Denny Ellerman Center for Energy and Environmental Policy Research Massachusetts Institute of Technology New Directions in Regulation Seminar JFK School, Harvard University October 22, 2007. Massachusetts Institute of Technology Center for Energy and Environmental Policy Research. - PowerPoint PPT Presentation

29

MIT CEEEPR The EU CO 2 Emissions Trading Scheme A. Denny Ellerman Center for Energy and Environmental Policy Research Massachusetts Institute of Technology New Directions in Regulation Seminar JFK School, Harvard University October 22, 2007 Massachusetts Institute of Technology Center for Energy and Environmental Policy Research

Transcript

MIT CEEEPR

The EU CO2 Emissions Trading Scheme

A. Denny Ellerman

Center for Energy and Environmental Policy Research

Massachusetts Institute of Technology

New Directions in Regulation Seminar

JFK School, Harvard University

October 22, 2007Massachusetts Institute of TechnologyCenter for Energy and Environmental Policy

Research

MIT CEEEPR

Topics

• Market Development

• 2005-06 Results: Over-allocation?

• Allocation choices

• Broader Implications

MIT CEEEPR

The EU ETS• 27-state multinational CO2 trading system

• Classic cap-and-trade covering large sources– About 45% of EU CO2 emissions

• Hybrid implementation of Kyoto Protocol– Trading and non-trading sectors

– Decentralized cap within a cap with CDM linkage

• 2005-07 trial period, 2008-12 second period, and post 2012 periods

MIT CEEEPR

The EUA Market• Mostly futures trading in front contract

– Also, spot but 10-15% of total volume

• OTC market initially, but exchanges developed quickly and account for 30-40% of volume– US allowance markets all OTC

• An EUA is a downloaded AAU, but non-EU AAUs are not acceptable; CERs/ERUs are.– Also any linked systems: probably Norway

MIT CEEEPR

Monthly EUA Trading VolumesDecember 2004 - September 2007

Average Member State Positions As % of Allocation, 2005 and 2006

-30% -20% -10% 0% 10% 20% 30% 40% 50%

Great BritainIreland

ItalySpain

AustriaGreece

SloveniaGermanyPortugalCyprus

DenmarkBelgium

NetherlandsFinlandPoland

HungarySweden

CzechFrance

SlovakiaLuxembourg

LatviaEstonia

Lithuania

EU Total

Net Long

Gross Long

Net Short

Gross Short

MIT CEEEPR

Average 05-06 Positions by Sector

-200 -150 -100 -50 0 50 100 150 200

Metal ore

Glass

Coke ovens

Ceramics, Bricks and Tile

Pulp and Paper

Refineries

Cement and Lime

Iron and Steel

Power and Heat

Mt CO2

Net Long

Gross LongNet Short

Gross Short

MIT CEEEPR

EU ETS: Over-allocation

• Not an issue until first data release• Muddled concept; conflated with being long• With inter-period banking constraint, sure to

be either long or short• Concept also used to imply no abatement; data

are showing abatement• Inherently difficult problem of ensuring

shortage with ambition is modest; ex post rarely coincides with ex ante

MIT CEEEPR

Topics

• Market Development

• 2005-06 Results: Over-allocation?

• Allocation choices

• Broader Implications

MIT CEEEPR

Allocation in the EU ETS

• Delegation to member states to decide total and distribution with 95% grandfathered

• Member state decisions subject to review by the European Commission– In practice, limited to the proposed totals, and– No ex post adjustment or quota management

• Huge data problems at installation level• Extended discussion between industry and

government on data and allocation principles

MIT CEEEPR

What Choices were Made?

• Allocations based on recent emissions– Benchmarking proved infeasible

• Shortage allocated to the power sector– More abatement possibilities & no competitive

problems

• Very little auctioning (4 MSs & 0.13% of total)

• New entrant and closure provisions– Potentially distorting effects but ubiquitous

MIT CEEEPR

Principles or Politics?• Near universal disapproval of grandfathering,

yet always chosen– Is there more than just politics & lobbying?

• Unacknowledged social norms?– Lockean prior use and squatter rights– EU variant: production conveys the right

• A convergence of fairness and expediency?– Allowances permit Coasian separation of

efficiency and equity– Assign rights to mitigate financial impact of the

change in prices and rules

MIT CEEEPR

NAP2 Differences

• More auctioning: 11 MS’s, 3% of total

• Some increase in benchmarking, but still little

• Substantially lower caps– Based on aggregate 2005 Verified emissions

– All East European MS’ suing in ECJ

– Wide variation among MSs (-19% in Denmark to +33% in Lithuania (relative to 2005 emissions)

• Updating at micro level only in East Europe

MIT CEEEPR

Evolution of Auctioning in the EU ETS

Member State Percent of Cap Auctioned

2005-07 2008-12

Denmark 5.0% 0%

Hungary 2.5% 4.3%

Lithuania 1.5% 2.9%

Ireland 0.75% 0.5%

Austria 0% 1.2%

Belgium 0% 0.3%

Germany 0% 8.8%

Italy 0% 5.8%

Luxembourg 0% 4.8%

Netherlands 0% 4.3%

Poland 0% 0.9%

UK 0% 7.0%

EU Total 0.13% 3.1%

MIT CEEEPR

NAP2 (2008-12) vs. NAP1 (2005-07)

% Relation to

1st Period Total

% Relation to 2005 Emissions

EU 15 - 11.4% - 6.1%

EU10 - 12.8% + 5.5%

EU25 - 11.7% - 3.9%

MIT CEEEPR

NAP2 Totals in Relation to NAP1 and 2005

-30%

-20%

-10%

0%

10%

20%

30%

40%

-35% -30% -25% -20% -15% -10% -5% 0% 5%

In Relation to NAP1 Total

In R

elat

ion

to 2

005

Emis

sion

s

Lthuania

Latvia

EstoniaMalta

Denmark

LuxembourgFrance

ItalySpain

Slovakia

Sweden

Portugal

Ireland

FinlandGermany

UK

Cyprus

SloveniaAustria

GreeceEU25

HungaryBelgium

Czech R

Poland

Netherlands

MIT CEEEPR

Topics

• Market Development

• 2005-06 Results: Over-allocation?

• Allocation choices

• Broader Implications

MIT CEEEPR

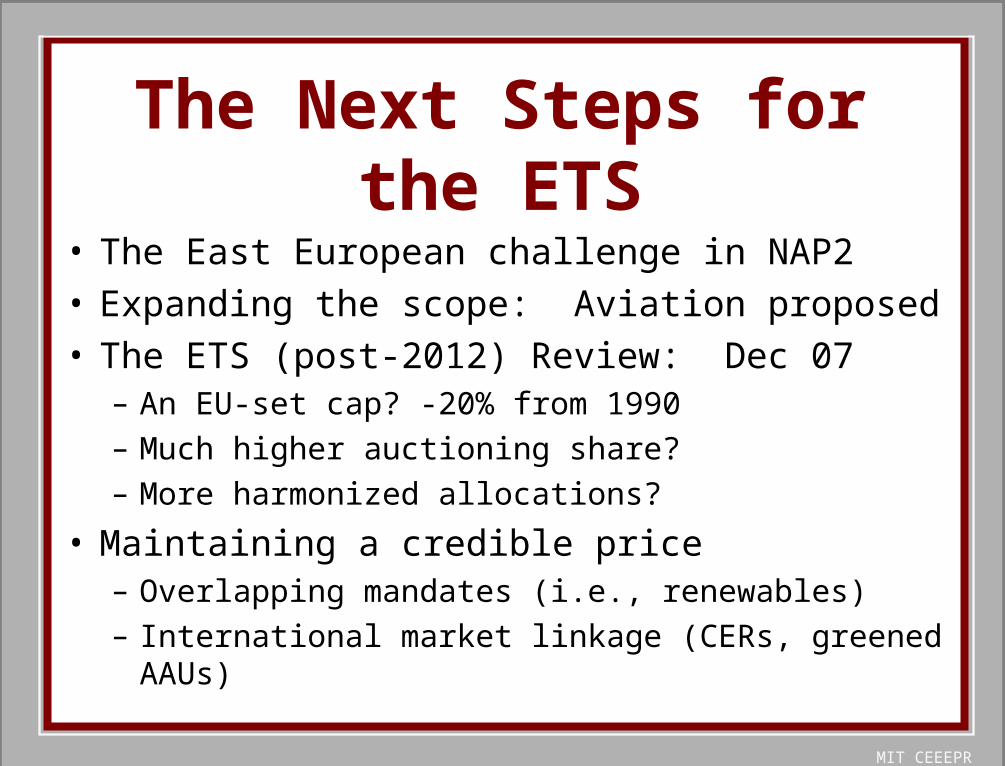

The Next Steps for the ETS

• The East European challenge in NAP2

• Expanding the scope: Aviation proposed

• The ETS (post-2012) Review: Dec 07 – An EU-set cap? -20% from 1990

– Much higher auctioning share?

– More harmonized allocations?

• Maintaining a credible price– Overlapping mandates (i.e., renewables)

– International market linkage (CERs, greened AAUs)

MIT CEEEPR

The EU ETS as Prototype• A multinational trading system with a uniform

price on carbon throughout the EU

• The east/west parallel to the global north/south divide– Differing criteria for EU15 and Accession-10

– Differing responsibilities for non-covered emissions

• What made all 25 join up?– The European idea?

– Or the benefits of the club?

MIT CEEEPR

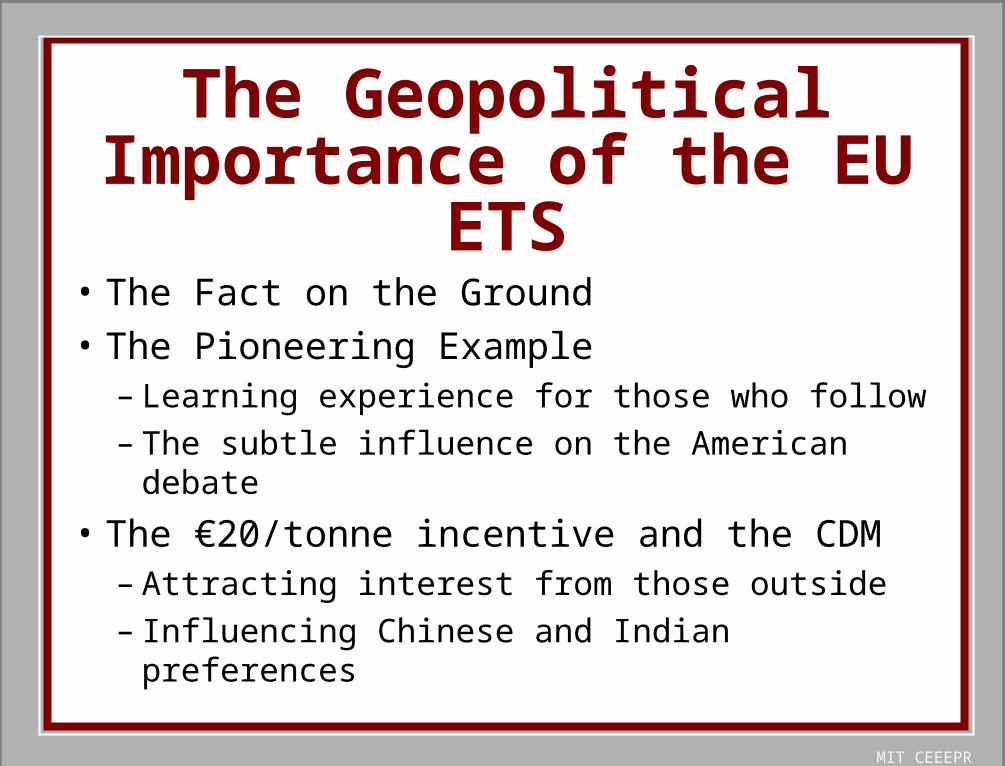

The Geopolitical Importance of the EU ETS

• The Fact on the Ground

• The Pioneering Example– Learning experience for those who follow

– The subtle influence on the American debate

• The €20/tonne incentive and the CDM– Attracting interest from those outside

– Influencing Chinese and Indian preferences

MIT CEEEPR

The Challenges Ahead

• Continuing the EU ETS and keeping it open

• Avoiding trans-Atlantic acrimony in global environmental diplomacy– First step is linking EU and US systems

• Developing combination of community and interest that will attract others (as in the EU)

• Finding a multinational institution to coor-dinate and negotiate accession/membership