Page 1

Asia Pacific Journal of Accounting and Finance

Volume 3 (1), December 2014

THE EFFECT OF BOARD DIVERSITY ON THE EXTENT OF

INTELLECTUAL CAPITAL DISCLOSURE (EMPIRICAL STUDY IN

INDONESIAN STOCKS EXCHANGE)

Ni Ketut Rasmini, Made Gede Wirakusuma, Ni Wayan Yuniasih*

Universitas Udayana

Denpasar

Email: [email protected]

Abstract

Board structure as one of corporate governance mechanism has two primary roles, which are

service or advisory role and control role. One of the main issues associated with board

structure and board role is board diversity. Board diversity is divided into demographic

diversity and cognitive diversity. This research examined the effect of board diversity on the

disclosure of intellectual capital.

Samples in this research were financial companies listed on the Indonesia Stock Exchange

during the period 2004-2009. The sample obtained by purposive sampling, and 33 companies

fit with the sample criteria. The hypothesis tested by using multiple regression analysis. The

result of hypothesis testing shows that gender diversity and diversity of nationality influence

the intellectual capital disclosure. The result also shows that variation of formal education

background (education diversity) and proportion of outside director (board‟s independence)

has no effect on intellectual capital disclosure. Firm size as a control variable is also has

positive effect on intellectual capital disclosure.

Keywords: diversity, directors, board of directors, intellectual capital disclosure.

Page 2

46 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

1. INTRODUCTION

The falls of some of the world‟s great companies, like Enron and WorldCom in the

United States, have raised questions on the practices of good corporate governance.

Transparency of information disclosed in the mandatory disclosure does not adequately

describe the condition of the company as a whole. Therefore, the company made a voluntary

disclosure to the market and the one of information included in the voluntary disclosure is

intellectual capital. Intellectual capital is a topic that in recent years began to frequently

discuss. In Indonesia, the phenomenon of intellectual capital (IC) began to flourish,

especially after the emergence of standards on intangible assets. According to SFAS 19,

intangible assets are non-monetary assets that can be identified and has no physical form and

held for use in the produce or deliver goods or services, leased to others, or for administrative

purposes (IAI 2007). Precise measurement and disclosure of the IC companies cannot set

despite some recognition of the benefits of IC in promoting the value and competitive

advantage.

The shape and the extension of disclosure are largely determined by corporate

governance. One mechanism of corporate governance is the structure or composition of the

board of directors and directors as an organ of a company that guarantees the application of

the principles of corporate governance and enhances the protection of creditors (Surya and

Yustiavandana 2006: 131). Board structure of an Indonesia‟s company is adopting a two tier,

which is consists of directors as managers and board of directors as a party to supervise

(Ward, 2008).

Based on resource dependency theory (Pfeffer and Salancik 1978), there are two

views that explain the role of the board of directors and directors in the company. The first

view is called with the relationship environmental perspective (environmental linkage

perspective). This perspective explains that the board of directors and directors are part of the

company and its environment, and they will provide information and resources for the

company to protect it from environmental uncertainty. Based on this view, individual

members of the board of directors and directors with backgrounds that vary will provide an

important resource for the company (Siciliano 1996). This view is related to the role or

functions of the board of directors and directors as an advisor or information provider

(advisory/service role) to the management of the company. The second view explains that the

board of directors and directors are also performing a function of the internal control (control

role), and through the efforts of the administration can affect the efficiency of the company.

The existence of the board of directors and directors is seen as the internal mechanisms that

control the selfish actions (self-serving behavior) so that management can maximize

shareholder value.

The one of important issues that related to its structure and functions of board is the

diversity of the board and directors. Diversity of the board and directors describe the

distribution of differences between members of the board relating to the characteristics of the

differences in attitudes and opinions (Ararat et al. 2010). Van der Walt and Ingley (2003) in

Luckerath-Rovers (2010) defines diversity in the context of corporate governance as the

composition of the board of directors and directors and the combination of qualities,

characteristics, and different skills of individual members of the council in relation to

Page 3

Rasmini, Wirakusuma, Yuniasih, The Effect of Board Diversity on The Extent of….. 47

decision-making and other processes in the company's board. According to Milliken and

Martin (1996) diversity of the board of directors and directors differentiated between

demographic diversity (observable) such as: gender, age, race, and nationality, as well as

cognitive diversity (not observable) such as: expertise (skills) and experience.

Carter et al. (2002) states that an important issue in corporate governance will be

faced by managers, directors, and shareholders in modern enterprise is the presence of the

gender composition, race, and culture of the board of directors and directors. The selection

board should consider the diversity of gender, race, age, and nationality as recommended by

the National Association of Corporate Directors Blue Ribbon Commission. The issue of

diversity of the board of directors and corporate codes of conduct are also considered when

assessing the effectiveness of corporate decision-making. Both are seen as indicators of

independence and accountability of decision making (Maier 2005).

Williams and O'Reilly (1998) mentioned that the higher of diversity on the board of

directors and directors, the higher variability of cognitive style, thereby further enriching the

knowledge, wisdom, ideas and approaches available to the company's board, and will

ultimately improve the quality of decision making. The greater diversity in board members

and directors will provide opinions and alternative problem solving is increasingly diverse,

because of the heterogeneous perspectives of individual board members. In addition, the

diversity of the board and directors also provide unique characteristics for companies that can

create additional value for shareholders and enhance corporate value (Carter et al. 2007).

Luckerath-Rovers (2010) explain two reasons why the composition of the board

directors and directors relating to the diversity of board members could affect the value of the

company. The first reason is because the boards and directors have the most influence in the

company's strategic decision-making. The second reason is that the board and directors also

have a role as a supervisor (supervisory role), which represents the interests of shareholders,

must respond appropriately challenge or the possibility of takeover, and monitor the

company's total value.

Diversity of the board of directors and directors in this study were measured using

criteria related to the demographic characteristics of gender, and nationality, as well as

criteria related to the cognitive characteristics in the form of formal education background

and proportion of independent board of directors.

Studies linking diversity to the board of directors and directors of the company IC

disclosure is need to be done, especially in Indonesia. Research on IC disclosure in Indonesia

is very interesting for several reasons. First, a global survey conducted by Taylor and

Associates in 1998 in Williams (2001) were the issues of disclosure of intellectual capital is

one of ten kinds of user information needs. Companies should respond to these needs by

making the disclosure of IC. IC to the present disclosure is voluntary so not all companies

make disclosures to the same extent. Second, the number of mandatory disclosure as required

by the accounting profession is only related to physical capital. In addition, this study wanted

to examine the influence of human characteristics that run in the area of corporate governance

mechanisms of IC disclosure.

Based on the description of research background, the formulation of the problem in

this study is whether the presence of women in the board of directors and directors, the

presence of the board and directors with foreign nationality, variation of formal education

Page 4

48 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

background of board and directors, and the proportion of independent board of directors

broad effect on IC disclosure of financial sector companies that were listed on the Indonesia

Stock Exchange during 2004-2009 period?

.

2. LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

Agency theory can be used to explain the relationship of corporate governance and

disclosure. According to agency theory, conflicts arise due to the asymmetry of information.

The existence of good governance is expected to reduce conflict by reducing information

asymmetry. One way to reduce information asymmetry is performing a more extensive

disclosure. To date, mostly of the IC disclosure is voluntary because the only physical capital

that has been set up by the accounting profession. If the company does not disclose

information about intangible assets, there will be present some negative consequences. For

example, stock price volatility occurs because investors have less information about the

company's intangible asset so that decisions made are not accurate. Based on a global survey

conducted Taylor and Associates in 1998 in Williams (2001) were the issues of disclosure of

intellectual capital is one of ten kinds of user information needs.

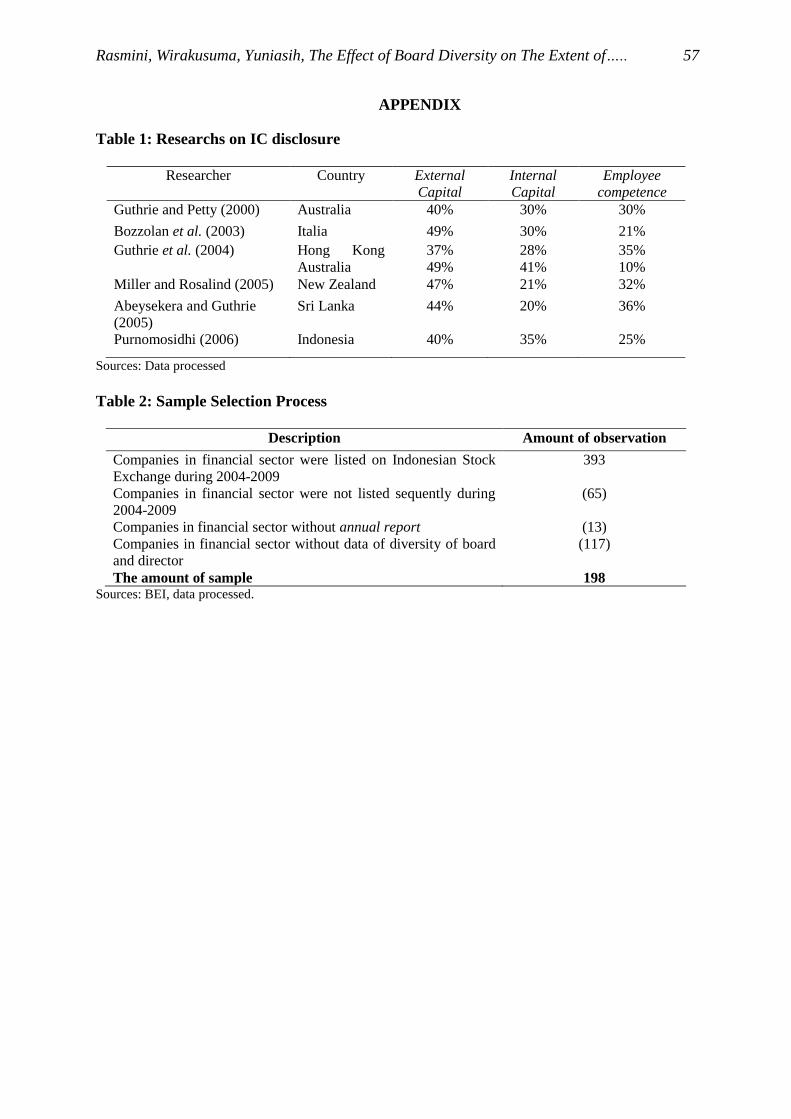

Research on intellectual capital disclosure practices have been conducted in various

countries. The results of research may be presented in Table 1 (see Appendix).

The composition and pattern of expression must not be separated from the

characteristics of decision makers. This study will investigate the influence of diversity of

board on IC disclosure by looking at the characteristics of board members. The presence of

women in structure of the board and directors of the company is one measure of diversity of

the board. The presence of women in the structure indicates that the company provide equal

opportunity for everyone (no discrimination), and it has a broad understanding of enterprise

and consumer markets, which in turn will increase reputation (legitimacy) and the value of

the company (Brammer et al. 2007 in Luckerath-Rovers 2010). Robbins and Judge (2008:

206) suggest that women generally have more detailed thoughts related to the analysis of

decision-making. They tend to analyze the issues before making a decision and the decision

process that has been made, resulting in a consideration of problems and alternative solutions

more closely. Williams (2000) and Swartz and Firer (2005) found the presence of women in

the board has a positive effect on IC performance. Carter (2003) and Siciliano (1996) found

that gender diversity has a positive effect on firm performance. A good performance will lead

the company to conduct a more extensive disclosure. Nalikka (2009) found that gender

diversity has a positive effect on voluntary disclosure. Therefore the hypothesis (H1) is

diversity of gender effect on broad of IC disclosure.

The existence of board and directors with foreign nationality is also a measure of

diversity of board that is often used in research. Oxelheim and Randoy (2001), Carter et al.

(2002, 2007), Marimuthu (2008), Ararat et al. (2010) found a positive effect of the presence

of foreign or ethnic minorities in the board to the company value. Their presence brings

valued opinions, perspectives, languages, beliefs, family background and diverse professional

experience, so enriching the knowledge of business and complex problem-solving

alternatives. In addition, the presence of foreign board members were able to convince

foreign investors that the company is professionally managed (Randoy et al. 2006). Oxelheim

Page 5

Rasmini, Wirakusuma, Yuniasih, The Effect of Board Diversity on The Extent of….. 49

and Randoy (2001) suggested that the presence of the directors and directors with foreign

nationality shows that the company has made the process of globalization and information

exchange in the network internationally. Williams (2000) and Swartz and Firer (2005) found

ethnic diversity within the board has a positive effect on IC performance. The excellent

performance of the company made the disclosure is likely to provoke a wider audience. The

presence of foreign directors on the board also may trigger the disclosure of information in

the hope of the company's credibility will increase. Therefore, the hypothesis (H2) is the

presences of foreign directors have a positive effect on the area of IC disclosure.

Formal education backgrounds of board of directors and directors is reflect of

cognitive characteristics that may affect the ability of the board in making business decisions

and manage the business (Kusumastuti et al. 2006). Siciliano (1996) found that diversity of

educational backgrounds associated with the background of the work the company's board of

directors has a positive effect on organizational performance, especially on social

performance. Instead, Goodstein et al. (1994) found a negative effect of formal education

background diversity on the ability of the board of directors of the company to make changes

to corporate strategy. Wallace and Cooke (1990) found that the directors who have a

background in accounting and business education may make a broader level of disclosure to

enhance the corporate image and credibility of management. Accordingly, hypothesis (H3) is

the education background of the board has a positive effect on the area of IC disclosure.

Diversity of board can also be measured from the level of independence of board

members. Composition of the board of independent directors with a strong enough will have

managerial oversight of behavior that is more stringent to protect the interests of shareholders

(Fama, 1980) and to increase shareholder value (Kusumastuti et al. 2006). Fama and Jensen

(1983) suggest that corporate boards dominated by outside corporate governance would result

in a stronger company because they are more independent oversight of management

behavior. Brickley and James (1987) in Agrawal and Knoeber (2000) stated that in addition

to a role in surveillance activities, the presence of outside directors will help to develop

management skills and business strategy with technology and market knowledge possessed

by them. One form of protection that can be done independent board is to do a more

extensive disclosure. Cerbioni and Parbonetti (2007) found that the proportion of independent

board has a positive effect on the disclosure of IC. Cheng and Courteney's (2006) using the

104 companies in Singapore found that the proportion of independent commissioner has a

positive effect on voluntary disclosure. Li et al. (2007) found that board composition has no

effect on IC disclosure. Different results found by Haniffa and Cooke (2000), namely the

existence of non-executive commissioner broad negative effect on voluntary disclosure. The

Hypothesis (H4) is the proportion of independent board of directors influence the broad of IC

disclosure.

3. RESEARCH METHOD

The object of research that used in this study was financial sector companies listed on

the Indonesia Stock Exchange during the years 2004-2009. The financial sector consists of

companies of banking, insurance, securities companies, financial institutions, and others. The

banking sector was chosen because; according to Firer and Williams (2003) the banking

Page 6

50 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

industry is one of the most intensive sectors of intellectual capital. In addition, from an

intellectual aspect, the overall banking sector employees in more homogeneous compared to

other economic sectors (Kubo and Saka 2002 as quoted by Ulum et al. 2008). Bank and

insurance can be categorized as an industry based on the intellect to innovate in products and

services, as well as the knowledge and flexibility is a critical aspect that determines the

success of the business (Sianipar 2009).

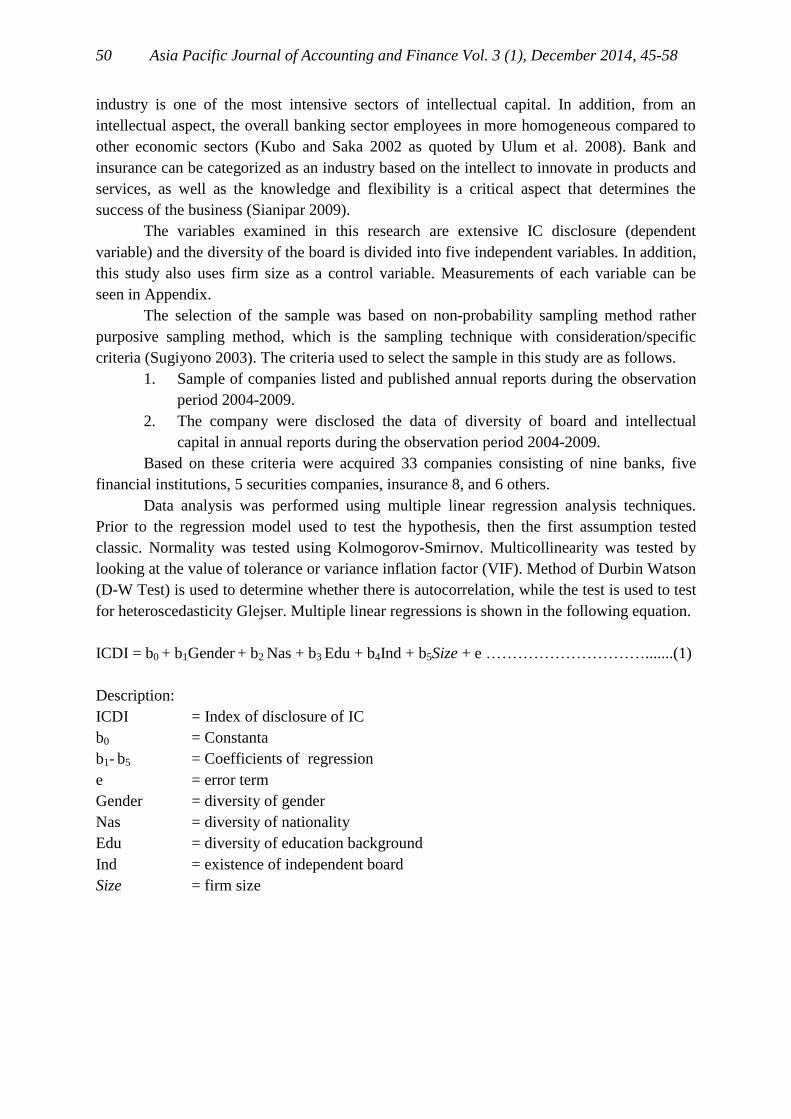

The variables examined in this research are extensive IC disclosure (dependent

variable) and the diversity of the board is divided into five independent variables. In addition,

this study also uses firm size as a control variable. Measurements of each variable can be

seen in Appendix.

The selection of the sample was based on non-probability sampling method rather

purposive sampling method, which is the sampling technique with consideration/specific

criteria (Sugiyono 2003). The criteria used to select the sample in this study are as follows.

1. Sample of companies listed and published annual reports during the observation

period 2004-2009.

2. The company were disclosed the data of diversity of board and intellectual

capital in annual reports during the observation period 2004-2009.

Based on these criteria were acquired 33 companies consisting of nine banks, five

financial institutions, 5 securities companies, insurance 8, and 6 others.

Data analysis was performed using multiple linear regression analysis techniques.

Prior to the regression model used to test the hypothesis, then the first assumption tested

classic. Normality was tested using Kolmogorov-Smirnov. Multicollinearity was tested by

looking at the value of tolerance or variance inflation factor (VIF). Method of Durbin Watson

(D-W Test) is used to determine whether there is autocorrelation, while the test is used to test

for heteroscedasticity Glejser. Multiple linear regressions is shown in the following equation.

ICDI = b0 + b1Gender + b2 Nas + b3 Edu + b4Ind + b5Size + e ………………………….......(1)

Description:

ICDI = Index of disclosure of IC

b0 = Constanta

b1- b5 = Coefficients of regression

e = error term

Gender = diversity of gender

Nas = diversity of nationality

Edu = diversity of education background

Ind = existence of independent board

Size = firm size

Page 7

Rasmini, Wirakusuma, Yuniasih, The Effect of Board Diversity on The Extent of….. 51

4. EMPIRICAL RESULTS AND DISCUSSION

The sample used in the analysis initially consisted of 198 observations (33 firms for

six years). Observations with a z-score below minus 2.90 or above 2.90 is considered as

outliers and excluded from the sample. A total of 15 observations are removed from the

sample so that the final sample to 183 observations. Testing for normality using the

Kolmogorov-Smirnov test showed a significance level of 0.065> 0.05. The test results

demonstrate the value of tolerance multicollinearity independent variable not less than 10%,

or 0.1 and the variance inflation factor (VIF) are all less than 10. The test results showed

autocorrelation in the first place but after the repair autocorrelation Lag Y is obtained by the

Durbin-Watson value of 1.980. This value is located between the dU (1.826) and 4-dU

(2.174). Glejser test results showed all the independent variables had no effect on the absolute

value of residuals. Based on these tests can be concluded that the regression equation in this

study have passed the test classic assumptions.

The results of hypothesis testing showed an adjusted R2 value is 0.475. This means

that the variance of independent variables that diversity of gender, diversity of nationality,

educational background diversity, the existence of an independent board, and the size of the

company is able to explain the dependent variable variant extensive IC disclosure by 47.5

percent, while the remaining balance of 52.5 percent is explained by other variables that not

included in the model. Based on the results of testing has known that the diversity of gender

and nationality have a positive influence on the area of IC disclosure. However, diversity

education and the existence of an independent commissioner have no effect on the area of IC

disclosure. Control variables firm size has a positive effect on the broad disclosure of IC with

t-value of 5.691 and 0.000 significance level <0.05.

Results of research on diversity of gender in the board of directors is in line with the

results of research conducted by Nalikka (2009) that gender diversity has a positive effect on

voluntary disclosure. Robbins and Judge (2008:206) suggest that women generally have more

detailed thoughts involved in the decision-making analysis. They tend to analyze the issues

before making a decision and process decisions had been made, resulting in consideration of

the problem and alternative solutions more closely. Therefore, women tend to like the

detailed information that can be used to analyze each alternative decision. Williams (2000)

and Swartz and Firer (2005) found the presence of women in the board of directors has a

positive effect on IC performance. A good performance ICs can trigger a company to conduct

a more extensive IC disclosure.

The results regarding the presence of foreign national‟s board members support the

hypothesis. Their presence brings valued opinions, perspectives, languages, beliefs, family

background, and diverse professional experiences, thus enriching the knowledge of business

and alternative problem solving is complex. In addition, the presence of foreign board

members were able to convince foreign investors that the company is professionally managed

(Randoy et al. 2006). Oxelheim and Randoy (2001) suggested that the presence of members

of the board of commissioners and directors with foreign nationality shows that the company

has made the process of globalization and information exchange in the network (network)

internationally. The presence of foreign directors on the board can lead to information

disclosure in the hope of the company's credibility will increase. Openness is shown by

Page 8

52 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

performing more extensive disclosures reply. This is in line with the results of this research is

the existence of a foreign national board member has a positive effect on the disclosure of IC.

Based on a global survey conducted Taylor and Associates in 1998 in Williams (2001) was

the issue of disclosure of intellectual capital is one of the ten types of information the user

needs. The broader of disclosure of IC is expected to increase the legitimacy of the company.

The results of this research on educational background do not support the hypothesis.

Formal education background of board of directors and directors are the cognitive

characteristics that may affect the ability of the board in making business decisions and

manage the business (Kusumastuti et al. 2006). However, this study did not find the same

thing because of education is not only acquired through formally channels. The ability of

members of the board of directors is also heavily influenced by their experience. In addition,

training courses can also affect one's decision to disclose some information, including

disclosure of information about IC. Therefore, the formal educational background is not the

only factor that will influence the decision to make disclosure of IC.

The existence of an independent member of board has no effect on the area of IC

disclosure. This study supports the results of Li et al. (2007) found that the composition of the

board of directors has no effect on IC disclosure. The results are not consistent with agency

theory. The existences of independent member of board are expected to cope with agency

problems and perform its role to protect shareholders. One form is to conduct a more

extensive disclosure. However, it is not proven in this study. Although the IC information

deemed important by Taylor and Associates study in 1998 in Williams (2001), but the

proportion of independent board member is not a determinant factor in making disclosure

decisions. The role of independent board of director with more emphasis on experience,

personal characteristics, and ability in carrying out its functions as compared to the

proportion of membership in the board of directors.

5. CONCLUSIONS AND SUGGESTIONS

Based on the research problem, the aims of research, theoretical background and

hypotheses and also the results of tests performed, it can be concluded that the diversity of

board, generally has a positive effect on IC disclosure, especially affected by gender and

nationality diversity. However, diversity of education background and the existence of an

independent board of directors are not able to explain adequately extensive IC disclosure.

Firm size as a control variable has a positive effect on the area of IC disclosure.

Several limitations affect the outcome of research and development needs to be

material in subsequent studies. The suggestions can be submitted are as follows.

1) Study was only conducted in the sector of financial companies that is listed on the

Indonesia Stock Exchange, subsequent research can do research with different objects

such as manufacturing companies to obtain consistent results.

2) The coefficient of determination (Adjusted R2) is equal to 0.475 which means the

variability of the dependent variable which can be explained by the independent

variable is equal to 47.5 percent, while the remaining balance of 52.5 percent is

explained by variables other than the research model. This means that there are other

variables that need to be identified to explain the influence of diversity on boards of

Page 9

Rasmini, Wirakusuma, Yuniasih, The Effect of Board Diversity on The Extent of….. 53

directors and extensive IC disclosure. Based on this research, other diversity variables

on board of directors that may influence the decision of the IC disclosure is cognitive

diversity such as experience, skill and competence (Coffey and Wang 1998) and the

diversity of demographics such as marital status (Slocum and Hellriegel 2007 in

Marimuthu 2008).

Page 10

54 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

REFERENCES

Abeysekera, I. K., and J. Guthrie. “An Empirical Investigation of Annual Reporting Trends

of Intellectual Capital in Sri Lanka.” Critical Perspectives on Accounting Vol. 16

No.3 (2005): 151-163.

Agrawal, A. and C. R. Knoeber. “Do Some Outside Directors Play a Political Role?” (2000),

Available at: http://ssrn.com/abstract_id=224133. Accessed 17 January 2011.

Ararat, M., M. Aksu, and A. T. Cetin. “Impact of Board Diversity on Boards‟ Monitoring

Intensity and Firm Performance: Evidence from the Istambul Stock Exchange.”

(2010), Available at: http://ssrn.com/abstract=1572283. (Accessed July 2010).

Bozzolan, S., F. Favotto, dan F. Ricceri. “Italian Annual Intellectual Capital Disclosure: An

Empirical Analysis.” Journal of Intellectual Capital Vol. 4, No. 4 (2003): 543-558.

Carter, D.A., B. J. Simkims, and W.G. Simpson. “Corporate Governance, Board Diversity,

and Firm Value.” The Financial Review No.38 (2002): 33-53.

_________, Frank D‟Souza, Betty J. Simkims, and W.G. Simpson. “The Diversity of

Corporate Board Committees and Financial Performance.” (2007), Available at:

http://ssrn.com/abstract=1106698 (Accessed July 2, 2010).

Cerbioni, F. and A. Parbonetti. “Exploring the Effect of Corporate Governance on Intellectual

Capital Disclosure: An Analysis of European Biotechnology Companies.” European

Accounting Review Vol.16, No.4 (2007): 791 – 826.

Coffey, B.S and J. Wang. “Board Diversity and Managerial Control as Predictors of

Corporate Social Performance.” Journal of Business Ethics Vol.17 (1998): 1595-

1603.

Fama, E. F. “Agency Problems and The Theory Of The Firm.” Journal of Political Economy.

88, No. 2 (1980): 288–307

and M. C. Jansen. “Separation of Ownership and Control.” Journal of

Law and Economics Vol. XXVI (1983), Available at: http://ssrn.com/abstract=94034.

(Accessed February 21, 2011).

Firer, S., and S. M. Williams. “Intellectual Capital and Traditional Measures of Corporate

Performance.” Journal of Intellectual Capital Vol. 4, No. 3 (2003): 348-360.

. Association between the Ownership Structure of Singapore Publicly

Traded Firms and Intellectual Capital Disclosures, Corporate Governance and

Intellectual Capital Research Paper 7, (2003)

URL:http://www.research.smu.edu.sg/faculty/cgic/Research/Research_Papers/CGICR

esearchPaper7.pdf.

Ghozali, I. Analisis Multivariate dengan Program SPSS. Semarang: Badan Penerbit

Universitas Diponegoro, 2006.

Goodstein, J., Kanak Gautam and Warren Boeker. “The Effects of Board Size and Diversity

on Strategic Change.” Strategic Management Journal Vol.15 (1994): 241-250.

Guthrie, J and R. M. Petty 2000. “Intellectual Capital: Australian Annual Reporting

Practices.” Journal of Intellectual Capital Vol. 1, No. 3 (1994): 241-251.

, R. M. Petty, and F. Ricerri. “External Intellectual Capital Reporting:

Contemporary Evidence from Hongkong and Australia.” (2004), Available at:

www.mgsm.edu.au/research. (Accessed June 2009).

Haniffa, R., and T. Cooke. “Culture, Corporate Governance and Disclosure in Malaysian

Corporation.” Presented at the Asian AAA World Conference. Singapore: 28-30

August, 2000.

Ikatan Akuntan Indonesia. Pernyataan Standar Akuntansi Keuangan No. 19. Jakarta:

Salemba Empat, 2007.

Page 11

Rasmini, Wirakusuma, Yuniasih, The Effect of Board Diversity on The Extent of….. 55

Kusumastuti, S., Supatmi, dan P. Sastra. ”Pengaruh Board Diversity terhadap Nilai

Perusahaan dalam Perspektif Corporate Governance.” Jurnal Ekonomi Akuntansi-

Universitas Kristen Petra (2006), Available at:

http://puslit.petra.ac.id/journals/accounting. (Accessed July 2, 2010).

Li, J., R. Pike and R. Haniffa. ”Intellectual Capital Disclosure in Knowledge Rich Firms: The

Impact of Market and Corporate Governance Factors.” Working Paper Series, No.

07/06. 2007.

Luckerath-Rovers, M. “Female Directors on Corporate Boards Provide Legitimacy to A

Company.“ (2010) Available at: http://ssrn.com/abstract=1411693. (24 Juli 2010).

Marimuthu, M. “Ethnic Diversity on Boards of Directors and Its Implications on Firm

Financial Performance.” The Journal of International Social Research. Vol. 1, No. 4

(2008): 431-445.

Meier, S. “How Global is Good Corporate Governance.” Ethical Investment Research

Services (2005) Available at: http://www.eiris.org/files/research

publication/howglobaliscorpgov05.pdf. (Accessed March 12, 2010).

Milliken, F., and Martins L. “Searching for Common Threads: Understanding the Multiple

Effects of Diversity in Organizational Groups.” Academy of Management Review

No.21 (1996): 402-434.

Nalikka, A. “Impact of Gender Diversity on Voluntary Disclosure in Annual Reports.”

Accounting and Taxation. Vol. 1, No. 1 (2009).

Oxelheim, L. and T. Randoy. “The Impact of Foreign Board Membership on Firm Value.”

Journal of Banking and Finance, Working Papers No. 567, (2001).

Pfeffer, J. and Salancik, G. The External Control of Organizations: A Resources Depedence

Perspective. New York: Harper & Row, 1978.

Ponnu, C.H. “Academic Qualifications of Board of Directors and Company Performance.”

The Business Review Cambridge Vol. 10, No.1 (2008): 177-181.

Purnomosidhi, B. “Praktik Pengungkapan Modal Intelektual pada Perusahaan Publik di BEJ.”

Jurnal Riset Akuntansi Indonesia Vol. 9, No. 1 (2006): 1-20.

Randoy, T., S. Thomsen, and L. Oxelheim. “A Nordic Perspective on Corporate Board

Diversity.” (2006) Available at:

http://www.nordicinovation.net/img/a_nordic_perspective_on_board_diversity_final_

web.pdf. (Accessed March 12, 2010).

Robbins, S. P. and T. A. Judge. Perilaku Keorganisasian. (Diana Angelica, Pentj). Ed. 12.

Jakarta: Salemba Empat, 2008.

Sianipar, M. “The Impact of Intellectual Capital Towards Financial Profitability and

Investors‟ Capital Gain on Shares: An Empirical Investigation of Indonesian Banking

and Insurance Sector for Year 2005-2007.” Makalah Disampaikan dalam Simposium

Nasional Akuntansi XII. Palembang: 4-6 November, 2009.

Siciliano, J.I. “The Relationship of Board Member Diversity to Organizational Performance.”

Journal of Business Ethics Vol.15 (1996): 1313-1320.

Sugiyono. Metode Penelitian Bisnis Cetakan ke-10. Bandung: Alfabeta, 2007.

Surya, I. dan I. Yustiavandana. Penerapan Good Corporate Governance: Mengesampingkan

Hak-hak Istimewaa demi Kelangsungan Usaha. Lembaga Kajian Pasar Modal dan

Keuangan Fakultas Hukum UI Ed.1. Cet.1. Jakarta: Kecana, 2006.

Swartz N-P and S. Firer. “Board Structure and Intellectual Capital Performance in South

Africa.” Meditari Accountancy Research Vol. 13 No. 2 (2005): 145-166.

Ulum, I., I. Gozhali, dan A. Chariri. “Intellectual Capital dan Kinerja Keuangan Perusahaan;

Suatu Analisis dengan Pendekatan Partial Least Squares.” Makalah Disampaikan

dalam Simposium Nasional Akuntansi XI. Pontianak: 23-24 Juli 2008.

Page 12

56 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

Wardhani, Ratna. “Tingkat Konservatisma Akuntansi di Indonesia dan Hubungannya dengan

Karakteristik Dewan sebagai Salah Satu Mekanisme Corporate Governance.”

Makalah Disampaikan dalam Simposium Nasional Akuntansi XI. Pontianak: 23-24

Juli, 2008.

Wicaksana, A. B. “Pengaruh Diversitas Dewan pada Kinerja Pasar: Kajian Empiris pada

Perusahaan yang Terdaftar di Bursa Efek Indonesia Tahun 2006-2008.” Thesis,

Denpasar: Universitas Udayana, 2010.

Wallace, R.S.O. and T.E. Cooke. “The Diagnosis and Resolution of Emerging Issues in

Corporate Disclosure Practices.” Journal of Accounting and Business Research, Vol.

20 (Spring 1990):143-151.

Williams, K.Y., and C.A. O‟Reilly. “Demography and Diversity in Organizations: A Review

of 40 Years of Research.” Research in Organizational Behavior No. 20 (1998): 77-

140.

Williams, S. M. “Is Intellectual Capital Performance and Disclosure Practices Related?”

Journal of Intellectual Capital Vol. 2, No. 3 (2001): 192–203.

Page 13

Rasmini, Wirakusuma, Yuniasih, The Effect of Board Diversity on The Extent of….. 57

APPENDIX

Table 1: Researchs on IC disclosure

Researcher Country External

Capital

Internal

Capital

Employee

competence

Guthrie and Petty (2000) Australia 40% 30% 30%

Bozzolan et al. (2003) Italia 49% 30% 21%

Guthrie et al. (2004) Hong Kong

Australia

37%

49%

28%

41%

35%

10%

Miller and Rosalind (2005) New Zealand 47% 21% 32%

Abeysekera and Guthrie

(2005)

Sri Lanka 44% 20% 36%

Purnomosidhi (2006) Indonesia 40% 35% 25%

Sources: Data processed

Table 2: Sample Selection Process

Description Amount of observation

Companies in financial sector were listed on Indonesian Stock

Exchange during 2004-2009

393

Companies in financial sector were not listed sequently during

2004-2009

(65)

Companies in financial sector without annual report (13)

Companies in financial sector without data of diversity of board

and director

(117)

The amount of sample 198 Sources: BEI, data processed.

Page 14

58 Asia Pacific Journal of Accounting and Finance Vol. 3 (1), December 2014, 45-58

Figure 1: The Measurements of Variables

No. Variable Measurement Reference

1. Intellectual capital

disclosure extent (Y)

ICDI is measured using dichotomy

approach, with code 1 for disclosed and 0

for undisclosed. ICDI ítems are presented in

Figure 2.

Cerbioni and

Parbonetti (2007),

and Purnomosidhi

(2006)

2. Diversity of gender

(X1)

The existence of woman in board is valued

in a dummy variable. If woman present in

board of director with code 1, and 0 for

contrary.

Ararat et al. (2010);

Kusumastuti dkk.

(2006); Wicaksana

(2010)

3. Diversity of

Nationality (X2)

The existence of foreign nationality in

board of director will defined into code 1

and 0 for contrary.

Ararat et al. (2010);

Kusumastuti et al.

(2006); Wicaksana

(2010)

4. Diversity of education

background (X4)

Variation of education background is

measured by percentage between member

of board with accounting, finance,

management and economic education

background and all of member of board.

Ponnu (2008),

Haniffa and Cooke

(2000).

5. Independent member

in board of directors

(X5)

Proporsion of independen member of board

of directors is compared to the whoe of

member in board of direcors.

Kusumastuti et.al.

(2006)

6. Firm Size (X6)

(Control variable)

Firm size is the value of the total assets of

the firm.

Cerbioni and

Parbonetti (2007)

Figure 2: Item of ICDI

Internal Capital External Capital Employee Competence

Intellectual Property

1. Patents

2. Copyrights

3. Trademarks

Infrastructure Assets

4. Management Philosophy

5. Corporate Culture

6. Information Systems

7. Management Processes

8. Networking Systems

9. Research Projects

1. Brands

2. Customers

3. Customer Loyalty

4. Company Names

5. Distribution Channels

6. Business Collaboration

7. Favourable Contracts

8. Licensing Agreements

9. Financial Contacts

10. Franchising Agreements

1. Know-how

2. Education

3. Vocational

qualification

4. Work-related

knowledge

5. Work-related

competence

6. Entrepreneurial

spirit

Sources: Purnomosidhi (2006), Cerbioni and Parbonetti (2007).