29

02/18/2014 1 Cohort Default Rates Challenging the Draft Rates Julia Alexander Compliance & Training Officer Nelnet Guarantor Solutions

02/18/2014

1

Cohort Default Rates

Challenging the Draft RatesJulia Alexander

Compliance & Training Officer

Nelnet Guarantor Solutions

02/18/2014

2

Agenda

• Cohort Default Rate (CDR) overview

Ch ll i d ft h t d f lt t• Challenging draft cohort default rates

– Incorrect data challenge (IDC)

• Why?

• When?

• What?

• How?• How?

• Resources

Cohort Default Rate Overview

02/18/2014

3

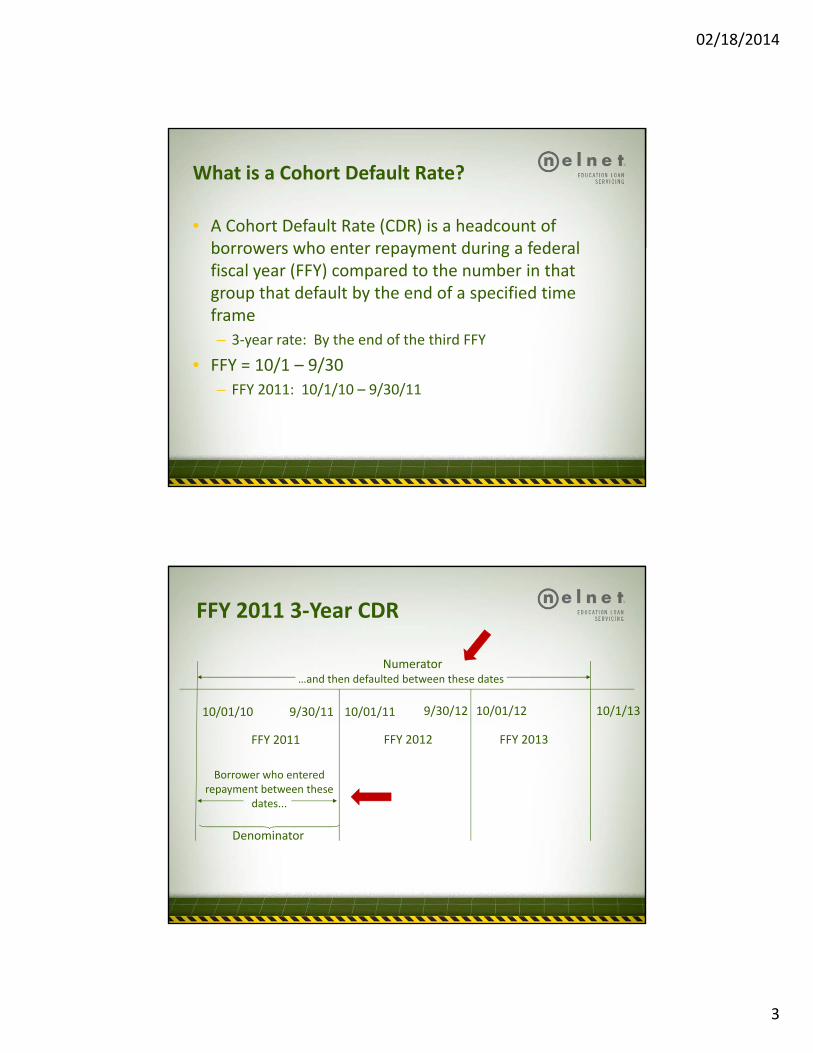

What is a Cohort Default Rate?

• A Cohort Default Rate (CDR) is a headcount of borrowers who enter repayment during a federalborrowers who enter repayment during a federal fiscal year (FFY) compared to the number in that group that default by the end of a specified time frame

– 3‐year rate: By the end of the third FFY

• FFY = 10/1 – 9/30FFY = 10/1 9/30

– FFY 2011: 10/1/10 – 9/30/11

FFY 2011 3‐Year CDR

…and then defaulted between these datesNumerator

10/01/11 9/30/12

FFY 2012

10/01/10 9/30/11

FFY 2011

Borrower who entered repayment between these

dates

10/01/12 10/1/13

FFY 2013

dates...

Denominator

02/18/2014

4

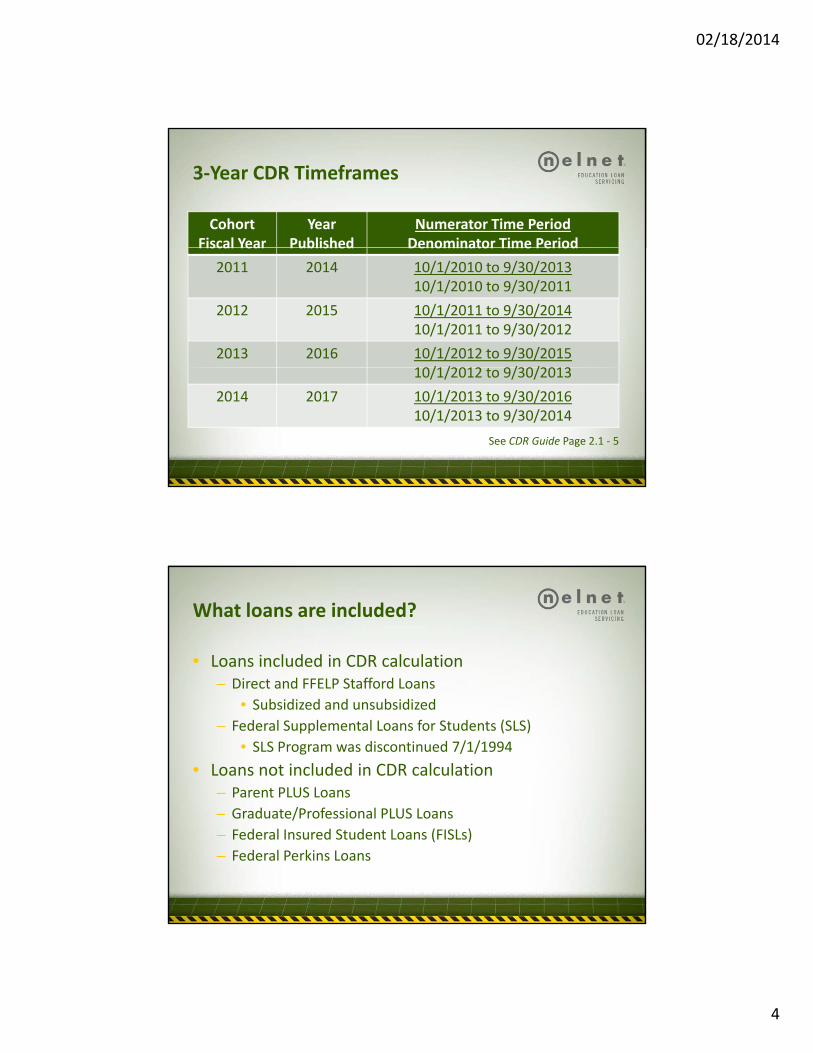

3‐Year CDR Timeframes

CohortFiscal Year

YearPublished

Numerator Time PeriodDenominator Time PeriodFiscal Year Published Denominator Time Period

2011 2014 10/1/2010 to 9/30/201310/1/2010 to 9/30/2011

2012 2015 10/1/2011 to 9/30/201410/1/2011 to 9/30/2012

2013 2016 10/1/2012 to 9/30/201510/1/2012 9/30/201310/1/2012 to 9/30/2013

2014 2017 10/1/2013 to 9/30/201610/1/2013 to 9/30/2014

See CDR Guide Page 2.1 ‐ 5

What loans are included?

• Loans included in CDR calculation– Direct and FFELP Stafford LoansDirect and FFELP Stafford Loans

• Subsidized and unsubsidized

– Federal Supplemental Loans for Students (SLS)

• SLS Program was discontinued 7/1/1994

• Loans not included in CDR calculation– Parent PLUS Loans

– Graduate/Professional PLUS Loans

– Federal Insured Student Loans (FISLs)

– Federal Perkins Loans

02/18/2014

5

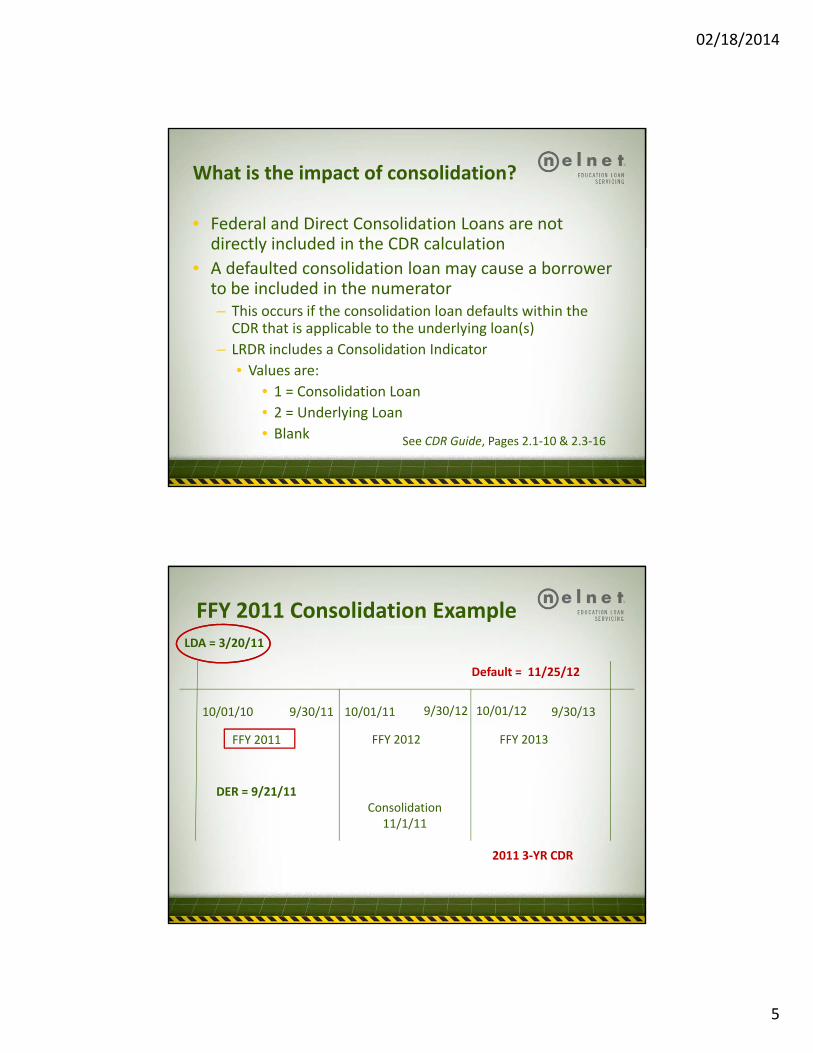

What is the impact of consolidation?

• Federal and Direct Consolidation Loans are not directly included in the CDR calculationdirectly included in the CDR calculation

• A defaulted consolidation loan may cause a borrower to be included in the numerator– This occurs if the consolidation loan defaults within the CDR that is applicable to the underlying loan(s)

– LRDR includes a Consolidation Indicator

V l• Values are:

• 1 = Consolidation Loan

• 2 = Underlying Loan

• Blank See CDR Guide, Pages 2.1‐10 & 2.3‐16

FFY 2011 Consolidation ExampleLDA = 3/20/11

Default = 11/25/12

10/01/11 9/30/12

FFY 2012

10/01/10 9/30/11

FFY 2011

10/01/12

FFY 2013

DER = 9/21/11

9/30/13

C lid tiConsolidation11/1/11

2011 3‐YR CDR

02/18/2014

6

When are the CDRs released?

• Draft rates– Released in February

• Official rates

– Released in September– Not public– No sanctions or benefits

apply

p

– Public

– Sanctions and benefits apply

• Draft 2011 3YR

C l l ti 1/11/2014

• Official 2011 3YR

C l l ti 7/26/2014

Technical Update GA‐2014‐01

– Calculation 1/11/2014

– Release 2/18/2014

– Calculation 7/26/2014

– Release 9/15/2014

When must a draft CDR challenge be submitted?

02/18/2014

7

What is the submission timeframe?

• School must submit the Challenge within 45 days of the timeframe begin date set by EDthe timeframe begin date set by ED

– The timeframe begin date is the sixth business day after the draft CDR release date

• FY 2011 3YR CDR IDC timeframe

– Begin date: Feb. 26, 2014

– End date: April 11, 2014p ,

• Data Manager must respond within 30 days from the date the timely challenge is received from the school

– DPM sets response date

Challenging the Draft Rates

02/18/2014

8

Why challenge the draft rate?

Benefits of Low Official CDRs

• Institutions with official CDRs below 15% for the 3 most recent fiscal years for which data is availablemost recent fiscal years for which data is available are eligible for benefits

– Effective for loans first disbursed on or after 10/1/2011

• Benefits:

– Exempt from 30‐day delay of first disbursement for first‐time freshman borrowerstime freshman borrowers

– Exempt from the requirement for multiple disbursements for a single term loan

02/18/2014

9

Impact of High Official CDRs

• Loss of low CDR benefits (see previous slide)

• If one 3YR CDR is greater than 30%If one 3YR CDR is greater than 30%– Default prevention plan required (34 CFR 668.217)

– New Submission Overview available at: http://www.ifap.ed.gov/DefaultManagement

• If the 3 most recent 3YR official CDRs are each greater than 30%– Loss of Direct Loans and Pell eligibilityg y

– Third 3YR official CDR (FY2011) will be released in Sept. 2014

• If the most recent official CDR is greater than 40%– Loss of Direct Loan program eligibility

34 CFR Subpart M 668.187

What are the draft rate challenges?

02/18/2014

10

Draft CDR Challenges

• Incorrect Data Challenge (IDC)

C t i t d t i th L R d D t il R t– Correct incorrect data in the Loan Record Detail Report (LRDR) before the official CDRs are released

– CDR Guide Section 4.1

• Participation Rate Index challenge

– Demonstrate a low borrower participation rate to avoid an anticipated sanction with the official CDR p

– CDR Guide Section 4.2

Incorrect Data Challenge (IDC)

• An IDC is how a school requests a correction to what it believes to be inaccurate data in the school’s LRDRit believes to be inaccurate data in the school s LRDR of the draft CDR

• If an IDC is successful, NSLDS is to be corrected, and the corrected data is used for calculating the school’s official CDR

• If a school does submit an IDC, the school cannot l h f h ffi i l CDR d ilater contest the accuracy of the official CDR data in an Uncorrected Data Adjustment (UDA) or an Erroneous Data Appeal (EDA) based on disputed data

02/18/2014

11

What can be challenged in an IDC?

Incorrect Data Challenges

• Borrower’s data was incorrectly reportedy p

• Borrower was incorrectly included

• Borrower was incorrectly excluded

02/18/2014

12

IDC Allegations

• See CDR Guide, Pages 3.1, 9‐12 for allegations related:related:

– Incorrect date entered repayment

– Incorrect default status

– Incorrect inclusion due to multiple loans

– Incorrect inclusion of borrower

– Incorrect exclusion of borrowerIncorrect exclusion of borrower

When does a loan enter repayment?

• A loan enters repayment after a 6‐month grace period that begins when a borrower ceased to beperiod that begins when a borrower ceased to be enrolled at least half‐time

– Graduates, withdraws, or drops below half‐time

• LDA/LHD + 6 months + 1 day = official repay date

– This date is generally used to determine which cohort year the borrower is included in for calculationthe borrower is included in for calculation

See CDR Guide, Page 2.1 – 9

LDA = 5/15/2010 6‐month Grace Period + 1 day Repayment Date = 11/16/2010

02/18/2014

13

When is a loan in default?

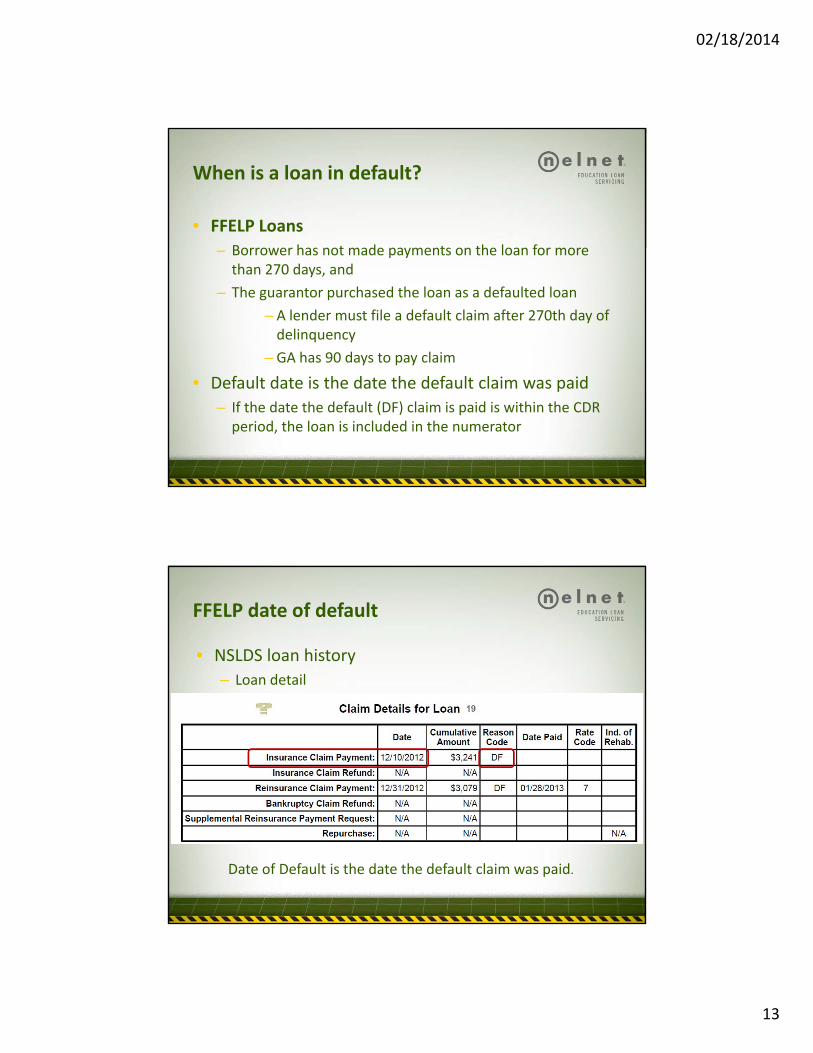

• FFELP Loans

B h t d t th l f– Borrower has not made payments on the loan for more than 270 days, and

– The guarantor purchased the loan as a defaulted loan

– A lender must file a default claim after 270th day of delinquency

– GA has 90 days to pay claim

• Default date is the date the default claim was paid

– If the date the default (DF) claim is paid is within the CDR period, the loan is included in the numerator

FFELP date of default

• NSLDS loan history

– Loan detail

Date of Default is the date the default claim was paid.

02/18/2014

14

When is a loan in default?

• Direct Loans (and ED held FFELP loans)

B h t d t th l f 270 d– Borrower has not made payments on the loan for 270 days

– A loan is considered in default for CDR purposes after 360 consecutive days of delinquency

– If the date the loan reaches 361 consecutive days of delinquency is in the CDR period, the loan is included in the numerator

Direct Loan Date of Default

• NSLDS loan history

L d t il– Loan detail

02/18/2014

15

How does rehabilitation affect CDRs?

• In order to rehabilitate a defaulted loan, the borrower must make 9 monthly on‐time payments within a 10‐y p ymonth period

• If the borrower rehabilitates the loan before the end of the CDR period, the borrower is not included in the numerator– 3YR 2011 CDR: Must complete rehab by 9/30/2013

• If the borrower rehabilitates the loan after the end of theIf the borrower rehabilitates the loan after the end of the CDR period, the borrower is included in the numerator– 3YR 2011 CDR: Rehab completed after 9/30/2013

See CDR Guide, Page 2.1 – 10

Date of Rehabilitation on NSLDS

• NSLDS loan history

L d t il– Loan detail

02/18/2014

16

CDR Calculation

Numerator

Refined for Rehabilitation

Denominator

55.05.055 or 5.5%10 20

FY 11 FY 12 FY 13

=45

.045 or 4.5%

Rehabs‐1025

1000 1000

Special Circumstances

• See CDR Guide pages 2.1, 12‐15 for:

– Special circumstances involving schoolsp g

– Special circumstances involving repayment

– Special circumstances involving loans that were discharged, canceled, or refunded

– Special circumstances involving loans that were repurchased

02/18/2014

17

Special Circumstances

• Situation: Borrower transfers to a subsequent school before grace period expiresbefore grace period expires

• Case study: – Student borrowed 2 loans while attending School A and then withdrew 8/13/2010

• Grace period did not expire between enrollments

– Student enrolled FT at School B on 1/10/2011 and then withdrew on 2/15/2011withdrew on 2/15/2011

– DER for loans borrowed at both schools is 8/16/2011; FY11

• Effect on denominator: Borrower is included in the cohort year when borrower entered repayment

Special Circumstances

• Situation: Borrower borrows loans at more than 1 school

• Case study:Case study:– Student borrowed 2 loans at School A and was HT until

withdrawing on 8/13/2010

– Student enrolled FT at School B on 8/15/11, borrowed 2 loans, and then withdrew 5/8/2012

• Grace period expired between enrollments

– DER for loans borrowed at School A = 2/14/2011; FY 11

– DER for loans borrowed at School B = 11/9/2012; FY 13

• Affect on denominator: Borrower is included in the cohort years when the borrower entered repayment for each school where the borrower obtained loans

02/18/2014

18

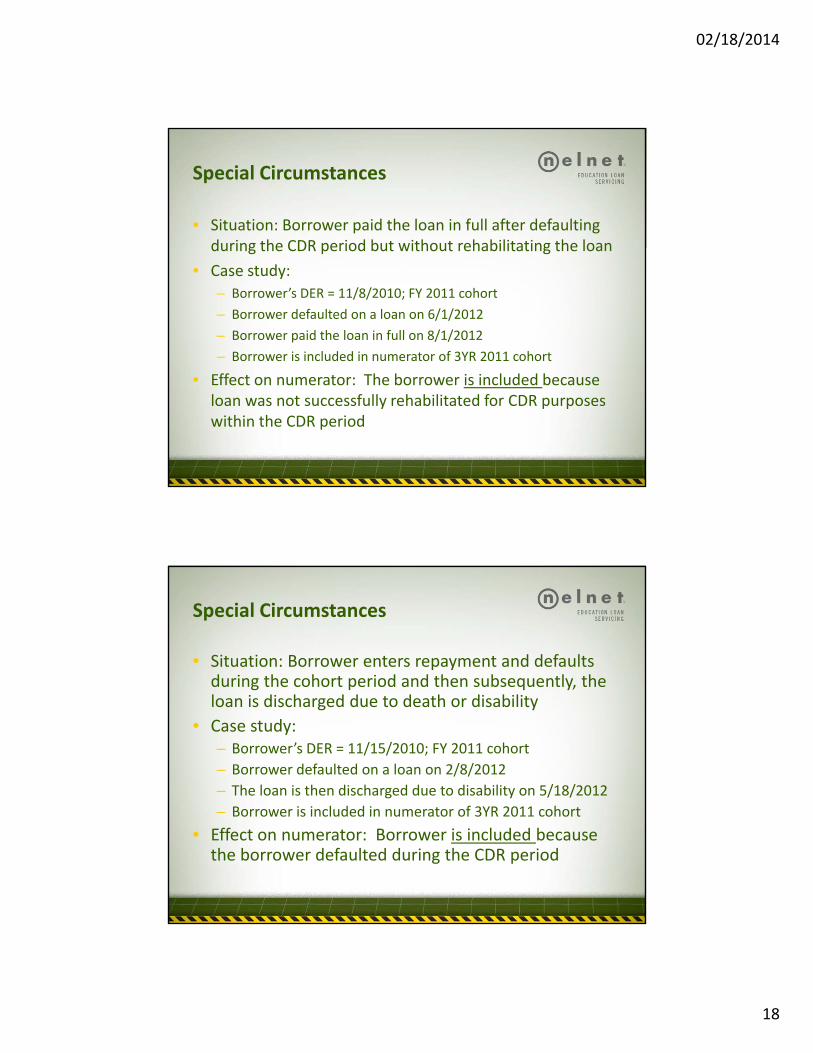

Special Circumstances

• Situation: Borrower paid the loan in full after defaulting during the CDR period but without rehabilitating the loanduring the CDR period but without rehabilitating the loan

• Case study:

– Borrower’s DER = 11/8/2010; FY 2011 cohort

– Borrower defaulted on a loan on 6/1/2012

– Borrower paid the loan in full on 8/1/2012

– Borrower is included in numerator of 3YR 2011 cohort

• Effect on numerator: The borrower is included because loan was not successfully rehabilitated for CDR purposes within the CDR period

Special Circumstances

• Situation: Borrower enters repayment and defaults during the cohort period and then subsequently, theduring the cohort period and then subsequently, the loan is discharged due to death or disability

• Case study:– Borrower’s DER = 11/15/2010; FY 2011 cohort

– Borrower defaulted on a loan on 2/8/2012

– The loan is then discharged due to disability on 5/18/2012

– Borrower is included in numerator of 3YR 2011 cohort

• Effect on numerator: Borrower is included because the borrower defaulted during the CDR period

02/18/2014

19

Other Circumstances & Allegations

• Split servicing– Not a valid allegationNot a valid allegation

– Must demonstrate data is incorrect

• Borrower did not receive full grace period– If a borrower defaulted, the default cannot be removed by the Federal Loan Servicers

– The DER and date of default (DD) can only be changed to later date based on the correct DERlater date based on the correct DER

– If DM agrees to update DER for a defaulted Direct Loan, the DD should be recalculated to be 360th day of delinquency based on the updated DER

How do we challenge for incorrect data?

02/18/2014

20

Obtain the Loan Record Detail Report

• ED sends the eCDR package to each school through SAIG destination pointSAIG destination point– Cover letter

– Reader‐friendly LRDR

– Extract‐type LRDR

• May request electronic LRDR via NSLDS– https://www.nsldsfap.ed.gov

– NSLDS “Report” tab

– Delivered to SAIG mailbox

– See CDR Guide, Chapter 2.2

What’s in an LRDR?

• LRDR gives details of each borrower included

N d SSN– Name and SSN

– Loan status

– Date entered repayment

– Date of default (if applicable)

– Loan type (FFELP or Direct)

– How loan is counted in CDRHow loan is counted in CDR

• Numerator, denominator, both, or neither

02/18/2014

21

Loan Record Detail Report (LRDR)

• Review Chapter 2.3 of the Cohort Default Rate Guide for information on how to read the LRDRfor information on how to read the LRDR

– Chapter 2.3 Part 2: LRDR Reader‐Friendly Format

– Chapter 2.3 Parts 3 & 4: LRDR Electronic Extract File

– http://www.ifap.ed.gov/DefaultManagement/guide/CDRGuidePart2.html

LRDR Codes

• The Usage Code Identifies how the loan is counted in the CDR calculationthe CDR calculation

CDR Guide Page 2.3‐7

02/18/2014

22

Review the LRDR Data

• Compare the information in the LRDR to the school’s own records and NSLDS to ensure the accuracy ofown records and NSLDS to ensure the accuracy of the data

• Remember that you are looking for:

– Data incorrectly reported

– Borrowers incorrectly included

Borrowers incorrectly excluded– Borrowers incorrectly excluded

Is a borrower incorrectly included?

• Review details for the borrowers who defaulted (the numerator)numerator)– Determine when each borrower left school or ceased to be enrolled at least half‐time

– Determine when each borrower should have entered repayment

– Confirm that the date they entered repayment actually falls within the cohort time frame

• Submit a challenge of any defaulted borrowers in the numerator who did not enter repayment during that period

02/18/2014

23

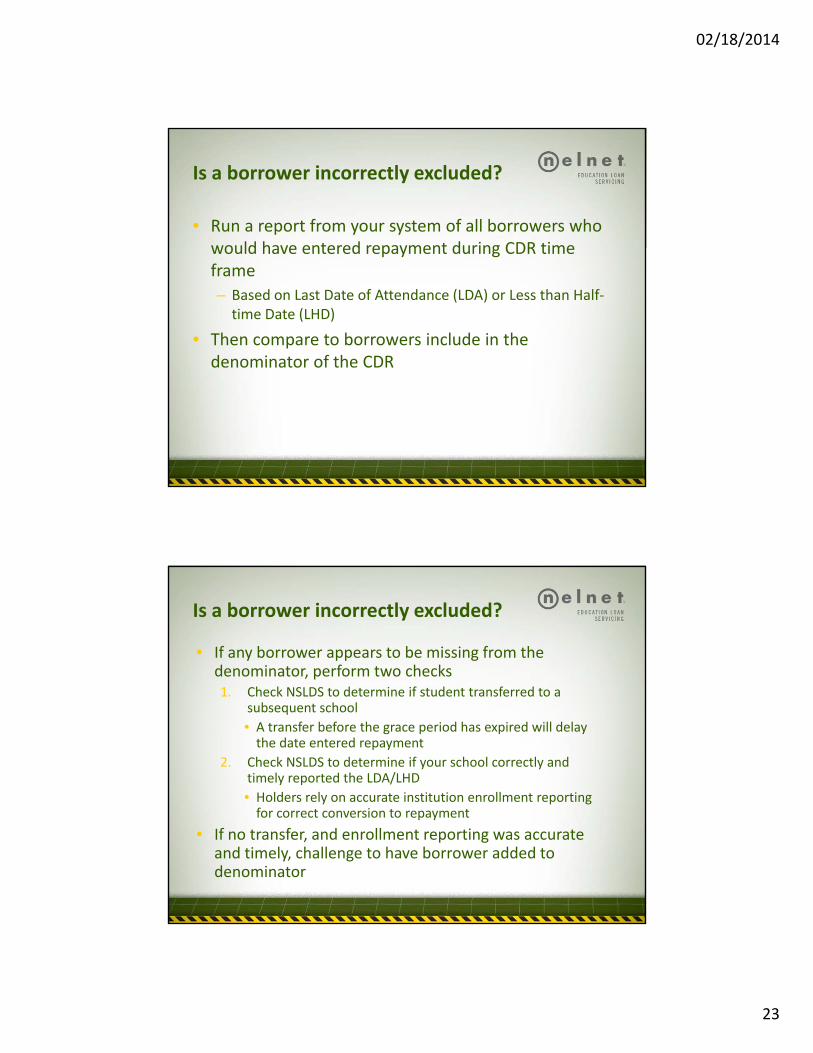

Is a borrower incorrectly excluded?

• Run a report from your system of all borrowers who would have entered repayment during CDR timewould have entered repayment during CDR time frame

– Based on Last Date of Attendance (LDA) or Less than Half‐time Date (LHD)

• Then compare to borrowers include in the denominator of the CDRdenominator of the CDR

Is a borrower incorrectly excluded?

• If any borrower appears to be missing from the denominator, perform two checks1. Check NSLDS to determine if student transferred to a

subsequent school

• A transfer before the grace period has expired will delay the date entered repayment

2. Check NSLDS to determine if your school correctly and timely reported the LDA/LHD

• Holders rely on accurate institution enrollment reporting for correct conversion to repayment

• If no transfer, and enrollment reporting was accurate and timely, challenge to have borrower added to denominator

02/18/2014

24

LDA and Repayment Date (DER)

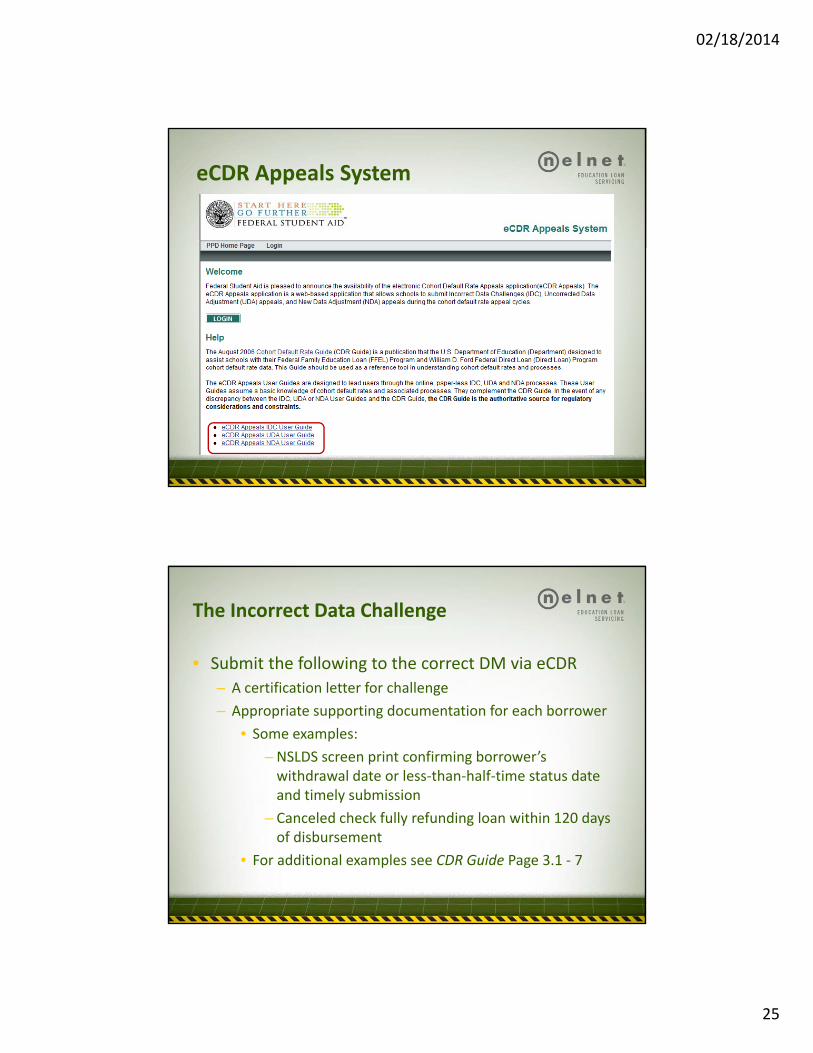

eCDR Appeals System

• Must submit challenge electronically through eCDR

D t M d i CDR– Data Managers respond via eCDR

– https://ecdrappeals.ed.gov

• Website also provides

– CDR Guide – revised September 2012

• IDC, UDA, NDA

FAQs– FAQs

– School demonstration sessions

• IDC, UDA, NDA

02/18/2014

25

eCDR Appeals System

The Incorrect Data Challenge

• Submit the following to the correct DM via eCDR

A tifi ti l tt f h ll– A certification letter for challenge

– Appropriate supporting documentation for each borrower

• Some examples:

– NSLDS screen print confirming borrower’s withdrawal date or less‐than‐half‐time status date and timely submission

– Canceled check fully refunding loan within 120 days of disbursement

• For additional examples see CDR Guide Page 3.1 ‐ 7

02/18/2014

26

What is the Data Manager’s role?

• Data Manager holding the loan reviews the challenge

M t i d i i ithi 30 d f i i• Must issue a decision within 30 days of receiving challenge via eCDR

• If agrees that a change should be made, corrects data in its internal system and NSLDS

– Prior to date for calculation of the official CDRs

What is the DPM’s role in IDCs?

• DPM (or OPD) Reviews Data Manager responses to incorrect data challenges (IDCs) submitted byincorrect data challenges (IDCs) submitted by schools to ensure that the responses are correct

• Default Prevention and Management (DPM) website

– http://www.ifap.ed.gov/DefaultManagement/DefaultManagement.html

• Contact information:• Contact information:

– Phone: 202‐377‐4259 (OPD hotline)

– Email: [email protected]

02/18/2014

27

NSLDS and CDRs

• Transition from 2YR to 3YR CDRs will be complete when the official 2011 3 YR CDR are released inwhen the official 2011 3‐YR CDR are released in September 2014

• Enhancements to NSLDS website

– All cohort default rates will display on NSLDS

• Under “Org” tab

LRDR is available for all rates– LRDR is available for all rates

What resources are available?

02/18/2014

28

Cohort Default Rate Guide

• http://ifap.ed.gov/DefaultManagement/CDRGuideMaster.html

• Provides Information on:– How rates are calculated

– How schools get rates and data

– Reviewing the LRDR

– Challenges, Adjustments, & Appeals

• FAQs are available• FAQs are available– http://www.ifap.ed.gov/DefaultManagement/faq/FAQ.html#faq01

FSA Data Center

• http://studentaid.ed.gov/about/data‐center/student/default

• Links to:• Links to:

– Searchable CDR database

– Lifetime CDRs

02/18/2014

29

Acronym Key

Acronym Meaning

CDR Cohort Default Rate

DD Date of Default

DER Date entered repayment

DPM/OPD Default Prevention Management/Operations Performance Division

ED U.S. Department of Education

FFY Federal Fiscal Year

IDC Incorrect Data Challenge

LDA Last date of attendance

LHD Less than half‐time date

LRDR Loan Record Detail Report

SAIG Student Aid Internet Gateway

Questions?

Julia Alexander

C li & T i i OffiCompliance & Training Officer

303.696.3606

Nelnet is glad to help schools access all the information needed to make their jobs easierNelnet is glad to help schools access all the information needed to make their jobs easier and to best help students. We cannot offer opinion or interpretation of FSA policies in all circumstances. If you have specific questions about your programs and procedures, we

recommend that you contact FSA.