Page 1

The Business Case for Bancassurance in Africa

11 August 2014

Presented By Charmaine Scott

Head Bancassurance, Rest of Africa, Standard Bank Group

African insurance Distribution & Bancassurance Conference

The Bancassurance Opportunity:

Page 2

1

Bank

Non-interest income via insurance products

Insurer

Leverage Banks

customers base

Customer

Convenience of one-stop shopping

Country

Increased GWP

contributes to GDP growth

Bancassurance benefits are quite well known

Success rests on

trust in the bank

Appropriate agreement between bank and insurance

company is vital

More appropriate

products Enabling regulatory

changes

Page 3

2

Impact of Insurance on the Economic Environment

Promotes economic activity:

Contributes to efficient capital accumulation:

Increases access to credit

Alleviates reliance on government aid

Source :What is the role of insurance in economic development, Lael Brainard, Zurich

Page 5

4

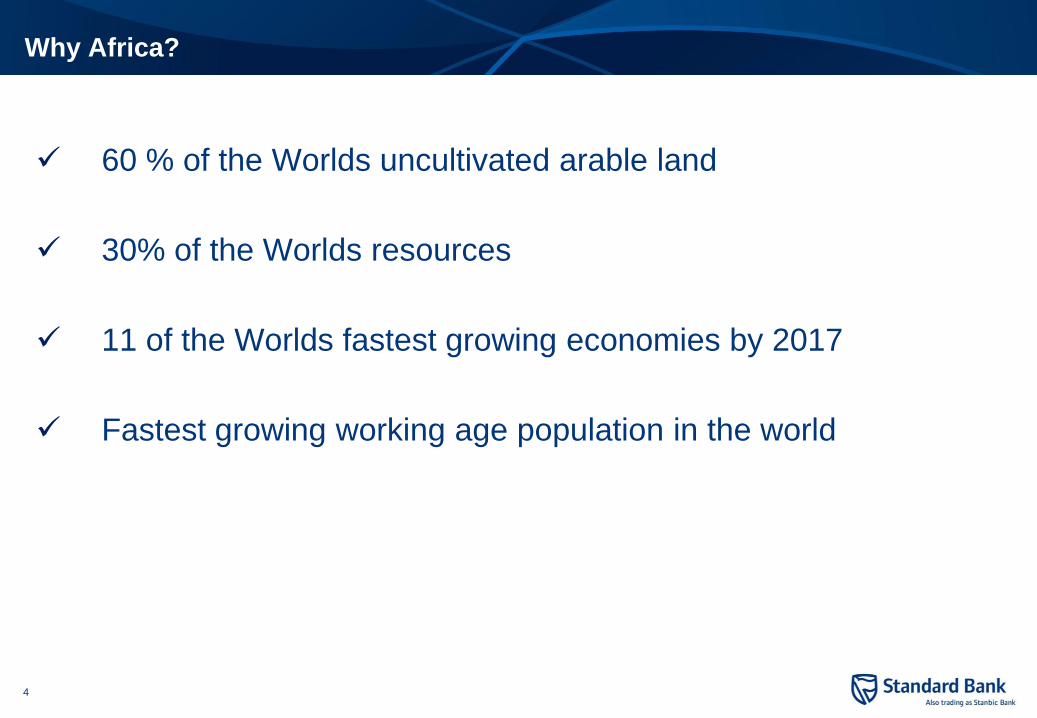

Why Africa?

60 % of the Worlds uncultivated arable land

30% of the Worlds resources

11 of the Worlds fastest growing economies by 2017

Fastest growing working age population in the world

Page 6

5

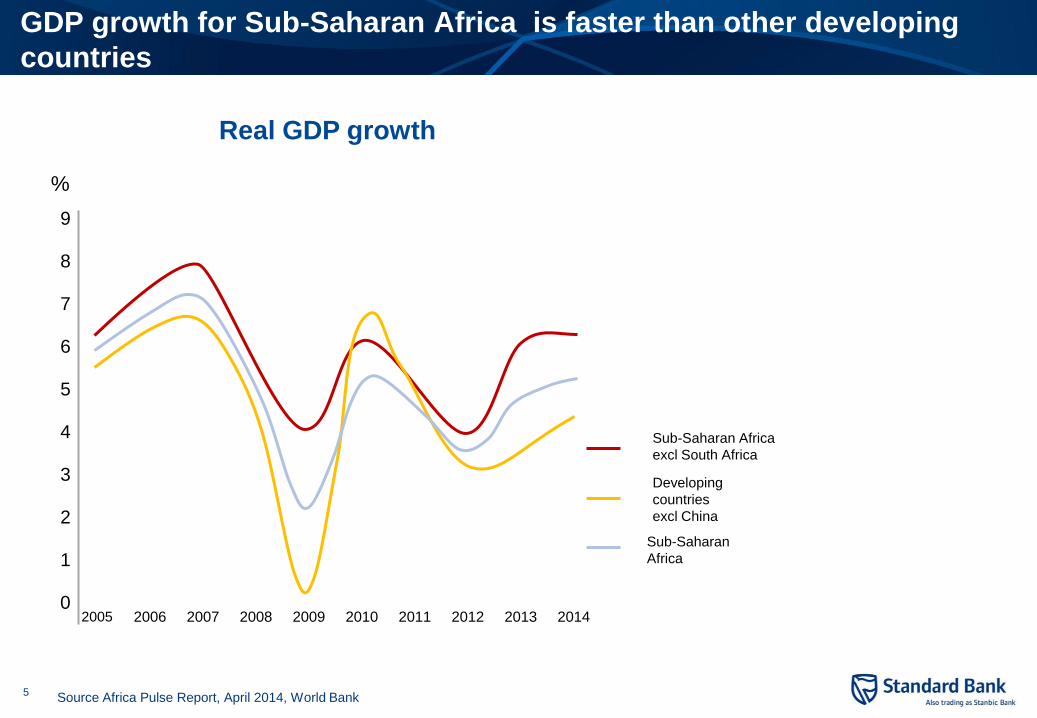

GDP growth for Sub-Saharan Africa is faster than other developing

countries

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 0

9

8

7

6

5

4

3

2

1

%

Real GDP growth

Sub-Saharan Africa

excl South Africa

Developing

countries

excl China

Sub-Saharan

Africa

Source Africa Pulse Report, April 2014, World Bank

Page 7

6

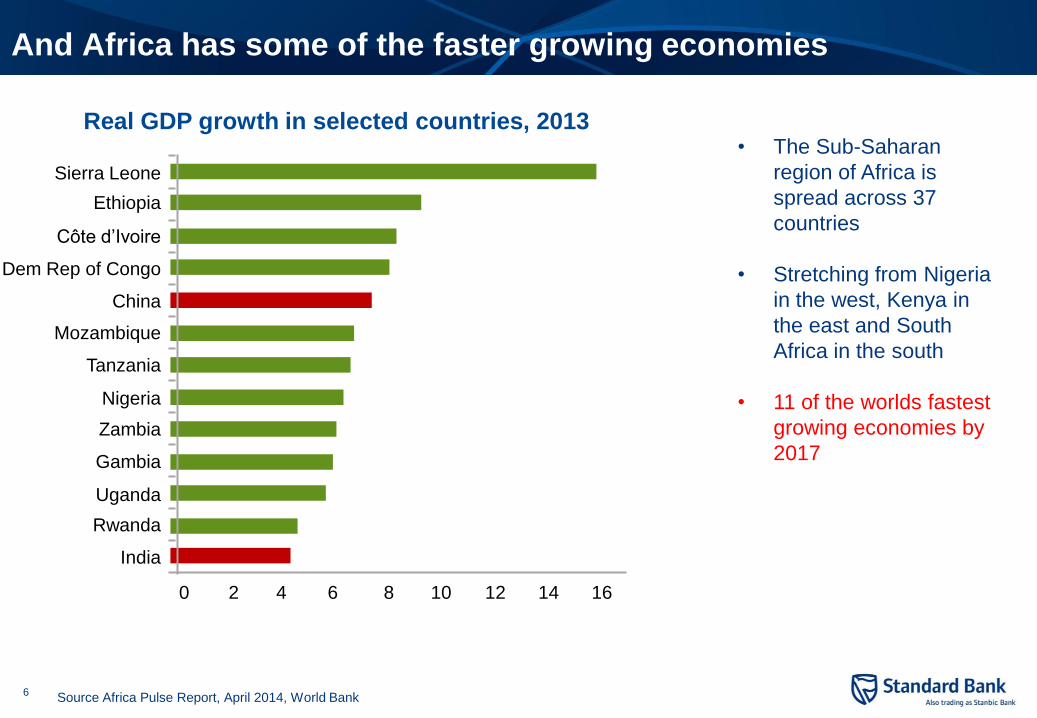

And Africa has some of the faster growing economies

China

Sierra Leone

Ethiopia

Côte d’Ivoire

Dem Rep of Congo

Mozambique

Tanzania

Nigeria

Zambia

Gambia

Uganda

Rwanda

India

0 2 4 6 8 10 12 14 16

Real GDP growth in selected countries, 2013

Source Africa Pulse Report, April 2014, World Bank

• The Sub-Saharan

region of Africa is

spread across 37

countries

• Stretching from Nigeria

in the west, Kenya in

the east and South

Africa in the south

• 11 of the worlds fastest

growing economies by

2017

Page 8

7

There are a number of factors driving this growth

The contribution

from resources has nearly doubled

over the last 10 years

Foreign direct

investment has

increased by 50%

since 2005

Consumer spending close to a

Trillion dollars

Mobile operator revenue

over US$40 million

Source Africa Pulse Report, April 2014, World Bank

Page 9

8

Mobile usage in many countries exceeds the global average

31% 26% 33% 31%

15-20% Shared use of

mobile accesses

Mobile Financial services Electricity Sanitation

Access to basic services in Sub-Saharan Africa

34.5% 49.8% 31.0% 30.0% 29.5%

Angola

Pop 20.8m

Ghana

Pop 26.3m

Kenya

Pop 44.2m

Tanzania

Pop

49.5m

Nigeria

Pop 172m

5148

1570

808 529 1452

GDP per Capita Mobile penetration

Source: GSMA Inteligence, IEA, World Bank, MDI Analysis

Page 10

9

The Question….

Are the insurance markets

in Africa leveraging off this

Economic growth?

Page 11

10

The average insurance penetration globally is around 7%, with

South Africa ranking third highest in the World

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Insurance penetration

Source Sigma World Insurance report 2010

• Penetration is based on

premium as a % of GDP

• South Africa is extremely

impressive at nearly 15%

being the third highest

overall insurance

penetration in the world.

• Why…?

Probably because of lack

of meaningful social

security provision.

Page 12

11

But in most of Sub-saharan Africa insurance penetration is lower than the

average

Ghana 1%

Nigeria 1%

Angola 1%

Namibia 10%

South Africa 15% Lesotho 6%

Botswana 3%

Swaziland 2%

Malawi 2%

Uganda 1%

Tanzania 1%

Zambia 1%

Mozambique 1%

Kenya 3%

Zimbabwe 5%

If we could

increase insurance

penetration to the

global average of

7% it means

premium income

increasing by

700%

Page 13

12

$0

$200

$400

$600

$800

$1 000

$1 200

$1 400

$1 600 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43

Current - Life Current - Short Term Axis

Insurance Market size is relatively low across most sub-

Saharan countries in Africa, especially life insurance

Source: Axco 2013 & Swiss Re – Insurance in sub-Saharan Africa

$7bn $10bn

Page 14

13

Bancassurance penetrations around the World

Japan 9%

Taiwan 63%

South Korea

37 %%

China 56%

Germany 20%

United Kingdom 16%

Italy 74%

USA <5%

Chile >30 %

South Africa >30%

India 25%

Brazil >50%

Mexico 14 %

France > 60 %

Source : Bancassurance around the World - LIMRA

Page 15

14

Penetration levels unpacked

Source Sigma World Insurance report 2010

• Europe is considered the

birthplace of

Bancassurance and

hence penetrations rates

are still very high

• Brazil, China, Korea and

Taiwan have only

aggressively started

targeting bancassurance

in the last 10 years.

• Mature countries like UK

and USA have lower

Bancassurance

penetration rates

75% 74% 65% 63%

56%

37% 30%

25% 20%

10% 9% 4% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Bancassurance contribution

Page 16

15

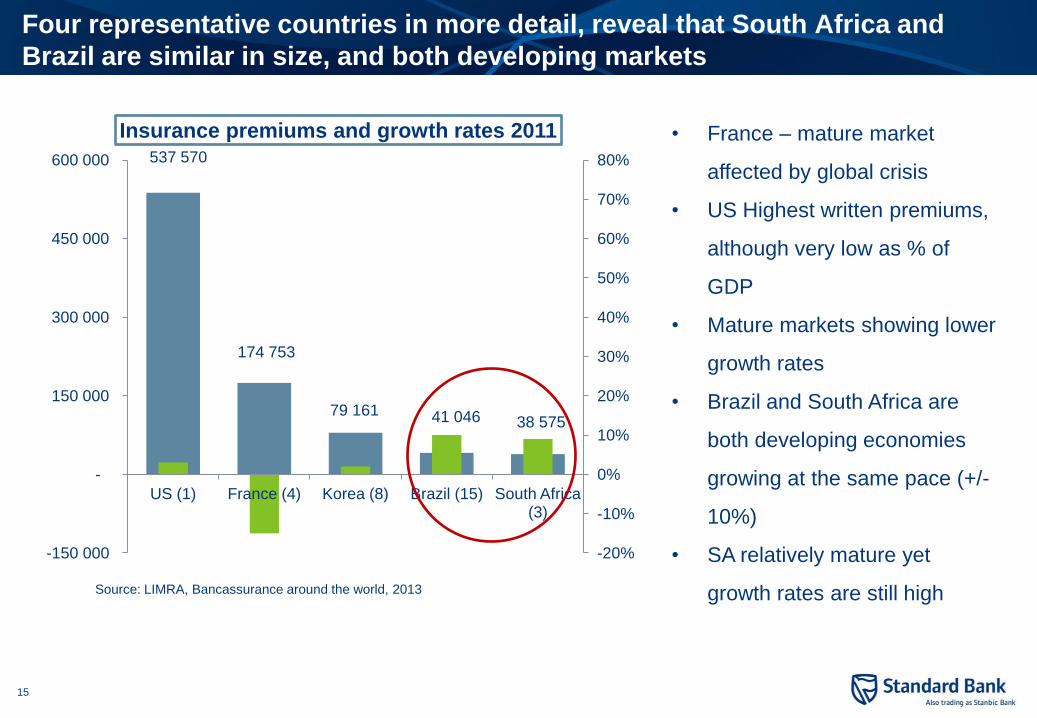

Four representative countries in more detail, reveal that South Africa and

Brazil are similar in size, and both developing markets

Source: LIMRA, Bancassurance around the world, 2013

537 570

174 753

79 161 41 046 38 575

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

-150 000

-

150 000

300 000

450 000

600 000

US (1) France (4) Korea (8) Brazil (15) South Africa (3)

Insurance premiums and growth rates 2011 • France – mature market

affected by global crisis

• US Highest written premiums,

although very low as % of

GDP

• Mature markets showing lower

growth rates

• Brazil and South Africa are

both developing economies

growing at the same pace (+/-

10%)

• SA relatively mature yet

growth rates are still high

Page 17

16

August 2003 – Bancassurance introduced to help distribute insurance at

a lower cost.

– Many banks, limited insurance distribution channels

Phased in over the next 5 years from credit life - then to more

sophisticated products

2003 – 2010 insurance market grew by ave of 9.5% per annum

Previously it was growing at rates of less than 2%.

Bancassurance penetration 0.5% - 37% over 5 Years

The Korea Story

Page 18

17

Korea – growing the insurance pie, everyone gets a bigger slice

Bancassurance, 25 , 1.0%

Employee, 850 , 34.0%

Solicitor, 1 413 , 56.5%

Agency, 213 , 8.5%

GWP $2.5bn US$m - 2003

Bancassurance, 6 171 , 37%

Employee,

1 452 , 9%

Solicitor, 5 940 , 36%

Agency, 2 937 , 18%

GWP$16.5bn US$m - 2008

Even solicitors who lost market

share as a % grew more than 4x

over the period

Bancassurance - Market Maker or Market Taker

Page 19

18

Is Bancassurance a “Fleeting Fad” or a “Solid Concept”?

Bancassurance has not developed equally throughout the world

due to:

–Different models used

–Maturity of the insurance market

–Regulations and tax laws

–Cultural preferences

–Consumer education

But it remains a popular channel of distribution around the world

Could Bancassurance be the key for Africa??

LIMRA: Bancassurance around the world

Page 20

19

19

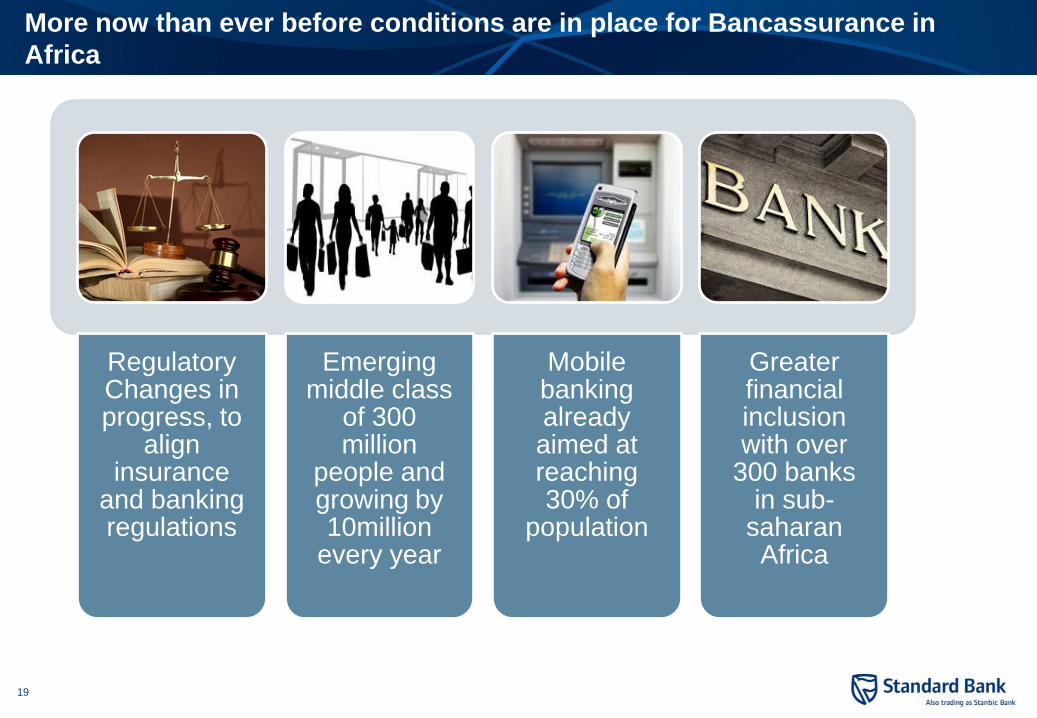

More now than ever before conditions are in place for Bancassurance in

Africa

Regulatory Changes in progress, to

align insurance

and banking regulations

Emerging middle class

of 300 million

people and growing by 10million

every year

Mobile banking already aimed at reaching 30% of

population

Greater financial inclusion with over

300 banks in sub-

saharan Africa

Page 21

20

Who wants the world when Africa is our oyster?

Page 22

21

References

Takeuchi, Y and Schwartz, M; Bancassurance around the World, Limra, 2013

Brainard, L; What is the role of insurance in economic development, Zurich Re,

Ernst &Young; Bancassurance: A Winning Formula; 2010

Gonulal, S; Goulder,N; Lest, R; Bancassurance: A Valuable tool for developing

insurance in emerging markets

Leary, Patrick: Bank Life Insurance Study 2012/2013

Zurich Re; The role of insurance in the Middle East and North Africa

http://tips.thinkrupee.com/articles/bancassurance

http://www.lloyds.com/lloyds/about-us/what-we-do/what-is-insurance

http://www.scor.com/images/stories/pdf/library/focus/Life