38

The External Environment for Developing Countries December 2008 The World Bank Development Economics Prospects Group

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | osborn-stokes |

| View: | 218 times |

| Download: | 1 times |

The External Environment for Developing Countries

December 2008The World Bank

Development EconomicsProspects Group

A deep synchronous downturn for OECD countries in fourth quarter... growth GDP growth **, percentage

change, q/q saar

-6

-4

-2

0

2

4

2008-Q1 2008-Q2 2008-Q3 2008-Q4E

Source: World Bank and National Agencies ** Q4 JPMorgan.

Japan

Euro Area

United States

-10

-5

0

5

10

15

20

25

30

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08

...with developing-country production now in decline, led by China

industrial production percentage change, saar

Source: World Bank data.

China

Developing excl China

Developing

Industrial countries

0.9

2.8

-0.5

-4

-3

-2

-1

0

1

2

3

4

5

Q1-2008 Q2-2008 Q3-2008

Source: Department of Commerce and DECPG calculations.

U.S. Q3-GDP drops 0.5% on massiveretrenchment by the consumer

growth of real GDP, and contributions to growth in percentage points

Key indicators point to deepU.S. recession in fourth quarter

retail sales, mfgr IP % saar [L], change in employment [R]

-20

-15

-10

-5

0

5

10

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

-500

-400

-300

-200

-100

0

100

200

Source: Departments of Commerce and Labor; Federal Reserve.

Industrial production [L]

Retail sales [L]

Change in non-farm employment (3mma, ‘000) [R]

0

1

2

3

4

5

6

Aug-07 Nov-07 Feb-08 May-08 Aug-08 Nov-08

Source: Thomson/Datastream.

Fed cuts Funds target to 0.0-to 0.25% with heavy “flight to quality” underway

Fed Funds target- and effective rates; T-

note- 2yr, T-note 10 yr

Fed Funds Target

LIBOR 3 months

T-note 10-year

T-note 2-yr

2.4

-3.7

-1.8

-5

-4

-3

-2

-1

0

1

2

3

4

Q1-2008 Q2-2008 Q3-2008

Source: Japan Cabinet Office and DECPG calculations.

Japan GDP drops 1.8% in Q3 oncontinuing negative trade outcomes

growth of real GDP, and contributions to growth in percentage points

ConsumptionGovernmentInvestment

Stocks Net Exports

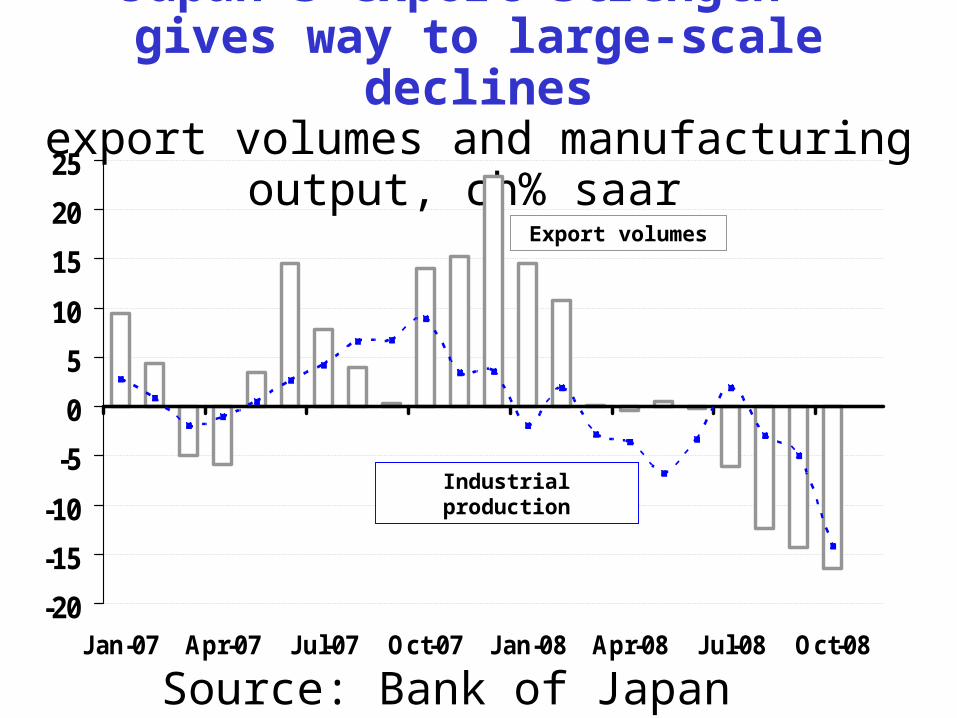

Japan’s export strength gives way to large-scale declines

export volumes and manufacturing output, ch% saar

-20

-15

-10

-5

0

5

10

15

20

25

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: Bank of Japan and Japan Cabinet Office.

Industrial production

Export volumes

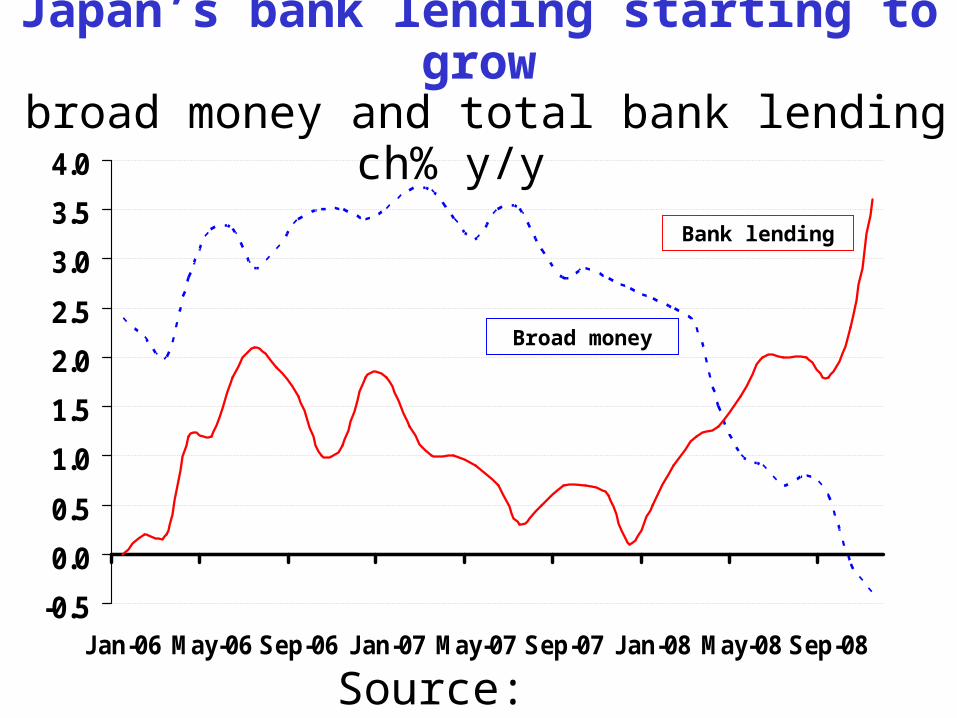

Japan’s bank lending starting to grow broad money and total bank lending ch

% y/y

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08

Source: Bank of Japan.

Bank lending

Broad money

2.7

-0.7 -0.8

-3

-2

-1

0

1

2

3

4

Q1-2008 Q2-2008 Q3-2008

Source: Eurostat and DECPG calculations.

Net exports pull Euro Area GDPfurther into recession in 3rd quarter

growth of real GDP, and contributions to growth in percentage points

Change in stocks GovernmentConsumptionInvestment Net Exports

German exports now in decline following sharp falloff in foreign orders

export volume ch% 3mma y/y [L] and

export orders, ch% saar [R]

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08-35

-28

-21

-14

-7

0

7

14

21

28

35

Source: Bundesbank-- Thomson/Datastream.

Export volume [L]

Export orders [R]

Inflation– an eventual “silver lining” for Europe?

HICP total ch% y/y [L], HICP-energy, ch% y/y [R]

0

1

2

3

4

Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08

-5

0

5

10

15

20

Source: Eurostat through Thomson/Datastream.

HICP-Total [L]

HICP-Energy [R]

Industrial production

Downturn in IP across OECD to dateas pronounced as in 2001 recession

industrial production, ch% (3m/3m saar)

-20

-16

-12

-8

-4

0

4

8

12

16

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Source: Thomson/Datastream, DECPG.

USA

Eurozone

Japan

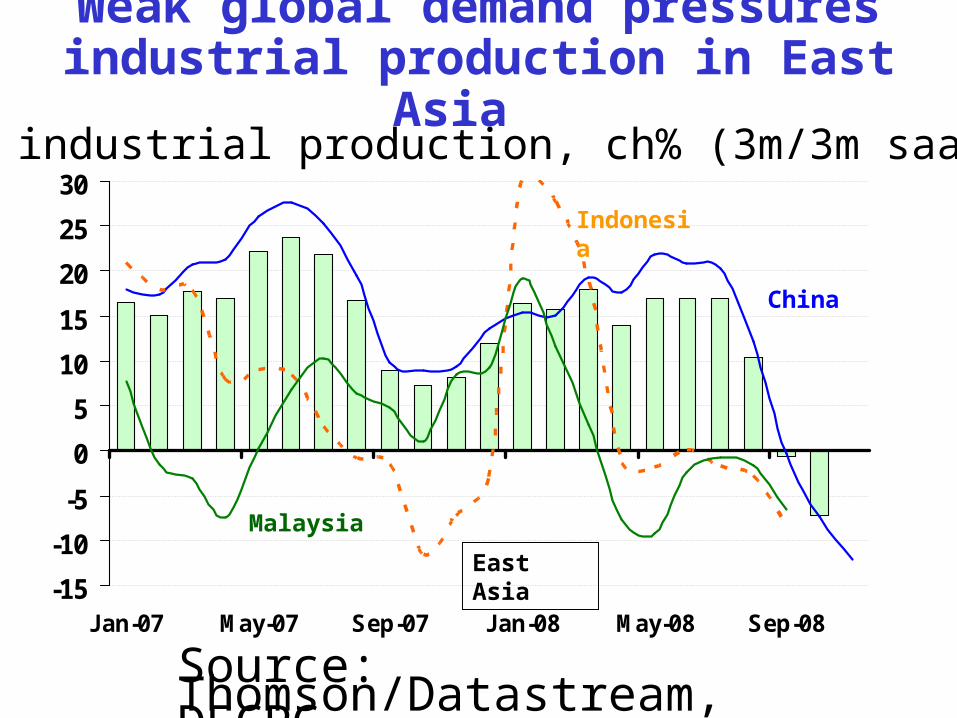

Weak global demand pressuresindustrial production in East Asia

-15

-10

-5

0

5

10

15

20

25

30

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08

Source: Thomson/Datastream, DECPG.

East Asia

China

industrial production, ch% (3m/3m saar)

Indonesia

Malaysia

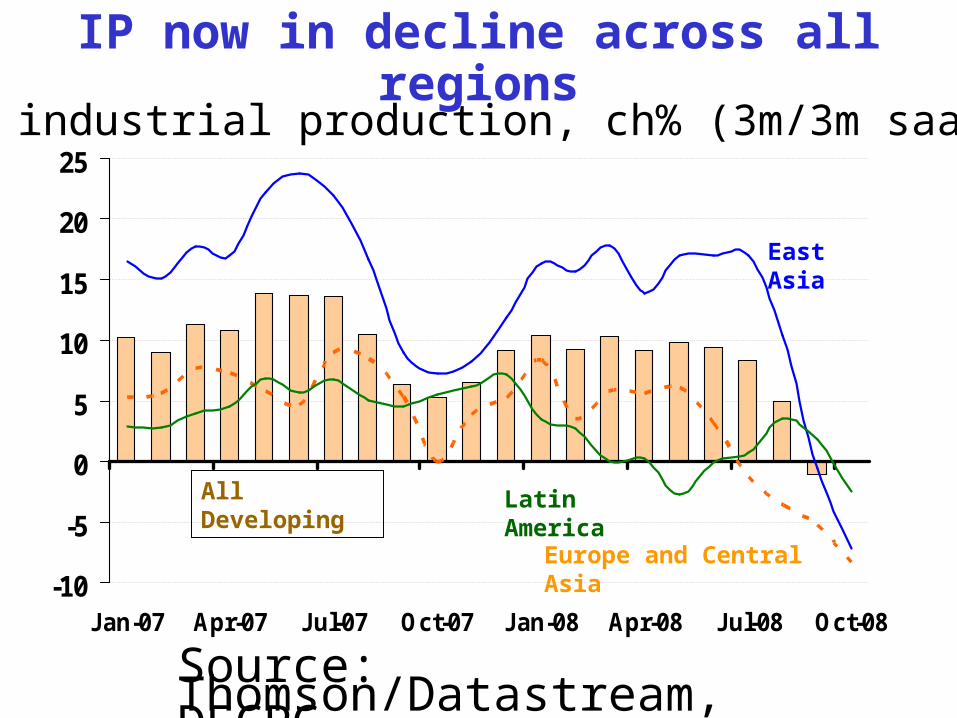

IP now in decline across all regions

-10

-5

0

5

10

15

20

25

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: Thomson/Datastream, DECPG.

All Developing

East Asia

industrial production, ch% (3m/3m saar)

Europe and Central Asia

Latin America

International trade

Key OECD imports compress as domestic demand falters

import volume: U.S, Japan, Germany and U.K. ch% 3mma y/y

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: National Agencies through Thomson/Datastream.

United States

Japan

Germany

U.K.

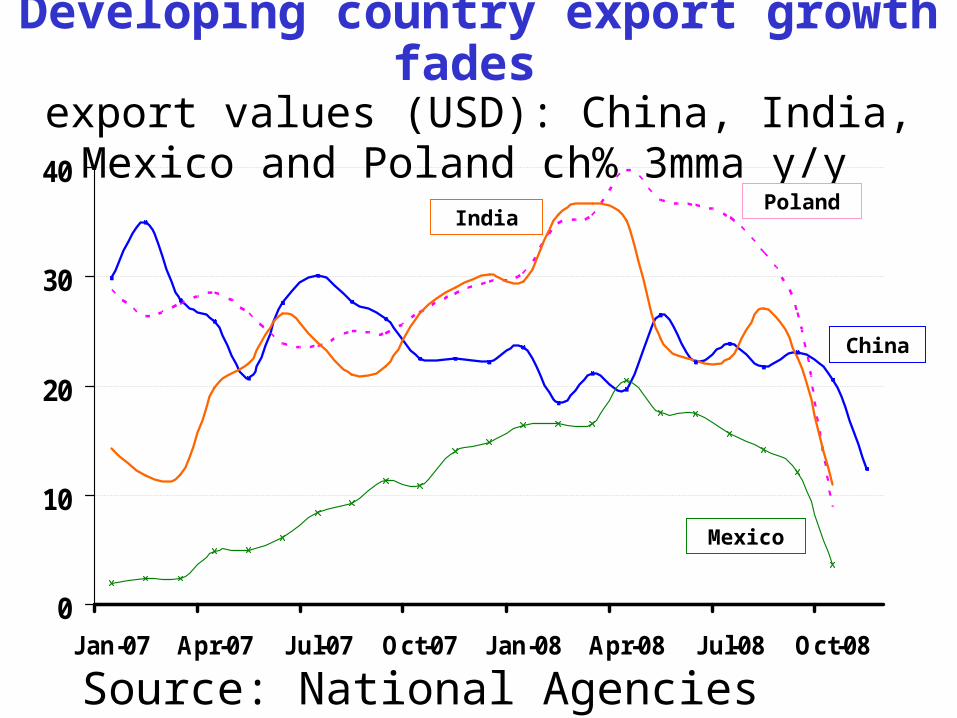

Developing country export growth fades export values (USD): China, India, Mexico

and Poland ch% 3mma y/y

0

10

20

30

40

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08

Source: National Agencies through Thomson/Datastream.

China

PolandIndia

Mexico

-250

-200

-150

-100

-50

0

50

100

Q1-2007 Q2-2007 Q3-2007 Q4-2007 Q1-2008 Q2-2008 Q3-2008

Source: Department of Commerce.

U.S. current balance improves slightlyin third quarter on better balance on non-

oil trade

Income

Services

Non-oilBOT

Oil balance

Transfers

Current account

Oil prices

Crude oil prices plunge back to 2004 levels on falling demand

20

40

60

80

100

120

140

160

Jan-04Jan-05

Jan-06Jan-07

Jan-08

$/bbl

World Bank Average

Source: Datastream and DECPG Commodities Group.

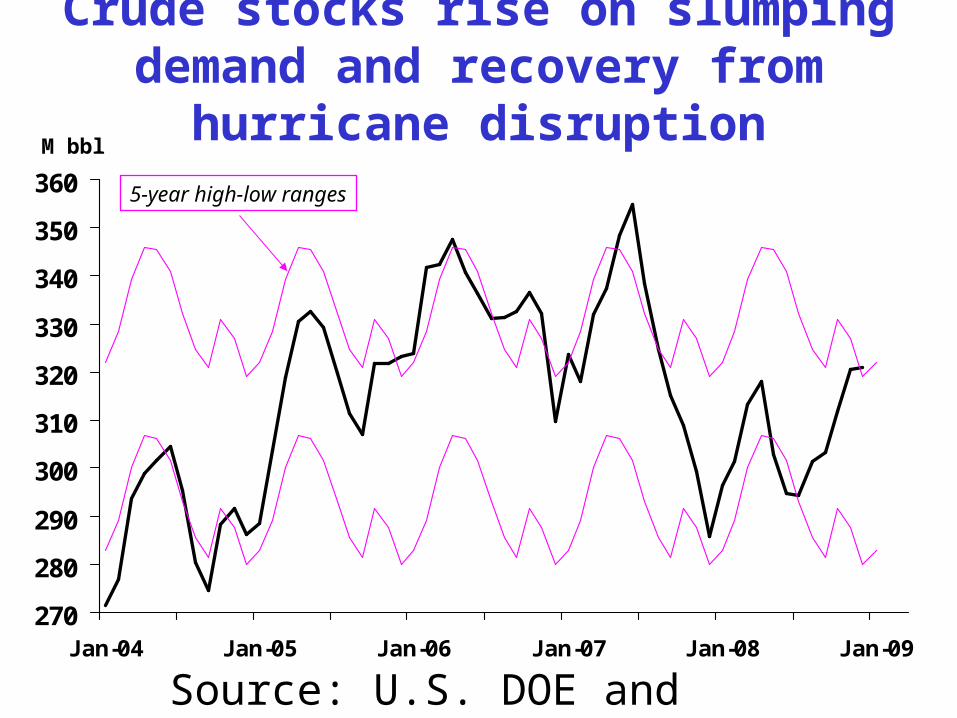

Crude stocks rise on slumping demand and recovery from hurricane disruption

270

280

290

300

310

320

330

340

350

360

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

M bbl

5-year high-low ranges

Source: U.S. DOE and DECPG Commodities Group.

WTI Futures Prices - NYMEX

40

50

60

70

80

90

100

110

120

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Dec 15

$/bbl

Monthly contract prices to Dec 2013* on select dates in 2008

Oct 31

Sep 30

Aug 29

Dec 5

Source: NYMEX and DECPG Commodities Group.

Non-oil commodity prices

100

150

200

250

300

350

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Grains

Fats & Oils

Other Food

Agriculture prices plummet on weak demand, falling oil costs and better

supply prospectsIndex 2000=100

Source: Datastream and DECPG Commodities Group.

Metals prices plunge on sharp decline in demand

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-05Jan-06

Jan-07Jan-08

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

Cu $/ton Ni $/ton

Copper

Nickel

Source: LME and DECPG Commodities Group.

Ocean freight rates sink on lack of demand and credit concerns

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-05 Jan-06 Jan-07 Jan-08

Baltic dry freight index

Source: Datastream and DECPG Commodities Group.

International Finance

Capital flows come to an effectivehalt over October and November

Source: DECPG Finance Team.

Gross capital flows to emerging markets

$ billion

H1 Q3 Total H1 Q3 Oct Nov YTD

Total 349 163 652 249 70 18 9 346

Bonds 107 20 146 58 9 0 0 67

Banks 156 101 312 146 60 18 9 232

Equity 86 42 194 45 2 0 0 47

Lat. America 69 54 156 57 13 3 1 73

Bonds 31 6 45 17 1 0 0 18

E. Europe 156 45 247 101 34 12 4 153

Bonds 50 5 64 32 8 0 0 40

Asia 93 47 188 64 14 2 2 81

Bonds 18 5 23 7 0.4 0 0 7

Others 31 16 61 27 9 1 2 39

2007 2008

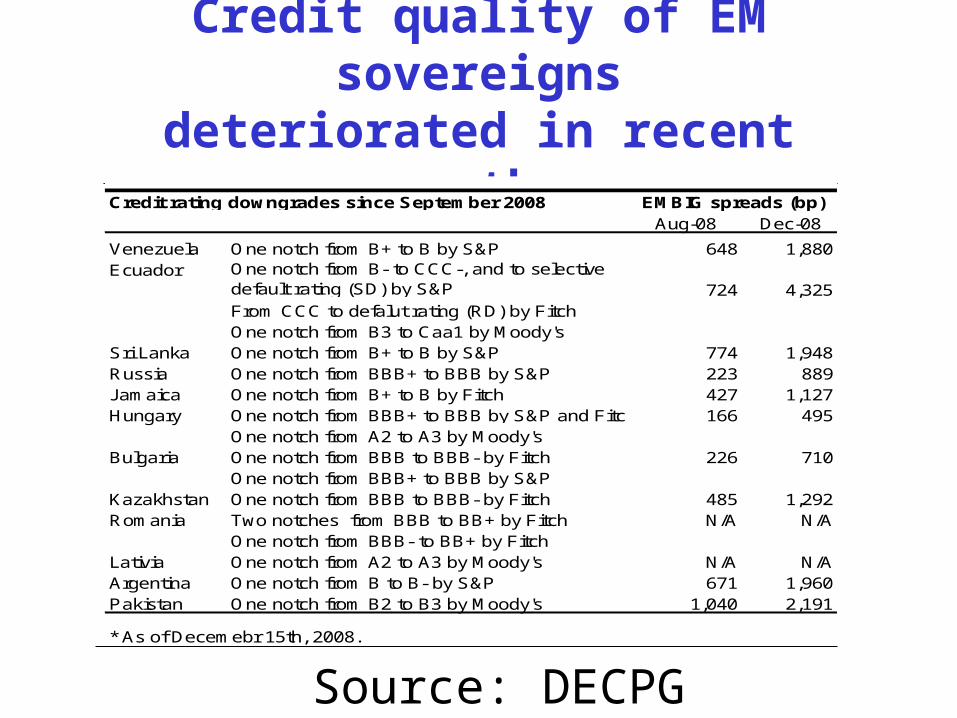

Credit quality of EM sovereignsdeteriorated in recent months

Source: DECPG Finance Team.

Credit rating downgrades since September 2008Aug-08 Dec-08

Venezuela One notch from B+ to B by S&P 648 1,880Ecuador One notch from B- to CCC-, and to selective

default rating (SD) by S&P 724 4,325From CCC to defalut rating (RD) by FitchOne notch from B3 to Caa1 by Moody's

Sri Lanka One notch from B+ to B by S&P 774 1,948Russia One notch from BBB+ to BBB by S&P 223 889Jamaica One notch from B+ to B by Fitch 427 1,127Hungary One notch from BBB+ to BBB by S&P and Fitch 166 495

One notch from A2 to A3 by Moody'sBulgaria One notch from BBB to BBB- by Fitch 226 710

One notch from BBB+ to BBB by S&P Kazakhstan One notch from BBB to BBB- by Fitch 485 1,292Romania Two notches from BBB to BB+ by Fitch N/A N/A

One notch from BBB- to BB+ by FitchLativia One notch from A2 to A3 by Moody's N/A N/AArgentina One notch from B to B- by S&P 671 1,960Pakistan One notch from B2 to B3 by Moody's 1,040 2,191

* As of Decemebr 15th, 2008.

EMBIG spreads (bp)

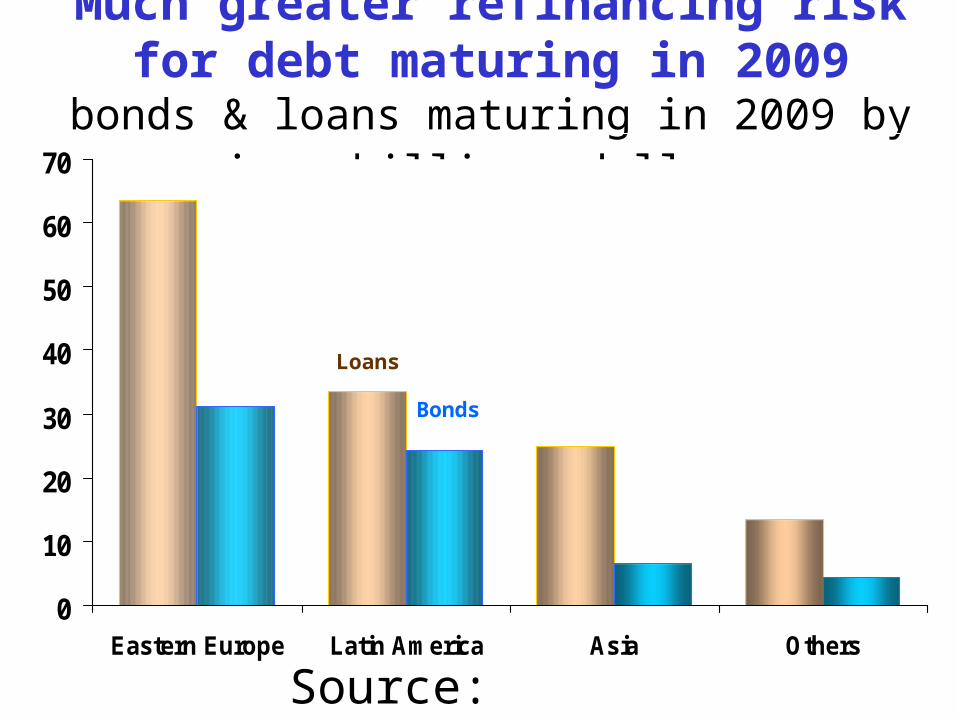

Much greater refinancing risk for debt maturing in 2009

bonds & loans maturing in 2009 by region, billions dollars

0

10

20

30

40

50

60

70

Eastern Europe Latin America Asia Others

Source: Bondware/Loanware.

Loans

Bonds

Currencies

1.230

1.270

1.310

1.350

1.390

1.430

1.470

1.510

1.550

1.590

1.630

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08

86

90

94

98

102

106

110

Source: Thomson/Datastream.

yen/USD

USD/Euro (inverse)

Dollar plummets since early December to reverse earlier gains

USD per Euro (inverse) [Left] and Yen per USD [right]

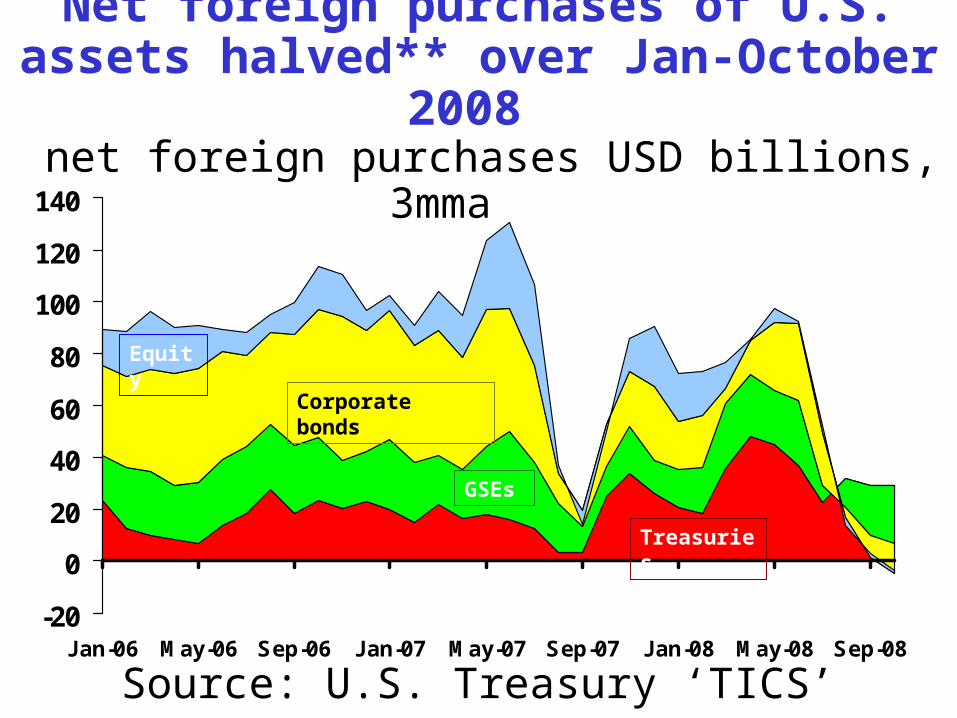

Net foreign purchases of U.S. assets halved** over Jan-October 2008

net foreign purchases USD billions, 3mma

-20

0

20

40

60

80

100

120

140

Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08

Treasuries

Source: U.S. Treasury ‘TICS’ database. ** Jan-Oct08 vs Jan-Oct07

GSEs

Corporate bonds

Equity

80

90

100

110

120

130

140

150

160

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08

Source: Thomson/Datastream.

Dollar surges... then retreats against EM currencies

LCU per USD indexes, Jan1 2008=100 [*increase = weaker LCU]

Turkish lira

Brazilian real

Indonesian rupiah

Korean won

Russian rouble

The External Environment for Developing Countries

December 2008The World Bank

Development EconomicsProspects Group