72

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | christiana-meghan-nichols |

| View: | 215 times |

| Download: | 0 times |

Understanding The Need For Life Insurance

The chief function of life insurance is to create an estate - that is, a definite sum of money. Some of the money paid to a beneficiary normally is used to meet current financial obligations created by the insured’s death. The remainder of the money may also be used to meet future needs of the insured’s beneficiary or beneficiaries.

Totaling the amounts required to pay for current and future expenses is often referred to as the “total needs approach” to determine how much life insurance a person should carry.

The chief function of life insurance is to create an estate - that is, a definite sum of money. Some of the money paid to a beneficiary normally is used to meet current financial obligations created by the insured’s death. The remainder of the money may also be used to meet future needs of the insured’s beneficiary or beneficiaries.

Totaling the amounts required to pay for current and future expenses is often referred to as the “total needs approach” to determine how much life insurance a person should carry.

Obligations At Death

Let’s begin with some immediate expenses incurred at death:

A funeral costs money. So do doctors; so does the ambulance and the

hospital, where even a short stay before death could add up to a sizable bill.

A new car, medical and funeral expenses, plus debts or current bills all comprise what are known as the deceased’s final expenses.

Final expenses, are also called dying expenses.

However, if people have a family dependent upon their income for their support and they die prematurely, we now have still other obligations they’re leaving behind, such as a:

Replacing the breadwinner’s incomeTaking care of the outstanding mortgage loan

on the house (if any)Today, almost everyone recognizes the

necessity of a good college education for their kids, if they hope to attain success in the business or professional world. Many conscientious parents consider it their duty – an obligation – to establish a fund for their children’s education.

Income taxes, estate and inheritance taxes, because they resulted from death, all go to make up what could be called “Death Taxes.”

The Need For Life InsuranceNo matter how many of these obligations an

individual leaves behind, there’s only one thing that will satisfy them…money! For this reason, a person who wants to relieve the family of obligations when he or she dies will plan to leave them with an estate – money – that is sufficient to cover all needs.

Laptop Needs ApproachThe needs approach looks at what the needs

of a family would be should the breadwinner die. These needs include paying off any final expenses, as well as meeting the requirements of the living.

When the total is reached, it is compared to the existing amount of insurance to meet those needs. If there is a shortage, that’s the amount of additional life insurance needed.

The Needs ApproachExample:

If Henry should die right now, he would leave his family in the following financial situation:

Final Expenses+Debts

25,000 Mortgage remaining

155,000 College costs (2 children)

80,000 TOTAL

260,000

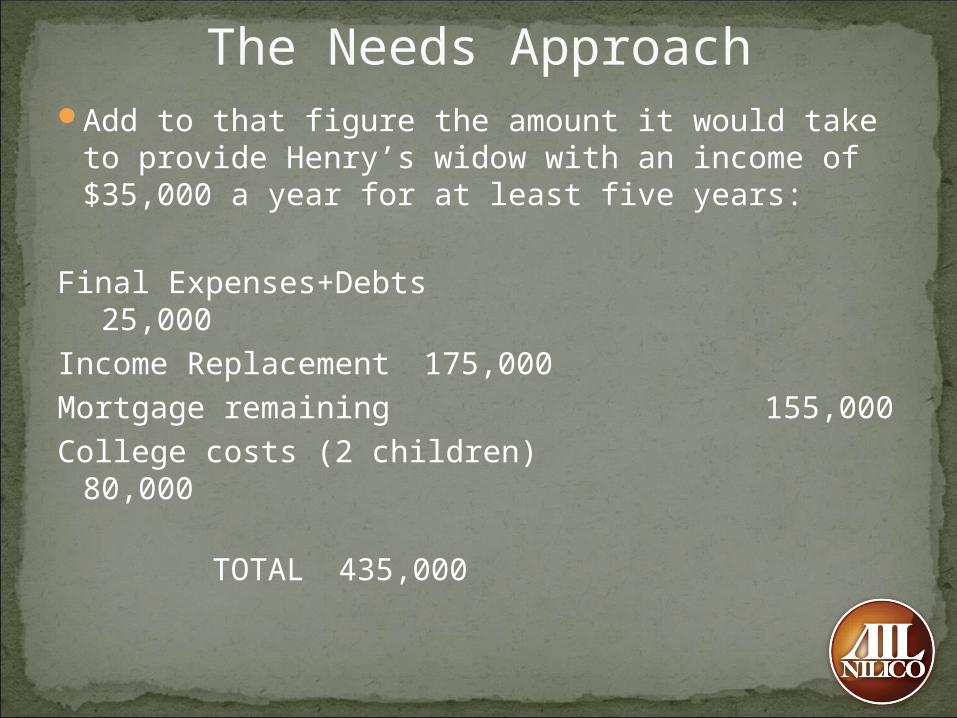

The Needs ApproachAdd to that figure the amount it would take to

provide Henry’s widow with an income of $35,000 a year for at least five years:

Final Expenses+Debts 25,000

Income Replacement 175,000Mortgage remaining 155,000College costs (2 children)

80,000 TOTAL

435,000

The Needs Approach

Let’s further suppose Henry had existing life insurance totaling $200,000. What additional amount of life insurance must Henry obtain according to the needs approach we’ve been discussing?

$235,000

BALANCE BETWEEN HUMAN ELEMENT AND TECHNOLOGY.

In our very competitive world, clients buy products today based on advertising messages, word of mouth, reputation etc.

In the AIL and NILICO world, clients buy our products because they like and trust the agent. The laptop presentation is key to show professionalism. However, equally important is the understanding of how to balance the human element with the technology.

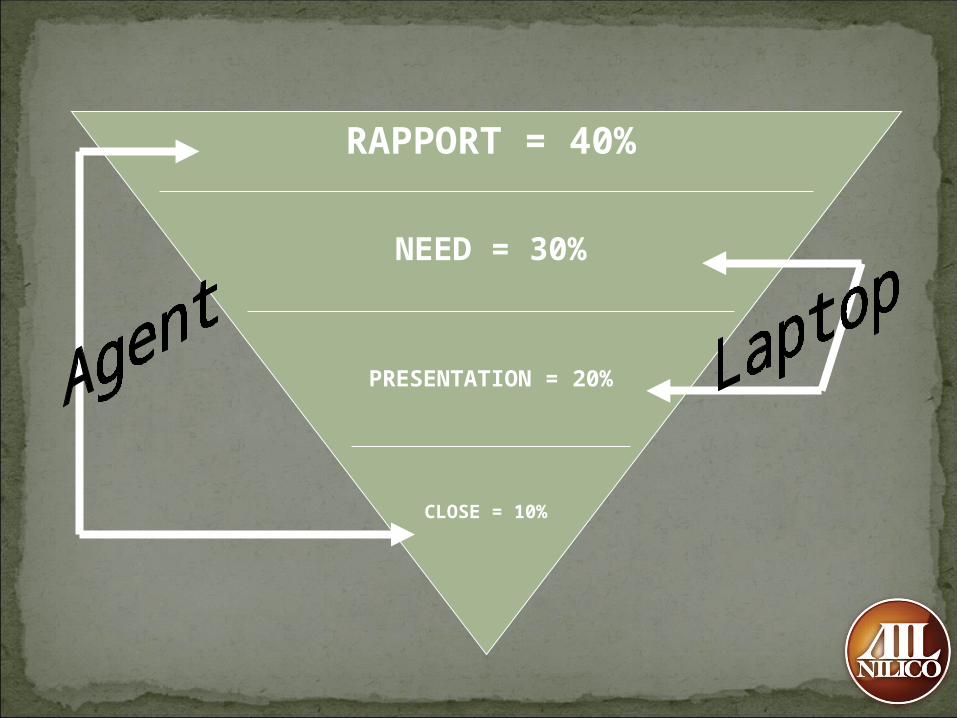

Here’s an example: Let’s imagine that the sale process is represented by an

upside down triangle. In it, you will see the percentages associated with each step of the sale:

Rapport – 40%; Need – 30%; Presentation 20%; Close 10%

We can easily assume then, if the laptop presentation takes care of the Need and Presentation part of the triangle, the human element must take care of the Rapport and Close. Therefore the balance between the technology and the human element must be 50-50.

RAPPORT = 40%

NEED = 30%

PRESENTATION = 20%

CLOSE = 10%

THE ART OF ESTABLISHING RAPPORT

Buyers today are more professional and better educated because they are bombarded with sales pitches over the radio and TV.

A professional agent can break through to all of this resistance by playing up to each customer as if that person is the first and the last client he/she will ever sell to. Make that customer want to do business with you.

People buy from agents they trust. Customers sometimes feel threatened by an

agent coming to their home. Their reaction can go from “run and hide”, to “make a lot of noise to scare the invader”, to “rise up and defend the territory”. Therefore everything an agent will do or say in the home will either produce tension or trust. Some sales people will back the customer into a corner and will start closing from the moment they walk in the home. This will build walls and not trust. Go slow, create trust and then move into your presentation. When your customer is tense, do something to ease the tension and when they are comfortable, proceed.

People buy from agents they respect.

When something goes wrong with your car you take it somewhere where you know they can fix it right. You trust your mechanic, if you like your car. Surely, you like your attorney, your accountant and your banker too, but not to fix your car. You listen to people you think will have something important to say. You look for signs of self confidence and success. Well, that is exactly how your prospects look at you. If you look, act and talk like you have something to say about things they need to hear, customers will give you the time to say it. Time, hence a few rules:

Respect the prospect’s time even when they don’t. Meaning: don’t spend more time than you need to make a sale presentation.

Respect the prospect’s territory. Remember that you are a guest so ask for permission to move around the room or come closer to show a brochure.

Respect your prospect’s intelligence by being straight and up front and not use trickery to gain on them.

When you walk into a house, find a place where you can sit comfortably and face the prospects in front of you. Put your hands on the table, relax and establish rapport.

Remember that people buy from you because they like you and they trust you. They buy you first, the company and the products after. Find something in common with your prospects and go from there. Avoid politics and religion. This should not last more than 15 minutes.

Scenario 1

Client: what’s this all about it anyway?

Agent; it’s about your (group) mail out to the members and the benefits you are entitled to.

Is this the first time you’ve mailed back the card?

Client: yes, it’s the first time

Agent: then let me start from the beginning and tell you what this is all about…..

Scenario 2

Client: no, I’ve mailed it before.Agent: anyone from the company ever been

here before to review the benefits with you?Client: no.Agent: then let me start from the beginning

and tell you what this is all about…..

Scenario 3

Client: no, I’ve mailed it before.Agent: anyone from the company ever been

here before to review the benefits with you?Client: yesAgent: did you apply for any of the programs

available at that time?Client: noAgent: then let me start from the beginning

and tell you what this is all about…..

Scenario 4

Client: no, I’ve mailed it before.Agent: anyone from the company ever been here

before to review the benefits with you?Client: yesAgent: did you apply for any of the programs

available at that time?Client: yes, I have a policy with youAgent: do you have a folder that looks like this?

(Show service file). Great, go get it for me please, so I can review your existing benefits while here and update your coverage. (It becomes a POS call)

The members who respond to the mail out from the group are entitled to receive additional benefits, if they qualify for it.

My job is simple: it is to provide you with the information of the no cost benefits that have already been negotiated for you and at the same time show you the additional benefits you may qualify for.

I’ll play a video for you that will explain the relationship between us and your group and explain better why I am here. (This first video is a MUST since it is an extension of the Warm Up).

(open your laptop, sign on and go to the first step)

Select a lead type and play video

AD&D TransitionThe first benefit is your no cost AD&D benefit.

This benefit has been negotiated for you by your (Group) as a way of thanking you for being a member in good standing.

(play video)

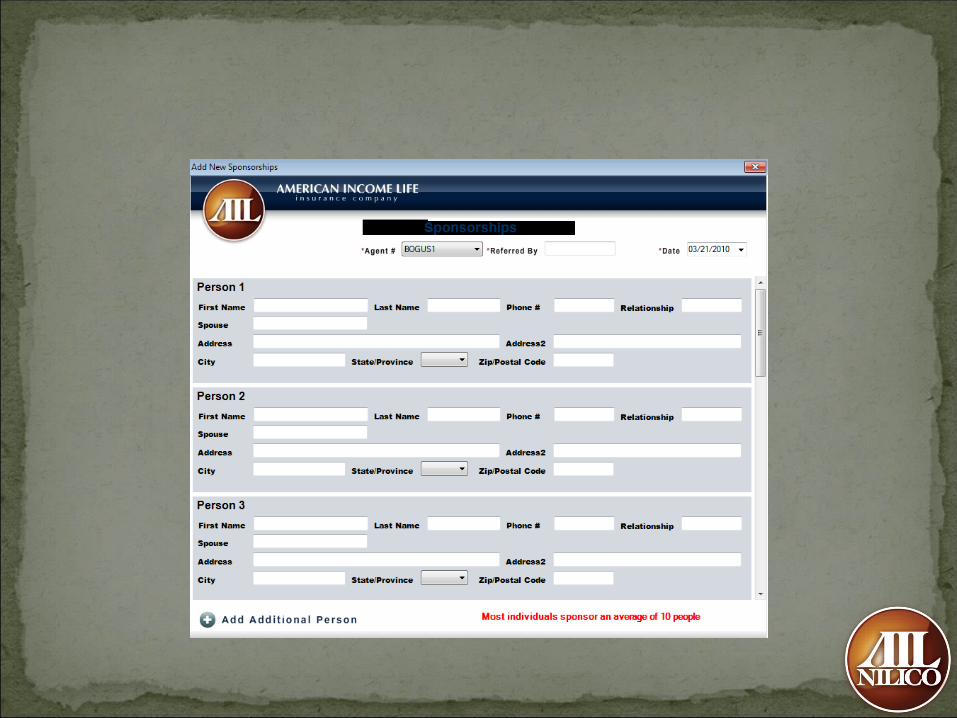

As you can see, we are trying to extend these benefit to the people in your circle of influence whom you know can use it.

Who would you like to sponsor first?

Asking For Referrals

a

The next benefit is the Child Safe kit which is designed to help protect your children. I’ll let the video explain better:

(play video)

Child Safe Transition

Our goal is to provide every family with kids these kits. For us to accomplish this, we are going to need your help:

Who would you like to sponsor first?

Asking For Child safe Referrals

Discount Card TransitionThis is an incredible value offered to the

members at no cost for the first year. It will provide you with 20% to 60% discounts on prescriptions, vision, hearing and chiropractic services.

(play video)

Who would you like to sponsor first?

Asking For Discount Card Referrals

This is your mandatory read off letter: (if you have the one of their group, please use that one)

It basically says that after I show you the benefits, explain to you how they work and answer all your questions, you give us a simple yes or no.

In other words if these benefits make sense as you’ll see they will, go ahead and take advantage of them, and if they don’t, here’s your (group) officer report form. I’ll have you complete this form to be returned to your (group) so they’ll get your feedback about these benefits.

Mandatory Read Off Letter Transition

Each member who sends back a card is

seen separately, because each member has a different need and a different want. What is right for you may not be right for the member I just saw, or the member that I will see after you.

Since everyone has a different need and a different want, this video will explain in simple words the need for these benefits.

Need For Life Insurance Video Transition

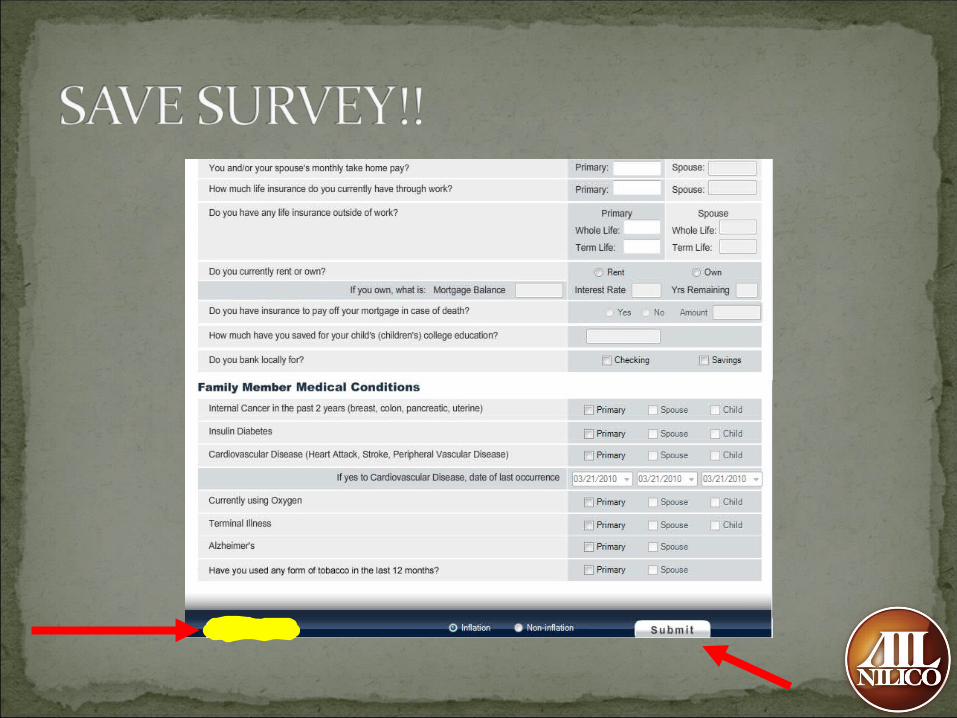

Now that you have more knowledge about the different types of insurance, I’ll go ahead and ask you some questions to see exactly what you qualify for and we’ll go on from there.

(proceed to survey)

Needs Analysis Survey Transition

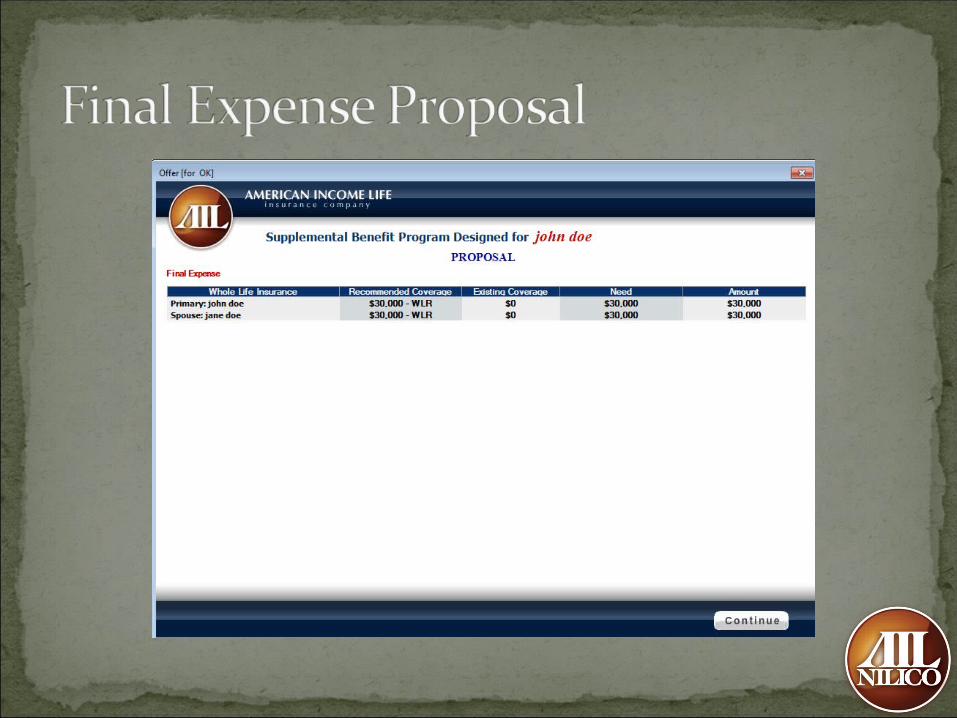

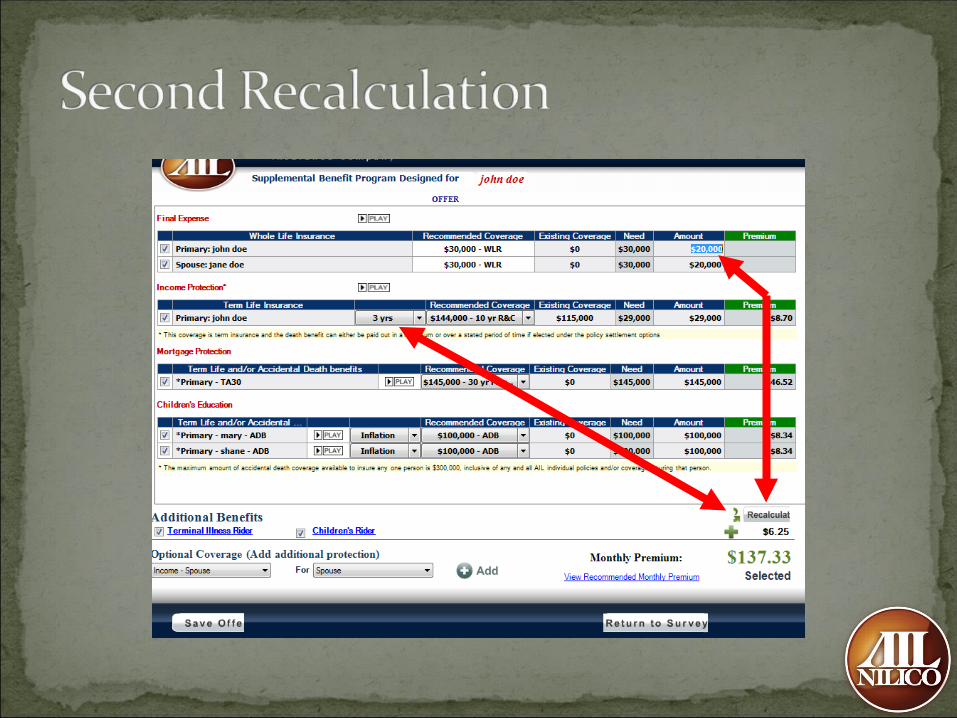

Preview reviewReview the recommended coverage, the

existing coverage, the need and the proposed amount

Ask a closing question: “Makes sense so far?”

Preview reviewReview the recommended coverage, the

existing coverage, the need and the proposed amount

Ask a closing question: “Makes sense so far?”

Preview reviewReview the recommended coverage, the

existing coverage, the need and the proposed amount

Ask a closing question: “Makes sense so far?”

Preview reviewReview the recommended coverage, the

existing coverage, the need and the proposed amount

Ask a closing question: “Makes sense so far?”

Final Proposal

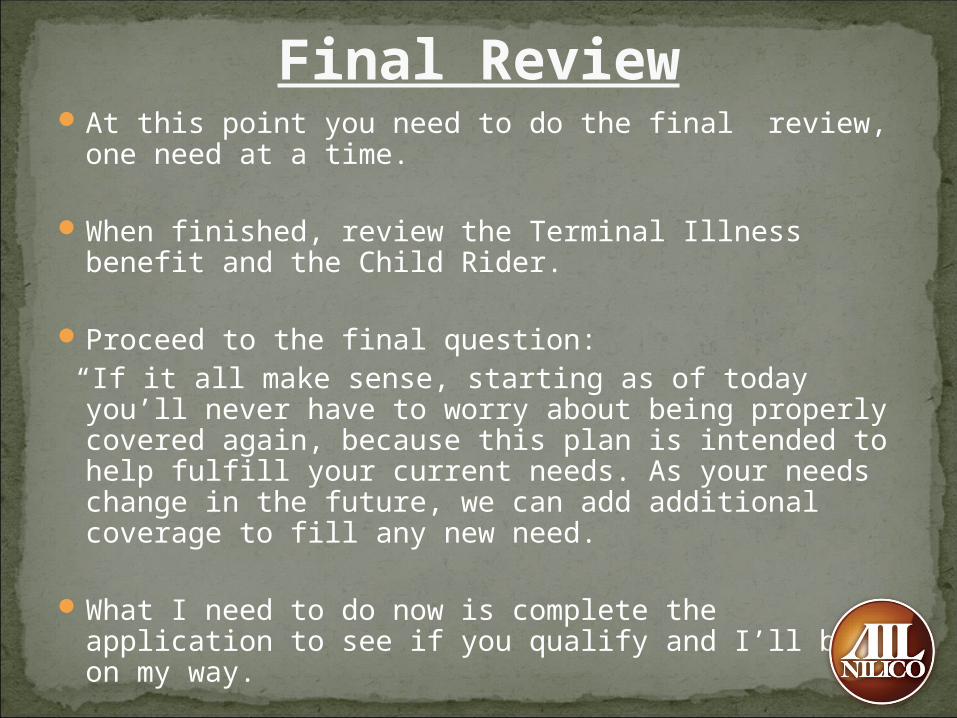

At this point you need to do the final review, one need at a time.

When finished, review the Terminal Illness benefit and the Child Rider.

Proceed to the final question: “If it all make sense, starting as of today you’ll never

have to worry about being properly covered again, because this plan is intended to help fulfill your current needs. As your needs change in the future, we can add additional coverage to fill any new need.

What I need to do now is complete the application to see if you qualify and I’ll be on my way.

Final Review

If the price objection comes up, move to reduce the plan, one item at a time.

Start with the whole life; reduce and recalculate; then ask: would this make you feel better?

Keep decreasing the items that have the highest price: WL, change the Re-adj. income from 5 yrs to 3 yrs etc…until the logic comes up with an amount that it is comfortable for the prospect.

The Key Point is to leave the full needs picture and reduce the cost. Do not take any of the needs away.

Objections

Objections

If you feel there’s no breakthrough on re-adjusting the proposal, ask one final question:

“Mr. prospect, if something were to happen unexpectedly, which one of these obligations would you rather have taken care of to protect your family at best?”

Depending on the answer, you want to proceed by adjusting the proposal to the product that is going to fulfill the obligation chosen by the prospect, exclude all other products and close: “This is exactly what you want. Does it make final sense?”

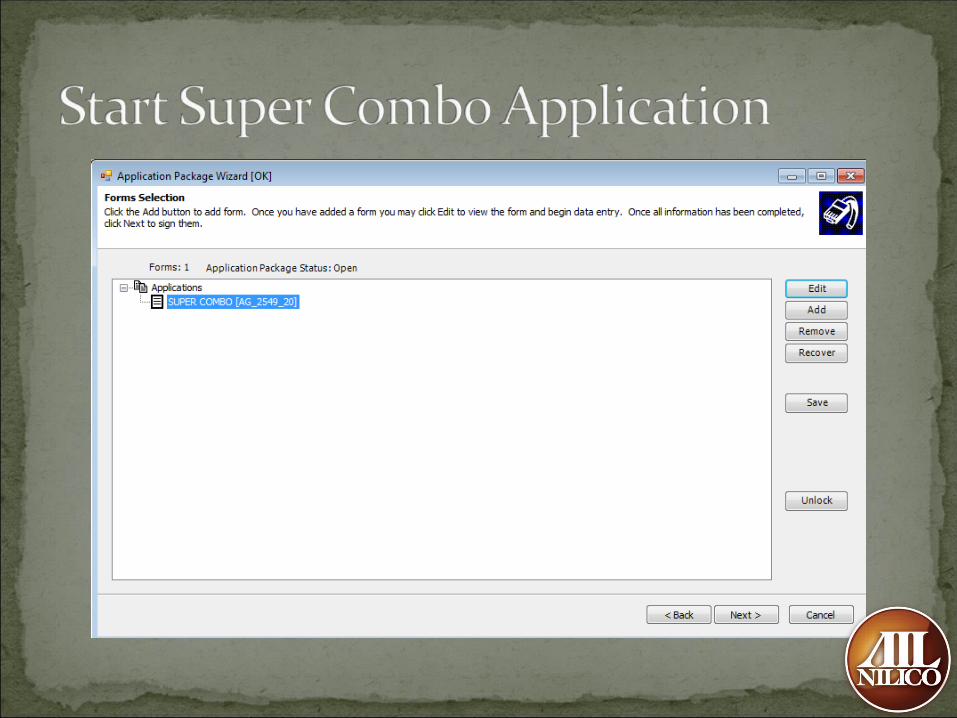

Proceed to EApp

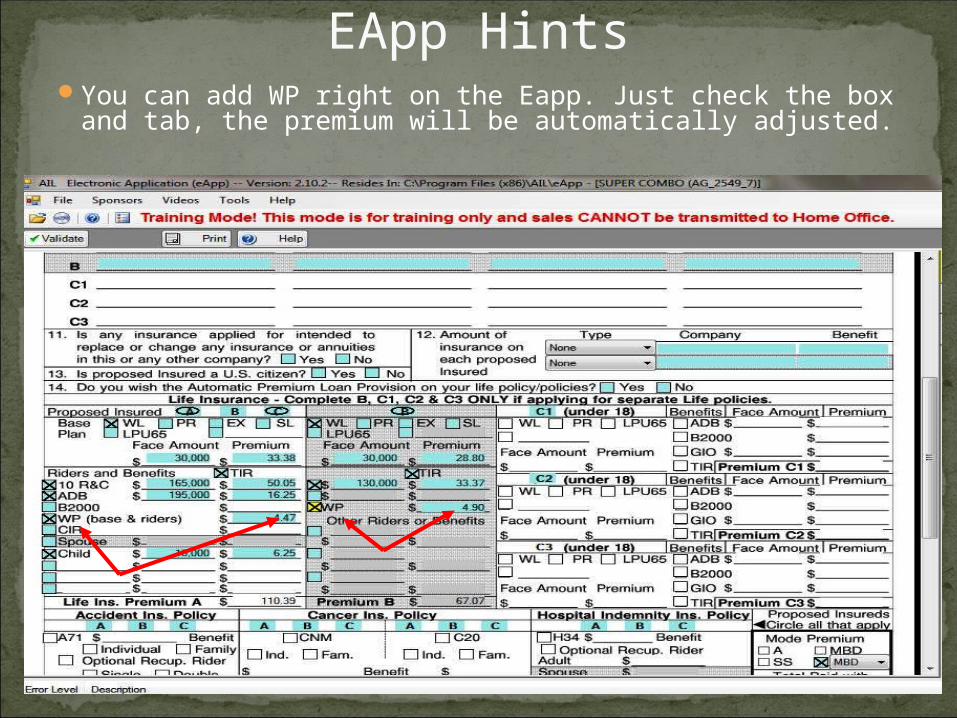

EApp HintsThe Maximum Amount of WLE that can be

manually proposed is $149,999:

EApp HintsYou can add WP right on the Eapp. Just check the box

and tab, the premium will be automatically adjusted.

EApp HintsIf QUESTION #13 is No for both insured, the wizard brings up only one residency addendum

for the primary insured. If you need to complete a second residency addendum, you will need to add it from the ADD feature on the wizard.

EApp Hints If a single person has more than $30,000 existing WL coverage and no

other obligations at death, the proposal comes up blank. You can manually add products from the Drop Down such as an A71000 or a Critical Illness Plan and an additional WL: Here’s a sample Proposal.

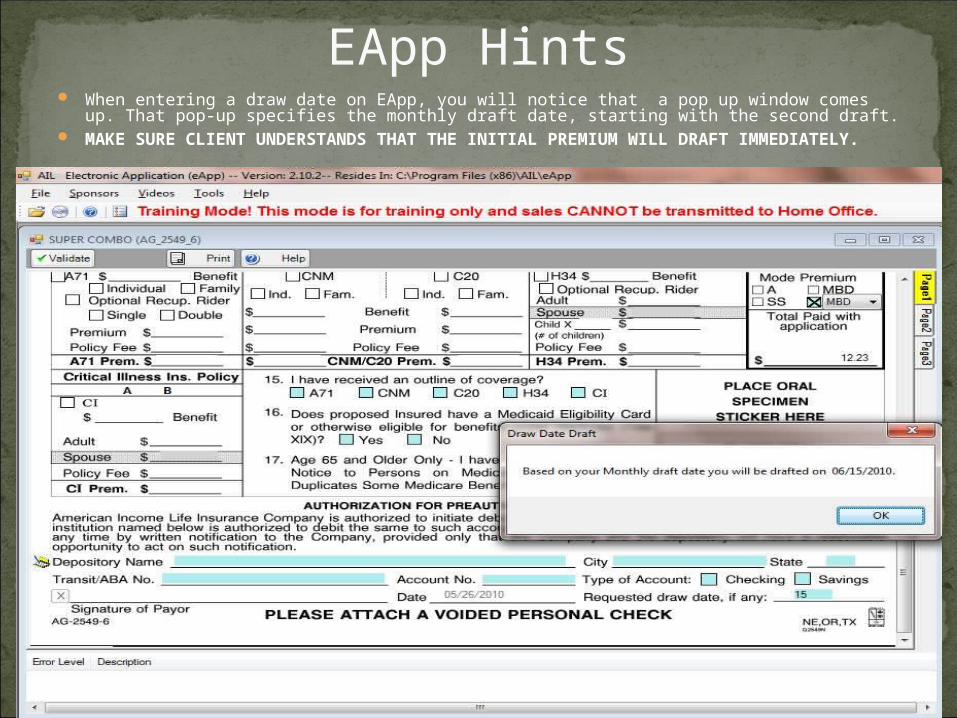

EApp Hints When entering a draw date on EApp, you will notice that a pop up window comes up. That

pop-up specifies the monthly draft date, starting with the second draft. MAKE SURE CLIENT UNDERSTANDS THAT THE INITIAL PREMIUM WILL DRAFT

IMMEDIATELY.

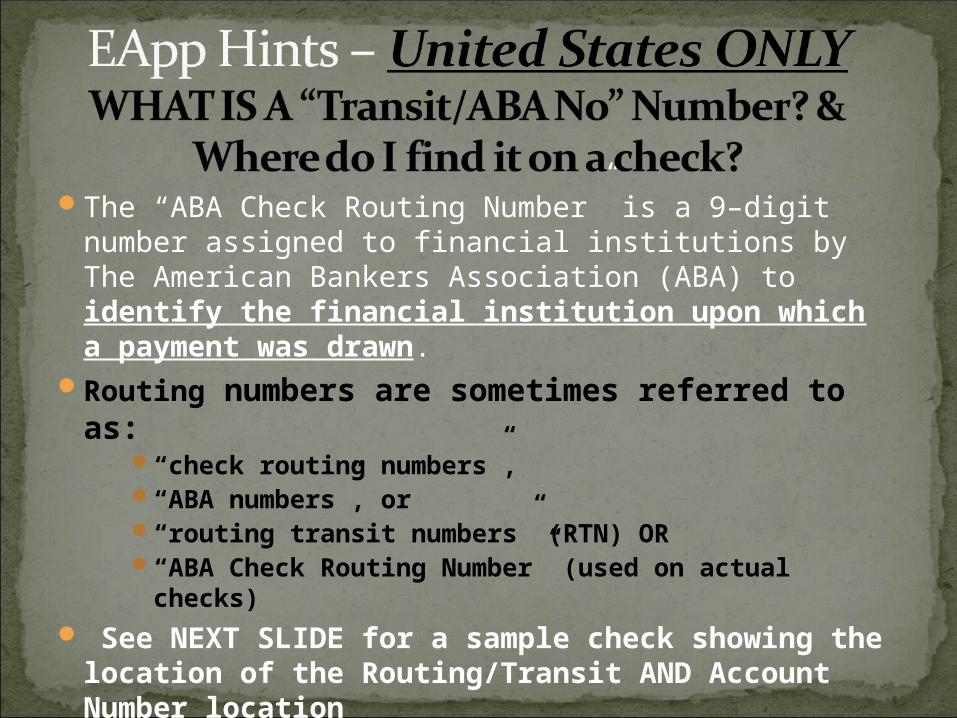

The “ABA Check Routing Number” is a 9–digit number assigned to financial institutions by The American Bankers Association (ABA) to identify the financial institution upon which a payment was drawn.

Routing numbers are sometimes referred to as:

“check routing numbers”, “ABA numbers”, or “routing transit numbers” (RTN) OR“ABA Check Routing Number” (used on actual

checks) See NEXT SLIDE for a sample check showing

the location of the Routing/Transit AND Account Number location

Refer to SAMPLE check below to know where to locate NINE (9) DIGIT “ ABA Check Routing Number” and Account Number

THE SAME SCHEME IS USED FOR ALL CHECKS FROM ALL US BANKS

Use this 9-digit # for Check Transit/ABA No

on ALL E-Apps