63

Driving Growth. Delivering Performance. The Past, Present and Future of Retail – Global Perspectives Chris Baker Senior Vice President, Head of Retail North America, Visa

Driving Growth.

Delivering Performance.

The Past, Present and Future of Retail –Global Perspectives

Chris Baker

Senior Vice President,

Head of Retail

North America, Visa

©2020 Visa. All rights reserved. Visa confidential

Agenda

Innovation and disruption – a brief history

The changing consumer

The current state and future of retail

Take home implications

1

2

3

4

©2020 Visa. All rights reserved. Visa confidential

Agenda

Innovation and disruption – a brief history

The changing consumer

The current state and future of retail

Take home implications

1

2

3

4

©2020 Visa. All rights reserved. Visa confidential

Industrial revolutions make it crucial for market leaders to anticipate and prepare for the future

Source: World Economic Forum

1785 20301845 1900 1950 2000

Inn

ova

tio

n

ElectricityChemicals

Combustion Engine

3rd revolution

ELECTRICITY1890-1920

ElectronicsAviationSpace

Services

4th revolution

INDUSTRY2.01950-1980

5th Revolution

DIGITAL2000-2030

Steam powerRailroad

SteelCotton

2nd revolution

STEAMLate 1800s

1st revolution

INDUSTRY 1.0Late 1700s

MechanizationManufacturing

Textile

©2020 Visa. All rights reserved. Visa confidential

In the digital revolution, waves of innovation are accelerating

Source: IDC, Internet World Stats, company filings

Huge innovation boost

Significant changes in consumption behaviors

New disruption every 2-3 years

% WW connected pop. 55%12%1% 24% 37%

1997 2004 2008 2011 2014 2017 2020

Data /A.I. economy

Wave 1Search

Wave 2Transactions

Wave 3 Social

Wave 4Experience

Wave 5Global omni-

platforms

©2020 Visa. All rights reserved. Visa confidential

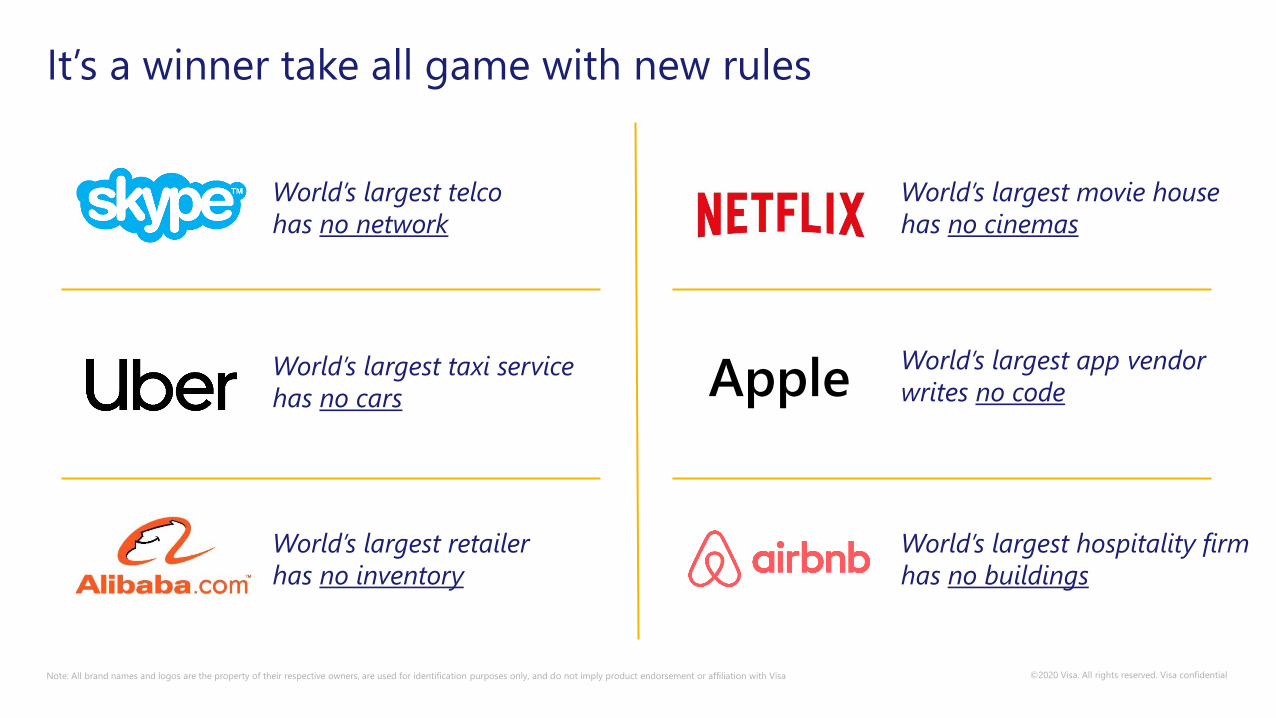

It’s a winner take all game with new rules

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

World’s largest telco

has no network

World’s largest taxi service

has no cars

World’s largest retailer

has no inventory

World’s largest movie house

has no cinemas

World’s largest app vendor

writes no code

World’s largest hospitality firm

has no buildings

Apple

©2020 Visa. All rights reserved. Visa confidential

Agenda

Innovation and disruption – a brief history

The changing consumer

The current state and future of retail

Take home implications

1

2

3

4

©2020 Visa. All rights reserved. Visa confidential

Consumers are also changing fast…

Sources: US Census Bureau, Pew Research Center, GSMA

…and enabling rapid change

©2020 Visa. All rights reserved. Visa confidential

Control Flexibility Personalization Speed

Instantism

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

Agenda

Innovation and disruption – a brief history

The changing consumer

The current state and future of retail

Take home implications

1

2

3

4

©2020 Visa. All rights reserved. Visa confidential

A tale of two retail worlds…

©2020 Visa. All rights reserved. Visa confidential

E-commerce continues to gain share globally and will rise to approximately 1/4 of all retail sales over the next five years

eMarketer Global Ecommerce 2019

Global Retail E-commerce Sales

10%

12%

14%

16%

18%

20%

22%28%

23%

21%

19%

17%

16% 15%

$7T

$4T

$0T

$2T

$1T

$3T

$5T

$6T

0%

5%

10%

15%

20%

25%

30%

20212017 2018 2019 2020 2022 2023

% ChangeRetail Ecommerce Sales % of Total Retail Sales

©2020 Visa. All rights reserved. Visa confidential

The picture is very different depending on retail category

eMarketer Global Ecommerce 2019.

Electronics

Books, Music, Video

2%

Apparel

Home Food & BeveragePersonal Care & Health

11%

49%

39%

25%

22%

10%

Total US Retail

E-commerce share of total sales by category, 2019 (U.S. only)

©2020 Visa. All rights reserved. Visa confidential©2019 Visa. All rights reserved. Visa confidential

I would not

shop online11%

I would shop online

with fewer hassles35%

I already shop

online some of

the time

54%

In Apparel, most customers already shop online

Source: 2018 Oliver Wyman Digital Shopping Survey

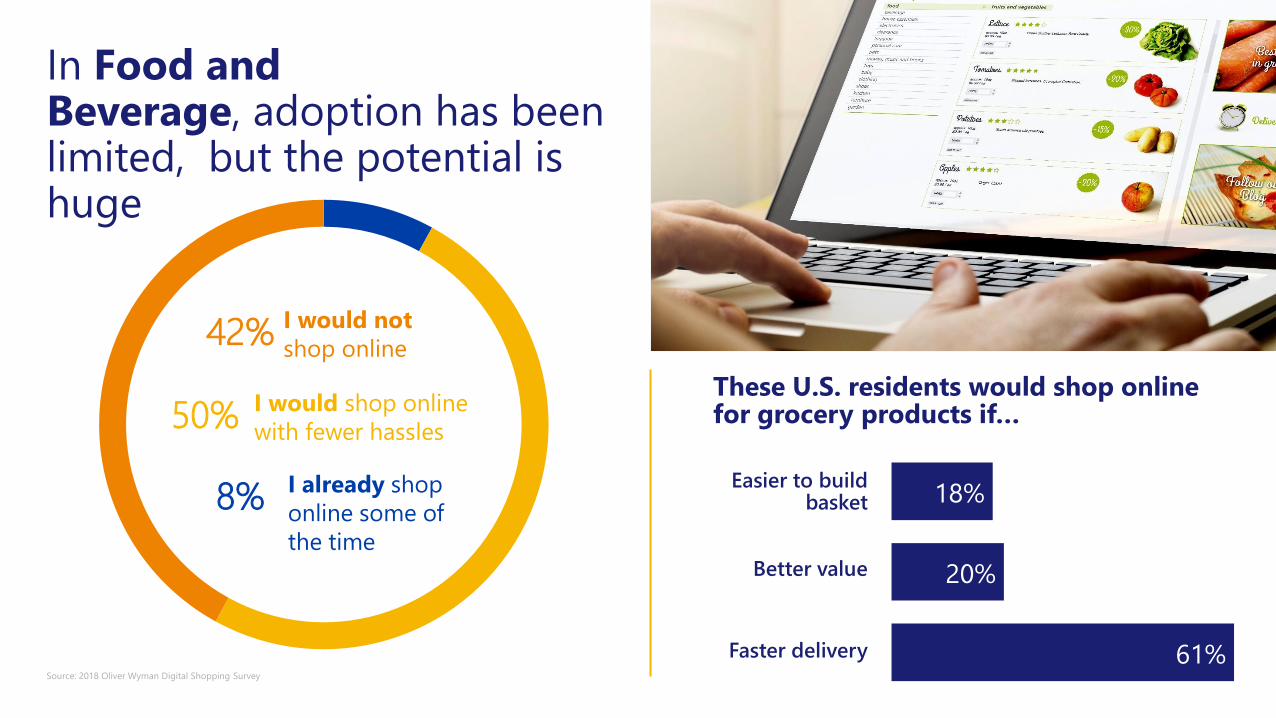

©2020 Visa. All rights reserved. Visa confidential©2019 Visa. All rights reserved. Visa confidential

I would not

shop online42%

I would shop online

with fewer hassles50%

I already shop

online some of

the time

8%

In Food and Beverage, adoption has been limited, but the potential is huge

Source: 2018 Oliver Wyman Digital Shopping Survey

These U.S. residents would shop online for grocery products if…

61%

20%

18%

Faster delivery

Better value

Easier to buildbasket

©2020 Visa. All rights reserved. Visa confidential

Challenges Solutions Example

Shopping experience built around

item selection

Plugins for featured products

Recipe boxes on subscription

Expensive fulfillment of

individual orders

Automated picking technologies

In-store order fulfilment

High delivery costs for fresh and

refrigerated products

Passive cooling

Food freshness tracking

Infrequent drops Retailer-logistics partnerships

Dynamic routing

Delivering fresh products when

customers are away from home

Refrigerated lockers

In-home delivery service

Barriers are coming down quickly…

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

Delivery

was

faster

Better

value

Easier to

build

basket

©2020 Visa. All rights reserved. Visa confidential©2019 Visa. All rights reserved. Visa confidential

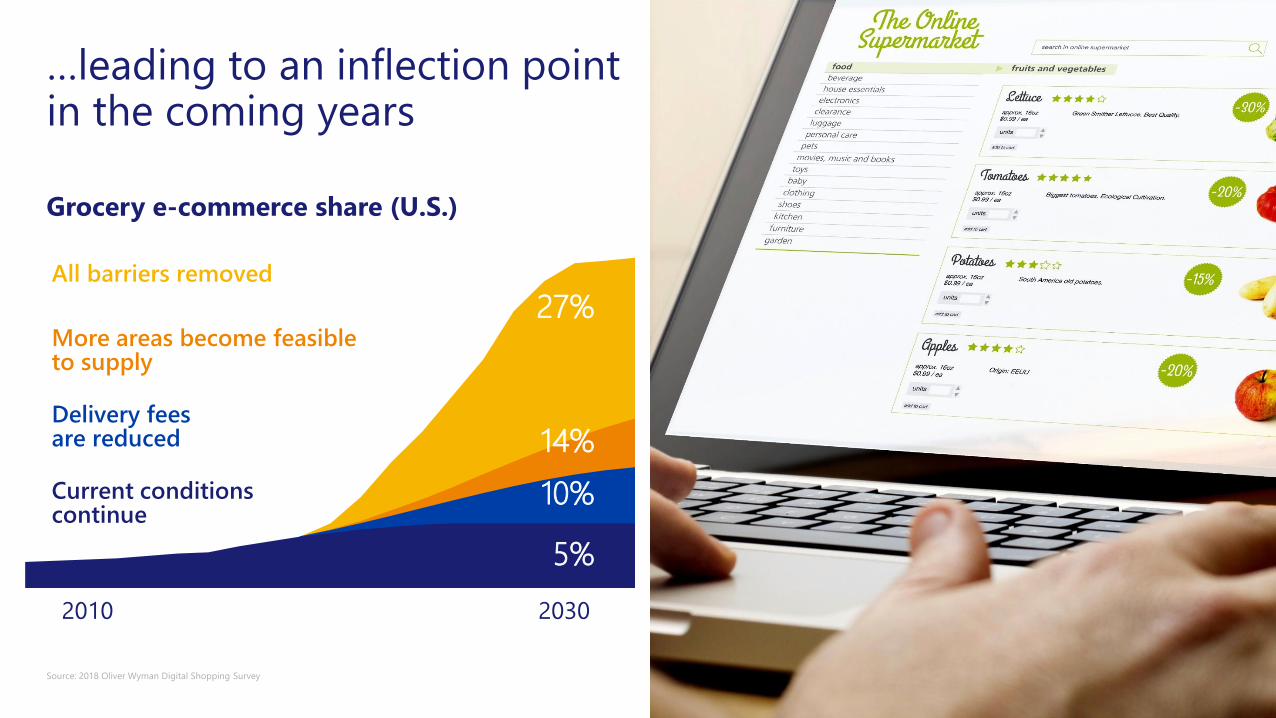

…leading to an inflection point in the coming years

Source: 2018 Oliver Wyman Digital Shopping Survey

2010 2030

Grocery e-commerce share (U.S.)

27%All barriers removed

14%

More areas become feasible to supply

10%

Delivery feesare reduced

Current conditions continue

5%

©2020 Visa. All rights reserved. Visa confidential

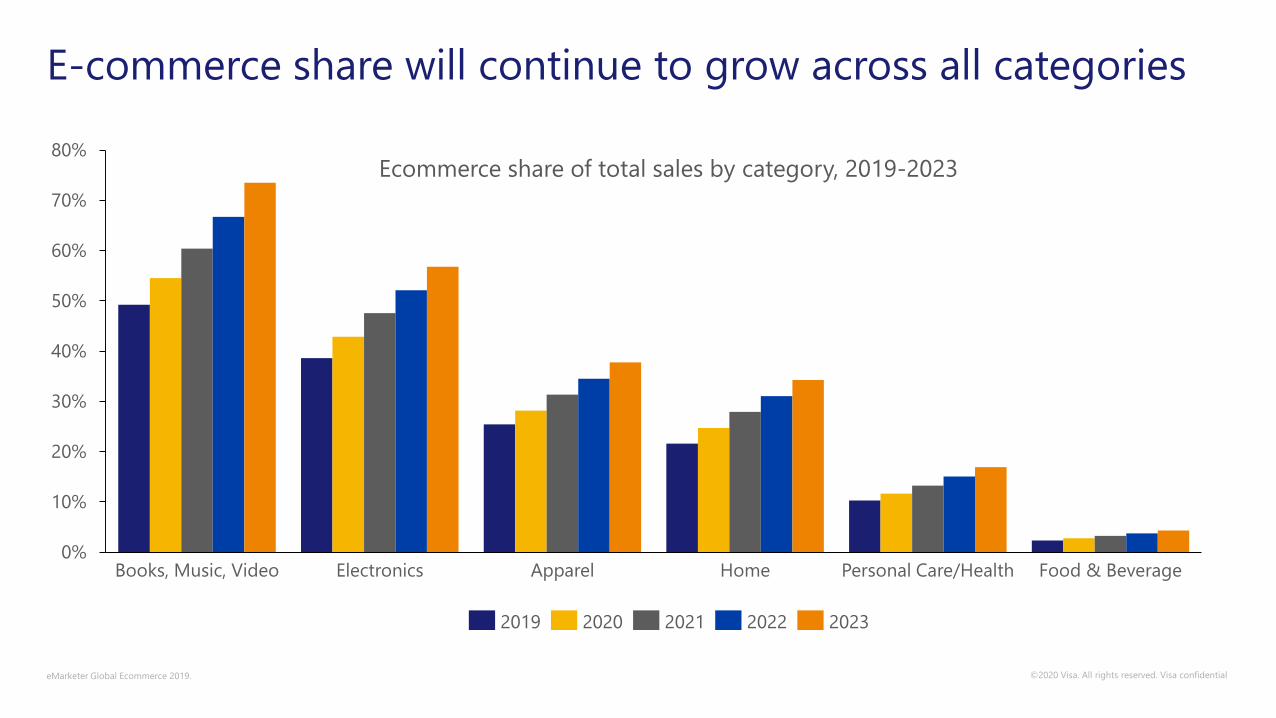

E-commerce share will continue to grow across all categories

eMarketer Global Ecommerce 2019.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Books, Music, Video Food & BeverageHomeElectronics Apparel Personal Care/Health

2019 2020 20222021 2023

Ecommerce share of total sales by category, 2019-2023

©2020 Visa. All rights reserved. Visa confidential

The picture is very different by geography, with China leading the way in terms of total e-commerce volume ($USD in 2019)

eMarketer Global Ecommerce 2019.

1.9T 586B 141B 115B 103B

82B 69B 50B 46B 27B

©2020 Visa. All rights reserved. Visa confidential

MENA is expected to see the most growth in the coming years

Source: Business Insider, The Future of Retail, December 2019.

1519

2329

3441

2019 20212020 2022 2023 2024

Total ecommerce volume ($USD B)

©2020 Visa. All rights reserved. Visa confidential

At a market or city level, the penetration of e-commerce and the prevailing fulfillment channel(s) will be highly variable

SHANGHAI MARSEILLE ST. LOUIS

©2020 Visa. All rights reserved. Visa confidential

A tale of two retail worlds…

©2020 Visa. All rights reserved. Visa confidential

The rise of online does not meanstores are dead!

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

Brick & mortar still dominates in the US and most markets…

Source: Business Insider, The Future of Retail, December 2019., figures represent end of Q3 in each year

9% 10% 12%

91% 90% 88%Offline

2017 2018 2019

Ecommerce

Share of US adjusted retail (2017-2019)

©2020 Visa. All rights reserved. Visa confidential

…but the role of the store needs to evolve!

Source: Business Insider, The Future of Retail, December 2019.

3.900

2.5002.100

1.800

3.100

5.100

2.400

7.800

5.500

9.271

2010 2011 201520132012 2014 2016 2017 2018 2019

Total Announced Store Closures in the US

©2020 Visa. All rights reserved. Visa confidential

Stores will look very different…

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

Less expensive to operate More experiential

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

…play new roles in omnichannel fulfillment…

In-store picking Dark stores and

central production

Drive up formats

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

…offer new, more seamless ways to shop and pay…

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

©2020 Visa. All rights reserved. Visa confidential

Autonomous checkout will expand

Source: Business Insider, The Future of Retail, December 2019.

Estimated # of stores

with autonomous checkout globally

500

1.500

3.000

5.000

7.250

10.000

2019 2020 2021 2022 2023 2024

40%

40%

15%

5%Unmanned

Convenience

Stores

Grocery Stores

Drug Stores

Small

Convenience

Stores

Types of stores

with autonomous checkout (by 2024)

©2020 Visa. All rights reserved. Visa confidential

Contactless (Tap to Pay) momentum will continue

Source: Business Insider, The Future of Retail, December 2019., Visa data

96%

62%70% 89%

©2020 Visa. All rights reserved. Visa confidential

A tale of two retail worlds…

©2020 Visa. All rights reserved. Visa confidential

…coming together to deliver a better overall experience for customers

Source: 2018 Oliver Wyman Digital Shopping Survey

80%

70%

60%

50%

40%

30%

20%

10%

0%

Electronics Apparel Grocery

Sector of Shopping

Level of

Satisfaction

Single Channel Multi-Channel

©2020 Visa. All rights reserved. Visa confidential©2019 Visa. All rights reserved. Visa confidential

The omni-channel revolution is happening…

but what is really happening?

©2020 Visa. All rights reserved. Visa confidential

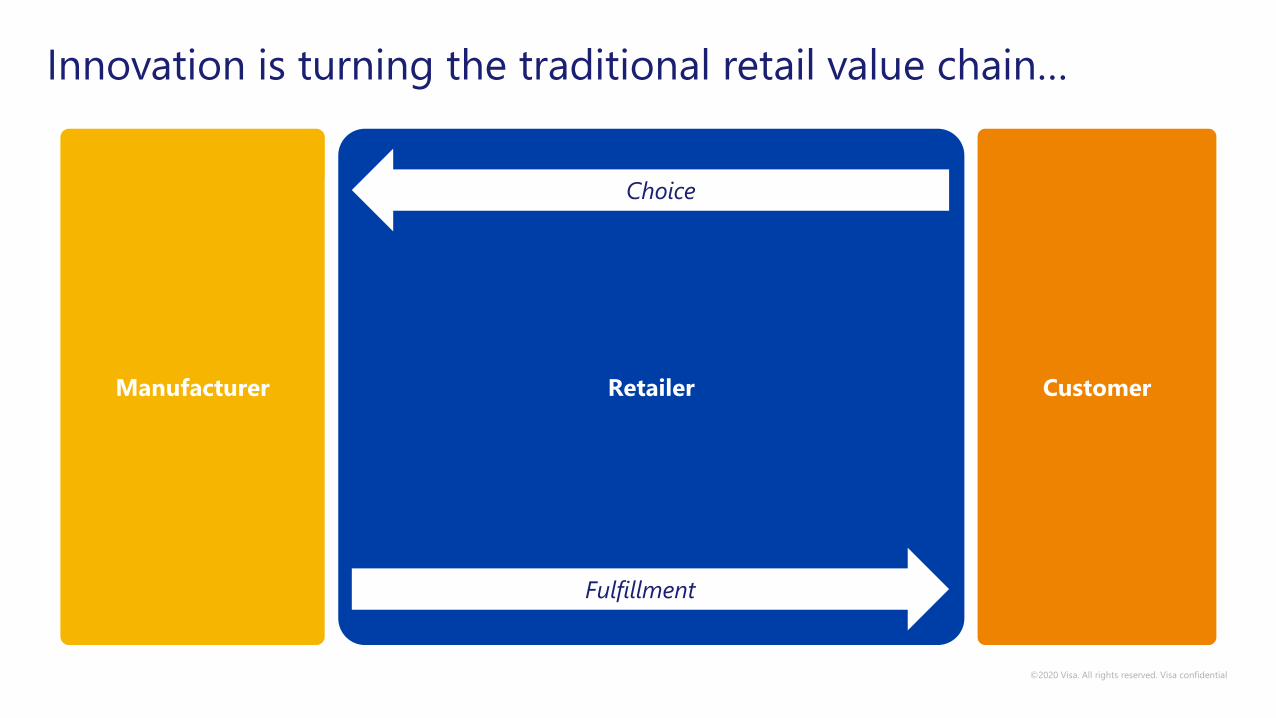

Innovation is turning the traditional retail value chain…

Manufacturer Retailer Customer

Fulfillment

Choice

©2020 Visa. All rights reserved. Visa confidential

…into this

Manufacturer

Retailer

Marketplaces

Direct-to-consumer

Fu

lfil

men

t in

term

ed

iary

Choice intermediary

Customer

©2020 Visa. All rights reserved. Visa confidential

“Direct to consumer” is not a new idea, but new commercial and service models make it appealing to consumers

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

Subscription ModelFlexible Trial-and-

Return Policy

Change in Price Point

vs. Incumbents

©2020 Visa. All rights reserved. Visa confidential

Delivery services (aka “fulfillment intermediaries”) are positioning themselves in between retailers and their customers

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

©2020 Visa. All rights reserved. Visa confidential

Digital assistants (aka “choice intermediaries”) could become a real threat to all incumbent players

Dinner for four

on Friday

night, please…le

t’s try

something new!

©2020 Visa. All rights reserved. Visa confidential

The “Marketplace” model is growing fast and now represents more than half of digital commerce globally

$515B $432B $344B $259B $96B

Largest Global Marketplaces by GMV (2018) in $USD

eMarketer Global Ecommerce 2019

©2020 Visa. All rights reserved. Visa confidential

Ecosystems that put it all together are locking in customers and building moats against competitors

Source: Daxue consulting, company filingsNote: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

Alibaba Tencent

Media &

Entertainment

Social

Choice

Local

Services

Technology/

R&DSearch Loyalty

Financial

Services

Logistics

O2O

Cloud

Computing

Commerce

PlatformsMarketing &

Data

Management

Media &

Entertainment

Social

Choice

Local

Services

Technology/

R&DSearch Loyalty

Financial

Services

Logistics

O2O

Cloud

Computing

Commerce

PlatformsMarketing &

Data

Management

©2020 Visa. All rights reserved. Visa confidential

Ecosystems that put it all together are locking in customers and building moats against competitors

Source: Company filingsNote: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

Amazon Walmart

Media &

Entertainment

Social

Choice

Local

Services

Technology/

R&D Search Loyalty

Financial

Services

Logistics

O2O

Cloud

Computing

Commerce PlatformsMarketing &

Data

Management

Media &

Entertainment

Social

Choice

Local

Services

Technology/

R&D

Loyalty

Financial

Services

Logistics

Cloud

Computing

Commerce

PlatformsMarketing &

Data

ManagementConnected

Life

Connected

Life

O2O

©2020 Visa. All rights reserved. Visa confidential

The new world of Retail

Manufacturer

Retailer

Marketplaces

Direct-to-consumer

Fu

lfil

men

t in

term

ed

iary

Choice intermediary

Customer

©2020 Visa. All rights reserved. Visa confidential

Major acquisitions:

As a result, we are seeing partnerships and M&A explode

Note: All brand names and logos are the property of their respective owners, are used for identification purposes only, and do not imply product endorsement or affiliation with Visa

Physical players seeking online capabilityOnline players seeking physical presence

+

Notable partnerships:

Major acquisitions:

Notable partnerships:

+

+

+

©2020 Visa. All rights reserved. Visa confidential

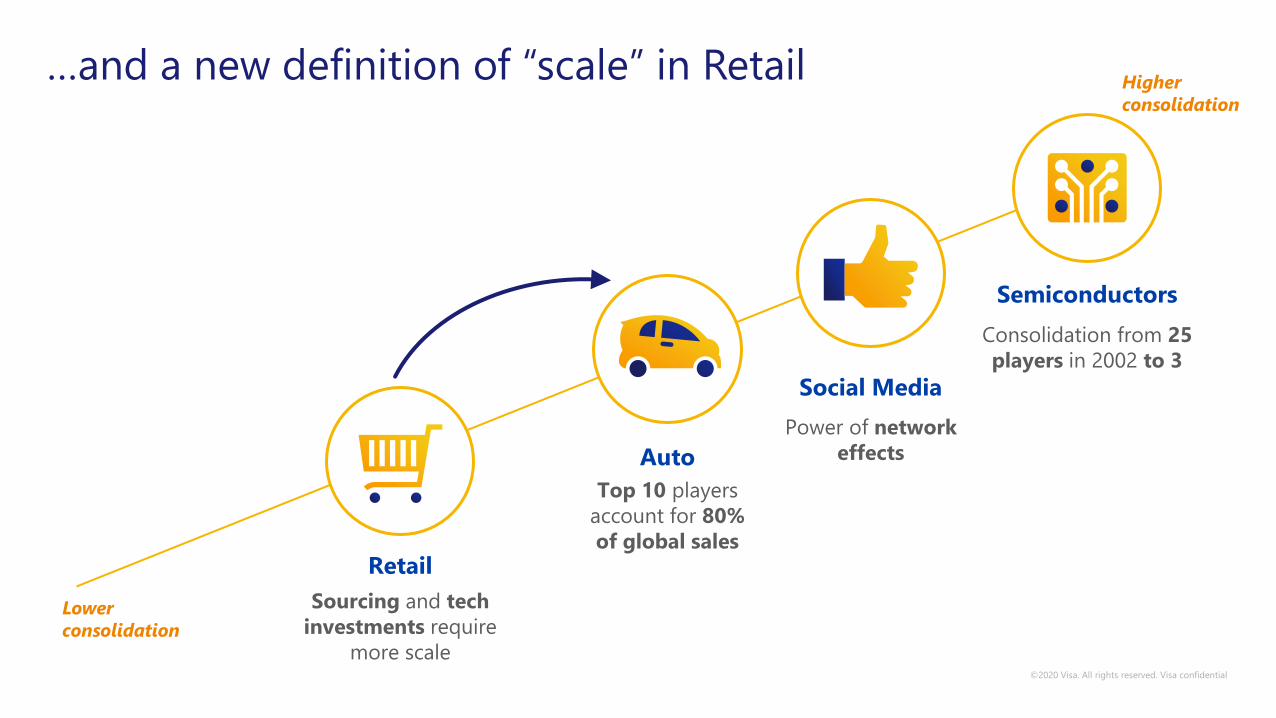

…and a new definition of “scale” in Retail

Retail

Sourcing and tech

investments require

more scale

Lower

consolidation

Higher

consolidation

Auto

Top 10 players

account for 80%

of global sales

Social Media

Power of network

effects

Semiconductors

Consolidation from 25

players in 2002 to 3

©2020 Visa. All rights reserved. Visa confidential

Six ways to win in the Future of Retail

Location Experience Product

Choice Fulfilment Ecosystems

©2020 Visa. All rights reserved. Visa confidential

Agenda

Innovation and disruption – a brief history

The changing consumer

The current state and future of retail

Take home implications

1

2

3

4

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

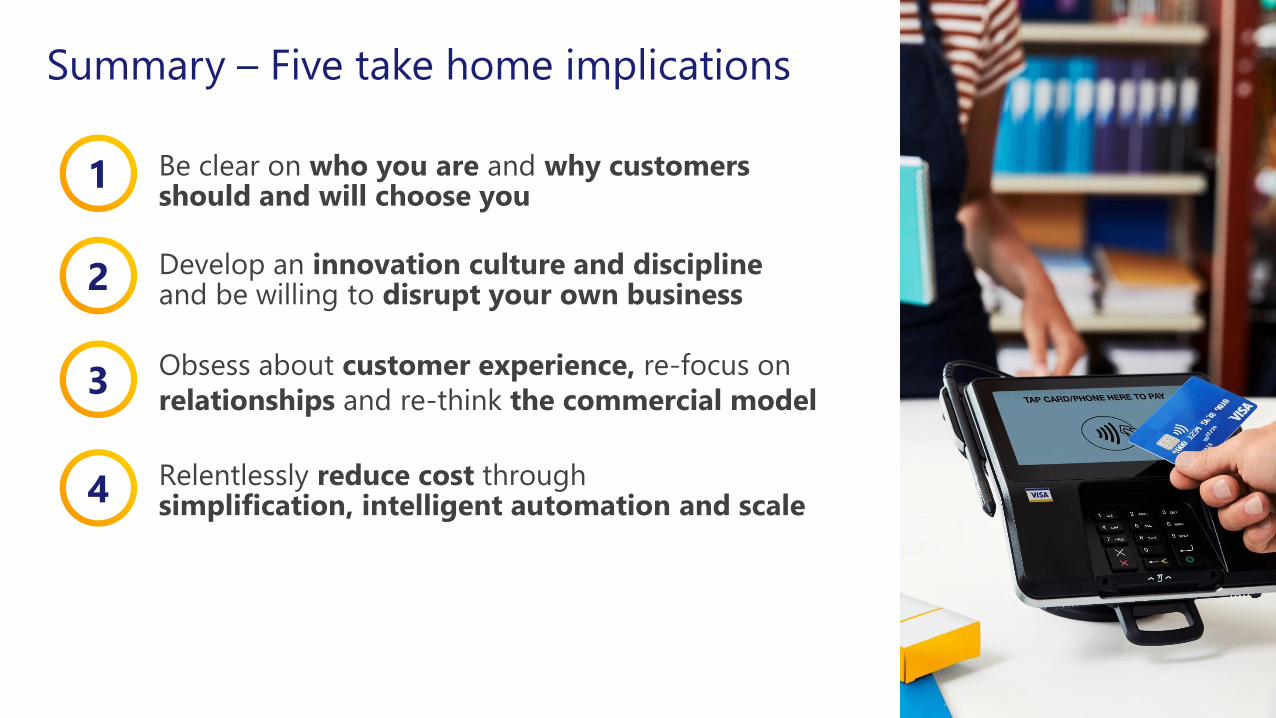

Summary – Five take home implications

©2020 Visa. All rights reserved. Visa confidential

Summary – Five take home implications

Be clear on who you are and why customers should and will choose you

1

©2020 Visa. All rights reserved. Visa confidential

Summary – Five take home implications

Be clear on who you are and why customers should and will choose you

Develop an innovation culture and discipline and be willing to disrupt your own business

1

2

©2020 Visa. All rights reserved. Visa confidential

Summary – Five take home implications

Be clear on who you are and why customers should and will choose you

Obsess about customer experience, re-focus on

relationships and re-think the commercial model

Develop an innovation culture and discipline and be willing to disrupt your own business

1

2

3

©2020 Visa. All rights reserved. Visa confidential

Summary – Five take home implications

Be clear on who you are and why customers should and will choose you

Obsess about customer experience, re-focus on

relationships and re-think the commercial model

Relentlessly reduce cost through simplification, intelligent automation and scale

Develop an innovation culture and discipline and be willing to disrupt your own business

1

2

3

4

©2020 Visa. All rights reserved. Visa confidential

Summary – Five take home implications

Be clear on who you are and why customers should and will choose you

Obsess about customer experience, re-focus on

relationships and re-think the commercial model

Relentlessly reduce cost through simplification, intelligent automation and scale

Choose your partners…wisely!

Develop an innovation culture and discipline and be willing to disrupt your own business

1

2

3

4

5

©2020 Visa. All rights reserved. Visa confidential

Be clear on who you are and why customers

Obsess about customer experience, re-focus on

customer relationships and re-think loyalty and the

commercial modelRelentlessly reduce cost and re-think your operating model through simplification, intelligent automation and scale

Choose your partners…wisely!

Develop an innovation culture and discipline and be willing to disrupt your own business

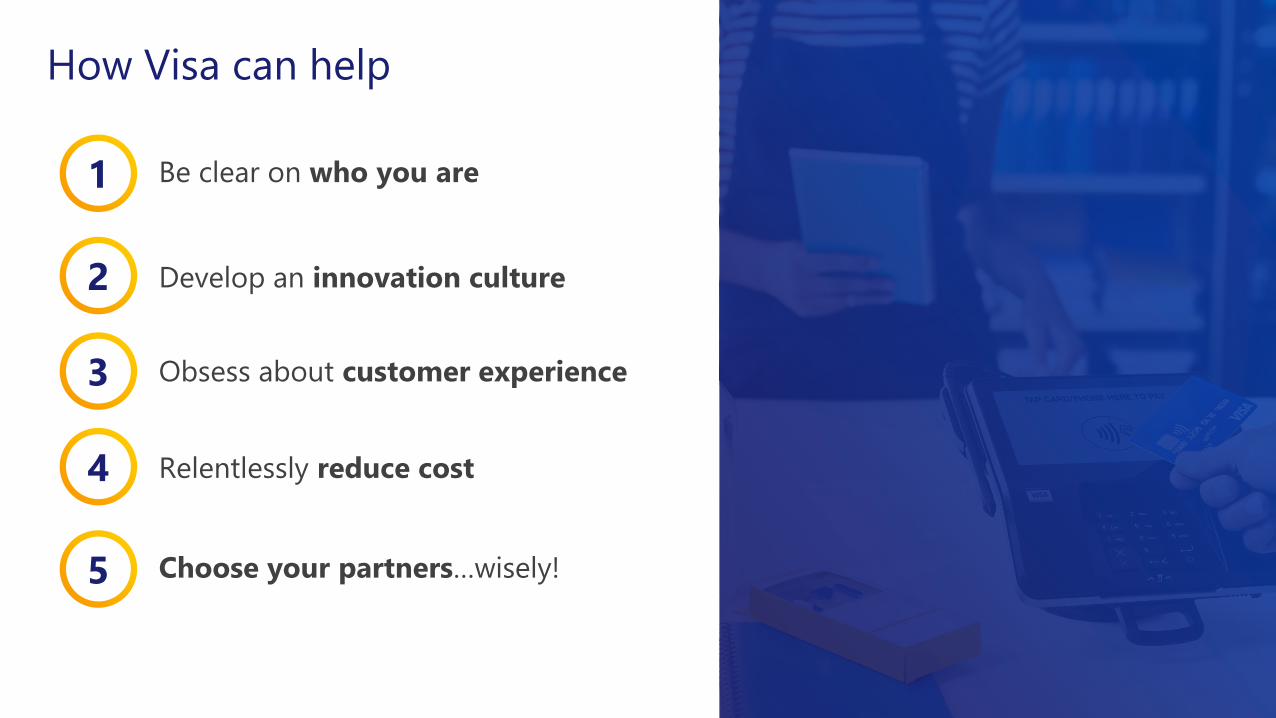

How Visa can help

1

2

3

4

5

©2020 Visa. All rights reserved. Visa confidential

Be clear on who you are and why customers

Obsess about customer experience, re-focus on

customer relationships and re-think loyalty and the

commercial modelRelentlessly reduce cost and re-think your operating model through simplification, intelligent automation and scale

Choose your partners…wisely!

Develop an innovation culture and discipline and be willing to disrupt your own business

How Visa can help

Innovation Centers

Data and insights

Loyalty strategy +

targeted customer offers

E-commerce tools

Financial tools for employees

…and much more

1

2

3

4

5

©2020 Visa. All rights reserved. Visa confidential

©2020 Visa. All rights reserved. Visa confidential

THANK YOU!