24

The Future of Pensions October 2010 Prepared for CUPE and PSAC

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 217 times |

| Download: | 2 times |

The Future of Pensions

October 2010

Prepared forCUPE and PSAC

2ENVIRONICS

Future of Pensions

• National Public Opinion Survey

– Commissioned by CUPE and PSAC

– 2,020 adult Canadians surveyed by telephone, August 6 to 28

– Margin of error +/- 2.2 percentage points at the 95% confidence level– Margin of error for Atlantic Canada +/-6.1 percentage points at the 95% confidence level

– Margin of error for the Prairies +/-4.4 percentage points at the 95% confidence level

– Margin of error for British Colombia +/-6.2 percentage points at the 95% confidence level

3ENVIRONICS

Support for increasing CPP benefits is widespread

Support for increasing CPP benefitsBy income 2010

100K plus

80 to 100K

60 to 80K

30 to 60K

<30K

Total 37 41 10 7 6

38 40 8 5 9

41 41 8 5 5

38 42 9 7 3

36 45 9 8 2

35 36 15 10 4

Strongly support

Support

Oppose

Strongly oppose

dk/na

Q. Recently there has been talk about expanding the CPP to help people save more for retirement. The CPP covers almost all workers. The amount that individual workers and employers pay into the plan would increase slowly over the next several years to provide higher retirement benefits from the CPP. Generally speaking do you support or oppose increasing Canada Pension Plan benefits? Is that strongly or somewhat?

Atlantic: 41% strongly support, 43% support

Prairies: 35% stronglysupport, 43% support

BC: 40% strongly support,36% support

4ENVIRONICS

Rate of changes to Canada’s pension system felt to be too slow

Q. As far as you know, are policy-makers moving too fast, too slow, or at the right pace in their efforts to deal with changes to Canada’s pension system?

Rate of changes to Canada’s pension systemBy age 2010

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 6 20 50 2 22

9 25 40 1 25

7 19 46 3 26

4 18 52 3 23

5 18 55 2 20

4 20 56 2 17

Too fast

Just right

Too slow

Not aware of changes

dk/na

Atlantic: 3% too fast, 50% too slow, 21% just right

Prairies: 4% too fast, 46% too slow, 20% just right

BC: 6% too fast, 40% too slow, 26% just right

5ENVIRONICS

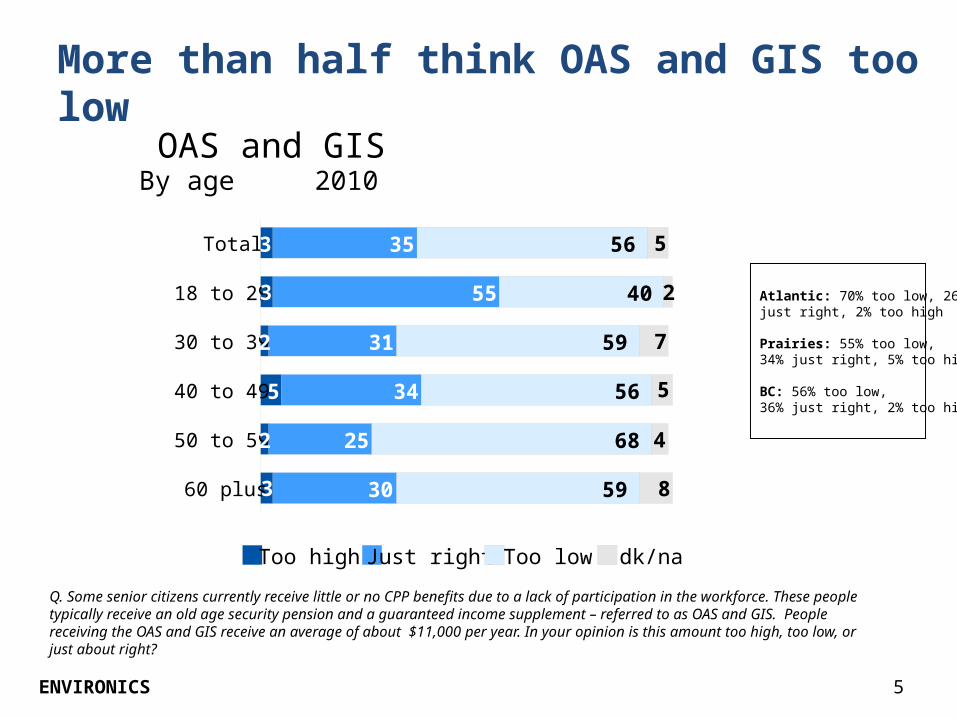

More than half think OAS and GIS too low

OAS and GISBy age 2010

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 3 35 56 5

3 55 40 2

2 31 59 7

5 34 56 5

2 25 68 4

3 30 59 8

Too high Just right Too low dk/na

Q. Some senior citizens currently receive little or no CPP benefits due to a lack of participation in the workforce. These people typically receive an old age security pension and a guaranteed income supplement – referred to as OAS and GIS. People receiving the OAS and GIS receive an average of about $11,000 per year. In your opinion is this amount too high, too low, or just about right?

Atlantic: 70% too low, 26%just right, 2% too high

Prairies: 55% too low,34% just right, 5% too high

BC: 56% too low,36% just right, 2% too high

6ENVIRONICS

Large majority support increasing OAS and GIS

Increase to OAS and GIS for those livingbelow poverty lineBy age 2010

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 61 20 7 6 5

53 26 10 8 2

60 23 10 4 3

58 23 7 6 6

65 18 6 5 5

69 13 2 7 9

Support – feels strongly

Support – does not feel strongly

Oppose – does not feel strongly

Oppose – feels strongly

dk/na

Q. It is estimated that approximately 200,000 Canadians live only on the OAS and GIS and are below the poverty line. Knowing this, would you support or oppose increasing the payments to these senior citizens? Do you feel strongly or not?

Atlantic: 74% strongly support, 14% support somewhat = 88% support

Prairies: 60% strongly support, 17% support somewhat = 77% support

BC: 58% support strongly, 22% support somewhat = 80% support

7ENVIRONICS

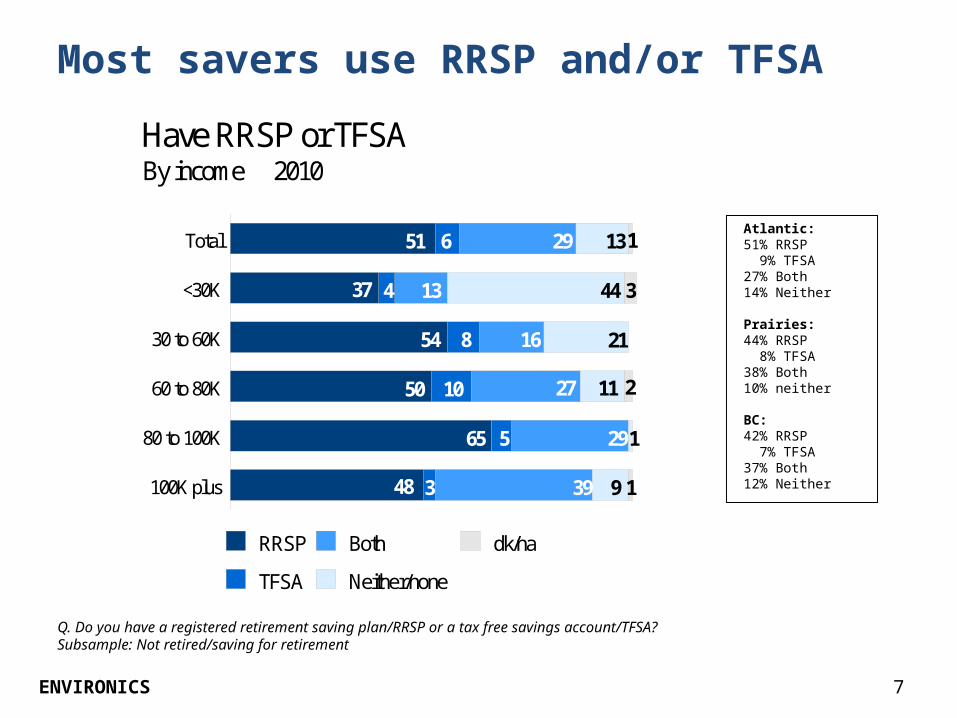

Most savers use RRSP and/or TFSA

Q. Do you have a registered retirement saving plan/RRSP or a tax free savings account/TFSA?Subsample: Not retired/saving for retirement

Have RRSP or TFSABy income 2010

100K plus

80 to 100K

60 to 80K

30 to 60K

<30K

Total 51 6 29 13 1

37 4 13 44 3

54 8 16 21

50 10 27 11 2

65 5 291

48 3 39 9 1

RRSP

TFSA

Both

Neither/none

dk/na

Atlantic:51% RRSP 9% TFSA27% Both14% Neither

Prairies:44% RRSP 8% TFSA38% Both10% neither

BC:42% RRSP 7% TFSA37% Both12% Neither

8ENVIRONICS

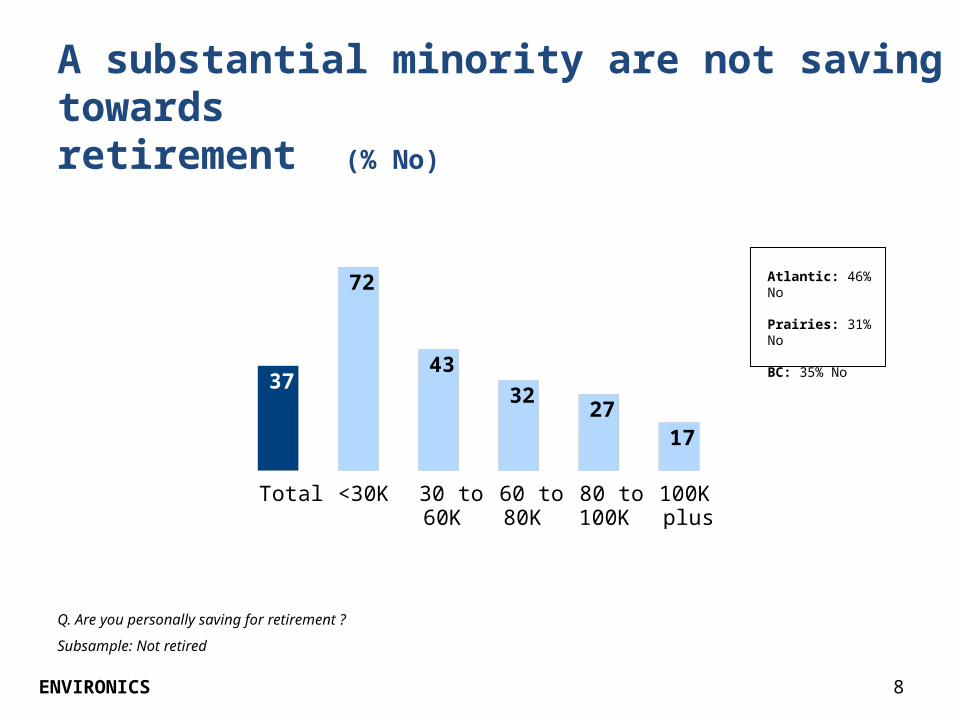

A substantial minority are not saving towardsretirement (% No)

Q. Are you personally saving for retirement ?

Subsample: Not retired

Total <30K 30 to60K

60 to80K

80 to100K

100Kplus

37

72

43

3227

17

Atlantic: 46% No

Prairies: 31% No

BC: 35% No

9ENVIRONICS

…primarily because they cannot afford it

Q. What are some of the reasons why you are not currently saving for retirement [IF HAVE PENSION: outside of your pension]?

Subsample: Not retired and not saving for retirement

dk/na

Other

Need information

Already old/retired/semi-retired

Don’t need to save/have pension at work

Not thinking about retirement/still young/other priorities

Not worried about retirement

Can’t afford/don’t have money 74

9

6

4

1

1

6

3

Atlantic: 70% can’t afford/don’t have money

Prairies: 68% can’t afford/don’t have money

BC: 81% can’t afford/don’t have money

10ENVIRONICS

More than half of Canadians say their income is not always sufficient to cover essentials

Q. Thinking about your household expenditures on essentials (rent or mortgage payments, utilities, or food and clothing), would you say your current household income is always sufficient, is often sufficient or is rarely sufficient to meet these essential expenditures?

Always Often Rarely Never dk/na

44 4132

41

2115

2 1 3

2001 2010

n/a

Atlantic:40% Always41% Often16% Rarely

Prairies:45% Always38% Often13% Rarely

BC:49% Always30% Often16% Rarely

11ENVIRONICS

Canadians tentative about ability to save for retirement

Q. Thinking about your financial future, how confident are you that you will be able to save enough to support yourself in retirement? Are you very confident, somewhat confident, not very confident or not at all confident?

Subsample: Not retired

Confidence in retirement savingBy age 2010

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 25 42 20 12 1

33 44 14 7 1

25 39 24 10 1

17 42 23 16 1

23 41 23 13 0.5

24 40 16 16 4

Very confident

Somewhat confident

Not very confident

Not at all confident

dk/na

Atlantic:27% Very confident42% Somewhat confident17% Not very confident12% Not at all confident

Prairies:29% Very confident45% Somewhat confident13% Not very confident12% Not at all confident

BC:25% Very Confident36% Somewhat confident22% Not very confident13% Not at all confident

12ENVIRONICS

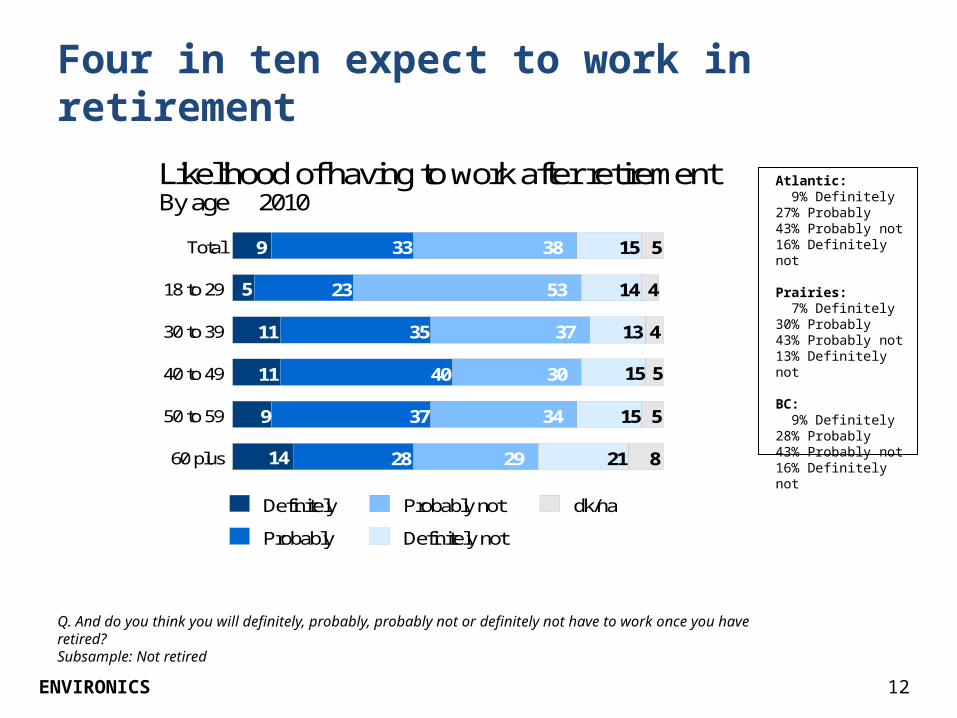

Four in ten expect to work in retirement

Likelihood of having to work after retirementBy age 2010

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 9 33 38 15 5

5 23 53 14 4

11 35 37 13 4

11 40 30 15 5

9 37 34 15 5

14 28 29 21 8

Definitely

Probably

Probably not

Definitely not

dk/na

Q. And do you think you will definitely, probably, probably not or definitely not have to work once you have retired?Subsample: Not retired

Atlantic: 9% Definitely27% Probably43% Probably not16% Definitely not

Prairies: 7% Definitely30% Probably43% Probably not13% Definitely not

BC: 9% Definitely28% Probably43% Probably not16% Definitely not

13ENVIRONICS

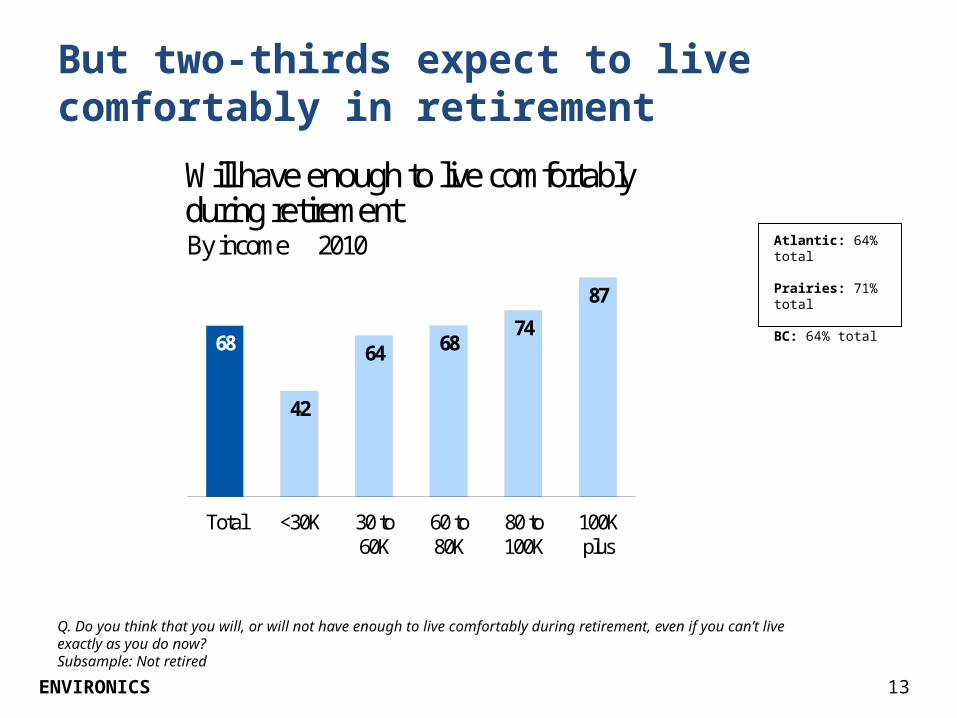

But two-thirds expect to live comfortably in retirement

Q. Do you think that you will, or will not have enough to live comfortably during retirement, even if you can’t live exactly as you do now?Subsample: Not retired

Will have enough to live comfortablyduring retirementBy income 2010

Total <30K 30 to 60K

60 to 80K

80 to 100K

100K plus

68

42

64 6874

87

Atlantic: 64% total

Prairies: 71% total

BC: 64% total

14ENVIRONICS

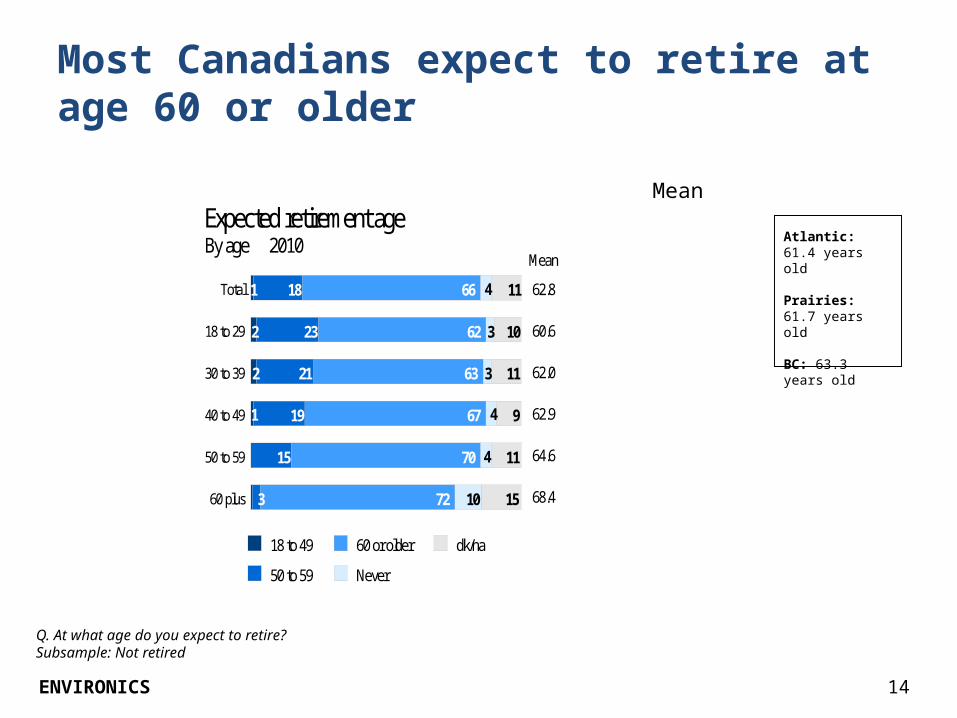

Most Canadians expect to retire at age 60 or older

Expected retirement ageBy age 2010

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 1 18 66 4 11

2 23 62 3 10

2 21 63 3 11

1 19 67 4 9

15 70 4 11

0.53 72 10 15

18 to 49

50 to 59

60 or older

Never

dk/na

62.8

60.6

62.0

62.9

64.6

68.4

Mean

Mean

Q. At what age do you expect to retire? Subsample: Not retired

Atlantic: 61.4 years old

Prairies: 61.7 years old

BC: 63.3 years old

15ENVIRONICS

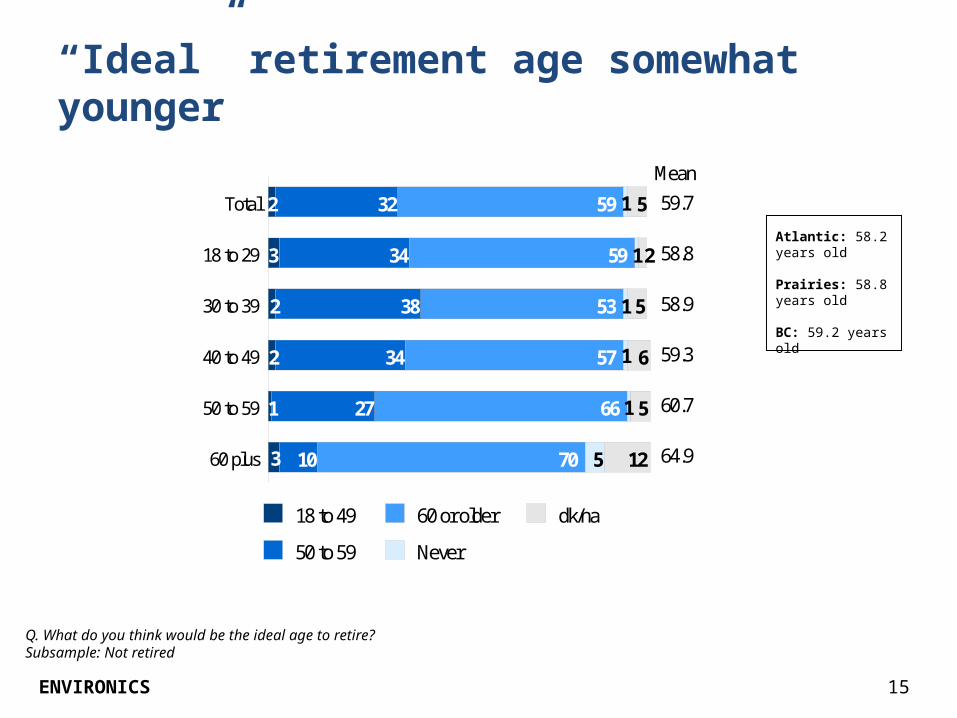

“Ideal” retirement age somewhat younger

Q. What do you think would be the ideal age to retire? Subsample: Not retired

60 plus

50 to 59

40 to 49

30 to 39

18 to 29

Total 2 32 59 1 5

3 34 59 1 2

2 38 53 1 5

2 34 57 1 6

1 27 66 1 5

3 10 70 5 12

18 to 49

50 to 59

60 or older

Never

dk/na

59.7

58.8

58.9

59.3

60.7

64.9

Mean

Atlantic: 58.2 years old

Prairies: 58.8 years old

BC: 59.2 years old

16ENVIRONICS

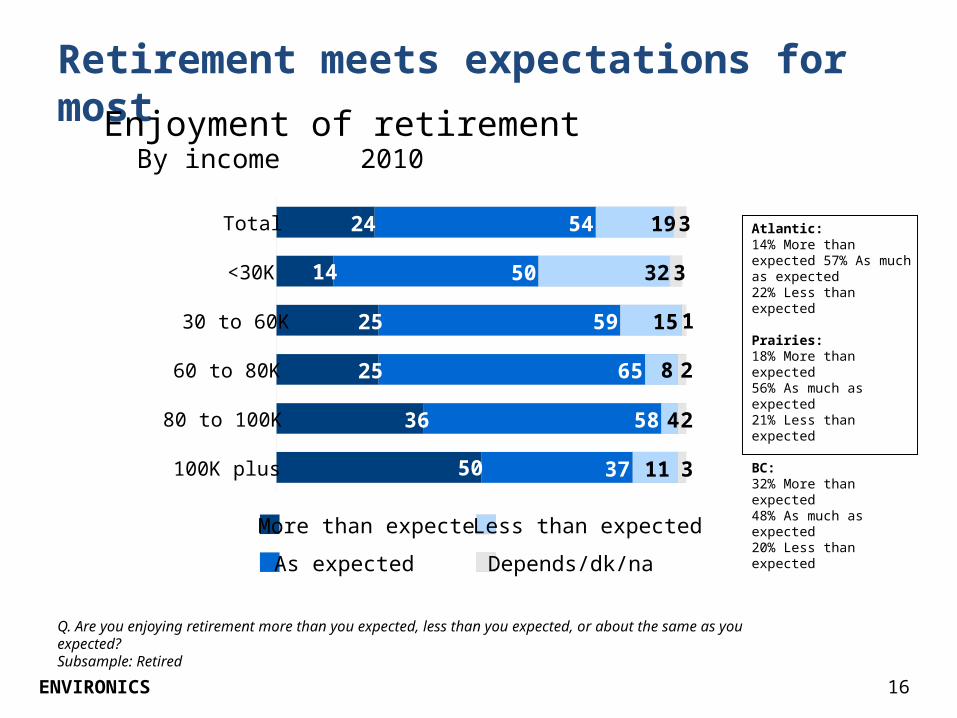

Retirement meets expectations for most

Q. Are you enjoying retirement more than you expected, less than you expected, or about the same as you expected?Subsample: Retired

Enjoyment of retirementBy income 2010

100K plus

80 to 100K

60 to 80K

30 to 60K

<30K

Total 24 54 19 3

14 50 32 3

25 59 15 1

25 65 8 2

36 58 4 2

50 37 11 3

More than expected

As expected

Less than expected

Depends/dk/na

Atlantic:14% More than expected 57% As much as expected22% Less than expected

Prairies:18% More than expected56% As much as expected21% Less than expected

BC:32% More than expected48% As much as expected20% Less than expected

17ENVIRONICS

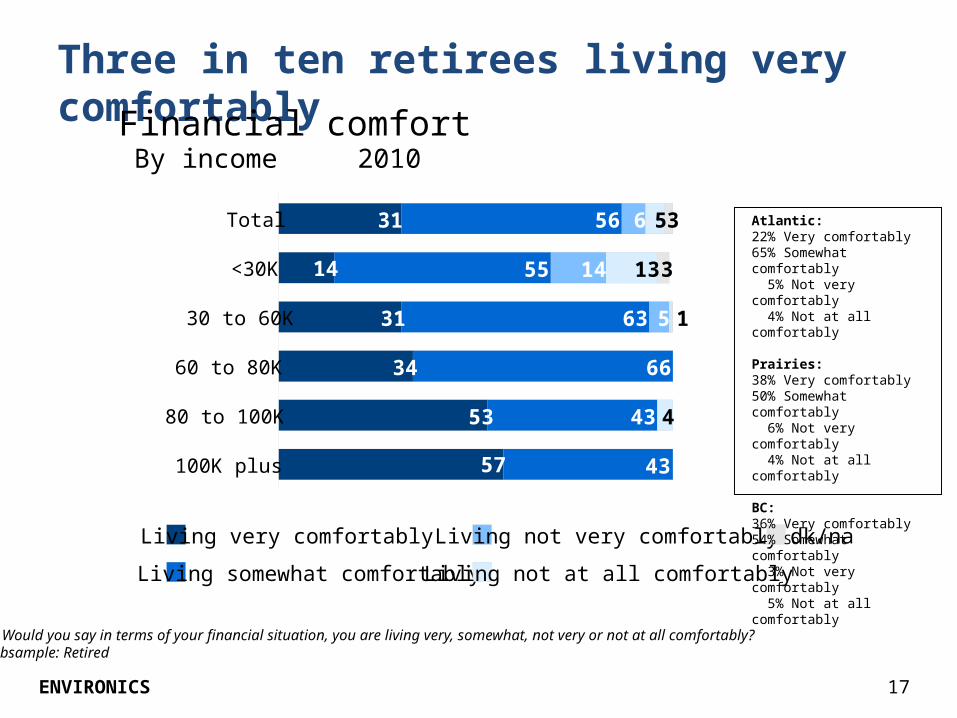

Three in ten retirees living very comfortably

Q. Would you say in terms of your financial situation, you are living very, somewhat, not very or not at all comfortably?Subsample: Retired

Financial comfortBy income 2010

100K plus

80 to 100K

60 to 80K

30 to 60K

<30K

Total 31 56 6 5 3

14 55 14 13 3

31 63 5 1

34 66

53 43 4

57 43

Living very comfortably

Living somewhat comfortably

Living not very comfortably

Living not at all comfortably

dk/na

Atlantic:22% Very comfortably65% Somewhat comfortably 5% Not very comfortably 4% Not at all comfortably

Prairies:38% Very comfortably50% Somewhat comfortably 6% Not very comfortably 4% Not at all comfortably

BC:36% Very comfortably54% Somewhat comfortably 3% Not very comfortably 5% Not at all comfortably

18ENVIRONICS

Most rely on a mix of retirement income sourcesSources of retirement income2010

dk/na

Other

Company/privatepension plan

Other savings/investments

RRSP/TFSA

Canada Pension Plan/other government pension

55

72

54

30

38

34

36

42

2

5

5

3

Anticipated – not yet retired

Current – already retired

Q. Retired: What are your current sources of retirement income?Q. Not retired: When you retire, on what sources of retirement income do you plan on relying?

Atlantic Prairies BC

67% 60% 60%

74% 77% 74%

46% 64% 46%

25% 32% 37%

34% 48% 44%

23% 37% 39%

53% 46% 34%

42% 49% 53%

19ENVIRONICS

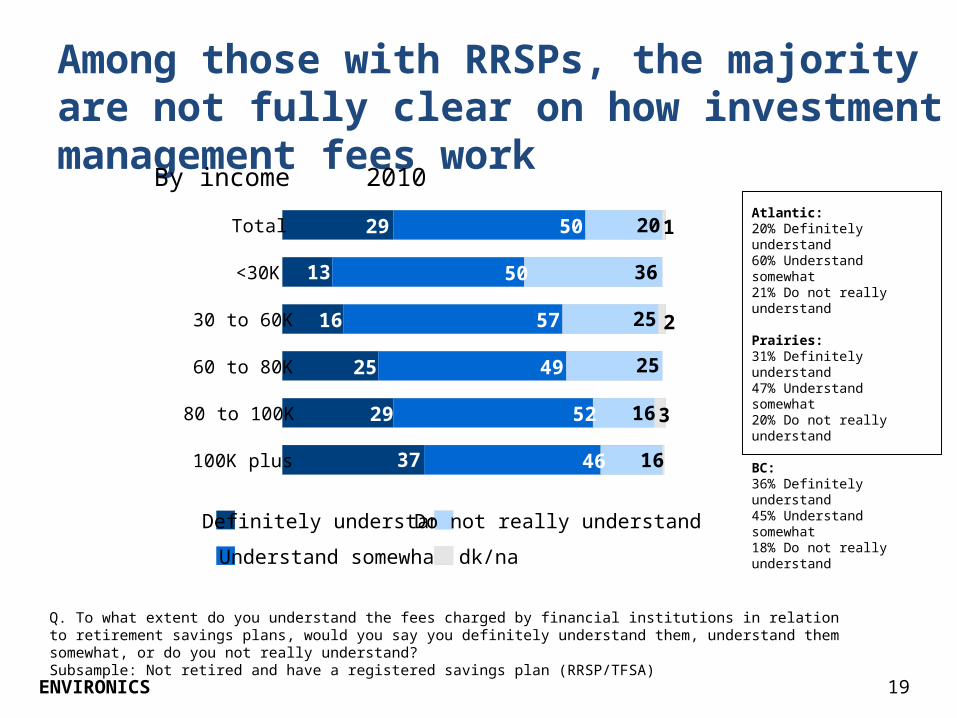

Among those with RRSPs, the majority are not fully clear on how investment management fees work

Q. To what extent do you understand the fees charged by financial institutions in relation to retirement savings plans, would you say you definitely understand them, understand them somewhat, or do you not really understand?Subsample: Not retired and have a registered savings plan (RRSP/TFSA)

By income 2010

100K plus

80 to 100K

60 to 80K

30 to 60K

<30K

Total 29 50 20 1

13 50 36

16 57 25 2

25 49 25

29 52 16 3

37 46 16 0.5

Definitely understand

Understand somewhat

Do not really understand

dk/na

Atlantic:20% Definitely understand60% Understand somewhat21% Do not really understand

Prairies:31% Definitely understand47% Understand somewhat20% Do not really understand

BC:36% Definitely understand45% Understand somewhat18% Do not really understand

20ENVIRONICS

Type of pension held is at odds with preferences

Q. Is your company pension the type that guarantees you a fixed amount of benefits when you retire, known as a defined benefit pension? Or is it one where the amount of benefits you will receive will vary depending on how well the pension fund investments perform, known as a defined contribution pension?Q. In your view, which of these two types of pensions is preferable, defined benefit, which pays a fixed amount when you retire, or defined contribution, where the amount of benefits received varies depending on the performance of the fund?

Subsample: Not retired, has a company or private pension plan

Fixed amount/defined benefit

Benefits vary/defined contribution

dk/na

42

68

39

22 20

10

Actual

Preferred

Atlantic 44% 61% 32% 27% 24% 12%

Prairies 43% 66% 37% 25% 20% 9%

BC 49% 77% 28% 11% 23% 12%

21ENVIRONICS

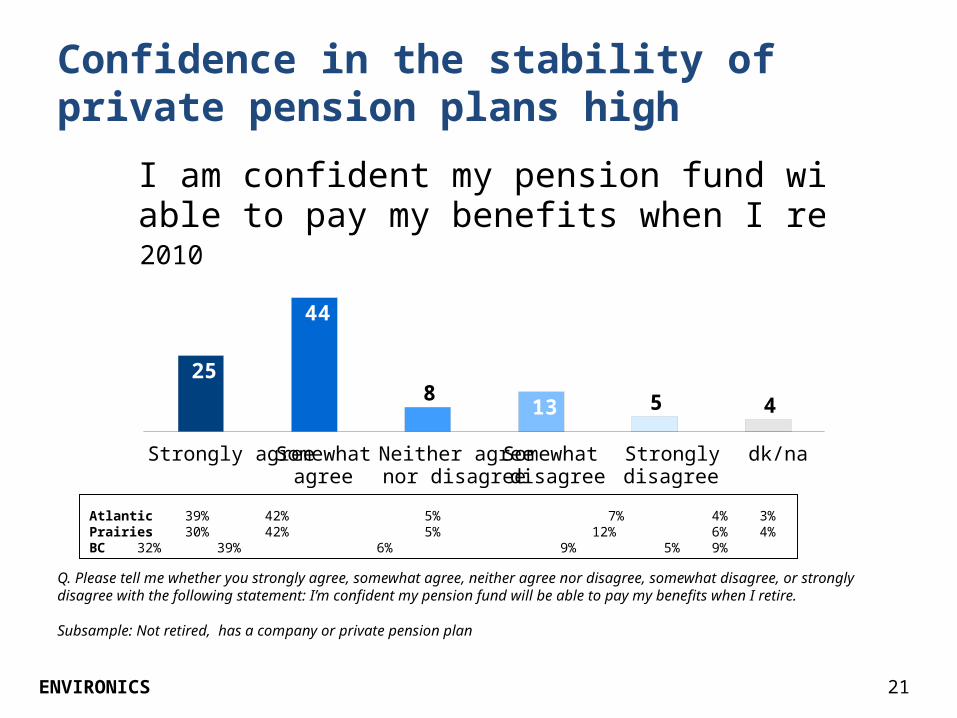

Confidence in the stability of private pension plans high

Q. Please tell me whether you strongly agree, somewhat agree, neither agree nor disagree, somewhat disagree, or strongly disagree with the following statement: I’m confident my pension fund will be able to pay my benefits when I retire.

Subsample: Not retired, has a company or private pension plan

Strongly agree Somewhat agree

Neither agree nor disagree

Somewhat disagree

Strongly disagree

dk/na

25

44

813 5 4

I am confident my pension fund will beable to pay my benefits when I retire2010

Atlantic 39% 42% 5% 7% 4% 3%Prairies 30% 42% 5% 12% 6% 4%BC 32% 39% 6% 9% 5% 9%

22ENVIRONICS

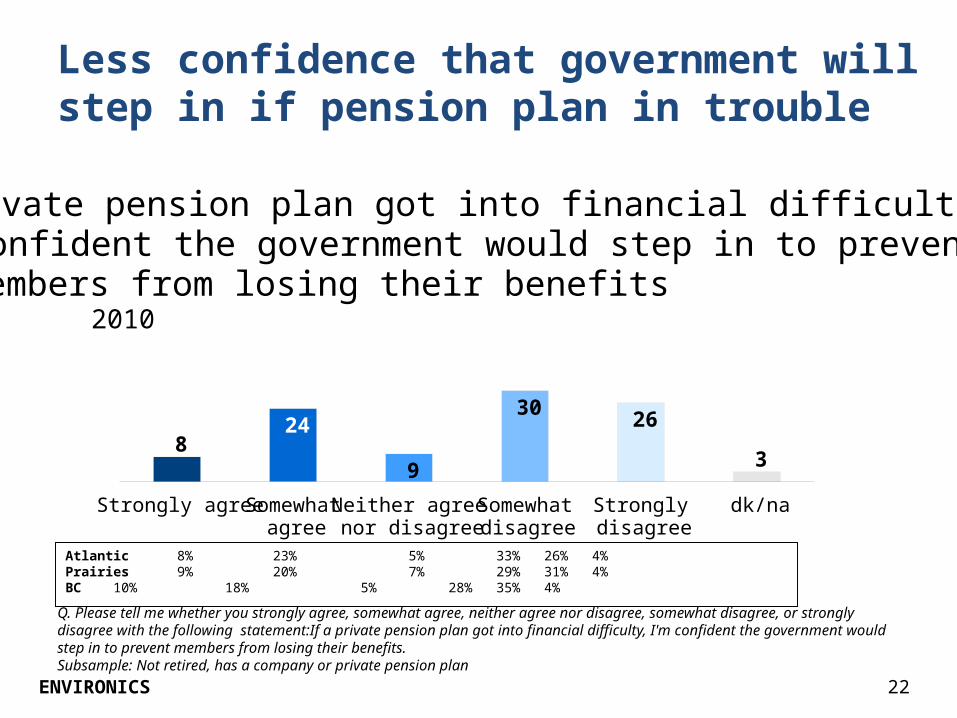

Less confidence that government will step in if pension plan in trouble

Q. Please tell me whether you strongly agree, somewhat agree, neither agree nor disagree, somewhat disagree, or strongly disagree with the following statement:If a private pension plan got into financial difficulty, I'm confident the government would step in to prevent members from losing their benefits. Subsample: Not retired, has a company or private pension plan

Strongly agree Somewhat agree

Neither agree nor disagree

Somewhat disagree

Strongly disagree

dk/na

824

9

30 26

3

If a private pension plan got into financial difficulty,I'm confident the government would step in to preventmembers from losing their benefits2010

Atlantic 8% 23% 5% 33% 26% 4%Prairies 9% 20% 7% 29% 31% 4%BC 10% 18% 5% 28% 35% 4%

23ENVIRONICS

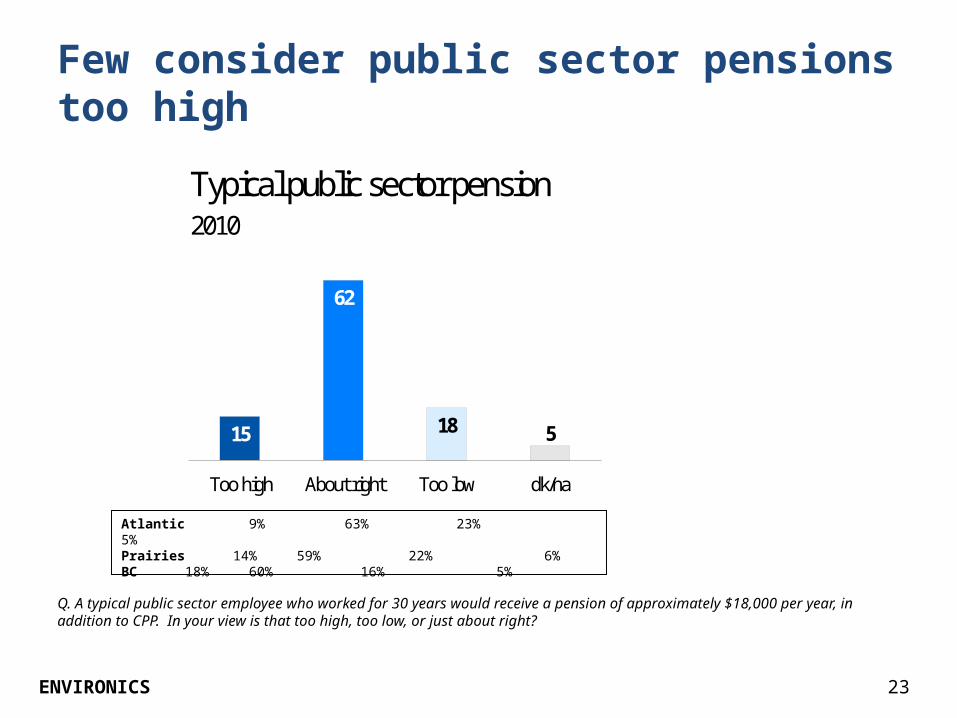

Few consider public sector pensions too high

Typical public sector pension2010

Too high About right Too low dk/na

15

62

18 5

Q. A typical public sector employee who worked for 30 years would receive a pension of approximately $18,000 per year, in addition to CPP. In your view is that too high, too low, or just about right?

Atlantic 9% 63% 23% 5%Prairies 14% 59% 22% 6%BC 18% 60% 16% 5%

www.EnvironicsResearch.ca

Tony CoulsonVice President

Environics Research Group [email protected]

613-230-5089