Page 1

The Bank of Israel’s New DSGE Model Project

Team: David Elkayam, Eyal Argov, Emanuel Barnea, Alon Binyamini, Eliezer Borenstein, Irit RozenshtromUpdated: 22 October 2009Prepared for presentation at the Central Bank Macroeconomic Modeling Workshop, Jerusalem - 28/10/2009

Page 2

Contents Overview of the project. Short description of the New Area Wide

Model (NAWM). 4 main deviations from NAWM:

Imports in exports. UIP condition. Time varying long-run real interest rate. Rest of the world model.

Page 3

Project Motivation

From 2005 until today, the main monetary model operated at the Bank of Israel to support interest rate decisions is: “Open-economy New-Keynesian small DSGE ‘lite’ model”. Four blocks:

Inflation Output gap Exchange rate Interest-rate

What's missing? The model is too small – real sector not rich enough, does not cover GDP

components, no labor market, no investment-capital dynamics. Limited amounts of questions you can ask. Loose ends on theory – ad hoc imported inflation equation, exogenous

investment, ad hoc “closing open-economy model”. HP filtered gaps – hard to present growth forecasts.

In 2008 the BoI Monetary Models Forum initiated the development of a new DSGE model for use in forecasting and policy analysis.

Page 4

The Project

Starting point – ECB’s “New Area Wide Model” Similar (RAMSES, NEMO, TOTEM)

Stages of the project: Study and replicate the NAWM – done. Derive analytical solution to steady state – done. Calibrate version for Israel – done. Implementing the model for practical use – ongoing Bayesian estimation of the model – ongoing Extensions of the model – future work

Financial frictions Search and matching labor market Distinction of business sector vs. government output.

Page 5

The New Area Wide Model (Christoffel et al. , 2008) – Main Economic Units Households:

Consume. Invest in capital stock. Rent capital services to intermediate goods firms. Save in domestic or foreign bond Monopolistic suppliers of labor – subject to Calvo (1983)

rigidity in wage setting. Domestic producers of intermediate goods:

Produce with labor and capital (and technology). Sell to local final good produces (C, I, G) and foreign

importers (X) In each market: monopolistic competition + Calvo (1983)

rigidity in price setting

Page 6

The New Area Wide Model (Christoffel et al. , 2008) – Main Economic Units Importers of intermediate goods:

Buy foreign output. Monopolistic competition + Calvo (1983) rigidity in price

setting (LCP). Final good producers (type C, type I):

Aggregate domestic and imported intermediate goods. Perfect competition.

Central bank: Sets nominal interest rate according to Taylor-type rule in order to meet IT.

Fiscal authority: exogenously sets government consumption and tax rates.

Foreign economy (y*, r*, π*): determined by VAR.

Page 7

Extension I: Imports in Exports In the NAWM exports are domestically produced (Not like C or I). Israel:

Export weight in GDP – 36%. Estimates of import intensiveness in exports are around 30%.

To model the use of imported intermediate goods in the production of exports: Not enough to model exports like other final goods (C, I) that are

produced with domestic and imported intermediate goods. We also want to maintain assumption of Local Currency Pricing.

Solution: Two stage production of exports: First stage: CES aggregation of domestic and imported intermediate

goods (like C and I). Second stage: Then brand-naming and monopolistic competition with

Calvo (1983) price rigidity.

Page 8

Extension I: Imports in Exports Domestic final goods firms

Final export good (before brand-naming) CES production function:

Final export good’s price aggregator (marginal cost of distributors):

Imported Intermediate goods

Domestic Intermediate goods

Final Export good before brand-naming

Page 9

Extension I: Imports in Exports Exporters

Domestic monopolistic exporting firms buy the homogenous export good ( ) at constant marginal cost –

Differentiate it using a simple production function:

Sell it abroad at a marked-up price, , to foreign retail firms. They set their price in foreign currency (LCP), and face a Calvo (1983) problem.

Page 10

Extension I: Imports in ExportsMarket Clearing Conditions Two equilibrium conditions defining nominal and real

GDP from the supply side: Nominal GDP:

NAWM:

BoI Model:

Real GDP: NAWM:

BoI Model problem – H, X, and QX are not the same good!

Solution:

Page 11

Extension I: Imports in ExportsExport demand shock

-1

0

1

2

3

4

5

0 5 10 15 20 25 30

Exports (x)

Imports (im)

Output (y)

Nominal interest rate (r)

inflation (πc)

Nominal exchange rate (S)

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0 5 10 15 20 25 30

-0.04

-0.03

-0.03

-0.02

-0.02

-0.01

-0.01

0.00

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0 5 10 15 20 25 30-0.06

-0.05

-0.04

-0.03

-0.02

-0.01

0.00

0.01

0.02

0.03

0 5 10 15 20 25 30

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0 5 10 15 20 25 30

Baseline Model Without IM in X

Page 12

Extension I: Imports in ExportsExport demand shock

-1

0

1

2

3

4

5

0 5 10 15 20 25 30

Exports (x)

Imports (im)

Output (y)

Nominal interest rate (r)

inflation (πc)

Nominal exchange rate (S)

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0 5 10 15 20 25 30

-0.04

-0.03

-0.03

-0.02

-0.02

-0.01

-0.01

0.00

0 5 10 15 20 25 30

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0 5 10 15 20 25 30-0.06

-0.05

-0.04

-0.03

-0.02

-0.01

0.00

0.01

0.02

0.03

0 5 10 15 20 25 30

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0 5 10 15 20 25 30

Correlation between Δx and Δim:

Observed in data: 0.50

Baseline Model: 0.38

Model without IM in X: – 0.08

Baseline Model Without IM in X

Page 13

Extension II: UIP ModificationsGeneral Overview

Three Modifications to the UIP condition:

I. Incomplete financial markets – external risk premium depends on foreign asset position (Benigno, 2001).

II. “Modified” UIP – external risk premium depends on expected and lagged nominal exchange rate (Adolfson et al., 2007).

III. “Modified” UIP compatible with persistent inflation target differentials.

Page 14

Extension II: UIP ModificationsThe explicit modeling

From the households budget constraint:Local bonds

Foreign bondsExternal risk premium

Local nominal rate

Foreign nominal rate

External risk premium

I. Foreign asset

position

II. Expected depreciation

III. Adjusted of inflation target differentials

“Modified” UIP

Page 15

Extension II: UIP Modifications External Risk Premium Shock

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

0 5 10 15 20 25 30

Real exchange rate (s)

External Risk Premium (ΓB*)

Output (y)

Nominal interest rate (r)

inflation (πc)

Nominal exchange rate (S)

Baseline Model Non - “Modified” UIP

-0.05

0.00

0.050.10

0.15

0.20

0.25

0.300.35

0.40

0.45

0 5 10 15 20 25 30

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0 5 10 15 20 25 30

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

0 5 10 15 20 25 30

-0.10

-0.05

0.000.05

0.10

0.15

0.20

0.250.30

0.35

0.40

0 5 10 15 20 25 30

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0 5 10 15 20 25 30

Page 16

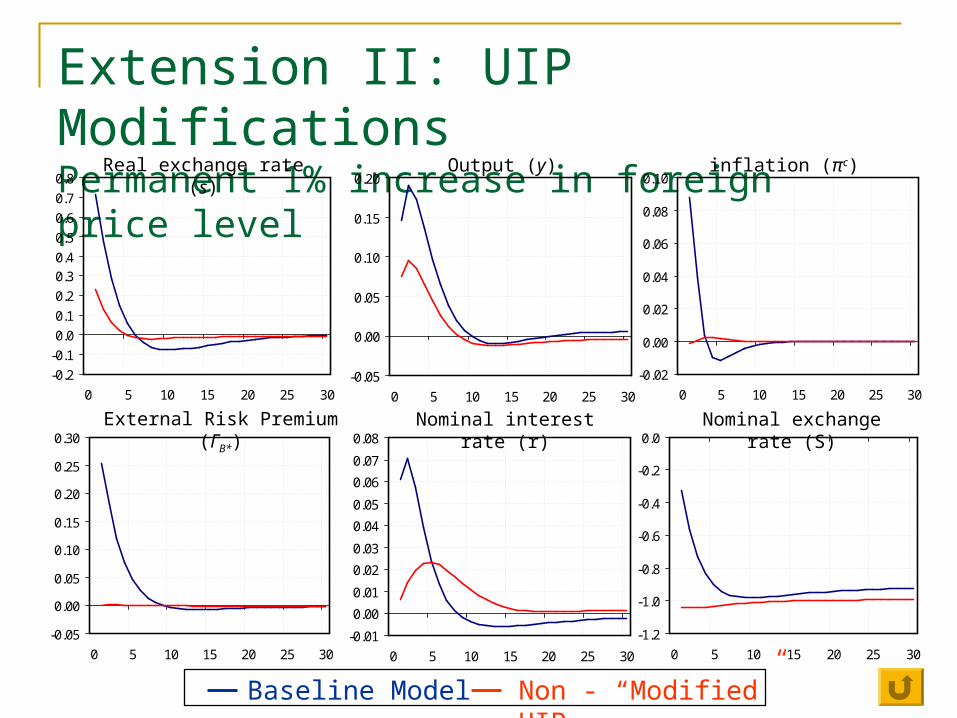

Extension II: UIP Modifications Permanent 1% increase in foreign price level

-0.2

-0.1

0.0

0.1

0.2

0.30.4

0.5

0.6

0.7

0.8

0 5 10 15 20 25 30

Real exchange rate (s)

External Risk Premium (ΓB*)

Output (y)

Nominal interest rate (r)

inflation (πc)

Nominal exchange rate (S)

Baseline Model Non - “Modified” UIP

-0.05

0.00

0.05

0.10

0.15

0.20

0 5 10 15 20 25 30

-0.02

0.00

0.02

0.04

0.06

0.08

0.10

0 5 10 15 20 25 30

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0 5 10 15 20 25 30-0.01

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0 5 10 15 20 25 30

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0 5 10 15 20 25 30

Page 17

Year-on-year Inflation and the Inflation Target – Israel and G4, 1992-2009

-4

-2

0

2

4

6

8

10

12

14

16

18

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

%

Israel: YoY inflation

Israel: Inflation target

Effective G4

Page 18

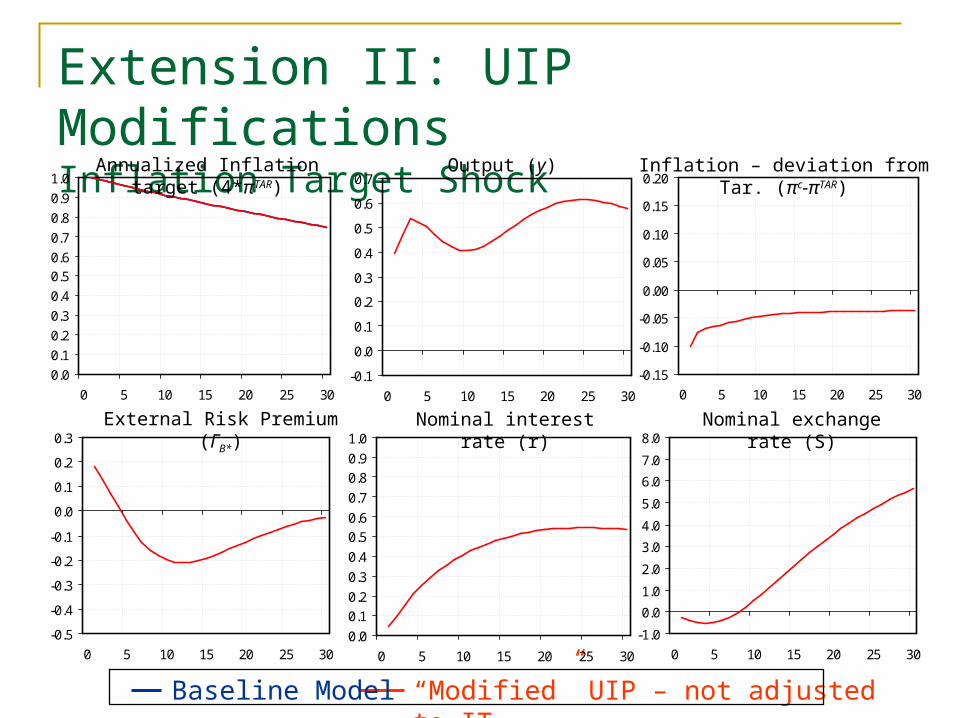

Extension II: UIP Modifications Inflation Target Shock

0.0

0.1

0.2

0.3

0.4

0.50.6

0.7

0.8

0.9

1.0

0 5 10 15 20 25 30

Annualized Inflation target (4*πTAR)

External Risk Premium (ΓB*) Nominal interest rate (r)

Inflation – deviation from Tar. (πc-πTAR)

Nominal exchange rate (S)

Baseline Model “Modified” UIP – not adjusted to IT

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0 5 10 15 20 25 30

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0 5 10 15 20 25 300.0

0.10.2

0.3

0.4

0.50.6

0.7

0.80.9

1.0

0 5 10 15 20 25 30

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

0 5 10 15 20 25 30

Output (y)

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 5 10 15 20 25 30

Page 19

Extension II: UIP Modifications Inflation Target Shock

External Risk Premium (ΓB*)

Output (y)

Nominal interest rate (r)

Inflation – deviation from Tar. (πc-πTAR)

Nominal exchange rate (S)

Baseline Model “Modified” UIP – not adjusted to IT

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 5 10 15 20 25 30

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0 5 10 15 20 25 30

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0 5 10 15 20 25 300.0

0.1

0.20.3

0.4

0.5

0.6

0.70.8

0.9

1.0

0 5 10 15 20 25 30

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

0 5 10 15 20 25 30

0.0

0.1

0.2

0.3

0.4

0.50.6

0.7

0.8

0.9

1.0

0 5 10 15 20 25 30

Annualized Inflation target (4*πTAR)

Page 20

Extension III: Time Varying LR Real RateMotivation

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

01-92 01-94 01-96 01-98 01-00 01-02 01-04 01-06 01-08

5-10 Years Ahead Forward Real Interest Rates (Derived from Government Indexed Bonds)

Israel

US

US (Nominal)

Page 21

Extension III: Time Varying LR Real Rate We add to the model:

Financial shock and structure that allow expected long-run (5 to

10 years) interest rates to change over time.

Monetary policy uses long-run interest rates (forward 5 to 10

years ahead) as benchmark rates.

Use data on long-run interest rates in estimation.

Page 22

Extension III: Time Varying LR Real Rate The explicit modeling From the households budget constraint:

Domestic financial premium:

Local bonds

Foreign bondsExternal risk premium

Local nominal rate

Foreign nominal rate

III. Domestic financial risk

premium shock

II. Symmetric financial risk-

premium shock

I. External financial risk-

premium shock

Page 23

Interest rate rule:

Long-run fwd real-rate:

Short-run real rate:

Inflation

Long-run fwd real rate

Extension III: Time Varying LR Real Rate The explicit modeling

OutputLong-runSmoothing

Inflation target

Page 24

The observable 5-10 year forward real rate derived from indexed government bonds:

Extension III: Time Varying LR Real Rate The explicit modeling

Observed fwd rate

Model predicted fwd rate

Constant Measurement error

Time varying term premium

Page 25

Extension III: Time Varying LR Real RateMotivation

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

01-92 01-94 01-96 01-98 01-00 01-02 01-04 01-06 01-08

5-10 Years Ahead Forward Real Interest Rates (Derived from Government Indexed Bonds)

Israel

US

Model derived “pure” fwd real-rate

Page 26

Extension IV: The Rest of the WorldOptions at Hand How to model the rest of the world (i*, π*, y*)?

Single-equation AR. Problem: can’t apply structural foreign

shocks.

VAR (example - NAWM). Problem: “Well” looking structural

shocks depend on identification assumption.

Closed economy NK small model. Compared to AR: better fit, structural shocks.

Compared to VAR: worse fit, better interpretation of shocks.

Problem: variables relevant to world model may be less relevant to

Israeli economy. Solution: bridge equations.

Page 27

Extension IV: The Rest of the WorldThe world Model IS curve (world output):

Phillips Curve (CPI inflation) :

Taylor rule (CB key rates) :

Page 28

Extension IV: The Rest of the WorldObservable Variables Observable Variables:

i* – G4 effective CB key rates π* – G4 effective CPI inflation Δy* - Dilemma:

G4 effective output growth is more adequate for world model. G4 effective import growth (Δim* ) is more adequate to explain

Israeli exports:

Solution: use Δy* and Δim* in observable set. Define bridge equation:

Page 29

Extension IV: The Rest of the WorldRecap on Foreign Output Transmission Mechanism IS curve for G4 effective output (Δy* ):

Bridge equation for G4 imports:

Export demand equation

Page 30

Extension IV: The Rest of the WorldWorld Import Shock (blue) vs. World Demand shock (red)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0 5 10 15 20 25 30

World: imports (im*), output (y*) Output (y)

Nominal interest rate (r)

inflation (πc)

Nominal exchange rate (S)

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0 5 10 15 20 25 30

-0.04

-0.02

0.00

0.02

0.04

0.06

0.08

0 5 10 15 20 25 30

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0 5 10 15 20 25 30

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0 5 10 15 20 25 30

World import shock (Non structural) World demand shock (structural)

World: key-rate (r*), inflation (π*)

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 5 10 15 20 25 30

Page 31

Extension IV: The Rest of the WorldWorld Import Shock (blue) vs. World Demand shock (red)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0 5 10 15 20 25 30

World: imports (im*), output (y*) Output (y)

Nominal interest rate (r)

inflation (πc)

Nominal exchange rate (S)

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0 5 10 15 20 25 30

-0.04

-0.02

0.00

0.02

0.04

0.06

0.08

0 5 10 15 20 25 30

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0 5 10 15 20 25 30

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0 5 10 15 20 25 30

World import shock (Non structural) World demand shock (structural)

World: key-rate (r*), inflation (π*)

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 5 10 15 20 25 30

Page 33

Schematic Diagram: Resources and Uses

C Private Consumption

IM Imports

G Public consumption

I Investment

H Intermediate goods

)Y – Gross Domestic Product(

K Capital

L Labor

X Exports

Page 34

Schematic Diagram: Prices

PC Private Consumption

PIM Imports

PG Public consumption

PI Investment

PH Intermediate goods

)Y – Gross DomesticProduct(

RK Rent

W Wage

PX Exports

Page 35

Schematic Diagram: Production and Inputs

Nh Nh Nh Nh

Monopolistic CompetitionWage Rigidity (Calvo,1983)

Labor aggregateNf

Intermediate good Hf

Nh

Capital servicesKs

f

TechnologyZ, ε

Production Function

Hf

Hf

InvestmentI

Capital stockKh

Utilization rate

u

Adjustment costsInvestment productivity

Households

Page 36

Schematic Diagram: From Intermediate Goods to Final Goods

Hf Hf Hf Hf

Monopolistic CompetitionPrice Rigidity (Calvo,1983)

Homogenous local intermediate good

H (Y)

Final Local UsesC, I, G

Hf IMf IMf IMf

Homogenous imported intermediate good

IM

IMfIMf

Xf

Xf

Xf

Export (stage I) QX

Homogenous Export good

X

Monopolistic CompetitionPrice Rigidity (Calvo,1983)

Foreign products

X *

Foreign DemandY*

Perfect Competition

MCCalvo

Page 37

Schematic Diagram: Monetary Transmission Process (signs relate to interest rate hike)

Ls

Ks

RBoI interest

rateS

Nominal ExchangeRate

PIM

Imports prices

PcConsumer Price

Index

sReal Exchange

Rate

RM-πExpected real

interestRate (Market)

WWage

LD

KD RK

Rent

PH

Price of domestic intermediate goods

I

C

NX

Production costs

(-)

(-)

(+)

(+)

YOutput

Supply (-)

(+)

(-)

DemandFactors of production

(-)

(+)

(-) (-)

(-)

(-)

(-)

(-) (-)

(-)

(-) (-)

(+)

Demands