20

Consulting Market Trends The ALM Outlook: Production Strategy Consulting Strategy & Operations Consulting Research Series January 2017

Consulting Market Trends

The ALM Outlook: Production Strategy Consulting

Strategy & Operations Consulting Research Series January 2017

© 2017 ALM Media Properties, LLC 2

Consulting Market Trends

Contents

Overview 3

Market Size & Outlook 4

Market Structure 8

Client Demand Trends 10

Consulting Provider Trends 12

Methodology 18

About ALM Intelligence 20

© 2017 ALM Media Properties, LLC 3

Consulting Market Trends

OverviewWhat Is Production Strategy?

Production strategy forms part of the supply chain segment of the

broader strategy & operations (S&O) consulting market. The supply

chain segment encompasses services directed at improving the

efficiency and effectiveness of clients’ value chain activities.

Market SnapshotThe production strategy consulting market is currently in a hiatus

between the flurry of activity spurred by the simultaneous uptick

in labor costs in emerging Asia and the downdraft of energy costs

in North America, and the as-yet-unfulfilled promise of production

digitization. The result is a market on the cusp in terms of growth

and structure.

Demand TrendsBeset by a combination of persistently soft and volatile demand,

as well as a diminishing capacity to extract productivity gains,

manufacturers are questioning whether their prevailing strategic

configuration can move them beyond this impasse. At the same

time, ongoing changes in supply markets are overturning longstanding assumptions about where to produce, and emerging

production and information technologies are furnishing opportunities for reconfiguring production strategies.

Provider TrendsThe structure of the production strategy market differs more by degree

than kind from its historic configuration. Production operations occur at

the nexus of two strategic links. One is the horizontal value chain along

which physical inputs are transformed into outputs. The other is the ver-

tical hierarchy along which strategies are transformed into outcomes.

Production strategy consulting providers tend to emanate from one

of the four extremes of these links. But the provider landscape is not

standing still. Digitization is compelling existing providers to adapt their

services toward more integrated offerings. It is also creating conditions

conducive to new entrants closer to the information and operations

technologies that are disrupting production.

Market OutlookThis combination of demand and supply trends results in a market that, while growing somewhat below the broader supply

chain segment, has significant upside potential that is driven primarily by the demand side of the market. This potential

hinges largely on the pace of uptake of digital technologies and, to a lesser extent, political risk.

S&OConsulting

EnterpriseStrategy

Organization & Operating

Model Strategy

Finance

Mergers &Acquisitions

Research &Development

Customer

Sourcing &Procurement

CEO &COO

Services

CFOServices

CPO &CSCO

Services

CMO &R&D

Services

Supply Chain

Strategy & Operations Consulting Market Segments

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

!!

!!

!!

Strategy

Execution

Develop Source Make Deliver Service

Inputs Outputs

Production Operations Landscape

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

© 2017 ALM Media Properties, LLC 4

Consulting Market Trends

Production strategy makes up approximately one-fifth of the broader supply chain segment of the S&O consulting market,

with client spending in this area exceeding $X.X billion in 2015.

Market Size & OutlookMarket Size & Composition

Supply

Chain

Production

Strategy

Serv

ice

Ope

ratio

ns

Organization

& Operating

Model

Strategy

Supply Chain Planning

Logistics

Capital ProjectsSourcing &Procurement

Asset Lifecycle Management

Next-

Generation

Sourcing

Procurement

Operations

Organization

Front-O�

ceService

Back

-O�

ceSe

rvic

e

Busin

ess

Stra

tegyCap

ital

Stra

tegy

Ente

rpris

eSt

rate

gy

R&D

Customer

Product

Development

Innovation

Strategy

CommercialExecution

Production

OperationsCustomer Service

Pricing

Branding & Marketing

Finance Operations

Finance

Corporate Finance

& Treasury

M&A

M&AFinance

Strategy

JVs & A

lliances

CEO & COO ServicesCPO & CSCO Services CFO ServicesCMO & R&D ServicesSource: The ALM Outlook: Production Strategy Consulting, ALM Intelligence estimates

S&O Market $X.X Billion

© 2017 ALM Media Properties, LLC 5

Consulting Market Trends

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence estimates

Legend: Very Strong Strong Moderate Weak None

Production Strategy Regional Market Trends

Region Growth Trend Market Attributes

Asia Pacific Demand is down due to the decline in China’s manufacturing production growth since 2013, but overcapacity and rising labor costs are conducive to a sustained spending uptick.

EMEAConsulting spending is two-pronged. One focuses on cost performance largely through better alignment of product and production engineering, and the other emphasizes adapting produc-tion strategy for the adoption of digital technologies.

Latin AmericaThis is a highly fragmented region with a sparse and subscale indigenous manufacturing popula-tion that focuses demand on regional supply chain and location strategy. Cost performance is the overriding focus, given declining manufacturing output.

North AmericaUntil recently, this market was focused on nearshoring and reshoring from East Asia, but current spending growth revolves around adapting manufacturing strategies for additive manufacturing technologies and more real-time analytics.

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

Relative to the broader supply chain segment, client

spending on production strategy consulting is heavily

weighted toward the EMEA and North America markets,

reflecting the concentration of manufacturers with globally

dispersed operations in these regions.

Market Size & OutlookClient Spending by Geographic Region

© 2017 ALM Media Properties, LLC 6

Consulting Market Trends

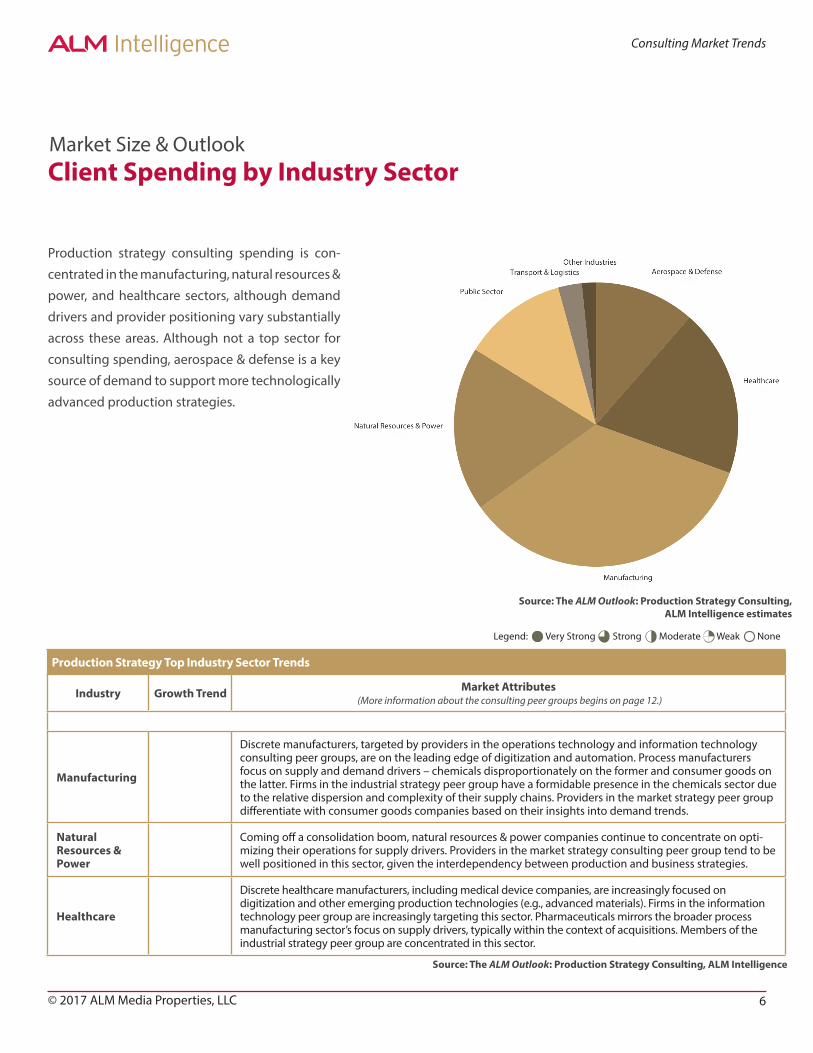

Production strategy consulting spending is con-

centrated in the manufacturing, natural resources &

power, and healthcare sectors, although demand

drivers and provider positioning vary substantially

across these areas. Although not a top sector for

consulting spending, aerospace & defense is a key

source of demand to support more technologically

advanced production strategies.

Market Size & OutlookClient Spending by Industry Sector

Legend: Very Strong Strong Moderate Weak None

Production Strategy Top Industry Sector Trends

Industry Growth Trend Market Attributes (More information about the consulting peer groups begins on page 12.)

Manufacturing

Discrete manufacturers, targeted by providers in the operations technology and information technology consulting peer groups, are on the leading edge of digitization and automation. Process manufacturers focus on supply and demand drivers – chemicals disproportionately on the former and consumer goods on the latter. Firms in the industrial strategy peer group have a formidable presence in the chemicals sector due to the relative dispersion and complexity of their supply chains. Providers in the market strategy peer group differentiate with consumer goods companies based on their insights into demand trends.

Natural Resources & Power

Coming off a consolidation boom, natural resources & power companies continue to concentrate on opti-mizing their operations for supply drivers. Providers in the market strategy consulting peer group tend to be well positioned in this sector, given the interdependency between production and business strategies.

Healthcare

Discrete healthcare manufacturers, including medical device companies, are increasingly focused on digitization and other emerging production technologies (e.g., advanced materials). Firms in the information technology peer group are increasingly targeting this sector. Pharmaceuticals mirrors the broader process manufacturing sector’s focus on supply drivers, typically within the context of acquisitions. Members of the industrial strategy peer group are concentrated in this sector.

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence estimates

© 2017 ALM Media Properties, LLC 7

Consulting Market Trends

Production strategy consulting spending is currently growing at a rate that is approximately 90% percent of the prevailing

growth rate in the broader supply chain segment. This relative growth shortfall reflects the falloff in the growth of manufac-

turers’ investment spending, which is translating into a reluctance to undertake substantial reconfigurations of production

strategies.

Base Case ForecastThe base case outlook for production strategy consulting spending growth is a moderate uptick in 2016, followed by a

downtrend in 2017 and 2018. This will be driven by an anticipated downshift in economic activity that will act as a drag on

growth across the broader supply chain segment.

Forecast ScenariosThe risk in this forecast increases significantly in 2017 and 2018. This upwardly biased risk is fueled largely by the potential

for a faster than expected adoption of digital technologies that disrupt production strategies. The other significant source

of potential upside risk is political in nature. While it would constitute a longer-term drag on production strategy consulting

spending growth, aggressive regulatory change or a more restrictive trade environment would likely spur short-term

spending. The more restricted downside risk emanates primarily from a larger than expected economic downturn that makes

companies curtail investment and defer significant changes to production strategies.

Market Size & OutlookMarket Growth Outlook

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence estimates

© 2017 ALM Media Properties, LLC 8

Consulting Market Trends

The distribution of production strategy consulting provider market share is highly positively skewed, with a substantial tail of

relatively small providers. This reflects the tendency of many providers to bundle production strategy services with broader

supply chain or digital transformation ones.

Top Production Strategy Consulting Providers

Revenue CY2015 ($ millions)

Providers

>$200 Firm A Firm B Firm C

$100 - $199 Firm D Firm E Firm F

$20 - $99 Firm G Firm H Firm I

Firm J Firm K Firm L

Firm M Firm N

<$20* Firm O Firm P Firm Q

Firm R Firm S Firm T

Firm U* The revenue tier with less than $20 million includes select providers and is not exhaustive.

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence estimates

Market StructureMarket Concentration

© 2017 ALM Media Properties, LLC 9

Consulting Market Trends

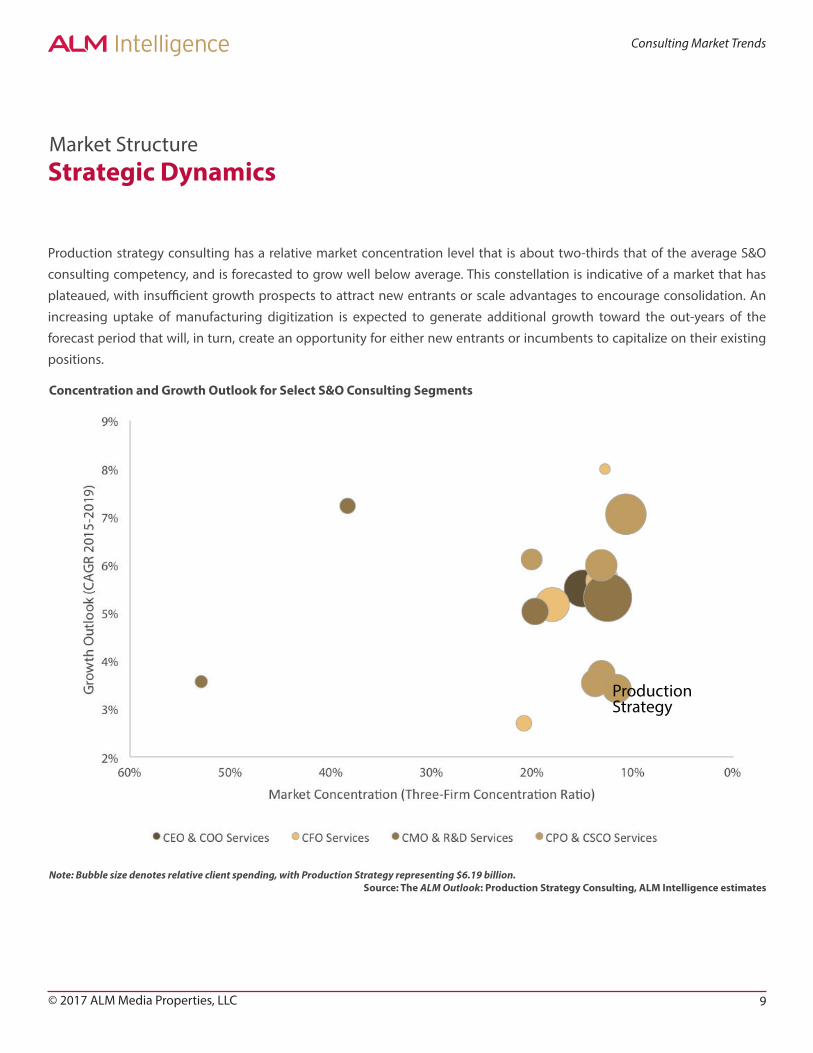

Production strategy consulting has a relative market concentration level that is about two-thirds that of the average S&O

consulting competency, and is forecasted to grow well below average. This constellation is indicative of a market that has

plateaued, with insufficient growth prospects to attract new entrants or scale advantages to encourage consolidation. An

increasing uptake of manufacturing digitization is expected to generate additional growth toward the out-years of the

forecast period that will, in turn, create an opportunity for either new entrants or incumbents to capitalize on their existing

positions.

Market StructureStrategic Dynamics

Production Strategy

Note: Bubble size denotes relative client spending, with Production Strategy representing $6.19 billion.Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence estimates

Concentration and Growth Outlook for Select S&O Consulting Segments

© 2017 ALM Media Properties, LLC 10

Consulting Market Trends

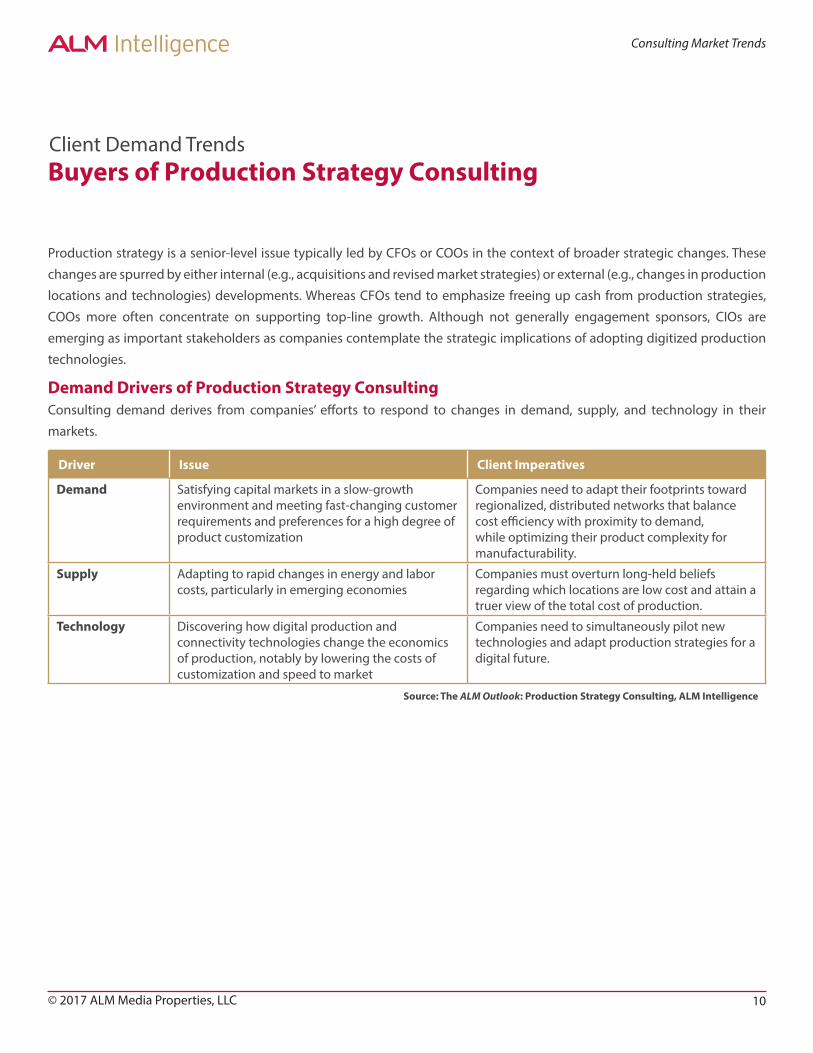

Production strategy is a senior-level issue typically led by CFOs or COOs in the context of broader strategic changes. These

changes are spurred by either internal (e.g., acquisitions and revised market strategies) or external (e.g., changes in production

locations and technologies) developments. Whereas CFOs tend to emphasize freeing up cash from production strategies,

COOs more often concentrate on supporting top-line growth. Although not generally engagement sponsors, CIOs are

emerging as important stakeholders as companies contemplate the strategic implications of adopting digitized production

technologies.

Demand Drivers of Production Strategy ConsultingConsulting demand derives from companies’ efforts to respond to changes in demand, supply, and technology in their

markets.

Driver Issue Client Imperatives

Demand Satisfying capital markets in a slow-growth environment and meeting fast-changing customer requirements and preferences for a high degree of product customization

Companies need to adapt their footprints toward regionalized, distributed networks that balance cost efficiency with proximity to demand, while optimizing their product complexity for manufacturability.

Supply Adapting to rapid changes in energy and labor costs, particularly in emerging economies

Companies must overturn long-held beliefs regarding which locations are low cost and attain a truer view of the total cost of production.

Technology Discovering how digital production and connectivity technologies change the economics of production, notably by lowering the costs of customization and speed to market

Companies need to simultaneously pilot new technologies and adapt production strategies for a digital future.

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

Client Demand TrendsBuyers of Production Strategy Consulting

© 2017 ALM Media Properties, LLC 11

Consulting Market Trends

Production Strategy Consulting Client NeedsAs companies respond to these drivers, they encounter a number of challenges that furnish the underlying needs consultants

must meet as they design and deliver solutions to their clients.

Objective Challenges Consulting ImplicationsLink technical network modeling skills with strategic imperatives and practical insights to arrive at a balanced production strategy.

Armed with new tools, companies are conducting more sophisticated analyses of make-or-buy and footprint choices. But they remain overwhelmingly focused on labor cost as the essential decision criterion and struggle to model scenarios that capture the true cost model across the value chain.

1. Align client stakeholders on a set of performance criteria grounded in the needs of the overarching business strategy that can guide fact-based model specification and evaluation.

2. Extend model boundary conditions by incorporating the full range of factors that must be evaluated, including the client’s ability to execute a transformation.

3. Combat the labor cost bias by quantifying the value of lead-time performance and production flexibility.

Instill a process for evaluating and adapting production strategy in response to ongoing contextual changes.

On the one hand, rapid changes in the external environment demand a more dynamic strategic renewal process. On the other hand, companies struggle to assemble and maintain resources for managing technical modeling as well as coordination across the functional silos that span the value chain. Because changing production strategies entails significant expenditures and public relations implications, functions are predisposed to sub-optimize for their respective priorities and constraints, and revert to conservative ambitions.

1. Develop tools clients can use to minimize time invested in structuring and cleaning data for scenario modeling, and avoid the debate and rework that results from an incomplete database.

2. Use visualization tools to quickly evaluate current footprints and arrive at a logical shortlist of scenarios for further analysis.

3. Rebalance away from pure modeling toward a transformation process oriented around more frequent (albeit potentially less expansive) renewals and enabled by an internal transformation capability.

Link the reconfiguration of operational assets and processes to a revised management system.

Too often, senior management is imprisoned by a prevailing paradigm grounded in noneconomic factors and invested in an existing power structure. This not only constrains the scope for change, but also creates misalignments between how a company organizes and manages its operations. This, in turn, can derail or reduce the benefits of change programs.

1. Coordinate with R&D on product complexity, procurement for make-or-buy decisions, and logistics for network design.

2. Redesign organizational structures and performance management systems by starting with the needs of customers.

3. Ensure suppliers can meet new requirements and reinvigorate supplier relationship management to optimize the push-pull crossover for the inventory management system.

Design a production strategy for a digital future.

Most companies lack a clear vision for how digital technologies will impact their production strategies and what they need to do now to be ready. Those companies that are trying to adopt new production technologies such as additive manufacturing struggle to achieve the expected impact.

1. Define the art of the possible through demonstration of live digital applications and prioritize initiatives through a library of proven-use cases.

2. Ally with technology vendors for insight or a coordinated go-to-market approach, but recognize the tension between these.

3. Rebalance clients’ focus away from technology towards the people and organizational changes that are critical for scaling pilots into transformations.

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

Client Demand TrendsBuyers of Production Strategy Consulting

© 2017 ALM Media Properties, LLC 12

Consulting Market Trends

Consulting Provider TrendsPeer Group Design & Characteristics

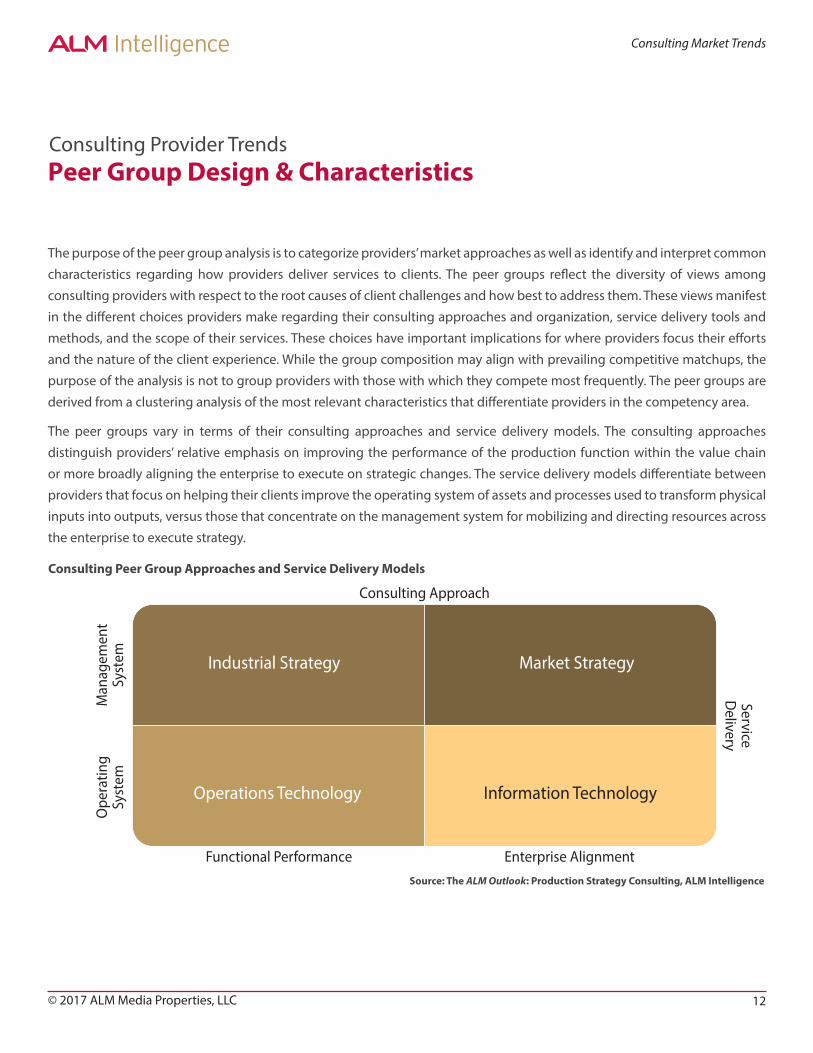

The purpose of the peer group analysis is to categorize providers’ market approaches as well as identify and interpret common

characteristics regarding how providers deliver services to clients. The peer groups reflect the diversity of views among

consulting providers with respect to the root causes of client challenges and how best to address them. These views manifest

in the different choices providers make regarding their consulting approaches and organization, service delivery tools and

methods, and the scope of their services. These choices have important implications for where providers focus their efforts

and the nature of the client experience. While the group composition may align with prevailing competitive matchups, the

purpose of the analysis is not to group providers with those with which they compete most frequently. The peer groups are

derived from a clustering analysis of the most relevant characteristics that differentiate providers in the competency area.

The peer groups vary in terms of their consulting approaches and service delivery models. The consulting approaches

distinguish providers’ relative emphasis on improving the performance of the production function within the value chain

or more broadly aligning the enterprise to execute on strategic changes. The service delivery models differentiate between

providers that focus on helping their clients improve the operating system of assets and processes used to transform physical

inputs into outputs, versus those that concentrate on the management system for mobilizing and directing resources across

the enterprise to execute strategy.

Industrial Strategy Market Strategy

Operations Technology Information Technology

Ope

ratin

gSy

stem

Man

agem

ent

Syst

em

Functional Performance Enterprise Alignment

Consulting Approach

ServiceD

elivery

Consulting Peer Group Approaches and Service Delivery Models

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

© 2017 ALM Media Properties, LLC 13

Consulting Market Trends

The objectives, business models, and operating models that characterize the peer groups reflect their positioning relative

to the two strategic links that intersect in production operations. Operations technology and industrial strategy approach

production strategy from opposite ends of the horizontal value chain, while market strategy and information technology do

so from opposite ends of the vertical strategy to execution hierarchy.

Consulting Provider TrendsPeer Group Functional Positioning

!!

!!

!!

Strategy

Execution

Develop Source Make Deliver Service

Inputs Outputs

MarketStrategy

Industrial StrategyOperations Technology

InformationTechnology

Consulting Peer Group Functional Positioning

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

© 2017 ALM Media Properties, LLC 14

Consulting Market Trends

The strategic approaches and service delivery priorities of the peer groups reflect the distinct objectives that inspire

consulting providers.

Peer Group Representative Providers Peer Group Objectives

Industrial Strategy

Firm A Firm B Providers in the industrial strategy peer group believe production strategy needs to be developed in the context of the end-to-end supply chain in a way that maximizes production efficiency and effectiveness. For this, they seek to simultaneously optimize make-or-buy with network design decisions for an overarching supply chain strategy.

Firm C Firm D

Firm E Firm F

Market Strategy

Firm G Firm HThe market strategy peer group starts from the premise that the purpose of production strategy is to furnish a competitive advantage that furthers the execution of the business strategy. Consistent with this point of view, the touchstone for this group’s service delivery is a translation of the business strategy into performance parameters that can guide the design and management of production strategy.

Firm I Firm J

Firm K Firm L

Information Technology

Firm M Firm N The information technology consulting providers are convinced that the mission of manufacturing is to prepare for and create a digital future. To realize this vision, they organize their service delivery around road mapping and deploying digital technologies.

Firm O Firm P

Firm Q

Operations Technology

Firm R Firm S Firms in the operations technology peer group concentrate on the nexus of product engineering and production technologies as the source of step-change strategies. Their service delivery blends design for manufacturability and broader value engineering methods, with a focus on new production technologies such as automation, additive manufacturing, and sector-specific applications of advanced materials.

Firm T Firm U

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

Consulting Provider TrendsPeer Group Composition & Objectives

© 2017 ALM Media Properties, LLC 15

Consulting Market Trends

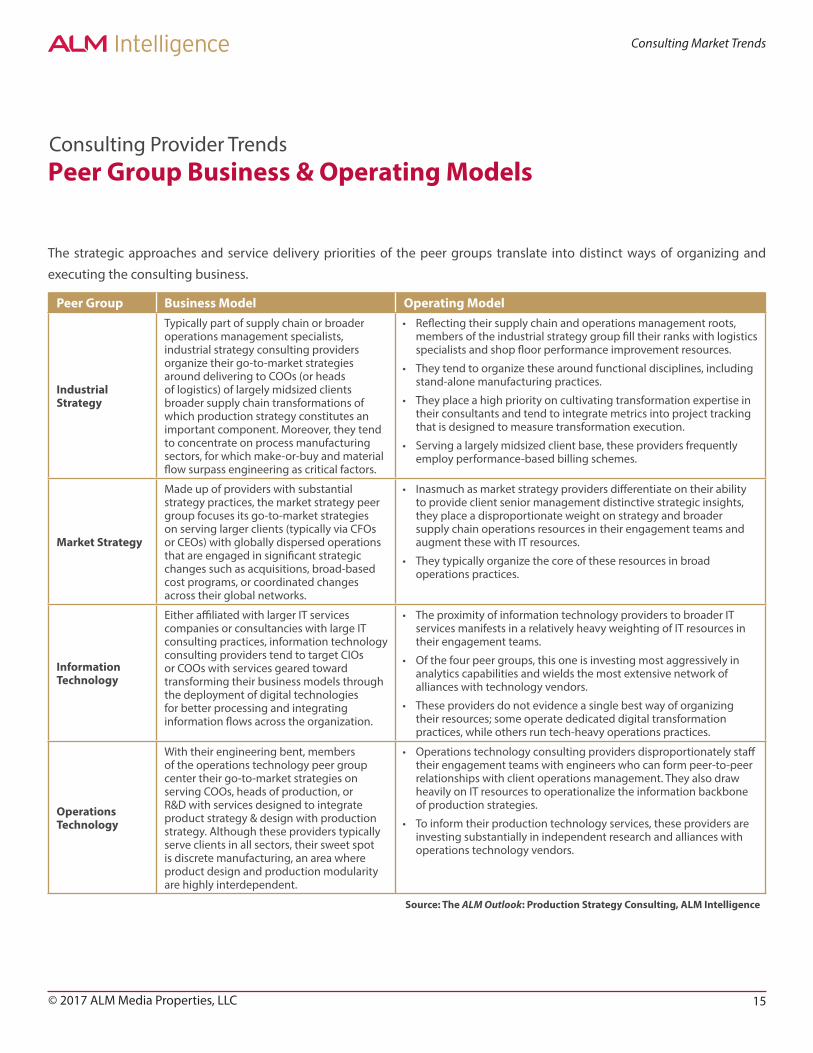

The strategic approaches and service delivery priorities of the peer groups translate into distinct ways of organizing and

executing the consulting business.

Peer Group Business Model Operating Model

Industrial Strategy

Typically part of supply chain or broader operations management specialists, industrial strategy consulting providers organize their go-to-market strategies around delivering to COOs (or heads of logistics) of largely midsized clients broader supply chain transformations of which production strategy constitutes an important component. Moreover, they tend to concentrate on process manufacturing sectors, for which make-or-buy and material flow surpass engineering as critical factors.

• Reflecting their supply chain and operations management roots, members of the industrial strategy group fill their ranks with logistics specialists and shop floor performance improvement resources.

• They tend to organize these around functional disciplines, including stand-alone manufacturing practices.

• They place a high priority on cultivating transformation expertise in their consultants and tend to integrate metrics into project tracking that is designed to measure transformation execution.

• Serving a largely midsized client base, these providers frequently employ performance-based billing schemes.

Market Strategy

Made up of providers with substantial strategy practices, the market strategy peer group focuses its go-to-market strategies on serving larger clients (typically via CFOs or CEOs) with globally dispersed operations that are engaged in significant strategic changes such as acquisitions, broad-based cost programs, or coordinated changes across their global networks.

• Inasmuch as market strategy providers differentiate on their ability to provide client senior management distinctive strategic insights, they place a disproportionate weight on strategy and broader supply chain operations resources in their engagement teams and augment these with IT resources.

• They typically organize the core of these resources in broad operations practices.

Information Technology

Either affiliated with larger IT services companies or consultancies with large IT consulting practices, information technology consulting providers tend to target CIOs or COOs with services geared toward transforming their business models through the deployment of digital technologies for better processing and integrating information flows across the organization.

• The proximity of information technology providers to broader IT services manifests in a relatively heavy weighting of IT resources in their engagement teams.

• Of the four peer groups, this one is investing most aggressively in analytics capabilities and wields the most extensive network of alliances with technology vendors.

• These providers do not evidence a single best way of organizing their resources; some operate dedicated digital transformation practices, while others run tech-heavy operations practices.

Operations Technology

With their engineering bent, members of the operations technology peer group center their go-to-market strategies on serving COOs, heads of production, or R&D with services designed to integrate product strategy & design with production strategy. Although these providers typically serve clients in all sectors, their sweet spot is discrete manufacturing, an area where product design and production modularity are highly interdependent.

• Operations technology consulting providers disproportionately staff their engagement teams with engineers who can form peer-to-peer relationships with client operations management. They also draw heavily on IT resources to operationalize the information backbone of production strategies.

• To inform their production technology services, these providers are investing substantially in independent research and alliances with operations technology vendors.

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

Consulting Provider TrendsPeer Group Business & Operating Models

© 2017 ALM Media Properties, LLC 16

Consulting Market Trends

The different priorities and choices about approach, methods, and scope implied by the peer groups result in distinct patterns

of capability. The figure below compares the average capabilities of peer group members to illustrate these patterns. Note

that the capability levels of individual group members do not necessarily match the group average, but their respective areas

of relative strength and weakness do.

Among the four peer groups, industrial strategy is the least internally consistent – a consequence of the varying degree of em-

phasis these traditionally operations-focused providers place on production strategy. The group’s overall capabilities are mod-

erate, with notable strengths in obtaining internal client insights and solution delivery. Both qualities are reflections of these

providers’ more practitioner-oriented consultant profiles. Having the strongest overall capabilities, the market strategy group is

particularly noteworthy for its strengths in diagnostics, the strategic and management system components of solution design,

and enabling tools for executing and sustaining solutions. Although it demonstrates the weakest overall capabilities and the

highest variability across competencies, the information technology group dominates the information portion of operating

system capabilities and has substantial strength in the organizational portion of management system capabilities. Sharing with

the market strategy group the distinction of possessing the highest overall capabilities, operations technology stands out for

its strategy, operations, and governance solution design abilities. The group also leads in project management capabilities.

Consulting Provider TrendsPeer Group Relative Capabilities

Diagnostics

Solution Design

Solution Delivery

Strong

Moderate

Weak

Relative Capabilities of Consulting Peer Groups

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

© 2017 ALM Media Properties, LLC 17

Consulting Market Trends

Peer Group CorrelationsConsulting providers naturally do not fit neatly into one or another of these peer groups, but instead exhibit varying degrees

of strategic and service prioritization. The figure below indicates the correlations of individual providers’ capabilities to the

group averages. These correlations indicate how closely an individual provider fits the pattern indicated by its group and the

extent to which the provider evidences elements of other groups.

Consulting Provider TrendsPeer Group Relative Capabilities

Firm A

Firm B

Firm C

Firm D

Firm E

Firm F

Firm G

Firm H

Firm I

Firm J

Firm K

Firm L

Firm M

Firm N

Firm O

Firm P

Firm Q

Firm R

Firm S

Firm T

Firm U

Indu

stria

l Str

ateg

yIn

form

atio

n Te

chno

logy

Mar

ket S

trat

egy

Ope

ratio

ns

Tech

nolo

gy

Consulting Provider Peer Group Correlations

Source: The ALM Outlook: Production Strategy Consulting, ALM Intelligence

© 2017 ALM Media Properties, LLC 18

Consulting Market Trends

MethodologyOverview

ALM Intelligence has been researching the management, financial and IT consulting industry for over 40 years, studying

the global consulting marketplace at multiple levels. The resulting market analyses help buyers of consulting services to

effectively target best in class providers, and help consulting providers to identify and evaluate business opportunities.

The research is conducted around three primary dimensions:

■ Consulting Service Lines

■ Client Vertical Industries

■ Global Geographic Regions

The proprietary research methodology comprises four components:

■ Extensive interviews with consulting practice leaders, financial analysts, consulting clients, and clientside industry experts

■ Data and background material from the proprietary library of research on the consulting industry and individual firms

■ Quantitative data collection from primary and secondary sources

■ Key economic data relevant to the sector(s) being analyzed

The research output for a project is derived predominantly from primary research.

Data is obtained through a centralized effort, with teams of analysts collecting, assessing, fact-checking, and refreshing

baseline information on leading consultancies and consulting markets. This information populates an extensive knowledge

base of consulting providers, widely regarded as among the most comprehensive in the world.

Working collaboratively, analysts narrow their research to the most discrete and pertinent intersection of consulting service/

industry/geography.

The experience and knowledge of the analyst team are critical to the success of these research endeavors. Directors and

associate directors average over a decade of consulting and/or analyst experience, with an emphasis on professional services.

Junior analysts typically bring an average of five years of consulting and/or analyst experience.

The group’s long-term relationships with consulting clients and industry leaders are based on trust and respect. ALM

Intelligence’s fundamental goal is to deliver objective assessments and insightful viewpoints on the management, financial

and IT consulting market.

© 2017 ALM Media Properties, LLC 19

Consulting Market Trends

MethodologyHow We Evaluate Consulting Markets

ALM Intelligence’s goal is to deliver objective analyses to help providers of consulting services understand the structure and

prospects of the markets in which they compete in order to assess business opportunities and competitive threats.

ALM Intelligence evaluates consulting trends with respect to a particular consulting area in terms of the following elements:

■ Market Size & Outlook: What is the size of the market in the context of the consulting area? What are the distribution

and drivers of client spending across geographic regions and industry sectors? What is the outlook for market growth and

how might different scenarios alter the expected trajectory?

■ Market Structure: What is the distribution of providers in the market? How concentrated is the market? What are the

provider-level strategic dynamics that will shape market structure in the context of changes in demand, barriers to entry,

and returns to scale?

■ Client Demand Trends: What are the drivers of client demand? How do client needs influence the nature of consulting

solutions?

■ Consulting Provider Trends: What differentiates providers in terms of their consulting approaches and service delivery

models? How are providers positioned relative to client functions and activities? What differentiates providers’ business

and operating models? How do the attributes of different provider peer groups manifest in patterns of capabilities?

In addition to briefings with consulting buyers and providers, ALM Intelligence uses a mosaic approach to derive its findings.

This incorporates primary research conducted with industry practitioners, academics, and other experts and secondary

research on providers’ public information and other third-party sources of data and analysis.

© 2017 ALM Media Properties, LLC 20

Consulting Market Trends

About ALM Intelligence

ALM Intelligence provides accurate and reliable market sizing and forecasts on consulting services worldwide, needs-analysis

and vendor profiling for buyers of consulting services, timely and insightful intelligence on the top consulting firms in their

respective markets, and operational benchmarks that measure consulting performance. ALM Intelligence’s research spans

multiple service areas, client vertical industries, and geographies. Our analysts provide expert commentary at consulting

industry events worldwide, and offer custom research for Management Consulting and IT Services firms. More information

about ALM Intelligence is available at www.consulting.almintel.com.

ALM, an information and intelligence company, provides customers with critical news, data, analysis, marketing solutions and

events to successfully manage the business of business. For more information, visit www.alm.com.

About the S&O Consulting Research SeriesALM Intelligence’s exclusive, qualitative assessments of provider capabilities at the engagement level inform buyers of

consulting services competencies. The S&O consulting series explores competencies within the corporate development

and corporate functions segments. Corporate development consists of enterprise strategy, organization & operating model

strategy, finance, and mergers & acquisitions. Corporate functions comprises supply chain, sourcing & procurement, customer,

and research & development.

For further information and to purchase ALM Intelligence research, contact [email protected], 855-808-4550.