The purpose of the present paper is to survey recent trends in the European automotive spare parts market. The distribution activity that the paper describes involves manufacturers, suppliers and dealers, but does not include repair service centres. Nor does it focus on the impact of Euro- pean regulations. The following countries are highlighted: France, Germany, Spain and Benelux. The flows we analyse are the physical (stock management and movements) and informational (order processing and replenish- ment) flows that are associated with the spare parts distribution activities that link manufacturers and dealers in the aforementioned countries. We also investigate manufacturers’ and dealers’ strategies for positioning them- selves on the market. We study current logistics organisations with a view towards appreciating how these strategies and organisations have evolved, and also in order to analyse the present and future role that is being played by the Block Exemption Regulation in auto-motive spare parts distribu- tion systems. Our first step was to examine the characteristics of the market: actors’ positions, specific products, logistical constraints and organisa- tional resources (e.g. networks, warehouses). By meeting with the market’s main protagonists, we could validate earlier research and identify flows clearly. We then established how European constraints, especially Block Exemption Regulation 1475/95, could influence future develop- ments. THE EUROPEAN AUTOMOTIVE SPARE PART MARKET ACTORS We interviewed car manufacturers, spare parts suppliers, non-indepen- dent dealerships and national inde- pendent repair chains associations in an effort to ascertain how the non-independent after sales spare parts market functions. The present report does not delve into the role of "original" spare parts suppliers. We observed that dealers’ turnover and profits breakdown as follows: ➢ Cars: 70% of all turnover, 50% of all profits ➢ Spare parts: 30% of all turnover, 50% of all profits For several years now, the European automotive after sales market has been going through widespread change as a result of the many mergers that have arisen in this sector. Existing networks have been evolving, moving towards an ever-greater degree of concentration. In the year 2002, the Block Exemption Regulation is due to expire, and this should lead to the distribution market being opened up to independent networks. The present study analyses the state of this market, as well as the major European car manufacturers’ strategies for coping with such economic changes. The Evolution of the European Automotive Spare Parts Distribution Market 70 Supply Chain Fo r u m An International Journal N°1 - 2000 www.supplychain-forum.com A study conducted by: Jolanda Bijl, Hélène Mordret, Bruno Multrier, Stephanie Nieuwhuys, Nicolas Pitot Students at the ISLI in Bordeaux… … supervisors: Sébastien Gannac European Business Manager EXEL Automotive Simon Hobbs Director and General Manager EXEL Automotive Mike Summers Vice-President EXEL Automotive

Transcript

The purpose of the present paperis to survey recent trends in

the European automotive spare

p a rts market. The distributionactivity that the paper describes

involves manufacturers, suppliers

and dealers, but does not includerepair service centres. Nor does

it focus on the impact of Euro -

pean regulations. The followingcountries are highlighted: France,

Germany, Spain and Benelux.

The flows we analyse are the

physical (stock management and

movements) and inform a t i o n a l( o rder processing and re p l e n i s h-

ment) flows that are associated

with the spare parts distributionactivities that link manufacturers

and dealers in the aforementioned

countries. We also investigatem a n u f a c t u rers’ and dealers’

strategies for positioning them-selves on the market. We study

current logistics organisations with

a view towards appreciating howthese strategies and organisations

have evolved, and also in order to

analyse the present and future role that is being played by the

Block Exemption Regulation in

auto-motive spare parts distribu-tion systems.

Our first step was to examine thecharacteristics of the market:

actors’ positions, specific products,

logistical constraints and organisa-

tional re s o u rces (e.g. networks,

warehouses). By meeting with the

m a r k e t ’s main protagonists, we

could validate earlier research andidentify flows clearly.

We then established how European

constraints, especially Block

Exemption Regulation 1475/95,

could influence future develop-

ments.

THE EUROPEAN AUTOMOTIVESPARE PART MARKET

ACTORS

We interviewed car manufacturers,

spare parts suppliers, non-indepen-

dent dealerships and national inde-

pendent repair chains associations

in an eff o rt to ascertain how

the non-independent after sales

spare parts market functions. The

present report does not delve into

the role of "original" spare parts

suppliers.

We observed that dealers’ turnover

and profits breakdown as follows:

➢ Cars: 70% of all turnover, 50% of

all profits

➢ Spare parts: 30% of all turnover,

50% of all profits

For several years now, the European automotive after sales market

has been going through widespread change as a result of the many

mergers that have arisen in this sector. Existing networks have been

evolving, moving towards an ever-greater degree of concentration.

In the year 2002, the Block Exemption Regulation is due to expire, and

this should lead to the distribution market being opened up to

independent networks. The present study analyses the state of this

market, as well as the major European car manufacturers’ strategies for

coping with such economic changes.

The Evolution of theEuropean AutomotiveSpare Parts DistributionMarket

7 0Supply Chain Fo r u m An International Journal N°1 - 2000 w w w. s u p p l y c h a i n - f o r u m . c o m

A study conducted by:

Jolanda Bijl,Hélène Mordret,Bruno Multrier,

Stephanie Nieuwhuys,Nicolas Pitot

Students at the ISLI in Bordeaux…

… supervisors:

Sébastien GannacEuropean Business Manager

EXEL Automotive

Simon HobbsDirector and General Manager

EXEL Automotive

Mike SummersVice-President EXEL Automotive

Hence the strategic importanceof the after sales market. Moreover,dealers' turnover involve thefollowing categories of parts: ➢ Manufacturer parts: 16-18% of allturnover➢ Supplier parts: 60% of all turnover➢ Public parts: 20-22% of all turnoverAs such, controlling distributionflows continues to be an issue ofstrategic importance.1

Furthermore, two types of behaviour were detected. Some customers would rather trade withdealers, either because of the professional standards of the maintenance services they provide(70%), or else due to the high quali-ty service and good relationshipsthat they maintain with their clients(30%). On the other hand, somecustomers prefer the independentnetworks because of their lowerprices (60%), high quality service(20%), and proximity (20%).

FLOWS

The distribution of automotivespare parts amongst major manufacturers, distribution centresand car dealers revolves around a certain number of physical (materials) and informational (com-munication) flows that enableactors to source:➢ the right parts: spare parts havingincreasingly become an integralpart of vehicle modules, ➢ in the right place: physical spareparts flows from manufacturers to dealers usually transit via national and/or regional distribu-tion centres, or else via large dealerships - especially since therehas been a decrease in the numberof dealers who receive direct deliveries from manufacturers or from national spare parts distribution centres (dealers seemto focus on a regional tier), ➢ at the right time: a distinction isgenerally made between urgentdeliveries and replenishment ope-rations: urgent orders are delivered

within 24 hours, whereas stockorders can take up to a week. Infact, for a few spare parts, leadtimes can sometimes be as long asa few weeks. However, this is sel-dom the case.

THE MARKET

The main objective of the automoti-ve sector is to lower its costs. This can be achieved through an optimisation of both of the aforementioned flows.

A schedule is made for each dealer,with a view towards reducingstocks to a minimum. The way inwhich this is accomplished differsfrom one manufacturer to the other,but we have noted that actors ten-ded to try to improve their distri-bution systems by using and/or bydeveloping advanced information systems.

These systems require a large investment - but they offer significant advantages (economies ofscale, lower stock levels, higher pro-fits, increasingly reliable deliveries,synchronisation of the supply chainand greater customer satisfaction).

Germany is the top automotivemarket in Europe, representing a20% share of the total E.U. market(Figure 1). This is followed by Italy(15%), the UK (13%), Spain (8%) and Benelux (5%). No other national market owns a share thatexceeds 4 % of the European total.

Note that the overall Europeanautomotive market has been in agrowth phase for more than 3 yearsrunning (figure 2).

The German group VAG is Europeanleader in vehicle sales: itsVolkswagen, Audi, Seat and Skodamakes accounting for a 22 % marketshare. VAG’s main competitors arethe French groups Renault-Nissan(15.5%), and PSA (13%).

A breakdown of the spare partsmarket (figure 3, see next page)shows Germany’s clear lead overthe other countries (45% marketshare), followed by France (27%),Benelux (19%) and Spain (9%).

71Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

1998Othera22%

Poland4%

Benelux5%

Spain 8%

France 13%

U.K13%

Italy15%

Germany20%

45000

40000

35000

30000

25000

20000

15000

10000

5000

0Germany France Spain Benelux

Thousands

1998

Cars Per Country

Source : L'argus de L'Automotive 10-99

1996

1997

1998

figure 1 : European Automotive Stock per Country

figure 2 : Evolution of the European Automotive stock

1. M. Boulet Desbareaux : Marketing Director.Opel France

- The German automotive spareparts market (figure 4) is carmartedby the following traits: The independent dealer network is lessdeveloped than in other countries.Manufacturer outlets continue to have a strong market position. For this reason, distribution is manufacturer-oriented. 50 % of allcar owners insist on original partsthat are sold by manufacturer outlets. In addition, the presence ofa large number of small dealersthroughout all of Germany is noteworthy, as is the fact that the country’s 12 largest cities each have their own independent distribution network.

- In the French spare parts market(figure 5), there is a 50/50 break-down between independent repairchains and manufacturer outlets.The 3 PL market is dominated bythree main actors: TAT, TNT andCalberson.

- In the Benelux (figure 6), spareparts distribution tends to bemanufacturer-oriented, though to alesser degree than in Germany. The3PL market is dominated by twoactors, who operate independentlyfrom one another, despite sharingthe same name: Parts ExpressBelgium, and Parts ExpressNetherlands (Van Duuren PartsDistribution). Their prices are only60 % of their nearest competitors’.

- The average customer profile inthe Spanish spare parts market isthe exact opposite of what it is inGermany. There are relatively fewmanufacturer outlets here, and theindependent network is quite

strong. Spain’s distribution net-work is dominated by independentdealers. In addition, it should benoted that the country is often a preferred destination for new production and distribution sites(figure 7).

In a nutshell, countries in NorthernEurope (Germany and Benelux)tend to have a more manufacturer-oriented distribution network;France’s network is evenly dividedbetween manufacturers and inde-pendent distributors; and in Spain,the market is dominated by inde-pendents.

THE DISTRIBUTION ORGANISATION OF THREEMANUFACTURERS

VOLKSWAGEN2

Since 1999, Volkswagen has beenunder pressure from fierce compe-tition. This was the year whenPeugeot's German sales increasedby 18 % (reflecting the success ofits Peugeot 206), at the expense ofVolkswagen’s domestic marketshare.

The VW group’s spare parts distri-bution network is supplied by specialised parts manufacturers

72Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

28,17

7,75

30,48

10,96

6,42

35%

30

25

20

15

10

5

1998

0Renault-Nissan PSA VAG Ford Opel-Seeb

Source : L'argusde L'Automotive 10-99

figure 4 : The leading automotive groups in France

figure 5 : The leading automotive groups in Germany

12,01

18,35

13,8612,93 12,77

199820

15

10

5

0VAG Ford Renault-Nissan PSA Opel-Saab

%

Source : L'argus de L'Automotive 10-99

figure 6 : The leading automotive groups in Benelux

14,43

10,52

28,23

12,98

8,76

30%

25

20

15

10

5

0VAG Opel-Seeb Ford Mercedes Renault-Nissan

Germany

Market:15.47 Billion

France

Market:9,23 Billion

Spain Benelux

Market:3,20 Billion

Market:6,60 Billion

Manufacturer Network

Source : GVA 1998 Source : FIEV.1998

Independent Network

Source : SFRNAUTO. 1998 Source : Forderman.1998

figure 3 : Spare parts market

(Volkswagen only produces bodyparts), and is comprised of sevenwarehouses spread across Germany- the latest being located in Kassel.

This central warehouse has an areaof 226,000 m2, and can hold 75,000of the 220,000 spare parts that thegroup offers. 60 % of its stock system has been automated. Theparts division follows an ABC pattern: the 15,000 A parts rotatevery rapidly (“fast movers”), andaccount for 80% of all sales. The Bparts rotate at a moderately rapidpace, and the C parts are “slowmovers”. Parts are stocked by refe-rence number. 120 wagonloads (60%) and 80 truckloads (40%) leavefor destinations all across the worldeach and every day of the year.

Since September 1999, Volkswagenhas been using a SAP software thathad been implemented with thehelp of Andersen Consulting. Stocklevels are controlled by a conti-nuous inventory system.

The clients in Europe to whomETZ Kassel makes deliveries areVW importers, the ten EuroWarehouses in Germany, and dea-lers in the Southern part of EasternGermany.

The German Euro Warehouses aremanaged by different 3LP’s - whoare free to select the transport providers that will be making the deliveries to Volkswagen’s 3,600 Audi dealers in Germany.Volkswagen organises and pays thetransport of spare parts to interna-tional destinations (VW importers). However, this spare parts distribu-tion network is fully co-ordinatedby an in-house SBU, VolkswagenTransport (ETZ ErsatzteilenTransport Zentrum), located inKassel (figure 8).

At present, "Rudolph Automotive"is responsible for the transport ofspare parts that are intended forthe Benelux and French markets.Transport to dealers in France isorganised by "Sernam" and "TAT";for dealers in the Benelux, it is organised by "Parts Express", a firmrelated to Volkswagen Dieteren andto PON Nederland. Orders for Spanish dealers are carried by "Bidoasoa”, which has adouble task: it delivers parts to thedomestic SEAT importer; andreturns carrying loads of theVolkswagen Polo parts that will bestocked in Germany for global distribution.

The dealers communicate with oneanother, and with the importers,via highly compatible national EDI systems.

VAG France’s spare parts (figure 9,see next page) are shipped fromKassel, and dispatched to VAGFrance, via Rudolph Automotive.From there, Sernam and TAT deliverparts to the dealers and to a num-ber of agents. Agents are also sup-plied by dealers. VAG France holdsa stock of 8 days. For weekly spareparts orders that are receivedduring week A, deliveries occurduring week B. Rush orders aredelivered at D+1 before 8.30 am.Information flows via the EDI system.

73Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

VW Importers Euro Warehouses Dealers

Order Type Stock Rush Stock Rush Stock and Rush

Means of Rail Air/road Rail Air/road Roadtransport

Frequency Weekly Daily Weekly Daily Daily

Lead Time As soon as < 24 hours As soon as < 12 hours < 12 hourswagon is wagon isloaded, it is loaded, it isdispatched dispatched

Cut off time - 6.30pm 6.30pm 6.30pm 6.30pm

21,66 20,99

11,4510,25

17,07

% 25

20

15

10

5

0VAG PSA Renault-Nissan Ford Opel-Saab

figure 7 : The leading automotive groups in Spain

2. Source: VW Transport Kassel: Mr Dietz,General Manager; Mr Rümelin; Mr Beckmann,Spare Parts distribution manager "Eastern"Germany, Mr Mueller, Strategic Logistics andRetail Manager; 2 March 2000

Rodolph Automotive Bidoasoa

Volkswagen TransporKassel

Pon NL D'ieteren B VAG F SeatSP

PartsExpress NL

PartsExpress B

SERNAM& TAT

Source : Volkswagen Kassel

Dealer Dealer Dealer Dealer

Figure 8 : VAG’s European Transport organisation

GENERAL MOTORS

GM Europe’s organisation is different from the other manufactu-rers’ (figure 10), in that the Group maintains on-site inventories ofspare parts wherever they aremanufactured (i.e., inside of the carplants themselves). GM Europe hasfive main European centres: two in Germany, one in Spain, one in theUK, and one in Sweden. It has nomanufacturing facilities in Franceand Italy, and has installed distribution centres in these twocountries. These two centres arereplenished via the five aforemen-tioned centres, and only storethose parts that are in greatestdemand.

TNT Logistics took over the GMEuro Express contract from UPS inNovember 1996 (figure 11).Orders are prepared in the following manner. GM created itsown bar codes, which contain all ofthe information that is necessaryfor order processing, such as the GM order number, the clientnumber, and the delivery number.TNT scans these numbers inside ofthe GM warehouses and takes careof the picking order. TNT Logisticsthen collects the parts from thevarious GM warehouses: OpelRüsselsheim (Germany), OpelBochum (Germany), Opel Zaragoza(Spain), Vauxhall Luton (UK) andSaab Sweden (Stockholm).

For express deliveries, all parts arecollected at night and taken to theLiege airport in Belgium. Parts forthe Benelux countries and for

Western Germany are transportedby road. Parts that are destined fordistinct destinations are carried by air/road. The average journeyrequires 24 hours, and the actualservice rate reaches 92 %, even though the company has established a performance target of98%. The number of annual ship-ments totalled 235,743 in 1999. This relatively low service rate is due tothe reorganisation of TNT Italy last year, and to the performances of the Italian information and distribution systems.

Thanks to an Internet-based tracingand tracking apparatus (the Delphisystem), clients are able to trace their order by entering the consignment note number. This system indicates the expected delivery date, time, location (country of origin and destination),order status (early, late or overdue)

and the reasons why orders are overdue. The customer service has been much more effective since this system was setup. At TNT’s premises in Rüsselsheim,where the GM Euro Express co-ordination centre is located,data is transmitted to a (more limited) internal TNT Lotus Notes-based information system.General Motors is the world leading car manufacturer. Opel and Saab are its flag bearers inEurope.

OPEL3

Opel’s, spare parts distributionorganisation’s objectives are tocreate a Dealer Parts Replenish-ment system (like Saab’s), establisha virtual warehouse that links up itsdealers, and to only have to dealwith a single type of order, i.e. withall of its orders revolving around replenishment operations.

The general policy is that each dealer must have a minimumof 2,000, and preferably 4,000 references on stock. Furthermore,Opel produces 40 % of its own spareparts, with specialised parts manu-facturers making the other 60%.

Opel's internal stock managementsystem is called Catalyst. All of theother systems have been develo-ped by EDS.

Opel Europe

Opel Europe has four central warehouses on its car productionsites in Spain, England, and at bothsites in Germany.

74Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

The two German warehouses havea total floor space of 450,000 m2. Inaddition, there are a number ofexternalised warehouses. The totalnumber of stocked references is250,000 and 150,000 lines are prepa-red daily for delivery to dealers.Some 1.200 employees work inthese warehouses.

The total warehouse floor space inSpain (Zaragoza) is 48,000m2. Inaddition, 150,000 m2 floor space has been externalised. The total number of stocked references is48,000, and 18,000 lines are prepa-red daily for delivery to dealers.Some 180 employees work in thesewarehouses.

The Vauxhall warehouse at Luton(UK) has a floor space of 250,000m2. It is fully owned and managedby Opel. There are 110,000 references on stock, and 30,000lines are prepared daily for deliveryto dealers. No details were available for theSaab warehouse in Sweden.The central warehouses deliver tothree types of clients: dealers,other warehouses; and distributioncentres in France and Italy. Opeldistinguishes between VOR, Rushand Stock orders.

Opel’s 3PL providers are:

Distribution to dealersin the Benelux

One example of Opel’s system is itscentral warehouse in Rüsselsheim,which makes daily deliveries to theBenelux dealer network. Dealersforward their orders before 5 pm to the Opel DC. At 7 pm, the parts are loaded by Parts Express for delivery the next morning. Theorders are collected and labelled byOpel pickers. With respect to the Internationalplatforms, some of the spare parts that are to be dispatched by the five central warehouses are prepared for dealer network distribution on platforms that arelocated in France and in Italy. Note

the closure of DC's in Ireland,Norway, Denmark, Holland,Belgium and Portugal - one of Opel's strategy is now that every new DCshould be managed by a third partylogistics provider. Poland was oneof the first countries to implementthis decision.

95% of all parts are supplied by thefour central warehouses. Threekinds of parts receive a specialtreatment:➢ Homogeneous parts are stockedright away➢ Heterogeneous parts are proces-sed before being stocked➢ Rush parts (500 lines/day) arecross-docked

There are about 8 weeks of stock in the warehouse, implying thatstocks rotate 6.5 times annually.There are a total of 30,000 references on stock: 14,000 smallparts; 1,000 accessories and paintitems; and 8,000 medium size andlarge parts. All in all, 1,800,000parts are stocked, 105,000 of whichare managed by Breger Transport.

The objective is to reduce the number of references by stockingonly the critical 20 % that accountfor 80 % of all sales.

Each and every day, 12,000 lines areprepared for delivery to dealers.The goal is to break this down into25 % urgent orders and 75 % stockorders. Currently, productivityamounts to 13.4 lines/hour/man.The target is 15 lines/hour/man.

75Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

VOR Rush Stock

Benelux TNT/Parts Parts PartsExpress Express Express

France TAT TAT Calberson(warehousing)

Breger(transport)

Spain TNT TNT Azcar/Gerposa

SaabSweden

VauxhallUK

Rùsselsheim D

TNTGM euro-express

Coordination Centre

ZaragozaSP

Opel BochumD

Liège B UK

Scandinavia

AU

I

FBenelux

SP

to Madrid orBarcelona via Paris

hubBxl.

Arnhem

Bx, Toulouse, Lyon, Paris

✈✈

Source : TNT Ruesselsheim (D)

figure 11 : GM Euro express

VOR Rush Stock

Percentage of all order 2 % 8 % 90 %

Order cut-off time 2 p.m. 2 p.m. 8 p.m.

Lead time 18 hours D + 1 D + 3

3. Source: Mr Pujot, logistics Manager OpelSpain; Mr Maraboti, Spare Parts StrategyManager Opel France; Mr Pignard, Spare PartsOperations Manager Opel France

F means factory, inasmuch as these four warehouse are located in the immediate vicinityof a car plant - whereas the other two only have a warehousing activity.

SAAB4

Saab is 50% owned by GeneralMotors, and shares many businesspractises with it. However, despitebeing part of the GM group, Saabdoes not have the same spare partsreplenishment system as Opeldoes. It is a prime example of amanufacturer having implementeda virtual order system on behalf of its dealers. Saab, aided by the Cap Gemini ICT consultinggroup, has developed a customised solution for its dealer parts replenishment system. The systemthat was hosen had to be able to respond reliably and rapidly to large scale globalinformation flows. Web technologywas selected as a basis for this newsystem.

Thanks to this infrastructure, Saabhas at its disposal a great deal ofcentralised information concerningthe parts being supplied to a particular dealer; the dealer’s current inventory (for any type ofpart); and its daily sales of any ofthe parts on its books. The importance of an intelligentparts management system such asthe ‘Dealer Parts Replenishment’(DPR) package is that it actuallyreduces total inventories, whilstsimultaneously increasing the probability that a part which is indemand is actually in stock.

In this way, the replenishment isbeing pulled to the dealer.Furthermore, the DPR system isavailable in local languages, anddoes not cost the dealer anything. The expected benefits of this newDPR system are threefold:➢ reputation for improved custo-mer service ➢ greater share of the after salesmarket➢ Improved inventory control andforecasting capacities for partsmanufacturers

RENAULT EUROPE

This French marque has its administrative offices at BoulogneBillancourt (near Paris). The recentmerger with Nissan has howeverpartially altered Renault’s organisa-tion. (figure 12).

Benelux is a good example of thegroup’s new shape (figure 13).

The Renault spare parts distribu-tion centre for the Benelux countries is located near Brussels(at Mechelen). Annual salesamount to 18 million. There is atotal warehouse area of 16,900 m2.Until a few months ago, the stocking area in the warehouse wasonly 7,500 m2, and this was far toosmall. For this reason, a new6.900m2 platform was created near the existing warehouse. The platform is used for stockingengines, gearboxes and windows;and also for order packing, rackingand shipment. This has enabled thewarehouse manager to use the former picking area as a stockingarea, thus increasing the total stocking area to 10,000 m2. A total of 46,000 references (out of 85,000) are stored in the Mechelen warehouse.

Renault parts are supplied byvarious Renault warehouses inFrance: Cergy Pontoise for smallparts, Flins for larger parts, Douaifor paints etc. Accessories aremanufactured and supplied byBelgian partners such as Philips,Brink, Bosch and Pioneer.

Three kinds of replenishment systems exist within the warehouse:➢ Tight flows: ordered weekly bySIG, a system that is to be replacedby a more modern one in the verynear future➢ Supplier 0-0-1: ordered every 3weeks by SIG (fast movers)➢ Supplier 0-0-2 :manually orderedevery 4 weeks (slow movers)

Two types of unsold stock aremanaged: "dead' stocks (parts thathave been in stock for two years);and the surplus stock of parts thathave been in stock for between one

76Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

and two years. These unsold spareparts are offered for re-sale inFrance - or else are destroyed if theFrench market is not interested inthem.

The central warehouse in Mechelenmakes direct deliveries to theBelgian clients, as well as a mixtureof direct and indirect deliveries toits Dutch clients. A distinction canbe made between replenishmentorders and urgent orders.

Mechelen has a limited number ofreferences on stock, and RenaultFrance cannot always deliver theparts that are being requested. Thismay account for the relatively lowservice level.

14,500 lines are prepared for dailyshipment. After 1 p.m., replenish-ment orders are transported in rollcages from Mechelen to a platform9km away, near the Zenne River. Onthis platform, orders are stocked in categories ranging from A to F:small parts in plastic boxes and larger ones on pallets.

Order picking is organised by zoneroutings. Each contains enoughparts for 3 to 6 truckloads.

The parts leave the platform late inthe evening for night-time deliveryin Belgium, or for delivery in theNetherlands early the next mor-ning, by noon at the lastest. Belgiandealers are delivered by Cat, andDutch 3PL in part by Parts Express,and in part by Gefco. This latterfirm only makes deliveries to itsclients via platforms, whereas Catand Parts Express make direct deli-veries.

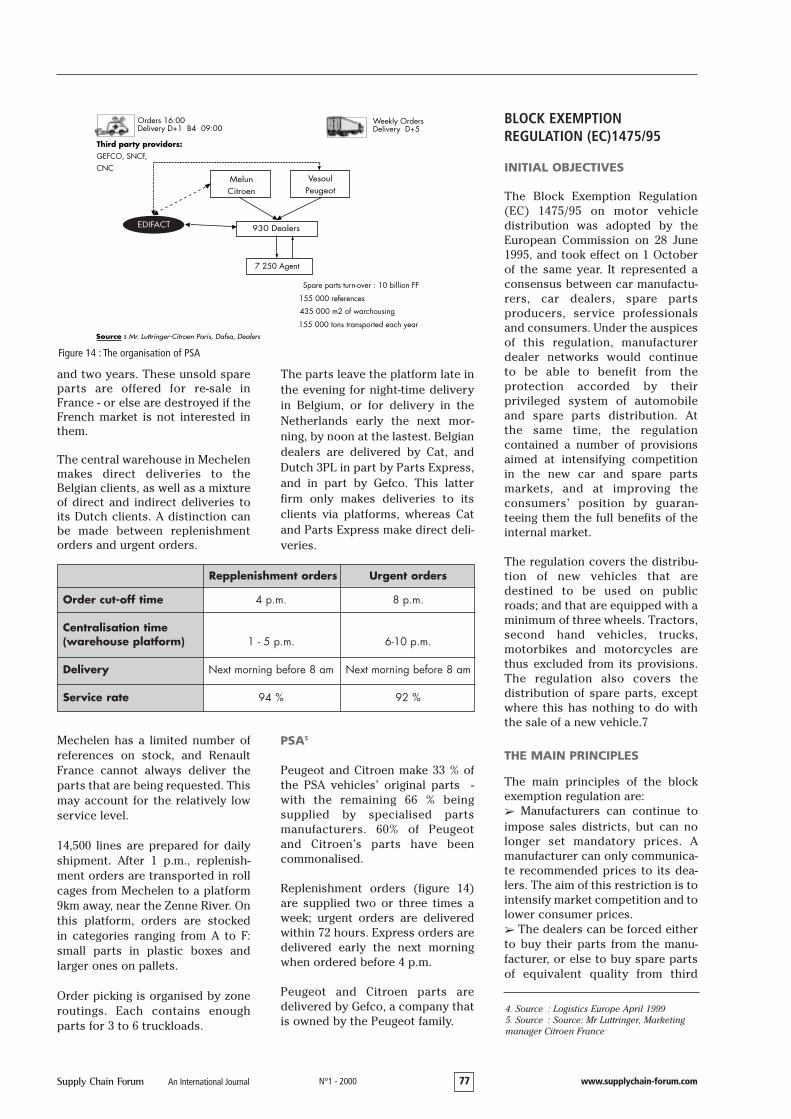

PSA5

Peugeot and Citroen make 33 % ofthe PSA vehicles’ original parts -with the remaining 66 % being supplied by specialised partsmanufacturers. 60% of Peugeot and Citroen’s parts have been commonalised.

Replenishment orders (figure 14)are supplied two or three times aweek; urgent orders are deliveredwithin 72 hours. Express orders aredelivered early the next morningwhen ordered before 4 p.m.

Peugeot and Citroen parts are delivered by Gefco, a company thatis owned by the Peugeot family.

BLOCK EXEMPTION REGULATION (EC)1475/95

INITIAL OBJECTIVES

The Block Exemption Regulation(EC) 1475/95 on motor vehicle distribution was adopted by theEuropean Commission on 28 June1995, and took effect on 1 Octoberof the same year. It represented aconsensus between car manufactu-rers, car dealers, spare parts producers, service professionalsand consumers. Under the auspicesof this regulation, manufacturerdealer networks would continue to be able to benefit from the protection accorded by their privileged system of automobileand spare parts distribution. At the same time, the regulation contained a number of provisionsaimed at intensifying competitionin the new car and spare parts markets, and at improving theconsumers’ position by guaran-teeing them the full benefits of theinternal market.

The regulation covers the distribu-tion of new vehicles that are destined to be used on publicroads; and that are equipped with aminimum of three wheels. Tractors,second hand vehicles, trucks,motorbikes and motorcycles arethus excluded from its provisions.The regulation also covers the distribution of spare parts, exceptwhere this has nothing to do withthe sale of a new vehicle.7

THE MAIN PRINCIPLES

The main principles of the blockexemption regulation are:➢ Manufacturers can continue toimpose sales districts, but can nolonger set mandatory prices. Amanufacturer can only communica-te recommended prices to its dea-lers. The aim of this restriction is tointensify market competition and tolower consumer prices.➢ The dealers can be forced eitherto buy their parts from the manu-facturer, or else to buy spare partsof equivalent quality from third

77Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

Orders 16:00Delivery D+1 B4 09:00

Weekly OrdersDelivery D+5

Third party providors:GEFCO, SNCF,CNC

MelunCitroen

VesoulPeugeot

930 Dealers

7 250 Agent

Spare parts turn-over : 10 billion FF

155 000 references

435 000 m2 of warchousing

155 000 tons transported each yearSource : Mr. Luttringer-Citroen Paris, Dafsa, Dealers

EDIFACT

Figure 14 : The organisation of PSA

4. Source : Logistics Europe April 19995. Source : Source: Mr Luttringer, Marketingmanager Citroen France

Delivery Next morning before 8 am Next morning before 8 am

Service rate 94 % 92 %

parties at terms set by the manu-

facturers - as long as these condi-

tions are not in contradiction with

the regulation’s article 85(3). For

example, a manufacturer can insist

on the use of the parts that it has

supplied in instances involving the

indemnities that have to be made

on a vehicle that is still under

warranty, as this is not in contra-

diction with article 85/3. The aim is

to ensure the quality and safety of

any product that the manufacturer

supplies.

➢ A rticle N°123/85 permits themanufacturer to prohibit authori-

sed dealers from supplyingcontract goods or correspondinggoods to 'resellers' who are not partof the distribution network. In this

w a y, the Block ExemptionRegulation acknowledges themanufacturer's interest in protec-ting its restrictive distribution sys-tem.

➢ The dealers are authorised to selld i ff e rent brands when these areclearly being stored and managedautonomously from one another

(the idea being to avoid any confu-sion of the consumer). This impliesthat managers and staff memberswill have to possess sufficient tech-nical knowledge of the diff e re n t

brands that are being sold. Wherethe decision has been taken tocreate a multi-brand store, the dea-ler does not need any authorisationfrom the manufacturer.

THE FUTURE

The regulation is due to expire

on September, 30 2002. The Comm-ission decided to exclude the auto-motive sector from the review thatit carried out in 1997. It sent outquestionnaires to all of the parties

that are involved in the motorvehicle distribution trade, (consu-mer associations, dealers, indepen-dent import e r / re p a i rers, indepen-dent importers, spare part manu-

f a c t u rers, firms that sell via theI n t e rnet and all motor vehiclemanufacturers).7

The findings of this assessment will

be published by December 2000 inan ad hoc report that will be compi-led by a consultative body, as indica-ted in the regulation’s article n° 11.

ONE MANUFACTURER’SREACTION TO THE REGULATION: MOTRIO

A good example of the way in which

manufacturers can adapt to thesenew economic conditions is Motrio,

the entity that Renault created inorder to regain clients that it had

lost to independent dealers andrepair agents. Renault’s multi-brand

policy is embedded in this concept– a modus operandi that has never-

theless gone through a number of

major changes since 1998.

In two years, Motrio’s sales haveskyrocketed, jumping from 65 mil-

lion francs in 1998 to an estimated150 MF in 2000. The entity’s best

sellers are its brake systems (32 %),

filters (25 %) and pre-heating units.Its clients are repair agents (69 %),

garages (21 %), and primary outlets(10 %).

Motrio lists 18 to 21 product fami-

lies (1038 references). Its current

priorities are to enlarge its assort-ment, and to develop trading rela-

tions with 85 % of Europe’s largestcar companies (at present, it trades

with 70 % of this group).I n t e rnational expansion has also

been rapid: in 1998, Motrio only tra-ded in France and Italy; in 1999,

Germany was added to this list; and

in 2000, it began trading in Portugaland Spain as well.

In a highly competitive enviro n-

ment, the spare parts market wouldappear to be vital for dealers – the

rewards that it offers can be sub-

stantial. Car manufacturers havethus been seeking to establish ever-

closer ties to their customers; anexample being the fact that every

manufacturer has devised a multi-parts strategy enabling it to repair

competitors’ vehicles.

THOUGHTS ON THE NEW EUROPEAN AFTER SALES AUTOMOTIVE MARKET

After analysing Block Exemption

Regulation 1475/95’s legalities, weasked experts what they thought

about the regulation’s impact on

the distribution of spare parts.

Some remain indiff e rent to theBlock Exemption. Their focus is on

present policy, i.e., the ever increa-sing number of regional logisticcentres that are being set up. As aresult, they concentrate on the loo-

sening of ties between the manufac-turers’ distribution centre and theindividual dealers.

Other experts predict that spareparts distribution regulations maybecome more liberalised - but that

there will never be a completelyderegulated market.

We also met experts who believe

that the Block Exemption will havea more significant impact on tradethan on logistics. Some manufactu-rers have already planned to chan-

ge their strategies in the near futu-re so as to incorporate this pheno-menon.

It would appear that deregulationwill indeed have a negative effecton manufacturers’ distribution net-works, and that independent distri-bution systems will expand as aresult. Certain OES’s are establi-shing alliances in an attempt toconsolidate their position; whilstm a n u f a c t u rers have been buyingindependent repair chains in orderto hold on to market share (e.g.,Ford, which bought Pit Stop andKwik Fit).

CONCLUSION

MARKET TRENDS

These examples illustrate thetrends that have affected the auto-motive industry’s behaviour for thepast few years. A wave of mergersthat is similar to the one that hasbrought manufacturers closer toge-ther (Daimler- C h ry s l e r, Renault-Nissan, GM-Saab, GM-Fiat, andFord-Volvo vehicles) has also takenplace in the automotive suppliersector. This could lead to an accele-ration of the trend towards multi-brand spare parts distribution.

In addition, distribution networkshave become increasingly concen-trated through the creation ofregional distribution platform swherein one actor controls the dis-tribution of vehicle and spare partsthroughout an entire region.

Figure 15 shows that 3PL organisa-tions have made the most progress

7 8Supply Chain Fo r u m An International Journal N°1 - 2000 w w w. s u p p l y c h a i n - f o r u m . c o m

in this direction. We have isolatedeach phase of the services thatthey provide, and highlighted theone that they are best at.

In light of the EuropeanCommission’s political actions,there is no doubt but there hasbeen an attempt to ensure fair com-petition between actors (this beingthe Article 86). After a decade ofstrict regulation between 1985 to1995, manufacturers should be pre-pared for market deregulationwhen it finally arrives (on 30September 2002, 7 years after theenactment of the Block ExemptionRegulation N° 1475/95, and 17 yearsafter the beginning of the process).The market’s main recent trendswould tend to indicate that theyare.

We also think that the BlockExemption Regulation’s initialobjectives have been supersededby changes in the economy; andthat they have become outdated.This opinion is based on our analy-

sis of the flows between manufactu-rers and their distribution network.Indeed, it would appear that within5 years, no more than four or fivegiant manufacturing groups willsurvive in the automotive industry.In a sense, economic reality, in andof itself, will have lead to the crea-tion of multi-brand outlets. TheEuropean Commission’s efforts toopen up the market will, to a cer-tain extent at least, have beenredundant.

OPTIMAL DISTRIBUTION FLOWS

In this highly competitive environ-ment, optimising spare parts distri-bution would appear to be an abso-lute necessity. This is an opportuni-ty for 3PL’s to propose a value-adding stock management servicethat can allow for an improved ser-vicing of manufacturer networks.The chart below (figure 16) visua-lises all of the services that a 3PLcould perform on behalf of a manu-facturer in the automotive aftersales rmarket.

For political reasons, dealers mightfind it difficult to allow a 3PL, oreven a manufacturer, to managestocks that they themselves own.For this reason, and in order tooptimise the distribution of spareparts, major investments will benecessary, revolving around the(re)purchase of dealer stocks.Moreover, this will allow 3PL’s tobuild a virtual warehouse, linkingdealers within a given region, with aview towards optimising each dea-ler’s stocks and floor space.

REFERENCES

Books :✓ “Mutations des stratégies logistiques enEurope”, SAMII Alexandre Kamyab,Nathan, 1996✓ “Western Europe’s component indus-try”, The Economist Intelligence Unit(IUT), 3Q 1998European Commission Reports :✓ Distribution Automobile CE, n°1475/95” published in the OfficialJournal, Explanatory Brochure,Commission of the EuropeanCommunities, 1995Specialised magazines :✓ Le Distributeur Automobile, N° 218✓ Auto Infos N°1095, p 37✓ Logistics Europe, April 1999✓ Stratégie Logistique, May-June 1999✓ Logistique et Management, ISLI, Oct.1999✓ La pièce de rechange, Oct-Nov 1999✓ L’argus de l’automobile, October 1998Research documents✓ “La logistique de distribution despièces de rechange automobiles”, Dafsa,1997✓ “EU Automotive Logistics”, MarketLineInternational, 1998International Newspapers✓ “Main manufacturers do not decreasetheir prices” and “Dreaming about chea-per cars is not realistic”, De Standaard;21 December 1999 (Belgium)✓ “TNT Logistics wins VW GroupWarehousing”, Contract Financial Times,10 May 2000Internethttp ://europe.eu.int/comm/dg04/aid/en/car.htm

79Supply Chain Forum An International Journal N°1 - 2000 www.supplychain-forum.com

VOR 18:00 hrsfor EuropeUrgent Orders 05:00Pativery D+1 B408:00 am

ReplenishmentOrders Day A B4Delivery DayBSCSD

Third party providers: Order preparationAbble to deliver at nightCustomised to car manufacturer brandsNoise reduction system

IntegratedIT System

European Dealers European AgentsCar manufacturer manages the stock

Nighteception

Figure 15 : Benchmarked Distribution Flows

Figure 16 : An Optimum Distribution Flow

6. L’Argus 11 October 19997. http://europa.eu.int/comm/dg04/aid/en/car.htm