The lifecycle of a mining project: from exploration through to a Mining Lease application. October 2007 James AH Campbell B.Sc (Hons) ARSM Dipl Datm (UNISA) MBA (Dunelm) FIMMM C.Eng C.Sci Pr.Sci.Nat. Managing Director – African Diamonds plc AK6 AK6 – – A Case Study A Case Study

Transcript

The lifecycle of a mining project: from exploration through to a Mining Lease application.

October 2007

James AH CampbellB.Sc

(Hons) ARSM Dipl

Datm

(UNISA) MBA (Dunelm) FIMMM C.Eng

C.Sci

Pr.Sci.Nat.Managing Director –

African Diamonds plc

AK6 AK6 –– A Case StudyA Case Study

Important NoticeImportant Notice♦

This presentation does not constitute or form part of any offer for sale or solicitation of any offer to buy or subscribe for any securities in African Diamonds plc nor shall it or any part of it form the basis of, or be relied on in connection with, or act as any inducement to enter into, any contract or commitment whatsoever. No reliance may be placed for any purpose whatsoever on the information or opinions contained in this presentation or on any other document or oral statement or on the completeness, accuracy or fairness of any such information and/or opinions. No undertaking, representation, warranty or other assurance, express or implied,

is made or given by or on behalf of African Diamonds plc or any of their respective directors, employees or advisers, as to the accuracy or completeness of the information or opinions contained in this presentation, and (save in the case of fraud) no responsibility or liability is accepted by any of them for any such information or opinions or for any errors, omissions, misstatements, negligence or otherwise contained or referred to in this presentation. The contents of this presentation have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000.

♦

This presentation does not constitute an offer to the public as referred to in section 85 of the Financial Services and Markets Act 2000 (as amended) of the United Kingdom and accordingly has not been nor will it be approved by any competent authority in the United Kingdom. This presentation is

not a prospectus within the meaning of the Prospectus (Directive 2003/71/EC) Regulations 2005 of Ireland and therefore has not been approved by the Irish Financial Services Regulatory Authorities being the competent authority for the purposes of Directive 2003/71/EC in Ireland. This presentation is not an offering document for the purposes of section 49 of the Investment Funds, Companies and Miscellaneous Provisions Act 2005 of Ireland.

♦

This Presentation has been prepared by the Directors of African Diamonds plc and is being issued solely to and directed at persons who have professional experience in matters relating to investments falling within Article 19(1)(a) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 ("FPO") or (b) high net worth entities and other persons to whom the presentation may otherwise lawfully be communicated, falling within Article 49(1)(a) of the FPO (all such persons together being referred to

as "Relevant Persons"). In consideration of the receipt of the presentation each recipient warrants and represents that he or it is a person falling within that description. Delivery of this information to any other person or reproduction, in whole or in part, without the prior consent of African Diamonds plc is prohibited.

♦

This information is being supplied to you, in whole or in part, for information purposes only and not for any other purpose. In particular, the distribution of this document in jurisdictions other than United Kingdom or Ireland may be restricted by law and persons into whose domain this document comes should inform themselves about, and observe, any such restrictions. Any failure to comply with these restrictions may constitute a violation of laws of any such other jurisdictions.

AgendaAgenda

♦

Why diamonds?♦

Birth of African Diamonds plc

♦

The deal with De Beers♦

Location, Location, Location

♦

How leading-edge technology re-started the exploration clock

♦

Modern approaches to diamond resource assessment♦

Parallel technical studies

♦

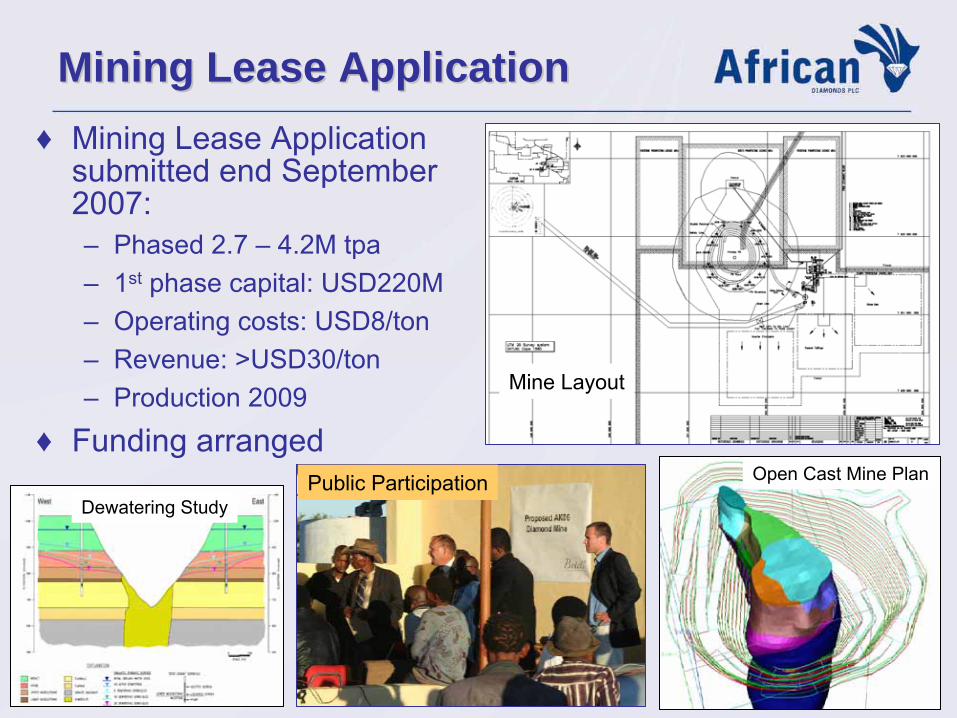

Mining Lease application♦

A note on company valuations during the different phases of project development

♦

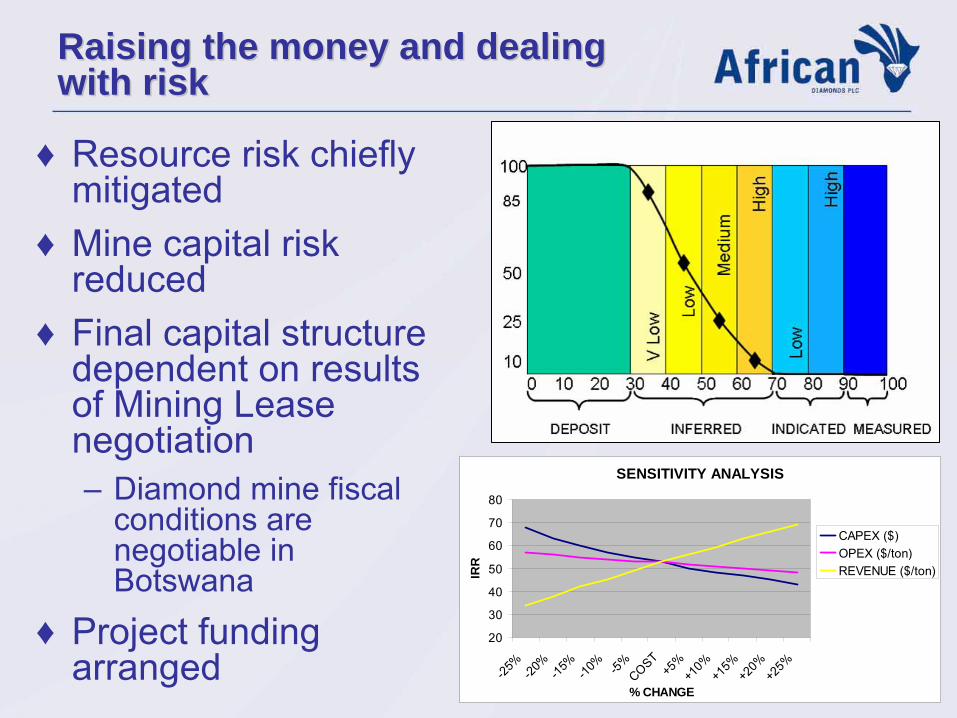

Raising the money and dealing with risk♦

Rewarding the shareholders

Why diamonds?Why diamonds?

♦

Retail market remains strong (6-7% p.a.)

♦

Low growth in supply (2-3% p.a.)

♦

Growing gap between supply and demand, particularly in the larger better quality goods:

♦

Few large primary diamond resource discoveries

♦

Long lead times on mine development

♦

Upward pressure on rough and polished prices

Reproduced with kind permission of WWW International Diamond Consultants Ltd & Allan Hochreiter Pty Ltd

Birth of African DiamondsBirth of African Diamonds

African Diamonds PLC successful placing and admission to AIM14 July 2003

African Diamonds plc (AFD.L), the Dublin-based diamond exploration and mining venture, is pleased to announce that it has successfully raised £800,000 (£659,000 net of expenses) through a Placing of 11,428,571 Ordinary Shares at 7p per share, valuing African Diamonds at £3.8 million. Shares begin trading today, 14 July 2003, on the Alternative Investment Market (AIM).

John Teeling, Executive Chairman of African Diamonds, said: "African Diamonds is an exciting venture that has taken an important

step forward today with the admission to the stock market. Despite the tough economic times of recent years, gemstones, as targets, have continued to grow in demand and value."

"We are fortunate to have the ground, the people, the skills and now the finance to give us a real opportunity to reach our goal of having a fully operational gemstone mine within three years."

The deal with De BeersThe deal with De BeersAfrican Diamonds partners with De Beers in Botswana22 April 2004

African Diamonds (AIM: AFD) and De Beers have signed an agreement to establish a joint venture company to explore for, and if successful, develop new diamond mines in Botswana. The agreement, which is subject to the approval of the relevant authorities, covers the current African

Diamonds licences in the country, as well as certain De Beers licences in the Orapa area. There are 29 known kimberlites on these licences of which 21 are located within the African Diamonds licence area. De Beers has an extensive database relating to the geology of the Orapa area, as well as specific information relating to the kimberlites and recent geophysical work suggests that certain of these may be larger than previously thought. This information will be made available to the joint venture company and a detailed intensive work programme managed by De Beers will commence immediately.

The initial focus of the work will be on specific highest potential targets among the kimberlite pipes on the licences around Orapa. Work on the 1,000 sq km licence north of the Orapa

mine will commence in 2004 by airborne and ground geophysics and by the use of exploration techniques exclusive to De Beers. A similar programme is planned for the Serowe licence currently held by African Diamonds, 120 km south east of Orapa. Work done to date by African Diamonds has indicated the possibility that new undiscovered kimberlites may exist at Serowe. Advancing this project to kimberlite discovery is the focus of exploration efforts in 2004.

Ownership of the joint venture will initially be 49% African Diamonds and 51% De Beers with De Beers funding the joint venture through to bankable feasibility study. De Beers' shareholding will rise to 70% upon completion of the first bankable feasibility study. The size of any mine resulting from the joint venture will decide whether it is managed by De Beers or African Diamonds with larger mines operated by De

Beers and those below an agreed threshold operated by African Diamonds, who will receive a preferential profit share in those operations of Newco.

John Teeling, Chairman of African Diamonds said, "This is an outstanding opportunity for African Diamonds. We know that we have good ground in Botswana and our exploration to date has produced a number of specific targets. As a result, we had interest from a number of potential partners, but none can match De Beers. They have unrivalled knowledge of diamonds and a wealth of exploration data built on forty years experience and commitment to Botswana. Their exploration expertise is the most advanced in the world and they have large full time exploration teams on the ground. African Diamonds management team will be actively involved in the programme on a consultancy and advisory basis. The Serowe and Orapa north licences will be explored with De Beers' proprietary cutting edge technology and with the use of specialist airborne techniques such as Bell Geospace.

We believe that our ground has the potential for large gem quality mines - and they will be the targets of our joint venture.

The potential in Botswana, already the worlds leading gem quality diamond producer, is immense. We are fortunate to have obtained excellent ground on which we have good exploration results. We now have a partner with the resources to realise the potential on our licences. This combination offers an exciting future".

The 3,743 km2 yellow ground is the AFD/DB joint venture. Of the 70+ diamondiferous kimberlites in the Orapa area, the AFD/DB joint venture control 34 with outstanding applications for additional pipes.

AK6

How leading edge technology How leading edge technology restarted the exploration clockrestarted the exploration clock

♦

AK6 discovered by De Beers in 1969 from follow-up of geophysical surveys

–

Declared to be low interest due to small size (c.3.3 ha Figure 1) and a preliminary assessment of the diamond grades (3cpht).

♦

The area was revisited in 1998 due to improved exploration technologies: geophysical surveys and drilling undertaken (Figure 2)

♦

2003/2004: 100-tonne (5 x 12”

holes) bulk sampling across kimberlite to test for macro-

diamonds:

–

Modeled global grade of 25cpht & diamond value of US$138/ct (+1mm)