14

Leading UK Service Charge Consultants Leases and the Code The critical role of UK commercial office lease provisions in shaping the service charge process. Discussion Paper

Leading UK Service Charge Consultants

Leases and the CodeThe critical role of UK commercial office lease

provisions in shaping the service charge process.

Discussion Paper

www.property-solutions.com

Page 2

Lease transparency and service charges: the critical role of UK commercial office lease provisions in shaping the service charge process.

At present, relatively little is known about the

degree to which an average UK commercial

lease complies with the Code’s requirements for

accountability and management transparency, or

whether these legal documents provide adequate

prescriptive guidance in these key areas. This

current paper reports on lease research conducted

by Property Solutions and Professor Andrew Holt,

from Metropolitan State University of Denver,

which reviews the provisions within leases at 90

UK multi-let commercial office buildings. The

research assesses the quality and transparency of

provisions within current commercial leases, and

identifies whether provisions exist that support the

requirements and objectives of the RICS Code.

While the Royal Institution of Chartered Surveyors (RICS) Code of Practice Service Charges in Commercial Property (RICS, 2014) attempts to promote best practice within the management and financial reporting practices for service charges, issues arise when the provisions of the underlying lease conflict with the Code’s requirements, or are silent as to the exact nature of the management, accounting, certification and auditing requirements for the service charge process. As a result, it is critical that modern commercial leases incorporate Code-compliant provisions that facilitate the adoption and dissemination of best practice.

www.property-solutions.com

Page 3

BACKGROUND

UK commercial service charges are not subject to

statutory legislation, with the requirements related

to their management being stipulated in individual

lease agreements. A service charge is only payable

if the lease specially requires it, and each individual

lease agreement may or may not contain specific

lease provisions that describe the financial reporting,

management, administrative, and audit processes that

apply when managing the service charge process.

Where an individual lease is silent in terms of these

requirements, the main practical guidance for the

building manager or managing agent comes from

the non-mandatory RICS Code of Practice, Service

Charges in Commercial Property, which came into

force in 2007 (RICS, 2014).

This paper is written at a time when a revised RICS

commercial Code is currently under development

and should be published during 2018. Considering the

official and unofficial versions, this will be the sixth

edition of the Code, following those published in 1996,

2000, 2006, 2011, 2014 (RICS, n.d.; Guide to Guide

to Good Practice Working Party, 2000, RICS, 2006,

2011, 2014). While the Code and its requirements have

promoted best practice, research indicates that overall

levels of compliance with its guidance remain poor,

both in the UK commercial office and retail sectors

(see Property Solutions, 2017, and Holt, Pal and White,

2017). There appears to be an “expectations gap”

between what commercial tenants may expect to

receive in terms of the service charge accounting and

administrative process and what managing parties

actually provide (Holt, 2015). The existing literature

provides a multitude of reasons, including the fact

that the Code is simply a non-mandatory guidance

note for members. Despite this, the RICS is clear

about the professional importance in following the

Code’s requirements:

A practitioner conforming to

the practices recommended in

this Code is unlikely to be

adjudged negligent on account

of having followed these

practices (RICS, 2014, p. 2).

Practitioners should only depart from the practice

recommended in the Code where there is good

reason to do so, such as when it conflicts with existing

lease terms. The Code cannot override the lease, but:

If read in conjunction with it, it

can enable users to identify the

best way forward in

interpreting that lease to

ensure effective management

of services (RICS, 2014, p. 7).

As a result, the clarity of existing commercial lease

provisions and the extent to which they incorporate

the Code’s recommendations play a critical

role in promoting the adoption of best practice

within commercial service charges. The Code

acknowledges the need for leases to incorporate

revised service charge provisions complying with

the principles and provisions of this Code. The City

of London Law Society and Practical Law Company

have drawn up documents for use by practitioners.

In addition, the British Property Federation (BPF,

2017) commissioned the Modern Commercial Lease

(MCL) template, which incorporates many of the

RICS Code’s accounting and reporting requirements.

www.property-solutions.com

Page 4

Despite the critical role of current lease provisions

in developing best practice, little is currently known

about the extent to which current lease terms either

conflict with or support the Code’s requirements. In

earlier research supported by Property Solutions,

Holt (2015) reviewed 20 leases at UK multi-let

office buildings larger than 50,000 sq. ft, and found

that none included a requirement for an audit

or independent accountants report or specified

whether accounts should be prepared on a cash or

accruals basis. In addition, only 50% of the leases

included a provision that entitled the occupier to

inspect the service charge records or vouchers.

While it is hard to generalize from such a small study,

this pilot exercise indicated the need for further

lease-based research, as lease deficiencies appeared

to exist that might prevent the adoption of the

Code’s best practice requirements.

This current study adds to the latest literature, providing the first large scale investigation of the extent to which commercial leases support the best practice recommendations of the RICS Code.

METHODOLOGY

Provisions within leases at 90 UK multi-let commercial

office buildings were reviewed by this study. The 90

leases were a random representative sample from a

population of 112 leases available to one service charge

management consultancy. While the source of the

documents may indicate a potentially biased dataset,

the 90 leases were prepared by 67 different legal

firms for 86 different landlords and 37 tenants. 82 of

the leases had an inception date after the publication

of the 2nd unofficial version of the RICS Code in

2000, and 62 were signed after the release of the first

official version of the Code in 2006. As a result, the

sample includes a variety of inception dates, with most

documents applicable for assessing whether “modern

leases” incorporate and/or support the best practice

recommendation of the RICS Code. The mean and

median length of each lease were 72.5 and 63 pages,

respectively. Table 1 provides a summary of the lease

length within the sample, and illustrates that most

modern leases tend to be shorter, and are moving

away from the typical norm of 25 years.

Table 1: Lease DurationLease Term No. %5 or less 18 20.0%

6-10 34 37.8%

11-15 23 25.6%

16-20 9 10.0%

21.24 1 1.1%

25 or more 5 5.6%

Total 90 100.0%

The move towards shorter lease durations is further

illustrated in Figure 1, which compares the inception

year of each lease with its duration, and shows that

more modern leases are typically shorter in length.

www.property-solutions.com

Page 5

Figure 1: Lease Inception Year versus Duration

0

5

10

15

20

25

30

1990 1994 1998 2002 2006 2010 2014

Leas

e te

rm in

yea

rs

Year of inception

In total, the 90 leases represented 2,076,008 sq. ft.

of demised occupied space in buildings whose total

service charge liability per annum was £78,562,042.

For the entire buildings represented by the 90

leases, the median annual service charge expenditure

was £495,775. Table 2 illustrates the range in

whole building annual service charge expenditure

represented by the leases, and highlights that 22.2%

of the sample represented commercial buildings

whose annual service charge expenditure exceeded

£1,000,000 per annum.

These often-considerable amounts of service charge

expenditure are not subject to statutory regulation

in terms of their annual accounting and financial

reporting, so occupiers face potential risk and

liability where the commercial lease fails to provide

adequate accounting provisions.

Table 2: Annual Whole Building Service Charge ExpenditureAnnual service charge No. %£50,000 or less 7 7.8%

£50,001 - £250,000 21 23.3%

£250,001 - £500,000 17 18.9%

£500,001 - £1,000,000 25 27.8%

£1,000,001 - £2m 12 13.3%

More than £2m 8 8.9%

Total 90 100%

www.property-solutions.com

Page 6

This is perhaps surprising given that the accounting

mechanisms for UK residential service charges are

regulated, and even small UK limited liability entities

that have an annual turnover of less than £1m face

mandatory annual reporting requirements (for more

details see Holt, 2015, and Companies House, 2016).

The data sample was used to assess the quality

and transparency of certain provisions within UK

commercial leases, and identified whether they

supported the requirements of the RICS Code.

The analysis focused on 14 critical areas within the

service charge process, including whether the lease:

• Referred to the RICS Code

• Explained the landlord’s covenant to provide

services

• Defined the service charge and what costs it

includes

• Explained whether the service charge was

collected in advance

• Included a dispute resolution provision

• Mentioned environmental sustainability

• Provided a clear and transparent accounting

process, including direction about:

• The accounting basis used (i.e. accruals or

cash accounting)

• The cost apportionment methodology

• The budgetary obligations

• The annual cost certification obligations

• The time period for certification

• The “audit” or independent review obligations

• The tenant’s ability to inspect the

documentation that supports the certificate

of annual expenditure

• The time period for inspecting the

documentation that supports the certificate

www.property-solutions.com

Page 7

For each of the 14 areas under investigation, the

researchers read the lease and determined whether

it supplied adequate direction and clarity on the

issue. By this process, each lease was assigned a

binary score of 1 or 0 in each area depending on

whether it provided full or inadequate direction or

clarity on the matter. Once this was complete, each

lease was assigned a rating out of 14 for overall

transparency and its level of support for the best

practice requirements of the RICS Code. In addition

to these fourteen core areas, additional lease analysis

was conducted other areas, including whether the

service charge was defined as rent or a service

charge cap applied.

While the processing and classification of the

lease data required some degree of subjective

interpretation on behalf of the researchers, the

data codification required was binary in nature, and

largely unproblematic where sufficient explanation

was provided within the lease. Judging the efficacy

of a lease provision might be contentious in theory,

but in practice, the nature of the service charge

renders the analysis relatively obvious. However,

given the poor level of explanation within many

commercial service charge leases, the difficulty of

subjective interpretation is not to be underestimated.

Whilst the quantitative data within this paper does

rely on qualitative judgements, the resulting data

are inherently sound and offer a valid examination of

current lease provisions.

RESULTS

General Results and Issues

The 90 lease documents varied widely in terms

of their layout, detail and prescription. This was

perhaps unsurprising as they were drawn up by 67

different legal firms for 86 different landlords, but

the researchers did not expect to see such wide

variations in layout given the existence of model

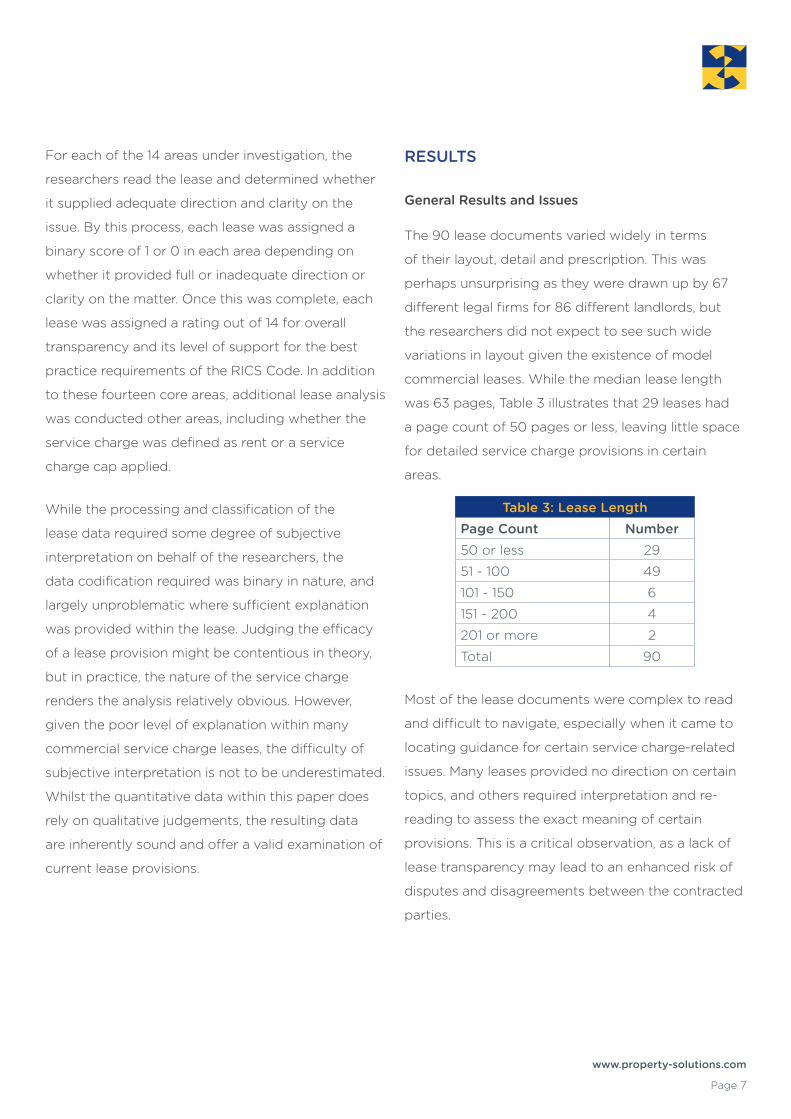

commercial leases. While the median lease length

was 63 pages, Table 3 illustrates that 29 leases had

a page count of 50 pages or less, leaving little space

for detailed service charge provisions in certain

areas.

Table 3: Lease LengthPage Count Number50 or less 29

51 - 100 49

101 - 150 6

151 - 200 4

201 or more 2

Total 90

Most of the lease documents were complex to read

and difficult to navigate, especially when it came to

locating guidance for certain service charge-related

issues. Many leases provided no direction on certain

topics, and others required interpretation and re-

reading to assess the exact meaning of certain

provisions. This is a critical observation, as a lack of

lease transparency may lead to an enhanced risk of

disputes and disagreements between the contracted

parties.

www.property-solutions.com

Page 8

Table 4: Analysis of Provisions within the 90 Leases

Lease Provision Content No. with Clear Provisions %

1 RICS Code referred to (of 82 relevant leases) 11 13.4%

2 Landlord’s covenant to provide services 84 93.3%

3 Service charge adequately defined 81 90.0%

4 Service charge collected in advance 84 93.3%

5 Dispute resolution process adequately defined 38 42.2%

6 Mention of environmental issues 31 34.4%

7 Details of accounting basis to be used ie. cash or accruals 0 0.0%

8 Apportionment methodology given 87 96.7%

9 Budgetary obligations set out 38 42.2%

10 Annual cost certification obligations set out 85 94.4%

11 Time period for certification given 19 21.1%

12 “Audit” obligations defined 37 41.1%

13 Tenant’s ability to inspect the documents supporting the certificate 44 48.9%

14 Time period for inspecting the documents supporting the certificate 25 27.8%

As only 13.4% of leases signed after the Code’s

inception directly referred to it, the industry should

incorporate lease provisions that protect both

parties by incorporating direct reference to the role

of the professional guidelines of the RICS.

While Table 4 identifies a number of weaknesses in

the overall level of transparency and detail within

commercial leases, it does not reveal the extent to

which individual leases provide the information and

guidance necessary for managing the service charge

arrangement. Figure 2 ranks the 90 leases by the

extent to which they supplied relevant information

for each of the 14 metrics highlighted in Table 4. Only

71.1% of the leases provided direction or transparent

guidance in 7 or more of the 14 areas, with 28.9%

providing relevant and adequate guidance in 6 or

less areas. While some of these 14 metrics, such

as supplying information about environmental

sustainability, may not by relevant for every lease

agreement, best practice dictates that modern

leases supply clear information about key aspects

of the lease and the service charge process.

In terms of whether the sample of leases provided

clear and transparent information about each of the

14 core metrics analysed by the research, results

were mixed. Table 4 shows the summarized results

of the study, which indicate that most leases fail

to include provisions that support many of the

best practice requirements of the RICS Code. For

example, a higher number of leases included detailed

provisions about environmental issues (34.4%) than

those that specifically mentioned the importance of

complying with the RICS Code (13.4%).

www.property-solutions.com

Page 9

Figure 2: Lease Transparency in 14 areas relevant to the RICS Code

0 1 2 3 4 5 6 7 8 9 10 11 12 13 140.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

1.1%3.3%

8.9%

14.4%

26.7%

15.6%

12.2%13.3%

1.1% 1.1%2.2%0.0% 0.0% 0.0% 0.0%

Areas

The individual lease rankings in Figure 2 identify fundamental problems in current levels of lease transparency

and guidance, and provide further evidence for why compliance with the RICS Code remains patchy at best.

As the lease establishes the contractual rights, obligations and duties of each party, it must be clearly written,

complete and incorporate best-practice(s). As the sample incorporated documents with an array of lease

inception dates, further analysis was conducted as to whether the signing year influenced the level of lease

transparency. Figure 3 shows the results organized by lease inception year, and illustrates that transparency

varies considerable even between leases signed in the same year. While the trend indicates a small yearly

increase in transparency, overall transparency levels are still relatively poor.

Figure 3: Overall Lease Transparency: Inception Year versus 14 metrics

0

2

4

6

8

10

12

14

1990 1994 1998 2002 2006 2010 2014

Sco

re v

ersu

s 14

met

rics

Year of lease inception

www.property-solutions.com

Page 10

ACCOUNTING RELATED ISSUES

While the general results presented in section 4.1 are

an important barometer of overall lease guidance for

the service charge process, more focused analysis is

needed to ascertain whether current lease provisions

support the Code’s key specific accounting and

audit guidance. Since its inception, the Code has

attempted to improve both the relevance and

reliability of the service charge accounting process,

and now includes detailed requirements for the

preparation, dissemination and review of the service

charge accounts (see Holt, 2015 and Holt, White

and Pal, 2017). To assess whether current leases

support the Code’s attempts at improving the

service charge accounting process, the provisions

in each lease were reviewed to see whether they

provided information relevant to the following nine

accounting-related metrics.

• The service charge defined; what costs it

includes

• The accounting basis used (ie accruals or cash

accounting)

• The cost apportionment methodology

• The budgetary obligations

• The annual cost certification obligations

• The time period for certification

• The “audit” or independent review obligations

• The tenant’s ability to inspect the documentation

that supports the certificate of annual

expenditure

• The time period for inspecting the

documentation that supports the certificate

While these nine metrics were previously analysed within the generic section 4.1 results, they will now be

specifically analysed for each lease. Figure 4 presents the results of the accounting-related lease analysis, and

reveals that only 11.1% of leases provided the necessary information in 7 or more of these key accounting areas.

Figure 4: Lease Transparency in 9 Accounting Areas relevant to the RICS Code

0 1 2 3 4 5 6 7 8 90.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2.2% 2.2%1.1%

11.1%

37.8%

14.4%

20.0%

7.8%

3.3%

0.0%

Areas

www.property-solutions.com

Page 11

In most cases, current leases were either silent or lacked direction in many key accounting areas, which

represents a failure to adopt the best practice requirements of the Code. Figure 5 illustrates whether the

overall level of these accounting omissions is influenced by the inception date of the lease, and the results

suggest that more recent leases still provide inadequate levels of accounting transparency and direction, with

little sign of time-related improvement.

Figure 5: Accounting Lease Transparency: Inception Year versus 9 Metrics

0

1

2

3

4

5

6

8

7

9

1990 1994 1998 2002 2006 2010 2014

Sco

re v

ersu

s 9

met

rics

Year of lease inception

Adopting a professional accounting approach

for the management of service charge costs

and monies is necessary for the protection of all

parties, so the failure of current leases to outline

key accounting processes and protocols is very

disappointing. For example, while Core Principle

24 of the RICS Code specifies that “managers

will issue budgets to occupiers, including an

explanatory commentary at least one month prior

to the start of the service charge year” and “detailed

statements of actual expenditure…within four months

of the service charge year-end” (RICS, 2014, p. 6),

most leases do not include provisions that support

such ideals. In many instances, leases do not include

a requirement for the preparation of an annual

budget (57.8% of leases), and specify differing time

periods for the provision of both budgets and annual

reconciliation certificates.

www.property-solutions.com

Page 12

In terms of other critical accounting aspects, 0.0%

of leases specified the accounting basis to be used

for the preparation of the annual service charge

accounts (0 of 90 leases). This is a critical omission,

as the RICS Code requires the annual accounts to be

prepared under the accrual basis. In contrast, 94.4%

of leases specified the process for the annual service

charge accounting and certification process, but only

21.1% specified a time period that the certification

must be completed within.

In terms of audit and independent assurance, only

41.1% of leases formally specified the “audit” or review

requirements for the service charge accounts, and

only 48.9% granted tenants with a right to inspect

the documents that supported the annual certificate

of expenditure.

Overall, in many accounting-related areas,

commercial leases provide a vacuum of direction

and guidance. As a result, it is no surprise that

many service charge accounting documents are

inconsistent, untimely, lack detail, and offer little in

the way of assurance to tenants (see Holt, 2015 for

more detail on these issues).

www.property-solutions.com

Page 13

CONCLUSIONS AND RECOMMENDATIONS

While some of the lease analysis results are

disappointing, they are hardly a surprise given the

results of the earlier lease research conducted by

Holt (2015). Most commercial leases are difficult

to navigate and lack clarity regarding key areas

of the service charge process. The analysis clearly

indicates that most leases are not adopting

the Modern Commercial Lease (MCL) template

commissioned by the British Property Federation

(BPF, 2017), which incorporates many of the RICS

Code’s core principles and requirements. As a result,

most leases enhance the risk of legal disputes

between the contracted parties.

As the forthcoming revised version of the RICS Code may be released as a Professional Statement, it will be interesting to see its impact, especially where many commercial leases fail to provide detailed guidance on the service charge process for both contracted and managing parties. Will issuing the Code as a Professional Statement bring the necessary impetus for the evolution of best practice in the field of service charge accounting and reporting? In theory, yes, as having the RICS review reports of actions in direct conflict with the provisions of the Code should deter non-compliance, at least from managing parties who are members of the RICS. However, even the Code’s release as a Professional Statement risks being undermined by current lease provisions that do not support its ideals.

While the publication of the 2014 RICS Code, its

associated 2013 RICS accounting guidance note

and the ICAEW Technical Release 11/13BL have

helped to establish a framework of “best practice”

principles for the preparation of service charge

accounts and their subsequent audit and review,

these have yet to implemented in most commercial

leases. The cause of this omission is hard to

determine, but it needs addressing, as the lease is

the driving force behind the service charge process

and currently appears to provide a legal barrier to

the development of best practice.

Property Solutions (UK) Limited

Registered in England No. [email protected]

+44 (0)1454 332211

www.property-solutions.co.uk