60

The End of Money Lecture 15 – Thursday, 28 October 2010 J A Morrison 1

The End of Money

Lecture 15 – Thursday, 28 October 2010J A Morrison

1

Lec 15: The End of Money

I. After Bretton WoodsII. Explaining Foreign Monetary

PolicyIII.The Future of Money

3

Lec 15: The End of Money

I. After Bretton WoodsII. Explaining Foreign Monetary

PolicyIII.The Future of Money

4

I. After Bretton Woods

1. What Changed?2. The Reinvention of the IMF

5

The BWS was an attempt to secure the benefits of

openness without sacrificing monetary policy autonomy (control over domestic price

level).

Keynes & White wanted to avoid the experience of the

1930s: policy autonomy secured by competitive

devaluations (adjustable ERs) and protectionist trade policy.

6

So, the BWS attempted to reconcile openness on trade and ER stability with policy autonomy by…

(1) Erecting moderate capital controls (on “speculative” capital)(2) Managing small imbalances through the IMF 7

Summary of the Bretton Woods System

8

• Stable ERs– ERs fixed within narrow band– No ER adjustments without consent of IMF– IMF makes loans to resolve imbalances stops

price-specie-flow

• Open Trade & Commerce– IMF created alongside Int’l Trade Organization ITO– IMF embraces burgeoning GATT regime

• Capital Controls– Currency convertible into gold or dollar– Limits on “speculative capital”

But in August 1971, Nixon “closed the gold window,” meaning: he unilaterally

devalued the dollar and he suspended convertibility.

After several successive conferences failed to

preserve the system, the Bretton Woods System was

essentially dissolved. 9

What changed?

10

Post-BW Monetary System• Disorderly ERs– Increasing Number of States Float– Others choose to fix (some

controversially so, like China)– Slower reactions to crises: 1994, 1997,

2008

• Regional currency agreements (Euro, CFA)– Decline of multilateralism

• Challenge to US power– Euro, Yen, & Yuan aspire to be Nth

Currency11

Official ER Regimes of Major Currencies

12

Fixed ER Regime Floating ER Regime

China; Hong Kong; Saudi Arabia

US; Euro; Britain; Russia; Japan; India; Australia; Poland; Switzerland

Note: These are the de jure (official) ER regimes. The regimes may not reflect market ER stability!!

I. After Bretton Woods

1. What Changed?2. The Reinvention of the IMF

13

Remember that the IMF was created principally to

manage the BWS. One of its purposes was to reconcile imbalances of payments.

14

But with the transition to floating ERs, the IMF

became an institution without a mission.

How did the IMF react?

15

Simply put, the IMF reinvented itself.

16

It went from trying to alleviate illiquidity to attempting to resolve

insolvency.

It went from trying to manage imbalances of

payments to redressing the supposed underlying causes

of those imbalances. 17

The Washington Consensus

• 1989: Formulated by John Williamson in context of Latin Amer crises & Post-Soviet Transition

• Supported by IMF, World Bank, & US Treasury

• 3 Pillars–Macroeconomic Discipline–Market Economy– Openness to World Economy (trade &

FDI)18

The New IMF: For Better or Worse

• Variable Track Record– Good: Eastern Europe & Mexico (1994)– Questionable: 1997 East Asian Financial

Crisis

• Gate Keeper for International Funding– Independent monitoring & rating – Potential tool of powerful countries

19

So now we know the broad contours of the history of

the international monetary system.

Let’s turn to consider how we, as social scientists, explain this empirical

record...20

The End of Money

I. After Bretton WoodsII. Explaining Foreign Monetary

PolicyIII.The Future of Money

21

How do we explain states’ foreign monetary policies?

Well, let’s return to Topic 3: Explaining Foreign

Economic Policy

22

Types of Explanations of FEP• Systemic/Structural Explanations– Variables: Distribution of Power;

International Regimes/Institutions– Examples: Steve Krasner; David Lake

• Domestic Explanations: 3 I’s– Ideas (Irwin)– Interests (Rogowski)– Institutions (North; Bailey, Goldstein, &

Weingast)

23

We’ve already applied these frameworks to explain trade

policy.

Now, we’ll employ them to explain some of the “critical junctures” in the history of

foreign monetary policy (FMP).

24

Remember that our mode here is to simultaneously...

(1) use the theories to explain the empirics;

and (2) use the empirics to test the theories.

25

First…

Charles Kindleberger, The World in Depression, 1929-

39, (1973).

26

“The explanation of this book is that the 1929 depression was so wide, so

deep and so long because the international economic system was

rendered unstable by British inability and United States unwillingness to

assume responsibility for stabilizing it in three particulars: (a) maintaining a

relatively open market for distress goods; (b) providing counter-cyclical

long-term lending; and (c) discounting in crisis.” (p 291)

27

Structural Theory• Hegemonic Stability Theory:

Hegemon provides vital public goods– Openness– Lender of last resort– Liquidity

• Theorists:– Steve Krasner: Trade openness– Charles Kindleberger: Stable

international financial system– Keohane: Int’l Regimes may stand in

place for hegemon 28

Second…

Jeff Frieden, “Exchange Rate Politics.”

29

“[I]ncreased levels of financial and commercial integration drive monetary

policy toward the exchange rate, make the exchange rate more distributionally divisive,

and lead to a more politicized context for the making of macroeconomic policy…All

else equal, domestically oriented producers prefer a flexible exchange rate,

internationally oriented ones a fixed exchange rate. Tradables producers prefer a weak (depreciated) currency, non-tradables

producersand overseas investors a strong

(appreciated) one.” (261)30

Frieden: Domestic Interests

• Increasing integration sharper political divisions– (Sound like Rogowski?)

• Map Interests onto preferences (p 260)– (1) ER Stability versus MPA– (2) High versus Low ER

31

So, FMP can be seen as a tool to serve domestic interests—

just like trade.

But FMP is far blunter an instrument than trade.

What are the implications of that for the usefulness of this type of explanation for FMP?

32

Third…

Karl Polanyi, The Great Transformation (1944).

33

(You’ve only had this in lecture, so I’ll recap it now.)

34

Polanyi: Domestic Institutions

• GS ideal sacrifices MPA• Practical Implications– Deflationary bias– Does not respond to unemployment

• Why would a state give up MPA? Serves capital at the expense of labor!

• Polanyi’s Historical Shift: democratization– Prewar: poor weren’t represented GS– 1930s Forward: poor stop putting up

with GS 35

Fourth…

G John Ikenberry, “Keynesian ‘New Thinking’ and the Anglo-American

Postwar Settlement.”

36

“I argue that a transatlantic group of economists and policy specialists, united by a common set of policy ideas and a shared view that past

economic failures could be avoided by innovative postwar economic

arrangements, led their respective governments toward agreement by identifying a set of common Anglo-American interests that were not

clearly seen by others.” (59)

37

So, Keynesian “New Thinking” pointed the way

to some kind of compromise between US and GB.

(Ikenberry, however, isn’t completely consistent on the nature of that

compromise.)

38

So, in Topic 2, we developed several different ways to explain

foreign economic policy: int’l structure, domestic institutions,

interests, & ideas.

We considered their explanatory power with respect to Trade

Policy.

And now we’ve done the same with Foreign Monetary Policy. 39

The End of Money

I. After Bretton WoodsII. Explaining Foreign Monetary

PolicyIII.The Future of Money

40

III. The Future of Money

1. Managing Monetary Systems2. Money Without Monetary

Sovereignty

41

States face a number of constraints in governing

their monetary systems…

42

Counterfeiting• Problem with fiat currency: giant

seigniorage!• John Locke’s fear– States don’t fear some dude in his

garage; states fear other states!– international norms are insufficient to

prevent economic warfare

• Examples:– Nazi Germany: Operation Bernhard (see

Counterfeiters, 2008)– North Korean Superdollars (or is it the

CIA?)43

Hoarding• Sometimes specific units of currency are

hoarded and/or disappear from circulation• Reasons:– Better Media:

• Small denominations can purchase more than large (“Big problem of small change”)

• But 10% charge at Coinstar machines!• Can’t use $100 bills at gas stations at night• Argentina: need coins for buses

– Intrinsic value surpasses exchange value: US penny and the rising price of copper

• Speculation: Argentina’s small coins today

44

Currency Competition

• Previously, we assumed monetary sovereignty

• But not all states have monetary sovereignty– Germany, 1923– Zimbabwe today

• Even the US dollar faces competition at home– Alternative Currency: foreign currency use at

home– Complementary Currency: Middlebury Money,

Ithaca Hours, Berkshares, E-gold, Bitcoin45

Speculative Attacks

• Predominantly affects leveraged, fixed regimes– Leverage: ratio of liabilities (circulating

cash) to reserves– Greater leverage greater risk

• May be organized or disorganized– Disorganized: panic run on the bank– Organized: coordinated attack by

entities with market power

46

47

Hmm. I wonder if I might try

that…

George Soros, “The Man who Broke the Bank of England”

Breaking the Bank of England

• GB joined European ER Mechanism (ERM) in 1990– Obliged to maintain ER within 6% band of European

currencies

• By 1992, Pound was overvalued; despite 15% interest rates

• Soros bet on devaluation: borrowed £6.5bn to buy Deutschmarks & Francs effect: market ER of GBP vis-à-vis DM fell

• Black Wednesday (16 Sept 1992): GB devalued GBP

• Soros converted back into GBP at new, lower ER, getting approximately £7.5bn

Soros then repaid £6.5bn loans, netting £1bn !! 48

Contagion• Currency values are often linked– Fixed: US & Hong Kong– Trade: Brazil & Argentina; US & Canada– Investment: 1997 East Asian Financial

Crisis

• Problems with one currency spread to linked currencies even if linked economies have no other problems

49

III. The Future of Money

1. Managing Monetary Systems2. Money Without Monetary

Sovereignty

50

Remember that we’ve been assuming that states enjoy monetary sovereignty--the ability to control the market value of domestic currency, currency used within their

borders.

51

Jerry Cohen, however, reminds us that this assumption has rarely

held true.

Across most of history, the “one-country, one-currency” correlation

has not been the rule.

Strong currencies have traveled abroad while weak currencies

have struggled to circulate even in their home markets. 52

This raises two questions:

(1) What determines the geography of money?

(2) What is the future of money?

53

The answer to both questions turns, in large part, on the operation of

currency hierarchy.

54

Currency Hierarchy• Currency Hierarchy: some currencies

perform the functions of money better than others

• Medium of Exchange:– Transactional Liquidity: easy to exchange– Transaction Network: lots of goods to

purchase

• Store of Value:– Capital Certainty: reasonable predictability

of asset value– Return: real rate of interest (controlling for

inflation) 55

Benefits of Monetary Sovereignty

• Monetary Policy Autonomy• Seigniorage• Political Symbolism• Insulation (Independence from

Foreign Influence)

56

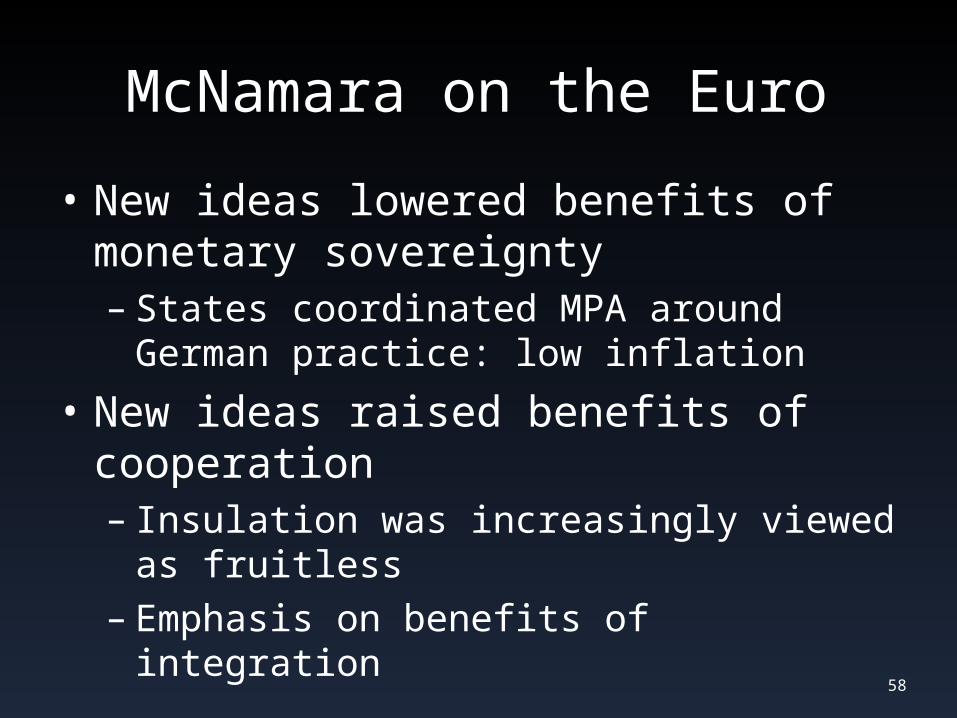

But if monetary sovereignty is so great, why have

several European countries given that up to adopt the

Euro?

57

McNamara on the Euro

• New ideas lowered benefits of monetary sovereignty– States coordinated MPA around German

practice: low inflation

• New ideas raised benefits of cooperation– Insulation was increasingly viewed as

fruitless– Emphasis on benefits of integration

58

Are such currency unions the wave of the future?

Europe might be special. Cohen thinks so. But McNamara seems to

disagree.

59

The answer might well depend on whether the

Europeans save the Euro!

59

What we Did Today

• (1) Finished History of the International Monetary System

• (2) Used frameworks from Topic 3 to explain Foreign Monetary Policy

• (3) Considered the potential future trajectory of the international monetary system

60