80

The Asian Banker Journal 1

The Asian Banker Journal 1

2 The Asian Banker Journal

The Asian Banker Journal 3

The Asian Banker Journal is published six times a year by

TAB INTERNATIONAL PTE LTD Incorporated in Singapore

Trendwatch Strategic thinking for Chinese banks is less diverse than it appears.

Noteworthy 8A selection of comments made by protagonists in the industry as it faces new challenges and further consolidation.

Current Account 10• Merger activity takes off in Taiwan• Many banks still seen missing ISO15022 deadline

Bank Notes 12• DBS TD Waterhouse expands in China• GE Capital’s latest acquisitions

Personal Account 16Dr Rozali Mohamed Ali, managing director and CEO of Bumiputra-Com-merce Bank discusses the benefi ts of outsourcing operational functions.

Operations & Technology 64Regional survey fi nds that most banks in fact treat CRM as a ‘nice to have.’

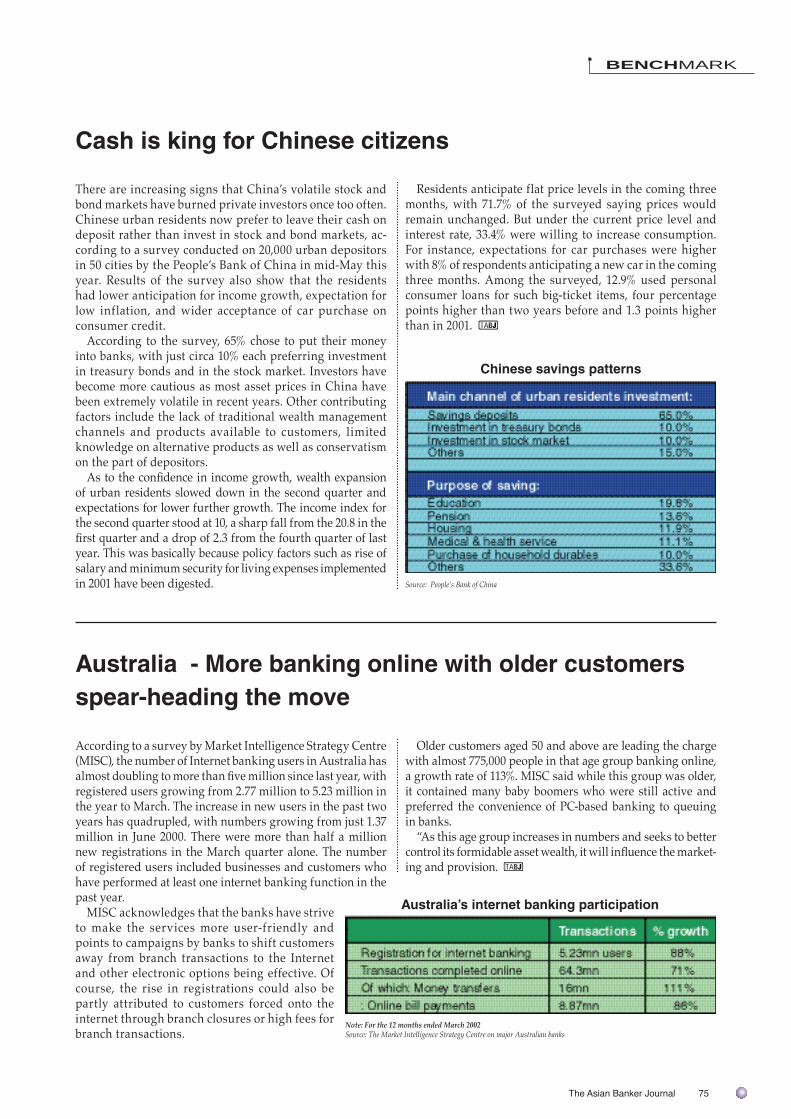

Benchmark 75• Chinese investors stay liquid• Internet banking in Australia doubles• Bankruptcies in Hong Kong rocket• Taiwanese regulator gets tough

Regular People 73Ratings Update 77Data File 78

Founder and Editor-In-ChiefEmmanuel Daniel l [email protected]

General EditorMatthew Taylor l [email protected]

Online EditorDiane Jorolan l [email protected]

Senior Researchers, ResearchFahim Uz Zaman l [email protected]

Edwin Basuki l [email protected] Ahmad l [email protected]

Li-May Chew l [email protected] Ee Eu l [email protected] Yih Lin l [email protected]

DirectorMei Fong, Chin Tel: (65) 6295 7302

[email protected], Global Client Services

Cyrus Daruwala Tel: (65) 6295 [email protected]

Business Development ManagersIeuan French Tel: (65) 6295 7310 (Research)

[email protected] Seng Tel: (65) 6295 7307 (Publication)

[email protected] Services

Jodine Phua Tel: (65) 6295 [email protected]

Subscription SalesJenny Kwong Tel: (65) 6295 7300

[email protected] & Database Administrator

Ivy Tan Tel: (65) 6295 [email protected]

Graphics & LayoutValen Siew Tel: (65) 6295 7313

Janet Chan Tel: (65) 6295 [email protected]

Advertising RepresentativesHong Kong: Godfrey Wu (MHI)

Tel: (852) 2591 1077 Fax: (852) 2572 [email protected]

USA: John Barrios (World Publication Services)Tel: 1 (201) 531 0760 Fax: 1 (201) 531 0827

[email protected] in Singapore by

Xpress Print Pte Ltd

MITA (P) 078/10/2002 (Singapore)KDN PPS 1301/9/2001 (Malaysia)

ISSN 02189615

Copyright Protected. Reproduction in any form prohibited except with permission.

For reprints, please call (Singapore) (65) 6295 7314

We are moving!We are pleased to inform our readers that in order to accommodate

the needs of our expanding business, our new address with effect from 1 October 2002 will be:�������������� � �������������������

10, Hoe Ching Road#14-06 Keppel Tower

Singapore 089315Tel: 65-62366500 Fax: 65-62366530

Editorial Offi ce:10 Hoe Chiang Road, #14-06, Keppel Towers, Singapore 089315

Tel: (65) 6295 7301/3/8/9/10 (Editorial); (65) 6295 7302/7 (Marketing); (65) 6295 7300 (Subscriptions); Fax: (65) 6295 4600

www.theasianbanker.com

4 The Asian Banker Journal

Cancellation Policy: • No refunds will be given for cancellation of The Asian Banker subscriptions.

Send in your subscription:By Fax: (65) 6236 6530, Telephone: (65) 6236 6500, E-mail: [email protected] orBy post to: T.A.B. International Pte Ltd 10 Hoe Chiang Road, #14-06 Keppel Tower, Singapore 089315

SUBSCRIPTION FORM

To receive our E-Newsletters, sign up at www.theasianbanker.com

I WISH TO PAY(PLEASE COMPLETE THIS SECTION)

❏ MasterCard ❏ Visa ❏ American Express ❏ Diners Club

Card No.: Expiry Date:

❏ By a non-negotiable cheque made payable to:

“TAB International Pte Ltd”

❏ Please invoice us

Amount: Cheque No.:

(add 4% GST for Singapore subscribers)

Issuing Bank:

Signature: Date:(As in credit card, if applicable.)

Name:

Designation:

Organisation:

Address:

Postal Code: City/Country:

Tel: Fax:

E-mail:

I would like (Please tick the appropriate box): ❏

❏ One-year subscription to THE ASIAN BANKER 300PLUS at US$620 which includes:• CD ROM (Excel format) and online access to database of Asia’s top 300 banks balance sheets• One year subscription to Asian Banker Journal (worth US$240)• Interactive access to Asian Banker Journal online edition for up to fi ve executives (worth US$490)

❏ One-year subscription to THE ASIAN BANKER JOURNAL only at US$240 which includes: • Six issues of Asian Banker Journal (bi-monthly)• Interactive access to online editions (subscribed issues) for up to fi ve executives (worth US$490)

The Asian Banker 300 Asian Banker Research is proud to present its inaugural ranking of the region’s top 300 commercial banks by asset size.

18

Interview Hsu Teh-Nan, President and CEO of Hua Nan Finan-cial Holding Company, discussed how Hua Nan has positioned itself for the future under its new holding company structure, progress on resolving NPLS, and the ongoing challenges of balancing political and commercial necessities.

68

Hsu Teh-Nan, Presi-dent and CEO of Hua Nan Financial Holding Company

The Defi nitive Annual Ranking and Survey of Asia’s Top Banks

The Asian Banker Journal 5

Hong Kong Convention & Exhibition Centre2 - 4 April 2003

w w w . t h e a s i a n b a n k e r . c o m

The summit to identify challenges and opportunities leaders in the fi nancial services industry will face in 2003 and beyond

For more information on sponsorships and exhibition opportunities,

please contact Mr. Cyrus Daruwala, Director, Global Clients Services at

tel: (65) 6236 6522, fax: (65) 6236 6530

or e-mail: [email protected]

“ Excellence in Process and Profi tability ”

6 The Asian Banker Journal

TRENDWATCH

China’s convenient conundrumIn the past year alone, I must have met CEOs of about 12 Chinese banks and countless senior executives, and the one signifi cant observation that I would make is just how synchronized the motivation of so many bankers in China appear to be these days.

All Chinese banks CEOs tell me that they are committed to adopting IAS accounting stand-ards, if they have not already done so. All are committed to transparency, shareholder value, corporate governance and all those darling phrases for investor confi dence.

To a standard question in my interviews and conversations, “which bank do you admire most?” the answer from bankers, whether from Beijing or Shanghai or Shenzen was unequivo-cally, “Citibank.”

Before any Citibanker uses this to fl utter their feathers, let me just say that my suspicion is that many Chinese bankers are spouting safe received opinion rather than bestowing considered admiration. It’s the same thing as associating the pianist Richard Clayderman to good music. A convenient name to swirl a decent conversation around in a pub without the inconvenience of the facts.

However, if the Chinese are still developing their perception of global issues, they are learning and learning very fast. I have seen a greater desire and even ability amongst Chinese bankers to develop proper “domain capabilities” in critical areas such as treasury, risk management and

operations than I have ever seen in non-China Chinese communities like Hong Kong and Taiwan.

I have watched the Chinese take the time to learn, to send their staff for training, to aspire to global best practices and to execute as quickly as their own regulators will allow them to.

In many cases, I have come away awed that many of the same CEOs of many Chinese banks who are so committed to market principles today were just a decade ago languishing as _’professors’ in state-owned universities or civil servants in a very socialist society.

In the development of my own assessment of the quality of Chinese banks and businesses, I am currently straddling two realities. On the one hand, I see the Chinese propensity to be a shameless consumer of global ideas - especially if they are branded ideas from America. To borrow from the title of a V.S Naipaul novel, they are “the mimic men.” On the other hand, I see the ability and the energies for the Chinese to create world class institutions, if they really wanted to.

There is no reason that we should not see such Chinese institutions within the next ten years. The current ambition of ICBC Bank, the country’s largest, to consolidate 1000 data centers into two within the year is a feat that has never been achieved anywhere else in the

world, but symptomatic of the kind of energies that banks in China are exhibiting.But there is the big ‘ what if’. Will we fi nd, after yet another decade of promises, the

Chinese banks in this millennium ending up similar to the Indonesian banks after the promises of the 1990s? Both are large countries. Both lure the rest of the world on the promise of their large population.

But understandably, both have their fair share of suave and self-serving men and women, just like the rest of humanity, no matter what is said about their national aspira-tions. It is a melancholy that I share with every private equity company looking to buy into Chinese banks today.

I guess I would think differently, if I could engage with a Chinese CEO about commitment or excellence, without referring to Citibank, or Richard Clayderman.

Source: State Statistical Bureau, Asian Banker Research

The non-state banks in China are very profi table these days (ROEs of Chinese businesses 2001)

The Asian Banker Journal 7

CALENDAR

• CeBIT Asia~ 2 - 5 September, Shanghai, Hannover Fairs • China Int’l Exhibition on Financial Banking Technology &

Equipment (CIFTEE)~ 15 - 18 September, Beijing • SmartCard Expo~ 18 - 20 September, New Delhi, Electronics Today • Sibos~ 30 September - 4 October, Geneva, S.W.I.F.T • Asia Pacifi c Financial Planning Conference~ 10 - 11 October, Singapore, Asia Financial Planning Journal • Backroom Operations For Financial Institutions~ 28 - 29 October, Singapore, The Asia Business Forum • Customer Retention in Banking & Finance~ 28 - 29 October, Singapore, The Asia Business Forum • Bancassurance~ 7 - 8 November, Singapore, The Asia Business Forum • CHINA Fund Management~ 18 - 19 November, Singapore, The Asia Business Forum • 4th bank.net~ 27 - 28 November, Mumbai, Exhibitions India Pvt. Ltd. • The Fourth Annual “The Asian Banker Summit”~ 2 - 4 April 2003, Hong Kong, The Asian Banker

Visit www.theasianbanker.com for the latest Calendar Updates.

LETTERS TO THE EDI-

I refer to the correction printed in the the Asian Banker Journal Issue 35 regarding our letter (relating to the article “Singapore: Consumer Credit business to share positive repayment informa-tion”). In order to refl ect the charge-off ratio for Singapore, in comparison with those reported for Hong Kong, the correct methodology would be the annualised percentage of “sum total of bad debt written off (for the quarter) against the rollover balance (position at the end of the quarter).

Annabel TanMarket Infrastrusture and risk advisoryMonetary Authority of Singapore (MAS)

EDITORIAL RESPONSE: Making cross border comparisons can be problematic because different countries calculate ratios in different ways and it is important not to compare apples with pears. Our numbers are different only because Hong Kong uses “total billings” as the denominator and Singapore uses “roll over balance”. We understand MAS’s rationale for using roll-over charge-off calculated as a fl ow, but, as we suggested last month, we do not have access to fi gures for Hong Kong calculated this way. Because Hong Kong uses total billings, we needed to compare like with like so we had to use sum total of bad debt against total billings for Singapore.

Singapore’s approximate charge-off for 1Q2002 (using rollover balance):= [Bad debts written off (Jan-Mar)/Rollover balance (Jan-

Mar)]/12 months=(7.8+8.0+8.1)/(2098.5+2193.6+2120.6)]/12 = 4.5% Charge-off ratio (using total billings) - As per Hong Kong’s

method:= [Bad debts written off (Jan-Mar)/Total card billings(Jan-

Mar)]/12 months= [(7.8+8.0+8.1)/(959.8+887.7+938.8)]/12 = 10.29%

LETTERS TO THE EDITOR:Fax to 65-6236 6530 or

e-mail: [email protected]

8 The Asian Banker Journal

NOTEWORTHY

A selection of comments made by protagonists inthe industry in the thick of battle in the past two months.

“ Banks can share their technology instead of each bank trying to re-invent the wheel. ”- Vepa Kamesam, deputy governor of the Reserve Bank of India, encouraging banks to pool in their technology resources instead of each putting up its own IT network

“ We are still at an early stage when it comes to co-operative ventures with the Bank of China on the credit card business. Right now only debit cards are in circulation in mainland China, The credit card product as we know it, is not yet available in this country. ”- Peter Wong, director of Standard Chartered Bank and head of Greater China operations, explaining the status of StanChart’s discussions with Bank of China about cooperative ven-tures, which would include credit cards. (With photo from StanChart)

“ No ... That’s why we decided to get married with a good bank fi rst, before all the pretty girls are married and you only have the ugly girls left. ”- Richard Tsai, Fubon Financial co-chief executive, on whether he would be willing to buy a bad bank and restructure it to realise its remaining value. Fubon Financial recently announced it would include Taipeibank in its holding company through a stock swap.

“ The sky won’t collapse. ”- Liu Jinbao, chief executive of Bank of China (Hong Kong), shaking off thoughts that woes in the US market could have affected the bank’s own IPO launch in July 25 this year.

“ Simply because we are the biggest bank in Singapore with the most customers ... on a probability basis it’s the highest for DBS. ”- Edmund Koh, managing director and head of consumer banking at DBS Bank, explaining why the recent Internet fraud cases in Singapore involved customers from DBS Bank.

The Asian Banker Journal 9

10 The Asian Banker Journal

CURRENT ACCOUNT

Taiwan: Merger news raise consolidation hopes Fubon Financial and Cathay Financial’s merger announcements with Taipeibank and UWCCB, respectively, signal that consolidation in overbanked Taiwan may fi nally be gathering pace.

When Fubon Financial announced its merger arrangement with Taipeibank last week, observers remarked that Taiwan had finally recommenced the consolidation process in its financial sector, which has been seeing slow progress of late. A few days later Cathay Financial Holdings announced its own merger plans with United World Chinese Commercial Bank (UWCCB), boosting sentiments that consolidation in Taiwan’s banking sector was on a roll.

The concept of financial holding companies (FHCs), however, is still under question - especially in Taiwan, where more than a dozen banks and insurance companies have converted to FHCs in late 2001 and early 2002. But not all these FHCs have displayed the progressive cross-selling skills of Fubon Financial, which claims that it sells 2.7 products per customer on average. If these new tales of acquisition result in a new rash of such mergers, Taiwan will fi nally fi nd out if the fi nancial holding structure is the best mechanism to drive consolidation.

”Despite the relatively small size of our existing banking platform, we have already had considerable success in

cross-selling a wide range of products through Fubon Bank, which is now de-riving over 25 percent of its revenue from fee-based products. Similarly, we see very signifi cant opportunities to increase fee-based income at Taipeibank,” said Richard Tsai, Fubon Financial’s co-chief executive offi cer.

”Over time, we expect to be able to increase Taipeibank’s traditional gross fee income ratios from 8 percent in 2001 [excluding gains] to levels more consist-ent with Fubon Bank, which posted a gross fee income ratio of 26 percent in 2001 [excluding gains],” Tsai said.

Taipeibank has 80 branches servic-ing 1.3 million clients, and assets of NT$654 billion.

The $2.4 billion deal between Fubon Financial and Taipeibank was shortly fol-lowed by Cathay Financial’s own merger announcement with UWCCB.

Cathay Financial’s and UWCCB’s merger, based on a stock swap valued at NT$114.6 billion ($3.4 billion), will create the fourth largest fi nancial institution in Asia (excluding Japan) and is the larg-est acquisition for a corporate entity in Taiwan. Cathay Financial, which con-

trols Taiwan’s biggest life insurer, said it expects to fully integrate UWCCB with Cathay United Bank by 2005, and the new company will have combined assets of NT$2,100 billion ($62.2 billion). The share-swap deal will also reportedly create Taiwan’s largest life insurance provider, and third-largest domestic credit card issuer.

”Bot h inst it ut ions wi l l benef it from a more highly developed bancas-surance channel, and from the ability to cross-sell products over a wider distribu-tion platform to more retail and corporate customers,” said UWCCB chairman Gre-gory Wang. Cathay Financial’s cross-sell ratio per customer stands at 1.3.

Doubts about the financial sector’s consol idat ion process were aired earl ier when the planned merger between Taishin Financial and Shin Kong Financial was scrapped less than two weeks after its announce-ment. In July, state-owned Bank of Taiwan, Land Bank of Taiwan and Central Trust of China had also re-jected a government-initiated merger plan, saying they would benefit mini-mally from the consolidation.

S.W.I.F.T. creates MUG for ISO 15022 laggards Currently only 30 percent of the world’s traffi c of S.W.I.F.T. securities messages is on ISO15022.

Too many banks will not be ready for ISO15022 compliance on time, so S.W.I.F.T. have been forced to deploy delaying tactics. Although there will be a big surge as many complete testing in the next three months, at the current rate this only looks like getting to about 50-60 percent by the November 16 deadline rather than the 90 percent plus expected by S.W.I.F.T.

Beyond November 16, users that have not migrated to the new ISO 15022 stand-ard will be charged a higher fee. The group, which will be discontinued on May 31, 2003, will be charged up to 1 euro (98 US cents) per message sent after November 16 this year. These users will be charged a monthly fee starting from 5,000 euros ($4,911), which will increase depending on the size of the institution and the proximity

to the May 31, 2003 closure date. The fee can rise to as high as 45,000 euros ($44,199).

S.W.I.F.T., which announced this month that it would stick to its original deadline for ISO 15022 migration, has created a Messag-ing User Group (MUG) for those that have yet to migrate to the new standard. The ISO 7775 MUG - a closed user group of non-ISO 15022 users - will be created separate from the main S.W.I.F.T. network.

The Asian Banker Journal 11

SPONSORED STATEMENT

Customer Centric Universal Banking

Risk and Profi tabilityBanks are paid to take risk. Yet the abil-ity of banks to monitor risk and return has become impaired, as business lines become more complicated and diverse. Banks need to develop new and effec-tive tools to manage the risks inherent in their various businesses. These risks include market risk, credit risk and operational risk. The risks a bank takes in its lending are intrinsically tied to the bank’s profi tability, as interest and fee income remains the core sources of earnings for banks.

Managing the plethora of information churned out by ever expanding portfolios of different businesses has turned risk management into an increasingly diffi cult task. As different departments of banks have established their own data monitor-ing and processing systems it has become very hard for risk managers to collate a coherent aggregate risk profi le for the banks’ businesses. Banks need now to as-sess the value provided by each customer across multiple channel business lines. This has created a need for better integration of technology infrastructure. Accordingly, bank’s have been driven to seek out inte-grated and extended enterprise customer centric software solutions such as System Access’s SYMBOLS.

SYMBOLSThe SYMBOLS product offers a solution that supports seemless integration of business operations across extended enterprises from back-offi ce operations support to front-end customer relation-ship management and personalized delivery of customer services. For risk management professionals there are specifi c modules, within the SYMBOLS Enterprise Operations Center, to allow bankers to set and monitor limits for individual exposures as well as sophis-ticated knowledge management tools to enable storage and easy retrieval of important information relating to the bank’s risk profi le.

The SYMBOLS Enterprise Operations Center consists of a comprehensive suite of applications that effi ciently support

the transaction processing needs of fi nancial institutions. The Limits control module allows the bank to control and monitor its risk exposures effectively on a client by client basis as well as providing a holistic picture of the risk profi le.

The SYMBOLS Limits Control Module provides the capability to manage credit and currency exposure limits at multiple product and geographic levels across the entire customer relationship. The customer can use many forms of credit and transact in multiple currencies while managing a complete exposure. SYMBOLS Limits Control also allows the fi nancial institution to manage its risk specifi cally with mobile high net worth and corporate customers. Exposures are monitored on-line with corresponding ability to approve or reject limit excesses. Specifi c account limits are maintained in the individual module translations. Client exposures, however, can span multiple credit facilities, across other SYMBOLS modules and including non-SYMBOLS legacy applications. The Symbols Limit Control module enables the user to grant faculties in a four level hierarchy of limits to any client or client group, employ limits against the bank’s total exposure to any product or line of business, and limit exposures in specifi c countries.

As well as monitoring and managing levels of risk, the SYMBOLS Enterprise

Operations Center has knowledge management functions that can help the bank to assess risks more ef-fectively. THE SYMBOLS Knowledge Manager provides an enterprise OLAP data-warehousing framework designed to specifi cally support fi nan-cial institutions in their enterprise data analysis and knowledge management needs. It provides a comprehensive database schema that captures and consolidates financial services op-erational data from other SYMBOLS systems or third party operational systems for further analysis.

The data store schema, with its suite of subject area data marts, supports en-terprise level analysis ot the financial institution and their customers. Based on user-defined rules and parameters, non-technical users can perform multi-dimensional drilldown and analysis of collated data to gather better intelligence to support their business and customers.

About System AccessSystem Access is a leading global fi nancial software provider of customer centric universal banking solutions for fi nancial institutions worldwide. Head-quartered in Singapore, it has regional offi ces in Geneva, London, Bratislava, Prague, Dubai, Manila and Bangkok with a staff of more than 400 to service the needs of customers in over 20 coun-tries across the Asia Pacifi c, Europe, Middle East and Africa.

Its fl agship product, SYMBOLS is the result of more than 800 man-years of extensive research and product develop-ment, and has a solution suite of over 30 modules designed to meet the needs of universal banking.

For more information or a copy of the Customer Centric Univer-sal Banking white paper, please contact System Access: Phone 65 6333-4533Email: [email protected]

The Asian Banker Journal 11

12 The Asian Banker Journal

BANKNOTES

base in its twin markets of Singapore and Hong Kong. Struthers declined to reveal the exact number of customers in each market, but put the total customer base at 45,000 with the bulk of the customer base in Singapore.

“We’ve been experiencing 30 percent annualized growth in the number of customer accounts since the start of the joint venture,” said Struthers. “Experience in other markets tells us that we need to build a customer base of at least 160,000 in the fi rst three years to be successful.”

This growth will primarily come organically, but he does not rule out the possibility of acquiring customer portfolios from other market players. This scenario plays itself out especially in Hong Kong, where the market is, in Struthers’s own words, “a slow, steady build” because of the fragmented nature, but also in Singapore, where analysts have been predicting a market shakeout

China is a market that online broker-age DBS TD Waterhouse is looking at, but the joint venture company be-tween Singapore-based DBS Bank and Canadian-based discount brokerage TD Waterhouse will move cautiously to explore the opportunities, says its CEO Ian Struthers in an interview.

“We’re very excited about the oppor-tunities in China and want to explore them. However, we’re moving cautiously and China is something we’ll build [sic] within the next few years,” he said.

Struthers said that the most obvious way to enter the China market was to tie up with a player that already has a presence and gives access to a sizable customer base. However, this was not the only way and added that DBS TD Waterhouse was “looking at a few dif-ferent models.”

In the meanwhile, DBS TD Waterhouse is concentrating on building its customer

Online Brokerage

China in a few years, says DBS TD WaterhouseDBS TD Waterhouse CEO Ian Struthers thinks long-term about China, even as he builds the franchise in Singapore and Hong Kong.

given the still-low trading volumes and price competition.

“While we are not looking at acquisi-tions as our main growth strategy, we’re very comfortable valuing portfolios, given our experiences in other markets,” he qualifi ed. “If opportunities arise, we’ll look seriously at them.”

When the high-profi le marriage be-tween Merrill Lynch and HSBC dissolved in tears, sceptics were already prepar-ing to sound the death knell for DBS TD Waterhouse, which they viewed as inhabiting a similar business model - a view that Struthers rejects.

He said, “From a business perspective, the joint venture between Merrill Lynch and HSBC failed for a simple reason. The premise of the joint venture was to gain access to a large number of existing custom-ers, which Merrill Lynch and HSBC did not achieve. Merrill Lynch did not afford access to its U.S. customer base, while the joint venture competed with HSBC’s own online brokerage for business in Hong Kong.”

“I don’t see how you can succeed if you can’t gain access to customers in your most important markets.”

Struthers said DBS TD Waterhouse will continue to focus on and leverage on its strengths - the strong presence of DBS Bank in Singapore and Hong Kong, and the ability to trade in multiple markets with a single account.

fi nance company SDL Leasing Singapore from UBS Capital Asia Pacifi c, and AGC from Westpac Banking Corporation. The deals gave GE Capital an increased foot-print in the auto fi nance business in Sin-gapore, and more than doubled its pres-ence in Australia and New Zealand.

Said Steve Bertamini, president of GE Capital Asia: “SDL provides an established platform for the growth of GE Capital in Singapore. We plan to continue to expand its auto fi nance business and to introduce

GE Capital, a unit of General Electric Co. of the US, has followed up its recent acquisitions in Singapore and Australia with a reported negotiation to buy a con-trolling stake in the credit card business of South Korea s Chohung Bank.

A Chohung Bank offi cial named GE Capital as being one of two parties inter-ested in purchasing a controlling stake in the South Korean bank s credit card unit, which it is planning to spin off.

Last month, GE Capital acquired auto

Acquisitions

GE Capital continues expansion in AsiaGE Capital had continued to add key acquisitions to its portfolio in Asia’ including NPL portfolios. It is also actively involved in outsourcing back offi ce operations.

customers to a broader range of consumers and commercial fi nance products.”

He also said GE Capital will “con-sider acquisitions that will fast track our growth in this promising and stable market.”

GE Capital’s business in Asia includes consumer fi nance, commercial fi nance, the acquisition and restructuring of non-performing loans, aircraft leasing and equity business. The company has purchased portfolios of non-performing loans in Thailand and is looking at buy-ing portfolios of such loans in Taiwan, South Korea and China.

Elsewhere in Asia, GE Capital has out-located its back-office operations in India It has 9,000 employees in Delhi and Hyderabad, and has plans to more than double this number to 20,000 by next year. GE Capital is also reportedly planning to outsource jobs such as risk analysis, insurance accounting and bill payment to India.

The Asian Banker Journal 13

14 The Asian Banker Journal

PERSONAL ACCOUNT

Planning for the integration was a major exercise

The following is extracted from an interview with Dr Rozali Mohamed Ali, managing director and CEO of Bumiputra-Commerce Bank, Malaysia, describing how the lessons learnt from developing e-business and outsourcing solutions have liberated the intellectual capital of the bank.

harmonization of systems and develop-ment of culture. It was inevitable that this was a time of trauma. A merger event is a dislocation in evolution. But very early on, we felt that we wanted to do as much as we could to transform the bank. Now, transformation means all kinds of things. What we really wanted to do was to create an operating model for a stronger bank. The short-term challenges were indeed rather serious, but we also strove to address the longer-term struc-tural challenges. We had to consider the liberalization of the fi nancial sector in our country, the convergence of fi nancial services, the entry of non-banks, some structural shifts away from lending as far as banks are concerned, as well as shifts induced by demographic changes. The merger presented us with an opportunity to tackle these issues.

So in 1999 when we were planning the merger, quite apart from the specifi c issues of merger integration and so on, we felt we had to do a lot more to build the foundations of the future bank. First of all, we needed to remove the legacy or-ganizational structures. They were rather traditional and had lost some shape with the passage of time. We instituted a complete review of all functions and a complete reorganization of the way in which we did things.

The creation of the new Islamic bank, Bank Muamalat Malaysia Berhad, took over many of the duplicate branches. But most of the operational work; such as the back offi ce, and processing was still be-ing duplicated. One of the major moves in the reorganization was to centralize or regionalize all the processing work, taking away the back office from the branches. This process was completed just over a year ago.

Centralization of processing neces-sitated a cultural shift, as the branches

The fi nancial crisis was a very diffi cult time for the economies of the region and of this country, and clearly for the banks. It also provided an opportunity for the country to restructure and reinvigorate its bank-ing sector. Directly or indirectly, because of the crisis, we were able to contemplate undertaking the merger between Bank Bumiputra and the Bank of Commerce.

Having been presented with this op-portunity, we saw the merger process as more than merely an aggregation of two banks. Obviously, there are the standard things that go into any merger - such as

Dr Rozali Mohamed Ali, managing director and CEO of Bumiputra-Commerce Bank, Malaysia

Editor’s note: Bumiputra-Commerce Bank, the second largest bank by assets in Malaysia, was established on October 1 1999, as the result of a merger of the former Bank Bumiputra Malaysia Berhad with Bank of Commerce. The government also created a third entity, Bank Muamalat, a new Islamic bank from some of the branches that overlapped when the two banks were merged.

The Asian Banker Journal 15

PERSONAL ACCOUNT

moved away from operations towards sales and service, with a greater degree of customer orientation. Quite apart from this cultural shift, which always occurs when two organizations merge, we saw the need for a broader shift, towards a more effective workforce. The typical bank worker of the future will be very, very different from the bank worker of today. The modern bank worker has to be able to exercise initiative much more. He or she will be conversant with some rather sophisticated tools of analysis and marketing as well as being versatile and fl exible.

As is typical in any merger situation, staff morale was rather low. There was a desire to maintain the status quo with the least possible change because anything else is uncomfortable. Through discus-sions with our staff (and also with the unions, which represent them) we were able to reach a common understanding of the need to upgrade all the people who work for us. Not just in the sense of having new certifi cates or getting a few more dollars a month, but really upgrade in terms of their ability and the way in which they approach work and the way in which they feel fulfi lled at the work that they do. Instituting this type of change is a slow process. It has to be managed very sensitively, but basically I think we’re on the right track.

Predictably, there was a fall in the number of staff last year when we em-barked on a voluntary separation exer-cise. We reduced staff numbers by about 20 percent. In any merger, that is essen-tial. More importantly, the age profi le of the staff has changed. It is now a little younger. The profi le of skills in the sense of higher, tertiary level skills and others is also in the process of changing. Now we have a reasonably stable structure, infusing younger and different talents, which was something that was diffi cult before the merger. It has also allowed us to embrace the latest strategic thinking and techniques.

The e-business is one important stra-tegic initiative that we have been devel-oping and leveraging since the date of the merger. Our e-commerce initiative is improving the reach and the ability to deliver of the bank. It has also allowed us to improve the actual running of the bank itself.

We created a group with specifi c and exclusive responsibilities called the

I-Commerce Group for this purpose. Establishing a separate unit was im-portant because activity related to the merging of the IT platforms threatened to submerge other initiatives. It is still a relatively small group of people but they are allowed and they are able to focus on this particular area and actually, they have done extremely well.

The trouble, of course, with building these kind of capabilities is that you are constrained because you have to justify them from a business-case point of view. Many internet banking initiatives tend to fail because the pick-up is too slow or the performance numbers don’t really meet expectations. We focus about 50-50 on products and delivery (like internet banking) and the other half on building an Internet infrastructure.

Developing an e-business platform doesn’t make much sense if we tell eve-rybody it’s so good but we don’t use it ourselves; particularly now that we have a unique and very effective integrated system for procurement and inventory. So we have in fact committed ourselves to using this to run our own business. We can expect good returns from that investment purely on the basis of our own utilization. But, of course, primarily it is for the customers, and the custom-ers are beginning to realize that this is an extremely good way of running their businesses too.

Planning for the IT integration was a major exercise because, in banking, you’re talking about millions of ac-counts, where you cannot afford to have a single mistake when you merge the systems. It’s particularly data intensive and, unfortunately for us, we merged in 1999. So we had to take extra precautions for Y2K and couldn’t really start the inte-gration process until a few months into the year 2000. But around the middle of last year, we achieved full integra-tion. That was another major exercise, because we knew that sooner or later we would have to fi nd a way to manage these areas more effi ciently.

In our organizational structure, the operations and IT unit was essentially autonomous, so we began to look at he possibility of outsourcing this function, almost immediately post-merger. There are many reasons why we wanted to do this. One of them is obvious. Manag-ing IT is a specialist job which banks may not be very good at doing unless

Mancano And Associates

.......The best boutique search fi rm on Boat Quay

Mancano And Associates is an established recruitment fi rm specializing in the fi nancial service and telecommunications industry. We are consistently retained by Fortune 500 institutions throughout South East Asia for our industry expertise. Mancano And Associates discreetly researches and recommends Asian experienced senior management professionals with extraordinary qualifi cations.

•Burma•Cambodia•Hong Kong•India•Indonesia•Malaysia

•Australia•Philippines•Singapore•Sri Lanka•Thailand•Vietnam

Banking & Financial

•Investment Banking•Corporate Finance•Direct Investment•Corporate Banking•Private Banking•Banking Operations•Equities•Fund Management•IT Banking System

Telecommunications

•Wireless Local Loop•Private Telephone & Telegraph•Paging•Cellular / Satellite•Network Management System (NMS)•Radio Network Planning•Installation Planning•Radio Base Station/Transmission Engineers

Mancano And Associates45A Boat Quay Singapore 049834 Tel: 6533 8128 Fax: 6533 0079

e-mail: [email protected]: www.mancano.com

Our consultants have executed assignments in:

Assignments undertaken:

16 The Asian Banker Journal

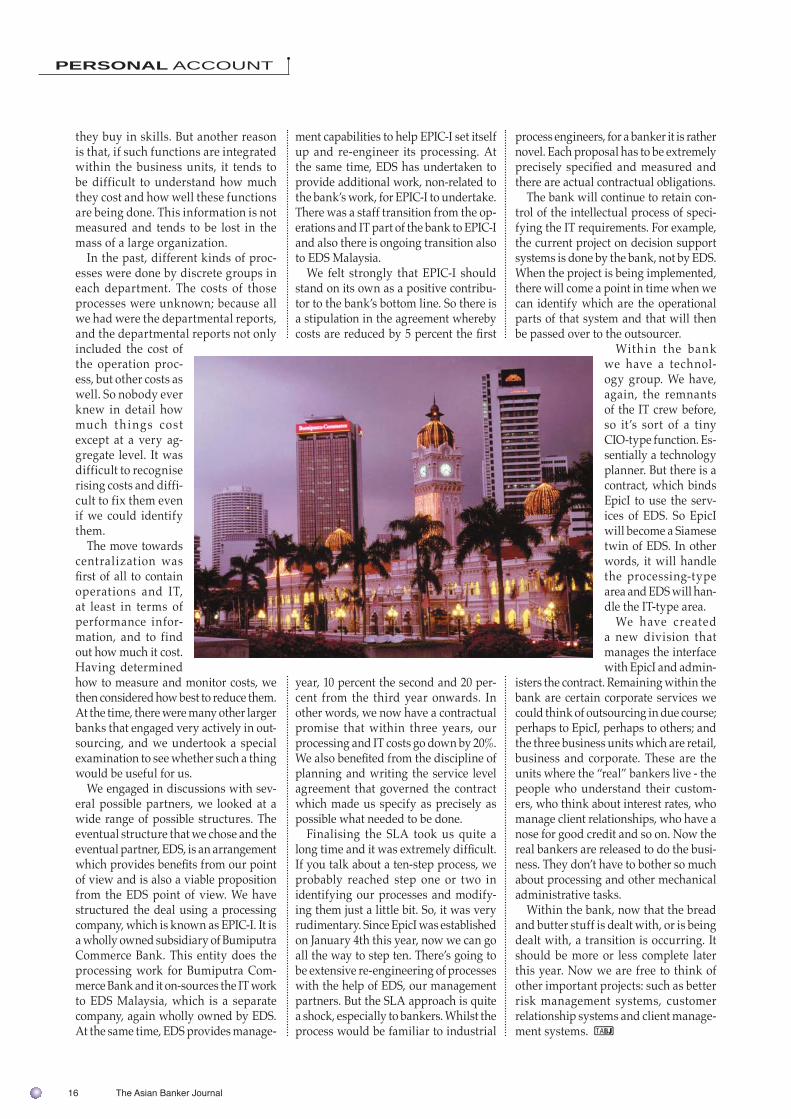

they buy in skills. But another reason is that, if such functions are integrated within the business units, it tends to be difficult to understand how much they cost and how well these functions are being done. This information is not measured and tends to be lost in the mass of a large organization.

In the past, different kinds of proc-esses were done by discrete groups in each department. The costs of those processes were unknown; because all we had were the departmental reports, and the departmental reports not only included the cost of the operation proc-ess, but other costs as well. So nobody ever knew in detail how muc h t h i ngs cost except at a very ag-gregate level. It was difficult to recognise rising costs and diffi-cult to fix them even if we could identify them.

The move towards centralization was fi rst of all to contain operations and IT, at least in terms of performance infor-mation, and to find out how much it cost. Having determined how to measure and monitor costs, we then considered how best to reduce them. At the time, there were many other larger banks that engaged very actively in out-sourcing, and we undertook a special examination to see whether such a thing would be useful for us.

We engaged in discussions with sev-eral possible partners, we looked at a wide range of possible structures. The eventual structure that we chose and the eventual partner, EDS, is an arrangement which provides benefi ts from our point of view and is also a viable proposition from the EDS point of view. We have structured the deal using a processing company, which is known as EPIC-I. It is a wholly owned subsidiary of Bumiputra Commerce Bank. This entity does the processing work for Bumiputra Com-merce Bank and it on-sources the IT work to EDS Malaysia, which is a separate company, again wholly owned by EDS. At the same time, EDS provides manage-

ment capabilities to help EPIC-I set itself up and re-engineer its processing. At the same time, EDS has undertaken to provide additional work, non-related to the bank’s work, for EPIC-I to undertake. There was a staff transition from the op-erations and IT part of the bank to EPIC-I and also there is ongoing transition also to EDS Malaysia.

We felt strongly that EPIC-I should stand on its own as a positive contribu-tor to the bank’s bottom line. So there is a stipulation in the agreement whereby costs are reduced by 5 percent the fi rst

year, 10 percent the second and 20 per-cent from the third year onwards. In other words, we now have a contractual promise that within three years, our processing and IT costs go down by 20%. We also benefi ted from the discipline of planning and writing the service level agreement that governed the contract which made us specify as precisely as possible what needed to be done.

Finalising the SLA took us quite a long time and it was extremely diffi cult. If you talk about a ten-step process, we probably reached step one or two in identifying our processes and modify-ing them just a little bit. So, it was very rudimentary. Since EpicI was established on January 4th this year, now we can go all the way to step ten. There’s going to be extensive re-engineering of processes with the help of EDS, our management partners. But the SLA approach is quite a shock, especially to bankers. Whilst the process would be familiar to industrial

process engineers, for a banker it is rather novel. Each proposal has to be extremely precisely specifi ed and measured and there are actual contractual obligations.

The bank will continue to retain con-trol of the intellectual process of speci-fying the IT requirements. For example, the current project on decision support systems is done by the bank, not by EDS. When the project is being implemented, there will come a point in time when we can identify which are the operational parts of that system and that will then be passed over to the outsourcer.

Within the bank we have a technol-ogy group. We have, again, the remnants of the IT crew before, so it’s sort of a tiny CIO-type function. Es-sentially a technology planner. But there is a contract, which binds EpicI to use the serv-ices of EDS. So EpicI will become a Siamese twin of EDS. In other words, it will handle the processing-type area and EDS will han-dle the IT-type area.

We have created a new division that manages the interface with EpicI and admin-

isters the contract. Remaining within the bank are certain corporate services we could think of outsourcing in due course; perhaps to EpicI, perhaps to others; and the three business units which are retail, business and corporate. These are the units where the “real” bankers live - the people who understand their custom-ers, who think about interest rates, who manage client relationships, who have a nose for good credit and so on. Now the real bankers are released to do the busi-ness. They don’t have to bother so much about processing and other mechanical administrative tasks.

Within the bank, now that the bread and butter stuff is dealt with, or is being dealt with, a transition is occurring. It should be more or less complete later this year. Now we are free to think of other important projects: such as better risk management systems, customer relationship systems and client manage-ment systems.

PERSONAL ACCOUNT

The Asian Banker Journal 17

The Defi nitive Annual Ranking and Survey of Asia’s Top Banks

Look us up on www.theasianbanker.com

Special Edition

Special EditionDisplay until 31 December, 2002

THE ASIAN BANKER 300

2 The Asian Banker Journal Special Edition

THE ASIAN BANKER 300

The Asian Banker Journal Special Edition 3

This Special Report was researched and written by CHEW LIMAY, CFA, manager, Asian Banker Research and published by The Asian Banker, incorporated as T.A.B. International Pte Ltd. Worldwide Copyright Protected. All rights reserved. ISSN 02189615 Singapore permit: MITA (P) 029/10/2001 Malaysia KDN PPS 1301/9/2001. Reproduction in any form prohibited except with permission. For reprints, please call Singapore 65-62957300. While every precaution is taken to ensure accuracy of the information in this report, The Asian Banker does not provide warranty of any kind for suitability of use of this report.

An intensifi ed will to tackle the problemsAsian Banker Research is proud to present its inaugural ranking of the region’s Top 300 commercial banks by asset size. In researching on our story, two pertinent issues confronting the region’s fi nancial institutions became apparent: the continuing high levels of non performing loans (NPLs), and the ongoing consolidation taking place within the industry.

An intensifi ed will to tackle the problems

Asian Banker Research is proud to present its inaugural ranking of the region’s Top 300 commercial banks. In researching on our story, two pertinent issues confronting the region’s fi nancial institutions became apparent: the continuing high levels of non performing loans (NPLs), and the ongoing consolidation taking place within the industry.

From the Editors

The editors of The Asian Banker Journal are pleased to present what is likely the fi rst extensive study of the balance sheet pro-fi les of the Asian banking industry since the economic crisis of the past few years.

One of the most important discoveries that we made in develop-ing these rankings is that a ranking of 500 banks for Asia is no longer relevant. A ranking of 300 banks is the most credible and usable list. Many smaller banks have either been consolidated or do not have reporting structures that are transparent enough to validate for this study.

This year’s ranking was developed entirely by a team led by Chew Limay, the lead data center and benchmark researcher at The Asian Banker Research. She was of the view that the progress being made by different banks across the region in resolving NPL problems has received less attention than the problem itself.

Limay and her team of course expect to interact extensively with subscribers of this report in order to further develop what has become the most authoritative ranking of fi nancial institutions for Asia.

Table of Contents• Intensifi ed will to tackle the problems w3• Index to The Asian Banker 300 12• The region’s largest banks by Assets 16• The largest banks in Greater China 28• The largest banks in ASEAN 29• Performance Rankings 30• Country Capsules 32

The full edition of this ranking in Excel sheet format, plus updates and analyst support are available by a subscription of only $620 per annum. Details are

available in the related advertisement in this Journal. Alternatively, please contact us at subs@asianbanker.

com.sg or call 65-62957300 or visit www.theasianbanker.com

THE ASIAN BANKER 300

4 The Asian Banker Journal Special Edition

577,939

4,014

1,828,192

503,111

259,725

66,499

6,904,320

148,536

65,982

16,881

33,724

189,009

491,109

2,500

586,982

124,064

11,275

11,813,860

18.5%

0.0%

16.2%

23.9%

7.2%

1.7%

na

3.6%

3.0%

na

0.2%

5.6%

13.6%

0.0%

3.1%

3.1%

0.1%

100.0%

4,833

2

4,226

6,234

1,884

454

-38,785

945

787

-81

50

1,464

3,553

8

810

817

29

-12,770

5.3%

0.0%

15.3%

3.3%

1.6%

0.2%

59.5%

1.4%

0.8%

0.1%

0.2%

1.5%

4.3%

0.0%

5.1%

1.2%

0.1%

100.0%

351,908

1,706

1,017,522

219,990

106,043

14,762

3,966,317

94,277

53,476

8,004

16,082

101,415

289,001

1,204

338,381

79,150

3,767

6,663,004

3.7%

0.0%

17.7%

4.2%

2.6%

0.6%

56.5%

1.3%

0.5%

0.2%

0.3%

1.5%

4.1%

0.0%

5.6%

1.2%

na

100.0%

300,487

3,364

1,448,789

339,538

212,414

50,801

4,619,305

102,487

41,585

14,074

20,533

124,956

335,897

786

458,070

96,032

na

8,169,117

4.9%

0.0%

15.5%

4.3%

2.2%

0.6%

58.4%

1.3%

0.6%

0.1%

0.3%

1.6%

4.2%

0.0%

5.0%

1.1%

0.1%

100.0%

Australia Bangladesh China Hong Kong India Indonesia Japan Malaysia New Zealand Pakistan Philippines Singapore South Korea Sri Lanka Taiwan Thailand Vietnam Total

11

1

16

18

30

8

109

17

5

4

7

3

13

1

43

11

3

300

How did the nations fare in TAB 300?

* excluding losses from Japan and Pakistan

Source: Asian Banker Research

In 2001's Asian Banker 300, the region suffered a total net loss of $12.8 billion. This is at the other end of the spectrum from net earnings of $23.8 billion in 2000. Of this, Japan's red ink stained the darkest, with losses of $38.8 billion as against a turnround of $3 billion the year prior. There is however hope that the losses, largely due to NPLs written off, could herald a new era with stronger recapitalisation and better lending.

CountryBanksin 300

Assets($mn)

Shareof total

Deposits($mn)

Shareof total

Shareof total

Net Profit($mn)

Shareof total *

Loans($mn)

Progress being made by banks in differ-ent parts of Asia to resolve their NPL problems has received less attention than the problem itself. The Asian Banker 300 identifi es the potential winners and losers. The former includes South Korea and India which have made the most decisive moves to root out the NPL problem. Progress however, remains slow in tackling NPLs in Japan, Taiwan, Thailand and Indonesia despite the crea-tion of asset management companies to help banks get NPLs off their books. In Hong Kong the level of NPLs varies from bank to bank dependent on the extent of lending to the mainland, whilst the weakness of the economy in Singapore has seen NPLs continue to rise, albeit from a low level.

This research also shows how the frenetic pace of Asia’s consolidation has taken its toll. A survey originally intended to cover the top 500 regional banks had to be whittled down to 300 as a tsunami of consolidations and occasional exits

wrought radical change on the banking landscape. We expect continuing consoli-dation activity as management strives to tackle the ongoing asset quality problems and address the relatively low profi tability provided by current banking structures.

The aggregated results of the sur-vey make disturbing reading. Whilst the number of banks in the region has shrunk, the benefi ts of this consolidation have yet to be realised and profi tability for most players remains marginal. The combined net profi ts of banks covered by the survey slid from a profi t of $23.8 billion into negative territory with a $12.8 billion loss, despite an anaemic rise in aggregated assets of 1.9% to $11.8 tril-lion. Japanese banks, which accounted for 36% of our coverage (109 banks) in TAB 300, continue to show the folly of earlier lending policies. In 2001, these banks haemorrhaged a staggering $39 billion, erasing a $3 billion bounce bank into the black in 2000. Asia ex-Japan numbers were more encouraging - total

net profi ts improved 25% to $26 billion - with especially inspiring numbers from India and South Korea.

Trying to tackle problem loansNPLs remain a serious problem for Asian Banks, and are likely to impair the speed of economic recovery in the region. Since the fi nancial crisis, local and international regulatory and supervisory bodies have been forced to adopt a pro-active stance to sort out the mess. Financially unsound institutions were subjected to take-overs and mergers, the lucky ones re-capitalised and some less fortunate banks liquidated. Few would disagree that these actions were essential to provide for the survival of the banking industry in Asia.

There is a growing will to tackle the problem. We see evidence of this in retrograde action to deal with existing problem loans. Some loans have simply been written off, but banks have been able to sell portfolios of dubious loans to government sponsored asset management

THE ASIAN BANKER 300

The Asian Banker Journal Special Edition 5

companies (AMCs). International invest-ment banks have acted as intermediaries using sophisticated fi nancial engineering to repackage distressed assets, extracting residual value by using credit derivative structures. Specialised vulture funds have also begun to circle, picking off individual and groups of bad loans, bringing a more pragmatic and short-term perspective to the workout process.

Predicament of major proportions Typically, about 2-3% of loans in a healthy bank will be non-performing - defi ned as those that are not serviced for at least three months - with a percentage of up to 5% considered acceptable. The hangover from the Asian fi nancial crisis means that it is unrealistic to expect a return to below these thresholds for Asian banks any time soon. Regional asset quality has deterio-rated to an extraordinary extent. Apart from Australia, South Korea and Hong Kong, the remaining countries have soured loans above the 5% threshold. In the worst instance, unoffi cial estimates claim that perhaps half of the loan port-folio in China is irretrievable. As such, the offi cial NPL numbers shown in the graph below need to be treated with some caution. Banks in some countries such as Malaysia (gross NPL: 18%), have tackled their non-performing loan problems with greater candour than, for example, Japan (NPL: 7%) although this may not be ap-parent from these numbers.

Whilst the recent history of NPLs in Asia starts in Japan, the Japanese banks can in no way be seen as a role model

in attempting to resolve the NPL issue. Over the last decade, policy-makers have largely ignored the problem, hoping that it would go away. NPLs in Japan are a legacy of asset infl ation in the late 1980s which lured banks into lending trillions of yen to finance asset purchases of property and shares at infl ated prices. When the fi nancial bubble burst, prices collapsed and loans went bad. Japan resolved about $400 billion worth of bad loans between 1998-2001, yet offi cials acknowledge that banking sector NPLs still hover around 40 trillion yen ($305 billion) or 6-7% of the total loan assets of its banking system. Many private sec-tor analysts believe the real level to be 60 trillion yen in EXCESS of this fi gure, depending on how problem loans are classifi ed. This would push the NPL ratio up nearer to 15-18% of total loan book, a surreal fi gure almost similar to Japan’s annual GDP.

China is another country where the level of NPLs has placed the local banks

in a precarious state. There, the problem is largely due to state banks being used as conduits for state spending on projects that yielded insuffi cient returns. NPLs prob-ably amount to as much as $3.2 trillion yuan ($378 billion) or 28% of the total loans outstanding by Chinese banks, with the four ma-jor state-owned banks responsible for 2/3rds of the total value. China’s biggest player, In-

dustrial and Commercial Bank of China (ICBC, No.5 in TAB300) acknowledged an NPL ratio of just under 30%, while Bank of China (BOC, No. 7) admitted recently to the group’s NPLs being 24%. More alarmingly, many foreign observ-ers believe the actual size of NPLs is understated because the way the Chinese categorize bad loans is relatively lenient compared to international accounting standards. Unoffi cial estimates put the banking system’s NPLs closer to 50%, making the banks technically insolvent! With Chinese banks yet to be granted authority to resolve their own NPLs, the growing NPL problem remains a colos-sal drag.

AMCs to the rescue...Elsewhere in the region, the problem ap-pears to pale alongside Japan and China. Nonetheless, NPLs are still an issue and in some cases, the situation is a great deal worse than it appears on the surface. Amongst the nations battered by the Asian crisis, the Philippines still has the worst acknowledged level of banking-system bad debt at 18.4% of total loans in the fi nancial sector. Malaysia comes a close second at 18%, followed by Indone-sia (12%) and Thailand (10.5%). All except the Philippines have been able to make the problem look better‚ via the creation of state-owned or state-supported Asset Management Companies (AMCs) to purchase bad assets from fi nancial insti-tutions at discounted prices, repackage and sell them.

One virtue of shifting NPLs from banks to AMCs is that it creates a transparent sale and disclosure process to make investors more comfortable. This unfortunately does not rectify the problem - in some cases, the sheer size of the residual legacy of bad debts in the aftermath of a fi nancial bubble is so great that even the govern-

Estimates place Japan’s banking sector NPLs at 100 trillion yen ($763 billion) ...almost similar to her annual GDP. Meanwhile, many foreign ob-servers believe the actual size of China’s NPL is understated...unoffi cial extimates put the fi gure closer to 50%.

THE ASIAN BANKER 300

6 The Asian Banker Journal Special Edition

ments are unable to deal with it. The Asian Development Bank (ADB) echoed the limitation of the AMC solution, saying ‘The overhang of NPLs held by AMCs is one factor retarding economic recovery by delaying corporate restructuring.’

...but progess still lackingDigging beneath the surface, we indeed found evidence that some AMCs have not made distinctive inroads into NPL disposal. The Resolution and Collection Corporation in Japan for instance, has so far bought up only a tiny fraction of NPLs in the system. A report released by Ernst & Young (EY) Asia Pacifi c Finan-cial Solutions last No-vember was similarly critical of the govern-ments for their lack of development in tacking NPLs. EY es-timated NPLs to have leaped-frog 33% in the last two years and amounted to some $2 trillion in November. This translates to lev-els of NPLs in Asia at roughly 29% of the re-gion’s combined GDP rather than official estimates of 17.3%.

Thailand and In-donesia have been amongst the slow-est in tackling the NPL problem. Even allowing for AMC purchases of NPLs from banks, progress in restoring finan-cial health has been disappointing. Despite the Financial Restructuring Agency in Thailand enlist-ing the help of foreign NPL advisors like GE Capital and Lend Lease to liquidate failed assets, subsequent disposal of the bad loans by the AMCs themselves have been slow.

In Indonesia, the Indonesian Bank Re-structuring Agency (IBRA) has hitherto merged four ailing state banks to form the biggest Indonesian bank - Bank Mandiri (No.80); sold 51% of Bank Central Asia (BCA, No.163) to hedge fund Farallon Capital of the United States for $540 million; and cleaned up and recapital-ize Bank International Indonesia (BII, No.282), a bank crippled by huge loans

Taiwanese banks into the red this year but prepare the stage for recovery in the coming years.

The key exception to weak reforms in tackling NPLs has been South Korea. Nowhere has the clean up been swifter or more successful. Although the govern-ment still has further to go with privati-sation and consolidation in the sector, reforms are moving along following the creation of the Korea Asset Manage-ment Co. (KAMCO) to tackle roughly 66 trillion won ($50 billion) of troubled debt transferred from Korean fi nancial institutions. With NPLs plummeting 980 basis points from 12.9% in 1999 to

3.1% by 1Q2002, clean up here is definitely seeing meaningful progress. However, giving banks a fresh start comes at a price - the Korean govern-ment has exhausted $117 billion or 25% of its GDP for this purpose, in contrast to Japan’s 14% and Taiwan’s less than 3% and Malaysia’s less than 5%.

Though commend-able efforts have been made via government-led programmes to address financial re-structuring and follow through with NPL disposition strategies, bar exceptions like Korea, the regional economies are gen-erally struggling to

keep on top of the NPL problem. Ernst & Young reckons that the cost of failing to move aggressively to resolve the is-sue will snowball into the “NPL Effect” - reduced economic expansion resulting in slower growth in standards of living, business investment, and tax revenue. There is a need for the different countries in Asia to grasp the bull by the horns and make a concerted and sometimes painful effort to clean up the NPL problem once and for all.

Hopefully, forward looking initia-tives such as the adoption of more so-phisticated lending criteria and better risk management tools that banks have begun implementing will limit the risks

made to a related party. The fi nancial mess is however far from over - next on IBRA’s list of disposal is that of Bank Niaga by October following twice-delayed attempts from unsatisfactory bids earlier. Other banks it is expected to move towards offl oading include Bank Mandiri, Bank Negara Indonesia (BNI) and Bank Rakyat Indonesia (BRI) fol-lowed by BII, Bank Bali, Bank Lippo and Bank Danamon. Although Indonesia has an urgent need to plug its budget defi cit, given the number of banks on offer and the limited investors‚ appetite for Indo-nesia, the completion of these sales will take some time yet.

Despite write-offs amounting to NT$530 billion ($15.1 billion) over the past three years, Taiwan’s has similarly witnessed an acceleration of NPL levels to circa 7.5% (with unoffi cial estimates at twice that), drifting further and further away from the Ministry of Finance’s goal to cut NPL ratios below 2.5% by June 2003. However, signs are surfacing that banks are facing up to the problem - the big 3 commercial banks (First Com-mercial (No.52), Hua Nan (No.56) and Chang Hwa (No.60)) have already begun liquidating billions in NT$ of NPLs, with each intending to dispose off between NT$42-60 billion ($1.2-1.7 billion) this year. Massive write-offs would put most

THE ASIAN BANKER 300

The Asian Banker Journal Special Edition 7

ORACLE ADS (FILM) ...COMPLETE...

THE ASIAN BANKER 300

8 The Asian Banker Journal Special Edition

Holdings (No.4). This follows the mar-riage between Fuji, Dai-ichi Kangyo and Industrial Bank of Japan earlier in 2000 to create the behemoth Mizuho Financial Group, possibly the world’s largest bank with assets exceeding $1.15 trillion.

For many nations, the primary impetus for merger activity is deeply entwined with the NPL problem. Regulators are trying to repair their fi nancial systems and lay the foundation for a strong eco-nomic recovery. The hoped-for results are greater effi ciencies, higher profi ts, streamlined management, better gov-ernance and better risk-management procedures. There is also the possibil-ity that we will see more cross border M&A activity. Although local relevance

remains important, especially in regions with vast rural clientele like China and India, the fact remains that local play-ers are disadvantaged in several arenas. Globalisation brings with it considerable advantages - economies of scale, cheaper cost of funds, resources to embrace technological advancements and inter-national branding expertise.

With government-led integration, the push for internationalisation, and several countries still over-banked, there remains plenty of scope for more consolidation. On that front, Singapore banks are emerging at the top of the consolidation pile in South East Asia. With the island-nation opening the banking market to international players,

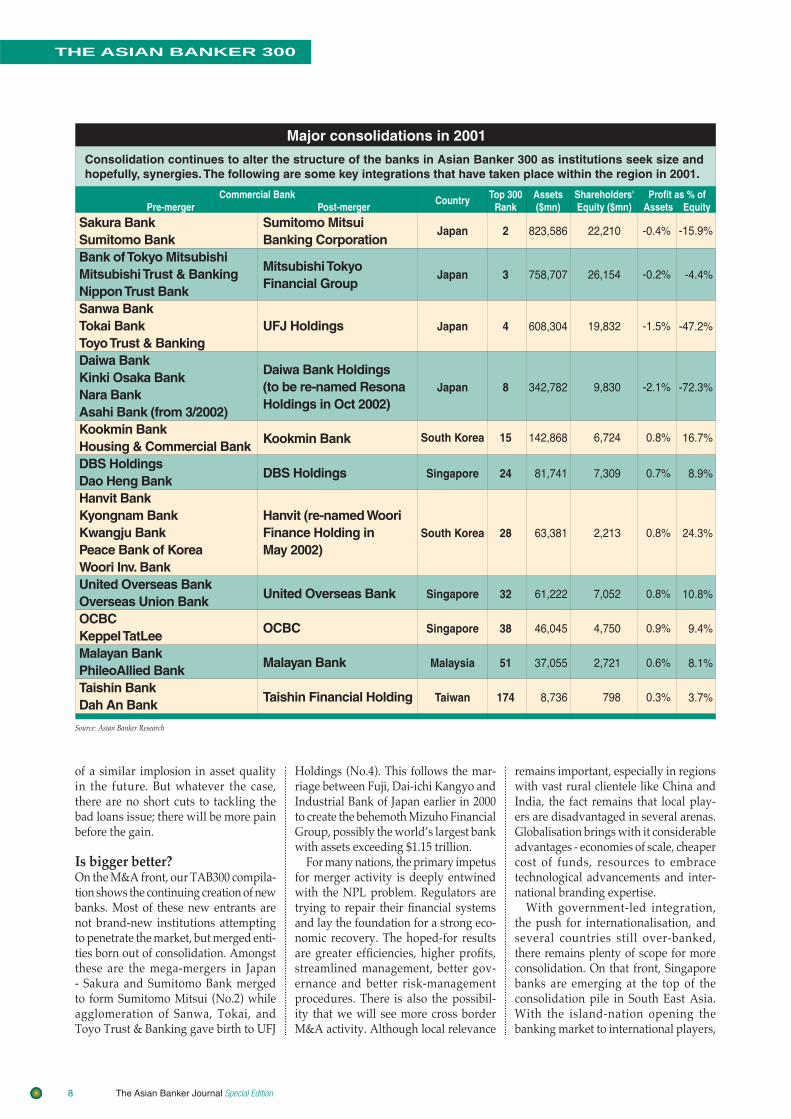

Major consolidations in 2001

Consolidation continues to alter the structure of the banks in Asian Banker 300 as institutions seek size and hopefully, synergies. The following are some key integrations that have taken place within the region in 2001.

Commercial Bank Pre-merger Post-merger

Country Top 300Rank

Assets($mn)

Shareholders'Equity ($mn)

Profit as % ofAssets Equity

Sakura BankSumitomo BankBank of Tokyo MitsubishiMitsubishi Trust & BankingNippon Trust BankSanwa BankTokai BankToyo Trust & BankingDaiwa BankKinki Osaka BankNara BankAsahi Bank (from 3/2002)Kookmin BankHousing & Commercial BankDBS HoldingsDao Heng BankHanvit BankKyongnam BankKwangju BankPeace Bank of KoreaWoori Inv. BankUnited Overseas BankOverseas Union BankOCBC Keppel TatLeeMalayan BankPhileoAllied BankTaishin BankDah An Bank

Sumitomo MitsuiBanking Corporation

Mitsubishi TokyoFinancial Group

UFJ Holdings

Daiwa Bank Holdings(to be re-named ResonaHoldings in Oct 2002)

Kookmin Bank

DBS Holdings

Hanvit (re-named WooriFinance Holding inMay 2002)

United Overseas Bank

OCBC

Malayan Bank

Taishin Financial Holding

Japan

Japan

Japan

Japan

South Korea

Singapore

South Korea

Singapore

Singapore

Malaysia

Taiwan

2

3

4

8

15

24

28

32

38

51

174

823,586��

758,707���

608,304���

342,782���

142,868��

81,741����

63,381���

61,222��

46,045��

37,055��

8,736

22,210���

26,154���

19,832���

9,830���

6,724��

7,309����

2,213���

7,052��

4,750��

2,721��

798

-0.4%���

-0.2%���

-1.5%���

-2.1%���

0.8%��

0.7%����

0.8%���

0.8%��

0.9%��

0.6%��

0.3%

-15.9%���

-4.4%���

-47.2%���

-72.3%���

16.7%��

8.9%����

24.3%���

10.8%��

9.4%��

8.1%��

3.7%

Source: Asian Banker Research

of a similar implosion in asset quality in the future. But whatever the case, there are no short cuts to tackling the bad loans issue; there will be more pain before the gain.

Is bigger better? On the M&A front, our TAB300 compila-tion shows the continuing creation of new banks. Most of these new entrants are not brand-new institutions attempting to penetrate the market, but merged enti-ties born out of consolidation. Amongst these are the mega-mergers in Japan - Sakura and Sumitomo Bank merged to form Sumitomo Mitsui (No.2) while agglomeration of Sanwa, Tokai, and Toyo Trust & Banking gave birth to UFJ

THE ASIAN BANKER 300

The Asian Banker Journal Special Edition 9

THE ASIAN BANKER 300

10 The Asian Banker Journal Special Edition

Average (ex-Japan & Pakistan)Japan

Taiwan�Bangladesh�

China�Philippines�

Sri Lanka�Malaysia�

Singapore�Indonesia�Australia�

India�Thailand�Vietnam�

South Korea�Hong Kong�

New Zealand

-20% -15% -10% -5% 0% 5% 10% 15% 20% 25%

Pakistan

Return on EquityReturn on Assets

Returns of regional banks still relatively unattractive

Source: Asian Banker Research

domestic banks are embracing the ad-age that size matters. What started off as seven banks during the crisis has been whittled down to three - DBS, UOB and OCBC - with the end product possibly being a mere duopoly. In Malaysia, gov-ernment initiatives forced 54 banks and fi nance companies to consolidate into 10 “superbanks”, each anchored by a major player. Bank Negara governor Tan Sri Dr Zeti further reiterated that the ideal long-term scenario could well be 3-4 key players with others providing ancillary niche banking services.

Merger mania has left banks in Singa-pore and its neighbour with an average customer base of 1.3 million/bank and 1.8 million/bank respectively. In contrast, Taiwan has 52 banks competing for 23 million customers (0.44 million/bank), some with market shares of just 1-2%.

To alleviate this problem of over-bank-ing which has led to excessive competi-tion in a market place where demand has been shrinking, Taiwan has introduced several measures aimed at encouraging consolidation of its banking sector. These include tax and accounting incentives and passing the Financial Holding Com-panies (FHCs) Act, which forces groups of related fi nancial-services companies to form single, bigger entities. These has resulted in at least a dozen banks and insurance companies converting to FHCs over the course of the last 12 months. Recent announcements of two large-scale merger plans - that between Fubon Financial and Taipeibank (No.116), and between Cathay Financial and United World Chinese Commercial Bank (No. 96) will hopefully set the stage for con-solidation in Taiwan’s banking scene following several other false starts.

In Hong Kong, three players - the glo-bal HSBC Group (No.11), Bank of China (HK) (No.20) and Standard Chartered Bank, dominate the banking scene. How-ever, there are also other 100-odd licensed banks and several tiny family-controlled banks with market shares of just 1% each competing for the remains of the pie. It will not be long before the consolidation tide sweeps up such tiny players.

Again, the concept that “bigger is better” was the main justifi cation used by Thai authorities to merge two state-owned banks - Siam City Bank (No.197) and Bangkok Metropolitan Bank (No.264) in 2Q2002, creating the country’s fi fth largest institution in a bid to boost their

profi tability and competitiveness. Follow-ing this, proposal for a potential merger between Krung Thai Bank (No.85) and Bankthai (No.206) to strengthen the larg-er Krung Thai Bank and meet regulatory goals of reducing the number of fi nancial institutions is being studied.

In South Korea, reform efforts after the Asian financial crisis saw Korean banks undergoing wrenching, state-led mergers to off-load weighty NPLs. Kookmin’s alliance last November with H&CB, Korea’s top mortgage bank, cre-ated a fi nancial giant with $143 billion in assets and dwarfed state-run No.2 Woori Finance Holding Co (asset base: $63 billion), a cluster of fi ve cash-strapped lenders grouped together in April 2001. Creation of the colossal bank, ranked No.15 in TAB300, added urgency to other lenders’ plans of possible alliances. Next in queue was the union of Hana (No.55) & Seoulbank (No.112), a marriage that would create a powerhouse with 84 tril-lion won in combined assets.

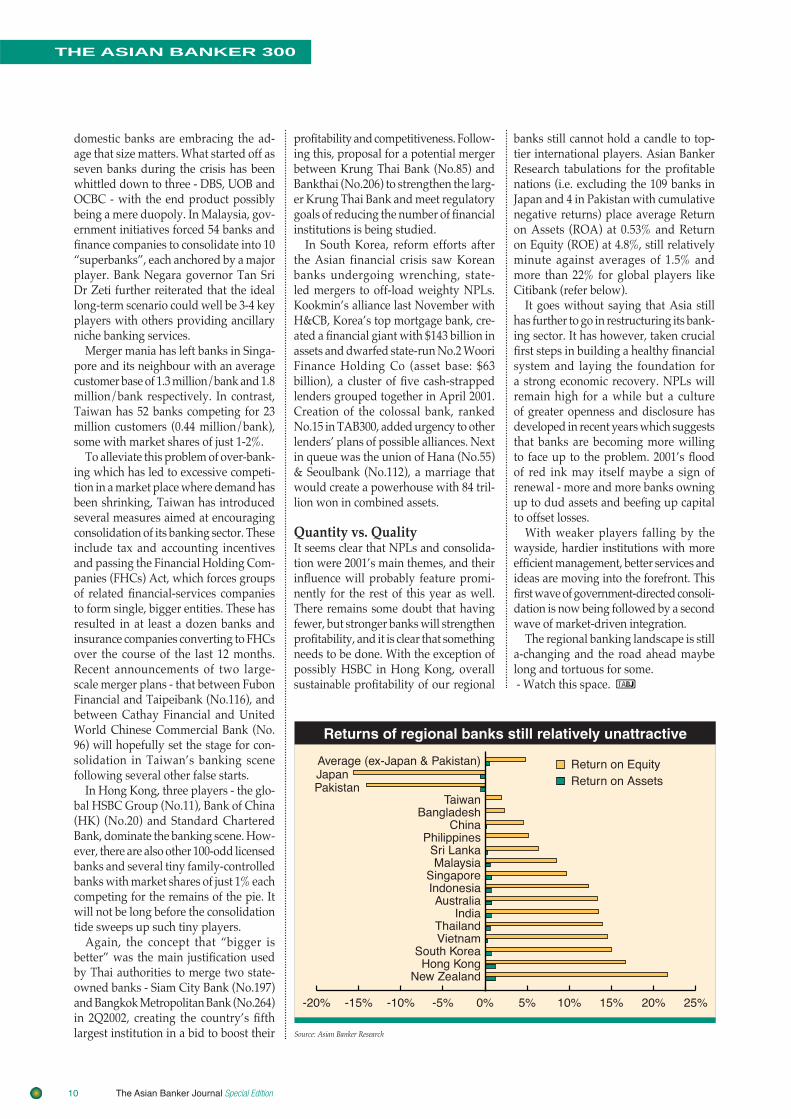

Quantity vs. Quality It seems clear that NPLs and consolida-tion were 2001’s main themes, and their infl uence will probably feature promi-nently for the rest of this year as well. There remains some doubt that having fewer, but stronger banks will strengthen profi tability, and it is clear that something needs to be done. With the exception of possibly HSBC in Hong Kong, overall sustainable profi tability of our regional

banks still cannot hold a candle to top-tier international players. Asian Banker Research tabulations for the profi table nations (i.e. excluding the 109 banks in Japan and 4 in Pakistan with cumulative negative returns) place average Return on Assets (ROA) at 0.53% and Return on Equity (ROE) at 4.8%, still relatively minute against averages of 1.5% and more than 22% for global players like Citibank (refer below).

It goes without saying that Asia still has further to go in restructuring its bank-ing sector. It has however, taken crucial fi rst steps in building a healthy fi nancial system and laying the foundation for a strong economic recovery. NPLs will remain high for a while but a culture of greater openness and disclosure has developed in recent years which suggests that banks are becoming more willing to face up to the problem. 2001’s fl ood of red ink may itself maybe a sign of renewal - more and more banks owning up to dud assets and beefi ng up capital to offset losses.

With weaker players falling by the wayside, hardier institutions with more effi cient management, better services and ideas are moving into the forefront. This fi rst wave of government-directed consoli-dation is now being followed by a second wave of market-driven integration.

The regional banking landscape is still a-changing and the road ahead maybe long and tortuous for some. - Watch this space.

THE ASIAN BANKER 300

The Asian Banker Journal Special Edition 11

THE ASIAN BANKER 300

12 The Asian Banker Journal Special Edition

Index To The Asian Banker 300

Name, Country and Rank

AAdelaide BankAgricultural Bank of ChinaAichi BankAkita BankAllahabad BankAlliance BankAMP BankAndhra BankANZ Banking Group (NZ)Aomori BankAozora BankArab-Malaysian BankAsahi BankASB Bank – NZAshikaga BankAsia Pacifi c BankAustralia & New Zealand Banking GroupAwa Bank

BBangkok BankBangkok Metropolitan BankBank Central AsiaBank DanamonBank for Foreign Trade of Vietnam (Vietcombank)Bank for Investment and Development (BIDV)Bank Internasional IndonesiaBank Islam MalaysiaBank LippoBank MandiriBank Negara IndonesiaBank of America (Asia)Bank of AsiaBank of AyudhyaBank of BarodaBank of CeylonBank of China (HK)Bank of China GroupBank of CommunicationsBank of East AsiaBank of FukuokaBank of IkedaBank of IndiaBank of IwateBank of KansaiBank of KaohsiungBank of KochiBank of KyotoBank of MaharashtraBank of NagoyaBank of New ZealandBank of OkinawaBank of Overseas ChineseBank of PanhsinBank of SagaBank of ShanghaiBank of TaiwanBank of the Philippine IslandsBank of The RyukyusBank of Western Australia (BankWest)Bank of YokohamaBank RakyatBank Rakyat IndonesiaBank SinopacBank Tabungan NegaraBankthaiBaodao Commercial BankBeijing City Commercial Bank

AustraliaChinaJapanJapanIndiaMalaysiaAustraliaIndiaNew ZealandJapanJapanMalaysiaJapanNew ZealandJapanTaiwanAustraliaJapan

ThailandThailandIndonesiaIndonesiaVietnamVietnamIndonesiaMalaysiaIndonesiaIndonesiaIndonesiaHong KongThailandThailandIndiaSri LankaHong KongChinaChinaHong KongJapanJapanIndiaJapanJapanTaiwanJapanJapanIndiaJapanNew ZealandJapanTaiwanTaiwanJapanChinaTaiwanPhilippinesJapanAustraliaJapanMalaysiaIndonesiaTaiwanIndonesiaThailandTaiwanChina

27110

10810723024727620515211437

28812

17949

24622

104

6926416323423928728227529880

144242266171138293207

238135

13315710617621319057

24995

11916718928312714627

18615415025

297191184292206229151

Bendigo BankBiwako BankBumiputra-Commerce Bank

CCanara Bank Cathay United BankCentral Bank of IndiaCentral Trust of ChinaChang Hwa Commercial BankChekiang First BankChiao Tung BankChiba Bank Chiba Kogyo BankChikuho BankChina Construction BankChina Development Industrial BankChina Everbright BankChina Merchants BankChina Minsheng Banking CorpChinatrust Commercial BankChinese BankChinfon Commercial BankChohung BankChugoku BankChukyo BankChung Shing BankChuo Mitsui Trust & BankingCitibankCitibank IndiaCITIC Industrial BankCITIC Ka Wah BankCommonwealth Bank of AustraliaCorporation BankCosmos Bank

DDaegu BankDah Sing BankDaisan BankDaishi BankDaito BankDaiwa Bank HoldingsDao Heng BankDBS Group HoldingDBS Kwong On BankDena BankDevelopment Bank of the Philippines

EE.Sun Commercial BankEhime BankEighteenth BankEnTie Commercial BankEON BankEquitable PCI Bank

FFar Eastern Intl BankFarmers Bank of ChinaFirst Commercial BankFubon Commercial BankFujian Industrial Bank

AustraliaJapanMalaysia

IndiaTaiwanIndiaTaiwanTaiwanHong KongTaiwanJapanJapanJapanChinaTaiwanChinaChinaChinaTaiwanTaiwanTaiwanSouth KoreaJapanJapanTaiwanJapanMalaysiaIndiaChinaHong KongAustraliaIndiaTaiwan

South KoreaHong KongJapanJapanJapanJapanHong KongSingaporeHong KongIndiaPhilippines

TaiwanJapanJapanTaiwanMalaysiaPhilippines

TaiwanTaiwanTaiwanTaiwanChina

268181110

125250155156

60260118

29121258

9215

6164

10977

207244

4648

145252

19209255

53187

17254218

149198142

66225

8105

24248257270

188143111224199243

222122

52182123

THE ASIAN BANKER 300

The Asian Banker Journal Special Edition 13

Name, Country and Rank

Fukui BankFukuoka Chuo BankFukuoka City BankFukushima Bank

GGifu BankGrand Commerical BankGuangdong Development BankGunma Bank

HHabib BankHachijuni BankHana BankHang Seng BankHanvit (Woori) BankHDFC BankHigashi-Nippon BankHigo BankHiroshima BankHiroshima-Sogo BankHokkaido BankHokkoku BankHokuetsu BankHokuriku BankHong Leong BankHongkong Chinese BankHowa BankHSBCHSBC Bank MalaysiaHsinchu Intl BankHua Nan Commercial BankHua Xia BankHyakugo BankHyakujushi Bank

IICBC (Asia)ICICI Indian BankIndian Overseas BankIndusind BankIndustrial & Commercial Bank of Vietnam (Vietincombank)Industrial and Commercial Bank of ChinaIndustrial Bank of KoreaInternational Bank of AsiaInternational Bank of Taipei Intl Commercial Bank of ChinaIyo Bank

JJammu & Kashmir BankJeonbuk BankJoyo BankJuroku Bank

KKagawa BankKagoshima BankKanto Bank

JapanJapanJapanJapan

JapanTaiwanChinaJapan

PakistanJapanSouth KoreaHong KongSouth KoreaIndiaJapanJapanJapanJapanJapanJapanJapanJapanMalaysiaHong KongJapanHong KongMalaysiaTaiwanTaiwanChinaJapanJapan

Hong KongIndiaIndiaIndiaIndiaVietnamChinaSouth KoreaHong KongTaiwanTaiwanJapan

IndiaSouth KoreaJapanJapan

JapanJapanJapan

11528992

223

2312208244

22643553328

2361407941

1207284

13039

15829125111

20817756

1477074

22190

202195295261

540

2631737663

2772863467

16583

196

Kaohsiung Business BankKeiyo BankKinki Osaka BankKita-Nippon BankKiyo BankKookmin BankKorAm BankKorea Exchange BankKorea First BankKrung Thai BankKumamoto Family BankKyushu Bank

LLand Bank of TaiwanLiu Chong Hing BankLucky Bank