IBM Institute for Business Value The contact center of the future: Spanning the chasms In telecommunications (telecom) markets around the world, service providers are looking for options to manage their way through the current downturn. Many carriers amassed a significant amount of debt to build out their network capacity in the late 1990s, and many of these networks remain underutilized because anticipated new service markets failed to materialize. Now, carriers are generating insufficient revenues to service their debt and are consequently facing debt defaults and bankruptcy. By Darryl C. Sterling, Doug Van Wingerden and Joseph Jorczak

Transcript

IBM Institute for Business Value

The contact center of the future: Spanning the chasms

In telecommunications (telecom) markets around the world, service providers are looking for options to manage their way through the current downturn. Many carriers amassed a significant amount of debt to build out their network capacity in the late 1990s, and many of these networks remain underutilized because anticipated new service markets failed to materialize. Now, carriers are generating insufficient revenues to service their debt and are consequently facing debt defaults and bankruptcy.

By Darryl C. Sterling, Doug Van Wingerden and Joseph Jorczak

Future contact center IBM Institute for Business Value1

Future contact center

Contents

1 Introduction

2 Customer-related market downturn

3 The importance of the contact center

5 Trends driving the contact center transformation

8 What is the contact center of the future going to look like?

10 Crossing the contact center chasms

12 Conclusion

13 About the authors

14 References

Introduction

Telecom service providers need to create new business models that permit the seamless rollout of multiple revenue-generating services with less risk, for less cost and in less time. The chal-lenge is that the current contact center operating model does not scale easily or quickly to support the launch of many new services. For this reason, how contact centers evolve to sup-port the next phase of service provider growth is extremely important to how successfully they emerge from the current market downturn.

IBM Business Consulting Services and the IBM Institute for Business Value research and analysis suggests that contact centers in today’s telecom business will follow a natural progres-sion of transformation, which will be critical as telecom service providers seek to transform and revolutionize their businesses. IBM Business Consulting Services and the IBM Institute for Business Value have identified three phases of contact center transformation characterized by key business decisions that create the blueprint for the next-generation telecom service providers (see Figure 1).

Figure 1. The three phases of contact center transformation.

Source: IBM Business Consulting Services analysis and IBM Institute for Business Value analysis.

Phase 1 Phase 2 Phase 3

Enhanced product- focused care

Enterprise-focused care

Inter-enterprise- focused care

Grab “low-hanging fruit” exposed by new technologies

Leverage a hub-and-spoke, enterprise contact center model

Busi

ness

val

ue c

hasm

Support advanced service offerings by linking care operations to business partners

Busi

ness

rule

s ch

asm

Future contact center IBM Institute for Business Value2

Future contact center

Customer-related market downturn

In the past few years, the global telecom industry has undergone the most pronounced “boom and bust” cycle in its history. In early 2000, the market capitalization of the top 39 global car-riers was at its height totaling US$2.9 trillion.1 However, as the U.S. economy declined along with other world markets, the telecom industry suffered severe declines in earnings and its market capitalization was reduced to US$1.4 trillion,2 less than half of its peak value. This dra-matic reversal of fortunes has left many carriers struggling to survive.

Many factors contributed to the global telecom business downturn, but one of the greatest challenges that telecom carriers have faced is finding new revenues to offset the debt incurred from adding capacity and upgrading their networks. Not coincidentally, there are also a number of customer-related issues associated with this revenue problem:

• Many of the core telecom services, such as fixed-line voice and mobile subscriptions, are approaching or have reached customer saturation points

• The increase in the number of competitors has unleashed market forces that have commod-itized the value of core telecom services to customers

• The availability of alternative telecom services from these competitors has created incentives for customers to substitute core telecom services for new services

• Many of the new services introduced into the market (for example, digital subscriber line [DSL] and mobile data/wireless Internet access) have not achieved the expected critical mass of consumer penetration (with the exceptions of Japan and Korea).

These factors have created two difficult market conditions for telecom service providers to manage. First, the portion of consumer money spent on telecom services in the pre-boom era is now being allocated over a broader array of services and a larger number of providers. Second, the cost of acquiring new customers continues to rise, making it more difficult for carriers to break even and create profitable customers over time. Under these circum-stances, there is a heightened emphasis on retaining customers and increasing the earnings per customer.

Future contact center IBM Institute for Business Value3

Future contact center

Meanwhile, customer satisfaction levels for core wireline telecom services have been declining steadily over the past few years, resulting in higher churn rates. While churn has long been a critical issue for long-distance, mobile and Internet service providers, it is now also becoming a growing challenge for wireline voice providers as they face new types of competition. For the first time in many markets, the number of fixed voice lines is beginning to decline and viable competitors are starting to take away customers for the remaining lines.

The importance of the contact center

Customer service has become a critical component of differentiation for service providers as they recognize that improving customer loyalty, retaining customers and increasing revenues per customer are paramount to long-term success. As a result, telecom service providers have a tremendous amount at stake in regard to how they leverage their contact centers to create future value for the business. There are several reasons why contact center operations are drawing senior management attention today:

• The contact center is the primary touch point with the customer—Of the few primary cus-tomer touch points that exist (including sales and marketing), the contact center has the most direct and on-going contact with customers. Therefore, it is one of the most important tools that service providers have to sway customer loyalty to their favor.

• Contact centers are a revenue-generating mechanism—In the past, service providers had limited opportunities to leverage contact center functions to achieve corporate goals. However, advances in technology, including customer relationship management (CRM), have created new opportunities to transform the contact center into a more-efficient revenue-generating entity.

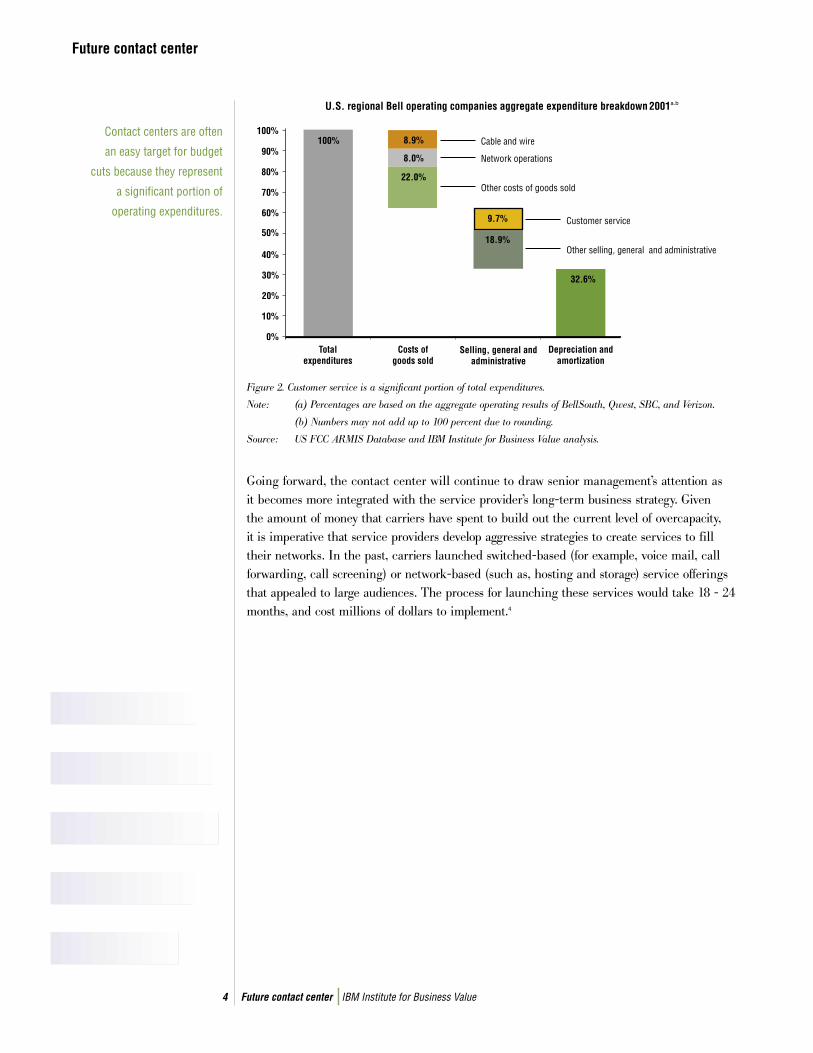

• Contact centers can reduce overall operating expenses—Historically, the contact center has been a high-cost operation—typically 8 to 12 percent of expenditures3 (see Figure 2). The downturn of the telecom market has placed increased pressure on service providers to reduce operating costs. Service providers must continue to look for effective ways of lowering their contact center costs while simultaneously improving customer loyalty and increasing revenues.

Future contact center IBM Institute for Business Value4

Future contact center

Figure 2. Customer service is a significant portion of total expenditures.

Note: (a) Percentages are based on the aggregate operating results of BellSouth, Qwest, SBC, and Verizon.

(b) Numbers may not add up to 100 percent due to rounding.

Source: US FCC ARMIS Database and IBM Institute for Business Value analysis.

Going forward, the contact center will continue to draw senior management’s attention as it becomes more integrated with the service provider’s long-term business strategy. Given the amount of money that carriers have spent to build out the current level of overcapacity, it is imperative that service providers develop aggressive strategies to create services to fill their networks. In the past, carriers launched switched-based (for example, voice mail, call forwarding, call screening) or network-based (such as, hosting and storage) service offerings that appealed to large audiences. The process for launching these services would take 18 - 24 months, and cost millions of dollars to implement.4

60%

50%

40%

30%

20%

10%

0%

U.S. regional Bell operating companies aggregate expenditure breakdown 2001a.b

70%

100%

80%

90%

100%

Total expenditures

Costs of goods sold

Selling, general and administrative

Depreciation and amortization

8.9%

8.0%

22.0%

32.6%

18.9%

Cable and wire

Network operations

Other costs of goods sold

Customer service

Other selling, general and administrative

9.7%

Contact centers are often

an easy target for budget

cuts because they represent

a significant portion of

operating expenditures.

Future contact center IBM Institute for Business Value5

Future contact center

Today, service providers need lower-cost and lower-risk options to launch services that cater to a broad audience or can be targeted at smaller, niche markets. The business architecture of the contact center operation will be a critical component of this new strategy from two per-spectives. First, the contact center will need to support a greater number of customers using a more diverse portfolio of services. Second, a well-run contact center—with the ability to collect customer information about how people really use applications and services—will be an immensely powerful and competitive tool for service providers to achieve their long-term business objectives.

Trends driving the contact center transformation

Whereas traditional contact centers focus on cost-effectively and efficiently completing transac-tions and resolving customer inquiries, the contact center of the future will provide critical corporate-level strategic advantage by generating business intelligence, reducing operating costs, and enabling a flexible and scalable customer support operation. Three macro-trends underpin the vision for the transformation of the contact center of the future: technology advances, business model flexibility and non-core business function outsourcing.

Technology advancesThe way that contact center technologies are networked together will have a greater and greater impact on how the contact center operation can be transformed. Many of the core technologies for the contact center, including public branch exchanges (PBXs), automated call distribution (ACD), computer telephony integration (CTI) and interactive voice response (IVR), are very mature. Although there have been incremental improvements in these technologies over the years, there has been little reason to change the contact center business model around these individual technologies. Implemented individually, these technologies drive incremental improvements. Implemented holistically, these technologies, combined with business process reengineering, can drive evolutionary—perhaps revolutionary—change in the telecom marketplace.

Three macro-trends

underpin the vision for the

transformation of the contact

center of the future: technology

advances, business model

flexibility and non-core

business function outsourcing.

Increased product

complexity is driving up the

number of contact center

incidents and total talk time.

Future contact center IBM Institute for Business Value6

Future contact center

Three additional technologies can potentially change the business models of the contact center: network-based routing, universal queuing and Voice over Internet Protocol (VoIP).

• Network-based routing—Although carriers are in the business of building and operating wide area networks (WANs), they have failed to leverage this expertise in their own enterprise networks for contact centers. Network-based routing is a vision for creating a centralized contact center architecture where the core technologies (for example, ACD, CTI and IVR) are removed from individual contact centers and placed on a WAN. After these technologies have been centralized, each contact center then accesses those technology functions through the network, creating a hub-and-spoke architecture. Technologically speaking, enterprise-based routing does not outwardly create any significant advantages. However, it does provide operating advantages because it allows a series of contact centers to interoperate and work in concert, creating economies of scale and increasing overall labor productivity.

• Universal queuing—This is a technology that allows all customer requests coming in from multiple channels to be aggregated into one universal queue for a contact center. The value of universal queuing is not as clear at the individual contact center level as it is at the enter-prise contact center architecture level. When a group of contact centers are networked, universal queuing actually creates opportunities for telecom service providers to establish enterprise-level business rules for managing customer service throughout the web of contact centers. In combination with networking, universal queuing goes a long way in making a telecom service provider’s customer service faster, as well as more accurate and consistent. In addition, it also provides carriers with opportunities to allocate labor resources better to dif-ferent types of customer service transactions.

• Voice over IP (VoIP)—Although not yet widely used today, VoIP or IP telephony, the two-way transmission of audio over a packet-switched IP network, is expected to have a sig-nificant impact on contact center operations. The biggest benefit for the contact center will be the savings in long-distance and local phone charges associated with enterprise-based network costs. In addition, VoIP can improve the performance of contact center agents because of the integration of voice and data technology solutions over an IP network. The general consensus is that VoIP is not ready for extensive deployment because of problems with IP voice call latency and call quality. But, as the technology matures in the near future, it will become a better solution for contact centers to integrate into their technology architecture.

Evolutionary technology

advances can bring about

revolutionary business

change if the technologies

are organized in the right

way and combined with

new business processes.

Future contact center IBM Institute for Business Value7

Future contact center

Business model flexibilityAs the global telecom industry slowly returns to profitability and moderate—but positive—growth, many industry executives believe that the business will go through a period of service provider consolidation, accompanied, or closely followed, by a business model transformation. As competitors merge, consolidate multiple contact centers, grow the business, sell off non-core assets, and create new business partnerships and business models, they will require the architectural flexibility to integrate or divest parts of the contact center operation quickly and efficiently. Therefore, an enterprise-based contact center architecture provides the business model flexibility required for this future.

Non-core business function outsourcingGiven today’s business climate, outsourcing is an option that is being explored by more and more service providers. For some service providers, outsourcing has such a material impact on the business that they consider outsourcing the entire customer care function. Other ser-vices providers who may not have thought that outsourcing was a viable business option are now considering outsourcing non-core or fringe functions of customer care that tend to be high-cost or can be outsourced easily to third-party service providers at a much lower cost. One example is when a telecom service provider outsources a non-core function to an offshore location with lower labor costs. Another example is a service provider outsourcing contact center functions that require specialty skills that are expensive and difficult to find. Likewise, there are opportunities to leverage the enterprise contact center architecture to outsource cus-tomer service functions when there are high and low transaction activity thresholds, or when certain types of intensive contact center campaigns are conducted over a short period of time.

Consolidation has become

a part of a much larger

transformational strategy.

Future contact center IBM Institute for Business Value8

Future contact center

What is the contact center of the future going to look like?

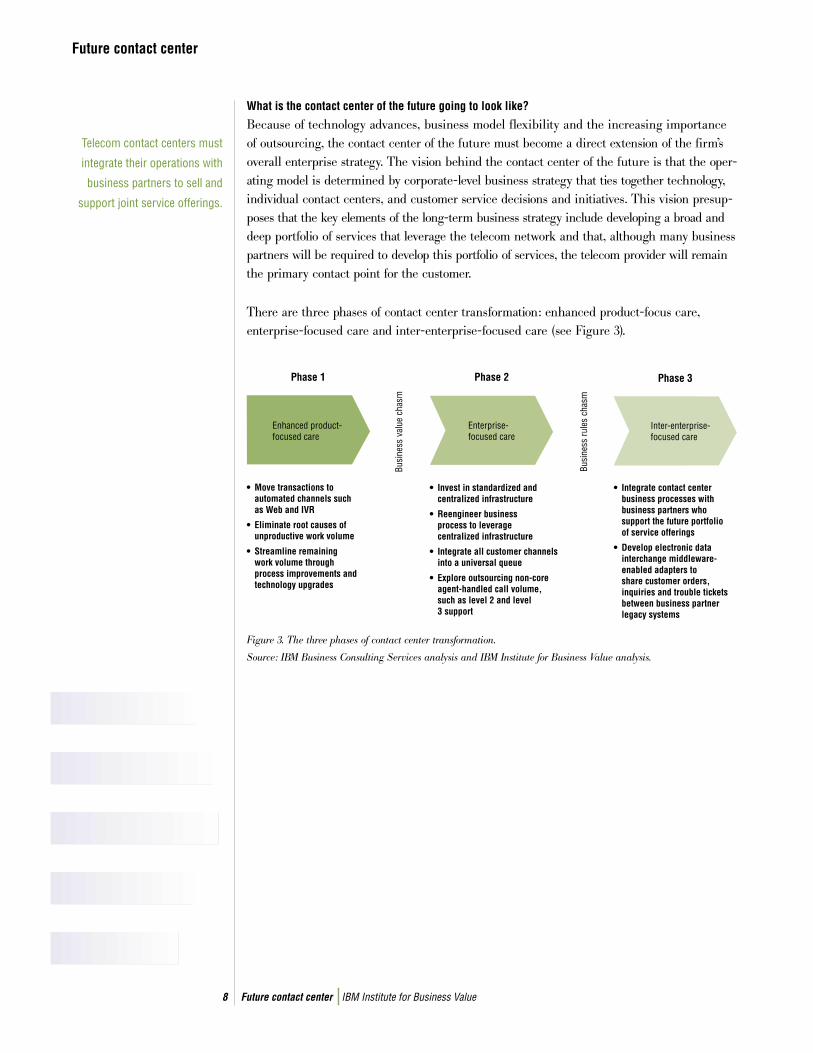

Because of technology advances, business model flexibility and the increasing importance of outsourcing, the contact center of the future must become a direct extension of the firm’s overall enterprise strategy. The vision behind the contact center of the future is that the oper-ating model is determined by corporate-level business strategy that ties together technology, individual contact centers, and customer service decisions and initiatives. This vision presup-poses that the key elements of the long-term business strategy include developing a broad and deep portfolio of services that leverage the telecom network and that, although many business partners will be required to develop this portfolio of services, the telecom provider will remain the primary contact point for the customer.

There are three phases of contact center transformation: enhanced product-focus care, enterprise-focused care and inter-enterprise-focused care (see Figure 3).

Figure 3. The three phases of contact center transformation.

Source: IBM Business Consulting Services analysis and IBM Institute for Business Value analysis.

Phase 1 Phase 2 Phase 3

Enhanced product-focused care

Enterprise-focused care

Inter-enterprise-focused care

• Move transactions to automated channels such as Web and IVR

• Eliminate root causes of unproductive work volume

• Streamline remaining work volume through process improvements and technology upgrades

• Invest in standardized and centralized infrastructure

• Reengineer business process to leverage centralized infrastructure

• Integrate all customer channels into a universal queue

• Explore outsourcing non-core agent-handled call volume, such as level 2 and level 3 support

Busi

ness

val

ue c

hasm

• Integrate contact center business processes with business partners who support the future portfolio of service offerings

• Develop electronic data interchange middleware- enabled adapters to share customer orders, inquiries and trouble tickets between business partner legacy systems

Busi

ness

rule

s ch

asm

Telecom contact centers must

integrate their operations with

business partners to sell and

support joint service offerings.

Future contact center IBM Institute for Business Value9

Future contact center

Enhanced product-focused careBecause most contact centers are focused on supporting specific products and services, the goal of phase one is to enhance the contact center’s ability to perform these functions. Phase one requires the execution of three strategies that produce operational enhancements in the contact center while reducing the financial investment. The first strategy is the automation of customer transactions over the Internet and the IVR. This strategy will be executed by leveraging improvements in technologies, such as speech recognition, natural language, text-to-speech, intelligent scripting and real-time personalization. The second strategy is to identify and eliminate the root causes of unproductive work volume (for example, repeat calls, transfers, unnecessary customer inquiries). This requires a systematic approach to collect-ing key business metrics and benchmarking performance, and conducting business process mapping to determine weaknesses in the workflow. The third strategy is to increase the effectiveness and efficiency of the remaining work volume. This strategy will be executed by leveraging improvements in technologies such as work force management, work flow and knowledge management.

Enterprise-focused careAfter the contact center has captured the value of operation and process improvements, attention needs to be turned to implementing the technology that can deliver customer care to any customer transparently across a network of contact centers. Phase two requires the creation of an enterprise contact center architecture that calls for a significant amount of investment in new technologies and the reorganization and reengineering of internal business processes to support these technologies. The goal of this phase is to create an enterprise view of contact center operations. Once created, this web of interoperable contact centers can work together to optimize customer service functions at the corporate level rather than at the line of business level. The contact center will be integrated with the larger CRM strategy and other business processes. A universal queuing model should also be established to create a blended multichannel customer service architecture that can optimize labor productivity through the intelligent routing of customer service transactions to the best-qualified and available cus-tomer service agents.

Future contact center IBM Institute for Business Value10

Future contact center

Inter-enterprise-focused carePhase three extends the capabilities of the contact center beyond their traditional boundaries within the telecom service provider. The main goal of extending the capabilities of the contact center beyond the organization is to create a more flexible system to integrate contact center business processes with multiple business partners. Here, the contact center becomes a key component of a service provider’s ability to transform the telecom business model by providing seamless customer service for telecom services that are bundled with business partner products and services. A critical success factor to this stage, however, is the development of strict and standardized business rules that facilitate the sharing of customer orders, inquiries and trouble tickets between business partner legacy systems. The vision in this phase is that the stan-dardization of these business rules will have the same impact on the telecom business as the introduction of electronic data interchange (EDI) had on the revolutionizing the supply chain.

Crossing the contact center chasms

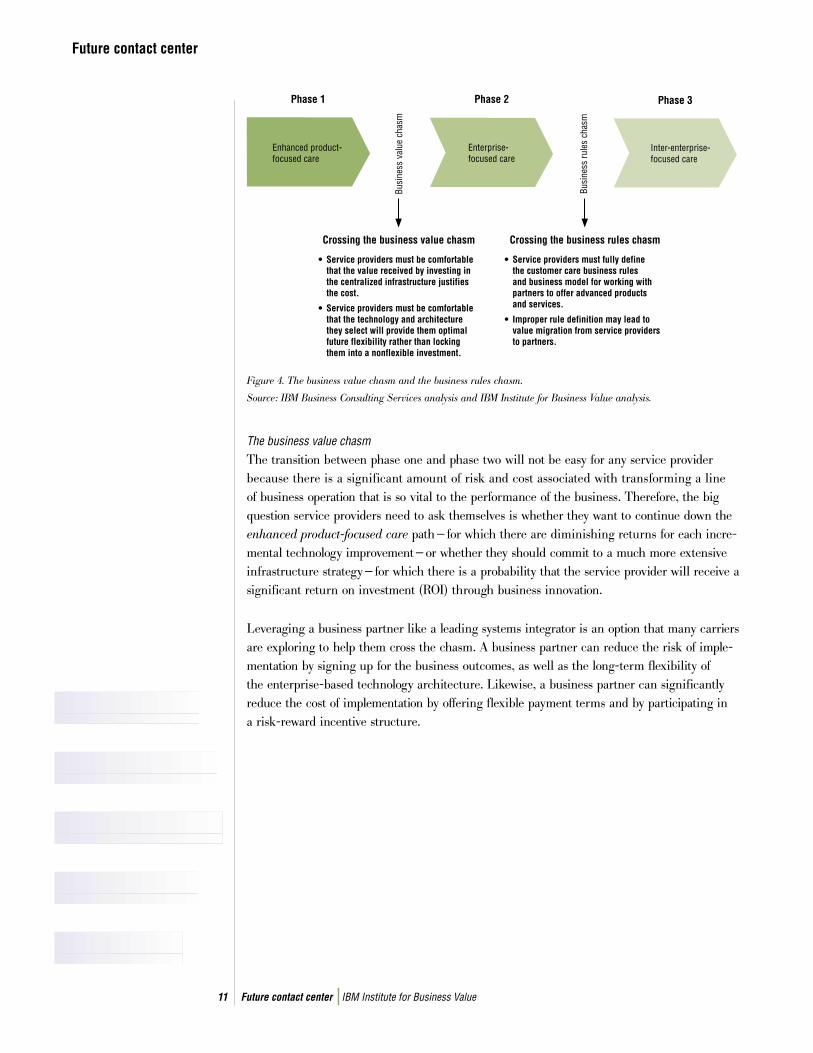

As service providers transform their customer care operations from one phase to another, they will encounter significant and systemic barriers to change. In fact, it is not enough to under-stand the benefits of moving from one phase to another. Service providers must understand the “chasms” that exist between each phase of the transformation. Chasms represent the com-plexities and challenges that need to be addressed by telecom service providers as they move through each phase of contact center transformation and as they balance the risk-reward in moving from one phase to another. Telecom service providers face two chasms in the natural progression to the contact center transformation: the business value chasm and the business rules chasm (see Figure 4).

Telecom service providers

face two chasms in the natural

progression to the contact center

transformation: the business

value chasm and the business

rules chasm.

Future contact center IBM Institute for Business Value11

Future contact center

Figure 4. The business value chasm and the business rules chasm.

Source: IBM Business Consulting Services analysis and IBM Institute for Business Value analysis.

The business value chasmThe transition between phase one and phase two will not be easy for any service provider because there is a significant amount of risk and cost associated with transforming a line of business operation that is so vital to the performance of the business. Therefore, the big question service providers need to ask themselves is whether they want to continue down the enhanced product-focused care path—for which there are diminishing returns for each incre-mental technology improvement—or whether they should commit to a much more extensive infrastructure strategy—for which there is a probability that the service provider will receive a significant return on investment (ROI) through business innovation.

Leveraging a business partner like a leading systems integrator is an option that many carriers are exploring to help them cross the chasm. A business partner can reduce the risk of imple-mentation by signing up for the business outcomes, as well as the long-term flexibility of the enterprise-based technology architecture. Likewise, a business partner can significantly reduce the cost of implementation by offering flexible payment terms and by participating in a risk-reward incentive structure.

Phase 1 Phase 2 Phase 3

Enhanced product-focused care

Enterprise-focused care

Inter-enterprise-focused care

Crossing the business value chasm

• Service providers must be comfortable that the value received by investing in the centralized infrastructure justifies the cost.

• Service providers must be comfortable that the technology and architecture they select will provide them optimal future flexibility rather than locking them into a nonflexible investment.

Busi

ness

val

ue c

hasm

Busi

ness

rule

s ch

asm

Crossing the business rules chasm

• Service providers must fully define the customer care business rules and business model for working with partners to offer advanced products and services.

• Improper rule definition may lead to value migration from service providers to partners.

Future contact center IBM Institute for Business Value12

Future contact center

The business rules chasmWhereas the business value chasm exists because of the significant costs and risks associated with the enterprise infrastructure implementation, the business rules chasm exists because of the inherent risks and advantages of interconnecting internal business operations with exter-nal business partners. An excellent analogy is to take a look at the early stages of e-business as it relates to the supply chain. The business benefits are easy to see, yet the implications of integrating an extranet or ecosystem of business partners without contemplating value migra-tion are significant. Seamless customer service will be a competitive differentiator. Customers do not want one 1-800 number for connectivity and service issues, another for hardware tech-nical support, another for software technical support, and so on. They will expect to call one support center for all their needs. Carriers need to establish business rules to ensure that their customers view them as the primary service provider, rather than a commodity connectivity provider. Carriers must also move quickly to establish business rules to determine how part-ners will link with their systems, rather than waiting for each partner to dictate how a carrier will link to them.

Conclusion

As telecom service providers expand their business model to offer a wide range of products and services, seamless customer care will be a short-term competitive differentiator and long-term competitive necessity. The journey to seamless customer care will not be easy, short or inexpensive. In addition, service providers can expect pressure for short-term financial and operating improvements along the way. As such, service providers must maintain a proper balance of short- and long-term investment decisions during the transformation. To achieve this balance, service providers must have a clear vision of the contact center of the future and its strategic importance to its business strategy. Moreover, service providers must also under-stand the steps to realize their vision and the natural barriers to the transformation. Not every telecom service provider will have the vision and fortitude to transform completely—and they will eventually pay a heavy price for this in the marketplace. Successful service providers will incorporate the contact center in their long-term business strategy, possess a clear end-state vision for the call center operation, and develop an achievable and executable transformation roadmap enabling them to rise above the competition and simultaneously deliver superior cus-tomer care and business results.

To discuss how we can help you plan for, and build a contact center for the future, please contact us at [email protected]. To browse other resources for business executives, we invite you to visit our Web site at:

ibm.com/services/strategy

Future contact center IBM Institute for Business Value13

Future contact center

About the authors

Darryl C. Sterling is an Industry Strategist in the Communications Sector for the IBM Institute for Business Value. His primary roles are to develop intellectual capital, analysis and thought leadership for both external clients and internal IBM constituents, primarily within the telecom and media industries. He is also responsible for evaluating technologies and their roles in creating and transforming business models. You can contact Darryl at [email protected].

Doug Van Wingerden is a Principal with IBM Business Consulting Services, part of IBM Global Services. He focuses on the telecom industry and his areas of specialty are customer relationship management (CRM) and e-business strategy. He is the offering leader and sub-ject-matter expert for the IBM CRM ASAP (Transformational Outsourcing) offering. He is also an original architect of the IBM e-business strategy consulting methodology. You can contact Doug at [email protected].

Joe Jorczak is a Senior Consultant with IBM Business Consulting Services, part of IBM Global Services. He focuses on the telecom industry and his areas of specialty are customer relationship management (CRM), process optimization and knowledge management. He develops e-business strategies and helps service providers transform their business to implement next-generation services and capabilities. He also helped to create the IBM Service Provider Delivery Environment and global telecom strategies. You can contact Joe at [email protected].

The IBM Institute for Business Value develops fact-based strategic insights for senior business executives around critical industry-specific and cross-industry issues. Clients in the Institute’s member programs—the IBM Business Value Alliance and the IBM Institute for Knowledge-Based Organizations—benefit from access to in-depth consulting studies, a community of peers, and dialogue with IBM strategic advisors. These programs help executives realize busi-ness value in an environment of rapid, technology-enabled change. You can send an e-mail to [email protected] for more information on these programs.

References1 IBM Institute for Business Value research and analysis.2 IBM Institute for Business Value research and analysis.3 IBM Business Consulting Services research and analysis.4 IBM Business Consulting Services and IBM Institute for Business Value research

IBM Global ServicesRoute 100Somers, NY 10589U.S.A.

Produced in the United States of America11-02 All Rights Reserved

IBM and the IBM logo are registered trademarks of International Business Machines Corporation in the United States, other countries, or both.

Other company, product and service names may be trademarks or service marks of others.

References in this publication to IBM products and services do not imply that IBM intends to make them available in all countries in which IBM operates.