39

| Date post: | 13-Feb-2017 |

| Category: |

Economy & Finance |

| Upload: | jean-blaise-nlemfu-mukoko |

| View: | 85 times |

| Download: | 1 times |

The Cyclical Behavior of the Markups in theNew Keynesian Models

Jean Blaise Nlemfu M.

June 2015

Jean Blaise Nlemfu M. 1 / 39

Outline

1 Introduction

Background

What This Paper Does

Findings

2 The Model

Firms and Price setting

Households and Wage setting

Monetary Policy

Aggregation

3 Calibration

4 Results

Staggered Price-Setting Model

Staggered Wage - Setting Model

Staggered Price-Setting and Staggered Wage-Setting Model

5 Conclusion

Jean Blaise Nlemfu M. 2 / 39

Background

"How markups move, in response to what, and why, is however nearly terra

incognita for macro. ... Some of these theories imply pro-cyclical markups,

..... Some imply, however, counter-cyclical markups, with the opposite

implication. ... But we are a long way from having either a clear picture or

convincing theories and this is clearly an area where research is urgently

needed." � Blanchard (2008), p.18

Jean Blaise Nlemfu M. 3 / 39

Role of price markup in the New KeynesianModels

Inspired by evidence of countercyclical price markup which builds upon

earlier work by Bils (1987) and Rotemberg and Woodford (1999)

Price markup is a key part of the transmission mechanism :

A positive demand shock leads output and marginal cost to increase.Because prices cannot adjust immediately, the markup falls.A positive technology shock lowers marginal cost and raises output.Because prices cannot adjust immediately, the markup rises.

Leading New Keynesian models with sticky prices and sticky wages

also predict countercyclical price markups in response to demand

shocks.

Jean Blaise Nlemfu M. 4 / 39

Evidence of procyclical price markup

Built upon recent work by Nekarda and Ramey (2013) and many

others

Evidence of acyclical or procyclical price markup conditional on supply

and demand shocks.

The question is :what will happen in a model where monopolistically competitivehouseholds set wages in staggered contracts ?

Wage markup varies

the focus on price markup in the literature is misplaced

Jean Blaise Nlemfu M. 5 / 39

What This Paper Does

Analyzes markup cyclicality using a medium-scale DSGE model

Inspired by Ascari, Phaneuf and Sims (2015) which built upon earlierwork by CEE (2005)An extended version with :

Non-zero steady-state in�ation

Roundabout production structure

trend growth in IST and neutral technology

aggregate �uctuations are driven by neutral technology, MEI and

monetary policy shocks

and most importantly both price and wage markups vary

assesses how positive trend in�ation a�ects the responses of price and

wage markups to shocks

Identi�es alternative sources of price and wage markups cyclical

behavior

Jean Blaise Nlemfu M. 6 / 39

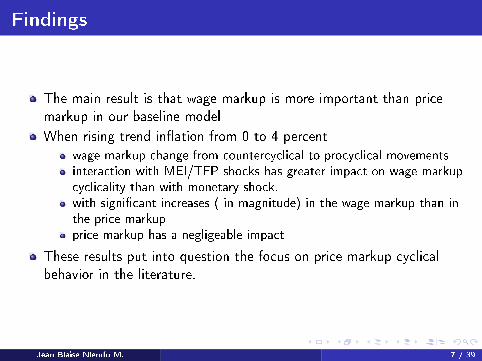

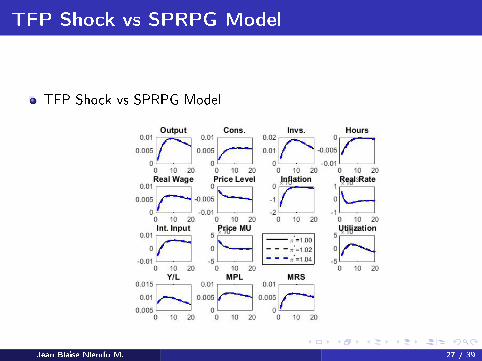

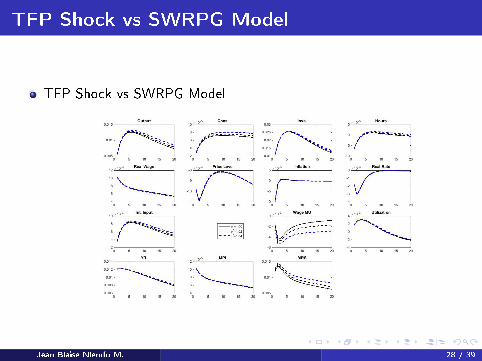

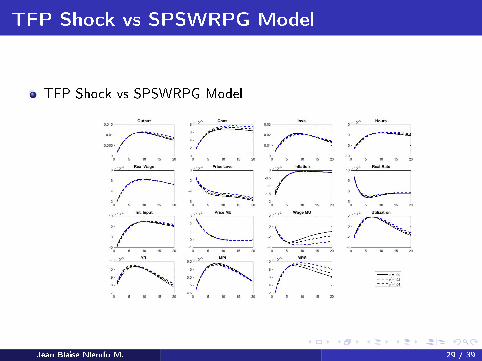

Findings

The main result is that wage markup is more important than price

markup in our baseline model

When rising trend in�ation from 0 to 4 percent

wage markup change from countercyclical to procyclical movementsinteraction with MEI/TFP shocks has greater impact on wage markupcyclicality than with monetary shock.with signi�cant increases ( in magnitude) in the wage markup than inthe price markupprice markup has a negligeable impact

These results put into question the focus on price markup cyclical

behavior in the literature.

Jean Blaise Nlemfu M. 7 / 39

Outline

1 Introduction

Background

What This Paper Does

Findings

2 The Model

Firms and Price setting

Households and Wage setting

Monetary Policy

Aggregation

3 Calibration

4 Results

Staggered Price-Setting Model

Staggered Wage - Setting Model

Staggered Price-Setting and Staggered Wage-Setting Model

5 Conclusion

Jean Blaise Nlemfu M. 8 / 39

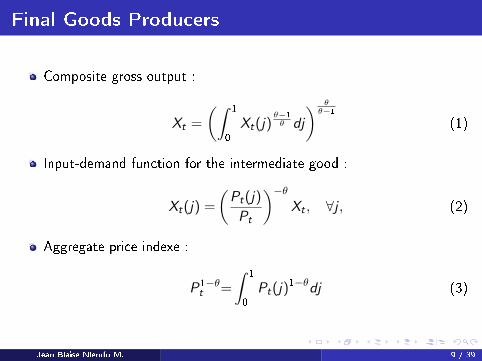

Final Goods Producers

Composite gross output :

Xt =

(∫1

0

Xt(j)θ−1

θ dj

) θθ−1

(1)

Input-demand function for the intermediate good :

Xt(j) =

(Pt(j)

Pt

)−θXt , ∀j , (2)

Aggregate price indexe :

P1−θt =

∫1

0

Pt(j)1−θdj (3)

Jean Blaise Nlemfu M. 9 / 39

Intermediate Producers

The production function for a typical intermediate producer j :

Xt(j) = max

{AtΓt(j)

φ(Kt(j)

αLt(j)1−α)1−φ

−ΥtF , 0

}, (4)

F is a �xed cost, and production is required to be non-negative.

Υt is a growth factor and F is chosen to keep pro�ts zero along a

balanced growth path.

At follows a process with both a trending and stationary component :

At = AtAτt , (5)

Aτt = gAAτt−1 (6)

The stochastic process driving the detrended level of technology At is

given by

At =(At−1

)ρAexp(sAu

At

), 0 ≤ ρA< 1 (7)

Jean Blaise Nlemfu M. 10 / 39

Pro�t Maximization and Price Setting

Firms set their price according to Calvo pricing

Since all updating �rms will choose the same reset price, the optimal

reset price relative to the aggregate price index is p∗t ≡P∗t

Pt.

The optimal pricing condition can be written:

p∗t =θ

θ − 1

x1,tx2,t

. (8)

The auxiliary variables x1,t and x2,t can be written recursively :

x1,t = λrtνtXt + βξpEt(πt+1)θx1,t+1, (9)

x2,t = λrtXt + βξpEt(πt+1)θ−1x1,t+1. (10)

Jean Blaise Nlemfu M. 11 / 39

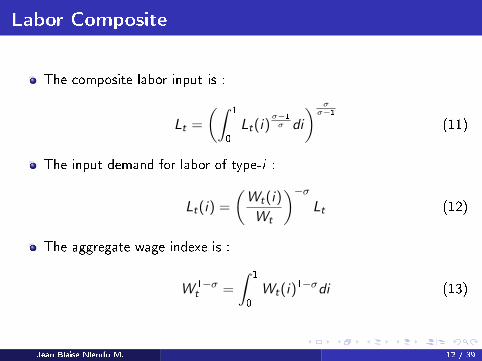

Labor Composite

The composite labor input is :

Lt =

(∫1

0

Lt(i)σ−1

σ di

) σσ−1

(11)

The input demand for labor of type-i :

Lt(i) =

(Wt(i)

Wt

)−σLt (12)

The aggregate wage indexe is :

W 1−σt =

∫1

0

Wt(i)1−σdi (13)

Jean Blaise Nlemfu M. 12 / 39

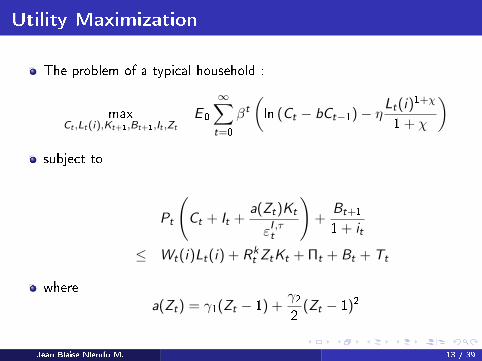

Utility Maximization

The problem of a typical household :

maxCt ,Lt(i),Kt+1,Bt+1,It ,Zt

E 0

∞∑t=0

βt(ln (Ct − bCt−1)− ηLt(i)

1+χ

1 + χ

)subject to

Pt

(Ct + It +

a(Zt)Kt

εI ,τt

)+

Bt+1

1 + it

≤ Wt(i)Lt(i) + Rkt ZtKt + Πt + Bt + Tt

where

a(Zt) = γ1(Zt − 1) +γ22

(Zt − 1)2

Jean Blaise Nlemfu M. 13 / 39

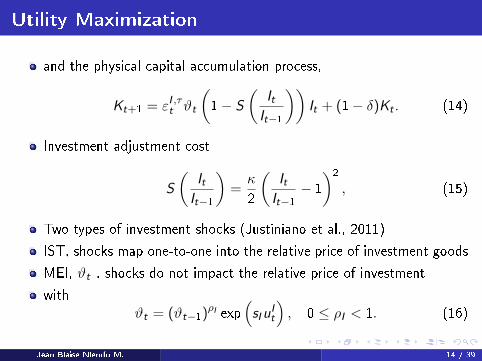

Utility Maximization

and the physical capital accumulation process,

Kt+1 = εI ,τt ϑt

(1− S

(ItIt−1

))It + (1− δ)Kt . (14)

Investment adjustment cost

S

(ItIt−1

)=κ

2

(ItIt−1− 1

)2

, (15)

Two types of investment shocks (Justiniano et al., 2011)

IST, shocks map one-to-one into the relative price of investment goods

MEI, ϑt , shocks do not impact the relative price of investment

with

ϑt = (ϑt−1)ρI exp(sIu

It

), 0 ≤ ρI < 1. (16)

Jean Blaise Nlemfu M. 14 / 39

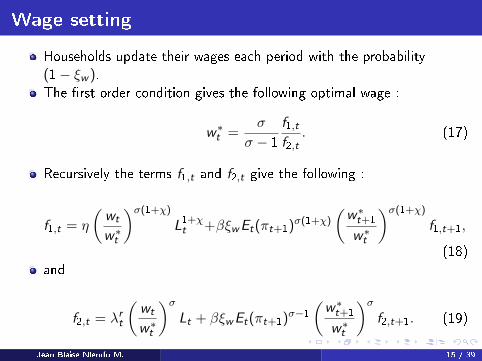

Wage setting

Households update their wages each period with the probability

(1− ξw ).

The �rst order condition gives the following optimal wage :

w∗t =σ

σ − 1

f1,tf2,t

. (17)

Recursively the terms f1,t and f2,t give the following :

f1,t = η

(wt

w∗t

)σ(1+χ)L1+χt +βξwEt(πt+1)σ(1+χ)

(w∗t+1

w∗t

)σ(1+χ)f1,t+1,

(18)

and

f2,t = λrt

(wt

w∗t

)σLt + βξwEt(πt+1)σ−1

(w∗t+1

w∗t

)σf2,t+1. (19)

Jean Blaise Nlemfu M. 15 / 39

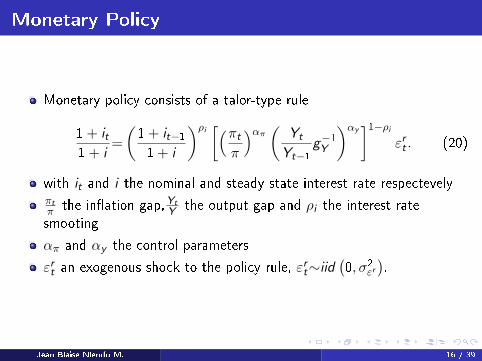

Monetary Policy

Monetary policy consists of a talor-type rule

1 + it1 + i

=

(1 + it−11 + i

)ρi [(πtπ

)απ(

Yt

Yt−1g−1Y

)αy]1−ρi

εrt . (20)

with it and i the nominal and steady state interest rate respectevelyπtπ the in�ation gap,Yt

Y the output gap and ρi the interest rate

smooting

απ and αy the control parameters

εrt an exogenous shock to the policy rule, εrt∼iid(0, σ2εr

).

Jean Blaise Nlemfu M. 16 / 39

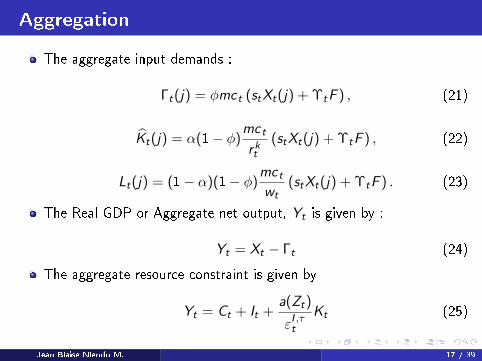

Aggregation

The aggregate input demands :

Γt(j) = φmct (stXt(j) + ΥtF ) , (21)

Kt(j) = α(1− φ)mct

rkt(stXt(j) + ΥtF ) , (22)

Lt(j) = (1− α)(1− φ)mctwt

(stXt(j) + ΥtF ) . (23)

The Real GDP or Aggregate net output, Yt is given by :

Yt = Xt − Γt (24)

The aggregate resource constraint is given by

Yt = Ct + It +a(Zt)

εI ,τtKt (25)

Jean Blaise Nlemfu M. 17 / 39

Outline

1 Introduction

Background

What This Paper Does

Findings

2 The Model

Firms and Price setting

Households and Wage setting

Monetary Policy

Aggregation

3 Calibration

4 Results

Staggered Price-Setting Model

Staggered Wage - Setting Model

Staggered Price-Setting and Staggered Wage-Setting Model

5 Conclusion

Jean Blaise Nlemfu M. 18 / 39

Calibration

Shock and Non-Shock Parameters borrowed from Ascari, Phaneuf and

Sims (2015)

Table: Non-Shock Parameters

β δ α η χ b κ γ20.99 0.025 1/3 6 1 0.7 3 0.05

θ σ ξp ξw φ ρi απ αy

6 6 0.66 0.66 0.61 0.8 1.5 0.2

Table: Shock Parameters

gA gI ρr sr ρI sI ρA sA1.00221−φ 1.0047 0 0.0020 0.95 0.0272 0.95 0.0029

Jean Blaise Nlemfu M. 19 / 39

Moments

Moments borrowed from Ascari, Phaneuf and Sims (2015)

Table: Moments

E (∆Y ) σ(∆Y ) σ(∆I ) σ(∆C ) ρ1(∆Y )

Model 0.0057 0.0078 0.0247 0.0048 0.539

Data (0.0057) (0.0078) (0.0202) (0.0047) (0.363)

σ(Y hp) σ(Chp) σ(I hp) σ(π) ρ1(π)Model 0.0169 0.0089 0.0555 0.0064 0.892

Data (0.0162) (0.0086) (0.0386) (0.0064) (0.907)

Jean Blaise Nlemfu M. 20 / 39

Outline

1 Introduction

Background

What This Paper Does

Findings

2 The Model

Firms and Price setting

Households and Wage setting

Monetary Policy

Aggregation

3 Calibration

4 Results

Staggered Price-Setting Model

Staggered Wage - Setting Model

Staggered Price-Setting and Staggered Wage-Setting Model

5 Conclusion

Jean Blaise Nlemfu M. 21 / 39

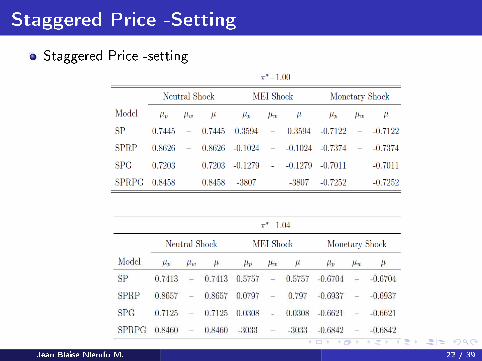

Staggered Price -Setting

Staggered Price -setting

Jean Blaise Nlemfu M. 22 / 39

Staggered Wage -Setting

Staggered wage -setting

Jean Blaise Nlemfu M. 23 / 39

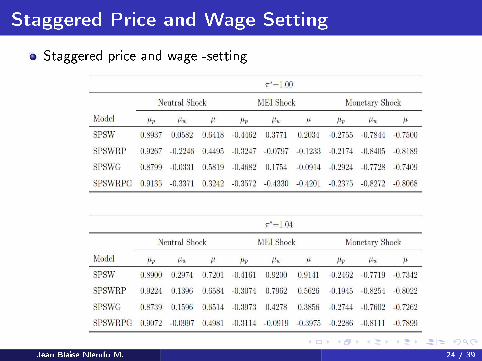

Staggered Price and Wage Setting

Staggered price and wage -setting

Jean Blaise Nlemfu M. 24 / 39

Outline

1 Introduction

Background

What This Paper Does

Findings

2 The Model

Firms and Price setting

Households and Wage setting

Monetary Policy

Aggregation

3 Calibration

4 Results

Staggered Price-Setting Model

Staggered Wage - Setting Model

Staggered Price-Setting and Staggered Wage-Setting Model

5 Conclusion

Jean Blaise Nlemfu M. 25 / 39

Conclusion

This paper analyzes markups cyclical behavior in a positive trend

in�ation medium-scale DSGE model

in a Staggered price-setting and staggered wage-setting model with

imperfect competition and trend in�ation rising from 0 to 4 percent,

wage markup is more important than price markup

The focus on the price markup in the literature is misplaced

More resarch is needed on the role of the wage markup

Jean Blaise Nlemfu M. 26 / 39

TFP Shock vs SPRPG Model

TFP Shock vs SPRPG Model

Jean Blaise Nlemfu M. 27 / 39

TFP Shock vs SWRPG Model

TFP Shock vs SWRPG Model

Jean Blaise Nlemfu M. 28 / 39

TFP Shock vs SPSWRPG Model

TFP Shock vs SPSWRPG Model

Jean Blaise Nlemfu M. 29 / 39

MEI Shock vs SPRPG Model

MEI Shock vs SPRPG Model

Jean Blaise Nlemfu M. 30 / 39

MEI Shock vs SWRPG Model

MEI Shock vs SWRPG Model

Jean Blaise Nlemfu M. 31 / 39

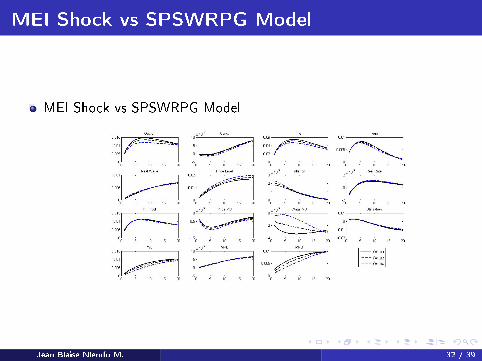

MEI Shock vs SPSWRPG Model

MEI Shock vs SPSWRPG Model

Jean Blaise Nlemfu M. 32 / 39

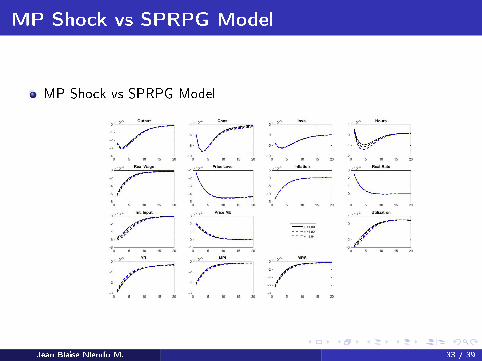

MP Shock vs SPRPG Model

MP Shock vs SPRPG Model

Jean Blaise Nlemfu M. 33 / 39

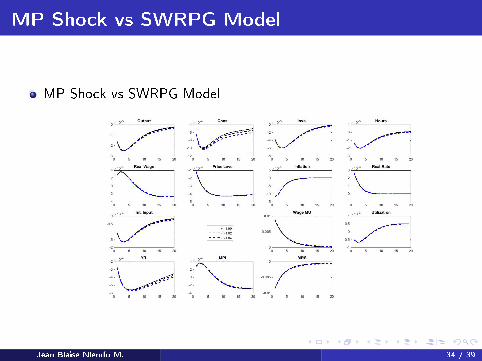

MP Shock vs SWRPG Model

MP Shock vs SWRPG Model

Jean Blaise Nlemfu M. 34 / 39

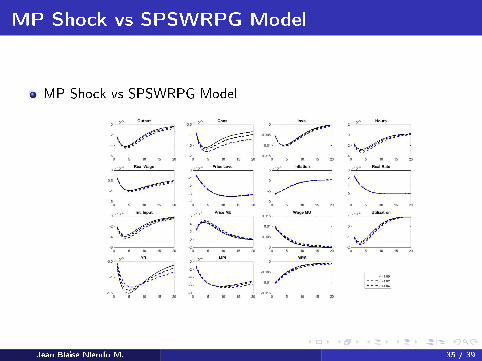

MP Shock vs SPSWRPG Model

MP Shock vs SPSWRPG Model

Jean Blaise Nlemfu M. 35 / 39

MP Shock vs SPSWRPG Model

MP Shock vs SPSWRPG Model

Jean Blaise Nlemfu M. 36 / 39

Staggered Price -Setting (FD �ltered)

Staggered Price -setting

Jean Blaise Nlemfu M. 37 / 39

Staggered Wage -Setting (FD �ltered)

Staggered wage -setting

Jean Blaise Nlemfu M. 38 / 39

Staggered Price and Wage Setting (FD �ltered)

Staggered price and wage -setting

Jean Blaise Nlemfu M. 39 / 39