11

The Considered Consumer

The Considered Consumer

20 years ago 10 years ago Today

The average number of clothing stores used regularly

In our Reshaping of Retail report last year, Hammerson heralded a new era in retail, that of the Considered Consumer. It is characterised by a consumer that is less concerned with the pure acquisition of products and is more concerned about their quality and real value. Our report this year uncovers that this attitude shows no sign of waning with the Considered Consumer becoming the new norm.

Consumers are not only more considered when it comes to their expenditure, they are also taking significantly more time on the buying process with browsing, researching and comparing taking the lion’s share of consumers’ time and energy.

In this year’s report, leading retail consultant Conlumino, has continued to challenge how consumers are spending and which locations are at the top of consumers’ shopping lists.

Despite being considered, consumers know what they want and don’t want from their retail experience. As choice increases, consumers are demanding more from their Convenience Shop and although it’s the most frequent type of trip, consumers are expecting more from what would have previously been considered a simple ‘pop to the shops’. The Experience Shop needs to excite, and retailers and destinations which become stale and boring will lose out. As for the Luxury Shop, a strong product alone is not enough; consumers value the feeling of indulgence throughout the entire experience.

The performance of different retail locations does however remain polarised and this will continue. Locations and stores have to offer an experience which goes above and beyond the ease and convenience of what online shopping can provide. This is regardless of size of location or region, and destinations that provide consumers with an interactive and inspirational offer will prosper.

David AtkinsChief ExecutiveHammerson

The retail environment is changing more quickly than ever. The digital revolution is having a profound effect on how people shop, and how retailers operate.

Continued era of the Considered Consumer 4

How we shop 11

Planned Purchasing – Goodbye impulse buys 7

The Luxury Shop 16

The Convenient Shop 12

The Experience Shop 14

A focus on fashion - The roving eye 9

Fast facts 2

Foreword 3

24/7 Sales 7

Browsing is the new buying 8

Conclusion 18

Average breakdown of non-food expenditure over the past year (%)

Impulse14.8%

Promotional18.0%

Browsing & bought18.8%

Planned48.8%

0.3 days 0.2 days 0 days

Browsing Research Purchasing Collection

Browsing Research Purchasing Collection

52min

23min

5min

3min

89min

16min

4min

2min

Purchasing duration - 10 years ago

0.8 days 0.9 days 1.7 days

Fast Facts Foreword

Contents

Purchasing duration - Today

3

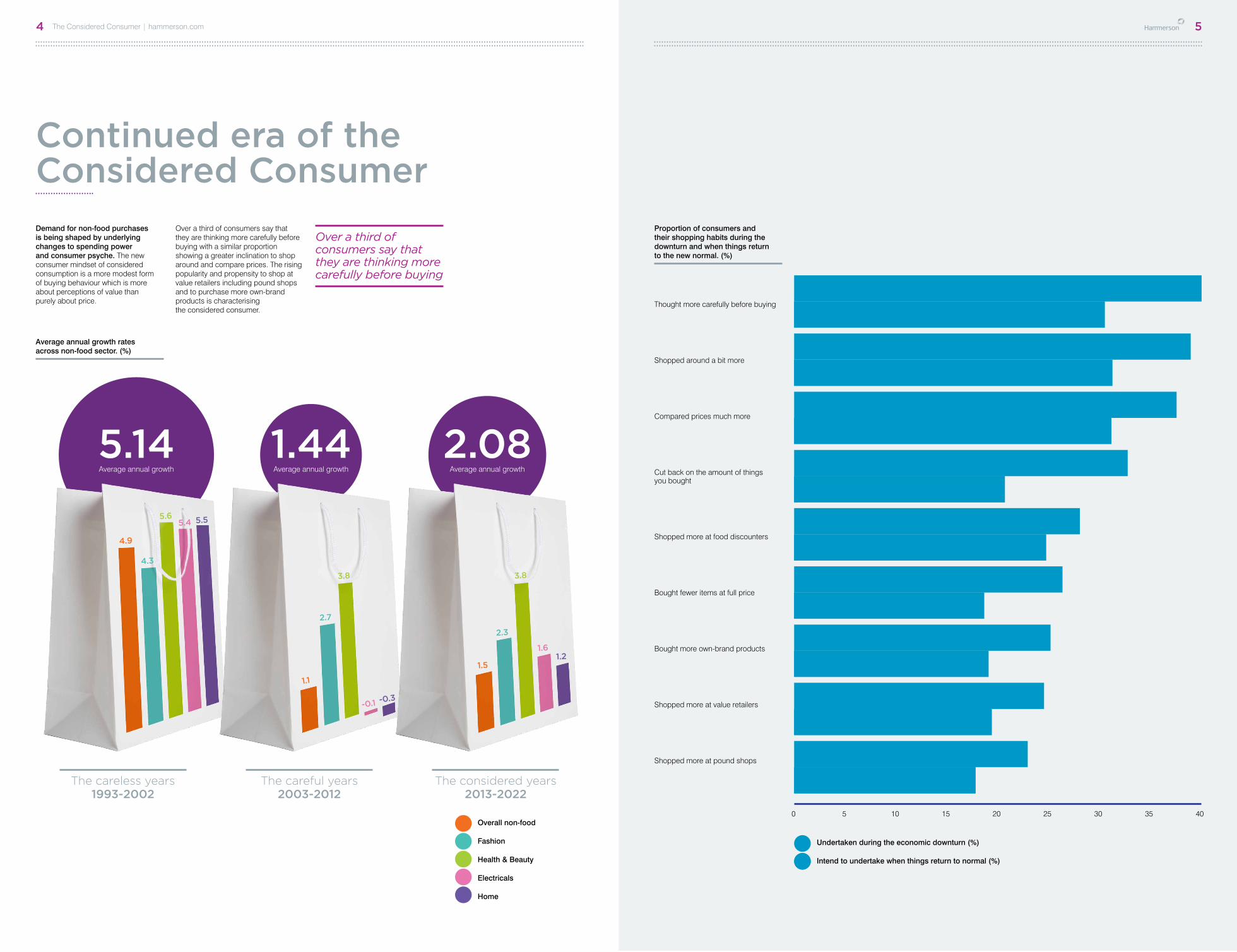

Continued era of the Considered Consumer

Demand for non-food purchases is being shaped by underlying changes to spending power and consumer psyche. The new consumer mindset of considered consumption is a more modest form of buying behaviour which is more about perceptions of value than purely about price.

Over a third of consumers say that they are thinking more carefully before buying with a similar proportion showing a greater inclination to shop around and compare prices. The rising popularity and propensity to shop at value retailers including pound shops and to purchase more own-brand products is characterising the considered consumer.

Over a third of consumers say that they are thinking more carefully before buying

Overall non-food

Fashion

Health & Beauty

Electricals

Home

Undertaken during the economic downturn (%)

Intend to undertake when things return to normal (%)

0 5 10 15 20 25 30 35 40

Thought more carefully before buying

Shopped around a bit more

Compared prices much more

Cut back on the amount of things you bought

Shopped more at food discounters

Bought fewer items at full price

Bought more own-brand products

Shopped more at value retailers

Shopped more at pound shops

The careless years1993-2002

The careful years2003-2012

The considered years2013-2022

5.14Average annual growth

1.44Average annual growth

2.08Average annual growth

4.9

1.5

1.1

4.3

2.3

2.7

5.6

3.83.8

5.4

1.6

-0.1

5.5

1.2

-0.3

Proportion of consumers and their shopping habits during the downturn and when things return to the new normal. (%)

Average annual growth rates across non-food sector. (%)

5The Considered Consumer | hammerson.com4

Planned purchasing – Goodbye impulse buys

24-7 Sales

There has been a significant shift in how consumers are spending and what triggers the initial purchase.

Planned purchases have increased at the expense of impulse shopping. Not only are consumers being more careful and considered with expenditure, the convenience of online shopping is making it easier to compare ranges and prices before purchasing.

Almost half of expenditure on non-food is now planned and compared to 12 months ago a third of consumers are impulse shopping less, reinforcing the ‘considered’ nature of shopping today.

Average breakdown of non-food expenditure over the past year (%)

While a sense of frugality is becoming more ingrained within the consumer psyche, the influence of discounting is waning. Shoppers are showing less enthusiasm towards promotions as a result of retailers upping the frequency of discounting over the past couple of years.

Deep, regular discounting has become a double edged sword. Sales are gradually losing impact, however, at the same time consumers are showing less inclination to purchase at full price if they know a discount event is on the horizon. Most consumers, 60% (especially women) say they will now wait until a product is on offer before purchasing. Nearly three quarters (70%), say they rarely purchase items at full price.

Most consumers 60% say they will now wait until a product is on offer before purchasing

Planned+24. 6%

Browsing & bought-5.0%

Promotional+17.6%

Impulse -32.7%

More

About the same

Less

Impulse14.8%

Promotional18.0%

Browsing & bought18.8%

Planned48.8%

Different types of shopping undertaken during the economic downturn (%)

7The Considered Consumer | hammerson.com6

0.3 days 0.2 days 0 days

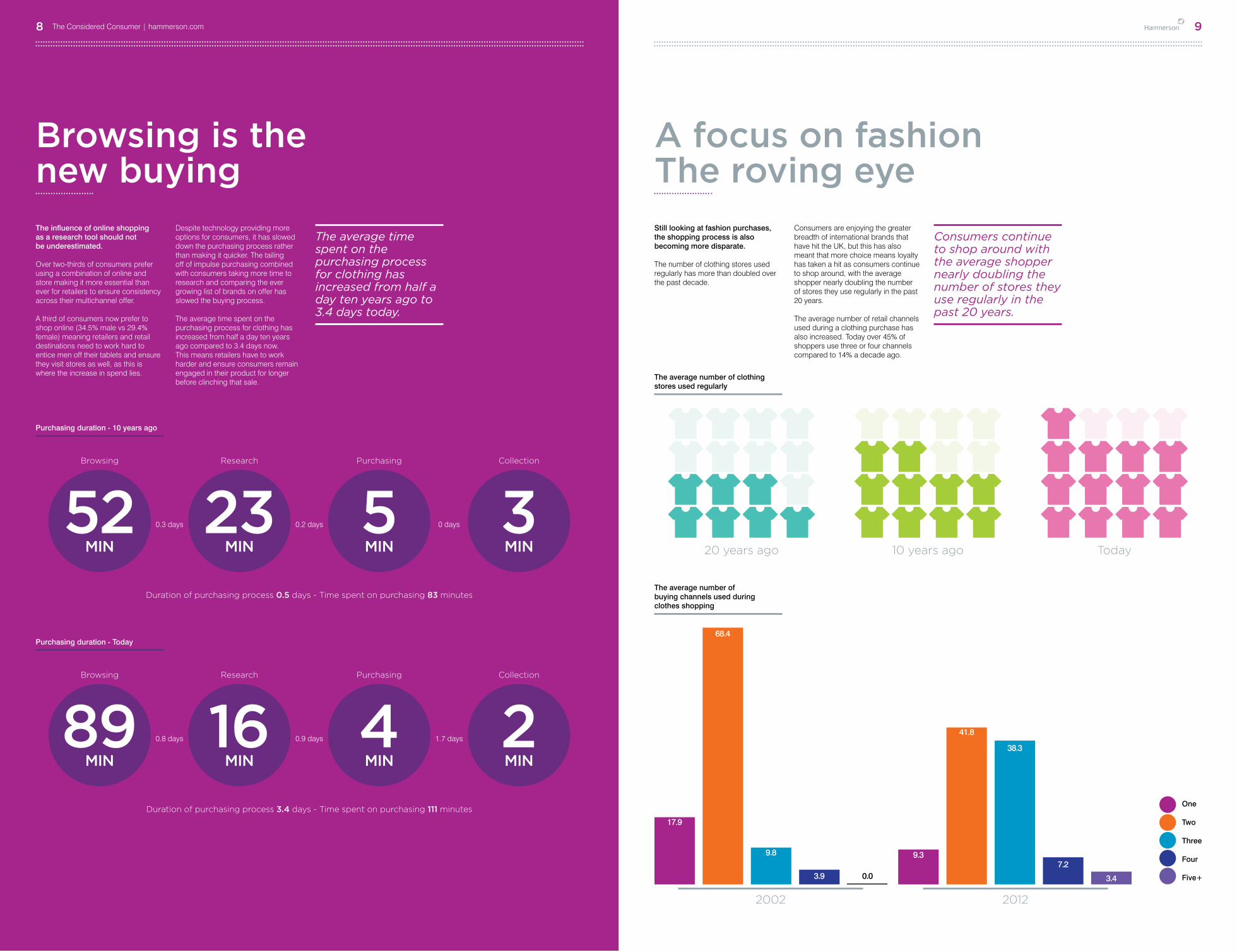

Browsing is the new buying

The influence of online shopping as a research tool should not be underestimated.

Over two-thirds of consumers prefer using a combination of online and store making it more essential than ever for retailers to ensure consistency across their multichannel offer.

A third of consumers now prefer to shop online (34.5% male vs 29.4% female) meaning retailers and retail destinations need to work hard to entice men off their tablets and ensure they visit stores as well, as this is where the increase in spend lies.

Despite technology providing more options for consumers, it has slowed down the purchasing process rather than making it quicker. The tailing off of impulse purchasing combined with consumers taking more time to research and comparing the ever growing list of brands on offer has slowed the buying process.

The average time spent on the purchasing process for clothing has increased from half a day ten years ago compared to 3.4 days now. This means retailers have to work harder and ensure consumers remain engaged in their product for longer before clinching that sale.

The average time spent on the purchasing process for clothing has increased from half a day ten years ago to 3.4 days today.

A focus on fashion The roving eye

Still looking at fashion purchases, the shopping process is also becoming more disparate.

The number of clothing stores used regularly has more than doubled over the past decade.

Consumers are enjoying the greater breadth of international brands that have hit the UK, but this has also meant that more choice means loyalty has taken a hit as consumers continue to shop around, with the average shopper nearly doubling the number of stores they use regularly in the past 20 years.

The average number of retail channels used during a clothing purchase has also increased. Today over 45% of shoppers use three or four channels compared to 14% a decade ago.

Consumers continue to shop around with the average shopper nearly doubling the number of stores they use regularly in the past 20 years.

Duration of purchasing process 0.5 days - Time spent on purchasing 83 minutes

Duration of purchasing process 3.4 days - Time spent on purchasing 111 minutes

Browsing Research Purchasing Collection

20 years ago 10 years ago Today

Browsing Research Purchasing Collection

52min

23min

5min

3min

89min

16min

4min

2min

Purchasing duration - 10 years ago

The average number of clothing stores used regularly

Purchasing duration - Today

0.8 days 0.9 days 1.7 days

One

Two

Three

Four

Five+

2002 2012

17.9

68.4

9.8

3.9 0.0

9.3

41.8

38.3

7.2

3.4

The average number of buying channels used during clothes shopping

9The Considered Consumer | hammerson.com8

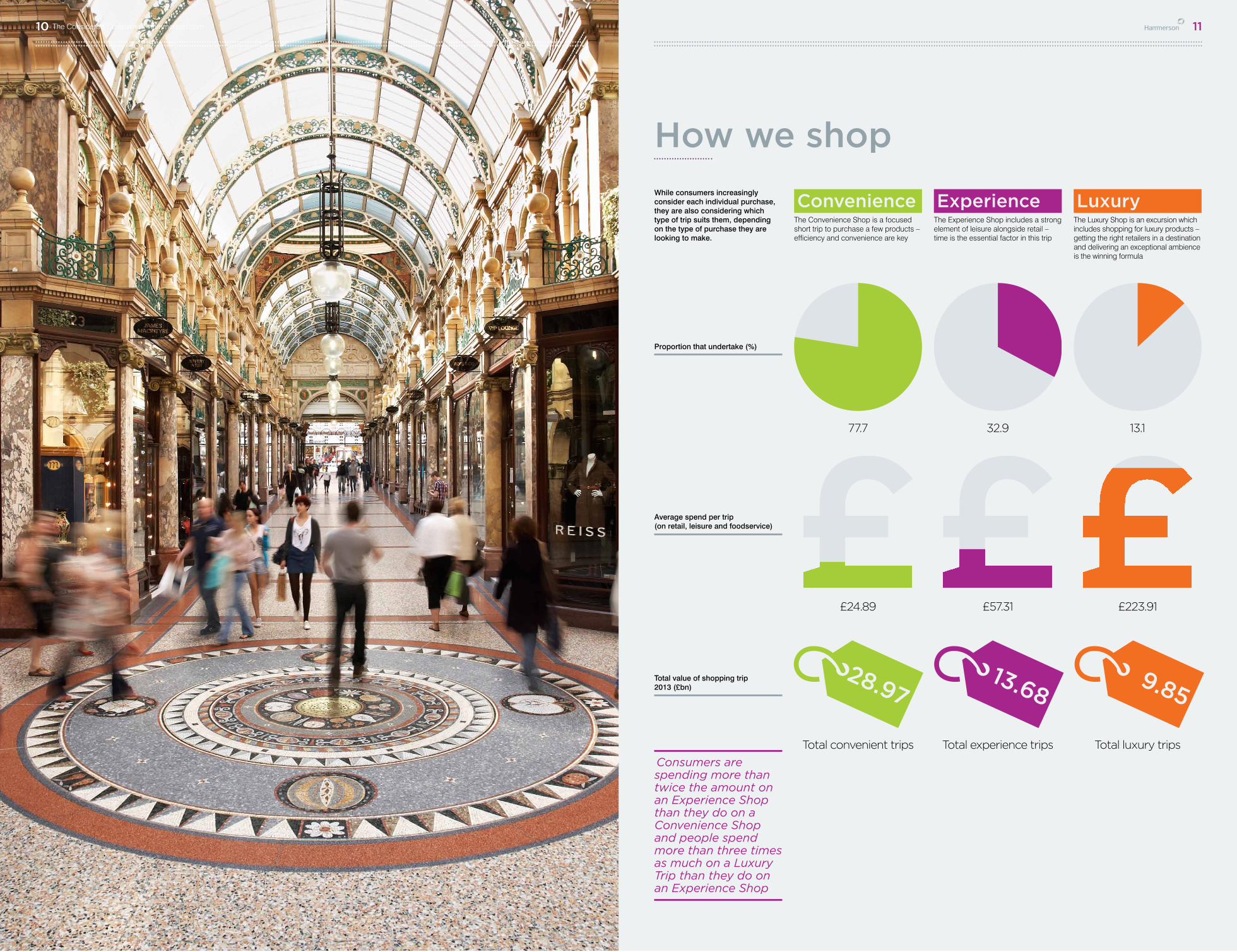

How we shop

While consumers increasingly consider each individual purchase, they are also considering which type of trip suits them, depending on the type of purchase they are looking to make.

The Convenience Shop is a focused short trip to purchase a few products – efficiency and convenience are key

The Experience Shop includes a strong element of leisure alongside retail – time is the essential factor in this trip

The Luxury Shop is an excursion which includes shopping for luxury products – getting the right retailers in a destination and delivering an exceptional ambience is the winning formula

Consumers are spending more than twice the amount on an Experience Shop than they do on a Convenience Shop and people spend more than three times as much on a Luxury Trip than they do on an Experience Shop

Convenience Experience Luxury

£24.89 £57.31 £223.91

77.7 32.9 13.1

Total convenient trips Total experience trips Total luxury trips

Proportion that undertake (%)

Average spend per trip (on retail, leisure and foodservice)

Total value of shopping trip 2013 (£bn)

28.9713.68

9.85

11The Considered Consumer | hammerson.com10

The convenient destinationTown centres, local high streets and retail parks are the most popular destinations for this type of shopping. Unsurprisingly convenience factors top the list of location drivers, however the right mix of retail is also a major factor in determining the right location for this type of shop.

The Convenience Shop

The convenience shop is evidence of the consumer holding more power than ever – they choose the price, they choose the time and they choose how they want to purchase.

The majority of consumers undertake a convenience trip at least every couple of weeks, with over a fifth doing so twice a week or more with the 25-34 year old age bracket spending the most (£31 per trip).

Icon shows frequency of undertaking convenient shopping trips in a year

Leisure offer6.2%

Ambience32.7%

Retail offer66.4%

Convenience84.1%

Click & collect - buying online and picking up

from a designate

Reserve online, buy in-store - reserving item(s)

online and pay instore

Click & collect (Collect+) - buying online and picking up from a collection point

At least a couple of times a week

Every one or two weeks

Every month or two

At most, once every six months

Less than once every six months

Fashion DIY & Gardening Homewares

Electricals Health & Beauty Entertainment

Furniture Stationery Jewellery

21.9% 42.9% 29.1% 1.1% 1.2%

41.7 %

37.7 %

8.6 %

Convenience of Click & CollectIn addition to retail parks’ traditional strengths, of convenience, accessibility and proximity to food stores, retailers’ growth of their multichannel offer combined with free parking are transforming retail parks into mini click & collect fulfilment centres. Nearly one in two women (47%) have used click & collect in the past year compared to 35% of men.

61.0% have used a click & collect service in the last 12 months

Location, location, locationAccessibility remains the key competitive advantage for retail parks, closely followed by savings on parking, as most fashion and retail parks are free. The change in focus of retail parks over the past five to ten years has also meant that consumers consider retail parks to be a pleasant environment to shop with the benefit of larger store sizes for a wider range of product and a handy mix of homeware and fashion. There is also a growing desire from consumers for catering, with restaurants and coffee shops becoming a growing part of the retail park mix.

Style, sandpaper and sandwichesRetail parks are growing in influence as a number of parks have shifted the majority of their focus from bulky goods and DIY to fashion. This is highlighted in which product categories consumers have used retail parks for with fashion coming out on top. With typical high street fashion retailers and department stores developing new formats for retail parks their appeal continues to grow.

Consumers are also expecting a more varied retail mix within their preferred retail park. 52.5% would like to see department stores, 50.2% expect a health and beauty specialist, with high street fashion retailers and everyday family restaurants both high up on the list at 43.7% and 40.1% respectively. Unsurprisingly, both homeware (50.2%) and DIY retailers (48.5%) continue to feature on the ideal retail park line up.

62.4% have used a retail park in the last 12 months

Icons show the proportion of consumers that have shopped at retail parks for different retail categories

34.2%

17.7%

9.0%

21.3%22.1%

11.8%

7.2%

11.6%

2.6%

13The Considered Consumer | hammerson.com12

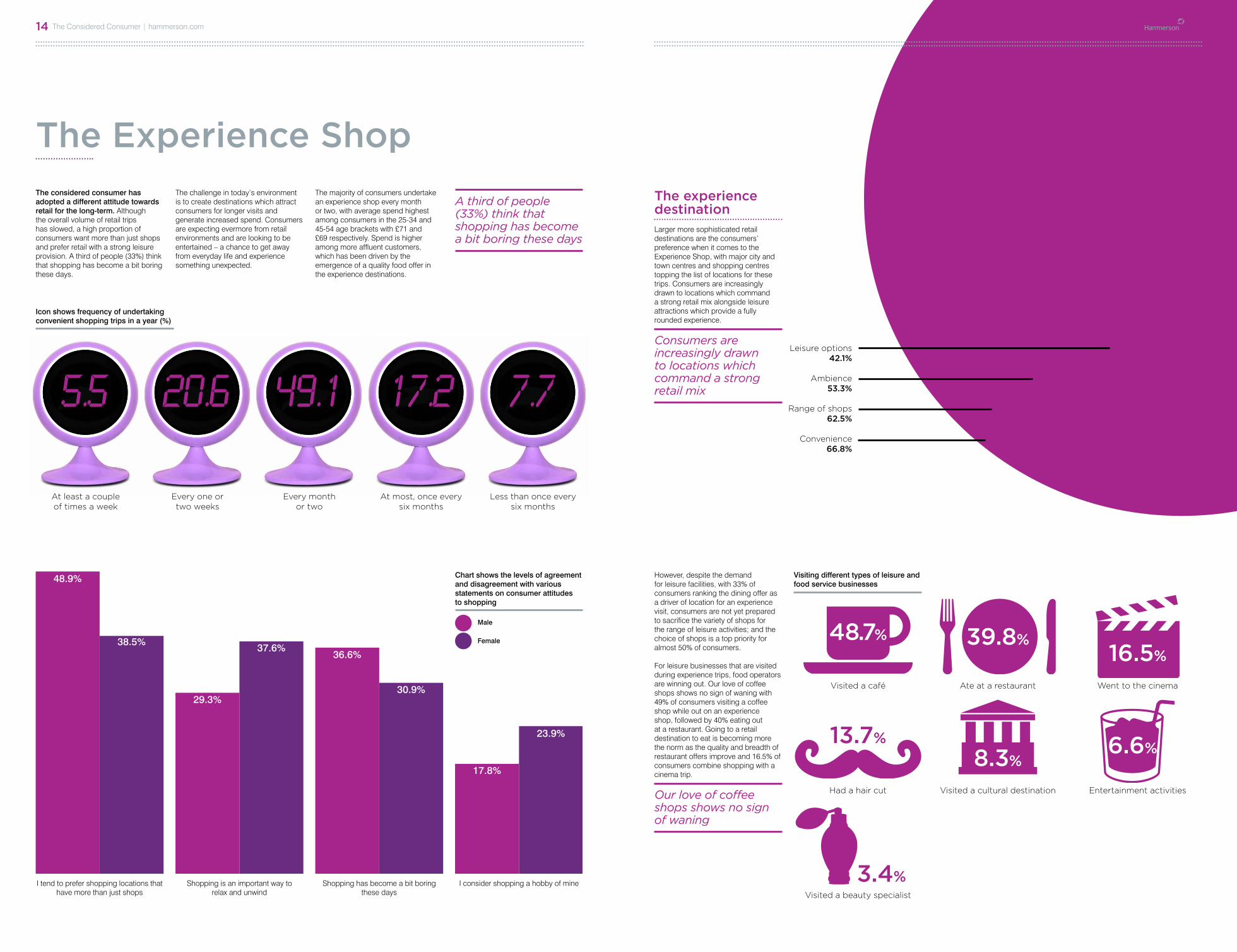

The Experience Shop

The considered consumer has adopted a different attitude towards retail for the long-term. Although the overall volume of retail trips has slowed, a high proportion of consumers want more than just shops and prefer retail with a strong leisure provision. A third of people (33%) think that shopping has become a bit boring these days.

The challenge in today’s environment is to create destinations which attract consumers for longer visits and generate increased spend. Consumers are expecting evermore from retail environments and are looking to be entertained – a chance to get away from everyday life and experience something unexpected.

The majority of consumers undertake an experience shop every month or two, with average spend highest among consumers in the 25-34 and 45-54 age brackets with £71 and £69 respectively. Spend is higher among more affluent customers, which has been driven by the emergence of a quality food offer in the experience destinations.

A third of people (33%) think that shopping has become a bit boring these days

The experience destinationLarger more sophisticated retail destinations are the consumers’ preference when it comes to the Experience Shop, with major city and town centres and shopping centres topping the list of locations for these trips. Consumers are increasingly drawn to locations which command a strong retail mix alongside leisure attractions which provide a fully rounded experience.

Consumers are increasingly drawn to locations which command a strong retail mix

However, despite the demand for leisure facilities, with 33% of consumers ranking the dining offer as a driver of location for an experience visit, consumers are not yet prepared to sacrifice the variety of shops for the range of leisure activities; and the choice of shops is a top priority for almost 50% of consumers.

For leisure businesses that are visited during experience trips, food operators are winning out. Our love of coffee shops shows no sign of waning with 49% of consumers visiting a coffee shop while out on an experience shop, followed by 40% eating out at a restaurant. Going to a retail destination to eat is becoming more the norm as the quality and breadth of restaurant offers improve and 16.5% of consumers combine shopping with a cinema trip.

Our love of coffee shops shows no sign of waning

Icon shows frequency of undertaking convenient shopping trips in a year (%)

Visited a café Ate at a restaurant Went to the cinema

Had a hair cut Visited a cultural destination Entertainment activities

Visited a beauty specialist

48.7%

13.7%

3.4%

16.5%39.8%

8.3%6.6%

Leisure options42.1%

Ambience53.3%

Range of shops62.5%

Convenience66.8%

Visiting different types of leisure and food service businesses

Chart shows the levels of agreement and disagreement with various statements on consumer attitudes to shopping

At least a couple of times a week

Every one or two weeks

Every month or two

At most, once every six months

Less than once every six months

5.5 20.6 49.1 17.2 7.7

I tend to prefer shopping locations that have more than just shops

Shopping is an important way to relax and unwind

Shopping has become a bit boring these days

I consider shopping a hobby of mine

48.9%

38.5%

29.3%

37.6%36.6%

30.9%

17.8%

23.9%

Male

Female

The Considered Consumer | hammerson.com14 15

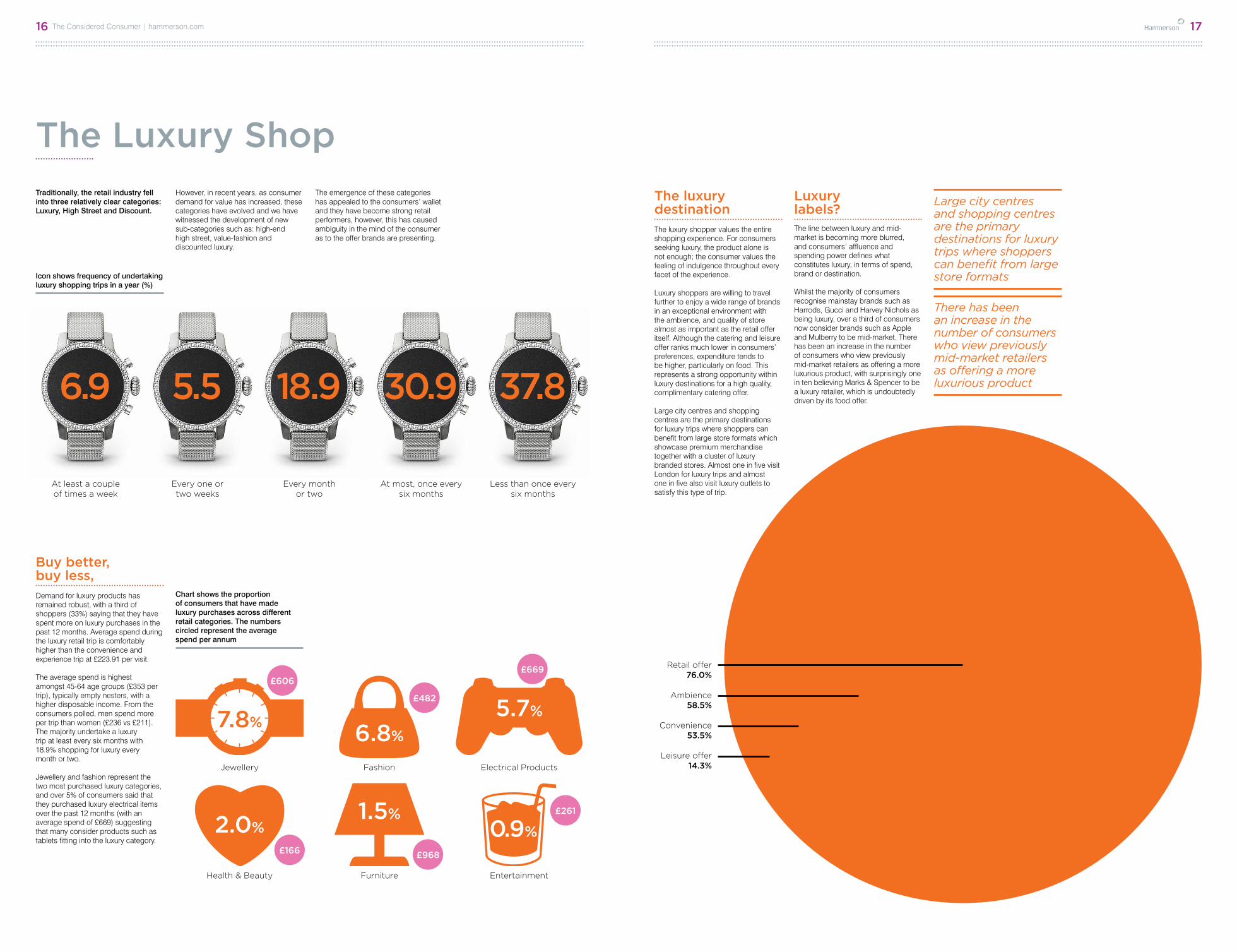

Buy better, buy less, Demand for luxury products has remained robust, with a third of shoppers (33%) saying that they have spent more on luxury purchases in the past 12 months. Average spend during the luxury retail trip is comfortably higher than the convenience and experience trip at £223.91 per visit.

The average spend is highest amongst 45-64 age groups (£353 per trip), typically empty nesters, with a higher disposable income. From the consumers polled, men spend more per trip than women (£236 vs £211). The majority undertake a luxury trip at least every six months with 18.9% shopping for luxury every month or two. Jewellery and fashion represent the two most purchased luxury categories, and over 5% of consumers said that they purchased luxury electrical items over the past 12 months (with an average spend of £669) suggesting that many consider products such as tablets fitting into the luxury category.

The luxury destination The luxury shopper values the entire shopping experience. For consumers seeking luxury, the product alone is not enough; the consumer values the feeling of indulgence throughout every facet of the experience.

Luxury shoppers are willing to travel further to enjoy a wide range of brands in an exceptional environment with the ambience, and quality of store almost as important as the retail offer itself. Although the catering and leisure offer ranks much lower in consumers’ preferences, expenditure tends to be higher, particularly on food. This represents a strong opportunity within luxury destinations for a high quality, complimentary catering offer. Large city centres and shopping centres are the primary destinations for luxury trips where shoppers can benefit from large store formats which showcase premium merchandise together with a cluster of luxury branded stores. Almost one in five visit London for luxury trips and almost one in five also visit luxury outlets to satisfy this type of trip.

Luxury labels?The line between luxury and mid-market is becoming more blurred, and consumers’ affluence and spending power defines what constitutes luxury, in terms of spend, brand or destination.

Whilst the majority of consumers recognise mainstay brands such as Harrods, Gucci and Harvey Nichols as being luxury, over a third of consumers now consider brands such as Apple and Mulberry to be mid-market. There has been an increase in the number of consumers who view previously mid-market retailers as offering a more luxurious product, with surprisingly one in ten believing Marks & Spencer to be a luxury retailer, which is undoubtedly driven by its food offer.

Large city centres and shopping centres are the primary destinations for luxury trips where shoppers can benefit from large store formats

There has been an increase in the number of consumers who view previously mid-market retailers as offering a more luxurious product

The Luxury Shop

Traditionally, the retail industry fell into three relatively clear categories: Luxury, High Street and Discount.

However, in recent years, as consumer demand for value has increased, these categories have evolved and we have witnessed the development of new sub-categories such as: high-end high street, value-fashion and discounted luxury.

The emergence of these categories has appealed to the consumers’ wallet and they have become strong retail performers, however, this has caused ambiguity in the mind of the consumer as to the offer brands are presenting.

At least a couple of times a week

Every one or two weeks

Every month or two

At most, once every six months

Less than once every six months

Icon shows frequency of undertaking luxury shopping trips in a year (%)

6.9 5.5 18.9 30.9 37.8

Chart shows the proportion of consumers that have made luxury purchases across different retail categories. The numbers circled represent the average spend per annum

£482

£669

£166

£261

Retail offer76.0%

Ambience58.5%

Convenience53.5%

Leisure offer14.3%Jewellery Fashion Electrical Products

Health & Beauty Furniture Entertainment

7.8%

2.0%

5.7%

6.8%

1.5%0.9%

£606

£968

17The Considered Consumer | hammerson.com16

Conclusion

Considered Consumption is here to stay and although this new consumer mindset is subtly different it has a significant impact on how people are buying and how brands and retail destinations evolve in this era. It’s a more modest form of buying; much more about perceptions of value than about price, which has come at the expense of impulse buying. The old consumer mindset is behind us and the new one needs attention in order to thrive in today’s retail environment.

Despite the focus on planned purchases, retail has become more complex

Discounting which became prevalent during the onset of the recession is losing its impact, however the knock-on effect is that the Considered Consumer increasingly expects to purchase less at full price while being happy to spend more when trading up for a more premium product.

Despite the focus on planned purchases, retail has become more complex. Surprisingly, technology has slowed the purchasing process down, as online and mobile make researching products accessible from everywhere. The average shopper has nearly doubled the number of stores they use on a regular basis as competition on the high street grows and the variety of channels available to purchase from means retail is a truly 24/7 experience, which requires meticulous consistency of quality and service from retailers.

Across the three types of shopping, it is clear that retail and leisure are becoming more heavily intertwined. Consumers are looking for more than just shops and this growing appetite from shoppers for an outstanding retail trip has driven Hammerson to develop its Product of the Future programme.

Still in its infancy, the initiative brings together the physical and the digital to enable exceptional retail experiences, which will create a blueprint of what a successful retail destination should encompass, now and in the future.

The fundamentals to this approach are:

• Developing iconic destinations• Being the best partner for

our retailers

• Offering facilities and services that exceed expectations

• Creating engaging and sociable spaces

• Pushing the boundaries of what a retail space can be to entertain and excite

The average shopper has nearly doubled the number of stores they use on a regular basis

The Considered Consumer Report has highlighted the ever increasing expectations from shoppers and the need for all destinations to offer more than just a simple row of shops. To continue to succeed we need to focus on ensuring that our existing centres and forthcoming developments surpass the expected benchmark set by today’s Considered Consumer.

Report methodologyConsumer Research in this report is based on a UK-nationally representative survey of 2,000 shoppers. All numbers relating to expenditure and forecast expenditure are taken from Conlumino’s own retail model. This is updated on an ongoing basis with inputs from official sources (such as the BRC and ONS), retailers’ results and trading updates, industry sources and other secondary sources. Unless otherwise stated all sources are derived from Conlumino’s and Hammerson’s own research and should be referenced to Hammerson/Conlumino.

QuantityI consider shopping as a hobby and I tend to buy lots of things; some of which I probably don’t need

QualityI tend to only buy things that I really want

Price-drivenLow prices are a strong purchase driver for me

Value-drivenSo many retailers are discounting all the time. I don’t mind paying more for better quality things

LoyalI typically shop at a handful of trusted retailers that are convenient for me to travel to

PromiscuousI look to shop around for the best value. Online shopping means that I now use shops that I didn’t even consider before

LocalThe local high street/town centre is my preferred retail location

multichannelI shop across different retail channels and locations depending on the type of trip

impulse-drivenI often like to browse the shops to research what I might like and buy it there and then

Research-drivenI find it more convenient to browse products and compare ranges and prices online before purchasing

The old mindset The new mindset

The Considered Consumer | hammerson.com18

designed and produced by apecreative.com

www.hammerson.com +44 (0) 20 7887 [email protected]

10 Grosvenor Street,London, W1K 4BJRegistered in England & Wales: 00360632

Printed on recycled paper