The four pillars of AEC have a differentiated impact on CLMV countries 1 A unique market: Free circulation of goods, services, capital and labor 2 A competitive region Common policies on competition, consumer protection, intellectual property, transports, energy, information technologies, e-commerce, some fiscal issues 3 An equitable development Covering the issue of SME’s as well as initiatives and technical assistance for CLMV Countries 4 Asean integration in the global economy Vietnam is part of the TPP negociation. Everibody is in Asean + 1 agreements and RCEP negociationsf

Transcript

The four pillars of AEC have a differentiated impact on CLMV countries

1 A unique market:Free circulation of goods, services, capital and labor

2 A competitive region Common policies on competition, consumer protection, intellectual property, transports, energy, information technologies, e-commerce, some fiscal issues

3 An equitable developmentCovering the issue of SME’s as well as initiatives and technical assistance for CLMV Countries

4 Asean integration in the global economyVietnam is part of the TPP negociation. Everibody is in Asean + 1 agreements and RCEP negociationsf

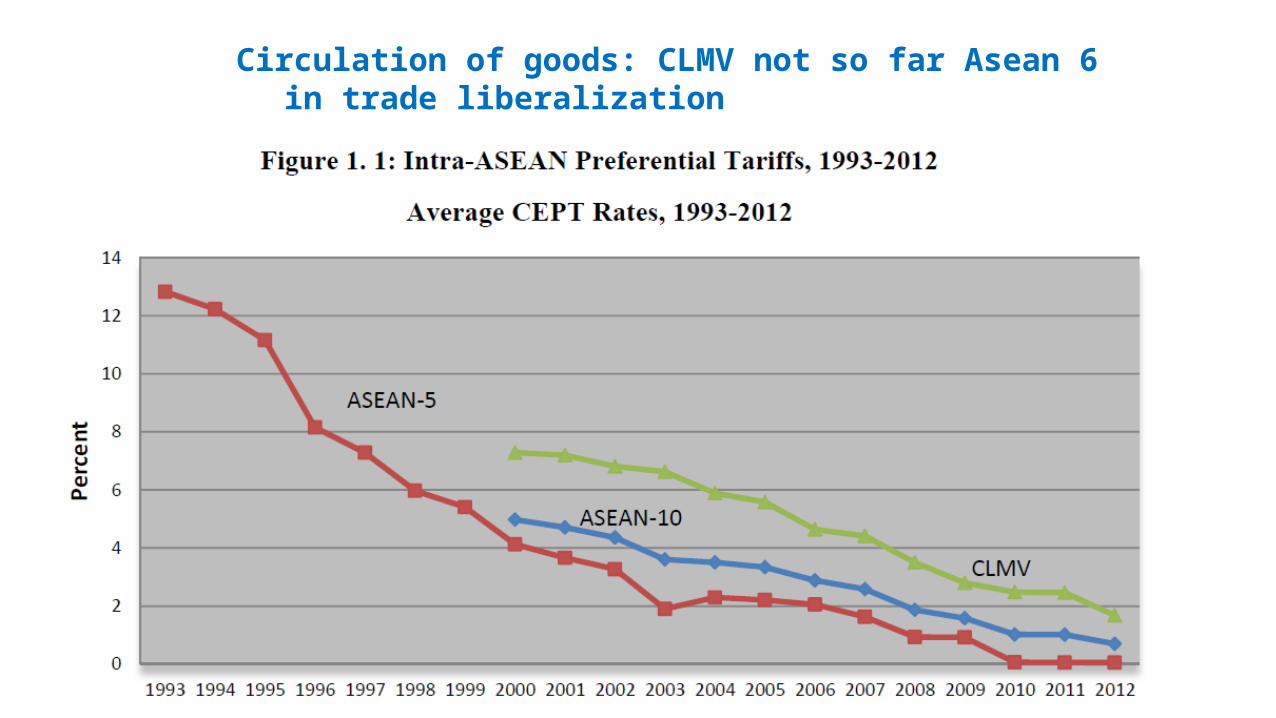

Where we start from: CLMV position is good in terms of trade openness

Source: ASEAN Integration Monitoring Report A Joint Report by the ASEAN Secretariat and the World Bank, 2013

As well as trade intensity

Capital goods, and more recently intermediate goods are the main feature of intra Asean trade

Diversification of exports is a major issue for Cambodia, Lao PDR and Myanmar

Circulation of goods: CLMV not so far Asean 6in trade liberalization

ATIGA (Asean Trade in Goods Agreement) Lists of commitments: exceptions to free trade ASEAN 6 Singapore No exception. Indonesia (list 2010 to 2015) Rice 30% CDs, 25% in 2015Cane sugar 30% in 2010, 5% in 2015Beetroot sugar and refined sugar, 40% in 2010, 10% in 2015Alcoolic beverages, explosives, urban or industrial waste, arms : MFN tariffThailand (list 2010)Cut flowers, grains : 5%Coffee, copra : 5% Philippines (list 2010 to 2015) Animals for reproduction : 5%Cock fighters : 5%Some animal products : 5%Rice : 40% in 2010, 35% in 2015Sugar : 38% in 2010, 5% in 2015 (28% in 2012, 18% in 2013…)Arms : MFN Malaysia (list 2010) Melons, mangos : 5% Rice : 20%Alcoolic beverages : MFN Tobacco : 5% Arms : MFN

Free circulation of goods

Vietnam (lists 2011 to 2013) Agricultural productsSome living animals 5%, Meat and meat products 5%Sugar, chocolate, pasta, bread, cakes/ 5%, Rice : 20% in 2011, 5% in 2013Fruits and vegetables, fruit juices : 5%, Wines and spirits 5%Tobacco : MFNIndustrial productsCement : 5% Oil condensates : 10%Naphta : 20% Oil : 20% Kerozène : 5%Gas, ammoniac, amino-acids : 5% Fertilizers, inks, paintings, lubrifiants : 5% Explosives : MFN Urban and industrial waste : MFN Some polymers and plastics : 5% Bicycles and motocycle tyres : 5%, Used tyres : MFNLeather and skins, articles in leather, wood and articles in wood, paper : 5%Diverse textile products : 5% Glassware, ceramics, jewelery, articles for cooking…: 5%Articles in iron, steel, aluminium, cables : 5%Naval motors, pomps, compressors, agricultural and construction machines: 5%Air cooling, fridges, washing machines, filters : 5%Equipments for transmission, sound recorders, mobile phones : 5%Trucks and cars : 70% until 2012, 60% in 2013Motocycles : 90% in 2011, 75% in 2012, 60% in 2013Boats : 5% Watchmaking : 5%Arms : MFN

ATIGA (Asean Trade in Goods Agreement) Lists of commitments: exceptions to free trade ASEAN 6

ATIGA (Asean Trade in Goods Agreement) Lists of commitments: exceptions to free trade

Myanmar: very few exceptions.Rice (5% in 2015), Wine (5%), soya sauce, dried beans, ice cream (5%)Fireworks and armament (MFN)

Lao PDRTariffs ranging between 5,7 and 10% for a number of agicultural products (live animals, bovine, swine and poultry meat, vegetables, tropical fruits, nuts, wine). 20% for some spirits, 5% for tobacco

Tariffs of 5% in 2015 for some industrial goods: cement, ash, light oils, kerosene, lubrifiants, chemicals for retail sales, ethylene, plastic bottles, tableware and kitchenware, paper, womens’ clothes

20% for motor vehicles and CKD, 5% for motorcycles

Cambodia

7% for vegetables and tropical fruits, 15% for cutflowers, live swine and horses,35% for poultry meat, duck meat and coco leafs

15% on lubricating oils and fuel oils, 25% on light oils, 35% on butyl alcohol and carbofuran35% on arms and 15% on detonators.

Perception of CLMV countries about AEC

MyanmarThe government would like to encourage investment in automobile (CKS assembly lines) but it did not keep a differentiation in its ATIGA offer.It remains very cautious on services liberalization, specially in banking and air transport,where local industry is very weak.There is also a lobby against low cost whisky from India, China or Thailand (but no residual protectionIn the ATIGA offer)CambodiaPreoccupations center on Cambodia’s weak position in terms of trade facilitation, logistics costs, energy costs.Preparation of the business sector to AEC is very limited, specially in SMES. Residual protection concentrates on food products and some energy related products.Lao PDRThe government tries to promote its economic preferentials zones for diversifying its industrial base. The impact of AEC on this policy is not clear (main investors are coming from other countries)VietnamVietnam is clearly in a better competitive position than other CLMV countries to benefit from AEC.The main question is motor vehicle trade liberalization. Japanese companies are going to be the main players: they can either promote local production or imports from Thailand.

Free trade: is it worth it?

Non tarif barriers: still many problems within Asean

Cambodia and Vietnam do not fare badly in terms of trade costs

Including for agricultural products

Vietnam is competitive in logistics performance

Specially in terms of timeliness

And not the worst for openness to foreign providers

Trade facilitation: one of the big challenges

Gats Commitments (WTO + AFAS)/AFAS Total commitments

Brunei 4.35 3.38 14.70

Cambodge 49 .08 1.21 59.88

Indonésie 9.52 1.56 14.85

Laos

Malaisie 25.40 1.26 32.00

Myanmar 4.94 3.00 14.82

Philippines 14.08 3.03 42.66

Singapour 22.66 1.09 24.69

Thaïlande 19.73 1.35 26.63

Vietnam 30.15 1.09 32.86

Moyenne Asean 13.0 1.58 20.53

Source : World Bank World Trade indicator for GATS commitments, Asean researcher for AFAS commitments, (Lim, 2008).

Services: AFAS is not a revolution

And trade restrictiveness in services tends to increase

Services: the case of Cambodia

Services: the case of Vietnam

Capital: FDI is essential for CLMV countries

But intra-Asean FDI is not dominant

Coming back to the four pillars of AEC…

A unique market:Free circulation of goods, services, capital and labor

2 A competitive region Common policies on competition, consumer protection, intellectual property, transports, energy, information technologies, e-commerce, some fiscal issues

3 An equitable developmentCovering the issue of SME’s as well as initiatives and technical assistance for CLMV Countries

4 Asean integration in the global economyVietnam is part of the TPP negociation. Everibody is in Asean + 1 agreements and RCEP negociationsf

![AEC Tunnel Lighting AEC TUNNEL LIGHTING - …old.annell.se/AnnellFiles/Brochure_Tunnel_ENG_low_Del1[2].pdf · AEC Tunnel Lighting AEC TUNNEL LIGHTING | 3 NERO e GRIGIO per marchi](https://static.documents.pub/doc/80x56/5b733ee97f8b9a95348de2ee/aec-tunnel-lighting-aec-tunnel-lighting-old-2pdf-aec-tunnel-lighting-aec.jpg)