26

The Brazilian Economy and the Pharmaceutical Market São Paulo, April 9th, 2010

The Brazilian Economy and the Pharmaceutical Market

São Paulo, April 9th, 2010

2

The Brazilian Economy

3

% per year

Source: IBGE and Ministry of Economy

GDP- Annual Growth Rate

4

Source: IMF

IMF Projected GDP growth

% Grouth

5

% contribution to GDP growth

* ProjectedSource: Central Bank of Brazil

Net Domestic and Foreign Demand

6

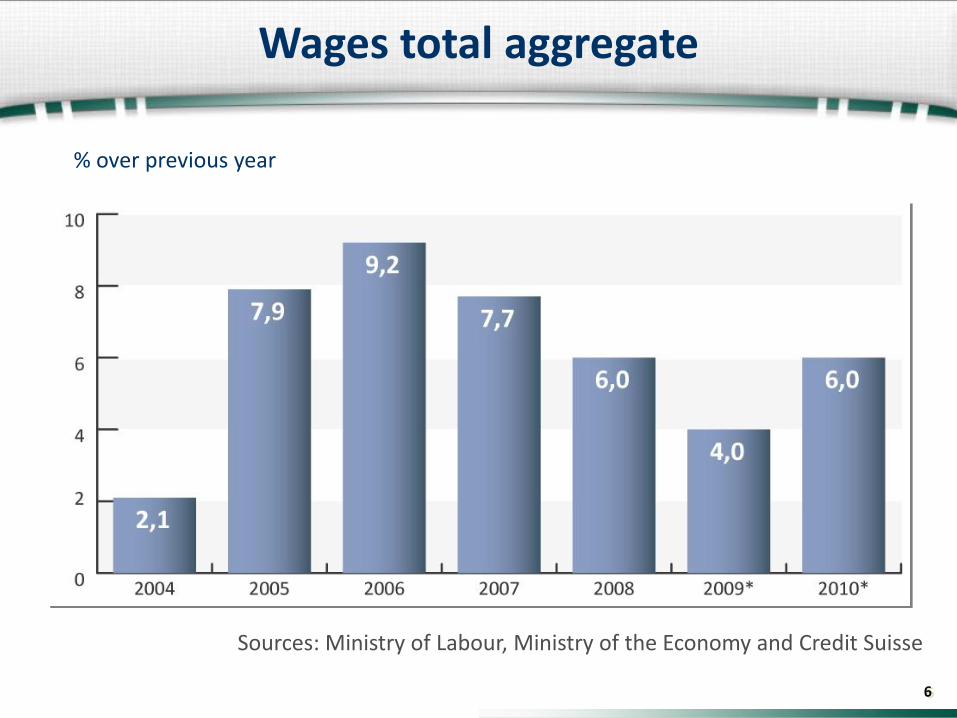

% over previous year

Sources: Ministry of Labour, Ministry of the Economy and Credit Suisse

Wages total aggregate

7

USD billions

* Up to 01/15/2010Source: Central Bank of Brazil

Foreign Exchange Reserves

8

% of GDP

Source: Central Bank of Brazil

Net Foreign Debt

9

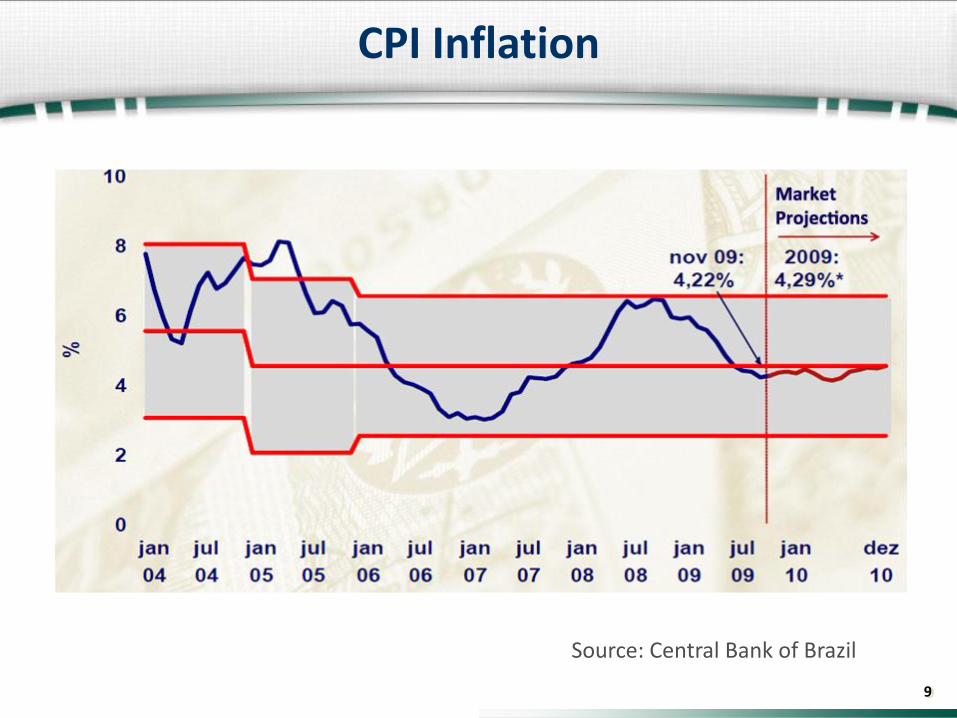

Source: Central Bank of Brazil

CPI Inflation

10

The Brazilian Pharmaceutical Market and the World Market

11

Worldwide $ 724.5 100.0 % 4.4 7.0

North America 311.9 43.1 1.3 6.9

Europe 237.4 32.8 5.4 6.5

AAA 72.3 10.0 15.7 13.2

Japan 68.6 9.5 2.6 2.9

Latin America 34.3 4.7 12.9 12.7

10 Key Markets 564.0 77.8 3.1 6.1

Audited Market 2008 % Growth (Const US$)

MAT Dec 2008 Sales US$bn % Mkt Shr 2008CAGR 03-07

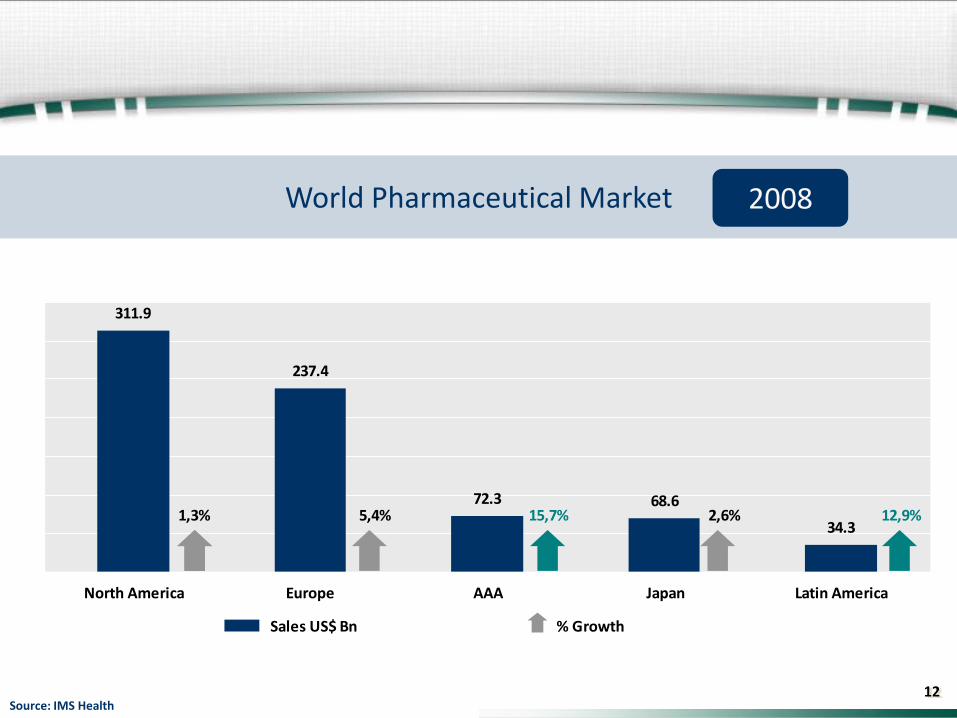

Growth in Asia and Latin America leads global market to an audited $725bn in 2008

Source: IMS Health

12

34.3

68.672.3

237.4

311.9

North America Europe AAA Japan Latin America

1,3% 5,4% 15,7% 2,6% 12,9%

Sales US$ Bn % Growth

World Pharmaceutical Market 2008

Source: IMS Health

13

Generic

19,221,5

23,6

26,4

30,2

2005 2006 2007 2008 2009

Brazilian Pharmaceutical Market 2009

53%

9%

50%

11%

48%

12%

45%

14%

42%

15%

38% 39% 40% 41% 43%

14,5%

2009

Source: IMS Health

R$billion

Pharma

Generic

OTC

14

19,221,5

23,6

26,4

30,2

2005 2006 2007 2008 2009

Brazilian Pharmaceutical Market (retail) 2009

62%

38%

60%

40%

58%

42%

56%

44%

54%

46%

14,5%

2009

Source: IMS Health

R$billion

Foreign Capital

Local Capital

15

Share of sales 2008US$ 34 billion

Brazil 36 %

Mexico 25 %

Venezuela 13 %

Argentina 9 %

Colombia 5 %

Others 12 %

LATIN AMERICA

Source: IMS Health

16

Country US$bn 2008% Mkt 2008

% Growth Const US$

2008

CAGR 03-07

US $ 291.0 40.2 1.1 6.8

Japan 68.6 9.5 2.6 2.9

Germany 41.1 5.7 4.9 3.5

China 19.6 2.7 26.7 21.6

Brazil 12.5 1.7 12.1 12.1

Turkey 10.5 1.5 11.1 21.9

Korea 9.6 1.3 11.2 12.6

Mexico 8.5 1.2 1.8 8.6

India 7.7 1.1 10.2 13.8

Russian Fed. 6.2 0.9 10.4 20.9

Three largest markets p/ comparison

Pharmerging maintain mostly strong growth

Source: IMS Health

17

RK US$ Ind.

09 08 Corporations Million Growth Evol.

Total 12.360 11,6%

1 1 EMS CORP 953 11,8% 100,2

2 2 SANOFI-AVENTIS 769 11,4% 99,8

3 3 ACHE 701 14,5% 102,6

4 4 MEDLEY 696 15,1% 103,1

5 5 NOVARTIS CORP 552 5,4% 94,4

6 7 EUROFARMA 489 26,6% 113,4

7 6 BAYER CORP 483 1,8% 91,2

8 8 PFIZER 374 0,6% 90,1

9 9 JOHNSON+JOHNSON CO 348 3,4% 92,6

10 10 GSK CORP 316 6,8% 95,7

Nota 1: Retail Only Stable

Accelerated Growth

Steep Drop

> 95 e < 105

> 105

< 95Source: IMS / PMB – MAT ABRIL 2009

Brazil - Top 10 - Pharma Companies

18

RK US$ Ind.

09 08 Corporations Million Growth Evol.

Total 12.360 11,6%

11 13 ASTRAZENECA BRASIL 297 24,4% 111,5

12 11 BOEHRINGER ING 276 2,4% 91,7

13 12 NYCOMED PHARMA LTD 269 5,1% 94,2

14 14 ROCHE 248 5,1% 94,2

15 16 BIOLAB 246 9,9% 98,5

16 15 D M IND. FTCA 240 1,6% 91,0

17 17 MANTECORP I Q FARM 236 6,0% 95,0

18 18 SCHERING PLOUGH 235 10,5% 99,0

19 24 SANDOZ DO BRASIL 228 43,4% 128,5

20 19 MERCK A. G. 216 12,1% 100,5

Source: IMS / PMB – MAT ABRIL 2009

Brazil - Top 11 – 20 Pharma Companies

Stable

Accelerated Growth

Steep Drop

> 95 e < 105

> 105

< 95

Nota 1: Retail Only

19

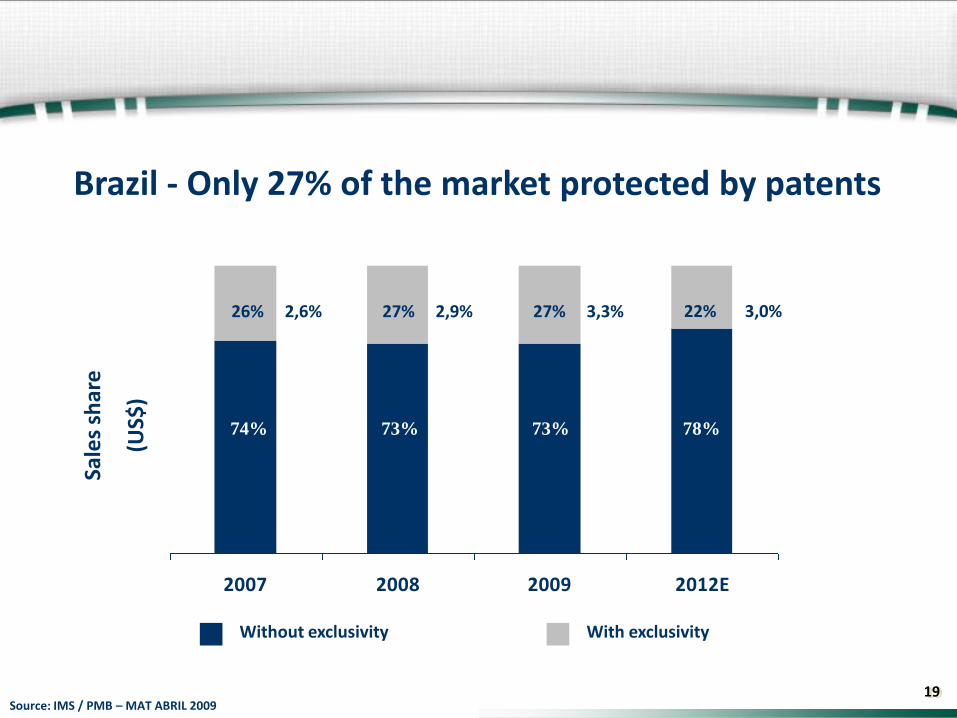

2007 2008 2009 2012E

Sale

s sh

are

(US$

)

26% 27% 27% 22%2,6% 2,9% 3,3% 3,0%

74% 73% 73% 78%

Without exclusivity With exclusivity

Source: IMS / PMB – MAT ABRIL 2009

Brazil - Only 27% of the market protected by patents

20

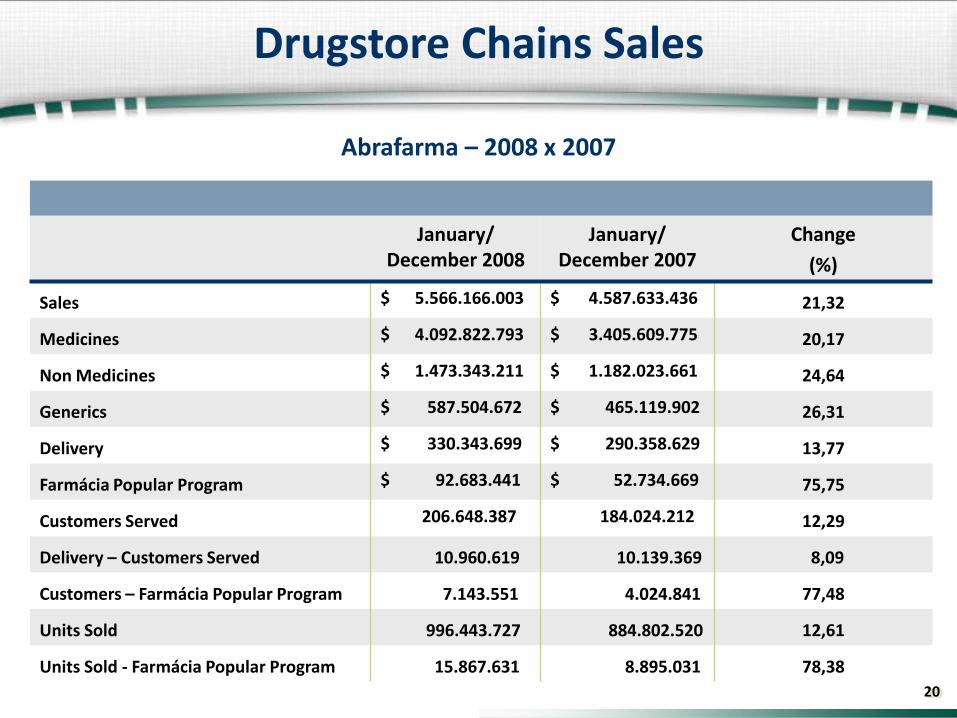

January/ December 2008

January/ December 2007

Change

(%)

Sales $ 5.566.166.003 $ 4.587.633.436 21,32

Medicines $ 4.092.822.793 $ 3.405.609.775 20,17

Non Medicines $ 1.473.343.211 $ 1.182.023.661 24,64

Generics $ 587.504.672 $ 465.119.902 26,31

Delivery $ 330.343.699 $ 290.358.629 13,77

Farmácia Popular Program $ 92.683.441 $ 52.734.669 75,75

Customers Served 206.648.387 184.024.212 12,29

Delivery – Customers Served 10.960.619 10.139.369 8,09

Customers – Farmácia Popular Program 7.143.551 4.024.841 77,48

Units Sold 996.443.727 884.802.520 12,61

Units Sold - Farmácia Popular Program 15.867.631 8.895.031 78,38

Abrafarma – 2008 x 2007

Drugstore Chains Sales

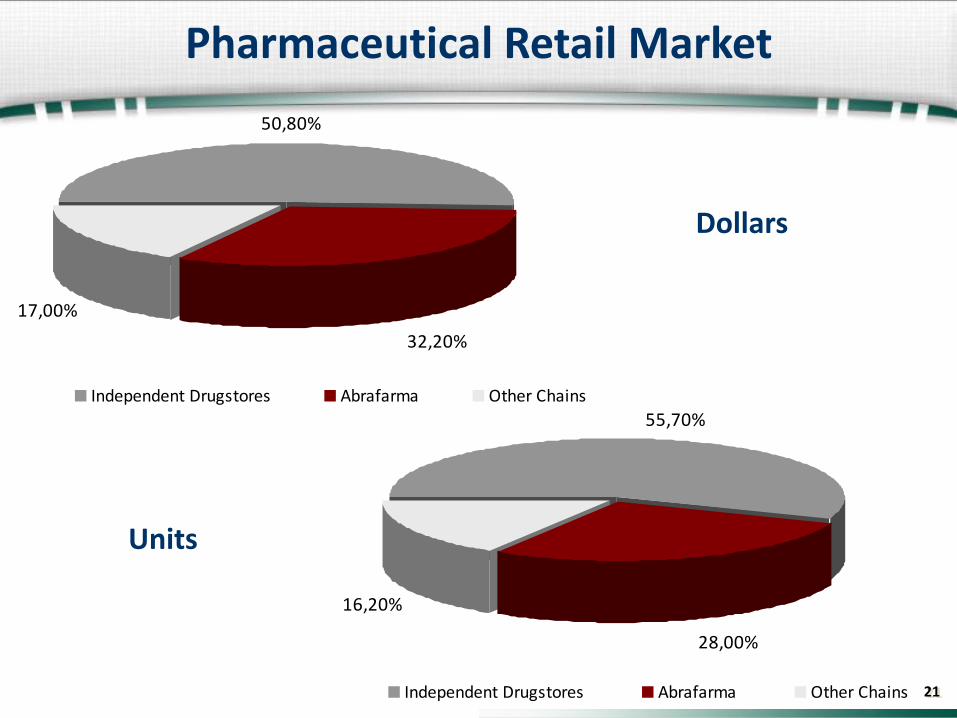

21

50,80%

32,20%

17,00%

Independent Drugstores Abrafarma Other Chains

55,70%

28,00%

16,20%

Independent Drugstores Abrafarma Other Chains

Dollars

Units

Pharmaceutical Retail Market

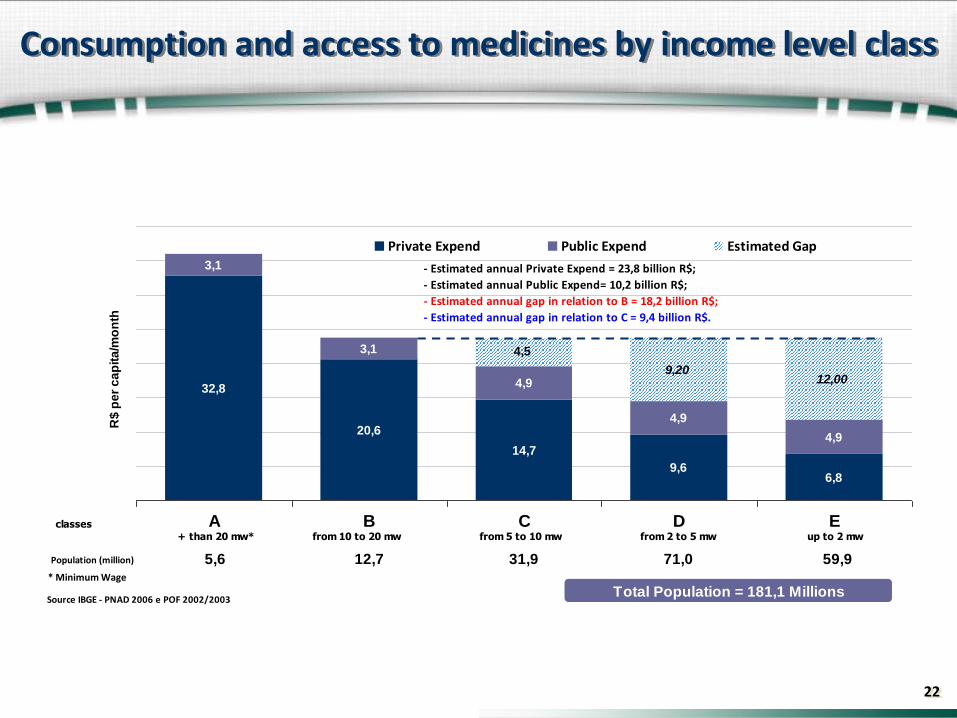

22

Consumption and access to medicines by income level class

32,8

20,6

14,7

9,66,8

3,1

3,1

4,9

4,9

9,2012,004,9

A B C D E

R$

pe

r c

ap

ita

/mo

nth

Private Expend Public Expend Estimated Gap

Source IBGE - PNAD 2006 e POF 2002/2003

4,5

- Estimated annual Private Expend = 23,8 billion R$;

- Estimated annual Public Expend= 10,2 billion R$;

- Estimated annual gap in relation to B = 18,2 billion R$;

- Estimated annual gap in relation to C = 9,4 billion R$.

+ than 20 mw* from 10 to 20 mw from 5 to 10 mw from 2 to 5 mw up to 2 mw

5,6 12,7 71,0 59,9Population (million)

classes

31,9

Total Population = 181,1 Millions* Minimum Wage

23

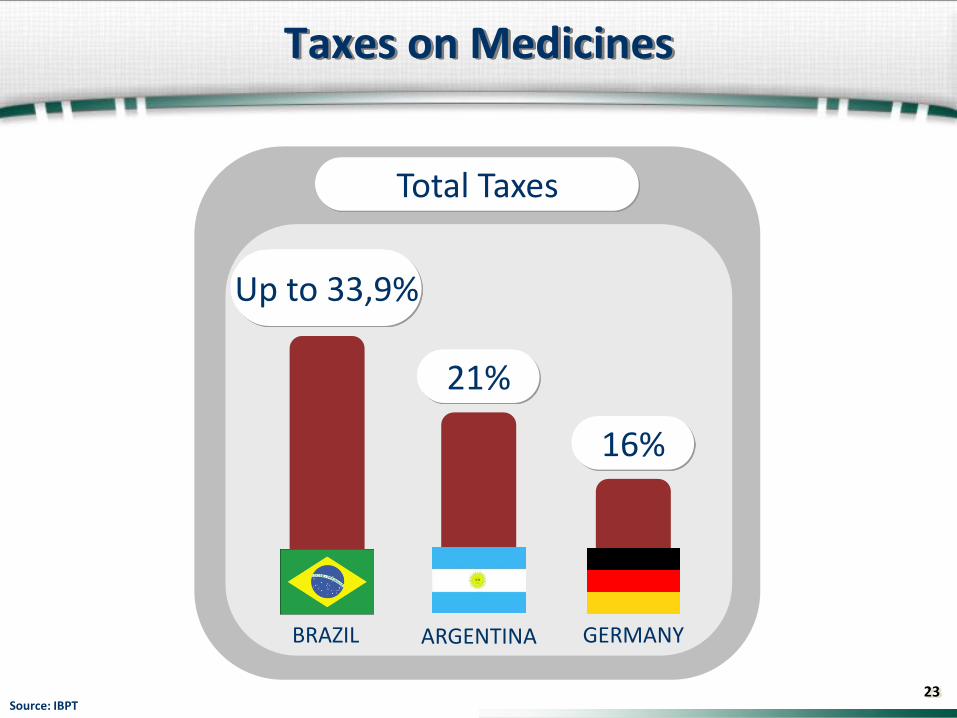

Taxes on Medicines

Source: IBPT

Total Taxes

Up to 33,9%

21%

16%

BRAZIL ARGENTINA GERMANY

24

Countries without Taxes on Medicines

Taxes

Source: IBPT

Exempt

UNITED STATES MEXICO

COLOMBIA UNITED KINGDOM

25

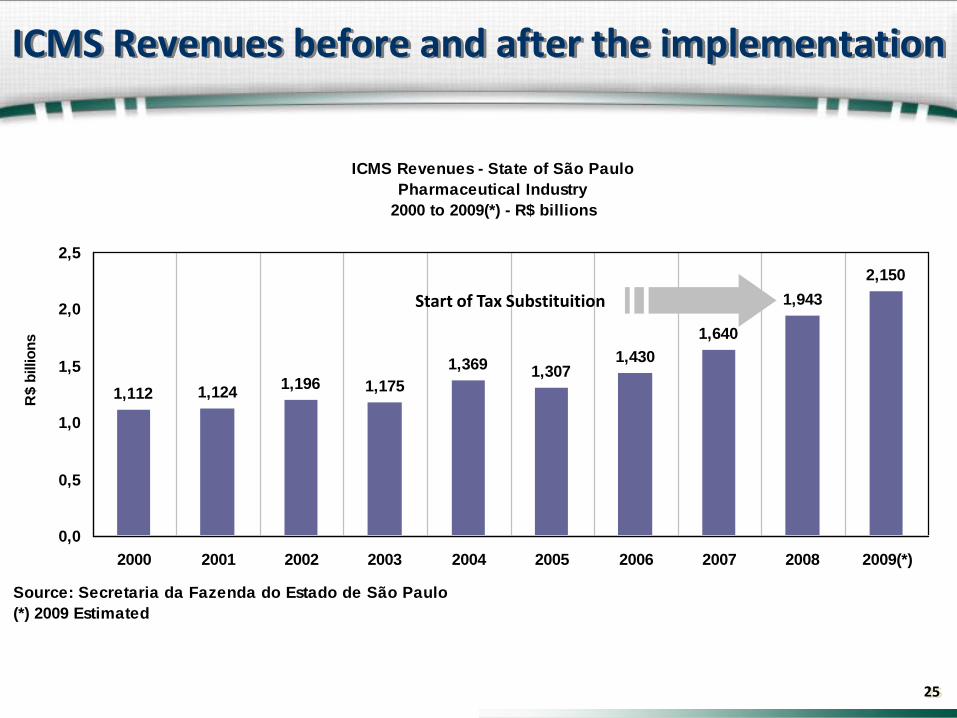

ICMS Revenues - State of São Paulo

Pharmaceutical Industry

2000 to 2009(*) - R$ billions

1,112 1,1241,196 1,175

1,369 1,3071,430

1,640

1,943

2,150

0,0

0,5

1,0

1,5

2,0

2,5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009(*)

Source: Secretaria da Fazenda do Estado de São Paulo

(*) 2009 Estimated

R$

billio

ns

ICMS Revenues before and after the implementation

Start of Tax Substituition

26

12,6%

13,1%

14,0%

15,1%

15,3%

15,5%

17,5%

20,6%

21,8%

28,2%

28,3%

30,3%

30,4%

30,4%

31,8%

32,3%

33,9%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Milk

Animal Medicines

Flour

Salt

Rice and Beans

Books

Cow Meat

Eggs

Fruits

Powder Milk

Boats/Airplanes

Theater/Movie

Toilet paper

Sugar

Tractor

Restaurant Lunch/Dinner

Human Medicines

Source: IBPT

Taxes on selected items