38

THE FUTURE OF LOW-COST AIRLINES AND AIRPORTS Eddy Van de Voorde Departement Transport en Ruimtelijke Economie Universiteit Antwerpen

THE FUTURE OF LOW-COSTAIRLINES AND AIRPORTS

Eddy Van de VoordeDepartement Transport en Ruimtelijke Economie Universiteit Antwerpen

1

Prof. Eddy Van de Voorde

BASED ON

Macario, R., Reis, V., Viegas, J., Meersman, H., Monteiro, F., Van de Voorde, E., Vanelslander, T., MacKenzie-Williams, P. and H. Schmidt

The consequences of the growing European low-cost airline sector

European Parliament, December 2007

2

Prof. Eddy Van de Voorde

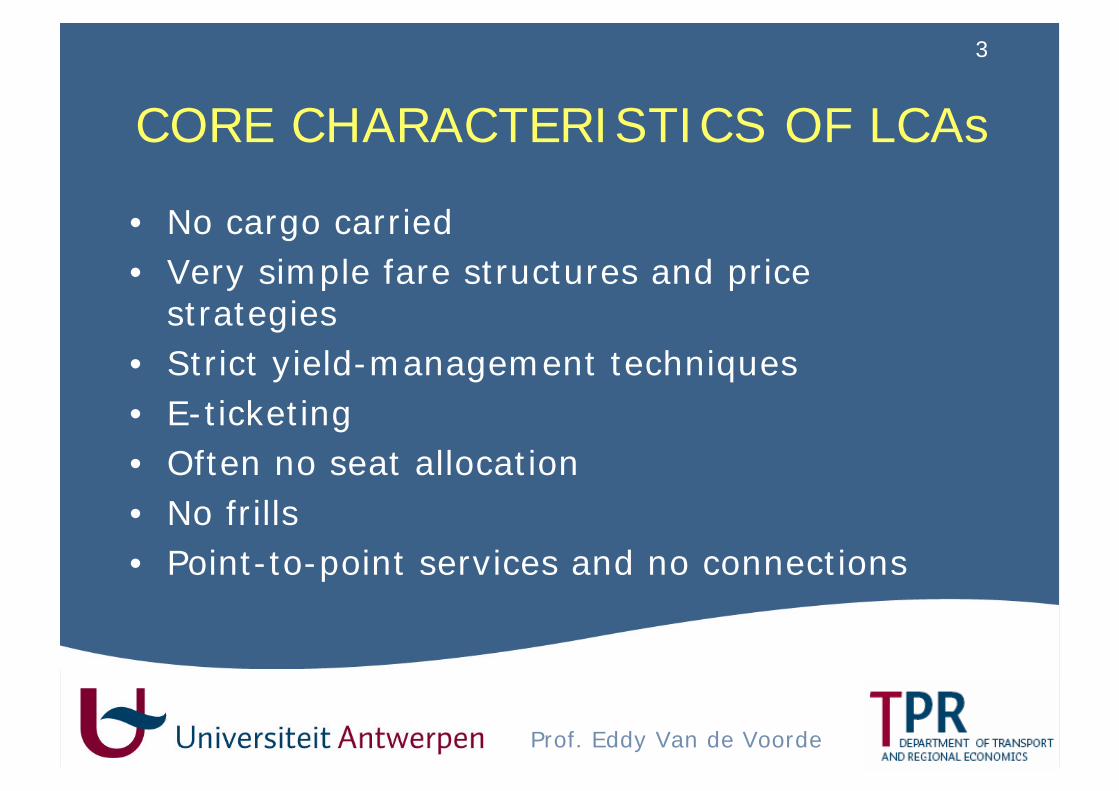

CORE CHARACTERISTICS OF LCAs

• High aircraft utilisation• Internet booking• Use of secondary airports• Minimum cabin crew• Lower wage scales• Lower rates of unionisation among employees• One class of seating• Short ground turn-around times

3

Prof. Eddy Van de Voorde

CORE CHARACTERISTICS OF LCAs

• No cargo carried• Very simple fare structures and price

strategies• Strict yield-management techniques• E-ticketing• Often no seat allocation• No frills• Point-to-point services and no connections

4

Prof. Eddy Van de Voorde

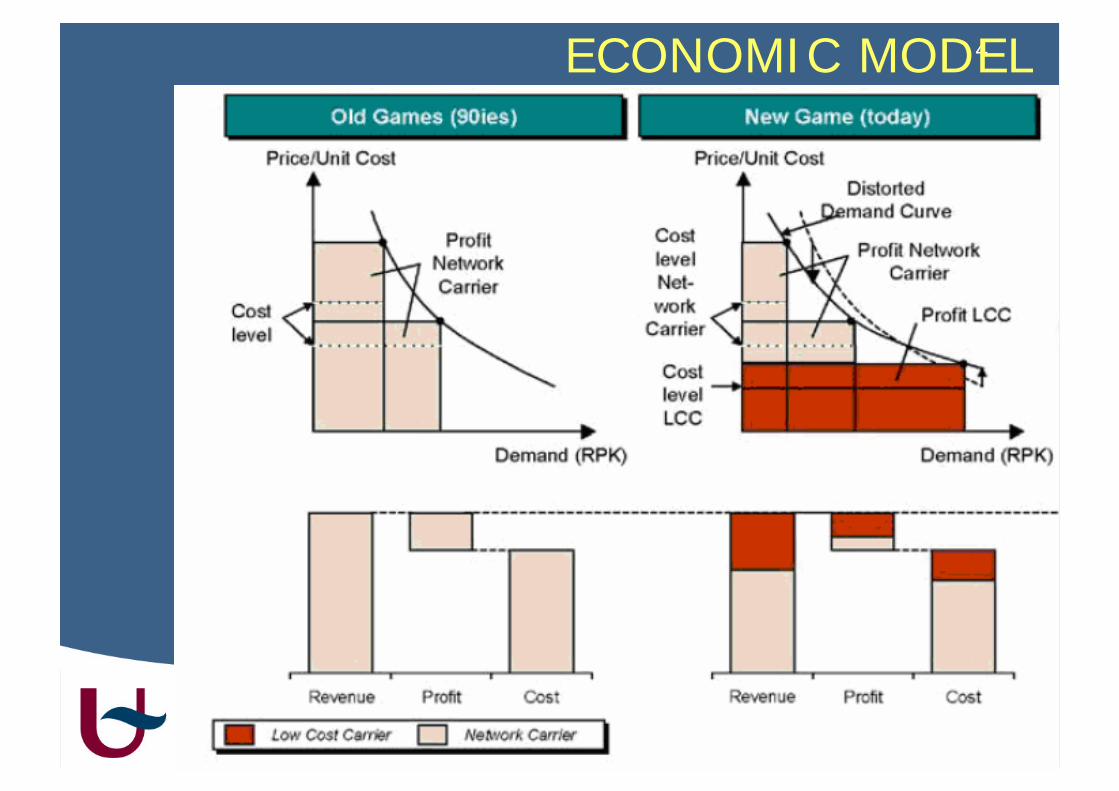

ECONOMIC MODEL

5

Prof. Eddy Van de Voorde

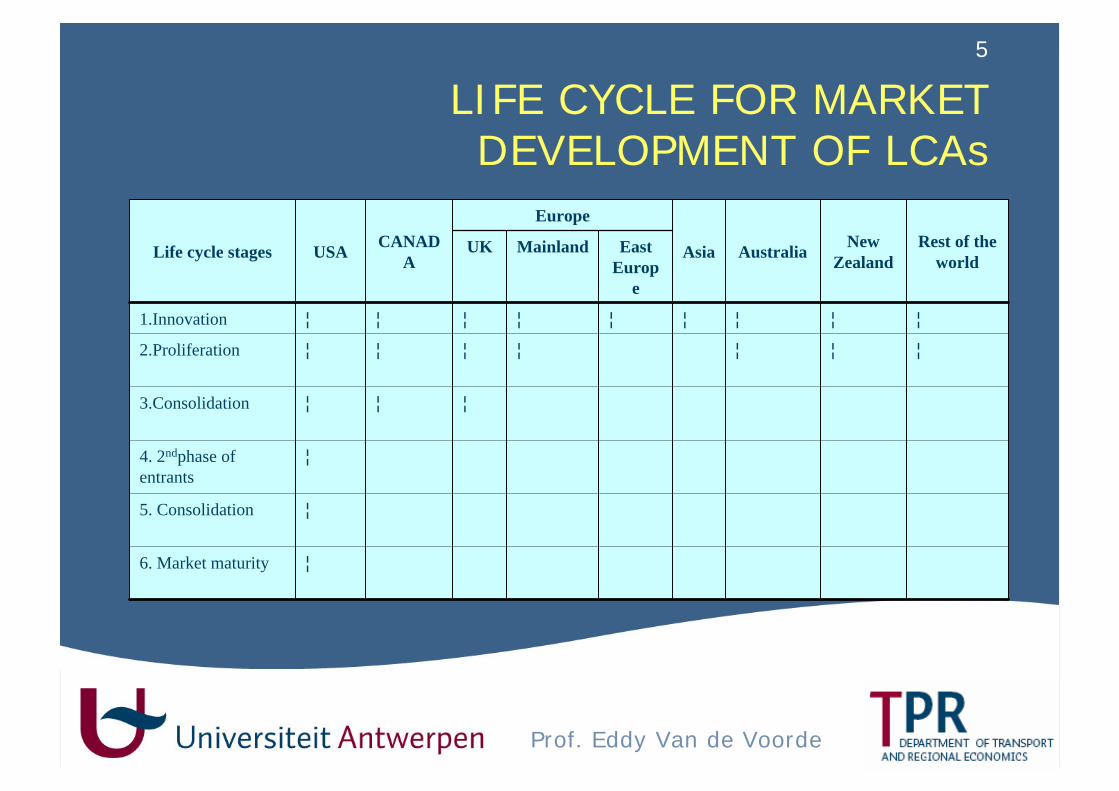

LIFE CYCLE FOR MARKET DEVELOPMENT OF LCAs

¦6. Market maturity

¦5. Consolidation

¦4. 2ndphase of entrants

¦¦¦3.Consolidation

¦¦¦¦¦¦¦2.Proliferation

¦¦¦¦¦¦¦¦¦1.Innovation

EastEurop

e

MainlandUK Rest of the world

New ZealandAustraliaAsia

EuropeCANAD

AUSALife cycle stages

6

Prof. Eddy Van de Voorde

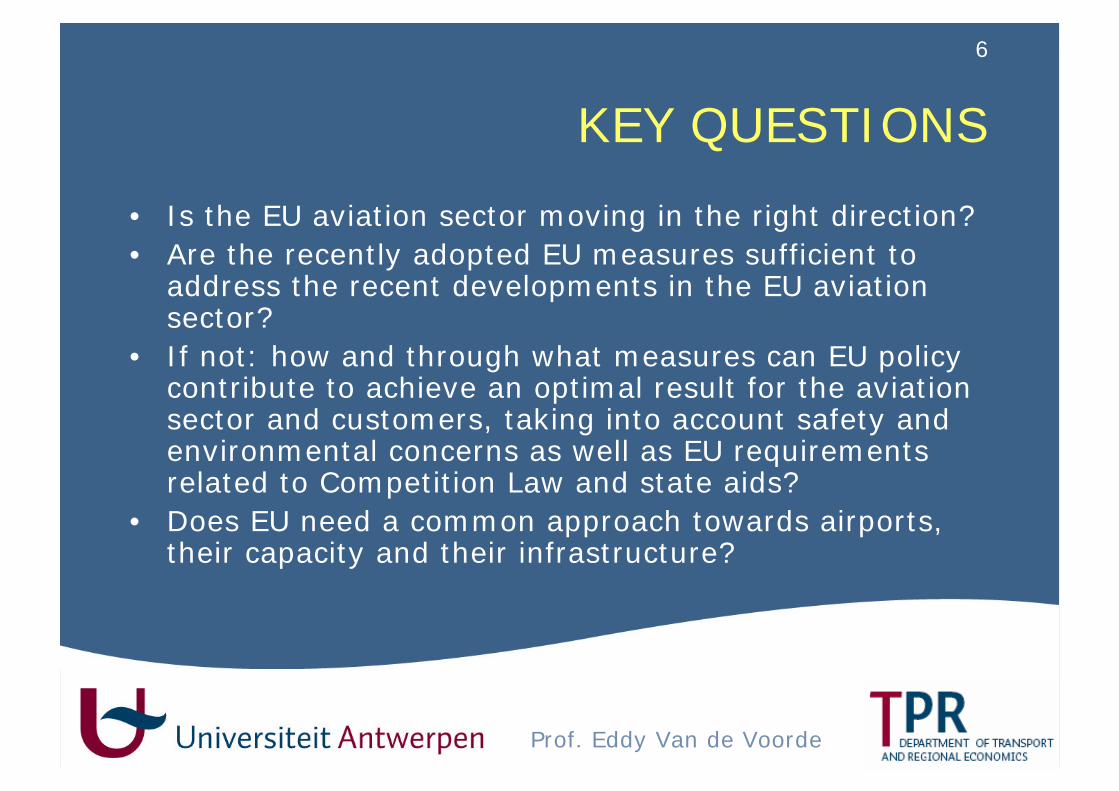

KEY QUESTIONS

• Is the EU aviation sector moving in the right direction?• Are the recently adopted EU measures sufficient to

address the recent developments in the EU aviation sector?

• If not: how and through what measures can EU policy contribute to achieve an optimal result for the aviation sector and customers, taking into account safety and environmental concerns as well as EU requirements related to Competition Law and state aids?

• Does EU need a common approach towards airports, their capacity and their infrastructure?

7

Prof. Eddy Van de Voorde

TYPOLOGY

• The Southwest-copycats (e.g. easyJet)• Subsidiaries (e.g. Snowflake)• Cost-cutters (e.g. Aer Lingus)• Diversified charter carriers (e.g. Thomsonfly)• State-subsidised companies competing on

price (e.g. Alitalia)

8

Prof. Eddy Van de Voorde

ADJUSTING BUSINESS MODELS

Legacy carriers• Discouraging potential entry of LCAs (e.g.

price decrease, capacity increase,…)• Acquisition of an LCA• Creation of an LCA within traditional carrier• Switch to more profitable markets• Radical transformation of full service carrier

into an LCA

9

Prof. Eddy Van de Voorde

ADJUSTING BUSINESS MODELS

LCAs• Tendency towards consolidation (e.g. Air

Berlin); economies of scope?• Revenue sources other than ticket sales (i.e.

LCA evolves into LFA)• Lower workforce costs• Financing from airports and/or local authorities• Customer on-board service

10

Prof. Eddy Van de Voorde

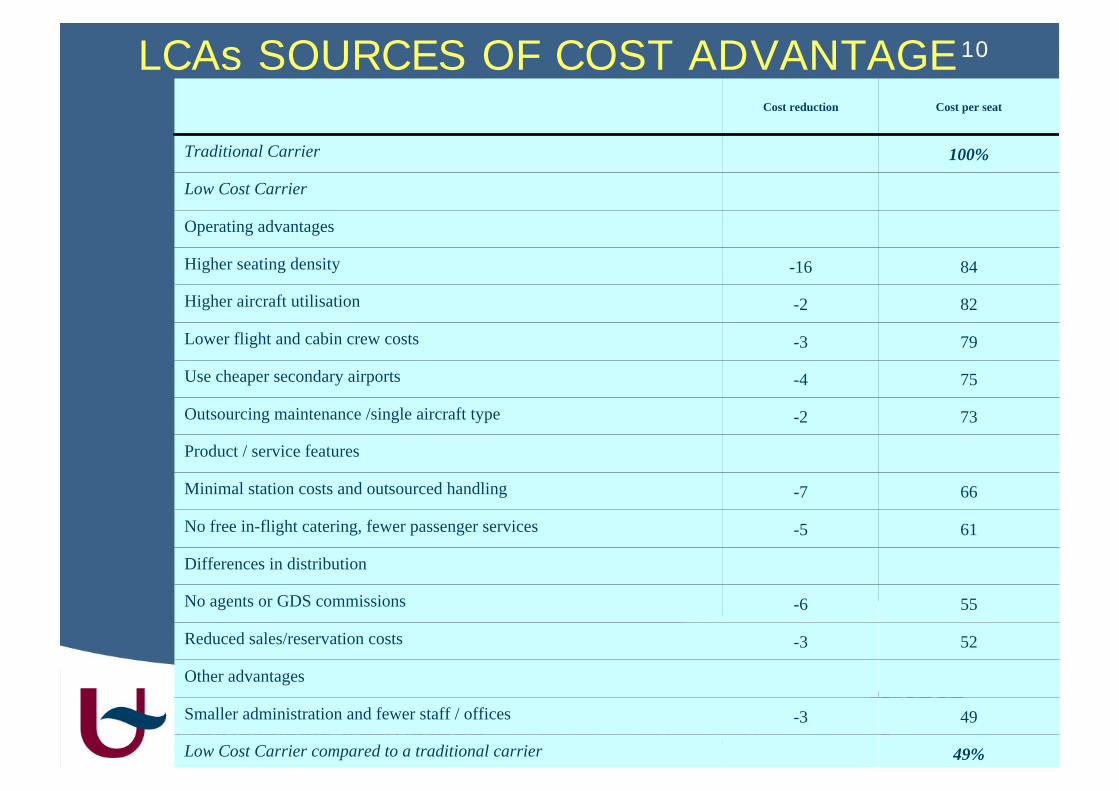

LCAs SOURCES OF COST ADVANTAGE

49%Low Cost Carrier compared to a traditional carrier

49-3Smaller administration and fewer staff / offices

Other advantages

52-3Reduced sales/reservation costs

55-6No agents or GDS commissions

Differences in distribution

61-5No free in-flight catering, fewer passenger services

66-7Minimal station costs and outsourced handling

Product / service features

73-2Outsourcing maintenance /single aircraft type

75-4Use cheaper secondary airports

79-3Lower flight and cabin crew costs

82-2Higher aircraft utilisation

84-16Higher seating density

Operating advantages

Low Cost Carrier

100%Traditional Carrier

Cost per seatCost reduction

11

Prof. Eddy Van de Voorde

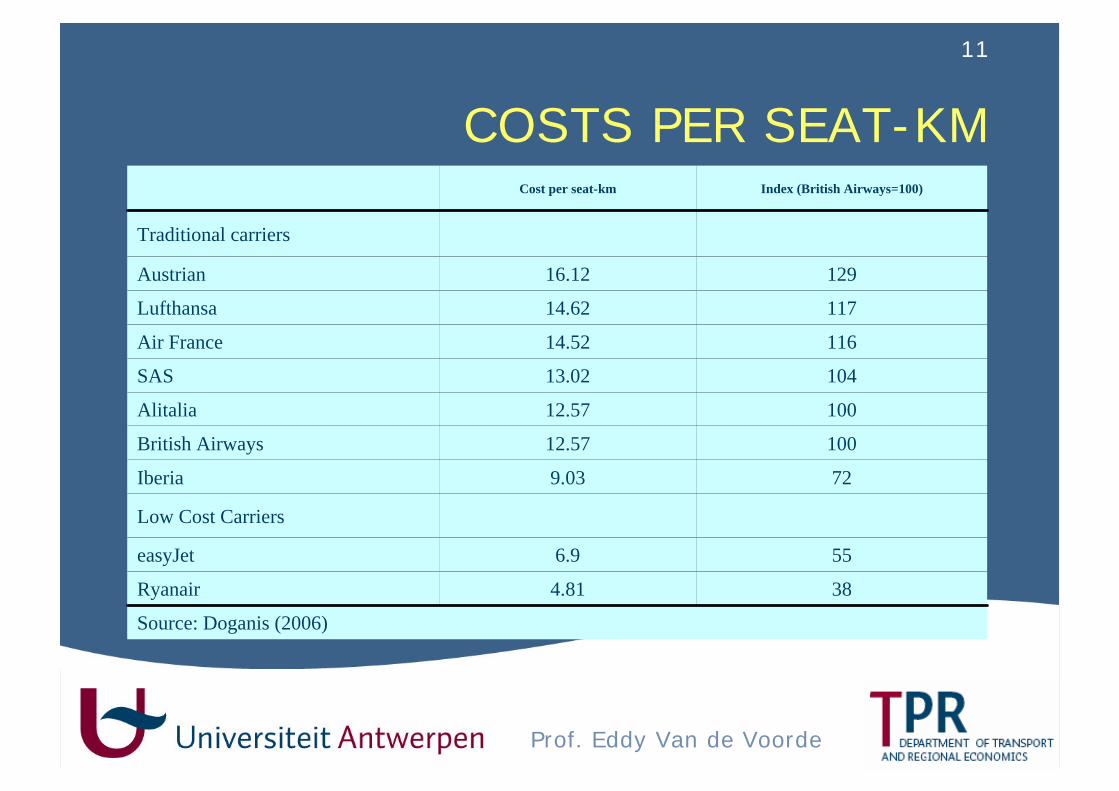

COSTS PER SEAT-KM

Source: Doganis (2006)

384.81Ryanair

556.9easyJet

Low Cost Carriers

729.03Iberia

10012.57British Airways

10012.57Alitalia

10413.02SAS

11614.52Air France

11714.62Lufthansa

12916.12Austrian

Traditional carriers

Index (British Airways=100)Cost per seat-km

12

Prof. Eddy Van de Voorde

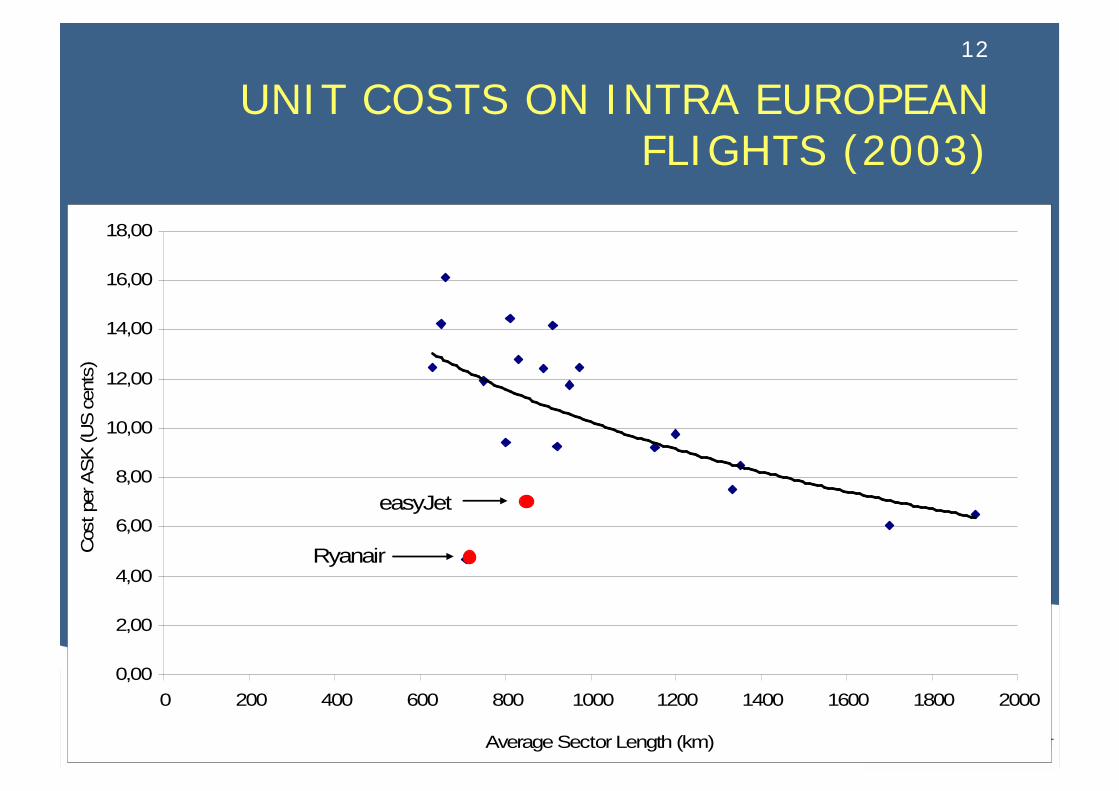

UNIT COSTS ON INTRA EUROPEAN FLIGHTS (2003)

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

18,00

0 200 400 600 800 1000 1200 1400 1600 1800 2000

Average Sector Length (km)

Cos

t per

AS

K (U

S c

ents

)

easyJet

Ryanair

13

Prof. Eddy Van de Voorde

THE CURRENT LCA MARKET

European LCAs have benefited from a veryliberal legal framework and geo-political factors such as:• The Single European Aviation Act• Underdeveloped air capacities• The enlargement of the European Union• Open-skies agreements

14

Prof. Eddy Van de Voorde

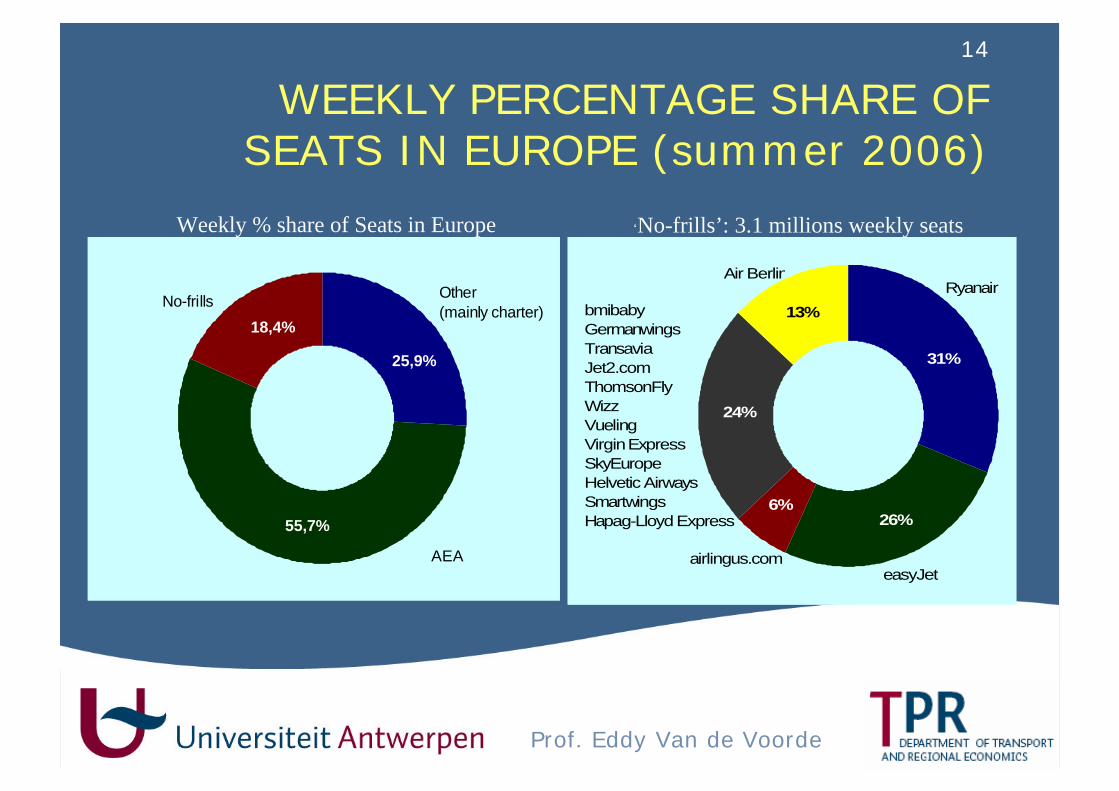

WEEKLY PERCENTAGE SHARE OF SEATS IN EUROPE (summer 2006)

Weekly % share of Seats in Europe

Other(mainly charter)

AEA

No-frills

25,9%

55,7%

18,4%

‘No-frills’: 3.1 millions weekly seats

Ryanair

easyJet

Air Berlin

airlingus.com

bmibabyGermanwingsTransaviaJet2.comThomsonFlyWizzVuelingVirgin ExpressSkyEuropeHelvetic AirwaysSmartwingsHapag-Lloyd Express

31%

26%6%

24%

13%

15

Prof. Eddy Van de Voorde

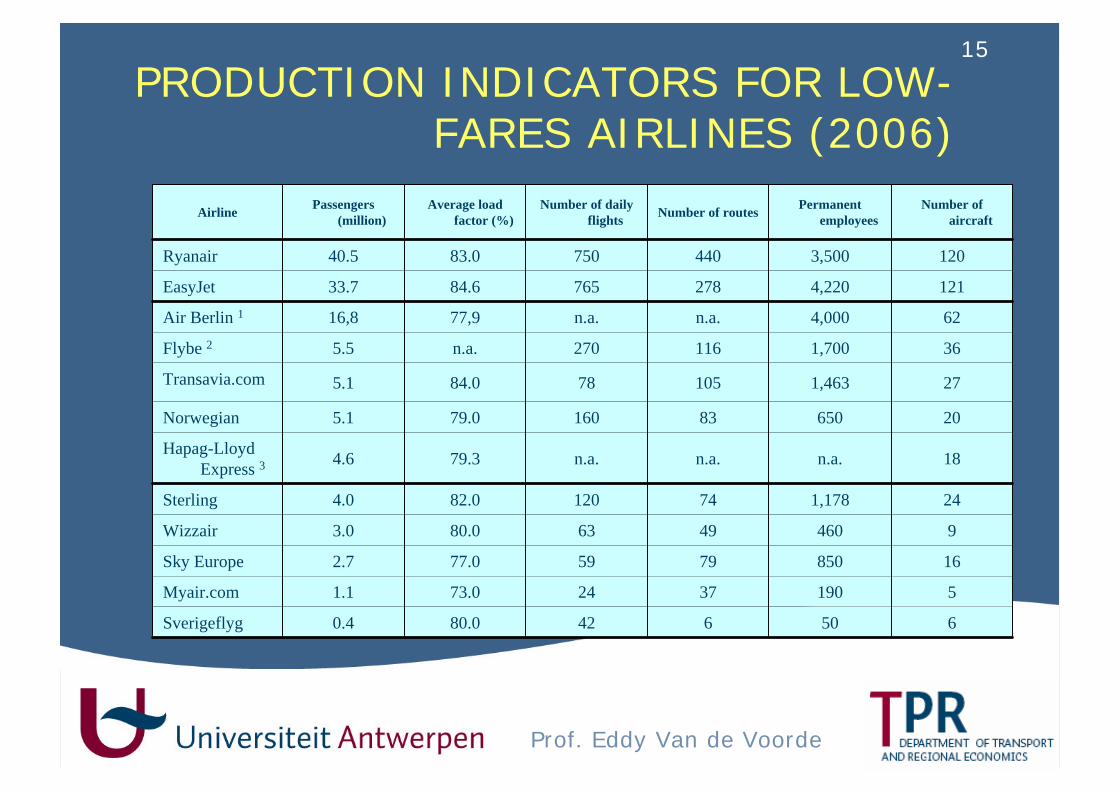

PRODUCTION INDICATORS FOR LOW-FARES AIRLINES (2006)

65064280.00.4Sverigeflyg

5190372473.01.1Myair.com

16850795977.02.7Sky Europe

9460496380.03.0Wizzair

241,1787412082.04.0Sterling

18n.a.n.a.n.a.79.34.6Hapag-Lloyd Express 3

206508316079.05.1Norwegian

271,4631057884.05.1Transavia.com

361,700116270n.a.5.5Flybe 2

624,000n.a.n.a.77,916,8Air Berlin 11214,22027876584.633.7EasyJet

1203,50044075083.040.5Ryanair

Number of aircraft

Permanent employeesNumber of routesNumber of daily

flightsAverage load

factor (%)Passengers

(million)Airline

16

Prof. Eddy Van de Voorde

AVOIDING MUTUAL COMPETITION?

• Ryanair: concentrates on smaller markets and regional airports

• easyJet: focussing on bigger markets and primary airports

• Important question: will potential overcapacityresult in a price war and/or a consolidationwave?

17

Prof. Eddy Van de Voorde

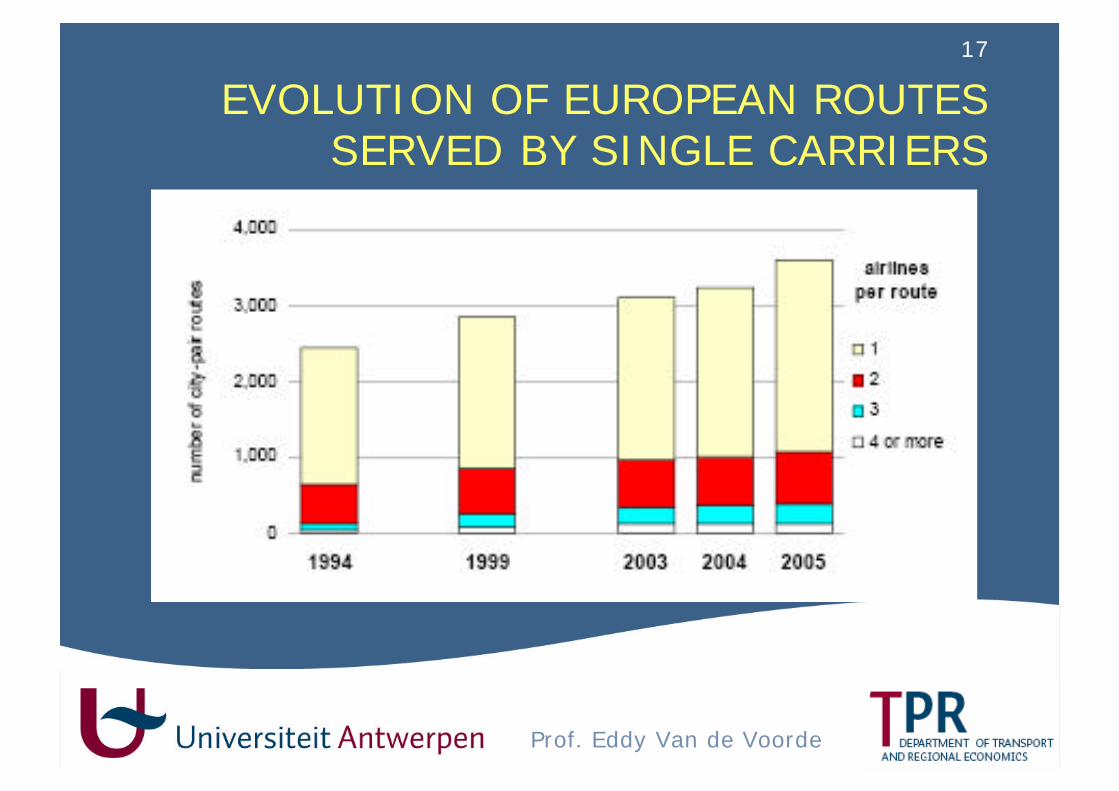

EVOLUTION OF EUROPEAN ROUTES SERVED BY SINGLE CARRIERS

18

Prof. Eddy Van de Voorde

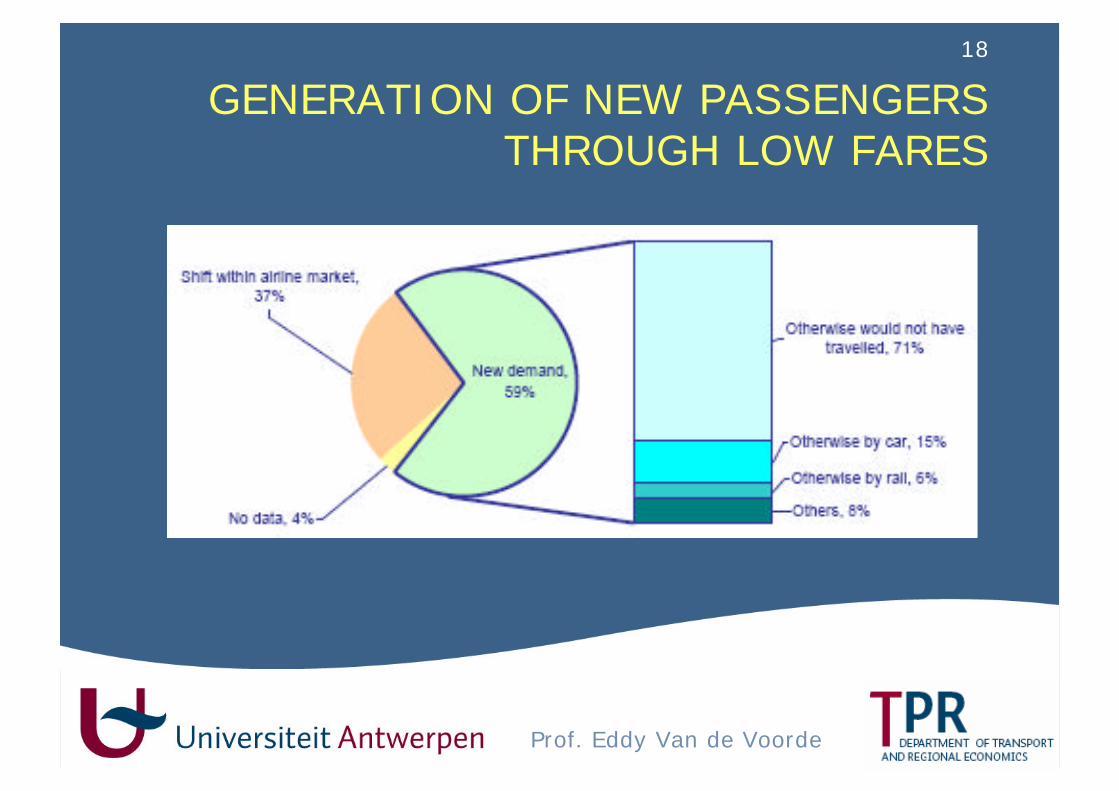

GENERATION OF NEW PASSENGERS THROUGH LOW FARES

19

Prof. Eddy Van de Voorde

TRENDS IN THE LCA MARKET

• The European LCA market continues to growstrongly: Ryanair (+23%) and easyJet(+16%) in 2006

• Deusche Bank (May 2007): volume growth of ca. 15% per annum, as a combination of shareshift, GDP growth and rising propensity totravel

20

Prof. Eddy Van de Voorde

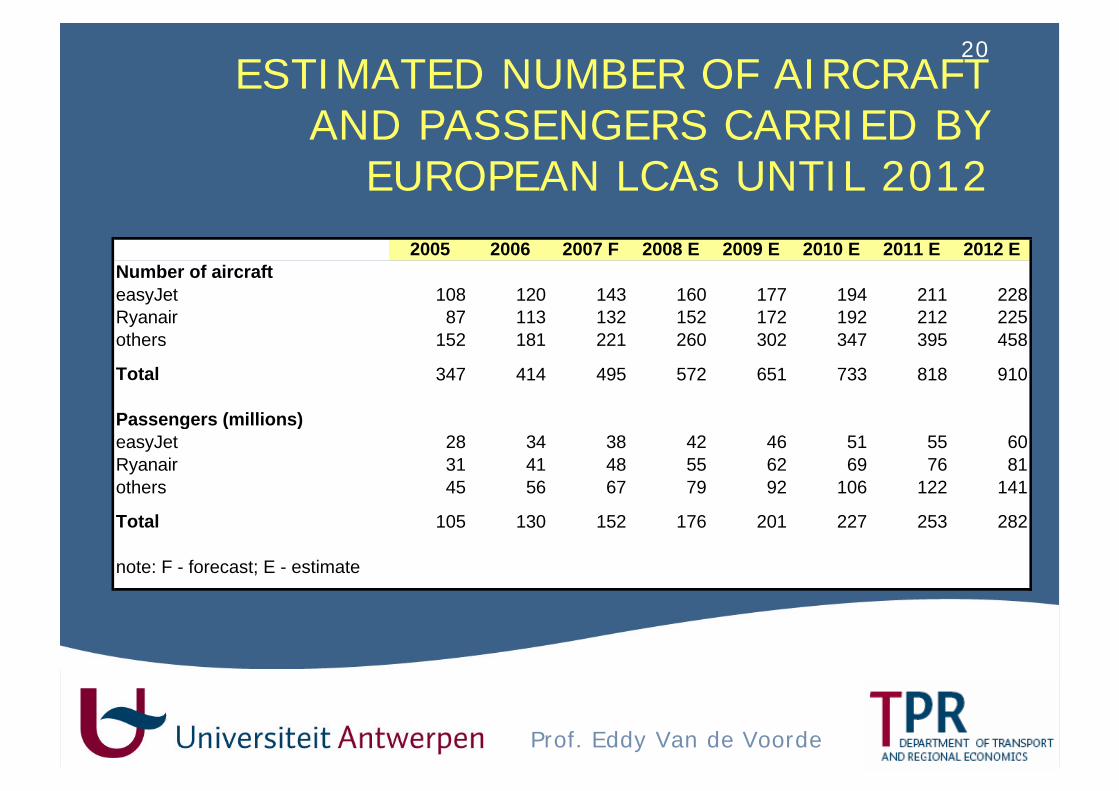

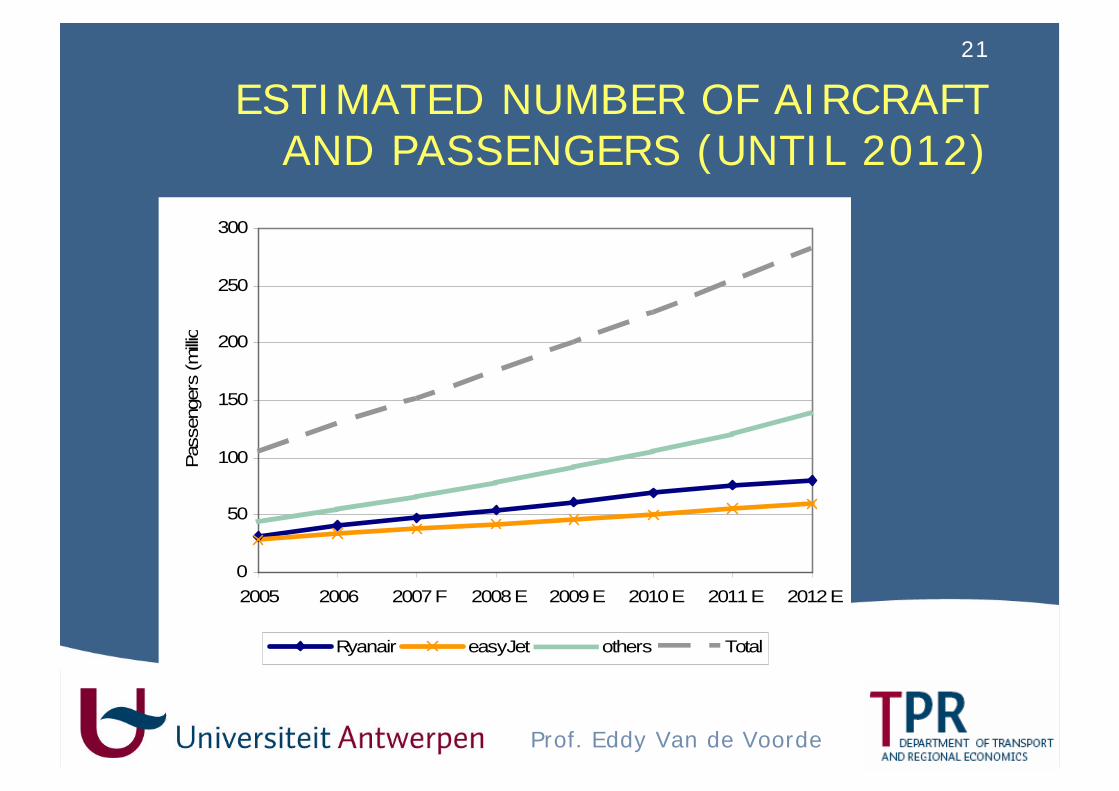

ESTIMATED NUMBER OF AIRCRAFT AND PASSENGERS CARRIED BY

EUROPEAN LCAs UNTIL 2012 2005 2006 2007 F 2008 E 2009 E 2010 E 2011 E 2012 E

Number of aircrafteasyJet 108 120 143 160 177 194 211 228Ryanair 87 113 132 152 172 192 212 225others 152 181 221 260 302 347 395 458

Total 347 414 495 572 651 733 818 910

Passengers (millions)easyJet 28 34 38 42 46 51 55 60Ryanair 31 41 48 55 62 69 76 81others 45 56 67 79 92 106 122 141

Total 105 130 152 176 201 227 253 282

note: F - forecast; E - estimate

21

Prof. Eddy Van de Voorde

ESTIMATED NUMBER OF AIRCRAFT AND PASSENGERS (UNTIL 2012)

0

50

100

150

200

250

300

2005 2006 2007 F 2008 E 2009 E 2010 E 2011 E 2012 E

Pas

seng

ers

(milli

ons)

Ryanair easyJet others Total

22

Prof. Eddy Van de Voorde

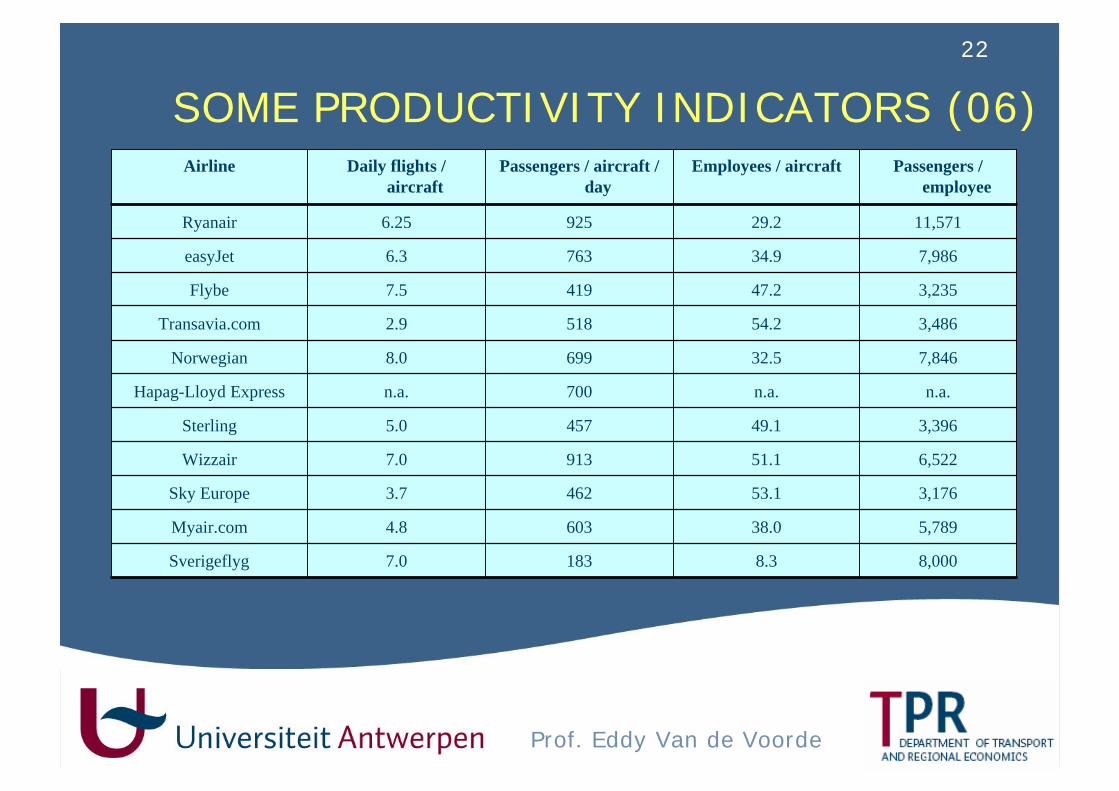

SOME PRODUCTIVITY INDICATORS (06)

8,0008.31837.0Sverigeflyg

5,78938.06034.8Myair.com

3,17653.14623.7Sky Europe

6,52251.19137.0Wizzair

3,39649.14575.0Sterling

n.a.n.a.700n.a.Hapag-Lloyd Express

7,84632.56998.0Norwegian

3,48654.25182.9Transavia.com

3,23547.24197.5Flybe

7,98634.97636.3easyJet

11,57129.29256.25Ryanair

Passengers / employee

Employees / aircraftPassengers / aircraft / day

Daily flights / aircraft

Airline

23

Prof. Eddy Van de Voorde

THE RISKS

Some inputs will become much more expensive, because of:• Current full order books of aircraft

manufacturers• Pilots shortage• Congested airports and airways

Crucial: the speed of adjustment!

24

Prof. Eddy Van de Voorde

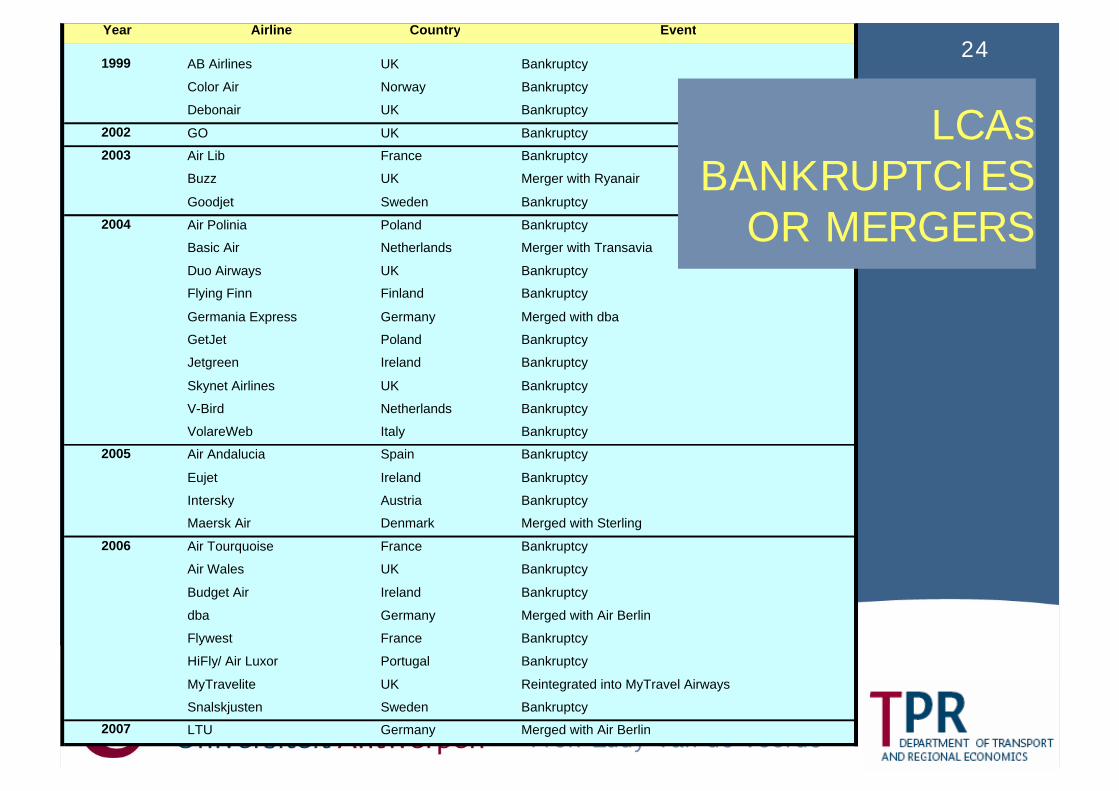

Year Airline Country Event

1999 AB Airlines UK Bankruptcy

Color Air Norway Bankruptcy

Debonair UK Bankruptcy

2002 GO UK Bankruptcy

2003 Air Lib France Bankruptcy

Buzz UK Merger with Ryanair

Goodjet Sweden Bankruptcy

2004 Air Polinia Poland Bankruptcy

Basic Air Netherlands Merger with Transavia

Duo Airways UK Bankruptcy

Flying Finn Finland Bankruptcy

Germania Express Germany Merged with dba

GetJet Poland Bankruptcy

Jetgreen Ireland Bankruptcy

Skynet Airlines UK Bankruptcy

V-Bird Netherlands Bankruptcy

VolareWeb Italy Bankruptcy

2005 Air Andalucia Spain Bankruptcy

Eujet Ireland Bankruptcy

Intersky Austria Bankruptcy

Maersk Air Denmark Merged with Sterling

2006 Air Tourquoise France Bankruptcy

Air Wales UK Bankruptcy

Budget Air Ireland Bankruptcy

dba Germany Merged with Air Berlin

Flywest France Bankruptcy

HiFly/ Air Luxor Portugal Bankruptcy

MyTravelite UK Reintegrated into MyTravel Airways

Snalskjusten Sweden Bankruptcy

2007 LTU Germany Merged with Air Berlin

LCAsBANKRUPTCIES

OR MERGERS

25

Prof. Eddy Van de Voorde

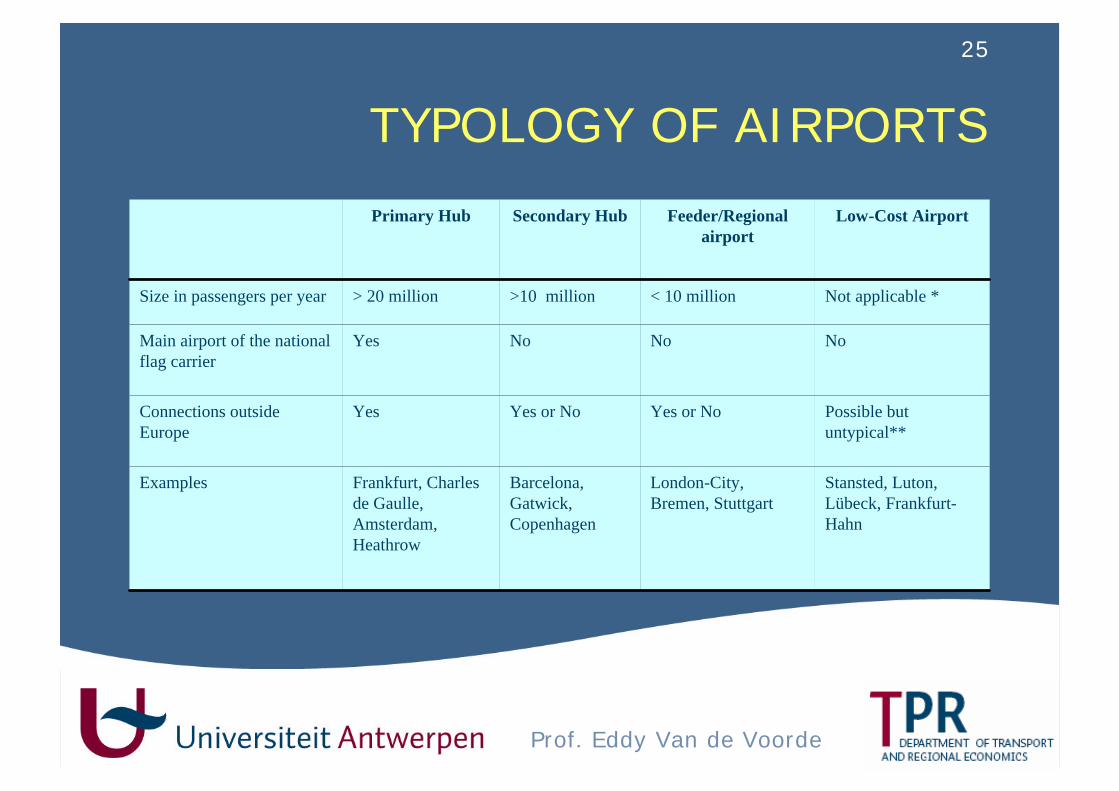

TYPOLOGY OF AIRPORTS

Stansted, Luton, Lübeck, Frankfurt-Hahn

London-City, Bremen, Stuttgart

Barcelona, Gatwick, Copenhagen

Frankfurt, Charles de Gaulle, Amsterdam, Heathrow

Examples

Possible but untypical**

Yes or NoYes or NoYesConnections outside Europe

NoNoNoYesMain airport of the national flag carrier

Not applicable *< 10 million>10 million> 20 millionSize in passengers per year

Low-Cost AirportFeeder/Regional airport

Secondary HubPrimary Hub

26

Prof. Eddy Van de Voorde

VARIOUS LOW-COST AIRPORT BUSINESS MODELS

• Lower aeronautical charges, leading to lowerfinancial return, so that one looks for othernon-aeronautical revenue sources

• Airport’s hinterland influences bargainingpower and positioning

• Low-cost market is highly volatile• Constant threat to abandon service

27

Prof. Eddy Van de Voorde

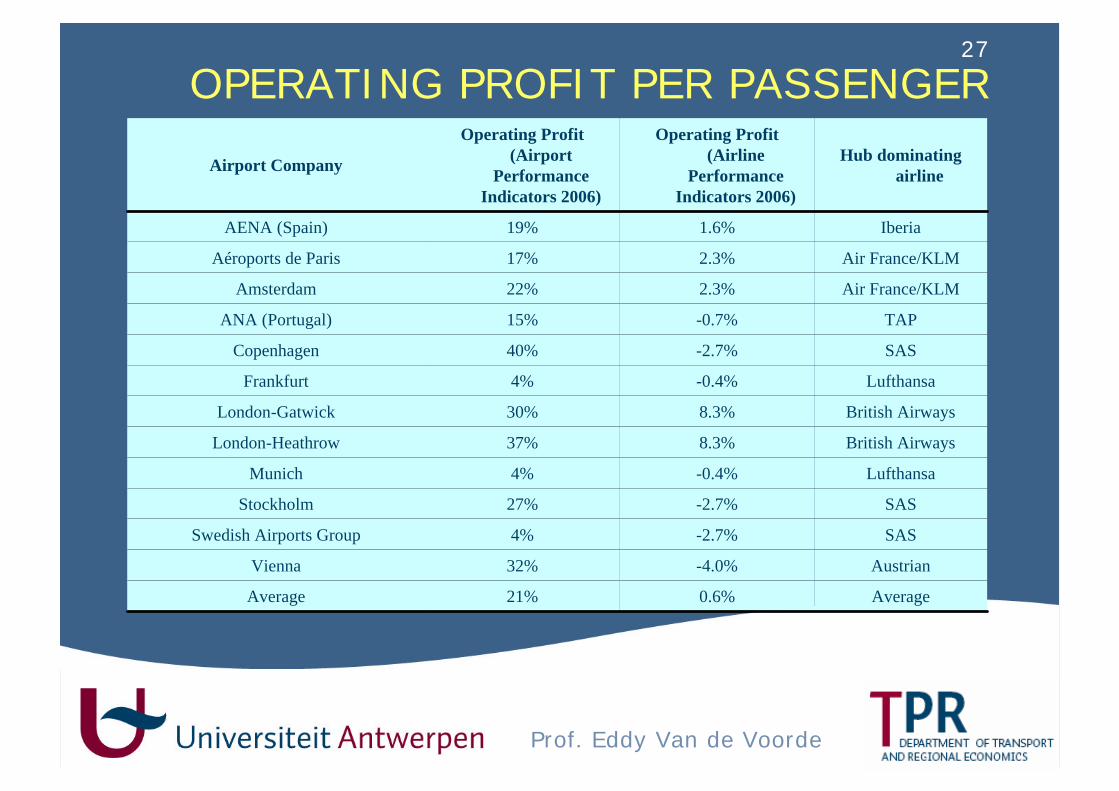

OPERATING PROFIT PER PASSENGER

Average0.6%21%Average

Austrian-4.0%32%Vienna

SAS-2.7%4%Swedish Airports Group

SAS-2.7%27%Stockholm

Lufthansa-0.4%4%Munich

British Airways8.3%37%London-Heathrow

British Airways8.3%30%London-Gatwick

Lufthansa-0.4%4%Frankfurt

SAS-2.7%40%Copenhagen

TAP-0.7%15%ANA (Portugal)

Air France/KLM2.3%22%Amsterdam

Air France/KLM2.3%17%Aéroports de Paris

Iberia1.6%19%AENA (Spain)

Hub dominating airline

Operating Profit (Airline

Performance Indicators 2006)

Operating Profit (Airport

Performance Indicators 2006)

Airport Company

28

Prof. Eddy Van de Voorde

UNDERSTANDING THE IMPACT OF LCA GROWTH

• Impact on prices• Impact on the environment• Impact on regional economies• Safety and security• Freedom of movement of persons• Competition in the air transport sector• Competition and coorperation with other

modes of transport

29

Prof. Eddy Van de Voorde

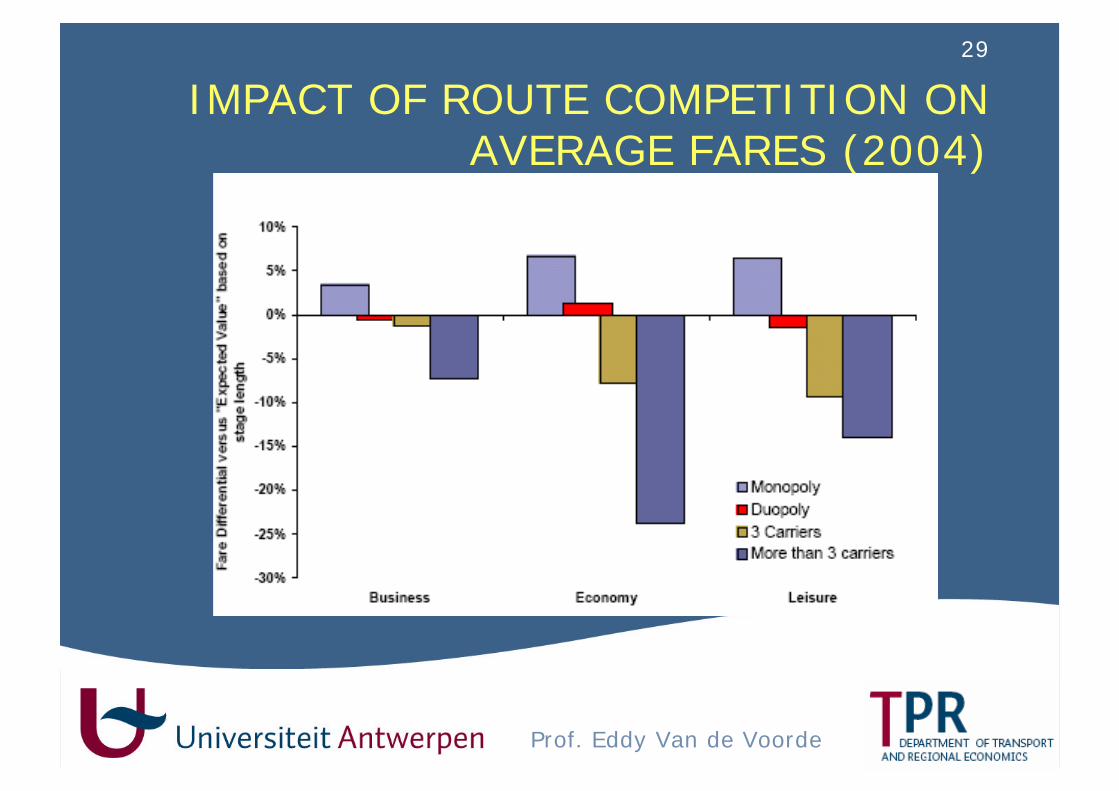

IMPACT OF ROUTE COMPETITION ON AVERAGE FARES (2004)

30

Prof. Eddy Van de Voorde

IMPACT ON REGIONAL ECONOMIES

Three main classes:• Direct effects (e.g. employment in activities

directly related to air transport)• Indirect effects (as a result of the increase in

flows of people)• Catalyctic effects (e.g. incoming investment)

31

Prof. Eddy Van de Voorde

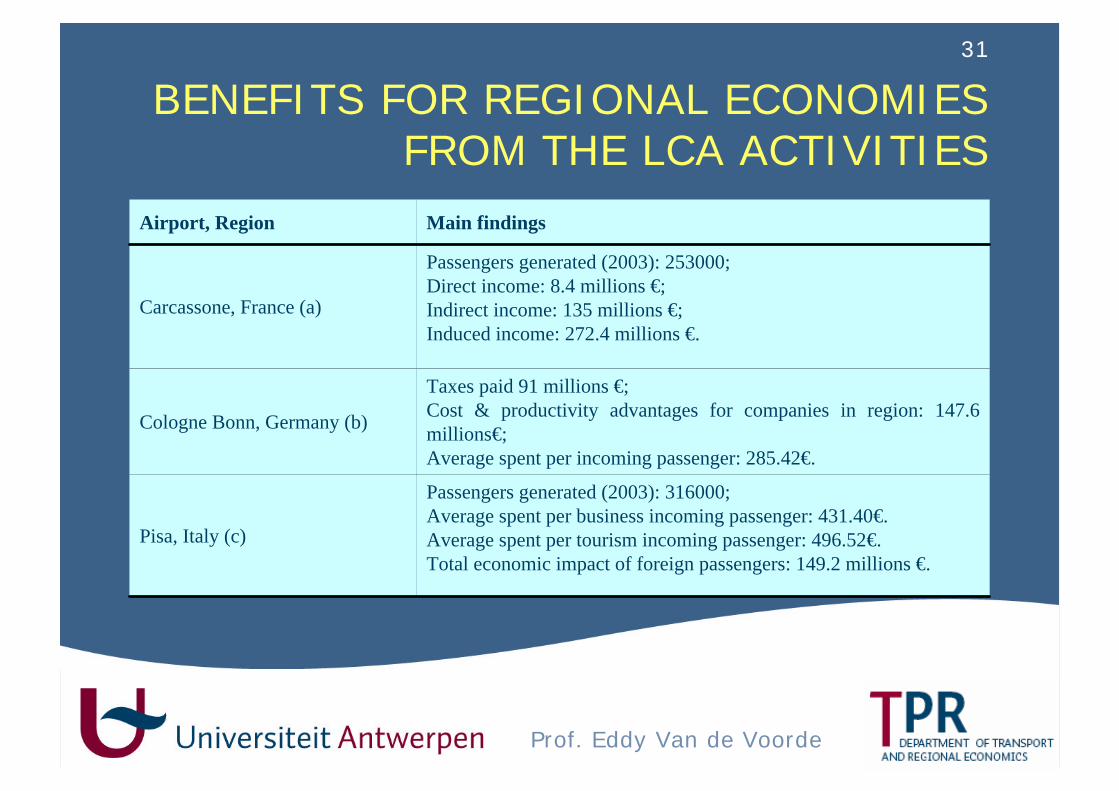

BENEFITS FOR REGIONAL ECONOMIES FROM THE LCA ACTIVITIES

Passengers generated (2003): 316000;Average spent per business incoming passenger: 431.40€.Average spent per tourism incoming passenger: 496.52€.Total economic impact of foreign passengers: 149.2 millions €.

Pisa, Italy (c)

Taxes paid 91 millions €;Cost & productivity advantages for companies in region: 147.6 millions€;Average spent per incoming passenger: 285.42€.

Cologne Bonn, Germany (b)

Passengers generated (2003): 253000;Direct income: 8.4 millions €;Indirect income: 135 millions €;Induced income: 272.4 millions €.

Carcassone, France (a)

Main findingsAirport, Region

32

Prof. Eddy Van de Voorde

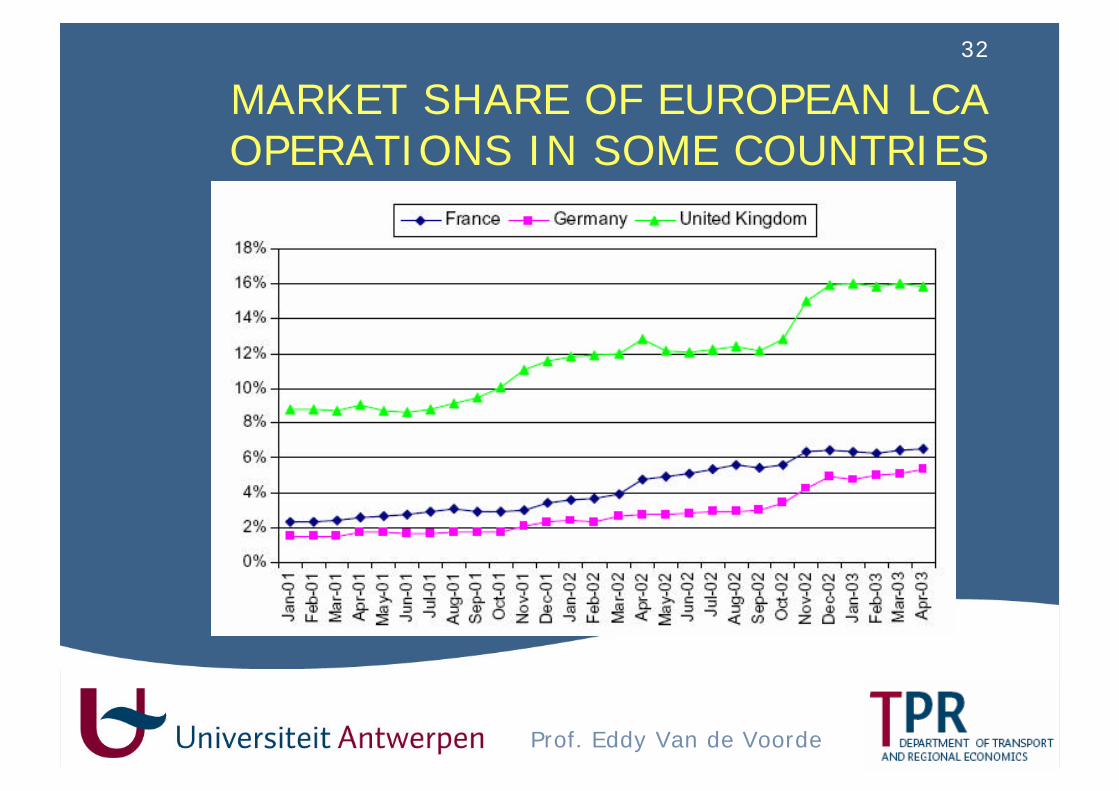

MARKET SHARE OF EUROPEAN LCA OPERATIONS IN SOME COUNTRIES

33

Prof. Eddy Van de Voorde

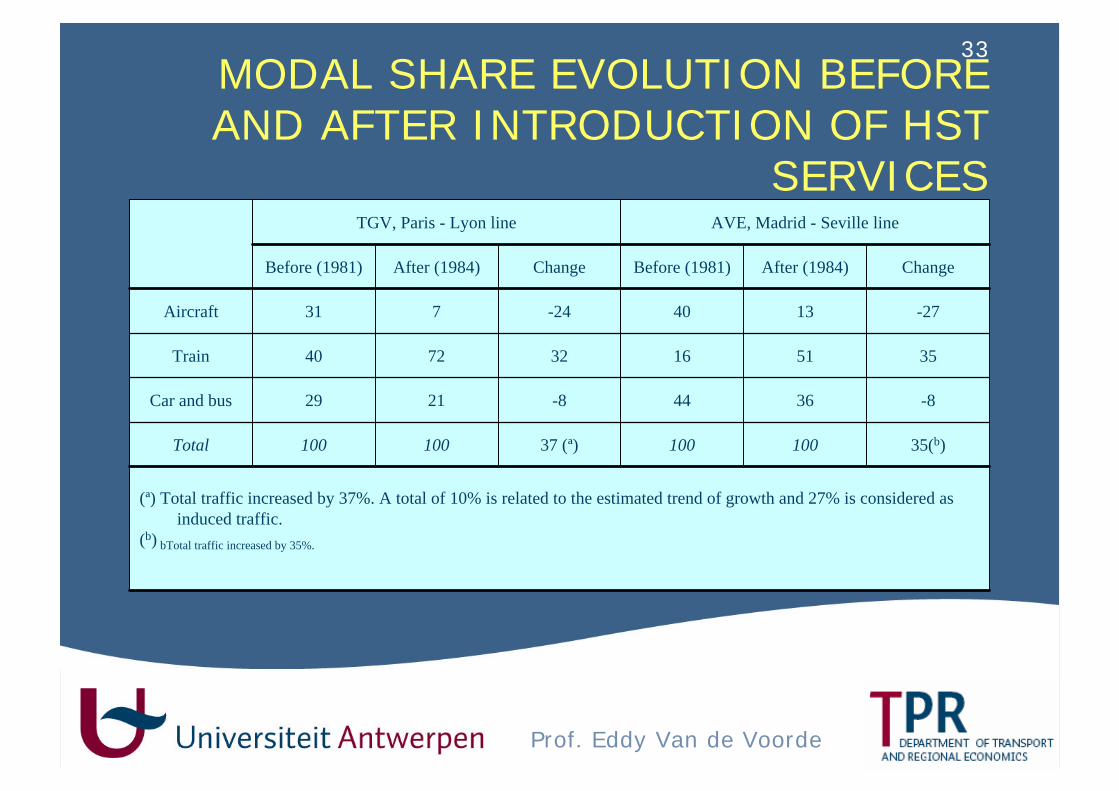

MODAL SHARE EVOLUTION BEFORE AND AFTER INTRODUCTION OF HST

SERVICES

(ª) Total traffic increased by 37%. A total of 10% is related to the estimated trend of growth and 27% is considered as induced traffic.

(b) bTotal traffic increased by 35%.

35(b)10010037 (ª)100100Total

-83644-82129Car and bus

355116327240Train

-271340-24731Aircraft

ChangeAfter (1984)Before (1981)ChangeAfter (1984)Before (1981)

AVE, Madrid - Seville lineTGV, Paris - Lyon line

34

Prof. Eddy Van de Voorde

CONCLUSIONS (1)

• Consolidation trend• Contestability characteristics should be

guaranteed• LCAs generate extra income from other

sources; any limit?• Avoid abuse of support by airports to new

airlines• Monitoring needed of all cost items

35

Prof. Eddy Van de Voorde

CONCLUSIONS (2)

• Reaction of LCAs to the new Europeanregulations such as compensation of travellersis not yet known

• Information is still insufficient on the possiblereactions of primary airports towards LCAs

• Some airports and airways are subject tocongestion, resulting in a shortage of goodslots

36

Prof. Eddy Van de Voorde

CONCLUSIONS (3)

• Unlike the airline sector, the European airportsector is expected to remain healthy and profitable

• There is competition between airports of the same size or role within the transport network

• Entries into the market are possible, most obviously by redeveloping former military airfields

37

Prof. Eddy Van de Voorde

CONCLUSIONS (4)

• No evidence that LCAs are causing anysignificant financial difficulty for larger airports

• It is clear that a unique LCA-model does notexist, even if most of the European LCAs usethe southwest model as their basic reference