50

THE FOREIGN EXCHANGE MARKET AND EXCHANGE RATES

| Date post: | 02-May-2017 |

| Category: |

Documents |

| Upload: | sanjay-adhikari |

| View: | 232 times |

| Download: | 3 times |

THE FOREIGN EXCHANGE MARKET AND EXCHANGE

RATES

Exchange rate…

• …is the price of one money in terms of another.

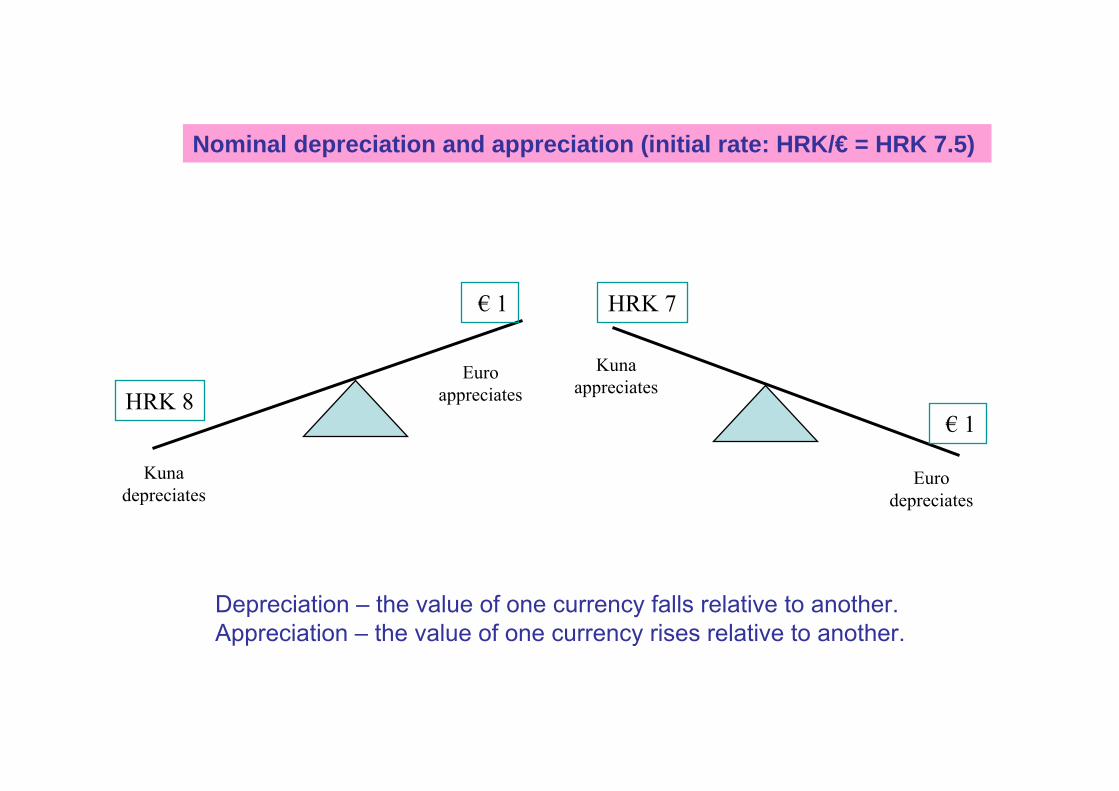

HRK 7

€ 1

Kuna appreciates

Euro depreciates

HRK 8

€ 1

Kuna depreciates

Euro appreciates

Nominal depreciation and appreciation (initial rate: HRK/€ = HRK 7.5)

Depreciation – the value of one currency falls relative to another.Appreciation – the value of one currency rises relative to another.

Foreign exchange market (FOREX market)

Foreign exchange market can be divided into 3 parts: inter-banks market, forward market and electronically connected network. Big commercial banks, brokers, central banks and multinational companies.

We differ SPOT and FORWARD markets.

Spot exchange market – where currencies are traded for current delivery.Forward exchange market – where currencies may be bought and sold for delivery in a future period.

Central bankCentral bank

BrokerBroker BrokerBroker BrokerBroker BrokerBroker

BankBank BankBank BankBank BankBank BankBank BankBank BankBank

BankBank‘‘ss clientsclients

Foreign exchange market organization

Foreign currency supply

Foreign currency demand

Foreign currency supplyForeign currency demand

Foreign

currency

supply

Foreign

currency

demand

Equilibrium and disequilibrium market exchange rate

D

S

Rate, E(α/β)

Quantity of β

E

Currency αdepreciates

Currency αappreciates

E1

Supply and demand on foreign exchange market and equilibrium exchange rate

E (α/ β)

D

E’’

E

E2

E4

Quantity of β0

D’

S

S’

E1

E3

E’

Supply and demand curves movement and equilibrium exchange rate

Hedging

• An activity to offset risk.• The forward exchange rate exceeds the spot

rate – FORWARD PREMIUM (depreciation of the currency is expected).

• The forward exchange rate is less than the spot rate – FORWARD DISCOUNT (appreciation of the currency is expected).

Types of foreign-exchange risk

1. Translation (accounting) exposure – the difference between foreign-currency-denominated assets and foreign-currency-denominated liabilities.

2. Transaction exposure – resulting from the uncertain domestic currency value of a foreign-currency-denominated transaction to be completed at some future date.

3. Economic exposure – the exposure of the value of the firm to changes in exchange rates. It is concerned with the sensitivity of the real domestic-currency value of long-term cash flows to exchange rate changes.

What makes exchange rate change?

• Long-term and short-term factors.

Long-term factors:

Decrease of the price level in country relative to the price levels in other countries causes appreciation of its currency. Productivity increase in country relative to other countries leads to greater demand for home currency which leads to the increase in nominal and real exchange rate of that currency. Change of the households and companies preferentions towardsforeign or home goods leads also to the change f the exchange rate.Inflation rate change influences the nominal exchange rate.Trade barriers increase demand for home currency and in the longrun lead to higher exchange rate for the country which introducedbarriers.

Parities1. Relative inflation rates2. Forward rates3. Interest parities

Balance of payments1. Current account2. Portfolio investment3. FDI4. Exchange rate regimes5. Official international reserves

Capital market1. Relative interest rates2. Expected economic growth3. Capital supply and demand4. Political stability5. Speculations and liquidity6. Political risks and control

Spotrate

Factors of the forming spot exchange rate

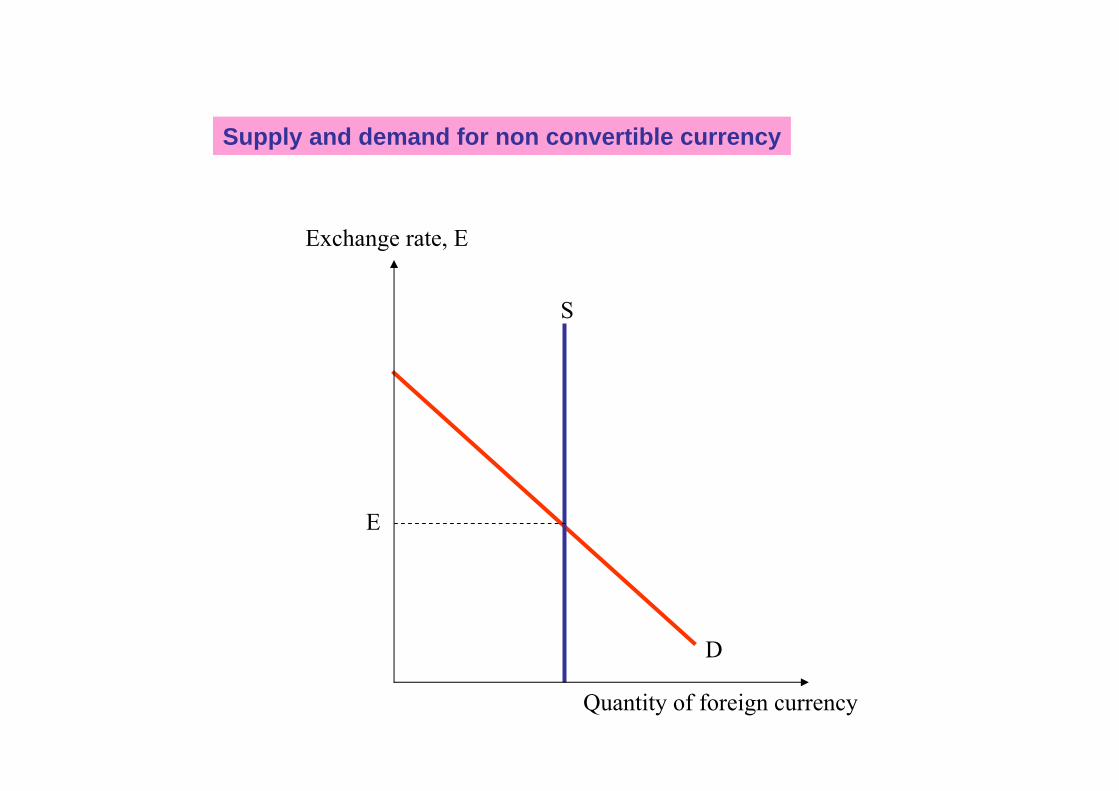

Currency non convertibility

Non convertible currencies – can not be freely exchanged for other currencies. Not tradable on foreign exchange market.

Exchange rate, E

Quantity of foreign currency

D

S

E

Supply and demand for non convertible currency

Exchange rate, E

Quantity of foreign currency

D1

S

E1

E2

Exchange currency deficit

D2

Increase in demand for non convertible currencies

Home inflation rate can be higher than foreign inflation rate due to expansive policy. Considering that nominal rate is fixed, real exchange rate depreciates (home currency appreciates), imports is relatively cheaper i home demand increases, increases demand for foreign currency which leads to excess demand for foreign currency in accordance with fixed rate and exchange currency deficit.

Exchange rate, E

Quantity of foreign currency

D1

S1

E1

E3

Exchange currency

deficit

D2

S2

1 23

Decrease in supply for non convertible currencies

Additional problem is the fact that exports decreases and foreign currency supply decreases which comes from exports. The lack of foreign currency becomes even bigger.

The real exchange rate

1. Absolute purchasing power parity;2. Relative purchasing power parity;3. Real exchange rate as the price ratio between

tradable and non tradable goods;4. Monetary theory;5. Interest rate parity (covered and uncovered);6. Efficient foreign exchange market and forward

exchange rate;7. The balance of payments equilibrium.

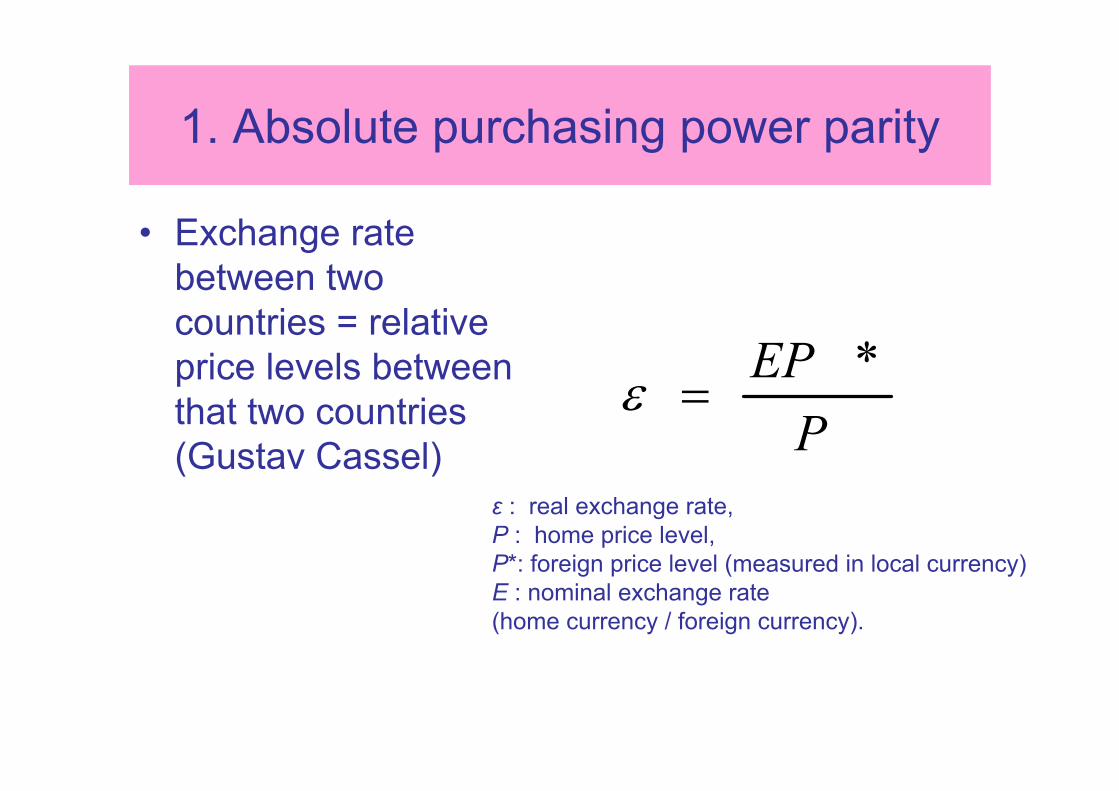

1. Absolute purchasing power parity

• Exchange rate between two countries = relative price levels between that two countries (Gustav Cassel) P

EP *=ε

ε : real exchange rate,P : home price level,P*: foreign price level (measured in local currency)E : nominal exchange rate (home currency / foreign currency).

2. Relative purchasing power parity

• Percentage change of the exchange rate between two currencies in certain period is equal to the difference between percentage change of the national price level in accordance to the basic period.

t

s

dt EE ⎟⎟

⎠

⎞⎜⎜⎝

⎛++

=ππ

11

0

Et = spot rate in time t E0 = spot rate in basic periodπd = home inflation rateπs = foreign inflation rate

•Currency with higher inflation rate is expected to depreciate.

% change of the foreigncurrency spot rate

Difference betweenexpected inflationrates (foreign and

home)

2

4

-5

-4

-1-3 -1-4 -2 2 41 3 5

3

1

-2

-3

-6 6

PPP line

P

Difference betweenexpected inflationrates (foreign and

home)

% change of the foreigncurrency spot rate

R

Relative Purchasing Parity

All points on the line show relative purchasing power parity because difference between foreign and home inflation rate suits percentage change of the exchange rate.

Total production

Tradable goodsNon tradable (local) goods

Export goods Import goods

Tradable and non tradable goods

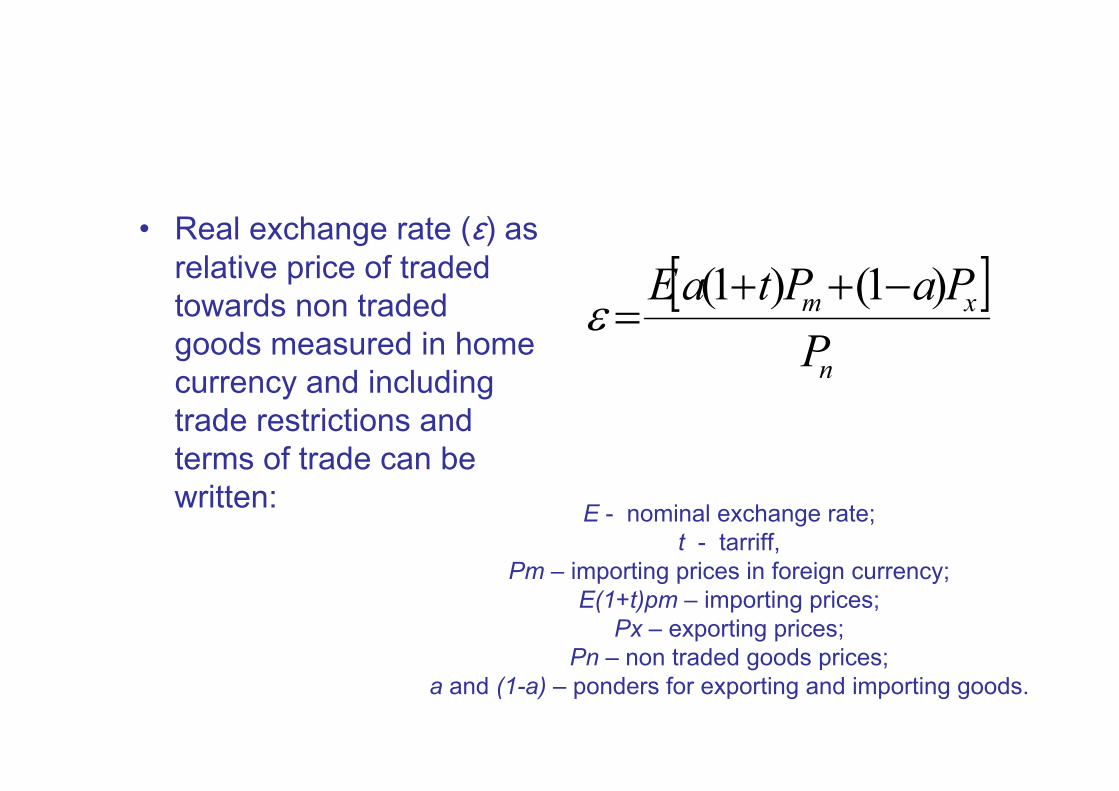

3. Real exchange rate as the price ratio between tradable and non tradable goods

•Real exchange rate is the relative price between tradable and non tradable goods.

Non

trade

dgo

ods

Traded goods

Real exchange rate= T/NT

T

NT EA

Real exchange rate as the price ratio between tradable and non tradable goods

The price ratio between traded and non traded goods can be divided into two price ratios: importing/non traded and exporting/non traded.

• Real exchange rate (ε) as relative price of traded towards non traded goods measured in home currency and including trade restrictions and terms of trade can be written:

[ ]n

xm

PPaPtaE )1()1( −++

=ε

E - nominal exchange rate;t - tarriff,

Pm – importing prices in foreign currency;E(1+t)pm – importing prices;

Px – exporting prices;Pn – non traded goods prices;

a and (1-a) – ponders for exporting and importing goods.

• Appreciation of home currency as a consequence of the faster growth of prices in non tradable sector leads to competitiveness decrease and tradable sector output decrease.

• If it is not possible to decrease the growth of prices of the non tradable sector for establishment internal and external balance then real depreciation (devaluation) is needed.

TradableTradable sectorsector outputoutput

TradeTrade deficitdeficit

Wages in non Wages in non tradable sectortradable sector

Macroeconomic equilibriumMacroeconomic equilibrium

Non tradable sector Non tradable sector equilibriumequilibrium

00

Equilibrium between tradable and non tradable sectors

If the production for export and production of imports substitutes is stimulated by real exchange rate, than the macroeconomic equilibrium curve will move to the right increasing economic activity, output, employment and wages in the middle and long run.

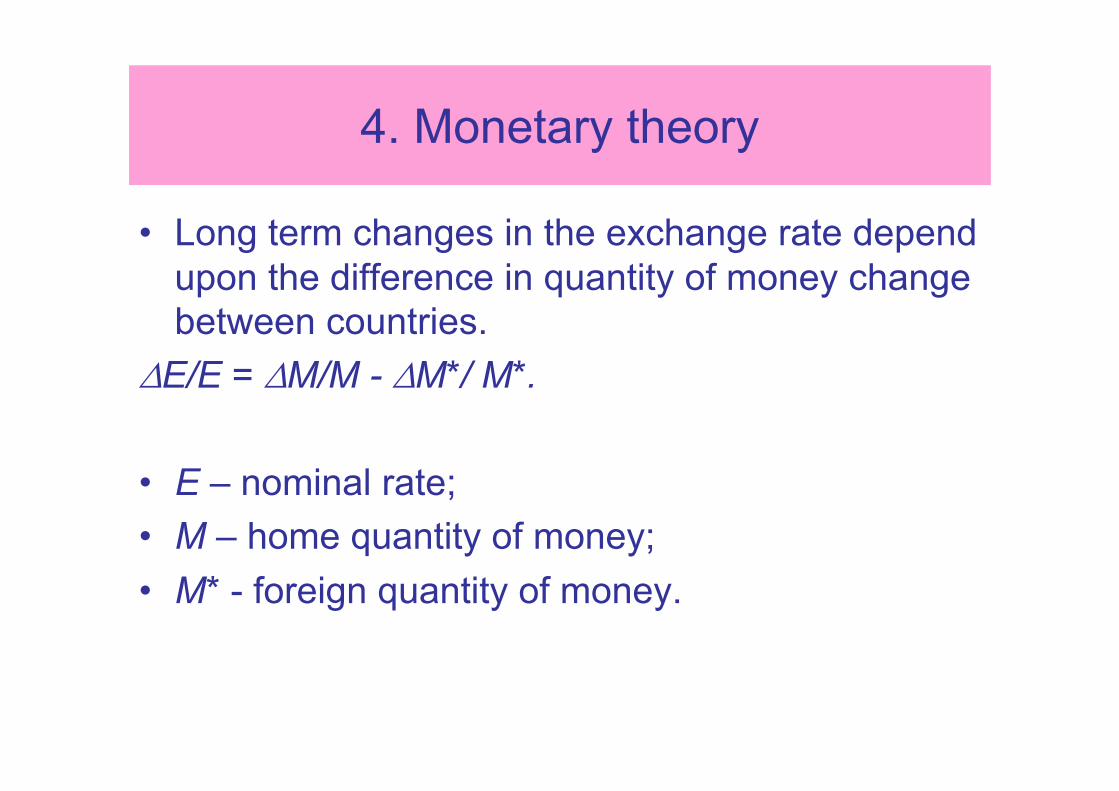

4. Monetary theory

• Long term changes in the exchange rate depend upon the difference in quantity of money change between countries.

∆E/E = ∆M/M - ∆M*/ M*.

• E – nominal rate;• M – home quantity of money;• M* - foreign quantity of money.

• Exchange rate and quantitative theory of money

• E = M*/M x Y/Y* x V*/V.

MS1

Quantity of money

MS2

i2

i1

Inte

rest

rate

MD

MS1

Quantity of money

MS2

i2

i1

Inte

rest

rate

MD

Money supply and interest rate

Increase of M Decrease of M

Pd2

t0

(a) Money supply, MS

time

(c) Price level in country, Pd

time

(b) Home interest rate, id

time

M1

t0t0

i1d

M2

Pd1

t0

i2d

E2α/β

(d) Exchange rate, Eα/β

time

E3α/β

E1α/β

Time adjustment after increase of money supply

Exchange rate, E (α/β)

E3

E1

E2

E1

E2

E3

S1

S2

D1

D2

Quantity of β

0

Short term, Smaller elasticity

Long term, Bigger elasticity

Short term and long term equilibrium: exchange rate overshoot

We have exchange rate overshoot when its current respond to the disturbance is bigger than its long term respond.

E

Long term equilibrium

exchange rate

Middle term cyclical path

Short term overshoot

Time

Difference between long term and short term trends

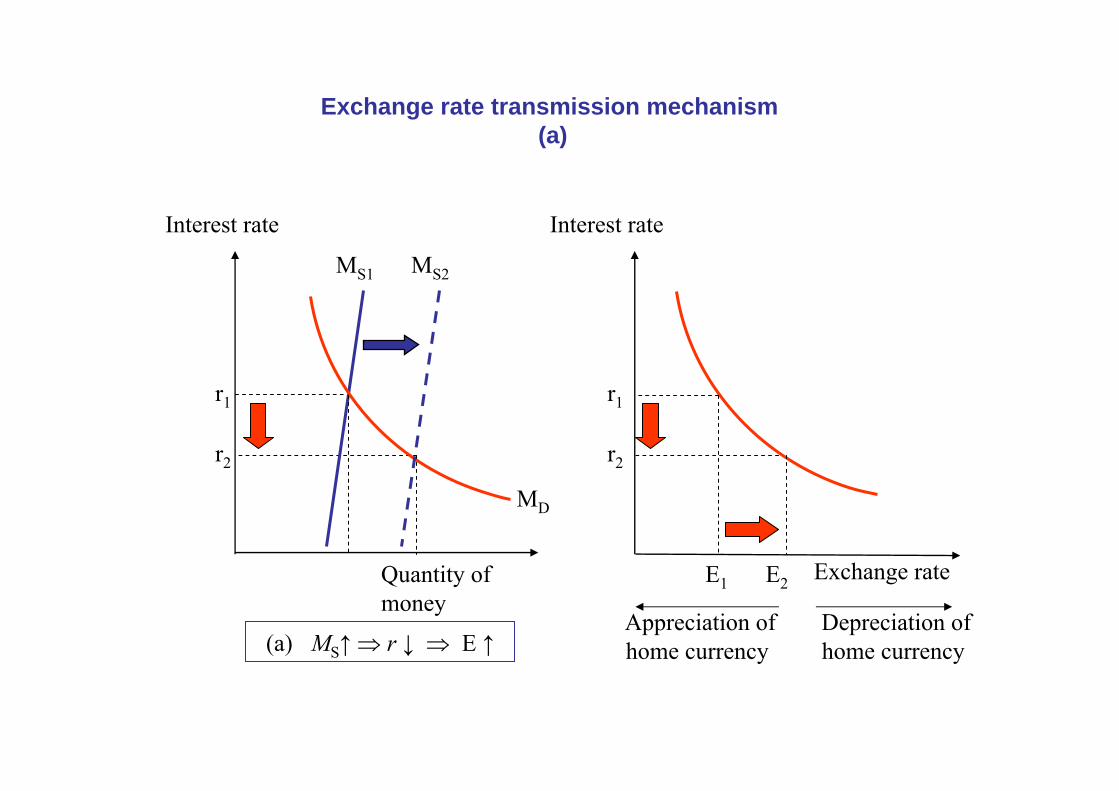

MS1

Quantity of money

MS2

r2

r1

Interest rate

MD

E2E1 Exchange rate

Interest rate

r2

r1

Appreciation ofhome currency

Depreciation ofhome currency(a) MS↑⇒ r ↓ ⇒ E ↑

Exchange rate transmission mechanism (a)

Imports, M

Exports, X

E1

E2

Exchange rate, E

M1 GDPM2 X1 X2

(b) E ↑⇒ M ↓ , X ↑⇒ Y ↑

E1

E2

Exchange rate, E

I+X1

Y1 Y2

I+X2

S+M2

S+M1

Exchange rate transmission mechanism(b)

MD = MS; Central bank influences

interest rate

Interest rate influences capital movement and

exchange rate

Exchange rate

determines net exports

Macroeconomic equilibrium determines price level and

real GDP

Interest rate determines investment

Monetary transmission mechanism

5. Interest rate parity theory

• Interest rate parity – the forward premium or discount is equal to the interest differential.

• Covered and uncovered interest rate parity.• Uncovered interest rate parity – the expected change in

the exchange rate is equal to the interest differential.

Time

r,i

t0

Real interest rate

Nominal interest rateIn

tere

st ra

te

Adjustment of the nominal and real interest rate to the increase of the money supply

Real interest rate = nominal interest rate – inflation rate.(Fisher equation: the nominal interest rate is equal to the real interest rate plus expected inflation.)

MS1

Quantity of money

MS2

i2

i1

Interest rate

MD

Money supply and nominal interest rate in short term

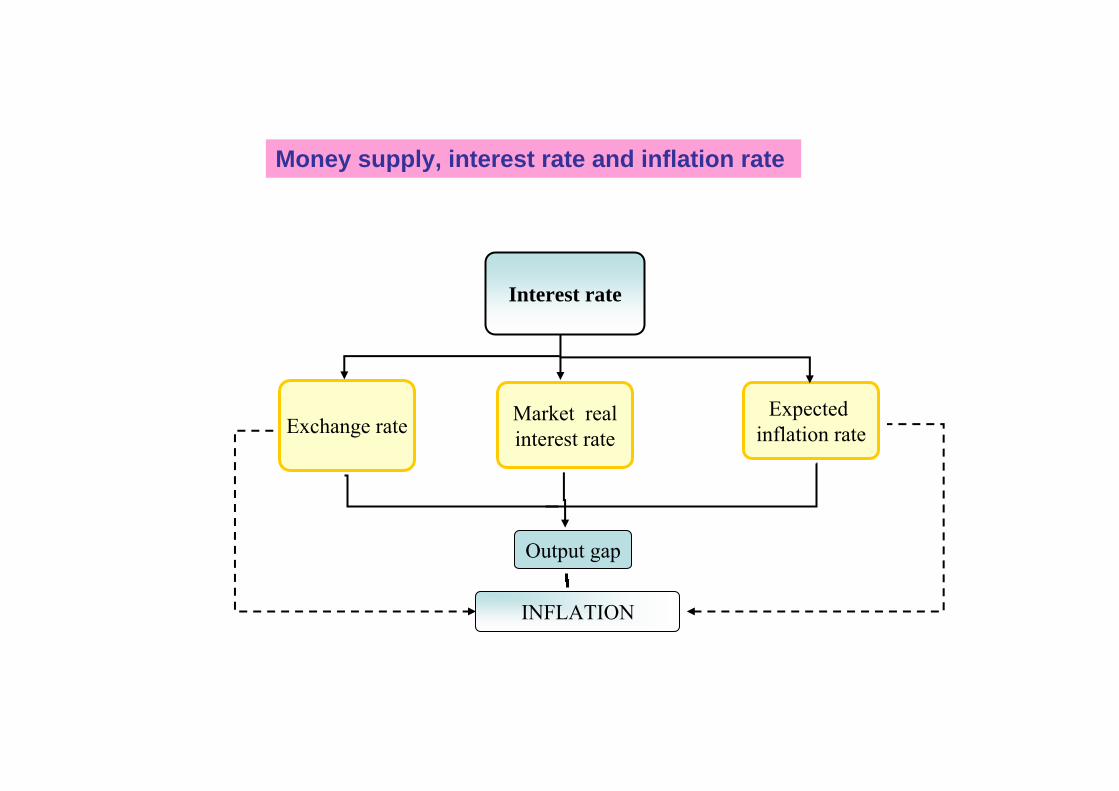

Expected inflation rate

Interest rate

Exchange rate Market realinterest rate

Output gap

INFLATION

Money supply, interest rate and inflation rate

i2i1

ieβ

E2

E1

E, α/β

E2

E1

i1iα

E, α/β

iα

(a) (b)

ieβ

ieβ

Consequences of the increase in home (a) and foreign interest rate (b) on the change of the exchange rate

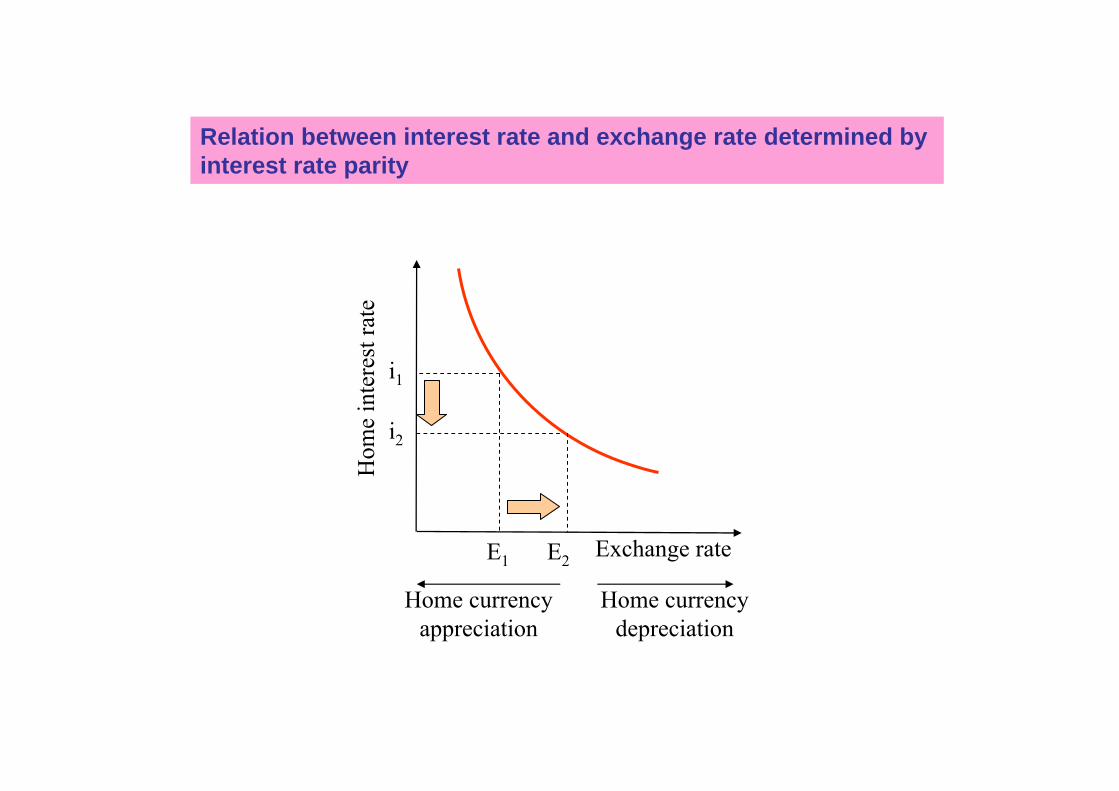

E2E1 Exchange rate

Hom

e in

tere

st ra

te

i2

i1

Home currency appreciation

Home currency depreciation

Relation between interest rate and exchange rate determined by interest rate parity

Real interest rate

Real exchange rate, ε

Exports

Exports as the exchange rate function

Real exchange rate as the interest rate function

Increase in real interest rate → currency appreciation → exports decrease

Real exchange rate, ε

From the real interest rate change to the exports change

Covered interest rate parity

• …when the difference between interest rates abroad and home equals the difference between spot and forward exchange rate.

Forward premium (F>S)

r*- r

r*- r

Forward discount (F<S)

Exports of capital

Exports of capital

Exports of capital

Imports of capital

Imports of capital

Imports of capital

Interest rate parity

Interest rate parity

45o

Covered interest rate parity and the movement of the capital

(F-S)/S (F-S)/S

6. Efficient foreign exchange market

• Efficient foreign exchange market is based on these assumptions:– small costs of foreign exchange transactions;– participants on the foreign exchange market have

information;– securities denominated in different currencies are

perfect substitutes.• Theory of efficient foreign exchange market:

forward exchange rate is indicator of the future movement of the spot exchange rate –forward parity - FP.

Interest rate parity theory determines:• Higher interest rate on currency is compensated

with forward discount.• Lower interest rate on currency is compensated

with forward premium.

If F > S currency is sold with premium and depreciation is expected. If F < S currency is sold with discount and appreciation is expected.

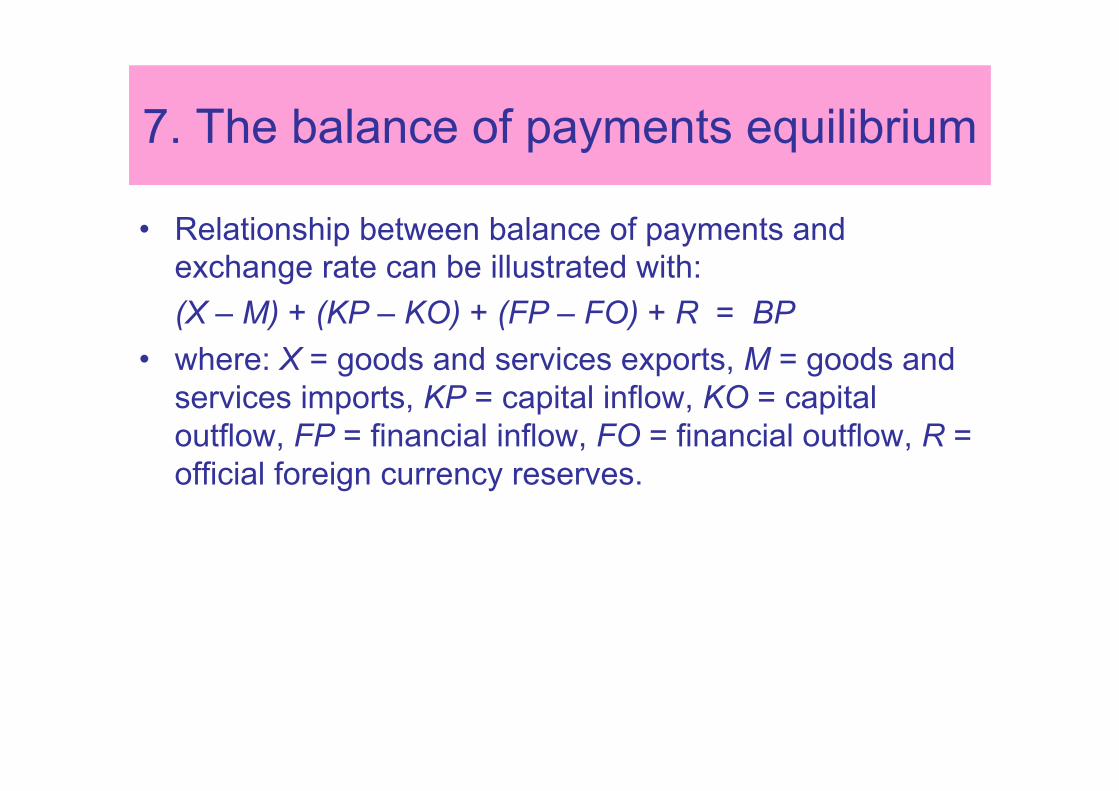

• Relationship between balance of payments and exchange rate can be illustrated with: (X – M) + (KP – KO) + (FP – FO) + R = BP

• where: X = goods and services exports, M = goods and services imports, KP = capital inflow, KO = capital outflow, FP = financial inflow, FO = financial outflow, R = official foreign currency reserves.

7. The balance of payments equilibrium

• Equilibrium real exchange rate: exchange rate which satisfies internal and external balance.

• Net savings (S-I) which is created at certain level of output equals net current account (NX), which does not have to be 0 necessarily and sustainable capital account:

• S – I = Current account = - Capital account.

Real exchange rate

Net exports, NX

Home net savings

NX(ε)

)()( *rIGCYISNX −−−=−=ε

ε*

NX*

Equilibrium exchange rate

Equilibrium real exchange rate