Seminar in International Economics: Dealing with Economic Crises JProf. Dr. Konstantin M. Wacker Chair of International Economics Gutenberg School of Management and Economics Johannes Gutenberg University Mainz Summer term 2015 Seminar Thesis The European financial crisis The role of capital flows and the distressed banking system Submitted by: Name Student ID: 1234567 Major: Master in International Economics and Public Policy Street City Email: [email protected]

Transcript

Seminar in International Economics:

Dealing with Economic Crises

JProf. Dr. Konstantin M. Wacker

Chair of International Economics

Gutenberg School of Management and Economics

Johannes Gutenberg University Mainz

Summer term 2015

Seminar Thesis

The European financial crisis The role of capital flows and the distressed banking system

Submitted by:

Name

Student ID: 1234567

Major: Master in International Economics and Public Policy

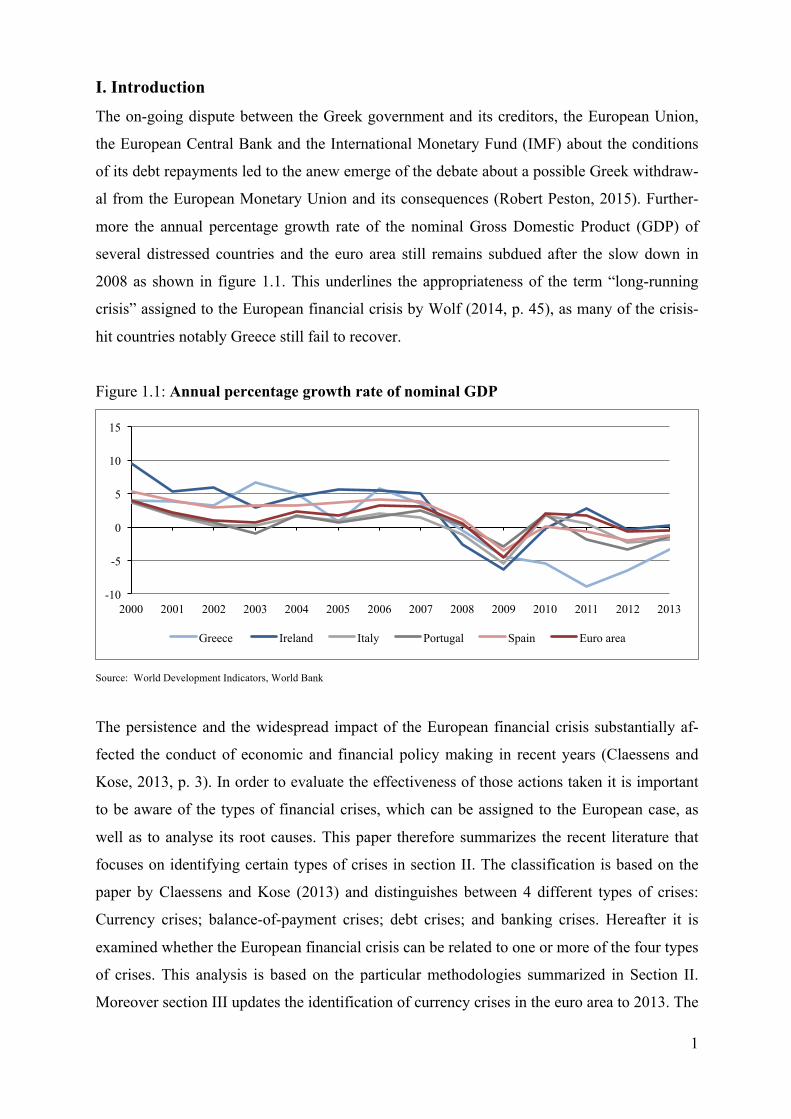

identification of the remaining types of crises covers time periods until 2011 and 2012, re-

spectively and provides the need for an update in further studies. The goal of this paper is to

analyse whether one or more of the aforesaid types of crises can classify the European finan-

cial crisis. Section IV examines the build up of pre-crisis current account deficits in the crisis-

hit countries of the euro area and the role of official capital flows after the outbreak of the

crisis, in particular the role of the Target system, in more detail.

While only one episode of a sovereign debt crisis can be identified in the respective period,

the European financial crisis can be characterised by several episodes of sudden stops and

banking crises. Capital exports to crisis-hit countries prior to the crisis tended to be excessive,

which caused large current account deficits in those countries and was a major factor of the

European financial crisis. The prevailing post crisis current account deficits in the crisis-hit

countries of the euro area can be attributed to official capital inflows, which counterbalanced

private capital outflows and thus mitigated the effects of the sudden stop episodes. The wid-

ening of Target balances, an example of public capital flows, reflects capital exports from the

core to the European periphery and in particular the crowding out of refinancing credits in the

former group of countries and increasing refinancing credits to the distressed banking sector

in the latter. While Target imbalances can be addressed by adopting the rules of the American

payment system, policy actions should focus on the persistent current account deficits and the

distressed banking system in the crisis-hit countries.

II. Literature

The methods used to identify and classify crises are various and often based on methodologies

derived from theories explaining these crises (Claessens and Kose, 2013, p. 22). It is im-

portant to distinguish between the identification of different types of crises. Whereas currency

crises and sudden stops can be objectively classified, the dating of debt and banking crises

involves qualitative and judgmental analyses (Claessens and Kose, 2013, p. 22). The subjec-

tive approach of the latter and variations in methodologies, notably in threshold values of cer-

tain indicators, explain the diversity of identification methods and their results (Claessens and

Kose, 2013).

II.1 Currency crises

Currency crises emerge in the event of a speculative attack on the currency. Possible out-

comes range from a devaluation, a sharp depreciation of the domestic currency, a sudden drop

in international reserves, to sharply increasing interest rates, depending on the degree of inter-

3

vention by the authorities (Claessens and Kose, 2013, p.12). Different dating approaches have

been evolved, which are based on the various outcomes of currency crises. Laeven and Va-

lencia (2013, p. 250) define a currency crisis as a nominal depreciation of the domestic cur-

rency vis-à-vis the US-Dollar of at least 30 per cent. The dataset of their study covers the pe-

riod from 1970 to 2011 and contains every country of the euro area, except Malta and Cyprus.

Furthermore, the rate of depreciation must be at least 10 percentage points higher than the rate

of depreciation of the previous year. This approach is based on Frankel and Rose’s (1996, p.

353) definition of a currency crisis. However, the latter use a threshold depreciation of 25 per

cent. The reason behind the second criterion is to avoid identifying independent currency cri-

ses every year, in countries with high inflation rates and thus high-expected rates of deprecia-

tion (Frankel and Rose, 1996, p. 353). As mentioned above monetary authorities have certain

instruments at their hands to defend the domestic currency in case of a speculative attack.

Hence, the previous approach may fail to identify a currency crisis, if an outflow of interna-

tional reserves or the adjustment in interest rates cushions exchange rate movements

(Claessens and Kose, 2013, p. 23). Glick and Hutchison (1999, p. 7) identify currency crises

on the basis of changes in an index of currency pressure, thus using the broader definition of

currency crises that includes unsuccessful attacks. The index is defined as a weighted average

of monthly per cent reserve outflows and monthly real exchange rate changes (Glick and

Hutchison, 1999, p. 7). The weights are inversely related to the variance of each component

of the index for each country, to equalize the influence of these components on the index

(Claessens and Kose, 2013, p. 23). Changes exceeding the mean by twice the country specific

standard deviation identify a currency crisis (Glick and Hutchison, 1999, p. 7). Kaminsky and

Reinhart (1999, p. 498) apply the same index. However, they use a change of three standard

deviations to catalogue a currency crisis. The differing threshold values may lead to differ-

ences in start and end dates of crises (Claessens and Kose, 2013, p. 22). Assessing these, yet

noteworthy, is beyond the scope of this paper.

II.2 Sudden stops and balance-of-payment crises

A sudden stop is characterised by a large and largely unexpected drop in international capital

inflows or a significant reversal in aggregate international capital flows to a country

(Claessens and Kose, 2013, p. 12). Disruptions in the supply of external financing affecting

the private and the public sector are classified as a sudden stop or a balance-of-payment crisis

(Merler and Pisani-Ferry, 2012, p. 8). Following the previous definition the literature focuses

on international capital flows to identify episodes of balance-of-payment crises. The method-

4

ology of Calvo, Izquierdo and Mejía (2004, p. 14) identifies a sudden stop, if at least one ob-

servation contains a year-on-year drop in capital flows that is two standard deviations below

the mean. The end of a sudden stop is determined by the first time the year-on-year change of

capital flows exceeds one standard deviation below its mean to incorporate the persistence

essential to many sudden stop episodes (Calvo, Izquierdo and Mejía, 2004, p. 14). A balance-

of-payment crises, once identified, starts when the year-on-year change in capital flows falls

one standard deviation below its mean. The latter threshold is set for symmetry reasons (Cal-

vo, Izquierdo and Mejía, 2004, p. 14). The determination of a valid proxy for international

capital flows is crucial. Since international reserves can be used to absorb disruptions in the

supply of external financing, episodes of sudden stops do not necessarily coincide with epi-

sodes of current account reversals (Edwards, 2004, p. 15). Thus, Calvo, Izquierdo and Mejía

(2004, p. 42) use the trade balance net of changes in international reserves in their empirical

study. Accordingly, their proxy incorporates private and public capital flows, mirroring the

evolution of the current account.1 However, according to Merler and Pisani-Ferry (2012, p. 3),

identifying balance-of-payment crises on the sole basis of the evolution of the current account

is a flawed approach, if the financial account includes official capital flows. Official capital

flows come along with net private capital flows, in case a stand-alone country is under an

International Monetary Fund programme or in a monetary union. Merler and Pisani-Ferry

(2012, p. 4), otherwise applying the approach of Calvo, Izquierdo and Mejía (2004), obtain

private capital inflows, by deducting official capital inflows from the current account balance.

The dataset of their study covers the period from 2002 to 2011 and contains every country of

southern Europe (Merler and Pisani-Ferry, 2012, p. 3). Sections III and IV cover the role of

official capital flows on the basis of the European financial crises more extensively.

II.3 Foreign and domestic debt crises

A foreign debt crisis occurs when a country is not able to, or purposely refuses to service its

foreign debt. The result can take the form of a sovereign and/or private debt crisis (Claessens

and Kose, 2013, p. 12). A domestic debt crisis in contrast is characterised by an explicit or

implicit default of domestic sovereign debt. The implicit default is realized either by inflating

the currency or by employing other forms of financial repression (Claessens and Kose, 2013,

p. 12). Since this paper focuses on foreign debt crises, in particular sovereign debt crises, only

the literature concerned with their identification is introduced below. External sovereign debt 1 Neglecting the primary income account and the secondary income account the evolution of the current account

is by definition equal to the evolution of the trade balance.

5

crises involve a specific year of default on payments, which facilitates the identification of

such crises (Claessens and Kose, 2013, p. 24). The start dates of defaults are obtained from

classifications of rating agencies or from international financial institutions. Laeven and Va-

lencia (2013, p. 250) rely on various databases to identify sovereign debt crises and to deter-

mine their start dates.2 Their methodology consists of an extension of the aforesaid definition

of sovereign debt crises. Besides episodes of sovereign debt default, the authors also identify

episodes of debt restructuring (Laeven and Valencia, 2013, p. 250). Das, Papaioannou and

Trebesch (2012, p. 8) point out that, while sovereign defaults and debt restructurings are

closely linked, they do not coincide, as both can occur independently. Furthermore, the empir-

ical study by Laeven and Valencia (2013, p. 250) considers defaults on private claims. Since

the authors are mainly interested in the identification of the crises themselves, rather than

their exact dating, they only provide start dates. This approach is sufficient for the purpose of

this paper, which is the classification of the European financial crisis. Therefore, the issue of

identifying the end date of sovereign debt crises summarized by Claessens and Kose (2013, p.

24) can be neglected and its description is beyond the scope of this paper. Lastly it is notewor-

thy, that other methodologies trying to identify sovereign debt crises focus on the surge in

spreads in sovereign bonds, which suggests an increasing probability of default (Claessens

and Kose, 2013, p. 24).

II.4 Banking crises

By providing maturity transformation a bank can raise social welfare, because it insures de-

positors against liquidity shocks (Diamond and Dybvig, 1983, p. 403). However, the resulting

maturity mismatch between its asset and liability side makes a bank vulnerable to coordina-

tion problems (Claessens and Kose, 2013, p. 18). Bank runs, a manifestation of such coordi-

nation problems, and failures can induce banks to suspend the convertibility of their liabilities

or cause government actions, like extending liquidity and capital assistance, and thus lead to a

banking crisis (Claessens and Kose, 2013, p. 12). Banking crises are mainly identified by us-

ing a qualitative approach, based on the combination of events. Those events can be bank

specific, like bank runs, or include government interaction, like forced closures or mergers,

government takeover or the extension of government assistance to one or more financial insti-

tutions (Claessens and Kose, 2013, p. 25). The advantage of the approach of using events to

2 The databases comprise of information from Beim and Calomiris (2001), World Bank (2002), Sturzenegger

and Zettelmeyer (2006), IMF staff reports, and reports from rating agencies (Laeven and Valencia, 2013, p.

250).

6

identify banking crises is its flexibility, which makes it possible to address the various mani-

festations of banking crises (Laeven and Valencia, 2013, p. 228). Some banking crises incur a

collapse of a significant fraction of the banking system, while in other cases bank closures can

be prevented by government intervention and regulatory forbearance, respectively (Laeven

and Valencia, 2013, p. 227). Furthermore, some banking crises can be related to a decrease in

aggregate demand shocks, while others are caused by idiosyncratic shocks (Laeven and Va-

lencia, 2013, p. 227). The methodology, developed by Laeven and Valencia (2013, p. 228),

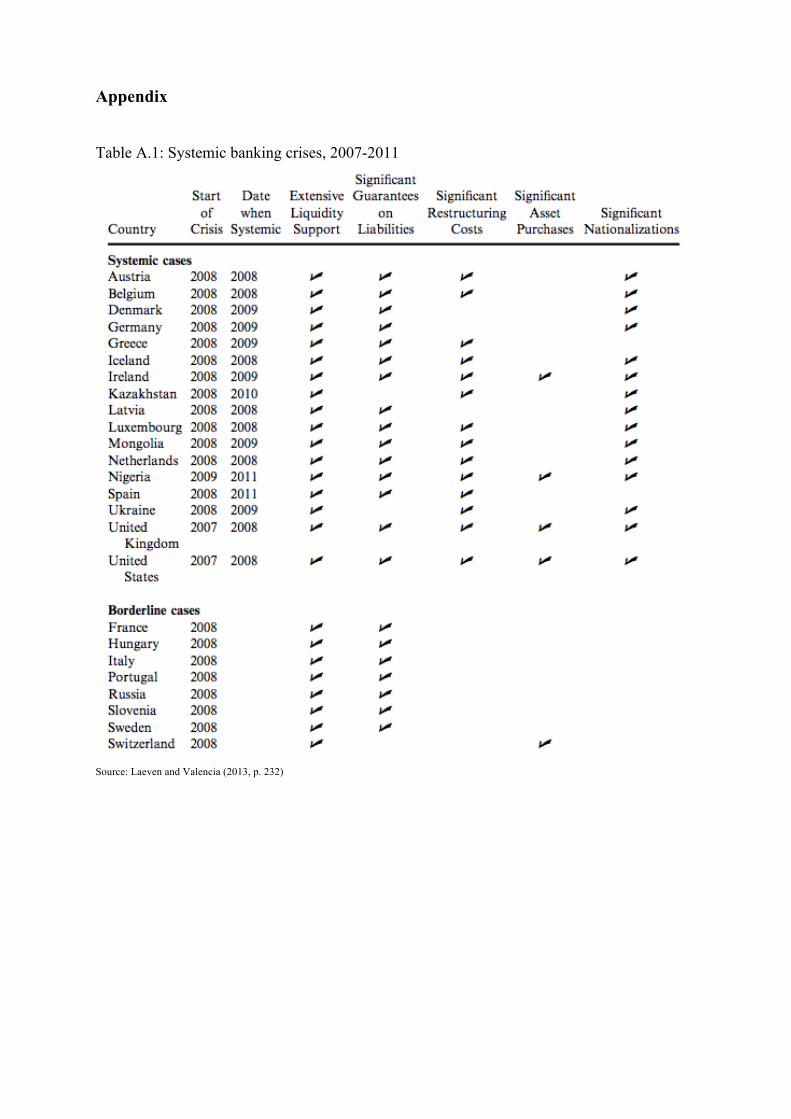

identifies a systemic banking crisis in case significant sign of financial distress in the banking

system and significant banking policy intervention measures can be observed. The start date

of a systemic banking crisis is defined as the date, when both criteria are met.3 The first crite-

rion is indicated by significant bank runs, losses in the banking system and bank liquidations

(Laeven and Valencia, 2013, p. 228). The second criterion incorporates deposit freezes and

bank holidays, significant bank nationalizations, bank restructuring gross cost of at least 3 per

cent of GDP, extensive liquidity support, significant guarantees put in place and significant

asset purchases. If at least three of the latter criteria are met, a systemic banking crisis is iden-

tified (Laeven and Valencia, 2013, p. 229). In some cases however government interventions

are implemented on a large scale, but consist of less than three measures. In these cases

Laeven and Valencia (2013, p. 229-230) apply a new sufficient condition for a crisis episode,

which replaces the initial one: A banking crisis is classified as systemic, when either (i) non-

performing loans exceed 20 per cent or bank closures are above 20 per cent of banking system

assets or (ii) fiscal restructuring costs of the banking sector exceed five per cent of GDP. The

end date of a systemic banking crisis is defined, as the year before real credit growth and real

GDP growth are positive for two successive years (Laeven and Valencia, 2013, p. 245).

III. The Classification of the European financial crisis

This section is concerned with the analysis of the recent European financial crisis. In particu-

lar it is examined, whether the aforesaid crisis can be related to one or more of the four previ-

ously described types of crises. The analysis is mainly based on the identification methodolo-

gies applied in the study of Laeven and Valencia (2013) and Merler and Pisani-Ferry (2012),

respectively. Their methods are introduced in the previous section. While this selection suf-

fers from a lack of completeness, it contains recent data about the European financial crisis.

3 As opposed to the identification of sovereign debt crises and currency crises, which only incorporates the start

dates of the crises, as explained previously, the dating of banking crises by Laeven and Valencia (2013, p. 228)

considers the start as well as the end dates.

7

By increasing the amount of studies, further research can broaden the scope of the analysis

and thus ensure a complete assessment.

III.1 Currency crisis

In May 2010, in the midst of the negotiations about the establishment of the European Finan-

cial Stability Facility (EFSF) and the European Financial Stabilisation Mechanism (EFSM),

respectively and the development of a rescue plan for Greece, European politicians started to

use the terminology of a systemic euro crisis (Sinn, 2010, p. 5). This subsection briefly exam-

ines, whether the usage of the aforesaid terminology was valid and thus, whether the Europe-

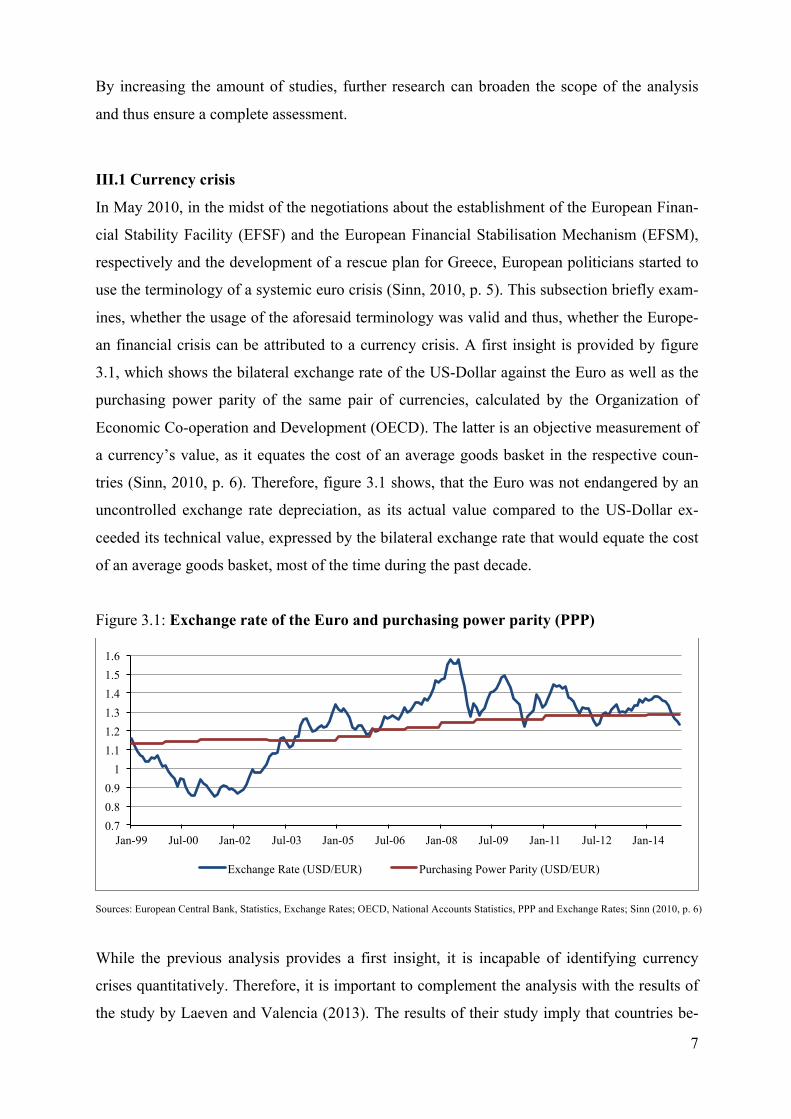

an financial crisis can be attributed to a currency crisis. A first insight is provided by figure

3.1, which shows the bilateral exchange rate of the US-Dollar against the Euro as well as the

purchasing power parity of the same pair of currencies, calculated by the Organization of

Economic Co-operation and Development (OECD). The latter is an objective measurement of

a currency’s value, as it equates the cost of an average goods basket in the respective coun-

tries (Sinn, 2010, p. 6). Therefore, figure 3.1 shows, that the Euro was not endangered by an

uncontrolled exchange rate depreciation, as its actual value compared to the US-Dollar ex-

ceeded its technical value, expressed by the bilateral exchange rate that would equate the cost

of an average goods basket, most of the time during the past decade.

Figure 3.1: Exchange rate of the Euro and purchasing power parity (PPP)

Sources: European Central Bank, Statistics, Exchange Rates; OECD, National Accounts Statistics, PPP and Exchange Rates; Sinn (2010, p. 6)

While the previous analysis provides a first insight, it is incapable of identifying currency

crises quantitatively. Therefore, it is important to complement the analysis with the results of

the study by Laeven and Valencia (2013). The results of their study imply that countries be-