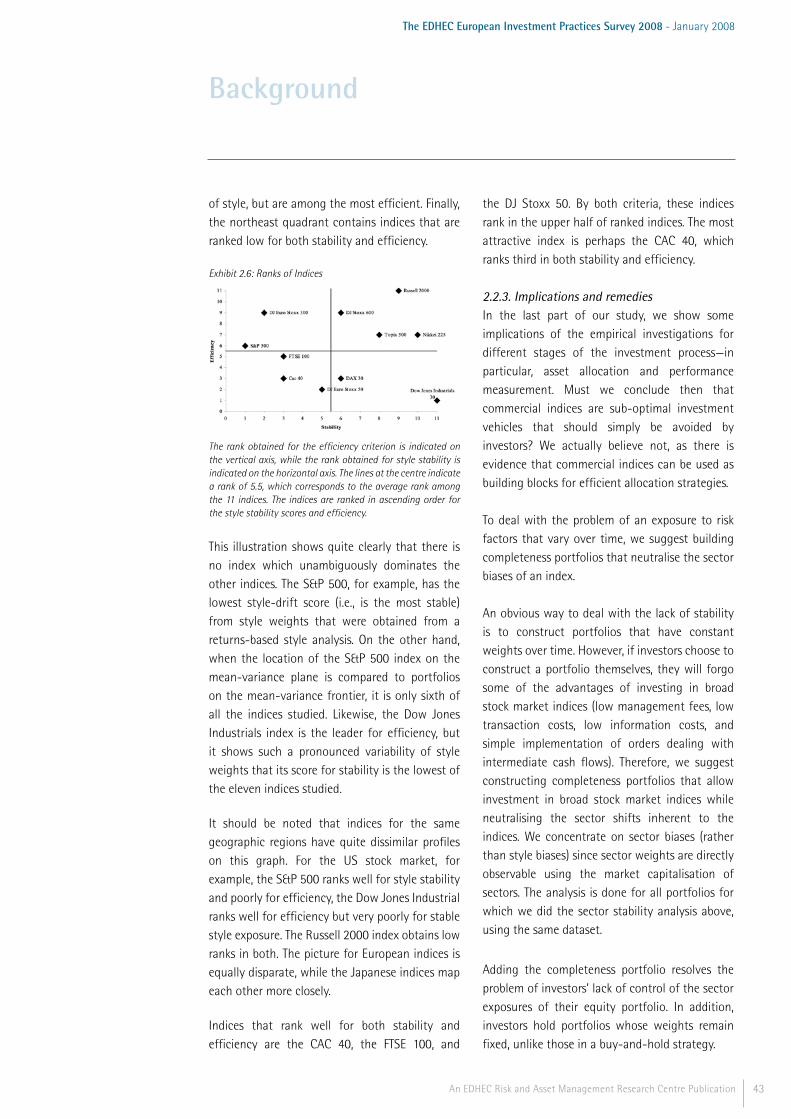

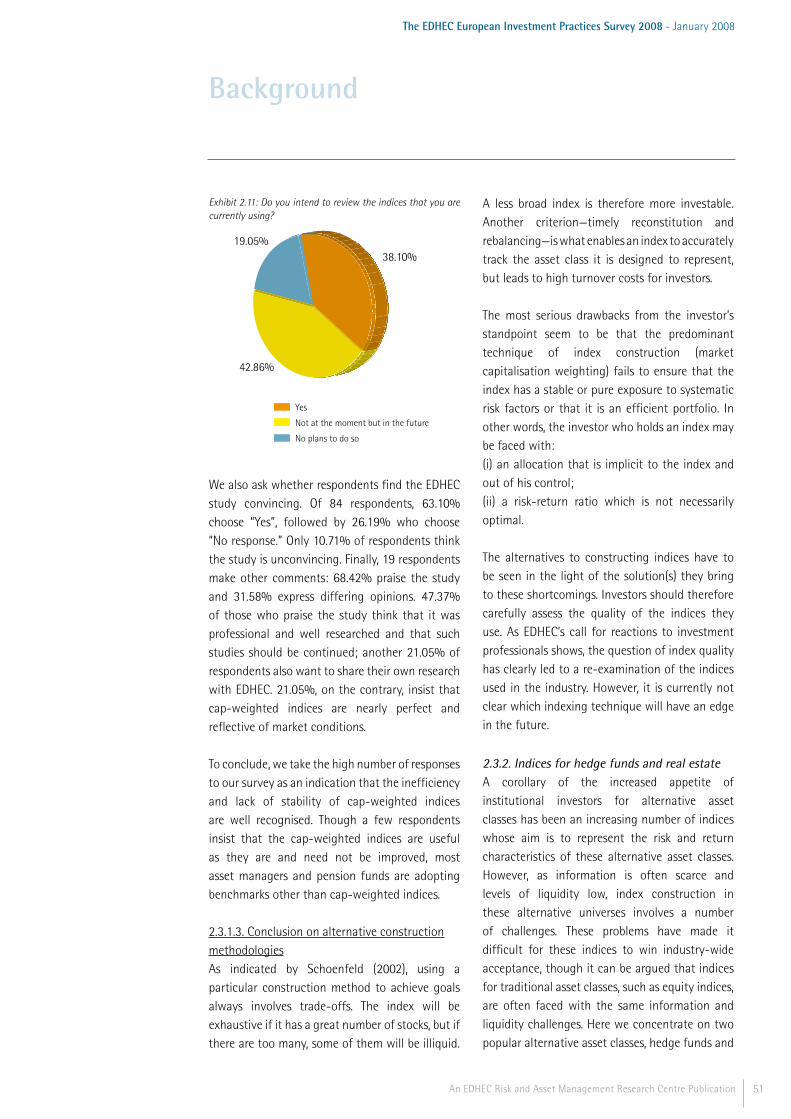

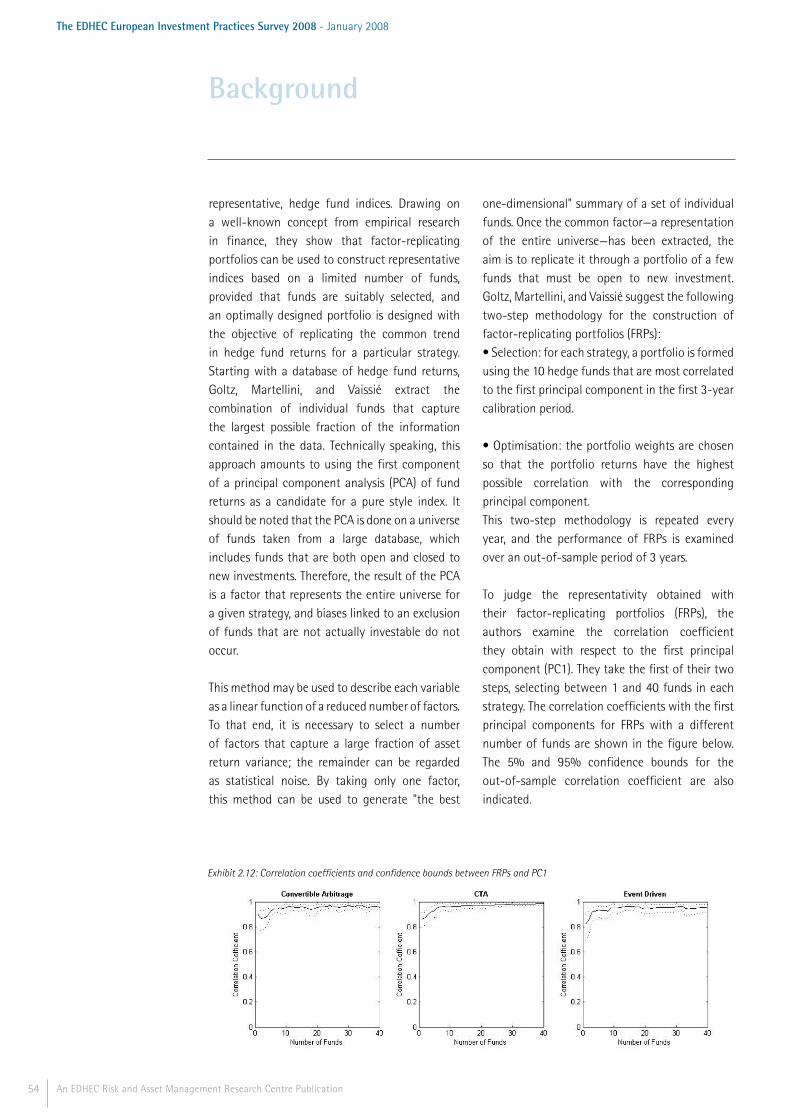

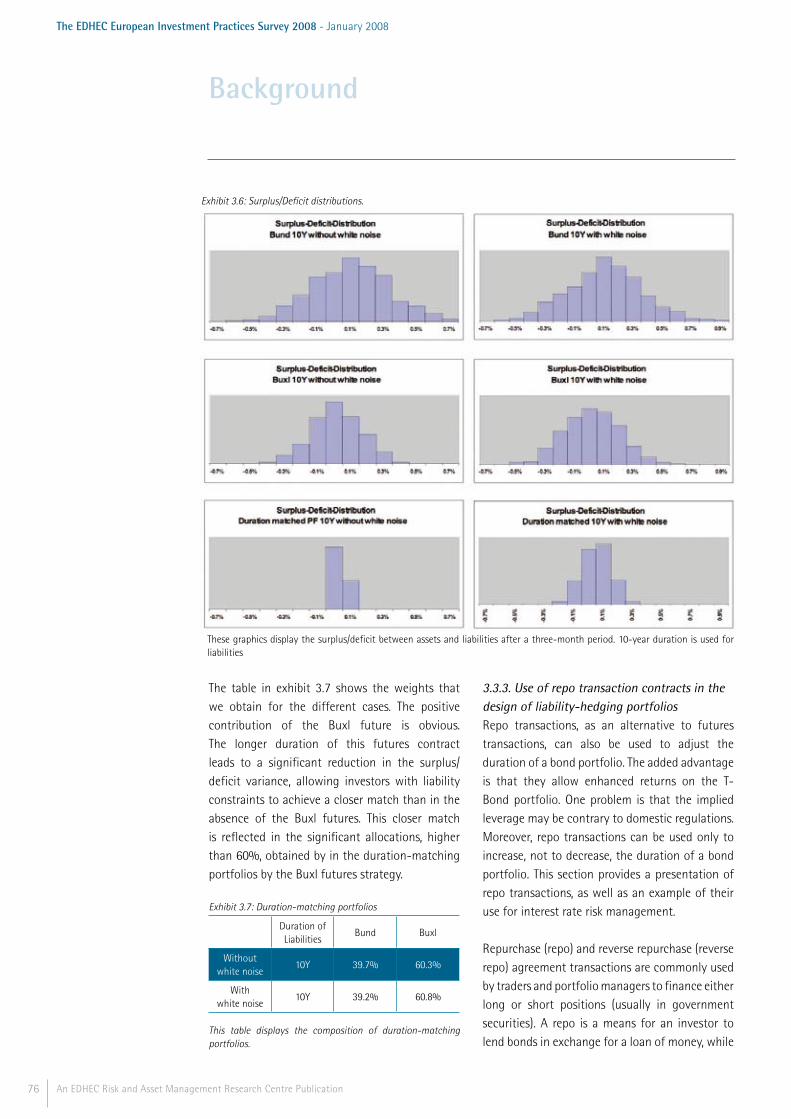

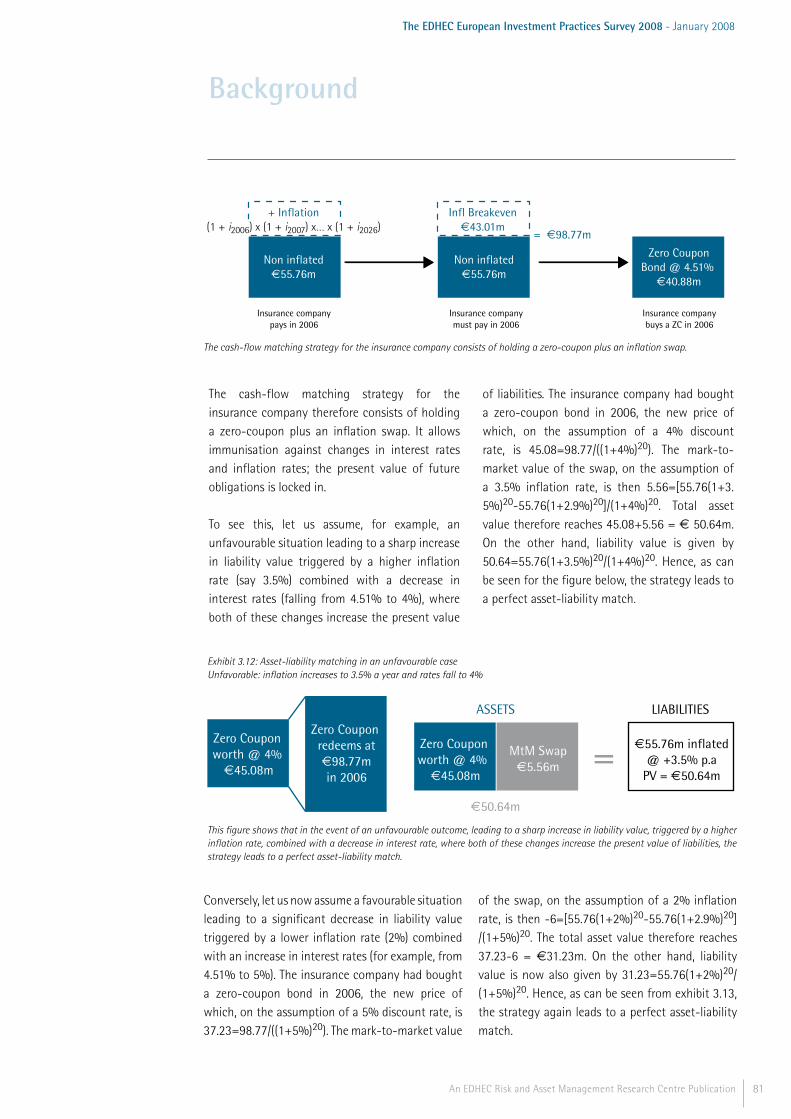

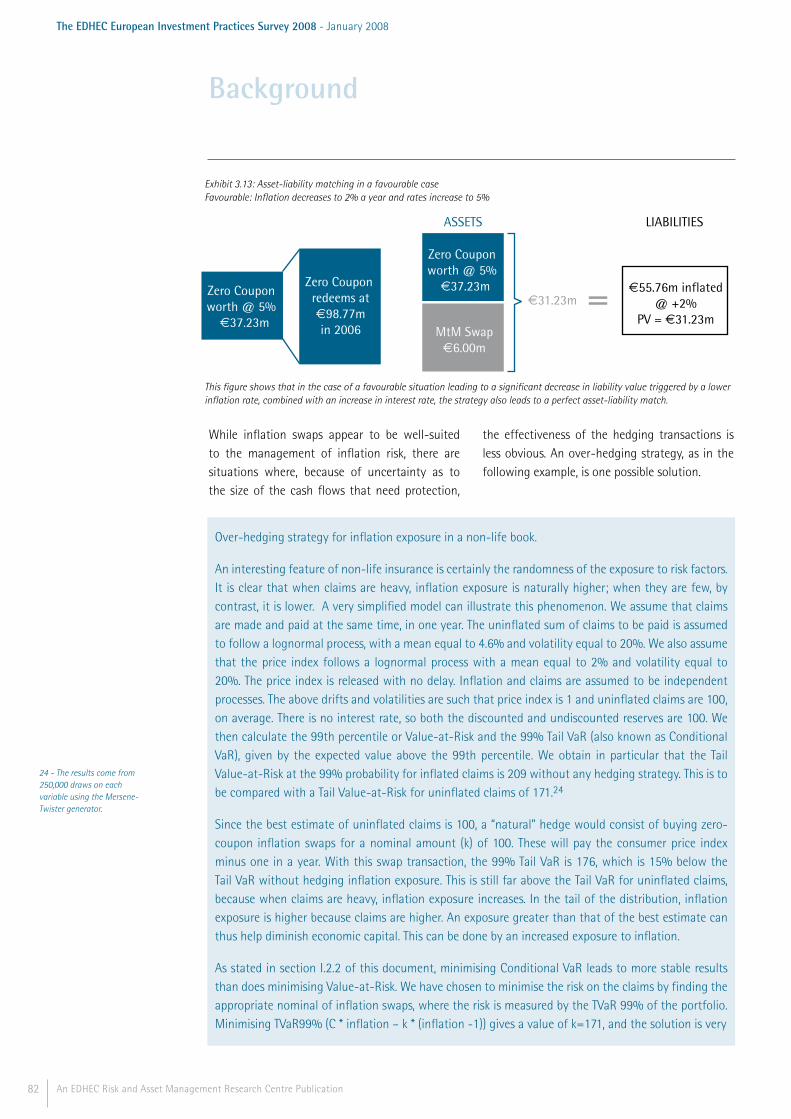

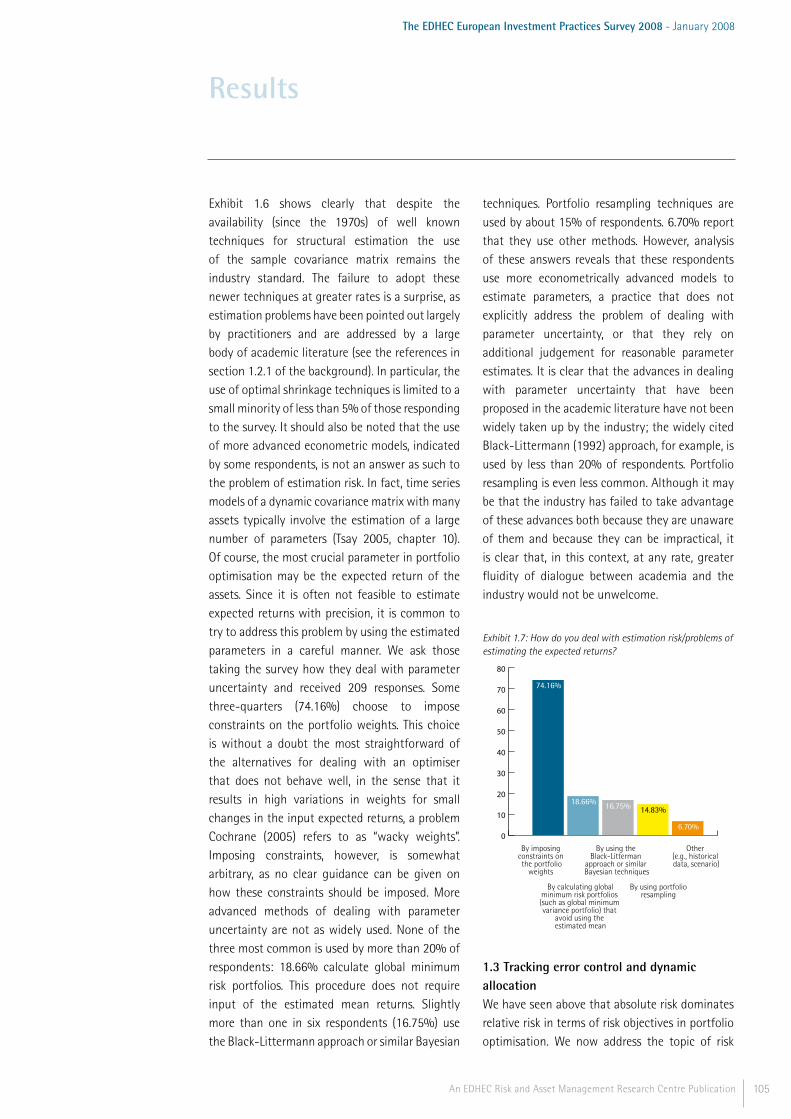

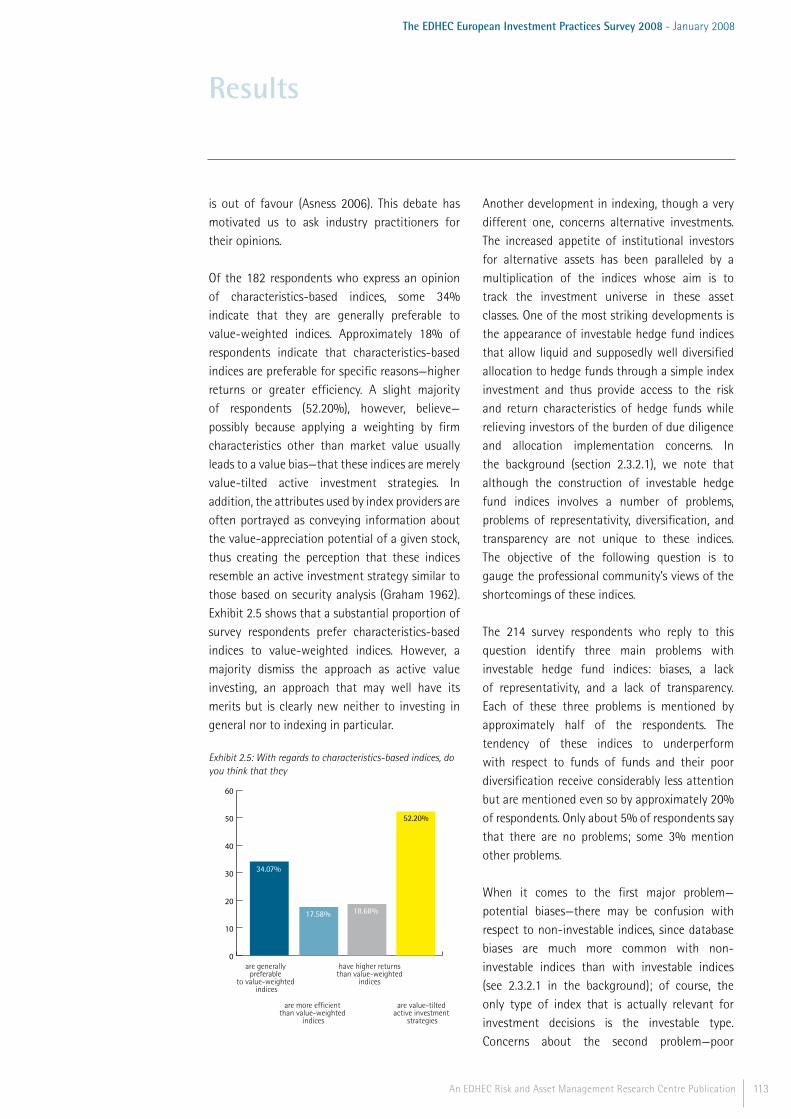

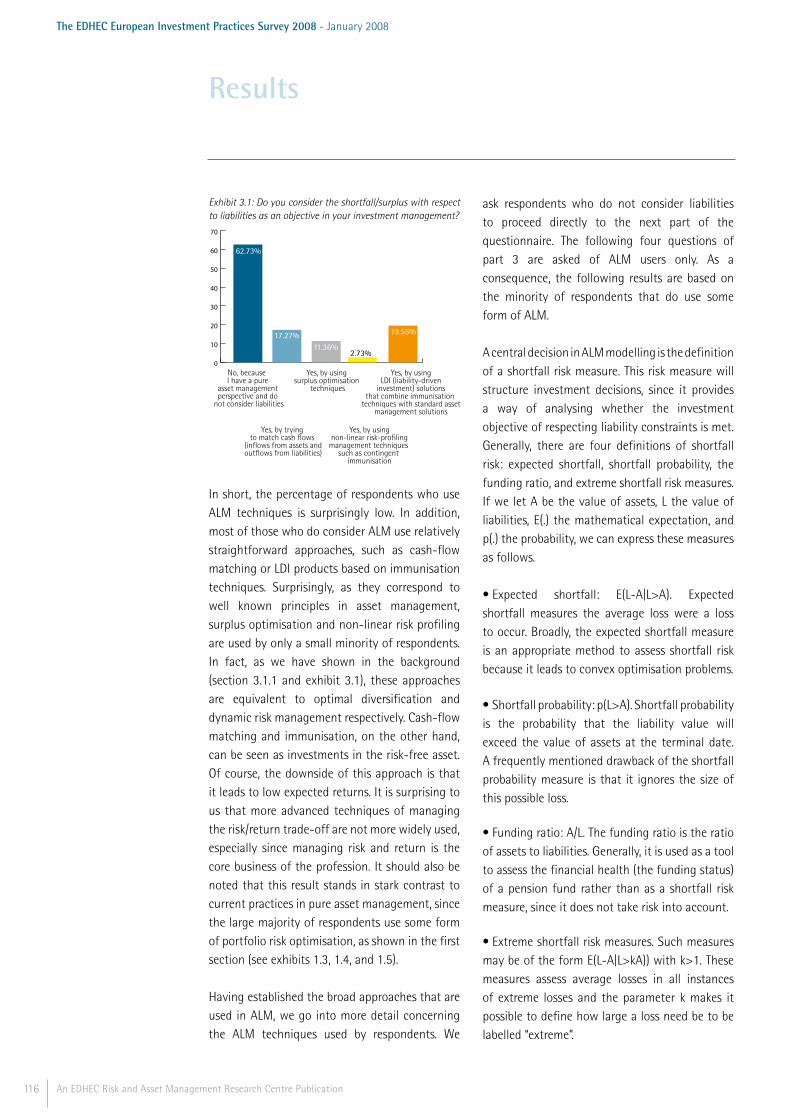

156

The EDHEC European Investment Practices Survey 2008 January 2008 An EDHEC Risk and Asset Management Research Centre Publication Sponsored by

The EDHEC European Investment Practices Survey

2008January 2008

An EDHEC Risk and Asset Management Research Centre Publication

Sponsored by

Foreword ............................................................................................................................................. 3

Methodology ..................................................................................................................................... 5

Executive Summary ........................................................................................................................ 11

Background ......................................................................................................................................17

1. Risk and Asset Allocation ...................................................................................................................... 18

2. Indices and Benchmarks ....................................................................................................................... 38

3. Asset Liability Management ................................................................................................................ 60

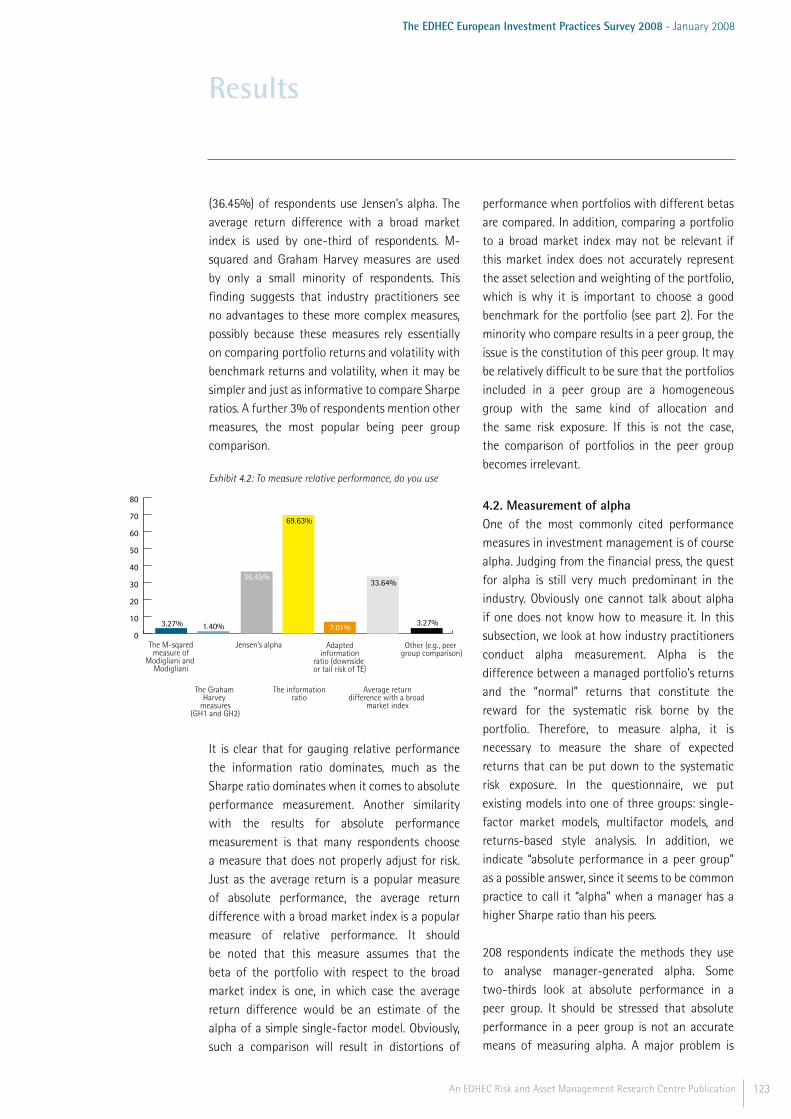

4. Performance Measurement ................................................................................................................. 83

Results ................................................................................................................................................99

1. Risk and Asset Allocation .................................................................................................................. 100

2. Indices and Benchmarks .....................................................................................................................108

3. Asset Liability Management .............................................................................................................. 114

4. Performance Measurement ...............................................................................................................121

Conclusion ...................................................................................................................................... 127

References ......................................................................................................................................131

Glossary ............................................................................................................................................141

About the EDHEC Risk and Asset Management Research Centre ................................ 148

About Newedge .............................................................................................................................151

Table of Contents

Published in France, January 2008. Copyright EDHEC 2008.The opinions expressed in this survey are those of the authors and do not necessarily reflect those of EDHEC Business School and Newedge.

3An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

Since it was set up in 2001, the EDHEC Risk and Asset Management Research Centre has monitored practices in the European asset management industry. The Centre’s surveys on the state of the industry look specifically at industry use of recent research advances and at best practices. These surveys have shed light on portfolio risk management, the use of indices and benchmarks, funds of hedge fund management, alternative diversification, and real estate investment.

The EDHEC Risk and Asset Management Research Centre has always made a point of doing research that is both independent and pragmatic. Our determination to make our research relevant and operational led us, in 2003, to publish the first studies on the policies of the European asset management industry. The initial EDHEC European Asset Management Practices survey compared the academic state-of-the-art in the areas of portfolio management and risk and the practices of European managers. This survey was complemented in the same year by a review of the state-of-the-art and the practices of European alternative multimanagers, the EDHEC European Alternative Multimanagement Practices survey, and followed by the EDHEC Funds of Hedge Funds Reporting survey, a survey that enabled us to observe the gap between the conclusions of academic research and the practices of multimanagers. In late 2006, as part of our indices and benchmarking research programme, we also produced the EDHEC European ETF Survey 2006, a major survey on the use of exchange traded funds by institutional investors in Europe.

The EDHEC European Investment Practices Survey 2008 has enabled us to compare industry practices and academic research in the fundamental areas of investment management. The three major components of the survey are an explanation of the methodology, a background (including a brief history of academic research into risk and asset allocation, indices and benchmarks, asset-liability management, and performance measurement), and, finally, the results, a presentation and analysis of the responses to our questionnaire as well as ten key conclusions.

We would like to extend our warmest thanks to Newedge, long-term partners for our industry surveys, whose support made the present survey possible. We are also grateful to Felix Goltz for coordinating the authors’ contributions, to Guang Feng for her help collecting the data, and to the publishing team led by Laurent Ringelstein.

Foreword

Noël AmencProfessor of FinanceDirector of the EDHEC Risk and Asset Management Research Centre

4 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

About the authors

Felix Goltz is a Senior Research Engineer and co-head of the Indices and Benchmark Research Programme with the EDHEC Risk and Asset Management Research Centre. His research focus is on the use of derivatives in portfolio management and the econometrics of realised and implied volatility. Felix studied economics and business administration at the University of Bayreuth, the Université de Nice Sophia Antipolis and EDHEC.He obtained his PhD in Finance from the Université de Nice Sophia Antipolis.

Véronique Le Sourd has a Master’s degree in Applied Mathematics from the Université Pierre et Marie Curie in Paris. From 1992 to 1996, she worked as research assistant in the Finance and Economics department of the French business school HEC and then joined the research department of Misys Asset Management Systems in Sophia Antipolis. She is currently a senior research engineer at the EDHEC Risk and Asset Management Research Centre.

The authors would like to thank Guang Feng, Daniel Mantilla and Niels van Heesewijk for able research assistance.

Noël Amenc is Professor of Finance and Director of Research and Development at EDHEC Business School, where he heads the Risk and Asset Management Research Centre. He has a Masters in Economics and a PhD in Finance and has conducted active research in the fields of quantitative equity management, portfolio performance analysis, and active asset allocation, resulting in numerous academic and practitioner articles and books. He is Associate Editor of the Journal of Alternative Investments and a member of the scientific advisory council of the AMF (French financial regulatory authority).

Lionel Martellini is Professor of Finance at EDHEC Business School and Scientific Director of the EDHEC Risk and Asset Management Research Centre. He holds graduate degrees in Economics, Statistics, and Mathematics, as well as a PhD in Finance from the University of California at Berkeley. Lionel is a member of the editorial board of the Journal of Portfolio Management and the Journal of Alternative Investments. An expert in quantitative asset management and derivatives valuation, Lionel has published widely in academic and practitioner journals, and has co-authored reference textbooks on alternative investment strategies and fixed-income securities.

Methodology

5An EDHEC Risk and Asset Management Research Centre Publ icat ion

6 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

The present survey focuses on the general investment practices of asset management firms, institutional investors, and private wealth managers. In the tradition of our surveys, it aims to give an account of the current practices in the industry and to compare these practices with the current state of the art as described by both academics and practitioners in the investment literature. A survey, however, is always subject to biases. The sources of these biases are the design of the questionnaire (the questions asked and the topics covered determine the results) as well as the sample of respondents, which may not be representative of the entire investment industry. To make these biases explicit, we will first describe the sample of participants that generated our results and then introduce the topics we have decided to address.

Survey ParticipantsOur survey is based on a questionnaire sent to industry participants in Europe from August 2, 2007 to October 1, 2007. The questionnaire generated responses from 229 institutions based in Europe. All 229 respondents specify their activities. A majority of the respondents (54%) are asset management or fund management companies. About one in four (24%) are institutional investors and pension funds. Private banks and family offices also make up a significant share (13%) of those responding to the questionnaire. Together, these three categories account for the large majority of our respondents. The remaining 9% are other investors such as consulting companies and investment banks.

Exhibit 1: Activities of the Respondents

Responses come from institutions with a wide range of assets under management. Overall, it can

be said that we cover all size categories and that the distribution over different size categories is quite smooth. In fact, one-quarter (24.89%) of the 229 respondents have less than €1 billion of assets under management. Slightly more than one-fifth (20.52%) of those responding to the survey manage between €1 billion and €5 billion. 7.42% manage between €5 billion and €10 billion; 18.34% between €10 billion and €50 billion, and 6.99% between €50 billion and €100 billion. Institutions with assets under management in excess of €100 billion make up a fifth (20.53%) of the responses. The remaining 1.31% do not indicate their AUM.

Exhibit 2: Range of Assets under Management of the Respondents

Below 1bn

1bn to 5bn

5bn to 10bn

10bn to 50bn

24.89%

20.52%

7.42%

18.34%

6.99%

1.31%

20.53%

50bn to 100bn

More than 100bn

No response

As is shown by the presence of almost 50 institutions managing in excess of €100 billion, our survey elicits responses from the major industry participants. At the same time, since these institutions account for only 20% of those responding to the survey, we can conclude that the responses we have received provide a fairly balanced view of asset management practices in institutions of all sizes.

The breakdown of survey respondents by country suggests that our confidence in the distribution of the sample in general is well placed. In fact, it is clear that most responses are obtained from institutions based in one of the three major European markets—the UK, France, and Switzerland. Each of these countries is home to between 16% and 21% of the

Methodology

Asset Management or FundManagement Companies

Institutional Investors/Pension Funds

Private Banks or Family Offices

Other (Consulting Companies, Investment Banks)

54.15%

24.02%

13.10%

8.73%

7An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

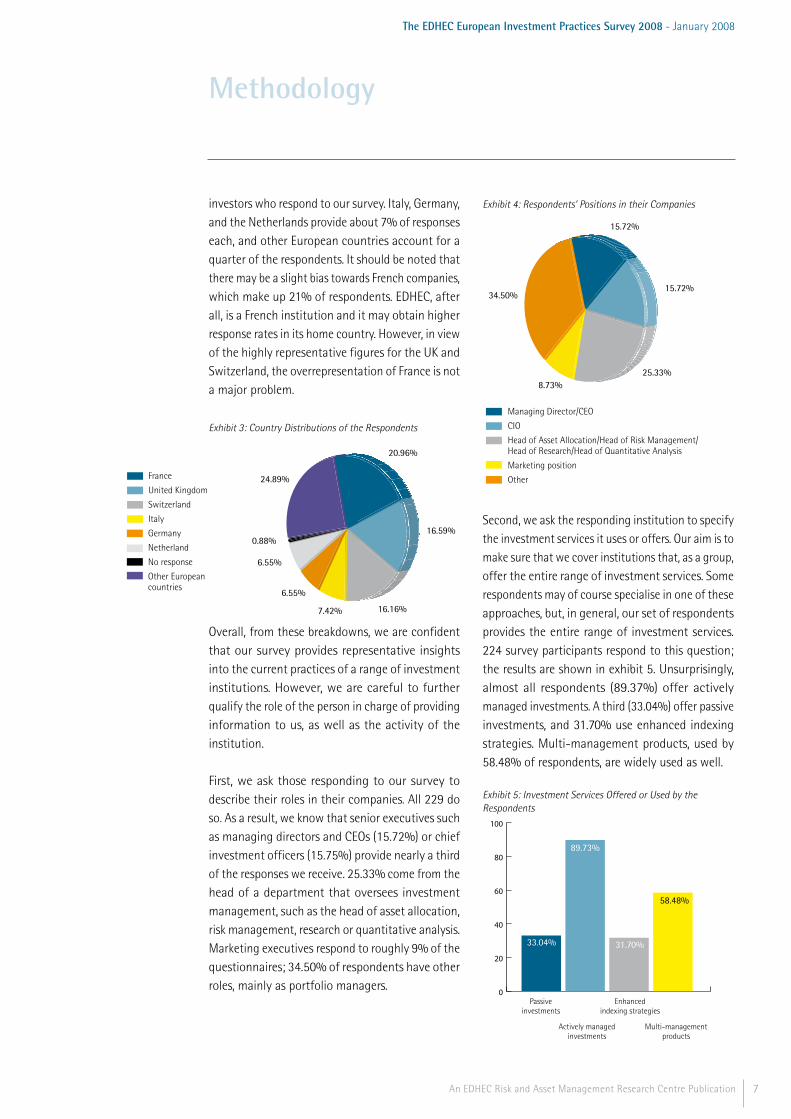

investors who respond to our survey. Italy, Germany, and the Netherlands provide about 7% of responses each, and other European countries account for a quarter of the respondents. It should be noted that there may be a slight bias towards French companies, which make up 21% of respondents. EDHEC, after all, is a French institution and it may obtain higher response rates in its home country. However, in view of the highly representative figures for the UK and Switzerland, the overrepresentation of France is not a major problem.

Exhibit 3: Country Distributions of the Respondents

Overall, from these breakdowns, we are confident that our survey provides representative insights into the current practices of a range of investment institutions. However, we are careful to further qualify the role of the person in charge of providing information to us, as well as the activity of the institution.

First, we ask those responding to our survey to describe their roles in their companies. All 229 do so. As a result, we know that senior executives such as managing directors and CEOs (15.72%) or chief investment officers (15.75%) provide nearly a third of the responses we receive. 25.33% come from the head of a department that oversees investment management, such as the head of asset allocation, risk management, research or quantitative analysis. Marketing executives respond to roughly 9% of the questionnaires; 34.50% of respondents have other roles, mainly as portfolio managers.

Exhibit 4: Respondents’ Positions in their Companies

Managing Director/CEO

CIO

Head of Asset Allocation/Head of Risk Management/Head of Research/Head of Quantitative Analysis

Marketing position

Other

25.33%

15.72%

8.73%

34.50%

15.72%

Second, we ask the responding institution to specify the investment services it uses or offers. Our aim is to make sure that we cover institutions that, as a group, offer the entire range of investment services. Some respondents may of course specialise in one of these approaches, but, in general, our set of respondents provides the entire range of investment services. 224 survey participants respond to this question; the results are shown in exhibit 5. Unsurprisingly, almost all respondents (89.37%) offer actively managed investments. A third (33.04%) offer passive investments, and 31.70% use enhanced indexing strategies. Multi-management products, used by 58.48% of respondents, are widely used as well.

Exhibit 5: Investment Services Offered or Used by the Respondents

0

20

40

60

80

100

58.48%

31.70%

89.73%

33.04%

Passiveinvestments

Enhancedindexing strategies

Actively managedinvestments

Multi-managementproducts

Methodology

France

United Kingdom

Switzerland

Italy

Germany

Netherland

No response

Other European countries

16.16%

16.59%

7.42%

6.55%

6.55%

0.88%

24.89%

20.96%

8 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

Overall, we are confident that the results are representative. Not only do we receive responses from 229 European institutions, but the breakdown of these institutions by assets under management and by country shows that we cover a range of institutions that corresponds broadly to the distribution found in the industry today. In addition, our respondents encompass the entire range of investment services. Finally, survey respondents are usually senior executives or high-level investment specialists.

Choice of TopicsHaving learnt in recent years about the risks of excessive reliance on asset selection models, investors and managers are showing unprecedented interest in asset allocation approaches as sources of performance. This heightened interest in asset allocation has led to innovation on two fronts. First, asset managers and investors are looking at increasingly sophisticated asset allocation methods in order to include more complex risk measures, the problem of parameter estimation, and investment constraints in the asset allocation process. Second, the emergence of alternative asset classes with risk profiles that are very different from those of traditional investments is creating new opportunities for asset allocation in both conceptual and operational terms. This innovation has an impact on the entire investment process, including asset allocation, risk management, and performance measurement. How these innovations have been adopted by industry practices is the focus of the present document. We decide to separate both the questionnaire and the background into four parts, each part addressing an important area of investment practice and the current developments in that area. Below, we address each topic in turn and point out what leads us to devote a large part of our survey to issues related to each topic.

First, we address the use of risk and asset management techniques. The techniques used in the industry are often rooted in academic publications. Often neglected in these publications, however, is the organisation of the investment process.

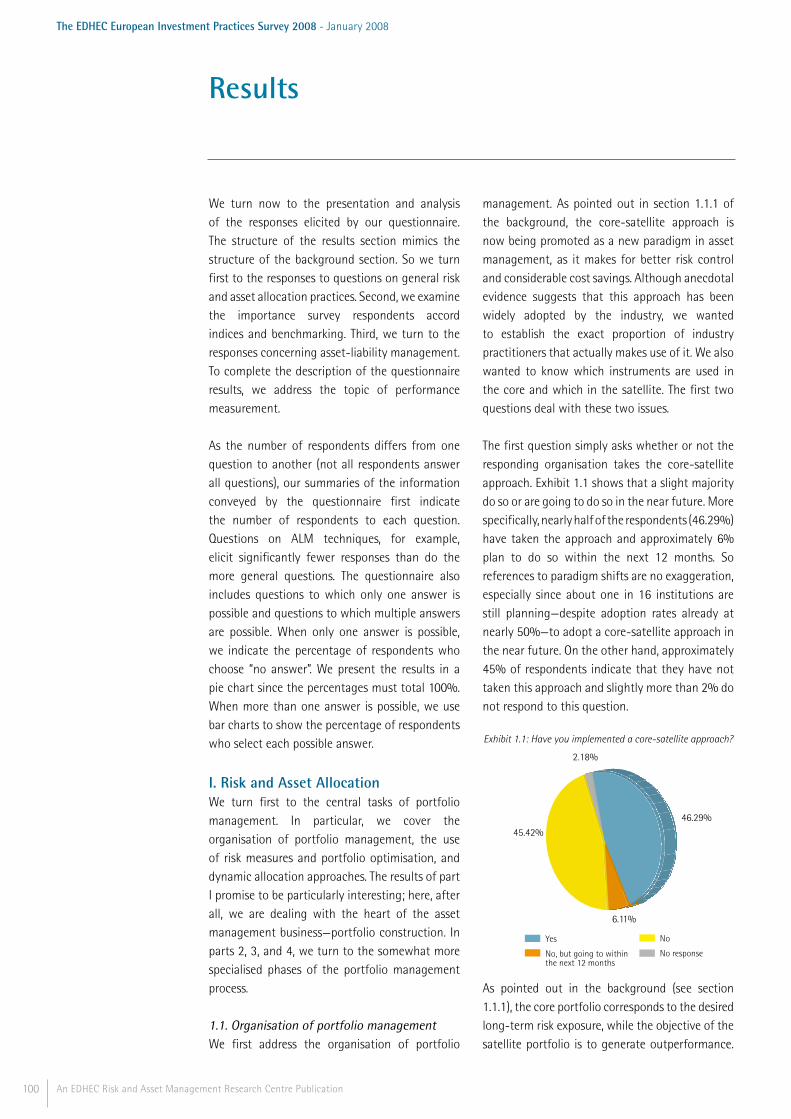

Recently, the industry has undergone a paradigm change with the adoption of core-satellite management. In this report, we emphasise the usefulness of this approach and establish to what degree it is actually used. In addition, since core-satellite management provides a basic framework, it is interesting to assess which instruments and asset classes are actually considered by practitioners within this framework. When used in practice, academic asset allocation models for portfolio management have come up against numerous obstacles. For example, mean-variance portfolio selection is known to suffer from an extreme sensitivity of weights to the input parameters, as well as from a definition of risk as portfolio volatility, a definition that does not necessarily reflect investor preferences. The solutions that have been proposed to improve portfolio choice models in practice thus revolve around changing the risk measure to more appropriate measures such as Value-at-Risk and around improving the estimation of input parameters. However, if we leave aside anecdotal evidence from industry conferences, it is not clear whether such techniques have been widely adopted. Moreover, the industry today is marked by a proliferation of dynamic trading strategies that are often marketed as structured products. Since the non-linear payoff of the structured product can be replicated by dynamic trading in the underlying asset and cash, a structured product will in effect correspond to a dynamic asset allocation strategy. Therefore, through investing in structured products it may be possible for investors to enjoy the benefits of dynamic asset allocation strategies while using the buy-and-hold investment approach they are comfortable with. However, from a conceptual standpoint, it is a challenge to integrate such strategies into broad asset allocation, since standard asset allocation approaches may not properly account for the non-linear nature of the products. In addition, there are other limits to the adoption of such strategies, including potential regulatory hurdles. One of the results of this survey is to show the dynamic strategies that are currently used and the proportion of institutions that actually use them.

Methodology

9An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

We then choose to look at the role of indices and benchmarks in portfolio management. While indices have played a significant role in performance measurement since the dawn of the industry, it should be emphasised that the number of investment products based on indices has multiplied over recent years—these products now include not only traditional index funds, but also exchange-traded funds, options, futures, and other derivatives. In addition to using indices for performance measurement, it is common for investors to use them for investment decision-making, i.e., in the investment processes and portfolio selection models described in the first topic. As part of the decision-making process, they are used either to find an optimal allocation to different indices or even to passively hold a single index that is assumed to be well diversified. However, the standard practice of using a capitalisation-weighting scheme for the construction of indices has been the target of harsh criticism. A number of papers (see, among others, Haugen and Baker 1991, Amenc, Goltz, and Le Sourd 2006, or Hsu 2006) point out that the mechanics of capitalisation weighting lead to trend-following strategies with inefficient risk/return trade-offs. In response to this criticism, equity indices with different weighting schemes now account for a share of index investment products. Of course, these investment products may be completely disregarded when it comes to actual investing, but indices are widely used as benchmark portfolios by investment managers, both for asset allocation and performance measurement purposes. For performance measurement, alternatives to using standard market indices include so-called normal portfolios or customised benchmarks, which are specifically designed to reflect the long-term risk exposure of a specific portfolio or manager, rather than the arbitrary risk exposure of a market index. In view of the many alternatives to standard market indices, it seems appropriate to provide a summary of—as well as some perspective on—recent developments in the area of indices and benchmarking. In addition, a very interesting question is how indexing innovations are perceived by investment practitioners and whether the numerous alternatives to standard

indices, such as customised benchmarks or new forms of indexing, are actually used by a significant proportion of investors and asset managers. And although indices have been in use for the equity class for decades, it is only recently that they have begun emerging for alternative asset classes. We describe the specific challenges to constructing these indices and attempt to establish whether practitioners believe that indexing is plausible when it comes to alternative asset classes. Third, we introduce the problem of asset-liability management (ALM) and describe how to implement a state-of-the-art ALM process. With ALM, it is possible to manage the constraints that stem from future commitments in an institutional investor's balance sheet. It should be noted that ALM is, in a sense, the most general form of asset management. In fact, the asset management techniques covered in the first topic may be perceived as a special case of ALM, where the benchmark return corresponds to the liabilities. Even in the absence of a benchmark, we can replace the latter with the risk-free rate. In practice, however, ALM techniques are largely limited to the investment processes of institutions such as pension funds, a limit that justifies their inclusion as a separate topic. The recent difficulties of liability-constrained investors have drawn attention to their investment practices. A so-called “perfect storm” of adverse market conditions at the turn of the millennium devastated many corporate defined benefit pension plans. Negative equity market returns eroded plan assets at the same time as declining interest rates increased the marked-to-market value of benefit obligations and contributions. In extreme cases, corporate pension plans were left with funding gaps as large as or larger than the market capitalisation of the plan sponsor. That institutional investors in general and pension funds in particular were so dramatically affected by the market downturns emphasises the weakness of investment practices. In particular, it has been argued that the asset allocation strategies implemented in practice, which used to be heavily skewed towards equities without any protection from their downside risk, were not consistent with sound

Methodology

10 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

liability risk management. In this context, a renewed interest in asset-liability management techniques has surfaced in institutional money management. New approaches referred to as liability-driven investment (LDI) solutions have appeared in the wake of recent changes in accounting standards and regulations that have led to an increased focus on liability risk management. As it happens, proposals for techniques to ensure the soundness of liability risk management are not in short supply. From an investor’s perspective, it is important to grasp the meaning of these techniques, to understand the structure of the offers, and to distinguish between real innovation and pure marketing. In the background, we provide an overview of current offers, as well as a theory of ALM. In the results, we compare the theory with current industry practices.

Our fourth topic is performance measurement. When it comes to the investment process, performance measurement is, after the phases completed with some of the techniques described above, the logical finale. Portfolio (or fund) performance evaluation is a key topic, both for managers, who want their skill to be recognised, and for investors, who are seeking the best investment product. The mutual fund market is highly developed and offers a wide range of products. The resulting competition among the different establishments has strengthened the need for clear and accurate portfolio performance analysis. For manager selection, investors want appropriate bases for comparison. They want to know if managers have reached their objectives—that is, if their return is high enough for the risks they have taken, how they compare to their peers, and, finally, whether the portfolio management results are to be put down to luck or to managerial skill that can continue to deliver these results. The portfolio return alone does not provide answers to all of these questions. So, as suggested by the growing body of academic and professional research into performance measurement, an active search for methods that provide information that meets investor expectations is underway. Besides models from portfolio theory, research in the area

of performance measurement has also dealt with real market conditions and developed techniques for cases where the restrictive assumptions of portfolio theory are not observed. At the same time, the choice of a performance measurement technique must reconcile ease of implementation and accuracy and comprehensibility of information. In the sections of this survey devoted to portfolio performance measurement, we provide background information on a range of performance measures and their underlying principles, as well as insights into currently used measures and procedures.

It should be noted that any organisation of the investment process is, to a certain extent, arbitrary. Different institutions may organise their investment processes in completely different ways. Our aim with this questionnaire is to facilitate responses by going from more general to more specific topics. In addition, we address the unifying themes of investment management rather than divide the survey into segments specific to each asset class or to each category of client. In fact, we believe that the common challenges underlying much of the investment process justify this choice. The remainder of the document will first review the investment literature on the four topics introduced in the background and then proceed to the original results of this survey, which reveals current perceptions and practices in the areas of risk and asset management, benchmarking and indices, asset liability management, and performance measurement.

Methodology

Executive Summary

11An EDHEC Risk and Asset Management Research Centre Publication

12 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

This survey assesses the current investment practices of asset management firms, institutional investors, and private wealth managers. Its aim is to give an account of the current practices in the industry and to contrast these practices with the recent state of the art in the investment literature. The survey results are based on a questionnaire that elicited more than two hundred responses from throughout Europe.

We address topics from four central areas of investment management practice: risk and asset allocation, indices and benchmarks, asset-liability management, and performance measurement. The questionnaire is fairly general and focuses on broad aspects and on broad classifications of approaches rather than on technical details. Our analysis of the responses shows that in practice there is a considerable diversity of methods and tools. Overall, however, the results provide evidence that many institutions, rather than fully exploiting the improved techniques that research has made readily available to them, currently settle for the most straightforward.

Risk and Asset Management TechniquesWe turn first to the central tasks of the portfolio management process. In this section, we cover the organisation of portfolio management and the techniques for portfolio optimisation.

Though the techniques used in portfolio optimisation are important for the resulting performance, the organisation of the portfolio management process itself must not be neglected. The core-satellite approach has recently been touted as a superior approach to portfolio management organisation, allowing as it does a clear separation of overperformance of the benchmark and choice of the benchmark management, along with considerable cost savings. The core-satellite approach is now widely used, with more than 50% of those responding to the questionnaire reporting that they use the approach or plan to do so

within the next 12 months. The results show, however, that a number of inconsistencies remain; it is not clear that this new approach is being used to its full potential. Among the inconsistencies are those revealed by the findings on the use of different management approaches within core-satellite portfolios. For example, traditional active management mandates are included in core portfolios, while alternative investments are mainly restricted to the satellite portfolio rather than used as diversifiers in the core. Moreover, it appears that the tracking error management methods that most clearly respect the separation of overperformance of the benchmark and choice of the benchmark have not been widely adopted: portable alpha methods are used by only about 20% of respondents and the completeness portfolio approach by less than 10%.

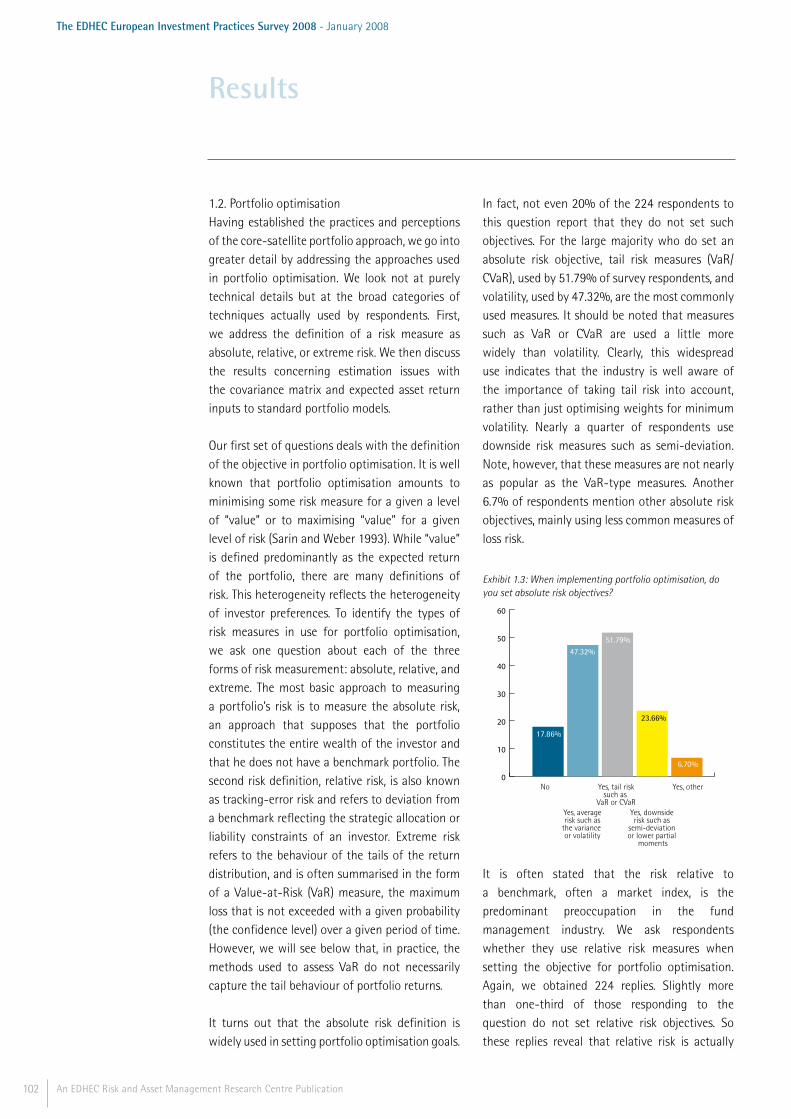

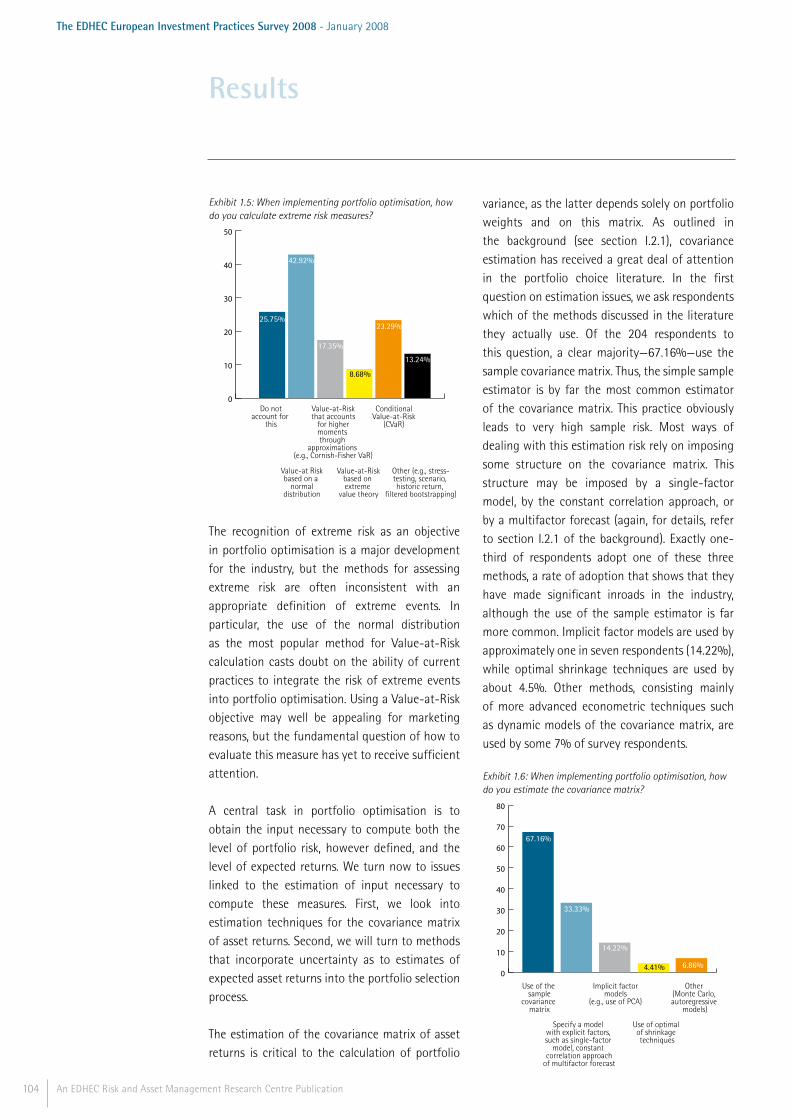

The results also show that, in addition to the traditional definition of risk as portfolio volatility, portfolio optimisation involves a variety of definitions of risk. In particular, extreme risk measures are now used by a majority of industry participants. However, it turns out that the most popular method used to calculate measures such as VaR or CVaR (chosen by more than 40% of those responding to our questionnaire) is to rely on the assumption of normal distribution, thus ignoring the fact that returns data are typically subject to non-trivial skewness and kurtosis. Only 17% make allowances for higher order moments through approximations such as that of Cornish-Fisher (1937), despite the ease of implementation of these approaches. Thus, more often than not, the so-called extreme risk measures are actually ill-defined.

Our survey also shows that advanced techniques of input estimation and optimisation are not widely used. In fact the predominant approach to covariance estimation remains to use the sample estimator (used by about two-thirds of respondents). This approach leads to maximum sample risk, which could be mitigated by

Executive Summary

13An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

techniques that impose some structure on the covariance matrix. Likewise, advances such as the Black-Littermann approach or portfolio resampling, advances that allow the integration of estimation risk, are used by only a minority of survey respondents (less than 20%). More ad hoc ways of avoiding estimation risk, such as imposing constraints on portfolio weights, are preferred.

Overall, although portfolio optimisation is at the heart of investment management, our survey makes it clear that only the most straightforward approaches are widely used and that more recent advances are largely ignored. On the other hand, the organisation of investment management has undergone profound change. The core-satellite approach is now emerging as the leading paradigm among European institutions.

Indices and BenchmarksThe second part of the survey raises a number of questions with respect to the use of indices and benchmarks. One of its aims is to determine the types of indices that are actually used and the criteria by which practitioners judge these indices. Since the indexing industry has seen numerous innovations in recent years, we also attempt to elucidate industry views of these innovations. Therefore, a large part of this topic deals with new indices, those for alternative asset classes as well as new forms of indexing that have recently been introduced in the equity arena.

Analysis of the responses makes it clear that traditional value-weighted indices maintain a very dominant position in spite of the substantial attention accorded new forms of indexing. On average, for example, more than three-quarters of assets under management are indexed to value-weighted indices. Characteristics-based and equal-weighted indices emerge as the most popular alternatives to value-weighted indices, though neither is used by much more than 20% of respondents. It should also be noted that respondents attribute relatively low importance

to the risk and return qualities of standard stock market indices, emphasising instead brand reputation and transparency. On the other hand, respondents are considerably more critical of the newly emerging hedge fund indices. Overall, these results highlight both the major role of indices in the industry and the willingness of respondents to accept indices on the strength of the history and reputation of the provider. With respect to the emergence of alternative indexing forms, it can be stated that there is no clear consensus as to which new form of indexing is preferred. In addition, from the responses we have obtained, we may wonder whether the growth of new forms of indices stems from the problems with value-weighting or simply from a search for return enhancement on the basis of the recent outperformance of these indices.

Asset-Liability ManagementAsset-liability management (ALM) is an investment process that explicitly takes into account the investor’s liability constraints and attempts to manage risk with respect to these constraints. In this section of the survey, we establish how widely the ALM approach is used and what particular techniques predominate.

Overall, the results indicate that ALM techniques are not as widely used in current practice as one might imagine. In particular, it is certainly rather surprising that, in their investment processes, nearly 40% of institutional investors fail to take into account shortfalls with respect to liabilities. Our results suggest that asset-based benchmarks such as the well-known stock market indices are of more concern in current practice than are liability-based benchmarks. It appears to us that more focus is needed on liability relative risk assessment and decision-making.

In addition, those who do consider ALM tend to use relatively straightforward approaches, such as cash-flow matching or LDI products based on immunisation techniques. Surplus optimisation

Executive Summary

14 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

techniques and non-linear risk profiling are used by only a small minority of respondents. Considering that these techniques correspond to well-known management principles in asset management (surplus optimisation corresponds to optimal diversification and non-linear risk profiling to dynamic risk management), this finding is surprising. Cash-flow matching and immunisation, on the other hand, can be seen as investments in the risk-free asset. Low expected returns, of course, are the downside. It is surprising to us that more advanced techniques of managing the risk/return trade-off are not more widely used, given that they are the core business tools of the profession. It should also be noted that this result stands in stark contrast to current practices in a pure asset management framework, in which the vast majority of respondents use some form of portfolio risk optimisation, as shown in the first section.

A further notable result is that measures of extreme risk are not widely used in an ALM context, while in pure asset management, most respondents do use such measures. In fact, only 25.57% of respondents do not account for extreme risk in the general question on portfolio optimisation. Finally, a noteworthy phenomenon is the extensive use of alternatives such as hedge funds and commodities to generate outperformance in the ALM framework.

Performance MeasurementWhile the above sections focus on constructing and implementing portfolios, an important final step—once the benchmark has been defined, the portfolio optimised, and risk controlled—is to assess the outcome of the investment process. This ex-post performance analysis is the topic of the final section of the survey.

It is striking that the performance measures currently used seem to centre on a limited number of standard indicators, such as the Sharpe ratio and the information ratio of a portfolio, used by 80% and 70% of respondents respectively.

Performance measures integrating the notion of downside risk are much less likely to be used. In addition, it turns out that downside risk measures are less widely used in performance measurement than they are in portfolio optimisation, a possibly surprising result, because in portfolio optimisation a single risk objective is often required, whereas in performance measurement, it may be useful to employ a wide range of measures. For this reason, there does not seem to be a good reason not to complement the standard Sharpe ratio with additional performance measures. Furthermore, the results show a frequent use of average returns in excess of the risk-free rate or of the average excess return with respect to a broad market index. In fact, these measures completely ignore the risk exposures of the portfolios under analysis.

Alpha analysis relies heavily on measuring absolute performance in a peer group. This is the predominant measure of alpha, used by nearly two-thirds of respondents, despite the fact that peer groups provide a very coarse adjustment for risk, leading to performance differences within the peer group that can be put down to investment style rather than to managerial skill. Style analysis, which allows precise adjustments with respect to style exposure, proves considerably less popular but is nonetheless used by a significant minority of slightly less than 40% of respondents. As it happens, the use of style analysis to construct a customised benchmark is the least popular choice among possible benchmarks. Only 40% of respondents construct customised benchmarks, while almost 50% choose specific (sector- or style-) indices, and almost 80% use broad market indices. From these results, it can be seen that popularity is inversely proportional to precision. In other words, the benchmarks that provide the crudest risk assessment are the most popular, while those that provide the most detailed risk assessment are the least popular. It should be noted as well that customised benchmarks allow more precise alpha measurement and that the process of customising a benchmark leads to a useful examination of the portfolio risk factors,

Executive Summary

15An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

an examination otherwise inexistent (when broad stock market indices are used) or undertaken in a much cruder fashion (when a single sector or style index is used).

Overall, industry practitioners rely largely on simple, well known performance measures to evaluate performance. However, reliance on these measures clearly comes at the cost of precise information on the risks and hence on precise performance measurement and attribution. If the industry wants to make sophisticated risk analysis an integral part not only of portfolio optimisation but also of portfolio evaluation, it will likely need to increase its awareness of modern performance measurement techniques.

Executive Summary

16 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

Background

17An EDHEC Risk and Asset Management Research Centre Publication

18 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

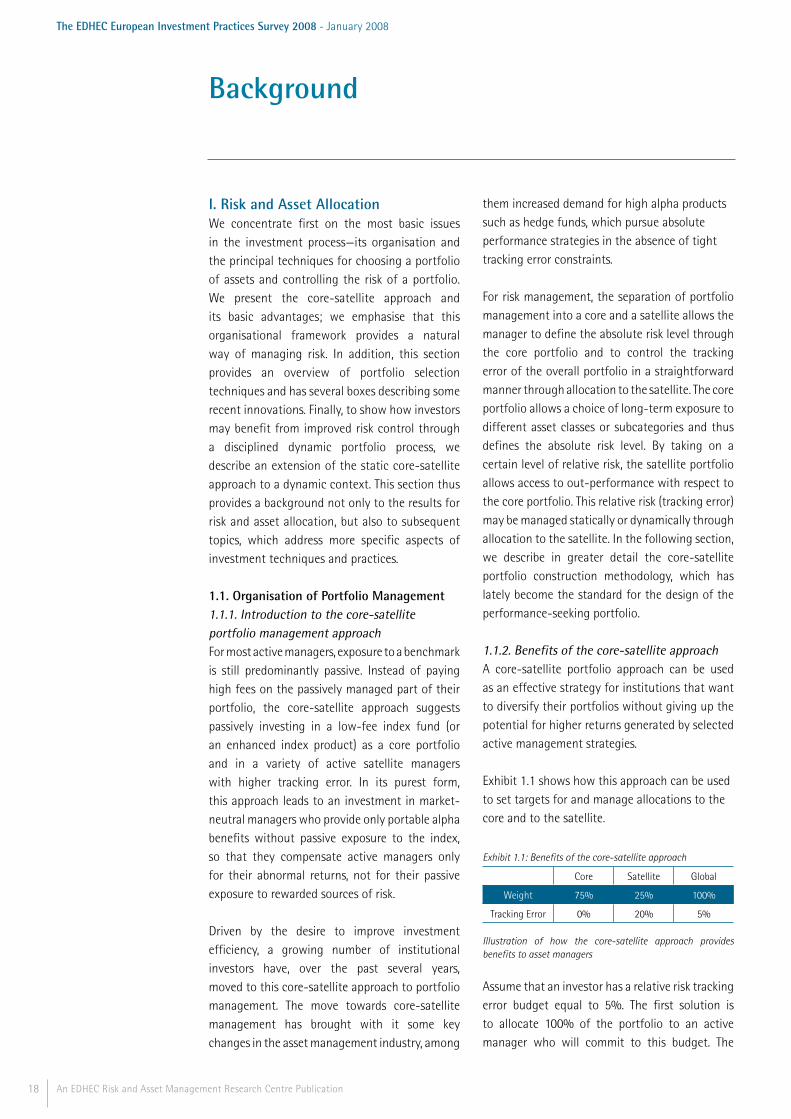

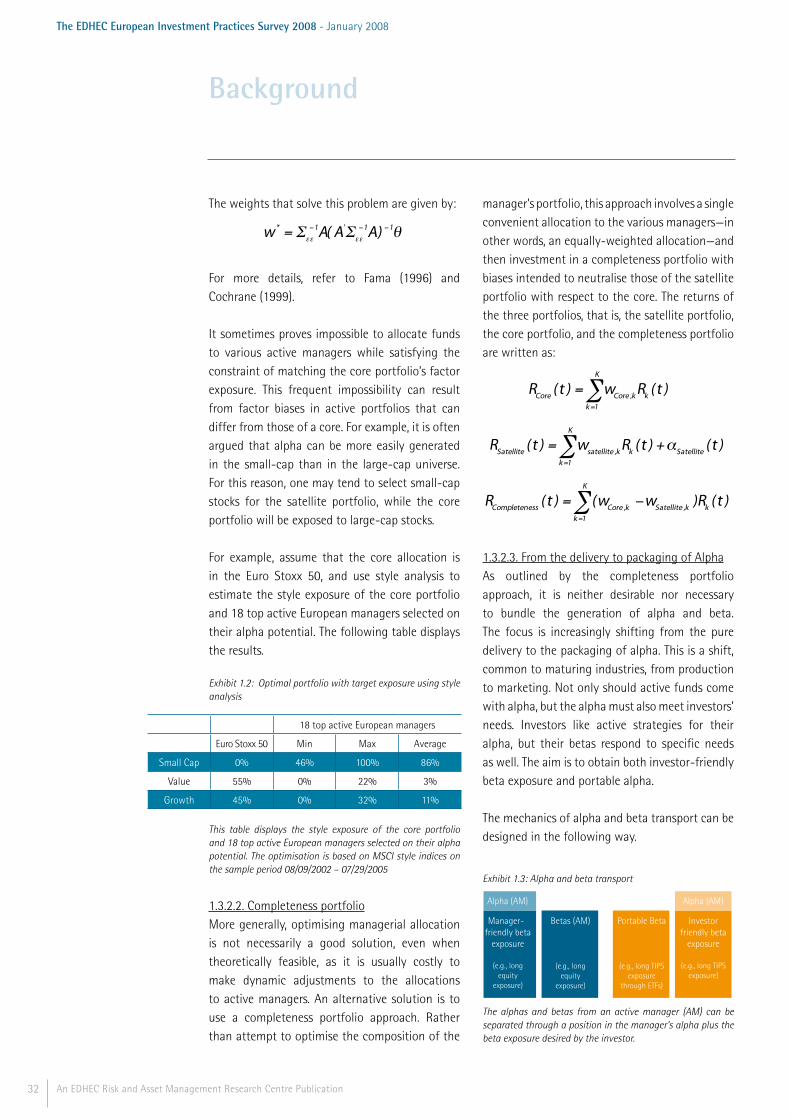

I. Risk and Asset AllocationWe concentrate first on the most basic issues in the investment process—its organisation and the principal techniques for choosing a portfolio of assets and controlling the risk of a portfolio. We present the core-satellite approach and its basic advantages; we emphasise that this organisational framework provides a natural way of managing risk. In addition, this section provides an overview of portfolio selection techniques and has several boxes describing some recent innovations. Finally, to show how investors may benefit from improved risk control through a disciplined dynamic portfolio process, we describe an extension of the static core-satellite approach to a dynamic context. This section thus provides a background not only to the results for risk and asset allocation, but also to subsequent topics, which address more specific aspects of investment techniques and practices.

1.1. Organisation of Portfolio Management 1.1.1. Introduction to the core-satellite portfolio management approachFor most active managers, exposure to a benchmark is still predominantly passive. Instead of paying high fees on the passively managed part of their portfolio, the core-satellite approach suggests passively investing in a low-fee index fund (or an enhanced index product) as a core portfolio and in a variety of active satellite managers with higher tracking error. In its purest form, this approach leads to an investment in market-neutral managers who provide only portable alpha benefits without passive exposure to the index, so that they compensate active managers only for their abnormal returns, not for their passive exposure to rewarded sources of risk.

Driven by the desire to improve investment efficiency, a growing number of institutional investors have, over the past several years, moved to this core-satellite approach to portfolio management. The move towards core-satellite management has brought with it some key changes in the asset management industry, among

them increased demand for high alpha products such as hedge funds, which pursue absolute performance strategies in the absence of tight tracking error constraints.

For risk management, the separation of portfolio management into a core and a satellite allows the manager to define the absolute risk level through the core portfolio and to control the tracking error of the overall portfolio in a straightforward manner through allocation to the satellite. The core portfolio allows a choice of long-term exposure to different asset classes or subcategories and thus defines the absolute risk level. By taking on a certain level of relative risk, the satellite portfolio allows access to out-performance with respect to the core portfolio. This relative risk (tracking error) may be managed statically or dynamically through allocation to the satellite. In the following section, we describe in greater detail the core-satellite portfolio construction methodology, which has lately become the standard for the design of the performance-seeking portfolio.

1.1.2. Benefits of the core-satellite approachA core-satellite portfolio approach can be used as an effective strategy for institutions that want to diversify their portfolios without giving up the potential for higher returns generated by selected active management strategies.

Exhibit 1.1 shows how this approach can be used to set targets for and manage allocations to the core and to the satellite.

Exhibit 1.1: Benefits of the core-satellite approach

Core Satellite Global

Weight 75% 25% 100%

Tracking Error 0% 20% 5%

Illustration of how the core-satellite approach provides benefits to asset managers

Assume that an investor has a relative risk tracking error budget equal to 5%. The first solution is to allocate 100% of the portfolio to an active manager who will commit to this budget. The

Background

19An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

second solution consists of allocating 75% of the portfolio to a purely passive product—an exchange traded fund (ETF), for example—or preferably to a strategy that is based on an efficient benchmark, and 25% of the portfolio to a 20% tracking error manager. This solution, consistent with a core-satellite approach to active asset management, offers two benefits.

First, allowing the active manager to deviate significantly from the benchmark leads to a better use of the manager’s skills. If the manager has reliable views on market trends and directions, a 5% tracking error constraint leaves him with too little room for active decisions consistent with these views. Beating the market is notoriously tough. Even harder is to beat it with one hand tied behind your back.

The second benefit is to allow a clear distinction between the value added by the design of the strategic asset allocation represented by the benchmark (core portfolio) and the out-performance generated by active portfolio management.

Indeed, the primary and arguably more important source of added-value is the optimal allocation decision that leads to the design of an efficient core portfolio (see below for state-of-the-art techniques involved in the design of core portfolios). This source of added-value should be rewarded, given that the design of the core portfolio can be a decision from the investor’s part (with the possible help of consultants) or a task delegated to the asset manager. The second source of added-value is the abnormal performance that is generated by active managers, which also deserves a separate reward. Similarly, the manager selection decision can be made by the investor (again with the possible help of consultants) or delegated to a multi-manager.

1.1.3. The arithmetic of core-satellite investingWe consider first a core-satellite approach with a single satellite. We show how to derive the

optimal proportion to invest in the satellite portfolio by setting the problem in a simple mean-variance analysis. We also demonstrate that, if the core portfolio perfectly replicates the benchmark, the information ratio of the overall portfolio is independent of the proportions of wealth in the core and the satellite and equal to the information ratio of the satellite portfolio.

We first consider a core-satellite approach with a single satellite portfolio. The mathematics are then straightforward. The overall portfolio corresponds to:

P = wS + 1-w( )C

where w is the fraction invested in the satellite (S), and 1-w is the fraction invested in the core (C). We now calculate the tracking error with respect to a benchmark B. We obtain:

P - B = wS + 1-w( )C - B = w S - B( ) + 1-w( ) C - B( )

If we now assume for the sake of simplicity that the core portfolio is perfectly replicating the benchmark, we get C=B, then we have:

P - B = w S - B( )As a result, we obtain:

TE P( ) = var P - B( ) = w var S - B( ) = wTE S( )

Consider the following example. We assume an investor has a target level of risk relative to a given benchmark, such as a 2.5% tracking error budget. Two options are possible. Either the investor hires one manager with a tracking error equal to 2.5% for the entire portfolio, or the investor forms a passive core portfolio and leaves 20% in an aggressively managed satellite with a

12.5% =

TE P( )w

=2.5%20%

tracking error.

The next step consists of deriving the optimal proportion w* to invest in either the satellite or the core portfolio. We solve the problem in the context of a simple mean-variance analysis.

Background

20 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

The optimisation program reads:

where IR(P) is the information ratio of the portfolio P with respect to the benchmark:

IR P( ) =

E(P - B)σ(P - B)

=E(P - B)TE P( )

(see, for, example Grinold and Kahn 2000).

When the core portfolio perfectly replicates the benchmark, the information ratio of the overall portfolio IR(P) is actually independent of the proportions of wealth invested in the core and the satellite and equal to the information ratio of the satellite portfolio IR(S) (as long as the proportion w is strictly positive). This can easily be seen from:

We may rewrite the optimisation program as:

U w( ) = IR ×w ×TE( S) - λw 2TE 2( S )

and the first-order condition reads:

∂U∂w

w*( ) = 0 ⇒w* =IR

2λTE S( ) For example, let us assume that the tracking error of the active fund is 5%, that the information ratio (IR) is 0.5, and that the coefficient of risk-aversion with respect to relative risk is λ = 0.2. Then, the optimal proportion invested in the active portfolio is:

w* =IR

2λTE S( )=

.52 × .2 ×5%

= 25%

The resulting tracking error is

TE P( ) = 25% ×5% =1.25%

Extending the analysis to the case of a satellite

S = wi Si

i =1

n

∑ invested in a number n of active

portfolio managers iS according to the proportions iw is straightforward. The excess return on the satellite portfolio is then:

S - B = wi Si - B( )

i =1

n

∑

and the tracking error of the satellite portfolio reads:

TE S( ) = wiwj σij

i , j =1

N

∑ - 2 wi σiB + σB2

i =1

N

∑⎛

⎝⎜⎞

⎠⎟

12

where ijσ is the covariance between portfolio managers iS and jS , and Bσ is the volatility of the benchmark.

It is then possible to find the optimal fraction invested in each active manager within the satellite portfolio so as to achieve the highest possible information ratio. Scherer (2002), among others, has shown that the optimal condition is that the ratio of return to risk contribution be the same for all managers:

wk αk

wk2σαk

2 + wkwj σkjj

∑⎛

⎝⎜⎞

⎠⎟

TE( S)

=wl αl

wl2σα l

2 + wlwj σkjj

∑⎛

⎝⎜⎞

⎠⎟

TE( S )

1.2. Diversification: Optimal Beta ManagementStrategic allocation is the first step in the investment management process. This step involves choosing from among the different asset classes or styles that, in accordance with the investor’s objectives, will make up the portfolio. Thus, strategic allocation defines the core. Strategic allocation may be done for the overall portfolio of assets or for a given asset class. In the latter case, the strategic allocation will determine the exposure to different subcategories (styles or sectors) of a given asset class (stocks, bonds, or alternative assets). It is also possible to

Background

U = E(P - B) - λσ 2(P - B) = IR P( ) ×TE P( ) - λTE 2 P( )

IR P( ) =

E(wS + 1-w( )C - B)σ(wS + 1-w( )C - B)

=wE( S - B)wTE S( )

= IR S( )

21An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

construct an optimal allocation for a given asset class directly from the individual assets. For each level of granularity (that is, the overall portfolio or the portion for a given asset class), it is necessary to define a core portfolio that willallow control and management of the strategic allocation. Today, asset allocation is playing a greater role in the investment management process. This interest in asset allocation can be explained by the results established by various empirical studies, which suggest that this step can contribute significantly to the result of the portfolio. Brinson, Hood, and Beebower (1986) and Brinson, Singer, and Beebower (1991) have shown, for example, that a considerable share (90%) of a portfolio’s performance can be attributed to the initial allocation decision.

Contrary to a common misperception, managing the core portfolio does not necessarily imply passive investment in a commercial index. It consists instead of using state-of-the-art asset allocation techniques to design an optimal benchmark based on investor preferences and constraints, liability constraints in particular.

Strategic allocation was formalised by the seminal work of Markowitz (1952), who was the first to quantify the link between the risk and return of a portfolio, and thereby introduced modern portfolio theory. Markowitz developed a theory of portfolio choice in an uncertain future based on a quantification of the difference between the risk of a portfolio’s assets taken individually and the global portfolio risk. His theory relates to maximising the utility of final wealth for a risk-averse investor, who measures risk through the variability of asset returns (volatility). Optimal portfolios, from a rational investor’s point of view, are defined as the portfolios with the lowest level of risk for a given return, or equally, as the portfolios with the highest return for a given level of risk. These portfolios are said to be efficient in the mean-variance sense.

Markowitz’s portfolio selection method therefore involves obtaining an optimal portfolio as a function of first order (expected return) and second order (variance and covariance) moment estimations of the returns of the asset classes under consideration. The quality of the estimation of these parameters is all the more decisive in that it has been shown that the portfolio optimisation program is characterised by very significant dependence on the initial conditions: minor discrepancies in the estimation of the parameters lead to very significant changes in the optimal allocation. This problem has been shown to be particularly acute in the case of errors in expected return estimation (Chopra and Ziemba 1993). As a result of the lack of robustness in Markowitz efficient frontier analysis, it has been suggested to focus on the only portfolio for which expected return estimates are not needed—the minimum variance portfolio. The key challenge then is to use a robust methodology for an enhanced estimation of the asset returns variance-covariance matrix, a problem that has been extensively studied in the literature. In the following section, we provide an overview of the main findings on how to mitigate the sample risk problem in the estimation of the second-order moments and co-moments of asset return distribution.

1.2.1. Enhanced estimates of covariance matricesSeveral solutions to the problem of asset return covariance matrix estimation have been suggested in the traditional investment literature. The most common estimator of return covariance matrix is the sample covariance matrix of historical returns.

S =

1T -1

Ht - H( ) Ht - H( ) '

t =1

T

∑

where T is the sample size, Ht is an Nx1 vector of returns in period t, N is the number of assets in the portfolio, and

H =

1T

Htt =1

T

∑

Background

22 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

is the average of these return vectors. We denote by Sij the (i,j) entry of S.

A problem with this estimator is typically that a covariance matrix may have too many parameters for the available data. If the number of assets in the portfolio is N, there are indeed N(N-1)/2 different covariance terms to be estimated. Because data are scarce, the problem is particularly acute in the context of alternative investment strategies, even when a limited set of funds or indices is considered; more often than not, after all, returns on alternative investments are available only infrequently.

One possible cure for the curse of dimensionality in covariance matrix estimation is to structure the covariance matrix in such a way as to reduce the number of parameters to be estimated. Of course, this cure invites two very important questions: how much structure should we impose? (the fewer the factors, the stronger the structure) and what factors should we use? There is a standard trade-off between model risk and estimation risk. The following options are available:

• Impose no structure. This choice involves low specification error and high sampling error, and leads to the use of the sample covariance matrix.1

• Impose some structure. This choice involves high specification error and low sampling error. Several models, including the single factor forecast (Sharpe 1963) and the multi-factor forecast (e.g., Chan, Karceski, and Lakonishok 1999), fall within this category. Another way to impose structure on the covariance matrix is to use the constant correlation model (Elton and Gruber 1973). This model can also be thought of as a James-Stein estimator that shrinks each pairwise correlation to the global mean correlation.

• Impose optimal structure. This choice involves medium specification error and medium sampling error. The optimal trade-off between specification

error and sampling error leads to optimal shrinkage towards the grand mean (Jorion 1985, 1986), to optimal shrinkage towards the single-factor model (Ledoit 1999), or to the introduction of portfolio constraints (Jagannathan and Ma 2003).

Another alternative is to consider an implicit factor model in an attempt to mitigate model risk and impose endogenous structure. The advantage of this alternative is that it involves low specification error (because of its “let the data talk” approach) and low sampling error (because some structure is imposed). Implicit multi-factor forecasts of asset return covariance matrix can be further improved by noise-dressing techniques and optimal selection of the relevant number of factors (see below). More specifically, we use principal component analysis (PCA) to extract a set of implicit factors. The PCA of a time-series involves studying the correlation matrix of successive shocks. Its purpose is to explain the behaviour of observed variables using a smaller set of unobserved implied variables. Since principal components are chosen solely for their ability to explain risk; a given number of implicit factors always captures a larger part of asset return variance-covariance than does the same number of explicit factors. One drawback is that implicit factors do not have a direct economic interpretation (except for the first factor, which is typically highly correlated with the market index). Principal component analysis has been used in the empirical asset pricing literature (Litterman and Scheinkman 1991, Connor and Korajczyk 1993, or Fedrigo, Marsh, and Pfleiderer 1996, among many others). From a mathematical standpoint, PCA involves transforming a set of N correlated variables into a set of orthogonal variables, or implicit factors, which reproduces the original information present in the correlation structure. Each implicit factor is defined as a linear combination of original variables. Define H as the following matrix:

Background

1 - One possible generalisation/improvement to this sample covariance matrix estimation is to assign declining weights to observations as they go further back in time (Litterman and Winkelmann 1998).

23An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

H = hit( )1≤t ≤T

1≤i ≤N

We have N variables hi , i=1,...,N, i.e., returns for N different assets, and T observations of these variables.2 PCA enables us to decompose htk as follows:3

htk = λi

i =1

N

∑ UikVti : = siki =1

N

∑ Vti

where U is the matrix of the N eigenvectors of H’HV is the matrix of the N eigenvectors of HH’

Note that these N eigenvectors are orthonormal. λi is the eigenvalue (ordered by degree of magnitude) corresponding to the eigenvector Ui. Note that the N factors Vi are a set of orthogonal variables. The main challenge is to describe each variable as a linear function of a reduced number of factors. To that end, one needs to select a number of factors K such that the first K factors capture a large fraction of asset return variance, while the remainder can be regarded as statistical noise:

htk = λi

i =1

K

∑ UikVti + εtk : = siki =1

K

∑ Vti + εtk

where some structure is imposed by assuming that the residuals εtk are uncorrelated. The percentage of variance explained by the first K factors is given by:

λii =1

K

∑

λii =1

N

∑

A sophisticated test by Connor and Korajczyk (1993) finds between 4 and 7 factors for the NYSE and AMEX over the period from 1967 to 1991, which is roughly consistent with the findings of Roll and Ross (1980). Ledoit (1999) uses a 5-factor model. We can select the relevant number of factors by applying some explicit results from the theory of random matrices (Marchenko and Pastur

1967).4 The idea is to compare the properties of an empirical covariance matrix (or, likewise, of a correlation matrix, since asset returns have been normalised to have zero mean and unit variance) to a null hypothesis purely random matrix such as one could obtain from a finite time-series of strictly independent assets. It has been shown (see Johnstone 2001 and Laloux et al. 1999 for an application to finance) that the asymptotic density of eigenvalues λ of the correlation matrix of strictly independent assets reads:

f λ( ) =T

2πN

λ - λmax( ) λ - λmin( )λ

λmax =1+NT

+ 2NT

λmin =1+NT

- 2NT

Theoretically speaking, this result can be exploited to provide formal testing of the assumption that a given factor represents information and not noise. However, the result is an asymptotic result that cannot be taken at face value for a finite sample size. One of the most important features here is that the lower bound of the spectrum λmin is strictly positive (except for T=N), and therefore, there are no eigenvalues between 0 and λmin. We use a conservative interpretation of this result to design a systematic decision rule and decide to regard as statistical noise all factors associated with an eigenvalue lower than λmax. In other words, we take K such that λK > λmax and λK+1 < λmax, where λ1 is the greatest eigenvalue.5

A problem of a different nature comes from the non-stationarity of the data. Numerous empirical studies have pointed out, for example, that the volatilities of asset classes are not constant over time and that an optimisation where the risk parameters are set equal to their past values would not, as a result of their non-stability, be very robust. The dynamic character of the parameters

Background

2 - The asset returns have first been normalised to have zero mean and unit variance.3 - For an explanation of this decomposition in a financial context, see Barber and Copper (1996).4 - Another decision rule would be: keep enough factors to explain x% of the covaria-tion in the portfolio.5 - If no factor is such that the associated eigenvalue is grea-ter than λmax, we take K=1, i.e., we retain the first component as the only factor.

24 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

renders the task of estimation more arduous, a challenge that can be addressed by the use of suitably designed statistical models such as Garch models. Good modelling brings robustness back to portfolio optimisation over a long period by relying on the stability of the models that define the variation in the risk parameters (variance-covariance) and no longer on the stability of the risk parameters themselves.

While it appears that there are a large number of techniques that can be used to allow better estimation of the variance-covariance matrix of asset returns, a major challenge remains: that of estimating the mean returns. It is for this reason that it has been suggested to focus on minimum risk portfolios whose derivation does not depend on any estimate of expected returns.6

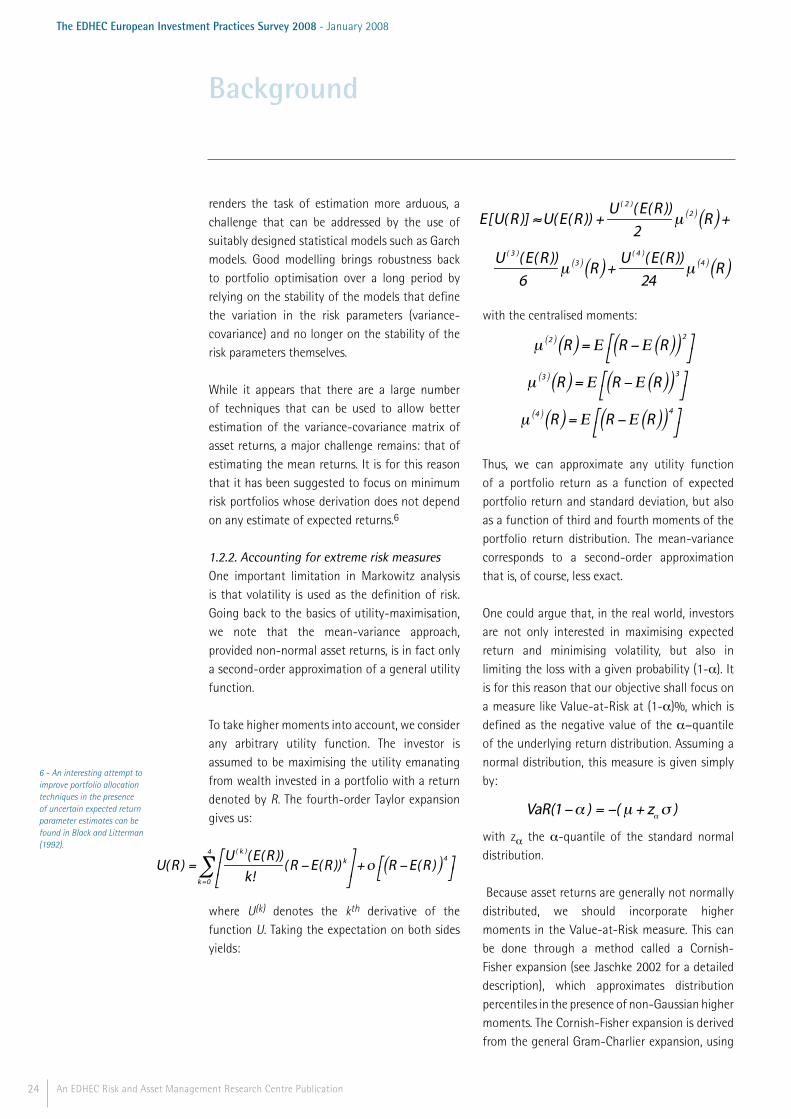

1.2.2. Accounting for extreme risk measuresOne important limitation in Markowitz analysis is that volatility is used as the definition of risk. Going back to the basics of utility-maximisation, we note that the mean-variance approach, provided non-normal asset returns, is in fact only a second-order approximation of a general utility function.

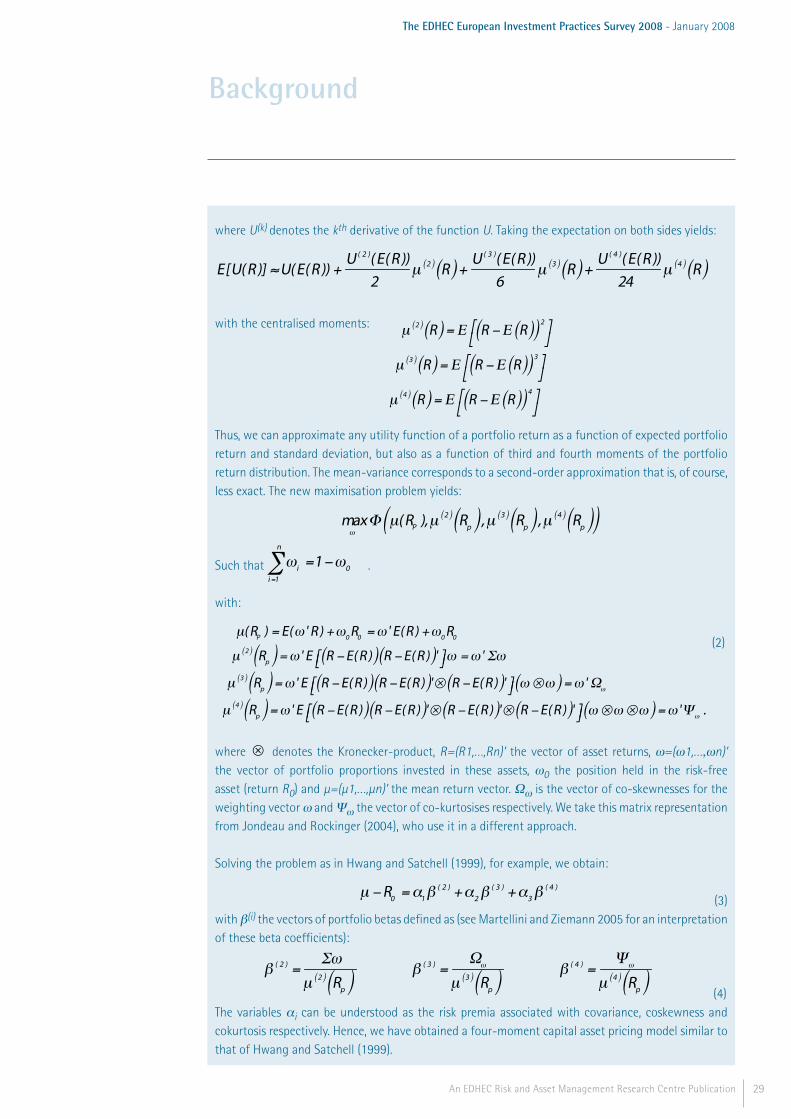

To take higher moments into account, we consider any arbitrary utility function. The investor is assumed to be maximising the utility emanating from wealth invested in a portfolio with a return denoted by R. The fourth-order Taylor expansion gives us:

where U(k) denotes the kth derivative of the function U. Taking the expectation on both sides yields:

with the centralised moments:

μ 2( ) R( ) = Ε R - Ε R( )( ) 2⎡⎣

⎤⎦

μ 3( ) R( ) = Ε R - Ε R( )( ) 3⎡⎣

⎤⎦

μ 4( ) R( ) = Ε R - Ε R( )( ) 4⎡⎣

⎤⎦

Thus, we can approximate any utility function of a portfolio return as a function of expected portfolio return and standard deviation, but also as a function of third and fourth moments of the portfolio return distribution. The mean-variance corresponds to a second-order approximation that is, of course, less exact.

One could argue that, in the real world, investors are not only interested in maximising expected return and minimising volatility, but also in limiting the loss with a given probability (1-α). It is for this reason that our objective shall focus on a measure like Value-at-Risk at (1-α)%, which is defined as the negative value of the α-quantile of the underlying return distribution. Assuming a normal distribution, this measure is given simply by:

VaR(1-α ) = -( μ + zα σ )

with zα the α-quantile of the standard normal distribution.

Because asset returns are generally not normally distributed, we should incorporate higher moments in the Value-at-Risk measure. This can be done through a method called a Cornish-Fisher expansion (see Jaschke 2002 for a detailed description), which approximates distribution percentiles in the presence of non-Gaussian higher moments. The Cornish-Fisher expansion is derived from the general Gram-Charlier expansion, using

Background

6 - An interesting attempt to improve portfolio allocation techniques in the presence of uncertain expected return parameter estimates can be found in Black and Litterman (1992).

U( R) =

U ( k )( E( R))k!

( R - E( R)) k⎡

⎣⎢

⎤

⎦⎥

k =0

4

∑ + ο R - E( R)( ) 4⎡⎣

⎤⎦

E[U( R)] ≈U( E( R)) +

U ( 2 )( E( R))2

μ 2( ) R( ) +U ( 3 )( E( R))

6μ 3( ) R( ) +

U ( 4 )( E( R))24

μ 4( ) R( )

E[U( R)] ≈U( E( R)) +

U ( 2 )( E( R))2

μ 2( ) R( ) +U ( 3 )( E( R))

6μ 3( ) R( ) +

U ( 4 )( E( R))24

μ 4( ) R( )

25An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

the standard normal distribution as the reference function. For a four-moment approximation of α-percentiles the following formula is given:

where S denotes the sample skewness, K the sample’s excess kurtosis and αz the α -percentile of the standard normal distribution. αz~ denotes the modified α -percentile. This approximation is built on the hypothesis that the underlying distribution is close to a normal distribution. We obtain the modified Value-at-Risk measure with confidence (1-α ):

VaRmod(1-α ) = - (μ + αz~ σ)

where σ denotes estimated values for the standard deviation and μ the mean.

Another relevant measure of extreme risk is the Conditional Value-at-Risk (CVaR), defined as the expected loss beyond the VaR, which focuses on the left tail of the returns distribution beyond a threshold, as opposed to a mere certain quantile as VaR does. Interestingly, CVaR would also be a preferred risk objective from an optimisation perspective. VaR is difficult to optimise when it is calculated over scenarios because it leads to non-convex optimisation problems; there are multiple extrema and the local optimisation algorithms are unsuccessful, whereas the global algorithms are inefficient. On the other hand, CVaR can be optimised through stochastic linear programs (Rockafellar and Uryasev 2000).7

In addition, VaR can in fact be used as a portfolio risk management tool. To achieve this objective, it must be possible to define the composition of a portfolio’s VaR and to analyse the impact of a new transaction on the total VaR of the portfolio. This is the objective of incremental VaR calculations. The goal of the incremental VaR is precisely to define the contribution of each asset to the total VaR of the portfolio. The total VaR of the portfolio is not equal to the sum of the VaRs of the assets that make up the portfolio, because there are correlations between the assets. The incremental VaR, for its part, is defined in such a way that the sum of the incremental VaRs is equal to the total VaR of the portfolio. It is obtained from the delta VaR, which is the vector of the VaR’s sensitivity to each asset. It is made up of partial derivatives of the portfolio’s VaR with respect to each asset. The incremental VaR of asset i is then calculated by multiplying the ith component of the portfolio's VaR delta by the quantity of asset i held. If we denote the proportion of asset i held in the portfolio as ix , the incremental VaR for asset i in portfolio P, denoted by )(PIVaR i , is given by:

IVaRi (P ) = xi

∂VaR(P )∂xi

If the incremental VaR of an asset is positive, it contributes to an increase in the total VaR of the portfolio. On the other hand, if the incremental VaR of the asset is negative, introducing it into the portfolio will decrease the total VaR.

Background

7 - At first, CVaR calculation seems to be complex, since it depends on the VaR itself, but little optimisation tricks can make it possible to calculate CVaR in an optimisation problem without having to know the VaR value. And, interestingly, optimisation of CVaR will help calculate VaR for that same level, as further explained in Rockafellar and Uryasev (2000).

%zα = zα +

16

( zα

2 -1)S +1

24( zα

3 - 3zα )K -1

36( 2zα

3 -5zα )S 2αz~

Improving Estimation of Higher Order Moments and Co-moments

It is clear that extending the risk space from one dimension (volatility) to three dimensions (volatility, 3rd and 4th central moments) increases exponentially the number of parameters to estimate. This ex-tension calls for robust estimation techniques such as structural estimators described in section 1.2.2 for the case of the variance-covariance matrix. As Martellini and Ziemann (2007) have shown, the constant correlation approach as well as the single factor approach may be extended to the context of higher order moments.

26 An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

Indeed, the single factor model is characterised by the projection of single asset returns (R) on the returns of a broad market index (F):

Rt = c + βFt + εt

On the assumption of uncorrelated residuals the covariance matrix may then be decomposed as:

Σ̂ = ββ' Var( F ) +Ψ̂

where Ψ̂ is supposed to be a diagonal matrix containing the estimated idiosyncratic variances. Consistent with the projection idea, suitable matrix manipulation techniques can be used to extend the model to the context of higher order co-moments. As demonstrated in Martellini and Ziemann (2007), the higher order co-moments of the portfolio can be written as:

μ 2( ) = ω ' M2ω

μ 3( ) = ω ' M3 ( ω ⊗ ω )

μ 4( ) = ω ' M4 ( ω ⊗ ω ⊗ ω )

with

As a result, the authors derive the single factor estimates of the corresponding higher order co-mo-ments as:

μ̂ 2( ) = ( ββ ') μ̂0

2( ) +Ψ̂

μ̂ 3( ) = ( ββ ' ⊗ β ') μ̂0

3( ) + Φ̂

μ̂ 4( ) = ( ββ ' ⊗ β ' ⊗ β ') μ̂0

4( ) + Υ̂

where ( )k

0μ̂ denotes the k-th central moment of the market index returns. The elements in Φ̂ and Υ̂ are obtained in accordance with the assumption of independent regression residuals.

As far as the constant correlation approach is concerned, the Cauchy-Schwartz inequality is used to define higher order correlation constants that are consistent with the Pearson correlation coefficient on the second order level. We recall this fundamental inequality:

E( XY )[ ] 2≤ E( X )E(Y )

If we let X and Y be centralised returns of some assets, this relation implies that the Pearson correla-tion coefficient (r) is bounded by 1:

r 2 =

E( XY )[ ] 2

E( X )E(Y )≤1

Accordingly, we can suitably define X and Y (excess, squared excess, and cubic excess returns of assets) so as to model all possible combinations of higher order co-moments and the corresponding higher order correlation coefficients. As a result, consistent with the formulas obtained in the case of the covariance matrix, higher order co-moments—that is, all elements in M2, M3, and M4—may be com-puted merely based on seven correlation coefficients and centralised univariate moments of the asset returns (Martellini and Ziemann 2007).

Background

M2 = Ε R - Ε R( )( ) R - Ε R( )( )'⎡⎣ ⎤⎦

M3 = Ε R - Ε R( )( ) R - Ε R( )( )' ⊗ R - Ε R( )( )'⎡⎣ ⎤⎦

M4 = Ε R - Ε R( )( ) R - Ε R( )( )' ⊗ R - Ε R( )( )' ⊗ R - Ε R( )( )'⎡⎣ ⎤⎦

27An EDHEC Risk and Asset Management Research Centre Publication

The EDHEC European Investment Practices Survey 2008 - January 2008

Both models considerably reduce the number of unknown parameters. Applying the sample estimators to calibrate a four-moment asset allocation model for portfolios containing 25 assets, for instance, re-quires 80 years of monthly data to ensure that the number of unknown parameters (23,725) does not exceed the number of observations. On the contrary, to fully establish estimates for the second, third, and fourth co-moment matrices (in M2, M3, and M4) for the same portfolio of 25 assets, the constant correlation and the single factor based estimations require only 103 and 107 parameters respectively. This leads to statistically well defined systems.

As shown in Martellini and Ziemann (2007), the gains due to the reduction of estimation risk over-come the losses due to specification error implied by the model restrictions and lead to statistically significant gains in out-of-sample utilities. Moreover, empirical evidence suggests that structural es-timators enhance the stability of portfolios as measured by the turnover rate in a rolling window portfolio construction framework. Consequently, the proposed structural estimators allow investors to take higher order moments into account without excessively increasing the number of parameters to estimate.

Background

8 - More generally, this reverse-engineering mechanism can be applied to infer the expected return estimate that can support any given asset allocation, and not necessarily an asset allocation corresponding to market cap weightings. 9 - Note that λ is the market risk aversion coefficient.

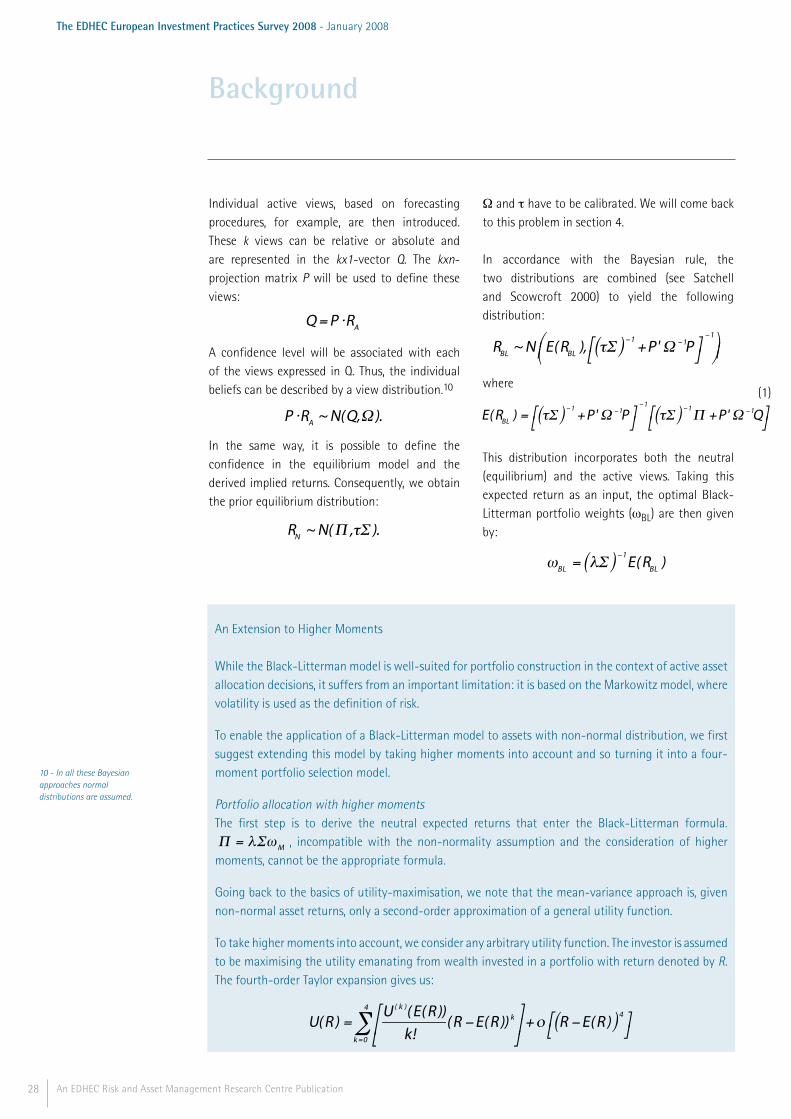

1.2.3. Enhanced estimates of expected returnsTo obtain expected returns as an input to portfolio optimisation, it is often useful to employ a beta pricing model. These models postulate a (usually linear) relation between the expected returns on an asset and the asset’s exposure to a number of risk premia. They may be used to create views on expected returns, given a prediction of risk premia and of risk factor exposures. In this section, we present a formal model that integrates views on expected returns into an asset allocation process. We provide a review of the Black-Litterman model. An extension to a setup where higher moments of return distribution are taken into account is pro-vided in an insert.

Since the seminal work of Markowitz (1952) there has been a strong consensus in portfolio manage-ment on the trade-off between expected return and risk. In the Markowitz world, risk is represen-ted by standard deviation. Given the investor's specific risk aversion, optimal portfolios and the so-called efficient frontier can be derived. Using this mean-variance approach, Sharpe (1964) and Lintner (1965) design an equilibrium model, the capital asset pricing model (CAPM), whose aim is to describe asset returns. Assuming homogenous beliefs, every investor holds the market portfolio derived from this equilibrium model.