THE FINANCIAL BENEFITS OF EXPANDING IN THE DEVELOPMENT AREAS By Roy THOMAS It is clear from the evidence submitted to the Hunt Committee1 that there is growing concern in many parts of the country over the extreme preference, which it is alleged, is accorded by the Board of Trade to the Development Areas. It has been argued that a continuation of existing policies could lead to a serious distortion of the pattern of industrial location; that it could impede the progress of industrial dispersal to new towns and reception areas; and that it could well result in a solution being found for the problems of existing Development Areas at the expense of creating new and equally intractable problems elsewhere. The purpose of this article is to evaluate the degree of preference currently enjoyed by the Development Areas. We shall also examine whether the changes in Development Area policy introduced since 1966 have significantly increased the margin of advantage in their favour. The 1966 Industrial Development Act replaced the former Development Districts by much broader Development Areas, and changed the system of investment incentives in both favoured areas and the rest of the country. The main changes in grants and taxation allowances on investment in manufacturing are summarised in Table 1. TABLE 1 Grants and Tax Allowances Local Employment Act, 1963, Finance Act, 1963 35 per cent in Special Development Areas. 'The Committee's Report was published, and Government proposals for limited assistance for a number of selected areas outside the present Development Areas were announced, as this article was going to press. 77 B Industrial Development Act, 1966 New Plant &' Machinery New Industrial Buildings Development Districts Rest of Britain Development Districts Rest of Britain Cash Grants 10% - 25% - Investment Allowances 30% 30% 15% 15% Initial Allowances Free Depreciation 10% 5% 5% New Plant & Machinery New Industrsal Buildings Development Areas Rest of Britain Development Areas Rest of Britain Cash Grants 40% * 20% * 25% f - Initial Allowances - - 15% 15% * £Ç nor ron+ nA 7Ç npr ront mr p'vnondi+urp inriirrpd in 1 01W-1 ORS

Transcript

THE FINANCIAL BENEFITS OF EXPANDING IN THEDEVELOPMENT AREAS

By Roy THOMAS

It is clear from the evidence submitted to the Hunt Committee1 that there isgrowing concern in many parts of the country over the extreme preference,which it is alleged, is accorded by the Board of Trade to the Development Areas.It has been argued that a continuation of existing policies could lead to a seriousdistortion of the pattern of industrial location; that it could impede the progressof industrial dispersal to new towns and reception areas; and that it could wellresult in a solution being found for the problems of existing Development Areasat the expense of creating new and equally intractable problems elsewhere.

The purpose of this article is to evaluate the degree of preference currentlyenjoyed by the Development Areas. We shall also examine whether the changesin Development Area policy introduced since 1966 have significantly increasedthe margin of advantage in their favour.

The 1966 Industrial Development Act replaced the former DevelopmentDistricts by much broader Development Areas, and changed the system ofinvestment incentives in both favoured areas and the rest of the country. Themain changes in grants and taxation allowances on investment in manufacturingare summarised in Table 1.

TABLE 1Grants and Tax Allowances

Local Employment Act, 1963, Finance Act, 1963

35 per cent in Special Development Areas.'The Committee's Report was published, and Government proposals for limited assistance

for a number of selected areas outside the present Development Areas were announced, as thisarticle was going to press.

* £Ç nor ron+ nA 7Ç npr ront mr p'vnondi+urp inriirrpd in 1 01W-1 ORS

78 BULLETIN

Prior to 1966, for investment in plant and machinery, far and away the mostimportant incentives were those administered by the Inland Revenue. TheInvestment allowance constituted a net additional allowance against tax overand above the normal statutory depreciation allowances. Thus, the 30 per centInvestment allowance, available in Development Districts and Non-Develop-ment Districts alike, raised the total of the allowances deductible from taxableincome over the life of an asset to 130 per cent of its net cost. The Initial allow-ance, on the other hand, is a form of accelerated depreciation. The amount ofthe Initial allowance claimed in any one year is deducted from the total of theallowances available to be set against tax in subsequent years. Free depre-ciation, in effect a 100 per cent Initial allowance, constituted the principal formof discrimination in favour of the Development Districts. To derive maximumbenefit from this provision, a firm had to make sufficient overall profit to be ableto claim the whole of the tax allowances arising from its expenditure in the yearin which the expenditure was incurred. The average delay before actual benefitwas reaped in the form of a tax remission was eighteen months. Receipt of theInvestment Grants, which have replaced the Investment and Initial Allowancesunder the new system, does not depend on a profit being earned. The new cashgrants are treated for tax purposes as capital receipts and, as such, are not liableto Corporation Tax. However, the amount of the grant is deducted from thecapital cost of the asset to which it relates in computing annual depreciationallowances. Thus, by virtue of the receipt of a grant, a firm's liability to tax overthe life of the asset is increased. Investment Grants are currently paid quarterlytwelve months after expenditure, although it is the ultimate intention to reducethe delay before payment to six months.

For expenditure on new industrial buildings, the 25 per cent Building Grantpreviously payable to firms in the Development Districts was retained in the newDevelopment Areas. For tax purposes Building Grants are treated in the sameway as Investment Grants. Whereas, however, a new network of regional officeswas set up under the 1966 Act to administer the Investment Grants, applicationsfor Building Grants continued to be subject to the approval of the Board ofTrade Advisory Committee. Moreover, unlike the Investment Grants, whichare not conditional on any increase in employment, Building Grants remainsubject to an employment proviso. Receipt of the full 25 per cent grant is depend-ent on the expectation of a reasonable density of employment in relation tofloor space. In caseswhere the density falls significantly below 40 workers per10,000 square feet, the rate of grant is generally scaled-down. On the other hand,in cases where a project offers a high density of employment, and in certainareas, a high ratio of male to female labour, or if the Board of Trade considersthat a firm faces exceptional problems which justify additional assistance, therate of grant can be increased to up to 35 per cent. In the forty-seven Employ-ment Exchange Areas, designated as Special Development Areas in November1967, 35 per cent has become the standard rate of grant. Since each applicationfor a Building Grant has to be negotiated separately with the BOTAC, the delaybefore receipt of grant can vary quite considerably. A survey conducted by theNorth East Development Council1 revealed an average delay of thirteen months

1 Reported in The Times, 28th February, 1968.

FINANCIAL BENEFITS IN THE DEVELOPMENT AREAS 79

in dealing with applications. Some reduction in administrative delays shouldresult from the passing of the Public Expenditure and Receipts Act in March1968. This Act makes the reference of applications for Building Grants to theAdvisory Committee a matter for the Board of Trade's discretion. The Boardhas since indicated that it does not intend as a general rule to refer applicationsinvolving building costs of less than 1O,000. A further speeding up in thepayment of Building Grants is promised as a result of the decision announcedby the President of the Board of Trade in July 1968 that grants would not beavailable after August 31st for non-industrial projects providing employment forless than fifty additional workers.

In addition to the Investment Grants and the Building Grants, firms inDevelopment Areas can qualify for various other forms of assistance, previouslyavailable under the Local Employment Acts, and retained in the IndustrialDevelopment Act, e.g. the discretionary BOTAC loans and grants for generalbusiness purposes.

An entirely new form of assistancè was introduced by way of an Amendmentto the 1967 Finance Act. Over and above the existing Selective EmploymentPremium, manufacturing firms in Development Areas were to receive anadditional Regional Employment Premium of 30s. per week for every full-timemale employee, with reduced rates for females, juveniles and part-time employeesThis new scheme was introduced in September 1967 for a guaranteed mimimumperiod of seven years. From April 1968, the payment of the Selective Employ-ment Premium to firms outside the Development Areas was discontinued. Thesefirms now qualify only for a straight refund of SET. This has effectively increasedthe differential subsidy in favour of manufacturing employment in the Develop-ment Areas (before Corporation Tax) to 37s. 6d. for every full-time maleemployee, and 18s. 9d. for females. The premia, together with the refund, arereceived three months after payment of SET. For Corporation Tax purposes thepremia are treated as current receipts. In assessing their net value, thefefore,increased liability to tax needs to be taken into account.

The introduction of new financial inducements has been accompanied by astrengthening of negative controls. The Industrial Development Act reduced theexemption limit on IDC controls from 5,000 to 3,000 square feet, and stipulatedthat ancillary buildings were henceforth to be treated as industrial buildings forpurposes of control. This attempt to close previous loopholes in the IDC mechan-ism was accompanied by the promise of a more rigorous application of controlsthroughout the Midlands and the South East. An attempt to assess the signific-ance of negative controls as an instrument of Development Area policy is bestpostponed until after we have completed our evaluation of positive inducements.

In evaluating the degree of fiscal discrimination enjoyed by firms in favouredareas, account will be taken only of standard benefits. There is no satisfactorymeans of including discretionary BOTAC general purpose loans and grants inthe assessment, as the amount of assistance which a firm receives, if any, and theterms on which it is offered, is decided by the Committee according to the meritsof each individual application. No account will be taken either of the assistancewith industrial training provided by the Department of Employment and Pro-

80 BULLETIN

ductivity When comparing current benefits with those available under thepre-1966 system, it should be borne in mind that the present DevelopmentAreas cover a much wider area than the old Development Districts. On theother hand, the assets which attract Investment Grants are more stringentlydefined than was previously the case with Investment Allowances. Officeequipment, canteen equipment, welfare equipment, and individual items costingless than 25 are generally excluded from eligibility. No account has been takenin the assessment which follows of the change in the geographical coverage offavoured areas, or of changes in qualifying assets.

We begin our evaluation of financial inducements by computing the presentvalue of the capital incentives available to firms under both the pre-1966 systemand the current system (a) in favoured areas and (b) in ordinary areas. Theresults are shown in Table 2.

TABLE 2

Present Value of Grants and Tax Savings arising from a unit capital expenditureon a 15 Year Mixed Project

For purposes of calculation it was assumed that the capital outlay is incurredat end-year 0, and is compounded of 60 per cent expenditure on new plant andequipment, 25 per cent on new industrial buildings, and 15 per cent on workingcapital. (This assumed composition of capital costs corresponds to the averagepattern of gross capital formation in manufacturing industry in 1961.4965).The rates of grants and of Investment and Initial allowances are as shown inTable 1. It is assumed that the various cash grants are received twelve monthsafter expenditure is incurred. The assumed rates of statutory annual depre-ciation allowances, which are based on the scale laid down in the 1963 FinanceAct, are as follows:

Building (Straight Line): 4 per cent.Plant (Reducing Balance): 20 per cent.

Firms are assumed to make sufficient overall profits to be able to claimcapital allowances in full as they arise. The tax savings arising from the capitalallowances are assumed to accrue eighteen months after expenditure. Finally,it was assumed that residual values are as indicated below:

Plant: Zero Scrap Value.Buildings: Written-Down Value (for Tax purposes).Working Capital: Recovered in Full at end of project.

The value to firms of capital allowances is inversely related to the rate of tax.Hence the switch from Income Tax and Profits Tax to Corporation Tax in

Rate of Discount

7% 10%Old System

.418 .378Non-Development District ... ... ... ...Development District ... ... ... ... ... .529 .503

New SystemNon-Development Area ... ... ... ... .311 .284Development Area ... ... ... ... ... .432 .406

FINANCIAL BENEFITS IN THE DEVELOPMENT AREAS 81

1965 considerably reduced the value to companies of the old taxation allowances.'In evaluating the pre-1966 incentives, the calculations were based on the rate oftax under the old system of company taxation. The operative rate was thereforetaken to be 56.25 per cent, compounded of Standard Rate Income Tax at 8s. 3d.and Profits Tax at 15 per cent. The summation of Income Tax and Profits Taxmakes the calculation of the present values of the old taxation allowances some-what easier than if the savings in Income Tax and in Profits Tax had been calcu-lated separately. It does, however, introduce a slight error into the calculation.In practice, annual and initial allowances were computed on the current year'sexpenditure for purposes of Income Tax assessment, and on the previous year'sexpenditure for Profits Tax. Thus the Profits Tax saving arising from the annualand initial allowances (but not the investment allowance) was lagged one year.By overlooking this one-year lag, we have in effect overestimated, but only veryslightly, the present values of the investment incentives under the old system.A rate of Corporation Tax of 42.5 per cent was taken as the operative tax rateunder the new system.

What emerges from Table 2 is that in both favoured areas and ordinaryareas, the value of the current investment incentives is considerably less than thevalue of the incentives available under the previous system. The depreciationin the value of the incentives, in fact, is even greater than it would appear fromthe Table. Under the old system of company taxation the return earned by thecompany was the same as that earned by its shareholders. Under the new systemthe company pays Corporation Tax on profits, but in addition, shareholders payIncome Tax on dividends and Capital Gains Tax on growth, so that the returnto the company is higher than the return to its shareholders. It follows that thevalue of investment incentives to a company's shareholders is less than theirvalue to the company. It is the value to the comany which has been calculatedin Table 2 since taxation allowances under the new system can be set againstCorporation Tax only. When comparing the value of the incentives under thenew system with those under the previous system, it follows that an allowancefor income tax and capital gains tax needs to be embodied in the rate of discount.The appropriate allowance will depend on a number of factors, e.g. a company'spay-out ratio, and the rate of turnover in the company's shares.2 However, theappropriate rate of discount under the new system corresponding to 7 per centunder the old, would probably be in the region of 10 per cent.3 From Table 2 itcan be seen that the present value of investment incentives in ordinary areasunder the new system, discounted at 10 per cent, falls short of the value of theold incentives, discounted at 7 per cent, by .134 on a unit capital expenditure.The corresponding short-fall in favoured areas is .123.

The above calculations of the value of incentives to firms in favoured areastake no account of the Employment Premia. The value of the premia to firmsembarking on new projects in Development Areas will clearly depend on the

1 See Alfred and Evans, 'The Corporation Tax and the Incentive to Invest', Tile InvestmentAnalyst, December 1964.

2 See, Lawson and Windle, Capital Budgeting and the Use of DCF Criteria in the CorporationTax Regime, Oliver and Boyd, 1967, Chap. 4.

See A. M. Alfred, 'The Correct Yardstick for State Investment,' District Bunk Review,June 1968.

82 BULLETIN

labour intensity of a project and the sex ratio of the prospective labour force. Ifone assumes a male: female ratio of 68:32,1 and that the premia are payable end-yearly for a period of seven years from the date of expenditure,2 it can be shownthat with a capital-labour ratio of just over f2,000 per worker, the present valueof the premia, after tax, arising from a unit capital expenditure, discounted at10 per cent, would be just sufficient to make up the short-fall of .123 indicatedabove. In other words, the inclusion of the employment premia would restorethe value of current financial incentives in favoured areas to their pre-1966 level.In the case of more capital intensive projects, the present value of currentincentives would be lower than pre-1966; in the case of more labour intensiveprojects they would be higher.

Clearly capital-labour ratios can vary considerably from industry toindustry and from project to project. For manufacturing industry as awhole, the value of capital per worker works out at roughly L2,7OO. Thereis little direct evidence on the capital-labour ratio of new investment in theDevelopment Areas. On the basis of floor area of factory space per job MichaelChisoim has suggested that the development areas tend to attract relativelylabour-intensive industrial employment.4 NEDC assumed a ratio of L2,000 perworker in new firms setting up in the old Development Districts.5 A surveycarried out by the Scottish Council6 revealed that capital expenditure of f288million by incoming firms over the period 1963-1966 had produced 102,000additional jobs, a ratio of 2,80O per worker. It is likely that this ratio would besomewhat reduced however if account were taken of the lag in the build-up ofemployment. It would seem, therefore, that a ratio of 2,5OO per worker wouldprobably be about right. Combining this figure with our earlier assumptionsregarding sex-ratios, and the duration of the REP scheme, the present values atdifferent rates of discount, of the employment premia, after tax, arising from aunit capital expenditure, can be calculated. It these are added to the presentvalues of the capital incentives, given in Table 2, we obtain the present value ofthe total standard financial benefits arising from a unit capital expenditure on a15-Year Mixed project in a Development Area. These are given below.

Rate of Discount Present Value7 per cent .541

10 per cent .5071 This was the ratio of male: female employment in new projects set up by manufacturing

firms that moved into 'Peripheral Areas' (roughly corresponding to the present DevelopmentAreas) in 1960-1965. See R. S. Howard, The Movement of Manufacturing Industry in theUnited Kingdom, 1945-1965. Board of Trade, 1968, Paras. 95 sq.

2 In practice the premia are payable at quarterly intervals. End-year discounting, however,introduces only a very slight error into the calculation. A more serious objection might beraised against the assumption implicit in the above analysis that firms take on their fullcomplement of workers from the very start of operations. In practice, it is more likely thatthere would be a gradual build-up of the labour force. The assumption is akin to the one madeearlier that the whole of the capital outlay is incurred at end-year 0. Both assumptions mightbe said to be unrealistic. Their function however is essentially illustrative, and in both cases,they considerably ease the task of calculation.

This figure is based on the value of the gross capital stock at 1958 replacement cost givenin the National Income and Expenditure Blue Book for 1968, Table 66.

' Michael Chisolm, 'The premium problem: is it worth 11,000 a job?', The Times BusinessReview, 28.4.67.

NEDC, Conditions Favourable to Faster Growth, HMSO, 1963, p. 24.6 Reported in the Board of Trade Journal, 14.7.67.

FINANCIAL BENEFITS IN THE DEVELOPMENT AREAS 83

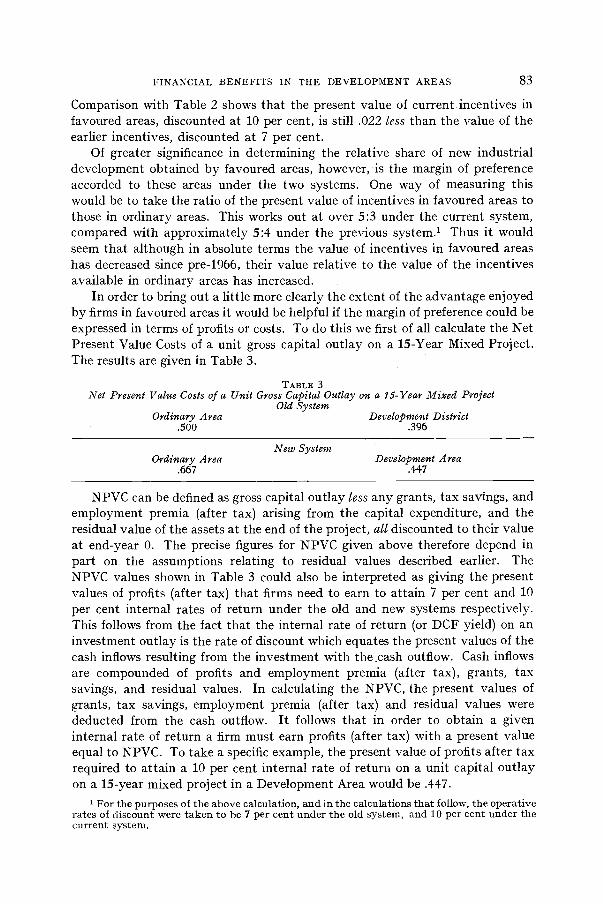

Comparison with Table 2 shows that the present value of current incentives infavoured areas, discounted at 10 per cent, is still .022 less than the value of theearlier incentives, discounted at 7 per cent.

Of greater significance in determining the relative share of new industrialdevelopment obtained by favoured areas, however, is the margin of preferenceaccorded to these areas under the two systems. One way of measuring thiswould be to take the ratio of the present value of incentives in favoured areas tothose in ordinary areas. This works out at over 5:3 under the current system,compared with approximately 5:4 under the previous system.' Thus it wouldseem that although in absolute terms the value of incentives in favoured areashas decreased since pre-1966, their value relative to the value of the incentivesavailable in ordinary areas has increased.

In order to bring out a little more clearly the extent of the advantage enjoyedby firms in favoured areas it would be helpful if the margin of preference could beexpressed in terms of profits or costs. To do this we first of all calculate the NetPresent Value Costs of a unit gross capital outlay on a 15-Year Mixed Project.The results are given in Table 3.

TABLE 3Net Present Value Costs of a Unit Gross Capital Outlay on a 15- Year Mixed Project

Old SystemOrdinary Area Development District

.500 .396

New SystemOrdinary Area Development Area

.667 .447

NPVC can be defined as gross capital outlay less any grants, tax savings, andemployment premia (after tax) arising from the capital expenditure, and theresidual value of the assets at the end of the project, all discounted to their valueat end-year 0. The precise figures for NPVC given above therefore depend inpart on the assumptions relating to residual values described earlier. TheNPVC values shown in Table 3 could also be interpreted as giving the presentvalues of profits (after tax) that firms need to earn to attain 7 per cent and 10per cent internal rates of return under the old and new systems respectively.This follows from the fact that the internal rate of return (or DCF yield) on aninvestment outlay is the rate of discount which equates the present values of thecash inflows resulting from the investment with the .cash outflow. Cash inflowsare compounded of profits and employment premia (after tax), grants, taxsavings, and residual values. In calculating the NPVC, the present values ofgrants, tax savings, employment premia (after tax) and residual values werededucted from the cash outflow. It follows that in order to obtain a giveninternal rate of return a firm must earn profits (after tax) with a present valueequal to NPVC. To take a specific example, the present value of profits after taxrequired to attain a 10 per cent internal rate of return on a unit capital outlayon a 15-year mixed project in a Development Area would be .447.

1 For the purposes of the above calculation, and in the calculations that follow, the operativerates of discount were taken to be 7 per cent under the old system, and 10 per cent under thecurrent system.

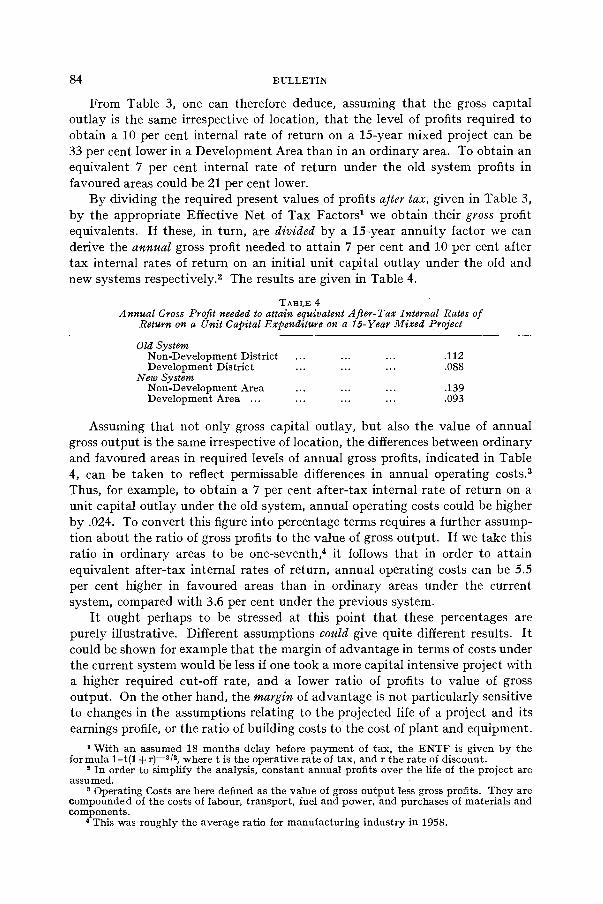

84 BULLETIN

From Table 3, one can therefore deduce, assuming that the gross capitaloutlay is the same irrespective of location, that the level of profits required toobtain a 10 per cent internal rate of return on a 15-year mixed project can be33 per cent lower in a Development Area than in an ordinary area. To obtain anequivalent 7 per cent internal rate of return under the old system profits infavoured areas could be 21 per cent lower.

By dividing the required present values of profits after tax, given in Table 3,by the appropriate Effective Net of Tax Factors' we obtain their gross profitequivalents. If these, in turn, are divided by a 15-year annuity factor we canderive the annual gross profit needed to attain 7 per cent and 10 per cent aftertax internal rates of return on an initial unit capital outlay under the old andnew systems respectively.2 The results are given in Table 4.

TABLE 4Annual Gross Profit needed to attain equivalent After-Tax Internal Rates of

Return on a Unit Capital Expenditure on a 15-Year Mixed Project

Old System

Assuming that not only gross capital outlay, but also the value of annualgross output is the same irrespective of location, the differences between ordinaryand favoured areas in required levels of annual gross profits, indicated in Table4, can be taken to reflect permissable differences in annual operating costs.3Thus, for example, to obtain a 7 per cent after-tax internal rate of return on aunit capital outlay under the old system, annual operating costs could be higherby .024. To convert this figure into percentage terms requires a further assump-tion about the ratio of gross profits to the value of gross output. If we take thisratio in ordinary areas to be one-seventh,4 it follows that in order to attainequivalent after-tax internal rates of return, annual operating costs can be 5.5per cent higher in favoured areas than in ordinary areas under the currentsystem, compared with 3.6 per cent under the previous system.

It ought perhaps to be stressed at this point that these percentages arepurely illustrative. Different assumptions could give quite different results. Itcould be shown for example that the margin of advantage in terms of costs underthe current system would be less if one took a more capital intensive project witha higher required cut-off rate, and a lower ratio of profits to value of grossoutput. On the other hand, the margin of advantage is not particularly sensitiveto changes in the assumptions relating to the projected life of a project and itsearnings profile, or the ratio of building costs to the cost of plant and equipment.

'With an assumed 18 months delay before payment of tax, the ENTF is given by theformula 1t(1 + r)_3/2, where t is the operative rate of tax, and r the rate of discount.

Z In order to simplify the analysis, constant annual profits over the life of the project areassu med.

Operating Costs are here defined as the value of gross output less gross profits. They arecompounded of the costs of labour, transport, fuel and power, and purchases of materials andcomponents.

This was roughly the average ratio for manufacturing industry in 1958.

Non-Development District ... ... .112Development District .088

New SystemNon-Development Area .139Development Area ... ... .093

FINANCIAL BENEFITS IN THE DEVELOPMENT AREAS 85

Since the assumptions actually used were chosen wherever possible in the lightof the available data on manufacturing industry, it is reasonable to concludethat the figures given above do provide some indication of the correct order ofmagnitude over quite a wide range of manufacturing projects.

The analysis would seem to indicate that while there are very definitefinancial advantages to be obtained from locating a new project in a Develop-ment Area, the margin of preference can hardly be regarded as so overwhelmingas to outweigh normal commercial and technical considerations. Empiricalstudies have indicated that while inter-regional cost differences can be quitenegligible once a project is firmly established, during the initial settling-in periodthe operating costs of new projects in peripheral areas can be higher by as muchas 20 to 30 per cent.1 This strongly suggests that in a good many instances, themargin of preference provided by the government's financial incentives will dono more than partially offset initial cost disadvantages. It is of course true thatthere are additional forms of assistance, which were not taken into account inthe above analysis, for which firms setting up new projects in favoured areasmight qualify. Total expenditure on such items as general purpose loans andgrants, assistance with training, and the transference of key workers, suggests,however, that these additional methods of assistance would be unlikely in themajority of instances to increase the margin of advantage in terms of costs bymore than one percentage point. It seems safe to conclude that the degree offiscal preference currently enjoyed by Development Areas should not in itselfresult in any serious distortion of the pattern of industrial settlement.

Comparison of the current position with the pre-1966 situation shows thatalthough the margin of advantage enjoyed by favoured areas has widened, thedifference is quite marginal. Nor does it seem likely that the extension in thegeographical coverage of favoured areas will significantly increase their relativeshare of new industrial development. The increase in terms of the number ofmanufacturing employees (in January 1966) in the Development Areas, com-pared with the old Development Districts, was only 13 per cent. The very muchlarger difference in land area is mainly due to the granting of Development Areastatus to peripheral rural areas, such as Mid Wales, with small and dispersedpopulations. In the absence of a large-scale planned influx of population theseareas are unlikely to attract new industry on any significant scale.2 Theirinclusion in the new Development Areas should not, therefore, in itself, seriouslyprejudice the prospects for industrial expansion in other parts of the country.A further point which should be noted is the continued exclusion from the newDevelopment Areas of parts of the less prosperous regions which have displayedthe greatest potential for industrial growth, e.g. the coastal belt of South EastWales. There seems to be very little justification therefore for the widely heldbelief that there has been a marked deterioration in the relative attractiveness ofthe so-called Intermediate Areas as a result of the measures taken since 1966.

It might be objected that in our evaluation of the Employment Prernia

1 See for example, W. F. Luttreil, Factory Location and Indus trial Movement, NationalInstitute of Economic and Social Research, 1962.

2 See Roy Thomas, Industry in Rural Wales, University of Wales Press, 1966, Chap. 8.

86 BULLETIN

account was taken only of the benefit to firms embarking on new projects inDevelopment Areas. Since the premia are available for new and existing projectsalike, it might be argued that in assessing the degree of fiscal preference enjoyedby favoured areas allowance ought to be made for the competitive advantageconferred by the premia on existing producers. It is true that in the short runthe premia might well encourage a more intensive use of existing capacity inthe Development Areas and thereby help to cushion these areas from the effectsof a cyclical contraction in output. There must come a point however when anyfurther increases in output and employment must be accompanied by anexpansion of productive capacity. This paper has been exclusively concernedwith the relative attractiveness of the Development Areas for new industrialinvestment. The additional stimulus to long-term industrial developmentprovided by the premia has been fully taken into account in the foregoinganalysis.

To draw any firm conclusions about the likely effect of incentives simply onthe basis of their value to firms and their implications for firms' cost structurescould well be misleading. There is considerable evidence that firms pay inade-quate regard to incentives. This may be due partly to the use of faulty methodsof appraisal, and also in part to uncertainty on the part of firms about theduration of benefits. Whether firms are likely to pay more regard to the incen-tives provided under the current system than under the old remains to be seen.A number of surveys have revealed that a good many firms failed to take accountof the tax savings available under the old system.1 A similar failure on the partof firms to take account of the effect of current incentives on their tax liabilityover the life of a project would clearly make them aear very much moreattractive than the old.

We turn finally to the other main weapon in the Board of Trade's armoury,viz. IDC controls. Not surprisingly, it is the application of these negativecontrols rather than the positive inducements which has aroused the fiercestopposition from certain quarters. Recent evidence suggests however that theBoard of Trade has administered the controls very much more liberally than wasgenerally recognised. In its latest annual report on the working of the LocalEmployment Acts, the Board of Trade for the first time, provides an analysis ofIDC refusals.2 This reveals that in the year 1967-1968 in the Midlands and theSouth East, refusals in terms of floor-space, accounted for less than one-sixth oftotal applications. Even allowing for the possibility that some firms may havebeen deterred from making applications in the belief that they would not besuccessful, it is clear that the controls have been very much less restrictive thanwas widely believed. Looking at IDC controls as an instrument of DevelopmentArea policy, it is significant that refusals in the whole of the Midlands and theSouth East amount to less than a quarter of the total area approved in theDevelopment Areas. This would seem to suggest that the contribution to

See, e.g. D. C. Corner and A. Williams, 'The Sensitivity of Businesses to Initial and Invest-ment Allowances', Ecoiwmica, Feb. 1965, and R. R. Neild, 'Replacement Policy', NationalInstitute Economic Review, Nov. 1964.

2 Local Employment Acts 1960 to 1966, Eighth Annual Report by the Board of Trade,HMSO, July, 1968, Appendix IV.

FINANCIAL BENEFITS IN THE DEVELOPMENT AREAS 87

industrial expansion in the Development Areas attributable to the IDC mechanismmay well have been quite marginal. Further evidence to this effect emergesfrom a recent survey conducted by the Confederation of British Industries.This showed that in the South East and East Anglia only 3 per cent of theschemes for which an IDC was required were actually diverted to the Develop-ment Areas.'

To conclude, it would appear that the margin of advantage conferred uponthe Development Areas by existing government policies is considerably lessthan is widely recognised. Moreover the degree of preference has increased onlymarginally as a result of the various measures taken since 1966. The operation ofnegative controls has been nowhere near as rigid as is often claimed, and itappears extremely unlikely that it could have resulted in any serious distortionin the pattern of industrial location. As to the positive inducements, our analysisconfirms the CBI view that they 'can contribute to offset costs'. However,insofar as the above analysis of the degree of preference accorded to firmsexpanding in the Development Areas is correct, it is hardly surprising that theCBI survey should conclude that they 'are not a "prime-mover" influencing afirm's location decision'.2

If there is to be any marked improvement in the relative position of theDevelopment Areas the retention of the existing degree of preference mustsurely be regarded as a minimum requirement. In addition if the fundamentalweaknesses of these areas are to be overcome more emphasis must be placed onindustrial re-training, environmental improvements and a strengthening of basicinfrastructure. In the past, the government has tended to relax its efforts onbehalf of the less prosperous regions at precisely those times when its policiesmight have been expected to yield positive results, viz, during the expansionphase of the stop-go cycle. In the coming months there is every indication of arevival in industrial investment. While clearly the government must be awaketo the possibility of the emergence of new problem areas, the dilution of thealready small margin of preference accorded to the Development Areas by thegranting of intermediate benefits elsewhere would seem at the present time to besingularly inopportune.

'CBI Regional Study, Regional Development and Distribution of Industry Policy, Sept.1968, para. 11.52.

Op. cit. para 12.56.

University College of South Wales and Monmouthshire, Cardiff.