MONETARY POLICY STATEMENT THE FIRST QUARTER TO 31 MARCH, 2004 Issued IN TERMS OF THE RESERVE BANK OF ZIMBABWE ACT CHAPTER 22:15, SECTION 46 By DR. G. GONO GOVENOR RESERVE BANK OF ZIMBABWE APRIL 2004 ___________ The Monetary Policy Statement is issued bi-annually, in January and June of each year.. In an attempt to lay out the Bank’s monetary policy stance and consistent with the 2004 National Budget and the Governor’s maiden Monetary Policy Statement announced on 18 December, 2003, it has become necessary, however to review and articulate complementary monetary measures on a quarterly basis at the same time, fulfilling the requirements of the Reserve Bank of Zimbabwe Act.

Transcript

MONETARY POLICY STATEMENT

THE FIRST QUARTER TO 31 MARCH, 2004

Issued

IN TERMS OF THE RESERVE BANK OF ZIMBABWE ACT CHAPTER 22:15, SECTION 46

By

DR. G. GONO GOVENOR

RESERVE BANK OF ZIMBABWE

APRIL 2004

___________ The Monetary Policy Statement is issued bi-annually, in January and June of each year.. In an attempt to lay out the Bank’s monetary policy stance and consistent with the 2004 National Budget and the Governor’s maiden Monetary Policy Statement announced on 18 December, 2003, it has become necessary, however to review and articulate complementary monetary measures on a quarterly basis at the same time, fulfilling the requirements of the Reserve Bank of Zimbabwe Act.

Table Of Contents INTRODUCTION AND BACKGROUND ..........................................................................................3 TURNAROUND PROGRESS TO DATE............................................................................................5 THE FINANCIAL SECTOR...............................................................................................................14 TROUBLED BANK FUND .................................................................................................................17 CORPORATE GOVERNANCE............................................................................................................19 EARLY WARNING SYSTEMS .........................................................................................................20 BANK INSOLVENCY AND INDIGENISATION ............................................................................21 MANAGEMENT OF CAPITAL ........................................................................................................23 LICENSING FRAMEWORK.............................................................................................................23 ASSET MANAGEMENT COMPANIES...........................................................................................24 MICROFINANCE INSTITUTIONS..................................................................................................25 OTHER SECTORAL REVIEWS AND INTERVENTIONS...........................................................25 GROSS NATIONAL PRODUCT (GDP)........................................................................................................25 AGRICULTURE..................................................................................................................................26 TURNAROUND RESPONSE .............................................................................................................27 MANUFACTURING ...........................................................................................................................32 MINING SECTOR...............................................................................................................................34 TOURISM SECTOR............................................................................................................................35 PUBLIC ENTERPRISES ....................................................................................................................36 GRAIN MARKETING BOARD (GMB)............................................................................................37 NATIONAL RAILWAYS OF ZIMBABWE (NRZ) .........................................................................37 ENERGY...............................................................................................................................................39 NATIONAL OIL COMPANY OF ZIMBABWE (NOCZIM)..........................................................40 ZIMBABWE ELECTRICITY SUPPLY AUTHORITY (ZESA) ....................................................41 TELECOMMUNICATIONS ..............................................................................................................43 EXPORT PROMOTION: BACKGROUND.....................................................................................44 EXPORT SUPPORT SCHEMES .......................................................................................................47 CARROT AND STICK EXPORT RETENTIONS SCHEME.........................................................47 TOBACCO SUPPORT PRICE........................................................................................................................53 FORM CD1 NON-ACQUITALS ........................................................................................................54 MOBILISATION OF DIASPORA FUNDS.......................................................................................56 OPERATION OF FOREIGN CURRENCY ACCOUNTS (FCAS).................................................59 EXCHANGE RATE MANAGEMENT..............................................................................................62 FOREIGN EXCHANGE FLOWS UNDER THE AUCTION SYSTEM.........................................64 MINING RIGHTS................................................................................................................................68 PRODUCTIVE SECTOR SUPPORT ................................................................................................70 ANTI-INFLATION MONEY SUPPLY MEASURES ......................................................................74 GOVERNMENT ACCESS TO RESERVE BANK WINDOW........................................................75 DISTRIBUTION OF BANKING SECTOR CREDIT ......................................................................77 INTEREST RATES POLICY .............................................................................................................79

1

ACCOMMODATION POLICY .........................................................................................................80 OPEN MARKET OPERATIONS INSTRUMENTS.........................................................................83 NATIONAL PAYMENTS SYSTEM..................................................................................................83 SOCIAL CONTRACT.........................................................................................................................86 TELECOMMUNICATIONS INDUSTRY.........................................................................................87 IMPORTANCE OF REGIONAL MARKETS ..................................................................................89 EXCHANGE CONTROL VIOLATIONS AND REPATRIATION OF FUNDS. ..........................92 FINANCIAL SECTOR CHARTER ...................................................................................................94 EXTENDED BANKING HOURS.......................................................................................................95 ENGAGEMENT WITH OUR CREDITORS ....................................................................................96 CONCLUSION.....................................................................................................................................98

2

RESERVE BANK OF ZIMBABWE

MONETARY POLICY STATEMENT: 2004 FIRST QUARTER

REVIEW 1. INTRODUCTION AND BACKGROUND 1.1 In terms of the Reserve Bank of Zimbabwe Act, Chapter 22:15,

section 46, I am required to issue the Monetary Policy Statement bi-

annually, in January and in June of each year.

1.2 It has, however, become imperative that the Reserve Bank makes a

much more frequent review of the policy framework on a quarterly

basis until such time as our macroeconomic environment is fully

stabilized.

1.3 My first Monetary Policy Statement of 18 December 2003, which laid

the Five Year Vision and its roadmap, has been in operation for a little

over 100 days.

1.4 Though seemingly short on the calendar, this formative stage of my

term as Governor has been tremendously hectic, marked by

sustained transformation in the financial sector, as well as the

emergence of a renewed deep spirit of public-private sector and labour

cooperation in the resolution of the country’s existing economic

challenges through action and ideas.

1.5 In my previous statement, I did profess my profound indebtedness to

various stakeholders from all segments of the economy who had

3

selflessly played a pivotal role in contributing to the strategic thinking

of the Reserve Bank.

1.6 I wish to once again, acknowledge with gratitude, the support that I

continue to receive from all stakeholders making up our socio-

political and economic universe.

1.7 The first quarter of the year has also taught us that, as a Nation, we

need unwavering commitment and endurance as we confront and see

through the pain and temporary setbacks that typically define a

home-grown dedicated and self-correction economic program which

we have collectively chosen to follow. We are, and should be,

masters of our own destiny with outsiders only coming in to assist

us.

1.8 As Monetary Authorities, we have also come to fully comprehend

the form, substance and destructive effects of the widespread

corporate incest, untoward behaviour and financial cannibalism

that had entrenched itself in our midst, spurred by the gratuitous

subordination of corporate governance norms in pursuit of

personal gain as well as a lax supervision and surveillance regime.

1.9 Naturally, like any other Central Bank the world over, we could not

sit, standby and watch whilst this cancerous development

worsened the plight of our economy in general and that of

depositors in particular. It is a cancer we needed to deal with

decisively and we remain on high alert to deal severely with any

resurgence of same.

4

1.10 Furthermore as Monetary Authorities, we are resolute in our

determination to build and sustain a financial sector with thoroughly

disciplined, honest and professional operators who will steer the

nation’s wealth towards lasting economic development as opposed to

short term gains.

2. TURNAROUND PROGRESS TO DATE

2.1. The purpose of this 2004 first quarter Monetary Policy Statement

Review is to take stock of the achievements registered and challenges

faced to date, from when the new monetary policy framework came

into effect on 1 January, 2004. In turnarounds, Vision is followed

by Strategy, followed by implementation. Frequent reviews and

monitoring of performance to consolidate the vision or to take

corrective actions are an indispensable part of any turnaround journey.

2.2. The Monetary Policy roadmap we unveiled in December 2003,

sought to achieve the following broad objectives, among others.

(a) Stabilize the inflationary spiral to maintain the internal value of the

Zimbabwe dollar, and hence, protect real incomes of corporates,

households, Government and society in general.

(b) Arrest pressures on the exchange rate to maintain the external value

of the Zimbabwe dollar through exchange rate stability, and

normalize foreign exchange market trading including accountability

thereof.

5

(c) Arrest job losses and increase employment levels through greater

capacity utilization and investment growth.

(d) Promote collective cooperation through stakeholder participation and

dialogue on matters of the national economy.

(e) Promote a stable, reliable, sound and effective financial system to

support economic growth and development.

(f) Re-engage the international community to lay a sound basis for the

re-establishment of Zimbabwe’s relations with international creditors

and other global business partners.

(g) Engage Zimbabweans in the Diaspora and involve them in the

turnaround of our economy and in other supportive initiatives.

(h) Begin to build foreign currency reserves of our own resources.

(i) Support productive sectors of the economy through low-cost finance

while allowing the market to determine rates for non-productive, non

priority level spending.

2.3 SUCCESSES TO DATE

(a) Whilst it is notably too early to fully account for successes and

failures of the turnaround initiative, as Monetary Authorities, we

are pleased to share with stakeholders some encouraging pointers

towards success in meeting our shared Vision of sustained economic

revival.

6

(b) Credit for these modest achievements, in line with my Maiden

Statement in December 2003, goes to all Zimbabweans, who have

rallied behind our efforts todate.

(c) On the inflation front, we have managed to burst the bubble of

runaway monthly increases in the general level of prices, as had

become the norm in 2003.

(d) Reflecting this, month-on-month inflation, which averaged 18% in

2003 and reached a peak of 33.6% in November, 2003, retreated to

13.7% in January, 2004, 6% in February, before further decelerating

to 5.9% in March, 2004.

Month-on-month inflation profile: January 2003-March 2004

miners, retailers, exporters, National Economic Consultative

9

Forum, Tourism, ZIMRA, Ministry of Industry and International

Trade and the President’s Office, among many others, to actively

engage each other on broad policy issues and alternative

implementation strategies and priorities.

(p) Though at inception, the Advisory Board was initially mandated to

focus on exchange rate matters, the richness of deliberations soon

compelled mutual convergence of minds on the expansion of the

Board’s mandate to also cover other broad monetary, and

structural policy issues.

(q) Activities of the Advisory Board, which has met religiously every

week since 19 January, 2004, have thus become a constant source of

inspiration to the Central Bank on the immeasurable strides that can

be achieved through stakeholder engagement and cross-pollination of

ideas.

(r) As Monetary Authorities, we also sought to arrest growing

unemployment, capacity underutilization and rapid decline in national

production through enhancement of producer viability and quick

removal of bottlenecks which militate against our economic revival

efforts.

(s) To this end, we are heartened by the positive feedback that is

coming from industry, commerce, agriculture, mining, tourism,

and the nascent informal sector, on the fruitful impact the

concessional financing facility is having on economic production, job

creation/preservation and capacity utilization.

10

(t) We had also pledged support to the informal sector during the

December 2003 Monetary Policy Statement.

(u) We are pleased to have set aside Z$12 billion for the informal

sector, which is being channeled through SEDCO for onward

disbursement to beneficiaries throughout the country, as we gear

to unlock this sector’s economic potential and grow the micro-

enterprises into economic giants of tomorrow.

(v) Realizing gold’s direct positive bearing on the country’s foreign

exchange reserves, we also undertook to enhance viability and

increase deliveries of this strategic resource to build up national

reserves. This achievement was made possible through the

cooperation of the miners themselves (small and large), Fidelity

Collection Centres, Ministry of Mines, and Law Enforcement agents

of the State.

(w) We are pleased to note considerable increase in gold deliveries over

the first quarter of 2004 as reported below:

(i) Over the period January-March 2004, 5.13 tonnes of gold,

worth US$67.3 million has been delivered, compared to 3.4

tonnes worth US$39.0 million recorded over the same

period in 2003. In growth terms this represents increases of

50.6% and 72.6% in volume and value terms, respectively.

11

GOLD SALES:MONTHLY US$ MILLIONS FIRST QUARTER COMPARATIVES FOR 2003 & 2004

0

5

10

15

20

25

30

Jan Feb Mar

US

$ M

ILLI

ON

S

2004

2003

Gold Sales in US$ millions

Year/Month Jan Feb Mar Cumulative

2003 14.9 14.4 9.7 39.0

2004 25.3 23.9 18.1 67.3

Growth ‘04/03 69.8% 66.0% 86.6% 72.6%

(x) This, coupled with growing confidence in the foreign exchange

auction system has seen us manage to realize total foreign exchange

inflows, including FCA liquidations, of US$333.5 million during the

first quarter of 2004, which compared much favorably with

US$301.7 million achieved for the entire 12 months in 2003.

(y) The experience over the last three months has humbled us in that

there is a general eagerness by Zimbabweans in industry and

commerce, agriculture, Government, labour, those in the Diaspora and

across all walks of life, to constructively put heads together in

supporting the worthy cause of turning around the economy.

12

(z) A key priority that we had also set to achieve, through monetary

policy, was the re-engagement of the international community

especially our creditors and global business partners.

(aa) To a large extent, some of the international creditors have already

started acknowledging our modest efforts towards re-defining

Zimbabwe’s space in the global marketplace. Our appreciation thus

goes to them individually and collectively as we expect our efforts to

find favor and support in due course.

(bb) We also sought to strengthen the financial sector through

discipline, enhanced corporate governance, impartial and close

supervision and surveillance, including the insistence of tighter

financial controls and risk management systems at institutional levels.

(cc) Evidence on the ground seems to firmly suggest that we are on

course towards meeting this objective.

2.4 OUR SHORT-COMINGS TO DATE

(a) As Monetary Authorities, we remain, deeply remorseful over the

failure of our systems to timeously and appropriately guide the market

in areas of prudential financial sector management.

(b) Most of the observed short-comings in the financial sector cannot

entirely be blamed on the sector participants. With hindsight, we as

the Central Bank feel that we could have guided the sector much

better than we did, especially during the last half of 2003, when a lot

13

of the short-comings seem to have accelerated. We are taking self-

corrective action in this regard.

(c) We have also, historically and most recently, not adequately and

consistently guided the market on our desired path of interest rates as

we pursued the twin objectives of a quick supply response and a

disinflation program. Thus the country’s interest rate structure has

been unnecessarily punitive to borrowers while at the same time

dis-incentivising savers. We seek to correct these shortcomings in

this Policy Review Statement.

(d) Notwithstanding these shortcomings, we remain resolute and are

encouraged by the ample signs of goodwill and unreserved

support all stakeholders are giving us.

3. THE FINANCIAL SECTOR 3.1 Major handicaps that have resulted in protracted liquidity and

solvency challenges at some financial institutions have largely

encompassed a combination of the following factors:

(a) Extensive diversion of management’s attention from the day to

day running of the financial institutions, with more focus placed on

running of commercial enterprises outside the job of running their

banks.

(b) High prevalence of insider loans typified by generous advances to

banks’ directors, management or associated corporates.

14

(c) Failure by some banks to widely diversify the shareholding

structures of their banks, leading to undue influence on the day to

day operations by the owner-managers.

(d) Imprudent credit risk management frameworks, marked by over

concentration of lending to a few associated groups of companies,

effectively increasing default risk, as well as hampering a wider

positive credit impact on other economic activities for

achievement of a broad-based supply response.

(e) Evasion from core banking business, and tying disproportionately

large sums of depositors’ funds in speculative activities, thereby

exposing their businesses to high risks of asset price bubbles.

(f) Deliberate utilization of local currency liquidity in purchases of

foreign currency from the illegal parallel and underground foreign

exchange markets for funding of offshore activities and accounts.

(g) Inadequate Board oversight, aggravated by cross-sitting by the

same Directors on more than one board of financial institutions,

which increased room for conflict of interest.

(h) Weak controls, guidelines, procedures and bank-wide risk

management frameworks.

3.2 A key part of the Reserve Bank’s mandate is to ensure that these

limitations are cleared, so as to build market confidence in the

financial sector and cultivate a smooth operation of the

intermediation process between savers and investors.

15

3.3 It is for these reasons that, the first quarter of the year has seen

Monetary Authorities taking various corrective measures, which

included:

(a) Placement of some financial institutions under curatorship

management;

(b) Enforcement of Board and management changes;

(c) Establishment of the Troubled Bank fund, under which support to

distressed banks was given to enable them to reposition their balance

sheets.

(d) Closure of some institutions where the degree of insolvency was

beyond reach of any salvage measures.

3.4 These measures, which formed the initial phase of re-orienting the

financial sector, were intended to arrest the propagation of

instabilities at a few institutions across the whole financial system.

3.5 Resolution of financial distresses and financial crises during the early

to mid-80’s and the 90’s in such countries as the Philippines,

Thailand, Malaysia, Spain, Argentina and Uruguay was achieved

through attentive focus on these key pillars of Central Bank

intervention.

3.6 As Governor of the Reserve Bank, I want to reassure the public that

our response to the challenges in the financial sector are always

16

guided by an express desire to protect depositors and creditors

interests, as well as safeguard the general stability of the financial

system.

3.7 As Monetary Authorities, we have also committed ourselves to closer

and more intimate communication with the public to ensure that

there is a clear understanding of the measures we take to resolve

financial sector challenges as they arise.

4. TROUBLED BANK FUND

4.1 To safeguard and minimize disruptive medium-term liquidity

mismatches, a Troubled Bank Fund was created in December 2003,

to serve as a contingent pool from which banks that faced liquidity

challenges accessed funding to stabilize their operations.

4.2 The Reserve Bank is pleased to note that the majority of the affected

Banks are taking satisfactory measures that are reorienting their

operations back to normalcy.

4.3 As Monetary Authorities, we want to assure the banking public that

the financial sector as a whole remains safe and sound, and is ready to

continue to play the critical intermediary role between savings and

investment in the economy.

5. CONSOLIDATED SUPERVISION

5.1 Under the framework of the Consolidated Supervision, which was

rolled out in January 2004, the Reserve Bank will now license bank

17

holding companies to ensure that these structures are not abused to

indulge in speculative non-banking business at the expense of stability

at the subsidiary financial institutions.

5.2 Where a locally registered bank holding company has subsidiaries

operating in other jurisdictions, the Reserve Bank as the home

supervisory authority will have the power to demand the closure of

the cross-border activities or imposing any limitations as would be

deemed fit.

5.3 Efforts are also in progress to expand the scope of Reserve Bank

oversight to microfinance institutions.

INTERNATIONAL RATINGS

5.4 In line with global trends and the need to encourage local banks to

conform to international best practice, with effect from the 1st of

January 2005, there will be a mandatory requirement that each

banking institution be subject to an agreed international rating

framework.

5.5 Banks are therefore, encouraged to prime their operations and

systems for this critical requirement, which is also meant to

enhance the scope for easier brokerage of correspondent banking

relationships between local financial institutions and their

international counterparties.

18

6. CORPORATE GOVERNANCE

BOARD COMPOSITION

6.1 In line with international best practice on corporate governance,

there is need to strike an appropriate balance between executive and

independent non-executive directors.

6.2 Consistent with this, it is now a requirement that boards of banking

institutions have majority of independent non-executive directors.

6.3 It should be noted that an independent director is a non-executive

director who:

(a) is not a representative of a shareholder which has the ability to control

or significantly influence management;

(b) has not been employed by and has no immediate family members who

have been employed by the financial institution in an executive

capacity in the preceding three years;

(c) is free from a significant business relationship as supplier, advisor, or

customer with the financial institution or its subsidiaries.

7. SEPARATION OF OWNERS FROM MANAGEMENT

7.1 Against the background of fundamental compromises of sound

corporate governance that we have seen displayed by owner-

managed institutions, and in the spirit of promoting greater

transparency and accountability in the financial sector, no

19

shareholder with a 10% stake or more shall form part of that

institution’s management, nor Chair the Board.

7.2 Banks are expected to comply with this requirement by not later

than the 30th of September 2004.

8. RISK MANAGEMENT

8.1 The Reserve Bank will closely monitor risk management systems and

practices in the financial sector. To facilitate this, the Bank will soon

introduce amended returns to tighten the management of

exposure to liquidity and interest rate risk.

8.2 With effect from January 2004, banking institutions in Zimbabwe are

required to allocate capital for market and operational risk. This

requirement will ensure that banking institutions hold adequate

regulatory and economic capital for the full spectrum of risks they are

exposed to.

9. EARLY WARNING SYSTEMS

9.1 The Reserve Bank will soon establish a comprehensive early warning

system, which is expected to provide valuable information on

potential distressed banks for preventative measures to be taken

before the challenges at the institution materialize.

20

10 BANK INSOLVENCY AND INDIGENISATION

10.1 Questions have been raised over the last three months about the

Central Bank’s attitude towards the indigenisation of the economy

in general and the financial sector in particular with a few

stakeholders innocently misconstruing our declared intolerance of

indiscipline and swift actions against such transgressions, as

evidence that the Central Bank is anti-indigenisation.

10.2 It is not the intention of the Bank to reverse the gains of indigenisation

registered todate – anywhere in the economy and least of all, in the

financial sector.

10.3 Our proven support of and enthusiasm to have indigenous banks does

not, however, imply that we will cast a blind eye at indiscipline or

create a separate, softer banking code for one class of banks while

insisting on international best practices on others. Our view is that

being indigenous imposes an even greater responsibility, obligation

and duty towards one’s country; towards one’s depositors and

towards one’s economy, a shortcoming which a few of our brothers

and sisters running and or owning indigenous institutions seem to

have forgotten.

10.4 We thus, strongly reject the notion that tries to equate indigenisation

with unsound corporate culture, cosmetic management, technical

mismanagement and fraud. Bank insolvency brings with it

consequences that go beyond the pockets of management, Board,

shareholders and depositors. Insolvent and badly run institutions are a

21

cancer to society in which they operate and we all know what a

cancerous part of the body can do to the rest, if not cured.

10.5 Events of the last few months have demonstrated vividly the

fatality to the whole economy and depositors of creating

indigenous institutions based on falsehood declarations,

appeasement and outright blackmail.

10.6 As monetary authorities, let it be known that we will not be swayed

from the course we have chosen to follow and the message to my

indigenous colleagues in the Banking Sector is please “shape-up to

international standards or pack-up”.

10.7 Time for short-cuts or intimidation is gone and gone for good.

Our country and its people expect nothing less than honesty,

uprightness and accountability from those to whom they entrust

their hard-earned savings and to this end, no amount of emotional

weeping will persuade us to compromise standards we have set for

the sector and its players.

11. ROLE OF EXTERNAL AUDITORS

11.1 Under the on-going enhancement of greater accountability and good

corporate governance, the Reserve Bank will formalize working

relationships with financial institutions’ external auditors in line with

international best practice.

22

11.2 The current challenges being faced in the financial sector have

revealed glaring instances of creative accounting by banking

institutions which passed the test of external auditors.

11.3 Closer cooperation between the Bank and the audit firms in seen as an

indispensable requirement for success of the cleanup process.

12 MANAGEMENT OF CAPITAL

12.1 The Bank has also been disturbed by imprudent capital management

at some institutions where the bulk of capital is tied up in assets that

can not be easily liquidated.

12.2 The Reserve Bank wishes to once again remind the market that

capital has to be seen as an important fall back position to each

operation, requiring that it be kept in a form that can easily be

transformed into liquid assets.

12.3 As a guideline, the Reserve Bank is now insisting on a maximum

threshold of 25% in respect of the proportion of fixed assts to total

balance sheet size.

13. LICENSING FRAMEWORK

13.1 The Reserve Bank has noted with great concern that some newly

licensed banks have been operating with no real capital but merely

book entries or borrowed funds.

23

13.2 With immediate effect, the Reserve Bank will now require promoters

of new banking institutions to deposit their start-up capital with the

Reserve Bank, whilst valuation of their project proposal is underway.

13.3 The Reserve Bank will rigorously evaluate the capacity of promoters

and their ability to provide additional capital before the granting of a

license is done.

14. ASSET MANAGEMENT COMPANIES

14.1 The Reserve Bank assumed the role of regulator of asset management

companies with effect from 1 January 2004.

14.2 As at 31 March 2004, the Reserve Bank had received 57 applications

for registration as asset management companies.

14.3 For the majority of the applications, it has been noted that the

information submitted fell far short of what is required in terms of the

minimum guidelines sent out to the market.

14.4 Because of this, only two applicants have been duly licensed, with one

application rejected.

14.5 It is, therefore, important that applicants fully comply with the

minimum requirements so as to expedite the appraisal process.

24

15. MICROFINANCE INSTITUTIONS

15.1 The reserve Bank has also assumed the role of regulator of

microfinance institutions with effect from January 2004.

15.2 More than 700 application forms have been collected for license

renewals as well as start-ups.

15.3 By the 31st of March 2004, a total of 50 duly completed application

forms had been submitted to the Reserve Bank and were at various

stages of the appraisal process.

16. OTHER SECTORAL REVIEWS AND INTERVENTIONS

Gross National Product (GDP)

16.1 There is agreement among all stakeholders that the performance of

our key productive sectors over the past few years has been

constrained by several factors outlined in my Maiden Monetary Policy

Statement of 18 December, 2003.

16.2 Against this background, overall GDP shrunk by a cumulative 30%

over the period 2000-2003, threatening to reverse the gains from

comprehensive economic programs that Government has implemented

over the past two decades.

16.3 It is for this reason that fiscal and monetary policy priorities are

attaching great importance on bringing a quick turnaround in the

country’s productive sectors.

25

17. AGRICULTURE

17.1 Agriculture remains the backbone of the Zimbabwean economy as it

pulls strong downstream linkages with manufacturing and other

key productive sectors, both as supplier and consumer of raw

materials.

17.2 Between 2001 and 2003, production in agriculture, hunting and

fishing declined by a cumulative 26%, undermining the country’s

resolve to be self sufficient on food security.

17.3 Underperformance in agriculture exerts pressure on the country’s

foreign exchange resources through grain imports to meet internal

deficits.

17.4 As indeed a proud Nation, we need to rebuild our food reserves

and consolidate on the historic Land Reform Program, one of

whose principal objectives was to spread land ownership to the

majority of Zimbabweans, and in the process, help to alleviate

poverty, through growth and development.

17.5 Major constraints facing our agriculture today, were adequately

captured in the Utete Presidential Land Audit Commission Report

of 2003 and the majority of them have been the subject of continuous

debate and attention within and outside Government circles, and I do

not wish to repeat them in this Review.

26

18. TURNAROUND RESPONSE

18.1 Regaining momentum in agriculture requires adoption of a dedicated

program of action that confronts those identified hurdles head-on.

18.2 His Excellency the President, Cde R. G. Mugabe, in various

speeches and addresses to the Nation, has spoken about the need

to deal decisively and conclusively with these constraints inorder to

fully realise the benefit of our Agrarian Reform Program.

18.3 As part of the turnaround process, the Reserve Bank is supporting

farmers under the following intervention entry points:

(a) Working capital, equipment and infrastructure financing under the

productive sector facility. Agriculture has benefited to the tune of

Z$522.2 billion or 36.8% of total disbursements under the

concessional financing facility between January and March 2004.

An additional Z$150 billion has also been ring-fenced from the

productive sector facility to finance the targeted 2004 winter

wheat, and barley program.

(b) As Monetary Authorities however, we remain worried that the

Nation runs the risk of missing critical land preparation, planting

and/or seed-bed preparation timetables for our winter cereal crop

production and for irrigated tobacco preparations unless all

stakeholders charged with this responsibility collectively move with

speed to source and provide farmers with tillage power and/or inputs.

We believe that would it be a tragedy of enormous proportions if we

fail to turnaround our economy on the back of a promising year in as

far as the weather is concerned.

27

(c) As Monetary Authorities, we stand ready to provide through

appropriate channels funds to meet well thought out programs to

regain lost ground on the production front.

(d) In view of observed constraints associated with giving money for

inputs directly to some farmers who have found themselves tempted

to use it for other purposes distant from agriculture, the Reserve

Bank will from now onwards require banking institutions to disburse

support funds directly to input providers, with ARDA, GMB and

others designated by the State assuming a distributive role directly to

the farmer(s) concerned.

(e) Furthermore, the coming months will seek to see the proper

accounting and recovery of the Z$60 billion funds disbursed to

farmers last year through the Land Bank Capital. Important lessons

should emerge from that audit exercise.

(f) The Bank has also given birth to a vibrant market for used agricultural

equipment to ensure full utilization of existing capacity and, hence

reduce pressure on the limited foreign exchange resources which

could potentially arise from the need to import equipment.

i. The used equipment scheme, which is being administered by

private sector experts from Astra Corporation’s FARMEC

Division and the Agricultural Research and Extensions Services

(AREX), had purchased equipment worth Z$12.69 billion by

the 6th of April 2004.

28

ii. The equipment scheme also seeks to increase mechanization

and production levels on the resettled farms.

iii. Beneficiaries of the equipment will be identified by AREX,

followed by equipment deployment mechanisms based on lease

hire arrangements and declared genuine need for such

equipment at each farm.

(g) Through the External Loans Coordinating Committee, a total of

US$118 million offshore facilities, including US$9 million under the

Memorandum of Deposit (MOD) arrangement, have been approved

for the financing of this year’s tobacco purchases on the auction

floors.

(h) Pre-financing of tobacco is beneficial to the economy as it brings

forward inflows of foreign exchange well before the actual

tobacco is exported.

(e) Contract Growing of Tobacco

(i) Experiences in other parts of the world, such as Brazil, testify to the

positive impact that contract growing arrangements can have on

agricultural productivity in general, and on tobacco yields in

particular.

(ii) This notwithstanding, as Monetary Authorities, we have noted with

concern the sharp emergence of “briefcase” operators who are largely

exploiting farmers under the guise of contract growing schemes.

29

(iii) Observed limitations on these arrangements are that:

(a) Some sponsors in the contract growing schemes have tended to leave

farmers hanging in desperation by partially meeting farmers’

working capital requirements, mostly for tillage and seed

procurement, without carrying the support through the entire cycle

of the crop, and yet are quick to claim ownership of the harvested

crop.

(b) Direct abuse of the concessional financing facilities has also been

noted, where some contractors purport to be the providers of our 30%

productive sector money but would want to levy additional charges to

contracted growers, and ultimately claim ownership of the crop.

(iv) As Monetary Authorities, we urge the relevant farmer representative

bodies, and the Ministry of Agriculture and Rural Development to

educate farmers on the operational modalities of viable and mutually

beneficial contract growing schemes.

(v) We also wish to remind and guide the market that contractors can be

one or a combination of the following two forms:

(a) Technical contractors, who provide farmers with technical assistance

and know-how; and/or

(b) Financing contractors, who cover the working capital requirements of

the farmers.

30

(vi) To further enhance productivity and to promote optimal generation of

foreign exchange earnings from tobacco, the Reserve Bank has taken

the following policy positions which will apply with immediate effect:

(a) Contractors for tobacco growing should show commitment by

employing their own funds when supporting farmers.

(b) A contractor can only buy tobacco to the extent of the financial

support they have given to the growers.

(c) At least 80% of the tobacco crop to be bought under contract growing

schemes should be backed by offshore lines of credit to ensure that

the country benefits from pre-export inflows of foreign exchange.

Contractors should, therefore, twin with established merchants

who have access to such offshore lines of credit.

18.4 Food security being a strategic priority to the country, the Reserve

Bank is playing an active role in the targeted winter wheat, barley and

tobacco program for 2004/05.

18.5 Targeted hectarage set by the Cabinet Action Committee for the

winter wheat program is 100 000 ha, with an anticipated output

totalling 420 000 tonnes. As Monetary Authorities, we stand ready

to support this program as part of ensuring food self-sufficiency

and we urge banks to be time sensitive to applications from our

farmers as the weather waits for no man.

18.6 Our interventions will need to be complemented by structural reforms

in the marketing arrangements for agricultural products, as well

31

as ensuring greater capacity at the Grain Marketing Board (GMB) to

effectively interface with farmers in ways that timeously meet

their cash-flow requirements. We take note and are pleased with

recent initiatives by the GMB in this direction.

18.7 Continued impartial cooperation and swift intervention by the law

enforcement arms of Government to thwart any illegal activities on

farms involving the destruction and/or theft of greenhouse

structures, tobacco barns and curing facilities, irrigation

infrastructures, cattle/crop theft and other forms of vandalism,

would also be a critical factor in stabilizing farm productive activities

and, hence, set a solid base for a quick turnaround in agricultural

performance. We are ready to play our part with determination.

18.8 Crops such as cotton, tea, coffee sorghum, sunflower, soya beans,

paprika, flowers and other horticultural products, among others, have

been neglected in terms of their full potential and capacity to generate

foreign currency for the country. We pledge our support for farmers

in these fields and commit our attention to their expanded and more

rewarding welfare this coming season and beyond. We urge the

financial sector to invigorate their support in these areas.

19 MANUFACTURING

19.1 Major challenges facing the manufacturing sector continue to

revolve around viability issues, capacity underutilization,

unsustainable power charges and foreign currency shortages,

among others. All these shortcomings are being addressed

consciously.

32

19.2 As part of a conscious strategy to address viability concerns of

this sector, manufacturing has received the highest allotment of

the concessional financing facility.

19.3 As of end of March 2004, manufacturing accounted for Z$683.7

billion or 48.1% of the total disbursements since the beginning of

this year.

19.4 The concessional productive facility is expected to continue to

ameliorate cash flow difficulties for the sector and help sustain

current employment levels.

19.5 The establishment of the foreign exchange auction system on 12

January 2004, has also brought relative certainty on the

availability of foreign exchange, albeit in limited amounts, to

industry.

33

19.6 Weighted Contribution of Key Manufacturing Sub-Sectors

Weight%

Metals & Metal Products 22.1

Drinks, Tobacco & Beverages 19.5

Foodstuffs 13.5

Chemical & Petroleum Products 11.5

Textiles & Ginning 11.0

Clothing & footwear 6.8

Paper Printing & Publishing 6.4

Transport Equipment 3.0

Wood & Furniture 3.1

Non metallic mineral products 2.3

Other Manufactured Goods 0.8

Total 100

20. MINING SECTOR

20.1 Mining remains an important industry to the national economy,

not only in terms of contribution to GDP and employment, but

also foreign exchange generation.

20.2 Major Mineral Exports

Mineral Proportion to total mineral exports

Gold 53.7%

Asbestos 13.3%

Nickel 10.6%

Platinum 4.9%

Other 17.5%

20.3 Constraints for the Mining Sector revolve around viability issues

due to the blend foreign exchange take-home rate, rising production

34

costs, inadequate foreign currency, high labour costs and rising prices

of consumable inputs.

20.4 To lay the ground for a quick turnaround, the mining sector has

accessed Z$115.8 billion from the Productive Sector Facility which is

about 8% of the total disbursements.

20.5 Further consolidation of the Mining Fiscal Regime to complement

other incentives for this key industry is strongly recommended to

Fiscal and Mining Industry Authorities in Government.

21 TOURISM SECTOR

21.1 Tourism receipts rose by 40.4% from US$11.4 million in 2002 to

US$16 million in 2003.

21.2 Reflecting improving tourist perceptions on Zimbabwe as a safe and

attractive destination, the number of tourist arrivals has been on a

marked upward trend since 2001.

21.3 The number of tourist arrivals increased by 47.3% from 739 284 in

2002 to 1 089 256 in 2003 due to continued improvement in

international sentiment on the Country.

21.4 Tourist Arrivals into Zimbabwe (absolute numbers)

Year Number of Tourist Arrivals

2001 1 456 948

2002 739 284

2003 1 089 256

35

21.5 The Tourism sector also benefited from the Productive Sector Facility,

accessing Z$15.7 billion during the first quarter of 2004.

22. PUBLIC ENTERPRISES

22.1 The country’s major parastatals, namely Grain Marketing Board

(GMB), NOCZIM, Wankie Colliery, ZISCO, National Railways of

Zimbabwe (NRZ), Air Zimbabwe, ZBC and ZESA have also

continued to face persistent economic challenges, including:

(a) Cash-flow deficiencies, largely caused by operational constraints and

debt overhang in a high interest rate environment.

(b) Shortages of foreign currency, which have constrained importation of

essential inputs and raw materials.

(c) Limited access to external lines of credit.

(d) Deterioration of infrastructure due to limited resources for

maintenance; and

(e) Limited new investment, among others.

22.2 Successful recovery of the national economy requires that we

articulate and implement eloquent reform programs to ensure

stable and uninterrupted service delivery by these public utilities.

36

22.3 It is important that the following measures form part of the revival

process:

23. GRAIN MARKETING BOARD (GMB)

23.1 Bolstering capacity of the GMB so as to be able to timeously interface

with farmers, ensuring that payments meet the desired pre-planting

cash-flow cycles of farmers. The GMB infrastructures around the

country need to be fully utilised more than ever before.

23.2 Timely announcement of marketing prices for key crops to enable

farmers to plan accordingly as well as increase certainty in

agriculture.

23.3 Application of an aggressive program to rebuild national stocks for

strategic grain.

24. NATIONAL RAILWAYS OF ZIMBABWE (NRZ)

24.1 Capacity constraints at the National Railways of Zimbabwe (NRZ)

cannot be allowed to deteriorate further if the country’s

productive sectors are to register a quick turnaround in response

to the supportive measures being implemented.

24.2 Bulk deliveries such as coal, tobacco, minerals, cotton lint, sugar,

maize and fuel have been directly affected by the capacity constraints

at the NRZ.

37

24.3 Thus, the challenges facing NRZ are not only affecting passenger

transportation but also movement of merchandise within the country,

as well as shipment of exports and imports. The situation is made

worse by the fact that road transport for bulk consignments is

relatively more costly to producers.

24.4 NRZ cash-flow problems that have been experienced over the past

few years, have culminated in the deterioration in the availability of

locomotives and the condition of other rail infrastructure.

24.5 The net effect of the decline in capacity has been the parastatals’

failure to move business on offer and hence a further deterioration of

the cashflow and revenue position.

24.6 Based on available business NRZ requires around 108 mainline

locomotives (DE10 class) compared to about 60 currently available.

24.7 DE10 Class Locomotive Availability Year 1999 2000 2001 2002 2003

Available for use 126 112 99 83 60

Requirement 109 118 120 107 108

(Shortfall)/Surplus 17 (6) (21) (24) (48)

Source: NRZ

24.8 Unavailability of locomotives has thus seriously impacted on the

company’s ability to return foreign wagons to the owning railway

administrations especially to Spoornet (South Africa Railways). This

limitation is resulting in NRZ paying monthly interchange costs of

38

around R6 million to Spoornet, effectively eating into the country’s

limited foreign exchange resources.

24.9 The Reserve Bank, as Monetary Authorities seeks to call upon the

Ministry of Transport and Communication to support efforts on

stimulating the productive sector by urgently putting in place a rescue

package for NRZ. We record encouragement on the back of current

initiatives being pursued by both the Ministry and NRZ management

itself.

24.10 The Reserve Bank of Zimbabwe is ready to work with the Ministry in

resolving this strategic national utility.

24.11 To this end, we plan to allocate foreign currency resources for the

refurbishment and acquisition of additional locomotives for NRZ

between now and end of year depending on forex availability.

24.12 It will also be critical that management at NRZ also focus on

enhancing operational efficiencies as part of a comprehensive

framework for long-term recovery.

25. ENERGY

25.1 Successful economic revival also requires that the country vigorously

pursues measures that ensure a strong and reliable energy supply base,

particularly on electricity, coal and fuel. There is need to synchronise

the management of these important energy activities without whose

joint and collaborative efficiency our efforts to turnaround the

economy will yield zero results.

39

26. NATIONAL OIL COMPANY OF ZIMBABWE (NOCZIM)

26.1 The liberalization of fuel procurement has brought considerable relief

to the pressure on NOCZIM to meet basic market demand for fuel.

26.2 There is, however, a continued strategic importance for NOCZIM to

re-build its capacity in fuel procurement.

26.3 Deliberate efforts are being made in restoring suppliers’

confidence and to maintain trading relationships with NOCZIM.

26.4 To this effect, the Reserve Bank has been in the forefront of

supporting the Ministry in negotiations with international creditors

with outstanding NOCZIM payments for fuel. These joint efforts are

expected to restore the creditworthiness of the strategic oil company

in international markets for the benefit of our economy.

26.5 The Reserve Bank is also pleased to share with stakeholders that

through tireless negotiations with international partners, NOCZIM has

entered into a joint venture investment to set up bulk oil storages and

a marketing arm in Mozambique. This investment is expected to

further stabilize the country’s fuel situation over the medium to

long-term.

26.6 Fuel Importation

(a) Stability in fuel availability to the productive sectors and the general

public is an indispensable requirement for successful economic

revival.

40

(b) In an effort to rationalize foreign exchange resources available, on 8

April, 2004, Authorized Dealers were directed to ensure that Direct

Fuel Importers (DFIs) utilize their FCA balances for own-use fuel

importation needs, so as to enable licensed fuel importers who import

to sale to the public, to be accommodated on the foreign exchange

auction.

(c) The Reserve Bank impresses upon Authorized Dealers to exercise

attentive scrutiny when processing foreign exchange bids for fuel

imports before passing them to the foreign exchange auction.

27. ZIMBABWE ELECTRICITY SUPPLY AUTHORITY (ZESA)

27.1 Stability in electricity supply is a critical requirement for a successful

economic turnaround program.

27.2 Ageing of generating equipment, as well as growing demand for

electricity has meant that Zimbabwe continues to be a net importer of

power to meet demand.

27.3 Against the background of foreign exchange shortages, ZESA has,

over the past few years experienced a build-up of foreign payment

arrears in respect of suppliers’ credits.

27.4 In an effort to steer the economy’s productive sectors onto a faster

growth path, particularly exports, it has become necessary that an

informed review of the performance of the dispensation that was

41

given to ZESA to bill exporters in foreign currency at source be

carried out with a view to making the arrangements more effective,

efficient and at the same time more friendly to exporters from a

logistics and uniformity point of view.

27.5 We are pleased with the understanding, cooperation and sensitivity

which ZESA has displayed over recent negotiations with consumers

which has led to significant reductions in the tariff structures without

impacting too adversely on its operational plans.

27.6 We are happy to have played a modest but supportive role to ZESA

and the consumers in our quest to balance the viability aspirations of

all parties concerned. The cooperation between us and ZESA is a

source of encouragement.

27.7 It is now thus critical that, as part of commitment to the turnaround

program, producers and providers of other goods and services reflect

these energy adjustments in their pricing structures so as to benefit the

economy through favorable trickle down effects on inflation.

28. HWANGE COLLIERY

28.1 Operational constraints, accentuated by ageing equipment and

limited foreign exchange to import spare parts have significantly

caused shortages of coal to the productive sectors.

28.2 As a result, a number of industrial and agricultural processes

requiring coal as an important source of energy are being

adversely affected.

42

28.3 Unavailability of adequate coal supplies is also limiting the

generation of electricity at Hwange Thermal Power Station,

further hampering the economic turnaround program.

28.4 The Reserve Bank, in close consultation with the Ministry of Energy

and Power Development and ZESA will put together a financing

package to enable participation by ZESA in coal mining activities to

enhance the strategic input-output synergies of coal production and

power generation.

28.5 The export incentives enunciated in this Statement are also expected

to increased foreign exchange inflows on the auction, which should

give the Reserve Bank leg-room to accommodate foreign exchange

requirements of Hwange Colliery to smoothen production during the

course of the year.

29. TELECOMMUNICATIONS

29.1 An effective telecommunication network is an important ingredient to

sustainable economic production.

29.2 To this end, greater efforts will be put on expanding and strengthening

this sector.

29.3 This would broaden the benefits the economy is already deriving from

wider participation in the provision of communication services,

following the liberalization of this sector by Government.

43

30. EXPORT PROMOTION: BACKGROUND

30.1 Government, through the 2004 Fiscal Budget and the State of the

Nation Address by His Excellency President R. G. Mugabe,

acknowledged the important role that our exporters play in the

economy and alluded to the need for this sector to be promoted in

order to generate more foreign currency for the country.

30.2 The December 2003 Monetary Policy Statement sought to achieve the

same through complementary policies.

30.3 Before coming to the new measures, it is important to point out that

Japan, Malaysia and other South East Asian countries once faced

similar foreign currency generation challenges if not worse than

our own situation.

30.4 But through carefully planned and executed policies, they emerged

stronger from their weaknesses than before. Zimbabwe can do the

same.

30.5 Smarting from devastation after the Second World War, Japanese

economic writers point out that “Japan succeeded beyond

expectations in developing and executing an export-driven, high-

growth economy on the back of its highly educated and dedicated

population. It soon became the world’s first “economic” miracle

after the Second World War despite its limited land resources,

zero mineral base and none of the other resources we take for

granted here.

44

30.6 The Economists point out that the world got to know post-war Japan

through its exports of electronics, cars and other high value-added

products. World policy makers also got to know of Japan through

its trade surpluses.1”

30.7 The same is the status now reached by China.

30.8 In Zimbabwe, we have land in abundance, are well endowed with a

variety of mineral deposits, wonderful climate and tourist

destinations, a developed and now disciplined financial sector and

functioning telecoms infrastructure, a capable manufacturing

sector and a highly educated population, all key ingredients for a

successful export-led growth strategy

30.9 One third of our population is “export intellectual property” which can

blend with those back home to make this country a jewel of Africa

that it deserves to be. Zimbabweans in the diaspora will always

remain Zimbabweans, with Zimbabwean roots, tastes, aspirations and

love for their country. As Monetary Authorities we cherish their

temporary existence wherever they are and invite them to contribute

ideas to the turnaround of this economy.

30.10 The world should get to know Zimbabwe better through our

agricultural and mineral exports, through value-adding manufacturing,

through visits to our tourist destinations and through the hard work

and dedication of our brothers and sisters in the diaspora..

30.11 Measures presented below are meant to kick-start and sustain this

drive towards foreign currency self-sufficiency.

45

30.12 Whereas Japan and other successful countries now have to “import

first in order to export”, the stage at which we are as a country

requires that we “export first in order to import”.

30.13 For us to succeed with this “export-first-and-import-later”

philosophy, we need as a country to have a PARADIGM Shift.

30.14 This paradigm shift is necessary given what has taken place in the

area of land reform, tourism, manufacturing, and other sectors of the

economy.

30.15 We have to make do with the post-land reform Zimbabwe of the new

millennium, a Zimbabwe that finds itself without many external

sources of foreign exchange support and a Zimbabwe which has to

rely primarily on itself first before looking for outside help.

30.16 If we had lines of credit in abundance we could afford to play hide

and seek games with our exporters, with our farmers, our tourism

players, manufacturers, miners and the financial sector but then, we

do not. This is what I mean by the need for a paradigm shift.

30.17 It is against this background that the following measures are being

implemented for the benefit of exporters.

46

31 EXPORT SUPPORT SCHEMES

31.1 The export-support measures presented in this Monetary Policy

Statement have been stress-tested for their fiscal neutrality.

31.2 As Monetary Authorities, we are thus convinced that the incentives

we are putting in place will not have adverse effects on the fiscus, as

the support framework has largely been guided by expected self-

financing export supply response, as well as beneficial exchange rate

effects on fiscal revenues.

31.3 Details of this fiscal neutrality of the supportive measures were shared

and discussed with relevant Authorities in the Ministry of Finance and

Economic Development.

CARROT AND STICK EXPORT RETENTIONS SCHEME

31.4 Advance Payments (a) In order to encourage exporters to timely acquit their export proceeds,

for all advance payments or prepayment proceeds, exporters are

currently allowed to retain 80% in their FCAs and the remaining

20% is sold to the Government at Z$824 per US dollar.

(b) In light of the significant impact on productivity of early repatriation

of foreign exchange, the carrot and stick incentive on advance

payments or prepayments has been enhanced to allow exporters

to retain 80% in their FCAs and to sell 20% at the ruling auction

rate.

47

(c) These retention levels will also apply to Tourism operators and

will enable use of a single rate and certainly address accounting

and billing problems currently being experienced in the tourism

industry, especially with regard to use of international credit cards.

31.5 BULK AND CONSIGNMENT EXPORTS

(a) Currently, in terms of Exchange Control Directive RE: 511, dated 24

December 2003, all companies exporting in bulk or on a

consignment basis and acquit their Form CD1s beyond 120 days,

are required to surrender 100% of their export receipts, of which 75%

is immediately sold to the auction and 25% surrendered to

Government at the rate of Z$824 against the US dollar.

(b) In order to recognize logistical constraints inherent in bulk shipments

and consignment exports and not to prejudice such exporters for

whom shipping delays are inevitable, exporters of approved

extensions beyond 120 days will be allowed to retain 30% (as

opposed to the current 0%) in their FCA’s, while 45% is required

to be immediately sold to the auction at the ruling auction rate

and 25% surrendered to Government at the rate of Z$824 against

the US dollar.

48

31.6 The Carrot and Stick Approach Scheme Will Now Be As Follows:

Form CD1, TR1,

TR2, CD3

Acquittal Period

(Days)

FCAs

Retention

Sold for

Government

Use (at

Z$824/US$)

Sold to Auction

(At ruling Auction

rate)

Prepayments 80% 0% 20%

1-30 70% 25% 5%

31-60 65% 25% 10%

61-90 55% 25% 20%

Exchange Control Approved Extensions

91-100 50% 25% 25%

101-120 40% 25% 35%

121 and above 30% 25% 45%

15% FOB Export Incentive Scheme

31.7 In an effort to maximise the attractiveness and effectiveness of this

scheme to exporters, following the implementation of the on-line

Form CD1 Computerised System at the Reserve Bank, measures have

been put in place to ensure that there are no delays in the issuance of

duty free certificates.

31.8 In this regard, the turn-around time for exporter’s applications to

Exchange Control relating to this and other export incentive schemes

has been reduced from 14 days to 5 working days.

31.9 In addition, for exporters to get immediate value from this Export

Incentive Scheme, the duty free certificates, which are tradable, will

49

now be extended to cover any payments to ZIMRA.

31.10 Currently the 15% FOB incentive scheme is based on the 75%/25%

blend exchange rate.

31.11 To further enhance exporter viability, the 15% FOB value will be

based on the ruling auction rate.

31.12 Waiver on Surrender Requirements on Incremental Exports

(a) Currently, the incremental value is being calculated on a quarterly

basis. For exporters to get a much faster realisation of the benefit of

the waiver on the surrender requirements on incremental exports and

to enhance its effectiveness to exporters demonstrating a progressive

growth in export volumes, the incremental value of exports will now

be calculated on a monthly basis.

31.13 Access to the Auction

(a) Exporters and non-exporters are currently accessing foreign currency

on the Auction system twice weekly and the amount which has been

on offer has to date averaged US$16 million per week. We remain

alert to the need to review both the frequency of auctions and the

amount available as inflows improve in line with the broad measures

herein contained.

50

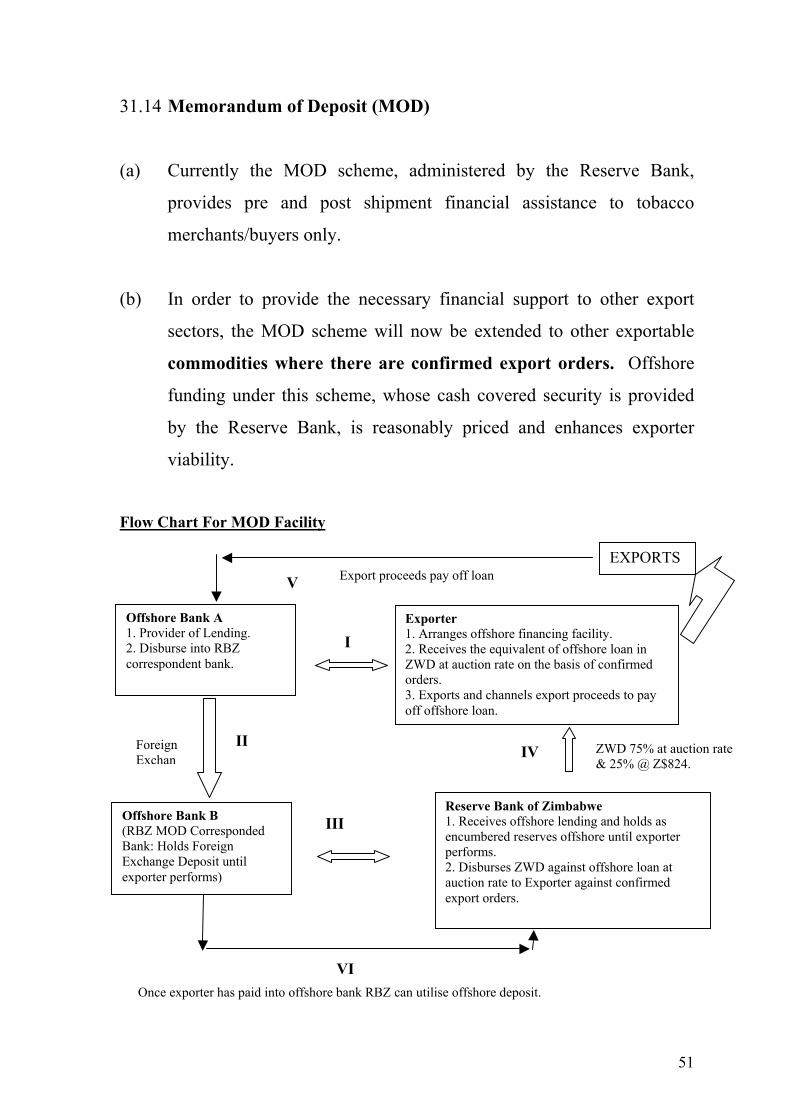

31.14 Memorandum of Deposit (MOD)

(a) Currently the MOD scheme, administered by the Reserve Bank,

provides pre and post shipment financial assistance to tobacco

merchants/buyers only.

(b) In order to provide the necessary financial support to other export

sectors, the MOD scheme will now be extended to other exportable

commodities where there are confirmed export orders. Offshore

funding under this scheme, whose cash covered security is provided

by the Reserve Bank, is reasonably priced and enhances exporter

viability.

Flow Chart For MOD Facility

Offshore Bank A 1. Provider of Lending. 2. Disburse into RBZ correspondent bank.

Offshore Bank B (RBZ MOD Corresponded Bank: Holds Foreign Exchange Deposit until exporter performs)

Reserve Bank of Zimbab1. Receives offshore lendinencumbered reserves offshperforms. 2. Disburses ZWD against auction rate to Exporter agexport orders.

Once exporter has paid into offshore bank RBZ can utilise offshore deposit.

III

Exporter1. Arranges offshore financing facility. 2. Receives the equivalent of offshore loan in ZWD at auction rate on the basis of confirmed orders. 3. Exports and channels export proceeds to pay off offshore loan.

EXPORTS

I

IV

Export proceeds pay off loan

II

ZWD 75% at auction rate & 25% @ Z$824.

V

we g and holds as ore until exporter

offshore loan at ainst confirmed

VI

Foreign Exchan

51

31.15 Measures will be put in place to ensure that the impact on money

supply growth is kept at a minimum.

31.16 Exporters’ post shipment foreign currency bills

(a) For those exporters who have no access to offshore lines of credit, and

hence can not access the MOD incentive, the Reserve Bank has

introduced post shipment foreign exchange bills whose features are as

follows:

• The bills will be issued on the basis of actual export shipments.

• The bills would be issued on 50% of the free on board (FOB) value of

shipments.

• The maximum tenor of the bills will be 90 days.

• The interest rate on the bills will be LIBOR + 5 percentage points.

(b) The operational modalities of this incentive would be as follows:

• Once an exporter has a confirmed export order, they apply for

the bills through their bankers.

• On shipment, and upon meeting of the normal credit requirements of

banks, the exporter draws the bills up to 50% of the FOB value on the

form CD1 and CD3 at the ruling auction rate.

52

• The Reserve Bank would disburse the Zimbabwe dollar equivalent to

the exporter to meet post shipment working capital requirements.

• On acquittal of the CD1s and CD3, after conforming to the existing

surrender requirements, the exporter would liquidate the bills –

principal plus interest.

31.17 Detailed operational modalities of this facility will be sent out to

Authorised Dealers and the market before the 30th of April 2004.

Flow Chart for exporters post shipment foreign exchange bills

25% @ auction rate Point A 50% FCA Exporter gets confirmed Orders 25% @ Z$824

Point B Point E Exporter applies through own bank After at most 90 days f or post shipment bills Exporter acquits CD1s and p ays off loan. Point C Point D Exporter ships exports RBZ disburses 50% of FOB value on CD1 @ auction rate. Loan at Libor + 5 percent points

31.18 Tobacco support price

(a) The MOD facility and the post shipment foreign exchange bills will

benefit direct exporters. In order to support tobacco growers who

export through the intermediation of tobacco merchants and

processors, the Bank has introduced a tobacco support price of

Z$750.00 (seven hundred and fifty Zimbabwe dollars) per kg.

53

(b) This facility, which will be administered by the Reserve Bank, would

be financed through incremental fiscal revenue from the increase

in import duty arising from use of the auction rate, complemented

by ring-fenced resources from cash flows arsing from repayments

under the concessional financing facility.

31.19 Operational modalities of this facility will be sent out to the market

within two days time from date of this announcement.

31.20 Reserve Bank Foreign Exchange Purchasing Centres

(a) In order to optimise foreign exchange inflows into the foreign

exchange pool, the Reserve Bank will soon open foreign exchange

purchasing centres at designated entry points into the country.

(b) I am pleased to report that a feasibility study for implementation

of this project has already been completed, and we are geared to

roll out the project not later than 30 June, 2004.

32. FORM CD1 NON-ACQUITALS

32.1 On two occasions, December 2003, and February 2004, the Reserve

Bank published a list of 320 companies whose form CD1 records at

Exchange Control indicated non-acquittals amounting to US$175

million.

54

32.2 Following this publication, and after intensive follow-ups with the

affected exporters, about 220 companies responded positively to the

Reserve Bank’s call for acquittal of overdue export receipts.

32.3 To date, from non-acquittals of US$175 million, a total of US$124

million (71%) has been fully accounted for, of which:

• US$89 million was on account of non-acquittals due to

administrative shortfalls, between exporter, receiving bank and

the Reserve Bank of Zimbabwe. The loopholes in this area

have been plugged to avoid repeat shortfalls.

• US$21 million was received by the Reserve Bank as foreign

currency cash regularising non-acquittals.

• US$14 million has been pledged by the affected exporters for

receipt as foreign currency cash by the 30th of April 2004.

32.4 Over 110 exporting companies with long outstanding export receipts

totalling US$36 million did not respond to the Reserve Bank’s call to

acquit their proceeds.

32.5 These cases are at various stages of prosecution.

32.6 As stakeholders, it is in our collective interest to move the economy

onto the recovery path through mutual cooperation. I therefore urge

exporters to ensure timely acquittal of their CD1s for our efforts

to bear fruits.

55

33 MOBILISATION OF DIASPORA FUNDS

33.1 In the 2004 National Budget, Government recommended that the

country enhances foreign exchange availability through appropriate

instruments and structures to attract foreign exchange from

Zimbabweans in the Diaspora.

33.2 With a total estimate of around 3.4 million Zimbabweans in the

Diaspora, the opportunity to unlock considerable foreign

exchange inflows via this avenue is huge.

33.3 In order to tap into this contribution to national development by our

fellow Zimbabweans in the diaspora, the Reserve Bank has put in

place an effective, and secure administrative, operational and legal

framework for the mobilization of foreign currency from the

Diaspora.

33.4 Under the new arrangements, foreign currency remittances from the

Diaspora shall be channeled through formal channels of Money

Transfer Agencies that will be licensed in terms of the recently

gazetted Exchange Control (Money Transfer Agencies) Order 2004.

33.5 The new foreign currency mobilization framework allows

beneficiaries of such funds in Zimbabwe to receive payouts in

foreign currency cash, travelers cheques, bank drafts or local

currency at a diaspora floor price of Z$5 200.00 or the auction price

which ever is higher.

56

33.6 Money Transfer Agencies paying out in local currency shall be

doing so for and on behalf of the Currency Exchange and foreign

exchange mobilized through these arrangements shall be available

to the auction. These resources are expected to boost foreign

exchange supply to the auction and enable the financing of more

transactions.

33.7 In addition to offering a market related exchange rate through the

auction, or at the diaspora floor price, whichever is higher, the

new money transfer arrangements have an added advantage of having

been developed in line with existing international standards and

are guided by the need to ensure high-level security for remitted

funds, efficiency in transmission and convenience to both senders

and beneficiaries.

33.8 The Reserve Bank has already invited new and existing Money

Transfer Agencies to apply to Exchange Control to participate under

these new arrangements and as at 20 April, 2004, the following

Money Transfer Agencies (Institutions) had been licensed with more

applications still being considered for licensing:

• Standard Chartered Bank

• Stanbic Bank

• CFX Merchant Bank-Money Gram

• Barnfords Global Financial Services

• Fredex Financial Services (Pvt) Ltd

• Kingdom Bank (Currency King Money Transfer)

• TransAfric Money Transfer

• POSB

57

33.9 As an incentive for Zimbabweans in the Diaspora to send money

home, the Reserve Bank has waived the charging of commissions

by money transfer agencies. This means that for all foreign currency

remittances made through this facility, beneficiaries in Zimbabwe

will be paid the full amounts converted at the ruling auction rate

or at the diaspora floor price of Z$5 200/US$, which ever is

higher.

33.10 Other innovative telecom-based money transfer systems are in the

process of being developed and their introduction will be announced

in due course.

BROKERAGE FEES

33.10 For their brokerage services, money transfer agencies will be paid

agency fees of 1,5% for every unit of foreign currency delivered to the

Reserve Bank. This brokerage fee level will be reviewed at the end of

each quarter and a volume (value) incentive given to Money Transfer

Agencies based on the quarter’s cumulative transfers to the Reserve

Bank.

33.11 The current commission arrangements for Authorized Dealers

stands at 0.5% and is paid by the customer selling foreign exchange.

33.12 To enhance viability of authorized foreign currency dealers and level

the playing field with money transfer agencies, the Reserve Bank will

now pay Authorized Dealers (Banks) an additional 1% for every unit

of foreign currency delivered to the Reserve Bank.

58