResponsetotheAspectofSocialization

Respondent’sOpinion Frequency Percentage

Verylow 13 8,7%

Low 24 16%

Average 79 52,7%

High 34 22,6%

Veryhigh 0 0

Total 150 100%

Source:ResultoftheQuestionnaire

Fromtheresultofquestionnaireinthetable1.6.aboveknownthatsocialization

factor is very desicive for public awareness to the concepts or products which are

owned by BankMualamat. From the questionnaire known that socialization aspect is

still less intense. 52,7% of respondents have average knowing on products of Bank

MualamatIndonesiaPalangkaRayaBranch,while16%havelowknowingonproducts

ofBankMualamatIndonesiaPalangkaRayaBranch.

Socialization by BankMuamalat Indonesia has a significant value to affect the

public use Bank Muamalat’s services However, based on those respondent’s opinion

above, socialization that has done by BankMuamalat shows an unsatisfactory result.

This socializationmust always be implemented so that public in Palangka Raya who

mostlyareMuslimwillknow,understandanddesiretouseIslamicbankservicesatlast,

so the purpose of Islamic bank establishment (Bank Muamalat Indonesia) as an

alternate means for Muslim to avoid interest system will be achieved. Socialization

aspectofBankMuamalatIndonesia(BMI)PalangkaRayaBranchisnotquiteoptimalas

showedbelow:

Page 13

79

Source:ResultoftheQuestionnaire

According to one customer of Bank Muamalat Indonesia who is living in Kereng

Bangkirai Urban Village, Sebangau sub‐district, which majority people living there are

Muslim,thatmostlypeopleinhisneighborhooddonotknowaboutproductsofferedbyBank

Muamalat Indonesia.Moreover, there are some people do not know that BankMuamalat

IndonesiaPalangkaRayaBranchisexist.9Indeed,itrelatedtolackofefforttosocializeits

products, especially from Bank Muamalat Indonesia Palangka Raya Branch itself.

Consequently, it is needed to socialize Bank Muamalat Indonesia Palangka Raya Branch

moreintensive.

d. PublicResponsetotheaspectofBenefit

PublicstatementontheexistenceofBankMualamat Indonesia(BMI)Palangka

RayaBranch for themost part respondpositively, itmeans that theywelcome to the

existenceofBMI. Itcanbeviewed fromrespondent’sanswerontheaspectofbenefits

which exist in the concept ofBankMuamalat Indonesia, those are tauhid (Oneness of

God),social(togetherness)andeconomy. Inareviewofaspectoftheanti‐usury(anti‐

riba),therearevariousopinionofrespondentbetweenagreeanddisagree.Theanswer

ofrespondentontheaspectofbenefitsthatexistinBankMuamalatcanbeviewedinthe

9Thisisfurtherstrengthenedbyopinionofsomestudentswhointerviewedbyauthor.

0

20

40

60

80

100

Very low Low Average High Very high

Series1

Page 14

80

table1.7.asfollows:

Table1.7. PublicResponsetotheAspectofBenefit

Respondent’sOpinion Frequency Percentage

StronglyDisagree 0 0%

Disagree 22 21,3%

Doubtful 32 19,3%

Agree 66 44%

StronglyAgree 23 15,3%

Total 150 100%

Source:ResultofQuestionnaire

Based on result of the questionnaire in the table 1.7. above is known that

publicresponsetotheaspectofbenefitgivenbyBankMuamalatisquitehigh.44%

ofrespondentsagree,while21,3%disagree,andtherestare19,3%stateddoubtful

and15,3%stronglyagree.

WhenauthortalktosomepeopleofKerengBangkiraiUrbanVillageininformal

interview, their reason in choosing tousebanking is theirneeded towithdraw funds,

withoutconsiderwhichisharam(forbidden)ornot.Indeed,inthiscase,theconceptof

haram(forbidden)ofbankinginterestsisverythin.Peoplethought,ifthereisanybank

thatallowinterests,whyshouldlookingforIslamicbank,especiallyifitslocationisnot

strategic. This thought generally used by Muslim in Palangka Raya, in addition to

emergency reasons.10 So that needed a proactive effort from all partieswho know

andunderstand aboutmuamalat to explain to public. Thosepublic opinion above

canbeviewedvisuallyasfollows:

10Authorheardthisthoughtwhenauthordidaninterview.Itwasalsoopinionbysomerespondentwhoarenon‐

customerofBankMualamat.

Page 15

81

Source:ResultDataofQuestionnaireDiagramonPublicResponsetotheAspectofBenefit

Actually,whetherinterestissamewithriba(usury)ornothadbeendiscussedby

MUI (Indonesian Council of Ulama) in workshop on Bank Interests and Banking at

Cisarua,Bogoron19‐22August 1990. In thatworkshop, itwas recognized about two

opinionsonbankinterests,thosewereanopinionwhichbelievedthatbankinterestsis

riba (usury) and forbidden, and other opinion which assumed that bank interests is

halal (permitted). Hereinafter, in the 4th National Conference of MUI period of 1990‐

1995onSeptember1990inJakarta,bothulama(expertinIslamiclawandeconomics)

whobelievedthatbankinterestsisharamandulamawhoassumedthatinterestishalal

theyagreedtodevelopasystemandprocedureofbankingwhich isnon‐interest.This

agreement contained in The Broad Outlines of the Work Programme of Indonesian

CouncilofUlama1990‐1995.11

Polemicoftheexistenceofbankinterestsitselfbecomeanobstacleforgrowth

and development of Islamic bank. According to Muhammad Hasbi’s opinion that

Islamic bank nowadays is getting less attention by people due to the controversy of

legal status of bank interests. Furthermore, and this is an expectation of Islamic

11Karnaen Perwata Atmadja, "Peluang dan Strategi Bank Tanpa Bunga dengan Sistem Bagi Hasil dalam Bisnis

Perbankandi Indonesia", inHamidBusyaib andMursyidi Prihantoro (ed.),BankTanpaBunga (Yogyakarta:Mitra GamaWidya,1993),p.1‐2.

0

10

20

30

40

50

60

70

Strongly disagree Disagree Doubtful Agree Strongly agree

Series1

Page 16

82

bankingpractitioners,governmentthroughMUI(IndonesianCouncilofUlama)should

unite public perception on bank interests to release fatwa (legal opinion or legal

pronouncement) that declare bank interests is haram (forbidden), and peoplemust

switchtoIslamicbankbasedonshariahasanalternative.12

e. PublicResponsetotheaspectofSocialSetting

SocialsettingaspectisacharacteristicofpeopleconditioninPalangkaRayathat

may affect public response on BankMuamalat Indonesia Palangka Raya Branch. That

thing above can be viewed from the result of questionnaire contained in table 1.8. as

follows:

Table1.8.PublicResponsetotheAspectofSocialSetting

Respondent’sOpinion Frequency Percentage

Verylow 9 6%

Low 39 26%

Normal 42 28%

High 55 37%

Veryhigh 5 3%

Total 150 100%

Source:ResultDataofQuestionnaire

Source:ResultDataofQuestionnaire

Astable1.8.abovecanbeknownifmostlyrespondentsagreethatsocialsetting

12WhenauthorinterviewanIslamicbankpractitionerinPalangkaRaya.

0

10

20

30

40

50

60

Very low Low Normal High Very high

Series1

Page 17

83

aspecthassignificantrole(37%forhighoption),while28%choosednormaland26%

choosed low. Itmeansthatcharacteristicofpeoplecondition isan importantthing for

Islamiceconomicsdevelopment,inthiscaseisBankMuamalatIndonesiaPalangkaRaya

Branch.Basedonrespondent’sopinioninthetable1.8.above,socialsettingaspecthas

significantroleforpublicinPalangkaRayatorespondtheexistenceofBankMuamalat

IndonesiaPalangkaRayaBranch.

5. Conclusion

Basedonanalysisresultto150respondentsthroughquestionnaire,soaccording

toproblemformulationinthisresearchcanbeconcludedasfollows:

1. Public response to Bank Muamalat Indonesia (BMI) Palangka Raya Branch is

good (positive). It showed by the result of research which mostly people in

Palangka Raya (respondent) respond positively to the existence of Bank

MuamalatIndonesia(BMI)PalangkaRayaBranch.

2. Public response on the aspects of product, service, socialization, benefit and

social setting is conformity to the expectation. In simple words, people in

PalangkaRayaaccepttheproductandtheyarepleasedwiththeperformanceof

BankMuamalatIndonesia(BMI)PalangkarayaBranch.

Page 18

84

REFERENCES

A,Chotib,1962.Bankdalam1slam,Jakarta:BulanBintang.Abdurraahman,Masduha. 1992,Pengantar danAsas‐asasHukumPerdata Islam (Fiqih

Muamalat),Surabaya:CentralMedia.Alsa,A,andSantoso,F.H.1997. “Faktor‐faktorPendukungdanPenghambatbagiDosen

Kelompok IlmuSosial‐HumanioradalamMelakukanPenelitianmelaluiLembagaPenelitianGadjahMada”,JurnalPsikologi,YearsXXIVNo.1June.

Anwar,NejaSyamsul,1995.PermasalahanProduk‐produkBankSyari’ah:Studi tentang

BaiMuajjal,Yogyakarta:P3MIAINSunanKalijaga.Anwar,Syamsul,PermasalahanProduk‐produkBankSyari’ah:StuditentangBaiMuajjal

(P3M,IAINSunanKalijaga,1995).Arifin,Zainul,1999.MemahamiBankSyariah,Jakarta:P.N.Alvabet.BAPPEDA&BPS,KotaPalangkaRayadalamAngka(PalangkaRaya:BPS,2005)Basyir, A. Azhar, 2000. Asas‐asas Muamalat (HukumPerdata Islam), Yogyakarta:

PerpustakaanFak.HukumUII.______________, 1994.RefleksiAtas PersoalanKeislaman: Seputar Filsafat,Hukum, Politik

danEkonomi,Bandung:Mizan.______________, 1993. Asas‐Asas Muamalat (Hukum Perdata Islam), Yogyakarta:

PerpustakaanFak.HukumUII.Busyaib, Hamid dan Mursyidi Prihantoro (ed.), 1993.Bank Tanpa Bunga, Yogyakarta:

MitraGamaWidya.Fauzi, Yuslam. "Peranan, peluang dan Tantangan Bank Syari'ah Sebagai Salah Satu

Lembaga Pemberdayaan Umat dalam Memasyarakatkan Ekonomi Syari'ah",Article in National Seminar on Islamic Economics and Congress of KoKaSEI ‐Indonesia,Semarang,12May2000.

Muslehuddin, Muhammad, 1994. Sistem Perbankan dalam Islam, Jakarta: Cet. II, PT.

RinekaCipta.Nadirsyah,1999."BungaBankdalamPerspektifIslam",YurisdiksiFirstEdition.Perwataatmadja, H. Karnaen dan H. Syafi’i Antonio, 1992. Apa danBagaimanaBank

Islam,Yogyakarta:PT.VeresiaGrafika.____________,1992.PeluangdanStrategiOperasionalBankMuamalahIndonesia,inM.Rush

Karim(Ed)BerbagaiAspekEkonomiIslam,Yogyakarta:TiaraWacanadanFEUII.Priyono, A.E., 1998. "Periferalisasi, Oposisi, dan Integrasi Islam di Indonesia (Menyimak

PemikiranKontowijoyo)",inDr.Kontowijoyo,ParadigmaIslam,Bandung:Mizan.

Page 19

85

Siddiqi,Nejatullah,KemitraanUsahadanBagiHasildalamHukumIslam,(Jakarta:Dana

BhaktiPrimaYasa,1992).

Singarimbun,MasridanSofyanEffendi,1989,MetodePenelitianSurvey,Jakarta:LP3ESSupardi,2005.MetodePenelitianEkonomi&Bisnis,Yogyakarta:UIIPressSyafi’i,MuhammadAntonio, "Konsep SyariahdalamBank Islam",ArticleShortCourse:

BankSyariahProspekdanOperasional,Penyelenggara:LembagaPendidikandanPengembanganBankSyariah(LPPBS).

Syihab,Umar,1996.HukumIslamdanTransformasiPemikiran,Semarang:DinaUtama.LawNo.10of1998joLawNo.7of1992onBanking,Jakarta:FirstEdition,SinarGrafika.Wahid,Agus,1995.DilemaBMIdiTengahTuntutanUmat,UlumulQur'anNo.4,Vol.Vi.Ya’qub, Hamzah, 1999. Kode Etik Dagang: Pola Pembinaan Terkait Hidup Alam

Berekonomi,Bandung:CV.DiponegoroYusdani, 2002. “Transaksi (Akad)dalamPerspektifHukum Islam”, Yogyakarta: Millah,

Vol.II,MSIUII.