The Crossings at Fleming Island Community Development District Refunding Analysis of Series 2007 Utility Revenue Bonds Talking Points: 1. An advance refunding today, with NPFG Insurance and an underlying rating from Moody's of A2 reflects the most debt service savings. 2. Based on certain assumptions, estimated savings is projected at $280,000 to $285,000 per year. 3. Preliminary projections indicate that a reduction in debt service and reduction in the targeted debt coverage to 1.05x could result in a decrease of the debt capacity charge from $40.99 per month to $32.81 per month, or approximately $8 per month. 4. In talks we've had with the Rate Consultant (PRMG), based on their high level estimates, for every additional $100k reduction to debt service we can lower the monthly debt charge by $2. 5. Next steps would be to authorize staff to begin the preparation of the Bond Documents for an advance refunding, to close in mid-November. 6. During the document preparation period, PRMG will be fine tuning the numbers and recommendations for funding certain accounts such as: a. Rate Stabilization Fund (15% or more) b. Renewal and Replacement Fund (for the Reuse System) c. Working Capital aka Liquidity (Cash to keep on hand for Operations) d. Revised Annual Debt Service Coverage Recommendation (Currently at 1.15x Debt Service). Under the new indenture this is being proposed as a 15% sum sufficient amount to be held in the Rate Stabilization Fund. (Note: the Insurers may require a little more than lx coverage, we have had discussions with them regarding 1.05x coverage, where the excess funds after the payment of debt service annually would flow to the redemption fund). 7. If the Debt Capacity Charges remained the same, then you would expect to generate in annual surplus the amount shown in (2) above, representing the projected annual debt service savings subsequent to the advance refunding. 8. Refunding the bonds, whether today or a year from now, would allow the District to: a. Modify the Rate Covenant and Coverage Requirement; b. Reduce the debt service reserve fund requirement; and c. Free up surplus funds in the operating account to be used for either i) reducing the refunding par or ii) transfer to the Unforeseen Fund to be used as the Board determines. October 19, 2016

Transcript

The Crossings at Fleming Island Community Development District Refunding Analysis of Series 2007 Utility Revenue Bonds

Talking Points:

1. An advance refunding today, with NPFG Insurance and an underlying rating from Moody's of A2 reflects the most debt service savings.

2. Based on certain assumptions, estimated savings is projected at $280,000 to $285,000 per year. 3. Preliminary projections indicate that a reduction in debt service and reduction in the targeted

debt coverage to 1.05x could result in a decrease of the debt capacity charge from $40.99 per month to $32.81 per month, or approximately $8 per month.

4. In talks we've had with the Rate Consultant (PRMG), based on their high level estimates, for every additional $100k reduction to debt service we can lower the monthly debt charge by $2.

5. Next steps would be to authorize staff to begin the preparation of the Bond Documents for an advance refunding, to close in mid-November.

6. During the document preparation period, PRMG will be fine tuning the numbers and recommendations for funding certain accounts such as:

a. Rate Stabilization Fund (15% or more) b. Renewal and Replacement Fund (for the Reuse System) c. Working Capital aka Liquidity (Cash to keep on hand for Operations) d. Revised Annual Debt Service Coverage Recommendation (Currently at 1.15x Debt

Service). Under the new indenture this is being proposed as a 15% sum sufficient amount to be held in the Rate Stabilization Fund. (Note: the Insurers may require a little more than lx coverage, we have had discussions with them regarding 1.05x coverage, where the excess funds after the payment of debt service annually would flow to the redemption fund).

7. If the Debt Capacity Charges remained the same, then you would expect to generate in annual surplus the amount shown in (2) above, representing the projected annual debt service savings subsequent to the advance refunding.

8. Refunding the bonds, whether today or a year from now, would allow the District to: a. Modify the Rate Covenant and Coverage Requirement; b. Reduce the debt service reserve fund requirement; and c. Free up surplus funds in the operating account to be used for either i) reducing the

refunding par or ii) transfer to the Unforeseen Fund to be used as the Board determines.

October 19, 2016

Crossings at Fleming Island Community Development District

Presentation to the Board of Supervisors

October 20, 2016

Presented by

MBS Capital Markets, LLC

TABLE OF CONTENTS

OVERVIEW

PROPOSED REFUNDING - SERIES 2007 BONDS

FUTURE ACTIONS

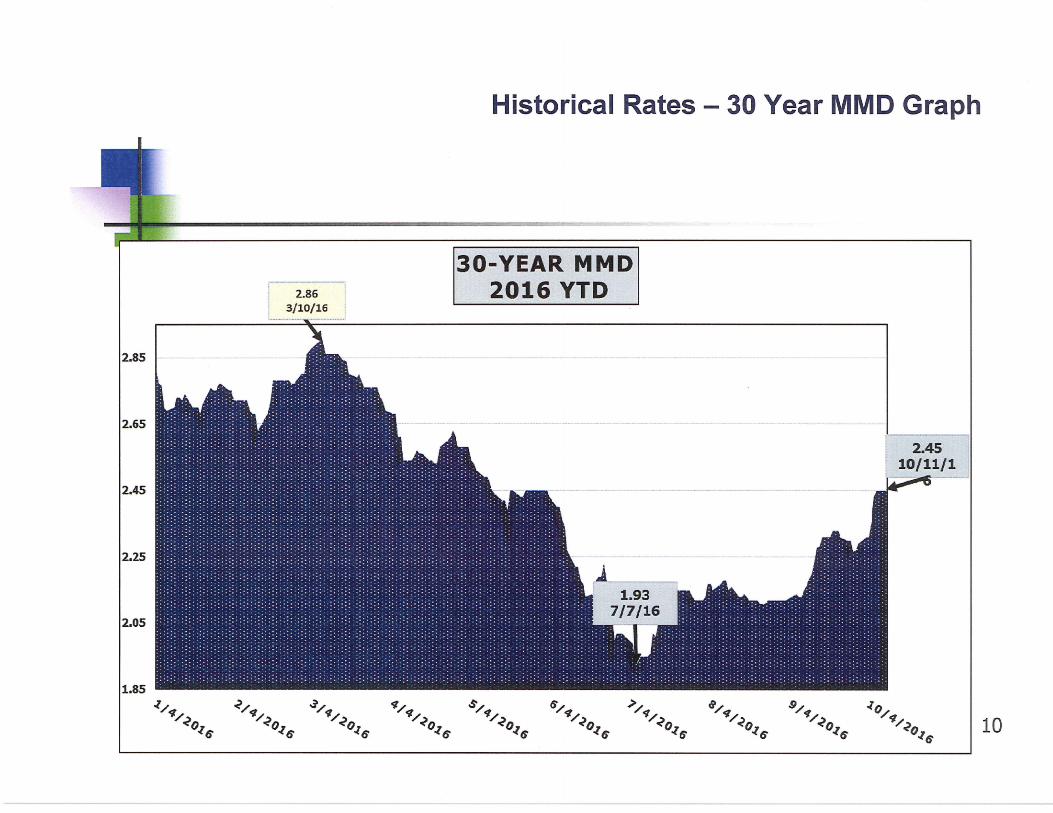

HISTORICAL MMD CHART-2016

Section 1

Section 2

Section 3

Section 4

2

Overview of Series 2007 Utility Bonds

The Crossings at Fleming Island Community Development District (the "District") issued its $28,900,000 Utility Revenue Refunding Bonds, Series 2007 (the "Series 2007 Bonds") in June, 2007.

The Series 2007 Bonds were AAA rated due to the MBIA insurance guaranteeing the payment of the debt service on the bonds.

The Series 2007 Bond proceeds were used to: 1. Refund and Redeem all of the Outstanding principal amount of the District's $15, 125,000

Utility Revenue Bonds, Series 1994; 2. Refund and Redeem all of the Outstanding principal amount of the District's $7,525,000

Utility Revenue Bonds, Series 1999; 3. Repay and extinguish certain indebtedness related to the construction and start-up

operations of the Utility System; 4. Make a deposit to the Reserve Account to defray a portion of the Reserve Account

Requirement for the Series 2007 Bonds; and s. Pay the Costs of Issuance of the Series 2007 Bonds, including the premiums on a financial

guaranty insurance and debt service reserve fund surety policy.

3

Overview of Series 2007 Utility Bonds

The Series 2007 Bonds began amortizing in 2008 and are currently outstanding in the amount of $24,650,000.

The Series 2007 Bonds are call protected until October 1, 2017 at which time they may be currently refunded at Par.

The Series 2007 Bonds may also be advance refunded prior to October 1, 2017 by establishing a refunding escrow for the defeasance of the Series 2007 Bonds upon the issuance of the Refunding Bonds. Based on the District's operating results, it appears it would be economically feasible to advance refund the Series 2007 Bonds, however there would be negative arbitrage if advance refunded.

The portion of the Series 2007 Bonds relating to the refunding of the Series 1999 Bonds (approximately 25°/o of the Bonds) may not be advance refunded again with tax exempt bonds. They may however be advance refunded with taxable bonds.

The breakdown of the Series 2007 Bonds follows: Par Related to the Series 1994 Current Refunding Bonds (2007-1) Par Related to the Series 1994 Advance Refunding Bonds (2007-2) Par Related to the defeasance of other indebtedness (2007-3) Total Par Amount of Series 2007 Bonds

$11, 135,000 $ 7,265,000 $10,500,000 $28,900,000

4

Overview of Series 2007 Utility Bonds

Several refunding options have been structured to provide the District with the information needed to determine the least cost and best savings to the District under each scenario.

5

Refunding Scenarios - 2007 Utility Bonds

• The Proposed Series 2016 Refunding Bonds have received an indicative rating from Moody's of A2.

• Currently the Series 2007 Bonds are insured by MBIA, now known as National Public Financial Guaranty (NPFG). In addition to providing bond insurance, NPFG also provided a surety bond to the District in lieu of a cash funded debt service reserve fund for 50°/o of the reserve fund requirement. MBS is pursuing NPFG's interest in insuring and providing a surety bond for the proposed Series 2016 Bonds. Bond insurance typically provides a lower average coupon than a simple bond rating due to the insurance of debt service payments by the insurer. (Refer to Scenarios 7 and 8 in the following slide.)

7

Proposed Series 2016 Utility Refunding Revenue Bonds

The table below illustrates the refinancing of the Series 2007 Bonds under current market conditions assuming four (4) different refunding scenarios and the projected refunding results under each scenario.

Il.:..I~-~-~-~~-~-e! .................... - .. ···········-~---···-·-·········-·····-···-··-··--·-··-----·--·-·------------·--··--·-····································· MADS= Maximum Annual Debt Service

l ~_E!venues I ___ $_5,~9.Q,000 1 .. : _ I Target Revenues . $1,676,040.20 I Expenditures 1 I $3.236.565 I ' 1--------------········------··-----------··-----··------------------------------··-----------·--'------··----------------------->-------- - - .. ··- ------·····----·--·--··-··--··-··--··-·-·······-··---------------·-------··············--··········-········-················-------------··-------------····--··------··----·-······-····--·········-········---··--····-··----····--, Net Income before Debt Service 1 $2,253,4351__ _______ :rota! Units! ___ ~ ______ : ______ 425.zj

!.P._E! bt s_~lce Exe_~~E! ___ _. ________ J_ _________ i ___ S_l.882.094 j - _, ________ --- . _ 1 _~_?_~.':!..~L~~Lt£.e:_~o__12~b_ ________________ $}_~?_1J !_~_et Income after Debt Service '. $371,341 , _ _ .. , ____ , I Debt Service Coverage . I 1.20 1 ' . I lcov~g;·R-eq-_ ul;:;~~~t_,·------;--~-·----~--------·l~lS·-·-·~=·=~----~==-=:--·-·-~------·--~------·---······--·-·------1

The above is preliminary, subject to change, based on current market conditions and certain assumptions, actual rate reduction to be determined by Rate Consultant. 11

"' c: 0 ·-..... 0 <( Q) I.. :J ..... :J

LL

Refunding Process-Public Offering

• Document Preparation • Prepare Documents - Week of October 24th • Reconvene Board Meeting on November 3rd

• Approved Delegated Award Resolution including • Supplemental Trust Indenture • Continuing Disclosure Agreement • Escrow Agreement • Bond Purchase Agreement

• Print and Mail - Week of November 7th • Price Bonds - November 14th