The author hereby grants to MUST permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part.

Signature of Author __________________________________________________________ Department of Transportation

August 2004

Certified by ______________________________________________________________ Dr. Leong Choon Heng

Accepted by ________________________________________________________________ Dr. Leong Choon Heng

Department of Transportation Head of MSc Transportation and Logistics

- i -

The Development of Third Party Logistics in Malaysia: An Overview

By

Salina binti Umar

Submitted to the Department of Transportation and Logistics in Partial Fulfillment of the requirements for the Degree of Master of Science in

Transportation and Logistics

Abstract The main objective of this thesis is to study the progress of local third party logistics (3PL) providers and analyze its development in Malaysia. The study takes into account the increasing demand for comprehensive 3PL services and capable 3PL providers, responses by 3PL providers to that demand, problems faced by the logistics industry and incentives provided by the Malaysian Government to promote the industry. The approach, concept and framework for this thesis are developed and based principally on the works of Susanne Hertz and Monica Alfredsson (2003), and M. S. Sohail and A. S. Sohal (2003). Based on the findings of the case studies, comparisons were made on 3PL classifications, relationships between 3PL providers and users and services offered. A mail survey was also carried out to strengthen the findings from the case studies. The study found that the majority of 3PL providers in Malaysia are still of the standard 3PL type, offering mainly traditional services such as transportation, warehousing and customs clearance.

ii

Acknowledgement I wish to thank everyone who helped me go through the Master of Science in Transportation and Logistics program for the past 2 years. Special thanks to Dr. Leong Choon Heng for pushing me to complete this thesis and to Chin, Sook Yeen, Saravanan, Chew, Visha and Yanti for sharing my anxiety. I would also like to express my appreciation to the Ministry of Science, Technology and Innovation for giving me the opportunity to gain invaluable knowledge in this field. Thank you so much! Sincerely, Salina Umar CA, CPA (Malaysia & Australia), CFP.

Table of Contents..........................................................................................................iii

List of Figures ...............................................................................................................vi

List of Tables ...............................................................................................................vii

1 Introduction........................................................................................................1 1.1 Malaysian Economy............................................................................2 1.2 Thesis Approach .................................................................................4 1.3 3PL Issues in Malaysia .......................................................................6

2 The Research Methodology and Theoretical Framework..................................8 2.1 The Research Approach......................................................................8 2.1.1 Qualitative Study ................................................................................8 2.1.2 Methods for Collecting Data...............................................................8 2.1.2.1 Literature Review................................................................................8 2.1.2.2 Interviews............................................................................................9 2.1.2.3 Survey ...............................................................................................10 2.2 Theoretical Framework.....................................................................14 2.3 Financial Performance ......................................................................14 2.4 Definitions of Central Concepts and Terms......................................14

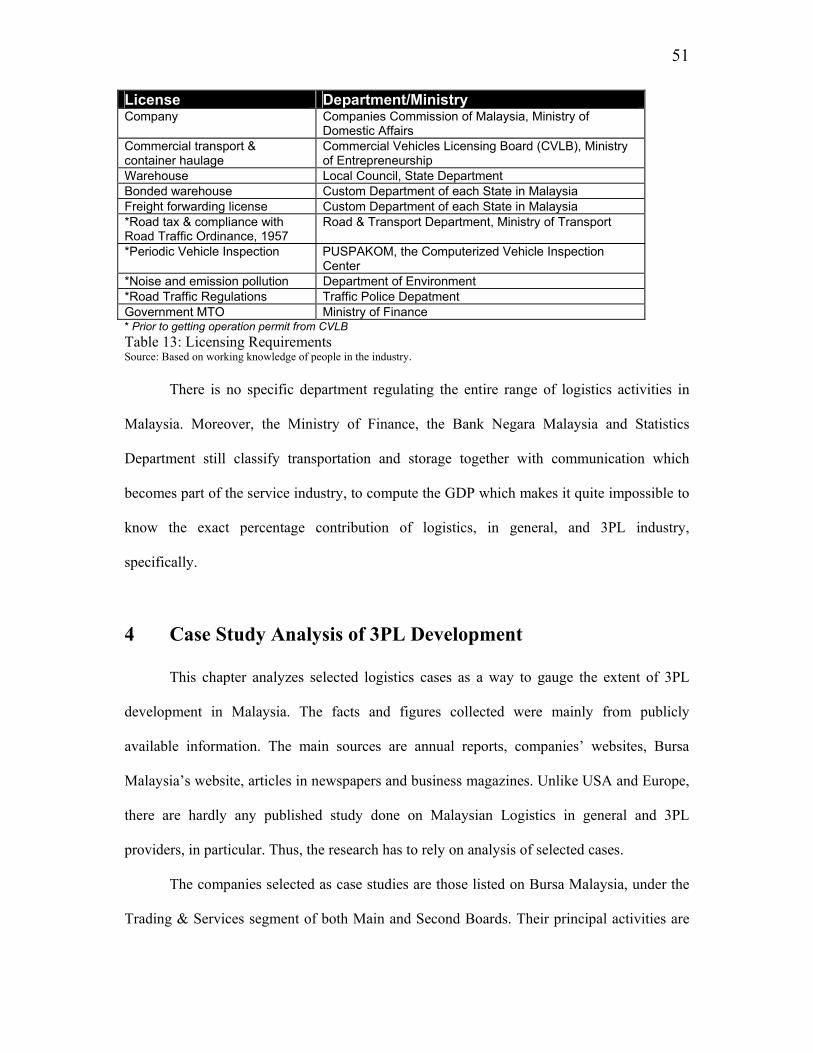

3 Literature Review.............................................................................................19 3.1 Industry Environment .......................................................................19 3.2 Third Party Logistics Development in Europe .................................20 3.3 Third Party Logistics Development in the USA...............................24 3.4 Studies on Malaysia ..........................................................................30 3.4.1 Review of Commissioned Studies ....................................................30 3.4.2 Review of Other Studies and Journal Articles..................................34 3.4.3 Sea.....................................................................................................38 3.4.4 Land Transport..................................................................................40 3.4.4.1 Conventional Truck ..........................................................................40 3.4.4.2 Container Haulage ............................................................................41 3.4.4.3 Rail....................................................................................................43 3.4.5 Air Cargo ..........................................................................................44 3.4.6 Freight Forwarding Services.............................................................46 3.4.6.1 Government-Appointed Multimodal Transport Operators (MTO)...47 3.4.7 Licensing Requirements....................................................................50

4 Case Study Analysis of 3PL Development......................................................51

4.1.1 History and Business.........................................................................55 4.1.2 Financial Highlights..........................................................................57 4.2 Integrated Logistics Berhad (ILB): ‘A Leader in Total Logistics’ ...57 4.2.1 History and Business.........................................................................58 4.2.2 Financial Highlights..........................................................................60 4.3 Konsortium Logistik Bhd (Konsortium/KLB): ‘A Logistics

Solutions Provider’ ...........................................................................60 4.3.1 History and Business.........................................................................61 4.3.2 Financial Highlights..........................................................................63 4.4 Malaysia International Shipping Corporation Berhad (MISC):

‘The Preferred Provider of World-Class Maritime Transportation and Logistics Services’ .....................................................................65

4.4.1 History and Business.........................................................................65 4.4.2 Financial Highlights..........................................................................68 4.5 Tiong Nam Transport Holdings Berhad (TiongNam/TNH):

‘Total Logistics Provider’ .................................................................69 4.5.1 History and Business.........................................................................69 4.5.2 Financial Highlights..........................................................................70 4.6 Century Logistics Holdings Bhd (Century/CLB): ‘Your Total

Logistics Partner’ ..............................................................................71 4.6.1 History and Business.........................................................................71 4.6.2 Financial Highlights..........................................................................73 4.7 Nationwide Express Courier Services Berhad (Nationwide/NW):

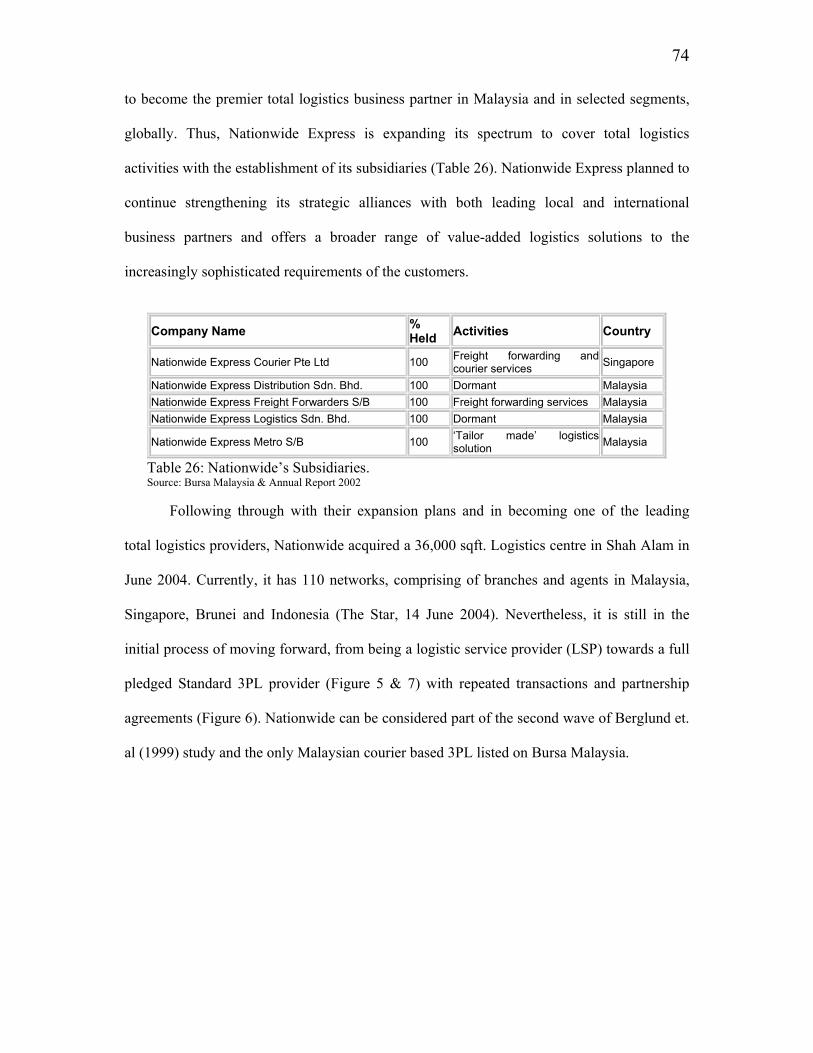

‘We Are More Than A Courier Company’.......................................73 4.7.1 History and Business.........................................................................73 4.7.2 Financial Highlights..........................................................................75 4.8 See Hup Consolidated Berhad (See Hup/SHC). ...............................75 4.8.1 History and Business.........................................................................75 4.8.2 Financial Highlights..........................................................................76 4.9 Tamadam Bonded Warehouse Berhad (Tamadam/TBW):

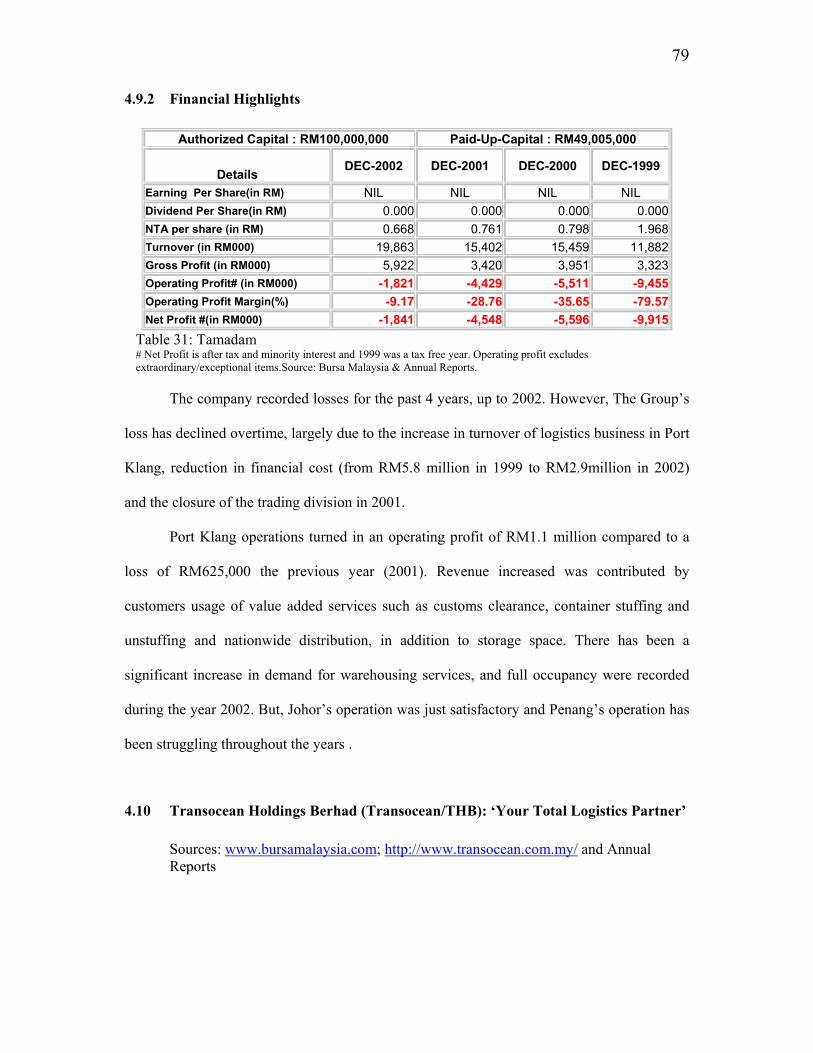

‘Providing the Most Efficient and Reliable Logistics Solution to Connect You to the World’...............................................................77

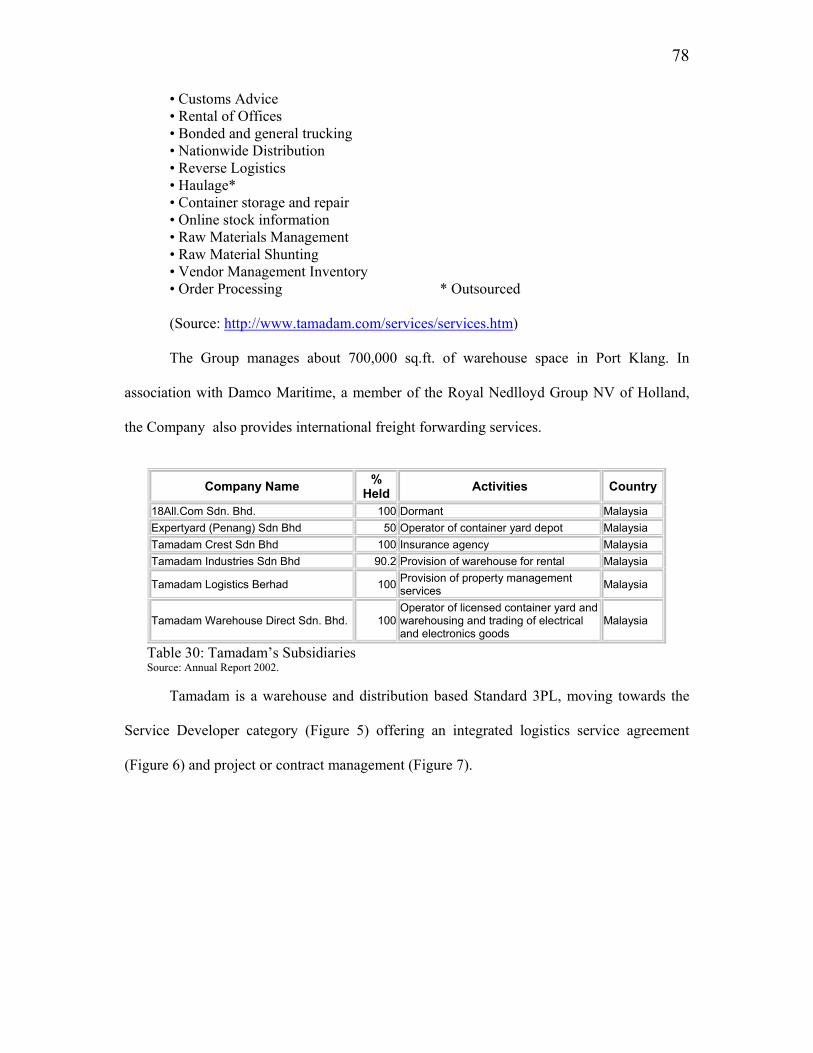

4.9.1 History and Business.........................................................................77 4.9.2 Financial Highlights..........................................................................79 4.10 Transocean Holdings Berhad (Transocean/THB): ‘Your Total

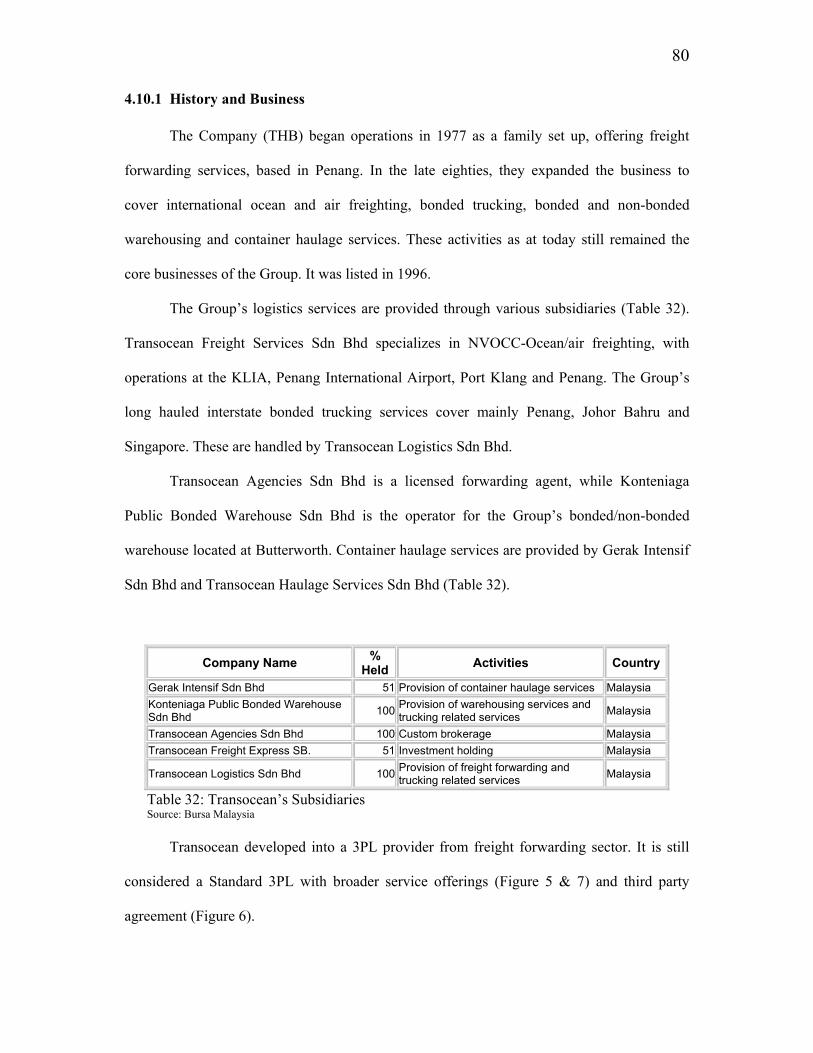

Logistics Partner’ ..............................................................................79 4.10.1 History and Business.........................................................................80 4.10.2 Financial Highlights..........................................................................81 4.11 Summary ...........................................................................................81

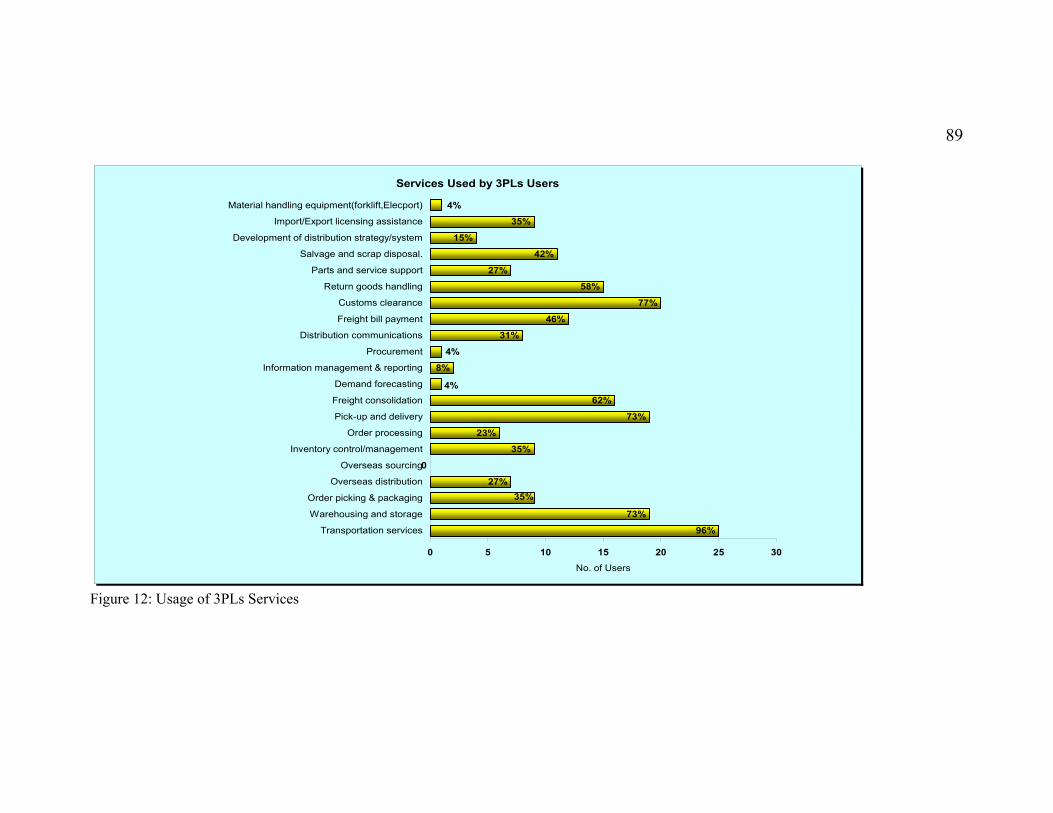

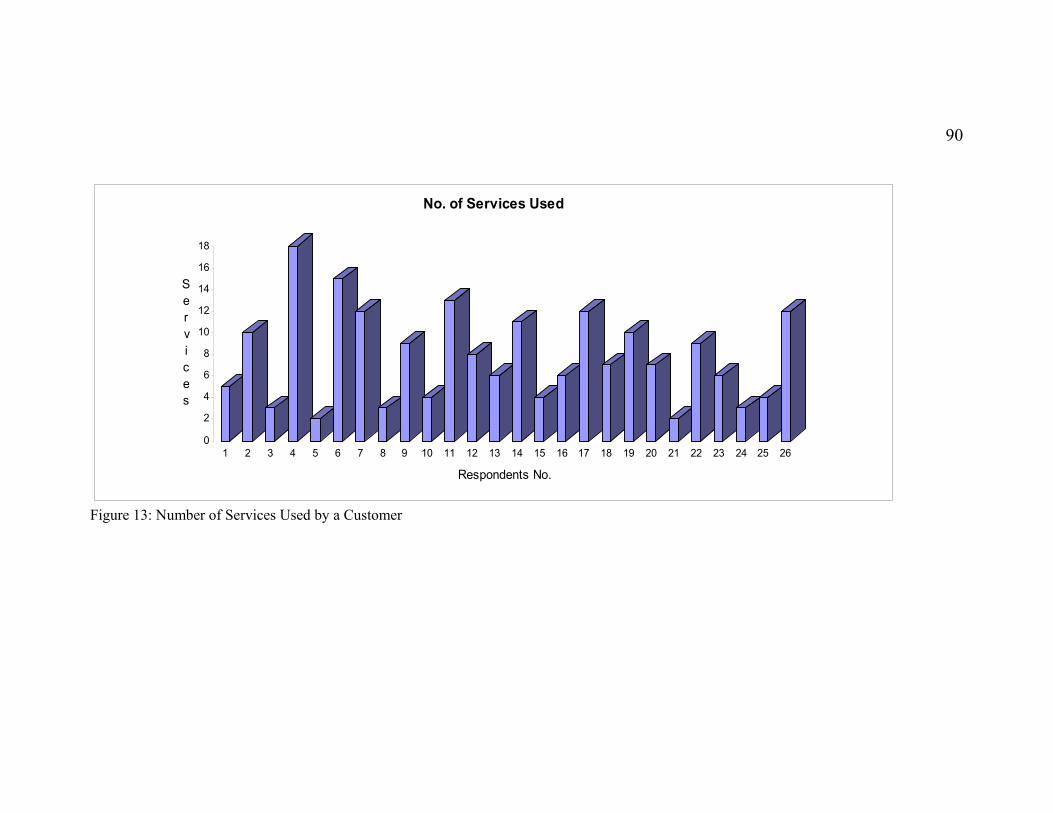

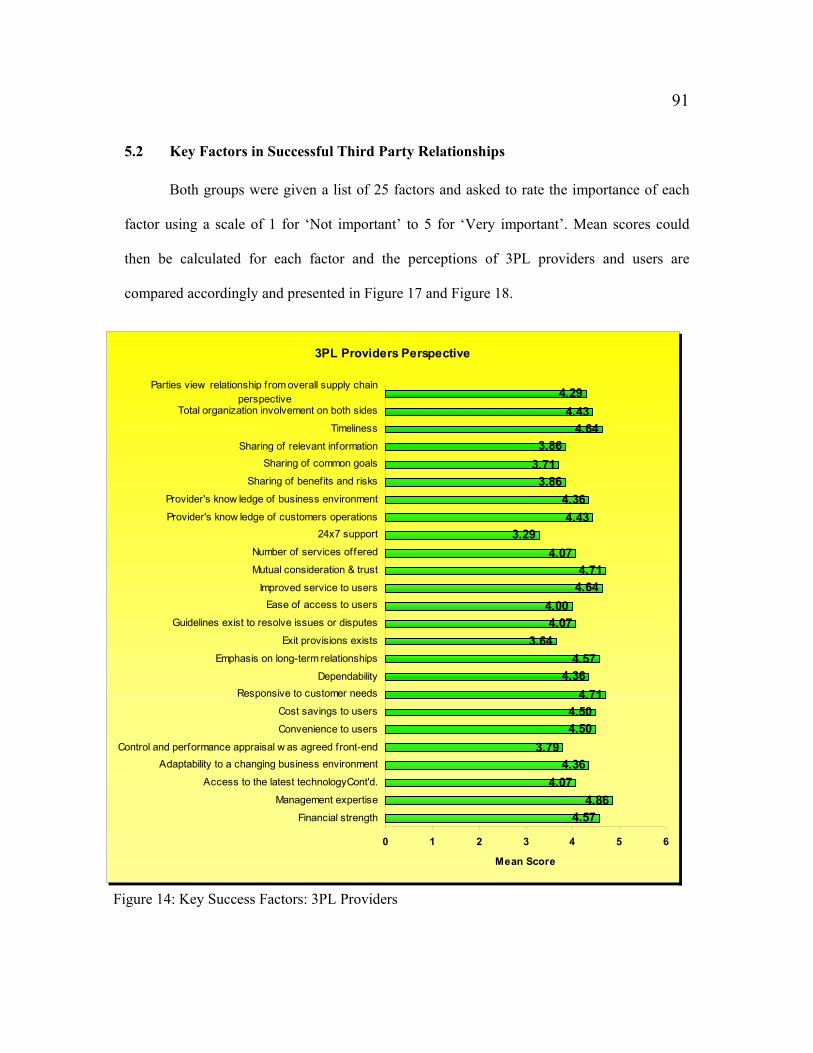

5. The Survey of 3PL Users and Providers..........................................................84 5.1 Services Offered and Used................................................................85 5.2 Key Factors in Successful Third Party Relationships.......................91 5.3. Overall Satisfaction with 3PL Relationships ....................................93

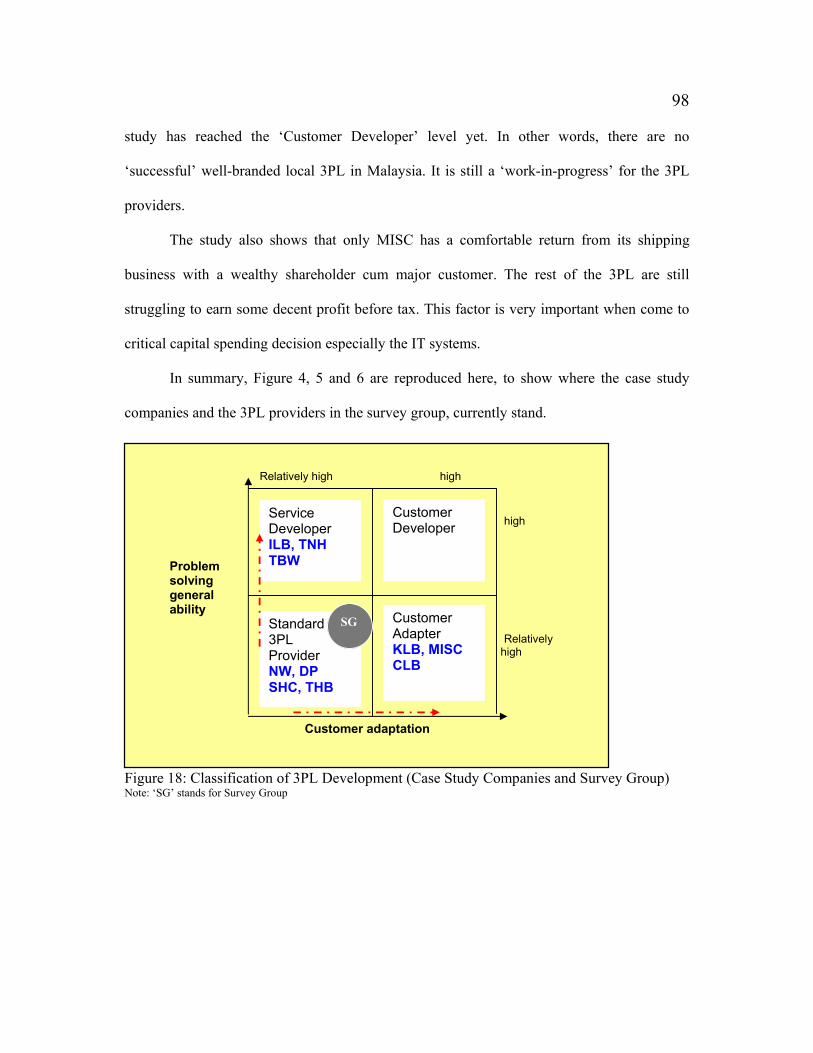

6. Conclusion .......................................................................................................95 6.1 Current Industry Scenario .................................................................95

v

6.1.1 The Evolution....................................................................................95 6.1.2 Services Provided..............................................................................97 6.1.3 Challenges.......................................................................................100 6.1.4 The New Road to Success...............................................................101

Bibliography ..............................................................................................................102 APPENDIX A: Tax Incentives for Integrated Logistics Service Providers APPENDIX B: Survey Listing for 3PL Users APPENDIX C: Survey Listing for 3PL Providers APPENDIX D: Survey Questionnaires APPENDIX E: Cover Letters

vi

List of Figures FIGURE 1: MAP OF MALAYSIA ....................................................................................................1 FIGURE 2: THE APPROACH ..........................................................................................................5 FIGURE 3: GROSS REVENUE BY INDUSTRY - 3PL IN THE USA ..................................................11 FIGURE 4: EUROPE 1996 - OUTSOURCED LOGISTICS .................................................................20 FIGURE 5: 3PL CLASSIFICATIONS .............................................................................................22 FIGURE 6: RELATIONSHIPS BETWEEN 3PL PROVIDERS AND USERS............................................25 FIGURE 7: THIRD PARTY LOGISTICS’ VARIANCES.....................................................................26 FIGURE 8: 3PL MARKET GROSS REVENUE GROWTH (USD BILLION).......................................27 FIGURE 9: LOGISTICS FLOW ......................................................................................................37 FIGURE 10: RESPONDENTS’ CHOICE..........................................................................................85 FIGURE 11: PROVISION OF 3PLS SERVICES ...............................................................................88 FIGURE 12: USAGE OF 3PLS SERVICES .....................................................................................89 FIGURE 13: NUMBER OF SERVICES USED BY A CUSTOMER .......................................................90 FIGURE 14: KEY SUCCESS FACTORS: 3PL PROVIDERS..............................................................91 FIGURE 15: KEY SUCCESS FACTORS: 3PL USERS .....................................................................92 FIGURE 17: THE USERS .............................................................................................................94 FIGURE 18: CLASSIFICATION OF 3PL DEVELOPMENT (CASE STUDY COMPANIES AND SURVEY

GROUP)...................................................................................................................98 FIGURE 19: RELATIONSHIPS BETWEEN 3PL PROVIDERS AND USERS OF THE CASE STUDY

COMPANIES AND SURVEY GROUP. ..........................................................................99 FIGURE 20: SERVICE OFFERINGS OF THE CASE STUDY COMPANIES AND SURVEY GROUP ........99

vii

List of Tables Table 1: Previous 3PL Surveys..................................................................................13 Table 2: Types Of 3PL Providers...............................................................................25 Table 3: 3PL By The Numbers In The USA For 2002 ..............................................28 Table 4: North American-Based 3PL Revenues: Net Revenue For 2002 Of More

Than Usd500 Millions..................................................................................29 Table 5: Container Transportation Chain Study 1996-Summary Of Findings ..........32 Table 6: Top 10 Malaysian Shipowners.....................................................................39 Table 7: The 5 Major Container Haulage Providers ..................................................41 Table 8 : Roles And Functions Of CHAM .................................................................41 Table 9: Number Of Licensed Container Haulage Companies..................................42 Table 10: Number Of Permits Issued For Prime-Movers And Trailers.......................42 Table 11: Total Containers Hauled (In Teus) ..............................................................43 Table 12: Government Appointed Mtos ......................................................................50 Table 13: Licensing Requirements ..............................................................................51 Table 14: Diperdana - Subsidiaries..............................................................................56 Table 15: Diperdana.....................................................................................................57 Table 16: Ilb-Subsidiaries ............................................................................................59 Table 17: Ilb.................................................................................................................60 Table 18: Klb-Subsidiaries And Associated Companies .............................................63 Table 19: Klb ...............................................................................................................64 Table 20: Misc-Subsidiaries And Associated Companies ...........................................68 Table 21: Misc .............................................................................................................68 Table 22: Tiong Nam’s Subsidiaries & Associate Companies....................................69 Table 23: Tiong Nam...................................................................................................70 Table 24: Century’s Subsidiaries And Associated Companies....................................72 Table 25: Century ........................................................................................................73 Table 26: Nationwide’s Subsidiaries. ..........................................................................74 Table 27: Nationwide...................................................................................................75 Table 28: See Hup’s Subsidiaries And Associated Companies...................................76 Table 29: See Hup........................................................................................................77 Table 30: Tamadam’s Subsidiaries..............................................................................78 Table 31: Tamadam .....................................................................................................79 Table 32: Transocean’s Subsidiaries ...........................................................................80 Table 33: Transocean...................................................................................................81 Table 34: Services Provided By Local 3PL Providers In Malaysia.............................83 Table 35: Most Commonly Offered And Used Services .............................................86 Table 36 : Evolution Of 3PLs In Malaysia ..................................................................97

1

1 Introduction

Malaya acquired its independence from Britain in 1957. In 1963, Malaysia was

created through the merging of Malaya and the former British Singapore, Sabah and

Sarawak. However, Singapore separated from the union in 1965. Economically, it has a

strategic location along the Straits of Malacca and the southern part of the South China Sea.

Figure 1: Map of Malaysia Source: website of the United Nations Development Programme (UNDP).

The transport industry in Malaysia, comprising of land, sea, air and pipelines has gone

through numerous changes especially in the 1990s in terms of infrastructure facilities,

operators, equipment, manpower and operating systems. Nevertheless, there was no cohesive

and comprehensive transport policy guiding the industry, but some mode-specific policy

statements were made on ad hoc basis. Two main contributors to the development of the local

transport industry are industrialization and international trade. These two key factors are

complementary in nature and created the necessary demand for transportation and logistics

services.

2

1.1 Malaysian Economy

The Malaysian economy in the 1950s and 1960s was agro-based, dominated by

rubber, palm oil, pepper and timber. In 1970, the agricultural sector contributed 30.9% to the

GDP compared to only 14.8% from manufacturing. The growth in manufacturing sector

began in the sixties and accelerated with introduction of the Investment Incentives Act, 1968

and promotion of the free trade zones (FTZ) in 1971. These incentives managed to attract

many multinational corporations (MNC) to establish export oriented operations supported by

competitive wage, good infrastructure facilities and economically and politically stable

environment.

In the early 1980s, the Government took several measures to develop selected heavy

industries such as iron and steel, petrochemicals, cement and automobile with the objective of

strengthening the industrial base and further develop our capabilities in manufacturing sector.

As a result, the manufacturing sector’s share in GDP rose to 33.1% in 1995.

The policy framework laid by the Industrial Master Plan (IMP) and the subsequent

liberation and deregulation of the economy after the recession in mid 1980s, provided the

foundation for rapid growth of manufacturing sector. It became the lead sector in 1987 when

its’ share of GDP rose to 22.6%, surpassing agricultural sector’s share of 21.7%. In 2003, it

has stabilized around 30% and estimated to stay between 30 to 31 percent for 2004. (Bank

Negara Malaysia, 2003)

It is difficult to foresee a far greater share of the economy, coming from

manufacturing. Based on the economic structure of developed countries, the next phase of

economic expansion has to come from the service sector that includes transportation and

logistics. Between 1990 and 2000, world services output was reported to have grown by 2.9%

and the share of services in world GDP expanded from 57% to 64% over the decade (World

3

Bank, 2001). In the case of Malaysia, the services sector expanded to 57% of GDP in 2002

(Ministry of Finance, 2003).

With the progressive realization of ASEAN Free Trade Area (AFTA), economic

integration in Southeast Asia and in the broader East Asia Region is making headway.

Companies have started establishing their manufacturing facilities in one or several ASEAN

countries and developing their distribution channels throughout ASEAN. For example, in

order to capture and support the ASEAN market, Volvo has set-up two plants in the region.

Both plants assemble similar models but some of the ‘work-in-progress’ cars from Volvo

Malaysia are sent to Volvo Thailand to be completed (The Star, 14 June 2004). As a result,

they require increasingly complex cross border supply chain management capabilities i.e.

financially strong and capable third party logistics (3PL) providers.

Moreover, “a new set of international trading disciplines for services under the

General Agreement on Trade in Services (GATS) and the World Trade Organization (WTO)

would make ASEAN, in general, and Malaysia, specifically, a target for investments as well

as an export market for multinational and global providers of services, including logistics

services. These global providers are highly competitive. On the other hand, Malaysian

services industries have not been brilliant as exporters due to capacity constraints,

technological backwardness and insufficient capitalization” (Sieh Lee, 2003).

The Government1 is aware of these increasing demands, competition and problems

faced by the logistics industry and have put in place the necessary infrastructure and

incentives to stimulate greater private sector initiatives to spearhead the logistics industry.

For example, apart from improving the basic logistics infrastructure such as roads, highways,

seaports and airports, the government initiated the multimodal transport operator (MTO)

status with the view of creating Malaysian 3PL providers. (This will be elaborated in Chapter

3).

4

Additionally, it provides tax incentives with a view of creating a more business-friendly

environment as well as facilitating the private sector to reduce their cost of doing business.

(Please refer to Appendix I for details). Given the context of the globalization of services and

growing competition in the logistics sector, this thesis aims to study the progress of local 3PL

and analyze its development in Malaysia and ability to compete, taking into account the

above-mentioned scenario.

1.2 Thesis Approach

There are numerous studies conducted and papers written on the development of

logistics industry and, specifically, the 3PL industry in the USA and Europe. Based on the

studies, we can conclude that the 3PL industry has gone through an evolution path. (This will

be covered under the literature review section later). Third party logistics (definitions are

given in the next chapter) form part of the Malaysian transportation industry. Like other

sectors, it is currently undergoing intense competition. Hence, the purpose of this thesis is to

explore the 3PL development in Malaysia and to examine whether the current environment

and strategies contribute positively to the development of 3PL. A comparison will also be

made with the USA and European experience.

In order to understand the concepts of 3PL and the global and local logistics scenario,

extensive literature review was done prior to the thesis proposal. The sources include

transportation journals2, global and local 3PL providers’ annual reports, theses on logistics

done at MIT and other universities, news articles in magazines and newspapers, websites and

a number of logistics and research books. In addition, a site visit to the IKEA Distribution

Center in Shah Alam, Selangor, was made to learn about the advantages and disadvantages of

using a 3PL provider as well as looking at the warehouse operation. Maersk Logistics

Malaysia Sdn Bhd is the 3PL provider for IKEA. It has operated IKEA’s Asia Distribution

Centers since 1999. A seminar given by Mr. J.J Ong from MasKargo, the freighting arm of

5

Chapter 1 STUDY OBJECTIVES & PROBLEM ANALYSIS

Chapter 2 RESEARCH

METHODOLOGY, DATA COLLECTION & THEORETICAL FRAMEWORK

Chapter 3 LITERATURE

REVIEW

Chapter 4 CASE

STUDIES

Chapter 6 CONCLUSION

Chapter 5 THE SURVEY

RESULT

Malaysia Airlines Berhad, provided useful insights into 3PL operations for air cargo. These

site visits and seminar contributed positively to the understanding of 3PL’s operations in

Malaysia.

This thesis is structured as follows: Chapter one deals with the introduction to

Malaysia, study objectives and problem analysis. The research methods, theoretical

framework and definitions of relevant concepts and terms are presented in chapter two.

Following that, the third chapter covers literature review on global scenario of 3PL industry,

specifically looking at Europe and the USA scenario and trends and issues in the Malaysian

3PL industry. The fourth chapter put forward the Malaysian case studies, and the fifth,

analyzes the survey result. Finally, the observations and conclusion of the paper are presented

in the last chapter. For easier understanding, a diagram for the thesis approach is presented

below:

Figure 2: The Approach

6

1.3 3PL Issues in Malaysia

Nowadays, managing change is the name of the game. Managers and owners of 3PL

providers need to be on alert and flexible enough to maneuver in a new direction when

challenged by changing market conditions, customers’ behavior and global or internal

business rulings, to name a few.

The introduction of ‘outsourcing’ concept had uplifted the importance of 3PL

industry. The manufacturers, especially, had realized the need to focus on their principal

activities and let the 3PL providers handle the logistics activities. At the start, only

transportation was outsourced but, nowadays, the whole logistics activities can be outsourced.

Majority of 3PL providers in Malaysia are small and medium sizes operators,

servicing the local area around major ports in Malaysia such as Port Klang, Port of Tanjung

Pelepas and Pasir Gudang, Penang Port, Kuantan Port and Bintulu Port. Co-existing with

these 3PL providers are the larger players listed on Bursa Malaysia (formerly known as Kuala

Lumpur Stock Exchange) and the global providers. Majority of the big local 3PL providers

are subcontracting to the smaller players some part of the logistics services e.g. conventional

transportation, warehousing service and equipments. This arrangement will provide

additional capacity to 3PL providers without having to spend substantial capital outlay and at

the same time provide a steady income to the subcontractors.

The main question that will be explored here is whether the 3PL development in

Malaysia will produce a strong 3PL sector or not. Associated with this central theme are the

following questions:

• What has been the trend in 3PL development in Malaysia?

• Was the development comparable to the USA and Europe?

• Which approach has the 3PL providers chosen in order to grow?

7

• Were they influenced by their customers in implementing their strategy of expanding

their business?

• Are there any local 3PL providers that will emerge as global players?

The thesis will address these issues.

8

2 The Research Methodology and Theoretical Framework

2.1 The Research Approach

The study relies heavily on disclosed and published materials such as logistics firms’

annual reports, journals, newspapers and business magazines articles, published reports

produced by consultants and special studies and reports commissioned by the Malaysian

Government. In addition, the study also relies on information provided by the 3PL users, 3PL

providers, industry experts and practitioners by means of survey and unstructured interviews.

2.1.1 Qualitative Study

Qualitative study is more appropriate for this research because the main research

problem of this thesis involves a lot of information that cannot be quantified such as the

companies’ strategies, differentiation of services offered and unique features of companies.

Nevertheless, some quantitative comparison will be made wherever possible using data

obtained from the questionnaire survey.

2.1.2 Methods for Collecting Data

The main methods used to collect data are literature review, interviews and a postal

survey.

2.1.2.1 Literature Review

Collecting vast amounts of information regarding global and local 3PLs through

literature review and compiling it into a meaningful form, which create the foundation for

further analysis, is almost the only way to cover such a broad subject in the allotted time.

Unpublished information and financial data needed for this thesis are hard to obtain directly

from the companies and are confidential in nature for commercial reasons.

9

Furthermore, gaining access to key decision makers and management in the 3PLs

across Malaysia is not feasible due to the time and economic constraint of this study. Even if

it might be possible to gain access to this level of personnel, it is certain that their corporate

positions will influence their views. Here, the data collected give a much more objective view

based on information that is publicly available and can be compared with various additional

sources to ensure its soundness and reliability.

Due to the time and cost factors and not to mention its convenience, government and

company websites as well as news information on the internet are important sources of data

throughout this study. Business magazines, newspapers and personal websites on related

subjects also provided differing views from various perspectives, which at times questioned

the corporate reasoning behind a certain decision taken up by companies concerned. Overall,

the collection of facts and figures from the annual reports of companies, their websites,

interviews, journals, newspaper and magazine articles form the backbone of the research and

the profiling of 3PL cases.

2.1.2.2 Interviews

Part of the study deals with the identification of similarities and differences between

local 3PL providers and international 3PL providers whereby strengths and inadequacies in

local 3PL providers could be identified.

A part of this process involves interviewing and testing the findings against the

learned opinions of people in selected positions that deal with the issues in question. These

interviews serve as a feedback and check on the thoughts and findings of the researcher. The

approach was not to conduct an in-depth research of a particular corporate function but to

concentrate on the overall corporate directions and dominant factors influencing its activities.

Interviews were made with selected industry experts and practitioners to get their

views on 3PL industry in Malaysia. Personnel from the following organizations were kind

10

enough to be interviewed on an informal basis (the information given was general industry-

wide comments and not company-specific):

1. Container Hauliers Association of Malaysia (CHAM);

2. Konsortium Logistik Berhad (KLB);

3. DHL Malaysia;

4. Westprise Sdn Bhd which provides trucking and haulage services to 3PL

providers (a subcontractor);

5. Multimodal Freight Sdn Bhd;

6. TNT;

7. BAX Global;

8. Linfox Logistics Sdn Bhd; and

9. MISC Agency Sdn Bhd.

2.1.2.3 Survey

The survey is one of the most common ways to collect data. Mail survey can be cost

effective compared to other methods even after taking into account the low rate of response.

To enhance empirical evidence, a mail survey was carried out to find out the providers’ and

customers’ views and experiences in providing or using 3PL services.

1. One hundred and fifty cover letters and questionnaires with postage-paid return

envelopes were sent to 150 companies that are most likely users of 3PL services,

selected from the Technology, Consumers, Industry and Trading segments of the

Main Board of Bursa Malaysia, plus the Federation of Malaysian Manufacturers

(FMM) Directory. (Please refer to Appendix II for the full list).

2. Thirty-five cover letters and questionnaires with postage-paid return envelopes were

sent to 35 companies that projected themselves as 3PL providers or claimed to be total

11

and/or integrated logistics providers. The list includes international and local

providers, which was compiled based on information available on their websites and

their latest Annual Reports. The local providers list was gathered from Bursa

Malaysia and the FMM Directory of service providers. As for the international

providers, an internet search was done to find the Malaysian offices or affiliated

companies of the well-known global providers such as DHL, UPS and Schenker.

(Please refer to Appendix III for the survey list).

The search for users started from the website of Bursa Malaysia ( the Kuala Lumpur Stock

As a starting point for sample selection and in order to ensure a high possibility that the

companies chosen are users of 3PLs, selection of the samples was guided by Cass Logistics’

percentage of 3PL gross revenue by industry for 2002 in the USA (Armstrong, 2003), as per

Figure 3 below.

Figure 3: Gross Revenue by Industry - 3PL in the USA

Food & Groceries 17%

Other 9%

Automotive 12%

Chemical & Utilities 12%

Industrial 12%

Healthcare 5%Consumer

Goods 13%

Retailing 13%Technology

13%

Source: Cass Logistics

12

The figure shows that 30% of the gross revenue came from food & groceries and

consumer goods industries. Technology, retailing, automotive, industrial, chemical & utilities

and healthcare contributed 61% and the rest were from other industries. Similar condition is

expected to be observed in Malaysia due to equivalent logistics needs of these industries.

Thus, the Technology, Consumers, Industry and Trading & Services segments of

Bursa Malaysia were selected. First, a check on the profiles of all the companies in those

segments was carried out to ascertain the companies’ activities. Those involved in IT

consultancy business, engineering or anything that do not depend on logistics or

transportation were removed from the list. Second, the addresses were copied from either

respective websites or the Listed Companies’ Profile page in the Bursa Malaysia’s website.

Third, the contact persons of companies, i.e. directors/executives chosen for the

survey were then extracted from its latest available Annual Report and at the same time the

address was also verified. Lastly, with the data collected, a final verification was done by

scrutinizing the announcements made for changes in address, directorship and management

by the companies to Bursa Malaysia after their Annual Report dates. This step is crucial in

order to reduce the probability of ‘return to sender’ incidence.

A total of 86 samples were selected through the above procedure. A further 64

samples were then selected from the FMM Directory to take into account the private limited

companies and manufacturers involved in the above-mentioned industries. The process was

much easier compared to the earlier one because all the relevant data of a company is

presented on the same page and the website, i.e. http://www.fmm.org.my/, is up to date.

For this reason, the initial search for the 3PL providers’ samples was done at the

FMM Directory but, unfortunately, not many 3PL providers are registered with FMM.

Accordingly, beside the Trading & Services segment of the Bursa Malaysia, the Northport’s

13

list of registered service providers in http://www.northport.com.my/servicedir_main.asp was

also used.

They were given a month to return the completed questionnaires. No follow-up was

done because the survey was arranged in such a way that the identities of respondents are

anonymous in a hope that they would be more willing to reply without fear or favor.

The questions were designed based on general ideas gathered from a survey of

various literatures listed in Table 1 below:

Survey/Study Title Author & Country Year

1 Third Party Logistics Services Usage By Large Australian Firms

Dapiran.P, Lieb. R, Millen. R, and Sohal, Australia

1996

2 Selection Criteria for Providers of Third Party Logistics Services: An Exploration Study

Mohan K. Menon et al, USA

1998

3 Logistics Service Provider Quality: Private Measurement, Evaluation and Improvement

Forrest E. Harding, USA 1998

4 Managing Effective Third Party Logistics Relationships: What Does It Take?

Sandor Boyson, USA 1999

5 Outsourcing Logistics: Status, Issues and Trends in Partnership

KPMG, Europe 2000

6 Third-Party Logistics: Some User vs Provider Perspectives

Paul R Murphy, USA 2000

7 The Use of Third Party Logistics Services by Large Americam Manufacturers, The 2001 Survey.

Robert Lieb & Brandon Shwarz, USA

2001

8 Third-Party Logistics Study Results and Findings of the 2002 Seventh Annual Study

C. John Langley Jr, Gary R. Allen and Gene R. Tyndall, USA

2003

9 The Use Of Third Party Logistics Services: A Malaysian Perspective

Sohail & Sohal, Malaysia 2003

10 Quality Management in Logistics: A Comparison of Practices Between Manufacturing and Retail Companies and Logistics Firms.

Shams Rahman, Australia

2003

Table 1: Previous 3PL Surveys

14

2.2 Theoretical Framework

The concept and framework for this thesis was developed principally based on the

works of Susanne Hertz and Monica Alfredsson (2003) and M.S. Sohail and A.S. Sohal

(2003). Hertz and Alfredsson studied the development of 3PL in Europe via case studies and

Sohail and Sohal explored the usage of 3PL services in Malaysia by means of mail survey in

year 2000. Concepts from these studies are used to delve into the development of 3PL

providers in Malaysia.

2.3 Financial Performance

Historical data from annual reports of a company measure its past performance

rather than its future plan and strategy. Yet, the previous financial performance does help in

giving indication of the company’s ability to move forward without incurring extra debts.

A long-term perspective needs to be taken to measure strategic and financial

performances (Algera & Paring, 2001). Hence, for the case studies, four-year results were

obtained from their Annual Reports submitted to Bursa Malaysia that was tabled during the

companies past Annual General Meetings and the reports were audited by licensed

accounting firms, in some cases by the big four accounting firms in the world, i.e. KPMG,

Ernst & Young, PWC and Deloitte.

2.4 Definitions of Central Concepts and Terms

This thesis will employ the following central concepts and terms according to the

meaning described.

15

Multinational Corporations (MNC)

A multinational corporation is a firm that operates in more than one country. The

United Nations defines MNC as a corporation that comprises entities in two or more

countries, regardless of legal form and field of activity. It operates under a coherent system of

decision making and common strategy and linked by ownership or otherwise that one or more

entities exercise significant influence over the activities of others.

Logistics

Broadly defined, logistics is the management of a process of a supply chain. It

comprises a number of interrelated and interactive activities covering procurement,

production and distribution. It is concerned with physical and information flows from raw

material through to the final distribution of finished product. (Langley, Allen & Tyndall,

2003).

The most quoted definition is by the Council of Logistics Management, which stated

that:

Logistics is the process of planning, implementing and controlling the efficient,

effective flow and storage of raw materials, in-process inventory, finished goods,

services, and related information from point of origin to point of consumption for

the purpose of conforming to customer requirements.

Contract Logistics

A contractual agreement to provide logistics services. Usually prices, length of

contract (term), services required and other considerations are defined and agreed to by the

parties.

16

Supply Chain Management (SCM)

The definition of ‘supply chain’ seems to be more common across authors than the

definition of SCM. Christopher (1992) define a supply chain as the network of organizations

that are involved, through upstream and downstream linkages, in the different processes and

activities that produce value in the form of product and services delivered to the ultimate

customer.

After studying a number of previous definitions, Mentzer et al. (2001) provide a more

refined definition from both ‘supply chain’ and SCM. Supply chain is a set of three or more

entities (organizations or individuals) directly involved in the upstream and downstream

flows of products, services, finances, and/or information from a source to a customer.

SCM is then defined as the systemic, strategic coordination of the traditional business

functions and the tactics across these business functions within a particular company and

across businesses within the supply chain, for the purposes of improving the long-term

performance of the individual companies and the supply chain as a whole.

Integrated Logistics

Integrated logistics is the process of anticipating customer needs and wants; acquiring

the capital, materials, people, technologies and information necessary to meet those needs

and wants; optimizing the goods or service producing network to fulfill customer requests;

and utilizing the networks to fulfill customer requests in a timely manner (Little, 1991).

Third Party Logistics (3PL)

Third-party logistics involves the use of external companies to perform logistics

functions that have traditionally been performed within an organization. The functions

17

performed by the third party can encompass the entire logistics process or selected activities

within that process. (Lieb, Millen & Wassenhove, 1993)

According to this definition, third party logistics includes any form of externalization

of logistics activities previously performed ``in-house''. If, for example, a company with its

own transport facilities decides to employ external transporters, this would, according to the

above definition, be an example of third party logistics. The same applies to a company

which closes its warehouse and instead uses an external warehouse.

Berglund (2000) in his doctoral dissertation describes 3PL as an external provider

who manages, controls and delivers logistics activities on behalf of a shipper. The

relationship can be formal or informal and should be mutually beneficial and a continuous

one. The activities performed can include all or a part of the logistics activities but at least

should include the management and execution of transport and warehousing activities.

A similar definition was offered by Coyle, Bardi and Langley (2003) i.e. ‘Essentially,

a third party logistics firm may be defined as an external supplier that performs all or part of a

company’s logistics functions’. However, they also pointed out that a ‘true’ 3PL providers

offer an integrated multiple logistics activities with solutions to logistics or supply chain

problems.

Lead Logistics Provider (LLP)

A value-added logistics provider, who manages other contract logistics operators and

provides supply chain consulting services for his customer (Armstrong, 2003).

Lead Logistics Manager (LLM)

A value-added lead logistics provider, who designs, builds and manages supply chain

assets, processes, people and technology (Armstrong, 2003).

18

Fourth Party Logistics (4PL)

Accenture, Inc. came up with the 4PL concept and bought the right to it. They defined

4PL as being a firm that assembles and manages the resources, capabilities and technology of

its own organization with those of complementary service providers to deliver a

comprehensive supply chain solution. 4PL leverages the capabilities of 3PLs and IT service

providers through centralize contact. It serves as an integrator that brings together customer

needs and resources available. (Langley et al., 2003).

Armstrong (2003) summed it up as a consultant operating in the capacity of an LLP,

LLM or Supply Chain Integrator.

19

3 Literature Review

3.1 Industry Environment

This literature review will look at how scholars have understood the development of

3PL in Europe and the USA. The progress of the 3PL industry is shaped by developments in

the world economy that are moving from being protected with trade barriers towards

liberalization. The introduction of Euro currency, the deregulation of truck and railway

industries in Europe and the USA for example, has changed the business environment

considerably (Algera & Paring, 2001).

A good model of a 3PL that move in tandem with the economic expansion is DHL's (with its

current advertisement slogan of ‘Moves the World’) move to become a leading 3PL provider

worldwide. It provides a wide range of activities from simple air, sea, road and rail

transportation, to warehousing, inventory management and distribution, supply chain

management, specialty services, and IT services (DHL, in press). A study done by Berglund,

van Laarhoven, Sharman and Wandel (1999) discovered that there were 3 waves of 3PL

development.

"The first wave happened in the 1980s when the traditional transport firms developed

into 3PL while the second wave started in early 1990s when courier firms such as TNT,

DHL, FedEx, etc. entered. In the last wave (late 1990s) the players entering have been

consultancy, financial firms and IT management firms such as Anderson Consulting, GE

capital and Manugistics" (Hertz & Alfredsson, 2003). Consequently, Gordon (2003) found

that the market is very fragmented, and there is a wide recognition that the service range

needs to be enhanced and technology processes optimized. Additionally, international

20

presence is necessary to meet shorter delivery time and value added services demanded by

customers.

3.2 Third Party Logistics Development in Europe

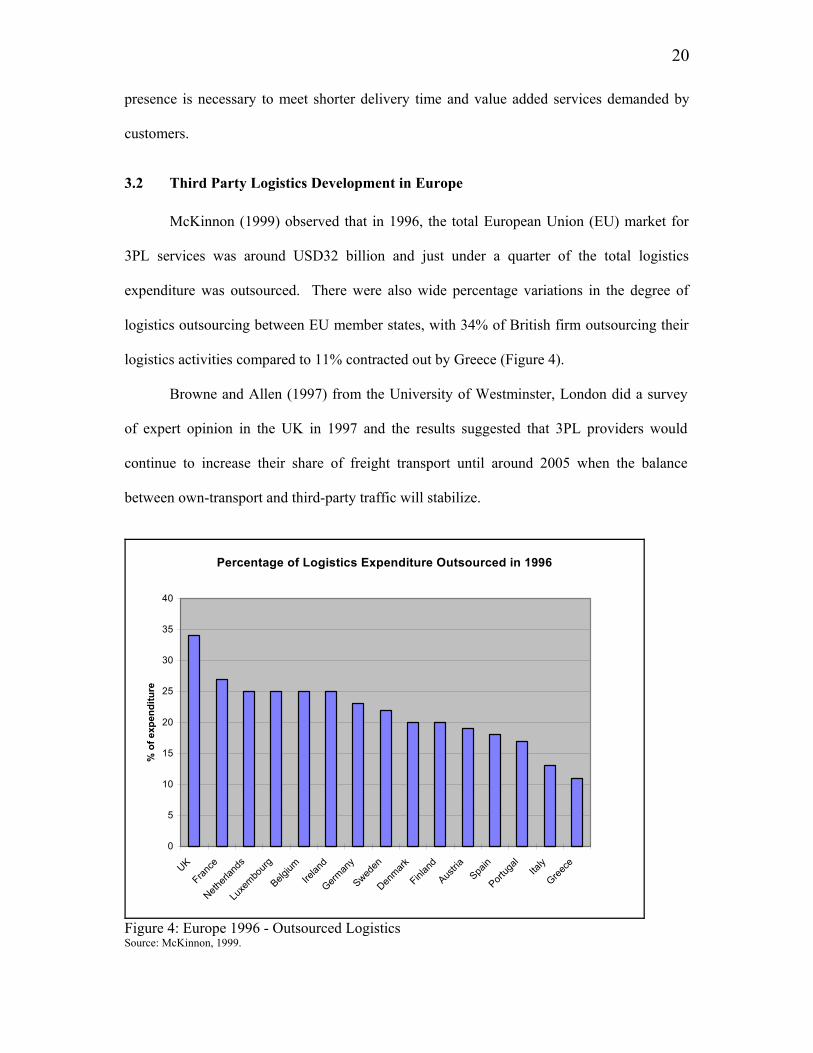

McKinnon (1999) observed that in 1996, the total European Union (EU) market for

3PL services was around USD32 billion and just under a quarter of the total logistics

expenditure was outsourced. There were also wide percentage variations in the degree of

logistics outsourcing between EU member states, with 34% of British firm outsourcing their

logistics activities compared to 11% contracted out by Greece (Figure 4).

Browne and Allen (1997) from the University of Westminster, London did a survey

of expert opinion in the UK in 1997 and the results suggested that 3PL providers would

continue to increase their share of freight transport until around 2005 when the balance

between own-transport and third-party traffic will stabilize.

Percentage of Logistics Expenditure Outsourced in 1996

0

5

10

15

20

25

30

35

40

UK

France

Netherl

ands

Luxe

mbourg

Belgium

Irelan

d

German

y

Sweden

Denmark

Finlan

d

Austria

Spain

Portug

alIta

ly

Greece

% o

f exp

endi

ture

Figure 4: Europe 1996 - Outsourced Logistics Source: McKinnon, 1999.

21

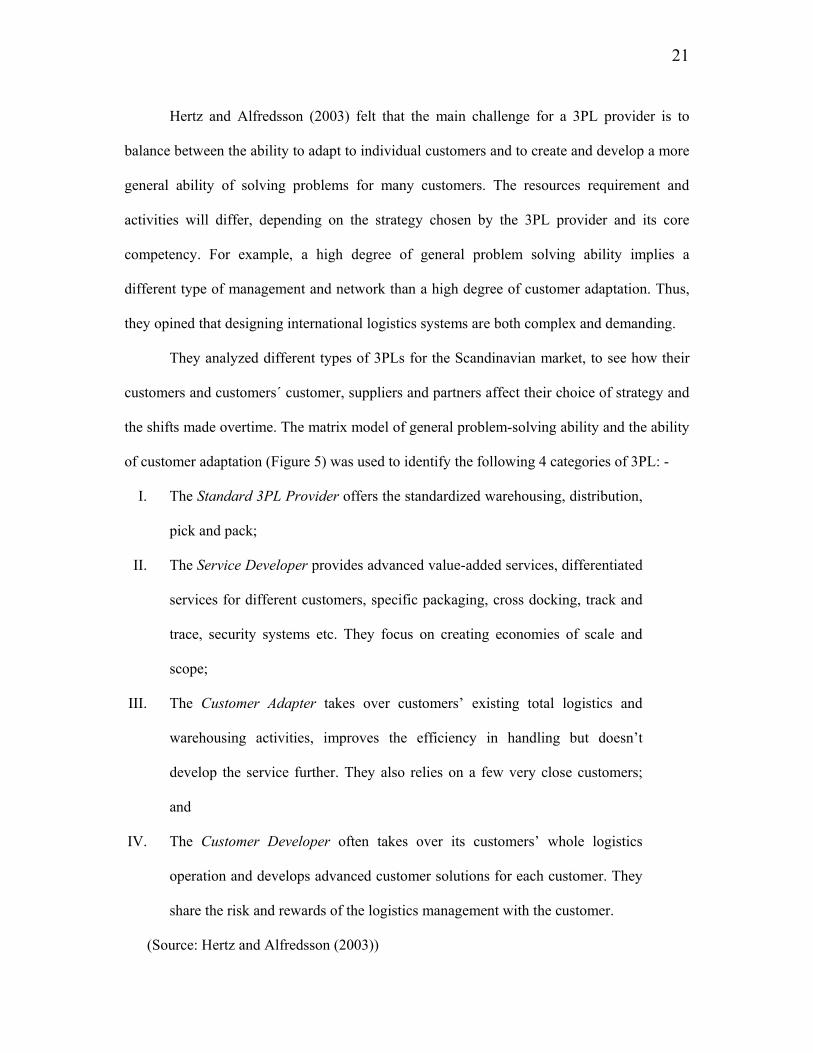

Hertz and Alfredsson (2003) felt that the main challenge for a 3PL provider is to

balance between the ability to adapt to individual customers and to create and develop a more

general ability of solving problems for many customers. The resources requirement and

activities will differ, depending on the strategy chosen by the 3PL provider and its core

competency. For example, a high degree of general problem solving ability implies a

different type of management and network than a high degree of customer adaptation. Thus,

they opined that designing international logistics systems are both complex and demanding.

They analyzed different types of 3PLs for the Scandinavian market, to see how their

customers and customers´ customer, suppliers and partners affect their choice of strategy and

the shifts made overtime. The matrix model of general problem-solving ability and the ability

of customer adaptation (Figure 5) was used to identify the following 4 categories of 3PL: -

I. The Standard 3PL Provider offers the standardized warehousing, distribution,

pick and pack;

II. The Service Developer provides advanced value-added services, differentiated

services for different customers, specific packaging, cross docking, track and

trace, security systems etc. They focus on creating economies of scale and

scope;

III. The Customer Adapter takes over customers’ existing total logistics and

warehousing activities, improves the efficiency in handling but doesn’t

develop the service further. They also relies on a few very close customers;

and

IV. The Customer Developer often takes over its customers’ whole logistics

operation and develops advanced customer solutions for each customer. They

share the risk and rewards of the logistics management with the customer.

(Source: Hertz and Alfredsson (2003))

22

Relatively high high high Problem solving general ability Relatively high

Customer adaptation Figure 5: 3PL Classifications Adapted from Hertz and Alfredsson (2003)

ASG Logistics, Transfargo, DHL and Cat Logistics were taken as their case studies to

illustrate the influence of the above-mentioned parties. In those cases, all of them took on

more advanced activities and increased integration with customers and continue their

development into Customer Developer category, as indicated by the three bold arrows in

Figure 5. They concluded that not only customers but also the customers’ customers and

partners have a heavy influence on 3PL providers’ strategic development since the 3PL

providers have a rather high degree of customer adaptation.

“In 2001, the European logistics industry is characterized by fragmentation where the

eight largest companies together have a market share of around 20%. The two largest

companies, Danzas and Schenker have each around 6%” (Algera & Paring, 2001).

In terms of consolidation, the 3PL industry in Europe was relatively late to initiate the

merger and acquisitions process (compared to the USA) because the big providers were

initially skeptical of the idea. But, they managed to catch up quickly with Deutsche Post

leading the pack.

Service Developer

Customer Developer

Customer Adapter

Standard 3PL Provider

23

Andersson and Norrman (2002) concluded that the globalization and its consequences

have forced the European logistics industry to consolidate, resulting in many mergers and

alliances in recent years. For instance, the former two largest transport and logistics

companies in the Nordic countries, BTL and ASG, were bought and incorporated into large

networks by Schenker, (May 1999) and Danzas, (April 1999) respectively. This trend has

brought into being, bigger and more powerful global logistics service providers as the number

of competitors declined.

In an analysis based on a client survey covering 1000 manufacturers and retailers

throughout a range of industry sectors, Datamonitor (2002) identified the following key

points in its ‘European Logistics Spend 2002– 3PL Potential’ study:

• “The largest 3PLs will remain strong in the consumer and retail sector while smaller

players will struggle. This is especially true for the UK market. Smaller players may

have to direct their business towards niche operations within this sector to remain

competitive.

• Road haulage still dominates the transport of goods in all industry sectors. As 3PL’s

market share grows, this could reduce the business being won by road haulage

companies and these players may have to enhance their service offering to remain

competitive in the long run.

• It may not be enough for 3PLs to regard the industry sectors with the largest logistics

spend dedicated to 3PLs as those with the greatest potential. Sometimes this will not

be the case and can be quite the opposite as markets become saturated with players

competing for the same business.

• Logistics providers will be looking to focus towards markets that are not only willing

to out-source their logistics requirements but also to develop relationships that involve

high levels of management and value added service. 3PL penetration in all industry

24

sectors will certainly grow, and providers must be aware of how and where to direct

their business.” (Source: Datamonitor (2002)

Furthermore, Datamonitor also established that there was a significant migration from

asset-based logistics to value added and integrated contract logistics solutions.

Total logistics spending in Europe for 2003 is estimated to be around the regions of

USD140-160billion per annum, of which USD35-40billion (25%) is directly contracted out to

3PL providers. Distributors, warehousing and transportation infrastructure companies such as

Spiegel and JC Penney have started offering 3PL services too (www.eyefortransport.com ,

Sept 2003).

3.3 Third Party Logistics Development in the USA

Bowersox, Daugherty, Droge, Rogers and Wardlow (1989) looked at the development

of logistics from the inter-organizational point of view, i.e. the relationship between provider

and user of logistics functions on a continuous scale, going from single transaction to

integrated service agreements, as shown in Figure 6.

This progress in terms of integration and commitment was mainly due to customers’

requirement, which the logistics providers willingly complied with because it provided them

with long-term flow of income and hopefully additional service agreements. This is similar to

the customer adaptation case mentioned earlier.

25

Figure 6: Relationships between 3PL providers and users Source: International Journal of Physical Distribution & Logistics Management, 2000. The logistics services are intended to encompass transportation, warehousing, distribution,

financial services, etc. Many of the 3PLs were formerly carriers, hauliers, warehouse owners,

freight forwarders and courier companies but some IT companies have started to offer

logistics services too (Langley et al., 2003). Table 2 summarizes the types of 3PL providers

in the USA.

Type Companies based in the USA Transportation based Ryder, Menlo Logistics, Schneider Logistics,

FedEx Logistics, UPS Logistics. Warehouse/Distribution based Exel Logistics, USCO, DSC Logistics Forwarder based Kuehne & Nagel, Fritz Financial based GE Information Services IT based Transplace, Nistero

Table 2: Types of 3PL Providers. Source: Langley et al., 2003.

Transportation companies extend beyond their traditional activities to provide a more

comprehensive service. Some of them are subsidiaries or division of large transportation

firms that utilize the parent company’s assets. Normally, distribution and warehouse

26

providers have already been offering inventory management, which make the transition to

integrated logistics services less complex.

By putting together packages of logistics services that is a mere extension of their

middleman role, the freight forwarders can promote themselves as non-assets based 3PL.

Financial based 3PL provides freight payment services, auditing, cost accounting control and

logistics management tools to monitor, book, track and manage inventory. IT based 3PL

offers web-enabled platform to bring together shippers and carriers worldwide to collaborate

on their transportation planning and execution.

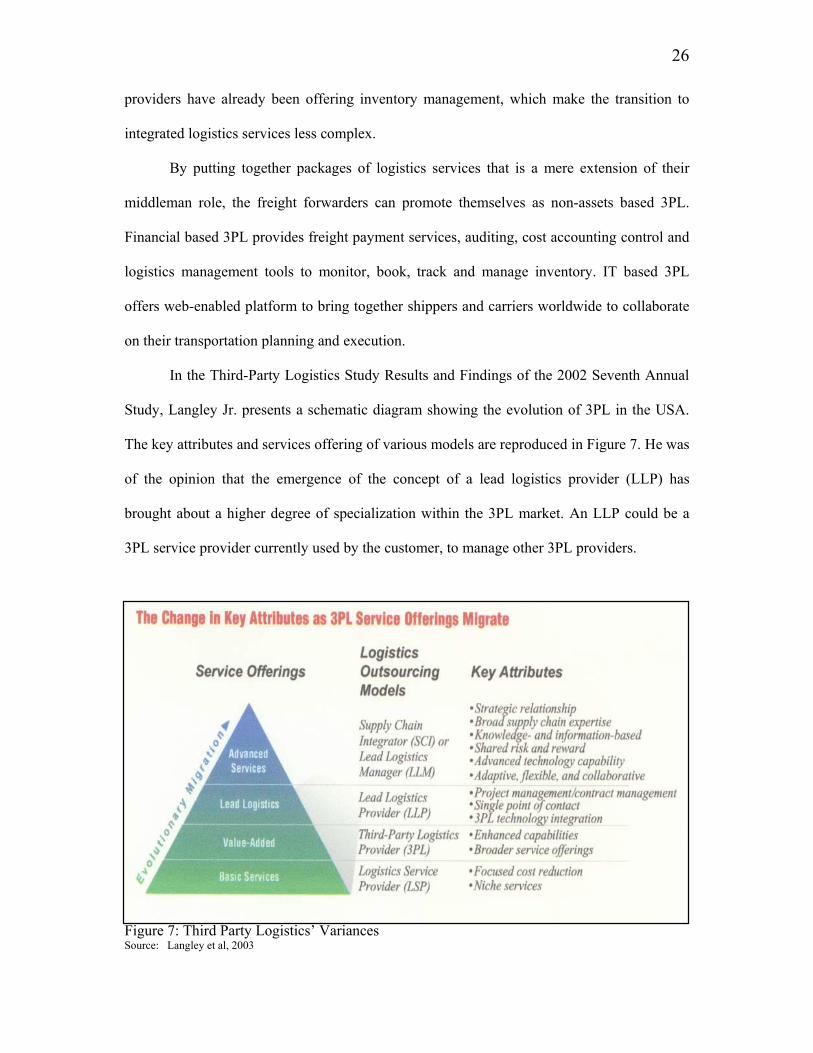

In the Third-Party Logistics Study Results and Findings of the 2002 Seventh Annual

Study, Langley Jr. presents a schematic diagram showing the evolution of 3PL in the USA.

The key attributes and services offering of various models are reproduced in Figure 7. He was

of the opinion that the emergence of the concept of a lead logistics provider (LLP) has

brought about a higher degree of specialization within the 3PL market. An LLP could be a

3PL service provider currently used by the customer, to manage other 3PL providers.

Figure 7: Third Party Logistics’ Variances Source: Langley et al, 2003

27

Nowadays, there is also an emerging trend of logistics consultants that provide

logistics advisory services focusing on strategy to develop and implement supply chain,

finance and technology selection such as Armstrong & Associates and BG Strategic Advisors

in the USA. Benjamin Gordon of BG Strategic Advisors noted that the 3PL industry is

extremely fragmented. Based on 2002 estimated revenue, there was no 3PL provider that

controls more than 6% of the total logistics market. The top 50 companies total revenue was

only USD27 billion compared to the total U.S. logistics market that was estimated to be over

USD65 billion which includes air and ocean freight, asset-based transportation, non-asset-

based surface transportation, value added warehousing and warehouse.

Each year, Armstrong & Associates Inc, a 3PL consulting firm, tracks the growth of

the industry while Accenture and Northeastern University in Boston survey 3PL executives

and the Fortune 500 manufacturers on their use of 3PL services. Figure 8 below summarizes

The survey results showed that the 3PL industry continues to grow and value-added

warehousing and distribution was the fastest growing segment of the industry, with $16.9

billion in revenues, up 10.5% (Table 3). Warehouse management is not only the fastest

growing segment of the industry but it is also the segment that yields the greatest cost

benefits to 3PL users and results in the greatest logistics service improvements to users.

Total 3PL gross revenues USD65 billion* Total 3PL gross revenues for value-added warehousing and distribution

USD16.9 billion*

Fortune 500 manufacturers using 3PLs 80%** Fortune 500 manufacturers using 3PLs for more than 5 years 72%** Fortune 500 manufacturers using 3PLs on a global basis 69%** Users who by from multiple providers 58%** Users who plan to increase their use of 3PLs 51%** Users who plan to decrease their use of 3PLs 13%** Users annual logistics budget paid to 3PLs 33%** 3PLs yielding greatest benefit to users Warehouse Mgmt

Service**

Table 3: 3PL by the Numbers in the USA for 2002 Sources: Armstrong & Associates and Accenture/Northeastern University

Several trends are driving the continued growth of the industry. Demand of total

logistics solution from 3PL providers and the increase of shipments to and from emerging

markets like eastern Europe, China, and South America led to the birth of large providers

like Fedex, APL Logistics, Excel and Maersk which are developing strong global logistics

solutions.

Gordon (2003) observed that the 3PL industry started to consolidate across modes and

geographies because there was an increasing preference among Fortune 1000 firms to deal

with one 3PL that could manage the entire logistics process. An example of multimodal

consolidation was UPS’ purchase of Fritz while examples of geographic consolidation were

Deutsche Post’s acquisition of AEI (Airborne Express Iberica) and Danzas’ and APL’s

purchase of GATX.

29

The Accenture survey also found increased interest in 4PL services offered by

providers whose specialty is designing, implementing, and managing total supply chain

solutions using capable 3PLs to execute the parts. As supply chains become more complex,

the integration of those solutions becomes more complex and a 4PL has the broad skills to do

that integration.

Unlike a 3PL provider who’s traditional focus has been on the organization and

management of assets such as facilities, vehicles and inventory, the 4PL providers’ focus is

towards the collection, coordination and management of information; leaving asset

management to the 3PL providers.

Table 4 shows us the US-Based 3PL providers which earned more than USD500

millions in net logistics revenue for 2002. Note that the first and second waves firms

mentioned by Berglund et al.(1999) are in the top ten lists but the third is yet to make an

impact.

In his thesis, Chew also noted that majority of these companies are also global

logistics providers with branches in 100 to 200 countries (Chew, 2003).

3PL Providers Net Logistics Revenue USDmil Exel Plc - Americas 1499 Ryder 1492 UPS Supply Chain Solutions 1402 Danzas Management Ltd. (DHL Danzas Air & Ocean) 1386 Schneider Dedicated Operations 1134 Penske Logistics 1054 Caterpillar Logistics Services, Inc. 1000 Tibbett & Britten Group Americas, Inc. 908 APL Logistics 723 Expeditors Int'l of Washington, Inc. 682 EGL, Inc.(Eagle) 672 TNT Logistics North America/CTI 635 J. B. Hunt Dedicated Contract Services 628 AmeriCold Logistics, Inc. 550 Table 4: North American-Based 3PL Revenues: Net Revenue for 2002 of more than USD500 million.

Source: website of Armstrong & Associates, Inc

30

3.4 Studies on Malaysia

Apart from short logistics articles written in local newspapers and business

magazines, this research could not find specific studies on the 3PL industry in Malaysia

except for a study on the usage of 3PL providers in Malaysia, done by Sohail and Sohal in

2003. It was published in Technovation Journal and the authors also confirmed that there

were no comprehensive studies reported in the literature focusing on the extent of 3PL by

firms in Malaysia (Sohail & Sohal, 2003).

3.4.1 Review of Commissioned Studies

Although several studies commissioned by the Government were not specifically

meant for 3PL, they help in understanding the conditions that affected its development. There

were a number of transportation and logistics related studies done by consultants appointed

by the Malaysian government when the country faced a crisis or whenever a drastic change of

policy was needed.

For instance, in 1988, the Government was aiming to minimize investments and

maximize the utilization of the existing system and infrastructure so the Malaysia National

Transport Policy Review was carried out to identify the critical bottlenecks to transport

efficiency. Among the key findings were that transport planning and coordination was

generally weak, with an overall plan not fully or effectively integrating the individual

components. Moreover, investment proposals were not always economically justified, with

inconsistent treatment of various modes.

It was recommended that a National Transport Act be drawn up to act as an umbrella

for all transport legislation and clearly outline the role of the Ministry of Transport. A strong

central planning unit should then be set up to guide overall transportation sector development.

31

Every transportation investment should be accompanied by economic analysis so as to allow

the Government to prioritize investments in times of resource constraint.

One of the studies that is relevant to this thesis is the ‘Container Transportation Chain

Study’ done by Coopers and Lybrand (C&L) in 1996 when there was a backlog of containers

movement at the ports. The objective of the study was to assist the Government in assessing

the overall efficiency of the logistics value chain and to recommend measures for

improvements. The findings are listed in Table 5.

32

Process Weakness/Inefficiency Importers submit documents to Forwarding Agents (FA)

Incomplete, inaccurate and delay in submission of source documents. Importers’ poor knowledge of pre-clearance.

FA makes Customs declaration/SA submits inward manifest.

FA not pro-active in pre-clearance High variance in set up & operational standards FA lacked professionalism Short transit time of voyage Last minute amendments by SA SA not computerized

Custom clearance, duty payment and Customs release

Outdated Customs Act and clearance system which does not support pre-clearance. Different legislations e.g Customs Act for manifest submission and Road Transport Act & CVLB Act for vehicle inspections. Late duty payment, haulage payment, Shipping Agent (SA) and handling charges payment.

FA obtains release documents and hand to Hauliers

Inadequacy in equipments especially during peak periods

Hauliers request for mounting

Inadequate prime movers and trailers, especially at Central and Southern regions Inefficient process Trailer detention Importers short opening hours

Terminal operator loads container

Inadequate equipments Time zone restrictions Free storage days

Container leaves gate Poor condition of roads/bridges around port Delays in EDI rollout Few ICDs Many short haul voyages Rapid growth of containers

Consignee receives container

Incomplete information No acceptance of service standards Complex processes

Table 5: Container Transportation Chain Study 1996-Summary of Findings

In summary, the logistics value chain in Malaysia has been found to be dynamic and

complex. The weaknesses and efficiencies of individual parties affect each other and have

negative impact on the overall performance. Significant improvement in performance will

require the introduction of new practices and a reduction in constraints currently faced by

33

individual parties within the value chain. Five key principles were proposed by Coopers and

Lybrand , i.e.

i. “Standardized monitoring system for performance measurement and control.

ii. More efficient regulated clearance process by amending the Customs Act to allow

clearance prior to manifest arrival and accepts House Bill of Lading for

consolidated freight.

iii. Upgrading professionalism of players within the transport chain by requiring

compliance to service standards before renewal of license.

iv. Ensuring appropriate investments and efficiency in the physical delivery process.

• Independent Total Logistics Service Providers/3PLs; and

• Other Significant Trade Facilitators.

37

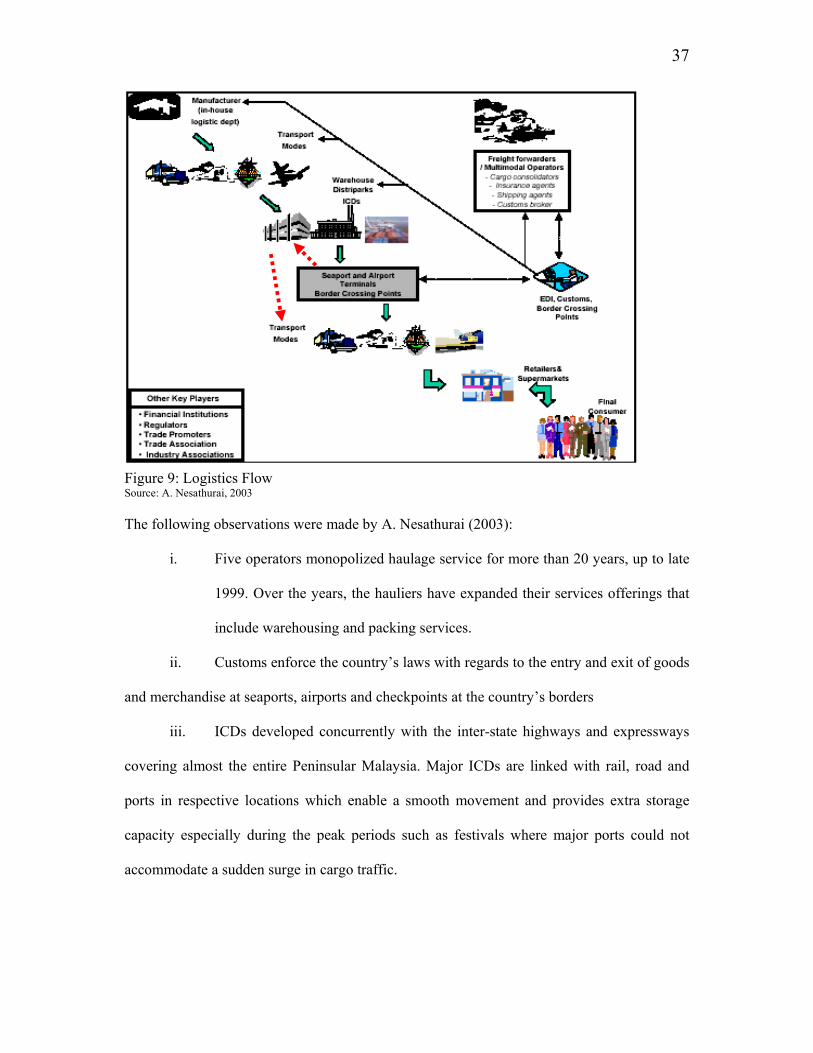

Figure 9: Logistics Flow Source: A. Nesathurai, 2003 The following observations were made by A. Nesathurai (2003):

i. Five operators monopolized haulage service for more than 20 years, up to late

1999. Over the years, the hauliers have expanded their services offerings that

include warehousing and packing services.

ii. Customs enforce the country’s laws with regards to the entry and exit of goods

and merchandise at seaports, airports and checkpoints at the country’s borders

iii. ICDs developed concurrently with the inter-state highways and expressways

covering almost the entire Peninsular Malaysia. Major ICDs are linked with rail, road and

ports in respective locations which enable a smooth movement and provides extra storage

capacity especially during the peak periods such as festivals where major ports could not

accommodate a sudden surge in cargo traffic.

38

iv. The distriparks provide value-added facilities such as packing and repacking,

labeling and assembling, sorting and consolidation and are located within the port’s Free

Commercial Zone (FCZ).

v. EDI systems linked the forwarding and shipping agents, port operators,

commercial banks, government agencies and customs to enable them to exchange data and

expedite the clearance of goods.

vi. Other facilitators comprise banks, insurance companies, licensing boards,

industry and trade associations. The banks and insurance companies provide a secured

business environment via credit and insurance facilities that guarantee the seller and buyer to

get the sale proceeds and the merchandise, safely.

The licensing boards control and monitor the performance of the logistics

sectors and finally, the industry and trade associations may influence the

Government’s policy direction with regard to trade and logistics matters.

A. Nesathurai (2003) was of the opinion that the fragmentation of modes of transport

(road, sea, rail, air) is costly because it led to barriers to transporters that have to change

mode, economic inefficiency and high social and environmental cost. For these reasons, he

proposed for a cohesive and unified transport policy for the whole transport systems. In view

of the fact that the industry is compartmentalized according to mode i.e. sea, land and air, and

the industry players are divided into various associations, this study will go through them

accordingly in order to track the development of 3PL in Malaysia.

3.4.3 Sea

As of December 2002, there were 63 shipowners represented by the Malaysian

Shipowners’ Association (MASA), which collectively own 451 vessels with a combined

gross tonnage of 4.7 million tons (MASA’s website- http://www.malaysianshipowners.org/).

39

Table 6 lists the major owners with more than 10 ships.

Company No. of ships 1 MISC Berhad 125 2 Bumi Armada Navigation Sdn Bhd 33 3 Perkapalan Mesra Sdn Bhd 33 4 Sykt Borcos Shipping Sdn Berhad 26 5 Highline Shipping Sdn Bhd 18 6 PDZ Holdings Bhd 13 7 Anjang Shipping Sdn Bhd 13 8 See Song & Sons Sdn Bhd 12 9 Malaysian Merchant Marine Bhd 11 10 Johan Shipping Sdn Bhd 11

Table 6: Top 10 Malaysian Shipowners Source: MASA’s website

However, only those highlighted provide cargo shipment (container, bulk, car carrier),

the rest cater for the oil industry (crew, tugboat, landing, etc).

Ever since the September 11 attacks, there has been a great deal of uncertainty in the

world market, and this has contributed to weakening of demand. The late chairman of the

MASA, Datuk Hj Mohd Ali Yasin noted that the incident has precipitated a chain of events

that have negative impact on shipping industry, globally. Malaysian shipowners are

anticipating slower growth in 2004 and the liner trade will be especially difficult. Local

shipowners were further grappling with increased costs and had to contend with severe

imbalance in demand and supply as a result of the recently concluded war in Iraq.

The new International Ship and Port Facility Security Code and security measures

such as the container security initiative, US Customs Trade Partnership Against Terrorism

and 24-hour advance manifest submission would also have an impact on Malaysian

shipowners operations and costs.

Ships require seaports to interface with inland modes of transportation. There are

multi-dimensional activities that are integrated within the logistics chain, provided at the

seaports to facilitate maritime trade. Thus, port is considered as a ‘trade facilitator’, i.e. a

linking point between sea and land transport in the logistics chain (Song, 2002).

40

More than 90% of the nation’s international trade was handled through seaport with

total tonnage cargo rising by 8.3% pa from 98.9 million tones in 1990 to 220.8 million tones

in 2000. At the same time, petroleum and gas increased its share from 11.8% to 30.5% of

total cargo handled by ports (NTPSS, 2003).

The Ministry of Transport has under its jurisdiction seven major federal international

ports - six ports located in Peninsular Malaysia, namely, Port Klang, Penang Port, Johor Port

at Pasir Gudang, Port of Tanjung Pelepas, Kuantan Port and Kemaman Port, and one in

Sarawak, i.e., Bintulu Port (http://www.mot.gov.my/english/Divisi_maritime.htm)

3.4.4 Land Transport

The demand for transportation, especially land transport has increased in tandem with

the growth in manufacturing. Land transportation comprises of the movement of general and

loose cargo by conventional lorries or trucks, containerized cargo by prime movers and

mixed cargo by rail. Road transport accounts for 90% of total freight movement which was

predominantly used for general cargo (45%), palm oil, logs and grains (NEAC 2003).

3.4.4.1 Conventional Truck

The size of the conventional lorry transport industry in terms of number of operators,

total fleet strength and tonnage handled is difficult to gauge as there is no regulatory body

monitoring the flow of all types of cargo within the country. Based on the Ministry of

Transport and the Malaysian Motor Traders Association, a total of 358,656 commercial

goods vehicles were registered in West Malaysia between 1988 and 1997. The average

growth was 30% between 1994 and 1997.

41

3.4.4.2 Container Haulage

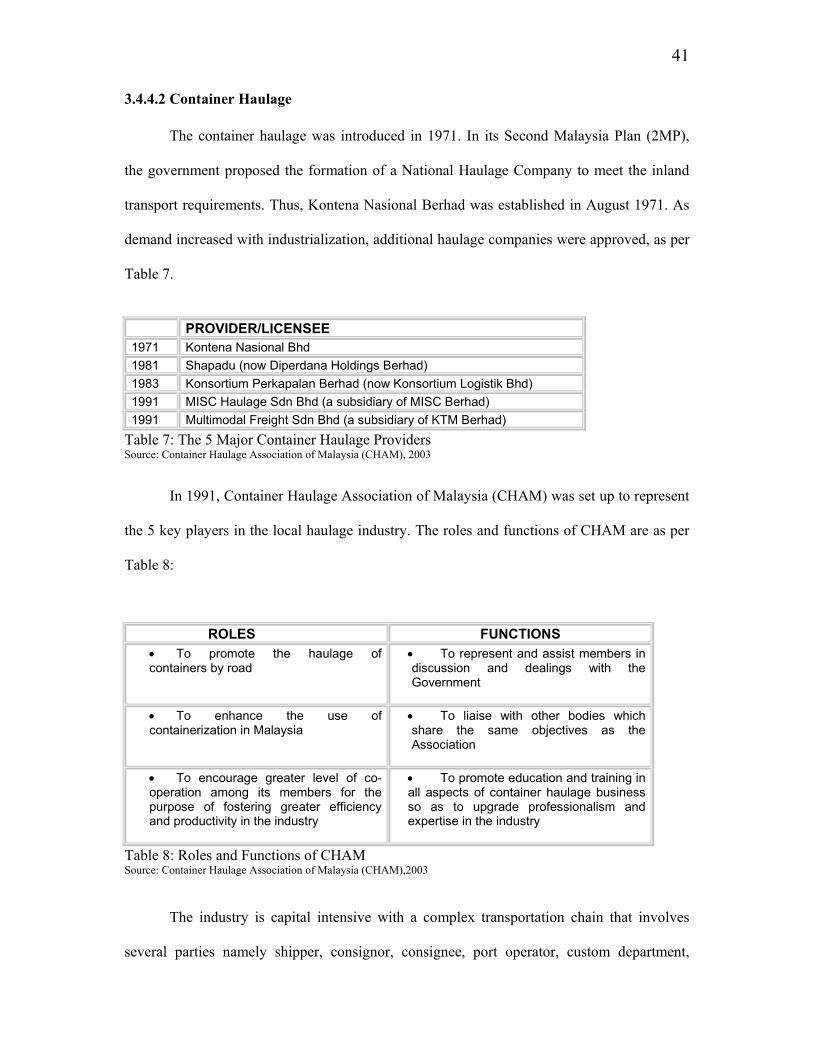

The container haulage was introduced in 1971. In its Second Malaysia Plan (2MP),

the government proposed the formation of a National Haulage Company to meet the inland

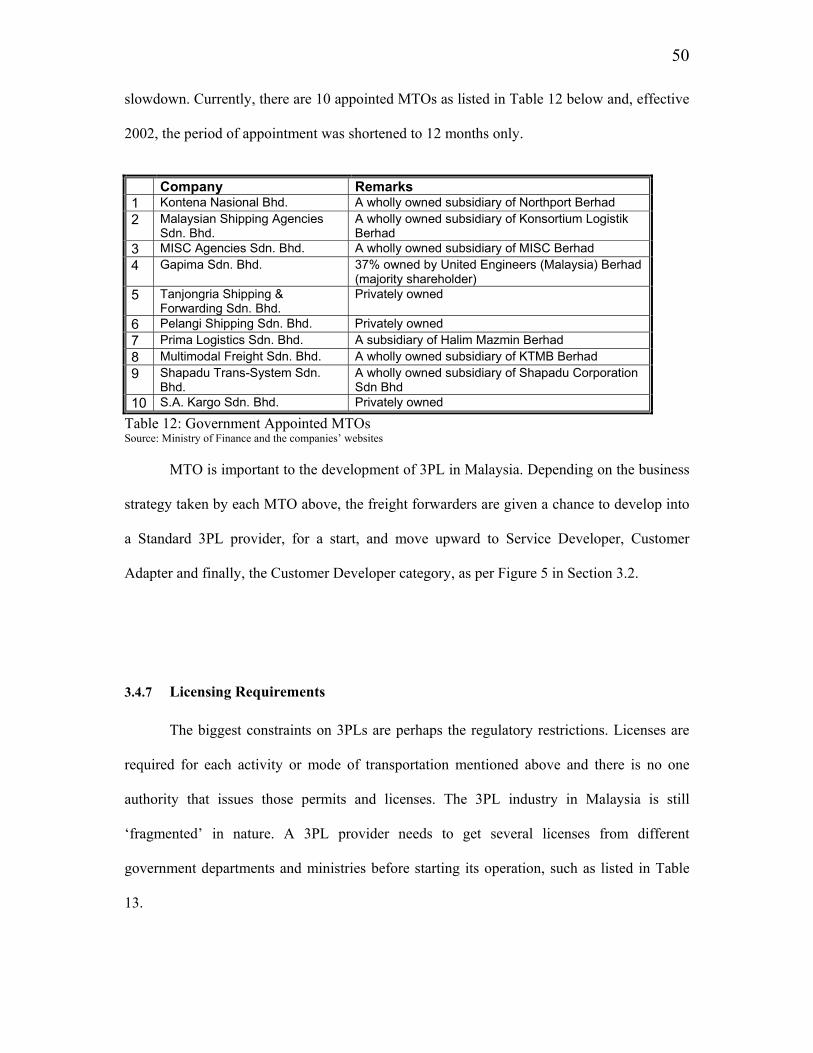

transport requirements. Thus, Kontena Nasional Berhad was established in August 1971. As

demand increased with industrialization, additional haulage companies were approved, as per

Table 7.

PROVIDER/LICENSEE

1971 Kontena Nasional Bhd 1981 Shapadu (now Diperdana Holdings Berhad) 1983 Konsortium Perkapalan Berhad (now Konsortium Logistik Bhd) 1991 MISC Haulage Sdn Bhd (a subsidiary of MISC Berhad) 1991 Multimodal Freight Sdn Bhd (a subsidiary of KTM Berhad)

Table 7: The 5 Major Container Haulage Providers Source: Container Haulage Association of Malaysia (CHAM), 2003

In 1991, Container Haulage Association of Malaysia (CHAM) was set up to represent

the 5 key players in the local haulage industry. The roles and functions of CHAM are as per

Table 8:

ROLES FUNCTIONS • To promote the haulage of containers by road

• To represent and assist members in discussion and dealings with the Government

• To enhance the use of containerization in Malaysia

• To liaise with other bodies which share the same objectives as the Association

• To encourage greater level of co-operation among its members for the purpose of fostering greater efficiency and productivity in the industry

• To promote education and training in all aspects of container haulage business so as to upgrade professionalism and expertise in the industry

Table 8: Roles and Functions of CHAM Source: Container Haulage Association of Malaysia (CHAM),2003

The industry is capital intensive with a complex transportation chain that involves

several parties namely shipper, consignor, consignee, port operator, custom department,

42

warehouse operator and others. Conservatively, the 5 hauliers spent at least RM3 billion by

the year 1999 on prime movers, trailers, land, buildings, equipments, depots and containers

monitoring systems (CHAM, in press).

Due to the continuing bottleneck crisis at the ports throughout Peninsular Malaysia up

to the year 2000 that resulted in customers paying extra port charges and demurrage for their

containers, the Government decided to deregulate the haulage industry and give more

licenses to new players4. Table 9 shows the increase in the number of licenses issued

throughout the years and Table 10 lists the increase in the number of permits issued for prime

movers and trailers.

2000 2001 % increase 2002 %

incr 2 yr % incr

Licensees 5 52 940 68 31 1,260

Table 9: Number of Licensed Container Haulage Companies Source: CHAM, 2003 YEAR PRIME-

In commercial definition, MTOs are actually international freight forwarders. The

operators are actually licensed freight forwarders and shipping agencies that are appointed to

carry out the responsibility for the transportation of goods from point of receipt in one

country to point of destination in another country. Thus, all Government entities must use the

service of the appointed MTOs for all their shipments through tender process.

In return, the MTOs must undertake that:

(a) “It shall, at all times, be registered with the Ministry of Finance, Malaysia;

(b) It shall promptly obtain and maintain in full force and effect any relevant

authorization or registration which may become necessary to obtain to enable it to