The Heterogeneous Effects of Government Spending: It’s All About Taxes. Axelle Ferriere 1 Gaston Navarro 2 1 European University Institute 2 Federal Reserve Board March 2017 These views are those of the authors and not necessarily those of the Board of Governors or the Federal Reserve System.

Transcript

The Heterogeneous Effects of GovernmentSpending: It’s All About Taxes.

Axelle Ferriere1 Gaston Navarro2

1European University Institute

2Federal Reserve Board

March 2017

These views are those of the authors and not necessarily those of the Board of Governors or the Federal Reserve System.

Motivation

Question:

How expansionary is government spending?

I Evidence: output increases, consumption does not decrease.(Barro & Redlick, 2011), (Blanchard & Perotti, 2002), (Ramey, 2016) More

I Puzzle: “Standard” models predict:

o A moderate output expansion, and a consumption decrease.(Hall, 2009)

o A contraction if distortionary taxes are used.(Baxter & King, 1993), (Uhlig, 2010) More

Notes: News variable is normalized by last quarter GDP. Source Ramey & Zubairy (2015). Vertical lines correspondto major military events.

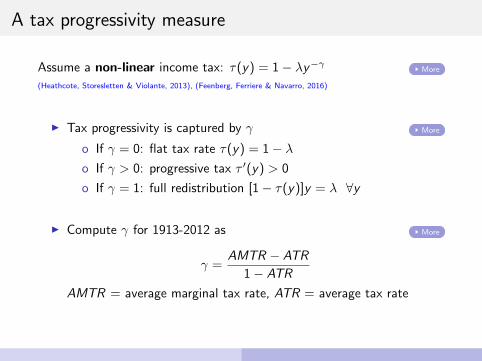

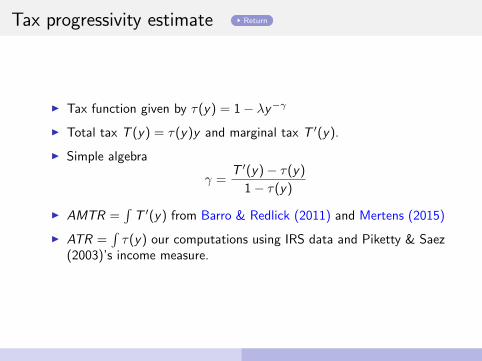

A tax progressivity measure

Assume a non-linear income tax: τ(y) = 1− λy−γ(Heathcote, Storesletten & Violante, 2013), (Feenberg, Ferriere & Navarro, 2016)

More

I Tax progressivity is captured by More

o If = 0: flat tax rate τ(y) = 1− λo If > 0: progressive tax τ ′(y) > 0

o If = 1: full redistribution [1− τ(y)]y = λ ∀y

I Compute γ for 1913-2012 as More

γ =AMTR − ATR

1− ATR

AMTR = average marginal tax rate, ATR = average tax rate

I Robustness using NBER TAXSIM data.

A tax progressivity measure

Assume a non-linear income tax: τ(y) = 1− λy−γ(Heathcote, Storesletten & Violante, 2013), (Feenberg, Ferriere & Navarro, 2016)

More

I Tax progressivity is captured by γ More

o If γ = 0: flat tax rate τ(y) = 1− λo If γ > 0: progressive tax τ ′(y) > 0

o If γ = 1: full redistribution [1− τ(y)]y = λ ∀y

I Compute γ for 1913-2012 as More

γ =AMTR − ATR

1− ATR

AMTR = average marginal tax rate, ATR = average tax rate

I Robustness using NBER TAXSIM data.

A tax progressivity measure

Assume a non-linear income tax: τ(y) = 1− λy−γ(Heathcote, Storesletten & Violante, 2013), (Feenberg, Ferriere & Navarro, 2016)

More

I Tax progressivity is captured by γ More

o If γ = 0: flat tax rate τ(y) = 1− λo If γ > 0: progressive tax τ ′(y) > 0

o If γ = 1: full redistribution [1− τ(y)]y = λ ∀y

I Compute γ for 1913-2012 as More

γ =AMTR − ATR

1− ATR

AMTR = average marginal tax rate, ATR = average tax rate

I Robustness using NBER TAXSIM data.

A tax progressivity measure

Assume a non-linear income tax: τ(y) = 1− λy−γ(Heathcote, Storesletten & Violante, 2013), (Feenberg, Ferriere & Navarro, 2016)

More

I Tax progressivity is captured by γ More

o If γ = 0: flat tax rate τ(y) = 1− λo If γ > 0: progressive tax τ ′(y) > 0

o If γ = 1: full redistribution [1− τ(y)]y = λ ∀y

I Compute γ for 1913-2012 as More

γ =AMTR − ATR

1− ATR

AMTR = average marginal tax rate, ATR = average tax rate

I Robustness using NBER TAXSIM data.

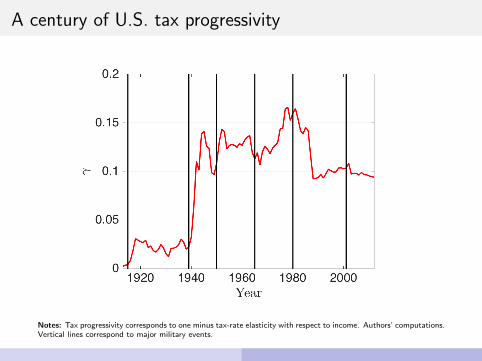

A century of U.S. tax progressivity

Notes: Tax progressivity corresponds to one minus tax-rate elasticity with respect to income. Authors’ computations.

A century of U.S. tax progressivity

Notes: Tax progressivity corresponds to one minus tax-rate elasticity with respect to income. Authors’ computations.Vertical lines correspond to major military events.

State dependent multipliers: local projection

The linear case: Jorda (2005)

o For a vector xt+h =[Yt+h−Yt−1

Yt−1, Gt+h−Gt−1

Yt−1

]xt+h = αh + AhZt−1 + βhg

∗t + trend + εt+h

- Shock g∗t

- Control Zt : lags of GDP, total spending and g∗t

o Cumulative multiplier at horizon h

mh =

h∑j=0

βYj

/

h∑j=0

βGj

State dependent multipliers: local projection

The linear case: Jorda (2005)

o For a vector xt+h =[Yt+h−Yt−1

Yt−1, Gt+h−Gt−1

Yt−1

]xt+h = αh + AhZt−1 + βhg

∗t + trend + εt+h

- Shock g∗t

- Control Zt : lags of GDP, total spending and g∗t

o Cumulative multiplier at horizon h

mh =

h∑j=0

βYj

/

h∑j=0

βGj

State dependent multipliers: local projection

The state-dependent case: Ramey and Zubairy (2016)

o For a vector xt+h =[Yt+h−Yt−1

Yt−1, Gt+h−Gt−1

Yt−1

]xt+h = I (st = P)

{αh,P + Ah,PZt−1 + βh,Pg

∗t

}+ I (st = R)

{αh,R + Ah,RZt−1 + βh,Rg

∗t

}+ trend + εt+h

o Progressive state (st = P) if γ is higher on average for the next 3 years.

More

+ Cumulative multiplier mh,P ,mh,R

o An Instrumental Variable estimation:

More More

+ Ramey and Blanchard Perotti shocks

State dependent multipliers: local projection

The state-dependent case: Ramey and Zubairy (2016)

o For a vector xt+h =[Yt+h−Yt−1

Yt−1, Gt+h−Gt−1

Yt−1

]xt+h = I (st = P)

{αh,P + Ah,PZt−1 + βh,Pg

∗t

}+ I (st = R)

{αh,R + Ah,RZt−1 + βh,Rg

∗t

}+ trend + εt+h

o Progressive state (st = P) if γ is higher on average for the next 3 years.

More+ Cumulative multiplier mh,P ,mh,R

o An Instrumental Variable estimation:

More More+ Ramey and Blanchard Perotti shocks

State dependent multipliers: local projection

The state-dependent case: Ramey and Zubairy (2016)

o For a vector xt+h =[Yt+h−Yt−1

Yt−1, Gt+h−Gt−1

Yt−1

]xt+h = I (st = P)

{αh,P + Ah,PZt−1 + βh,Pg

∗t

}+ I (st = R)

{αh,R + Ah,RZt−1 + βh,Rg

∗t

}+ trend + εt+h

o Progressive state (st = P) if γ is higher on average for the next 3 years.

More+ Cumulative multiplier mh,P ,mh,R

o An Instrumental Variable estimation:

More More+ Ramey and Blanchard Perotti shocks

Output multiplier: the linear case

Notes: Local projection; data 1913-2006; confidence intervals: 68%.

Output multipliers across states

Notes: Local projection; data 1913-2006; confidence intervals: 68%; window: 12 quarters.

Model

A Bewley economy with indivisible labor

Description of the steady-state:

+ A continuum of households:

- Bond economy with borrowing constraint.

- Indivisible labor choice.

- Idiosyncratic labor productivity shock.

More

+ A representative firm

+ Government:

- A constant level of government expenditures G .

- Financed by constant taxes and debt.

Households

The value function of an agent with productivity x and assets a is:

V (a, x) = maxc,a′,h∈{0,h̄}

{log c − D

h1+Φ

1 + Φ+ βEx′ [V (a′, x ′) |x ]

}subject to

c + a′ ≤ wxh + (1 + r)a− τk ra− τ (wxh) , a′ ≥ a

Productivity follows an AR(1) process: log(x it+1) = ρx log(x it ) + σxεit+1.

Tax progressivity will be captured by the shape of τ(·).

Firm and government

Government:

I Constant government expenditures G

I Government’s budget:

G + (1 + r)B = B +

∫{τk ra + τ (wxh)} dµ(a, x)

Firms:

+ Cobb-Douglas production function: Y = LαK 1−α

+ Firm’s static problem:

Π = maxK ,L

{LαK 1−α − wL− (r + δ)K

}Equilibrium definition Calibration Distribution of Wealth and Employment

Firm and government

Government:

I Constant government expenditures G

I Government’s budget:

G + (1 + r)B = B +

∫{τk ra + τ (wxh)} dµ(a, x)

Firms:

+ Cobb-Douglas production function: Y = LαK 1−α

+ Firm’s static problem:

Π = maxK ,L

{LαK 1−α − wL− (r + δ)K

}Equilibrium definition Calibration Distribution of Wealth and Employment

Government spending shocks

Experiment:

+ At t = 0, an unexpected shock:

- G increases by 1% and returns to steady state.

+ Financed with:

- Constant B and τ k

- A path for progressivity {γt}:

γt − γ = η(Gt − G )

- Adjust {λt} to satisfy its budget constraint:

Gt+rtB = τk rtKt+

∫ (1− λt(wtxht(a, x))−γt

)wtxht(a, x)dµt(a, x)

Government spending shocks

Experiment:

+ At t = 0, an unexpected shock:

- G increases by 1% and returns to steady state.

+ Financed with:

- Constant B and τ k

- A path for progressivity {γt}:

γt − γ = η(Gt − G )

- Adjust {λt} to satisfy its budget constraint:

Gt+rtB = τk rtKt+

∫ (1− λt(wtxht(a, x))−γt

)wtxht(a, x)dµt(a, x)

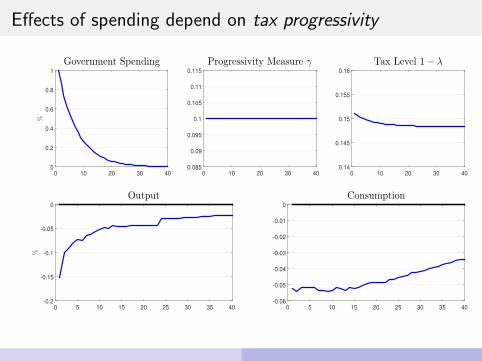

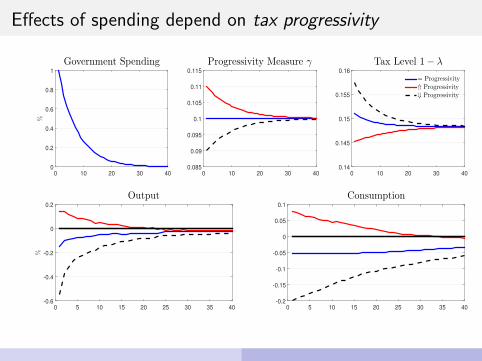

Effects of spending depend on tax progressivity

0 10 20 30 40

%

0

0.2

0.4

0.6

0.8

1

Government Spending

0 10 20 30 40

0.085

0.09

0.095

0.1

0.105

0.11

0.115

Progressivity Measure γ

0 10 20 30 40

0.14

0.145

0.15

0.155

0.16

Tax Level 1− λ

Effects of spending depend on tax progressivity

0 10 20 30 40

%

0

0.2

0.4

0.6

0.8

1

Government Spending

0 10 20 30 40

0.085

0.09

0.095

0.1

0.105

0.11

0.115

Progressivity Measure γ

0 10 20 30 40

0.14

0.145

0.15

0.155

0.16

Tax Level 1− λ

0 5 10 15 20 25 30 35 40

%

-0.2

-0.15

-0.1

-0.05

0

Output

0 5 10 15 20 25 30 35 40

-0.06

-0.05

-0.04

-0.03

-0.02

-0.01

0

Consumption

Effects of spending depend on tax progressivity

0 10 20 30 40

%

0

0.2

0.4

0.6

0.8

1

Government Spending

0 10 20 30 40

0.085

0.09

0.095

0.1

0.105

0.11

0.115

Progressivity Measure γ

0 10 20 30 40

0.14

0.145

0.15

0.155

0.16

Tax Level 1− λ

= Progressivity

⇑ Progressivity

Effects of spending depend on tax progressivity

0 10 20 30 40

%

0

0.2

0.4

0.6

0.8

1

Government Spending

0 10 20 30 40

0.085

0.09

0.095

0.1

0.105

0.11

0.115

Progressivity Measure γ

0 10 20 30 40

0.14

0.145

0.15

0.155

0.16

Tax Level 1− λ

= Progressivity

⇑ Progressivity

0 5 10 15 20 25 30 35 40

%

-0.2

-0.1

0

0.1

0.2

Output

0 5 10 15 20 25 30 35 40

-0.1

-0.05

0

0.05

0.1

Consumption

Effects of spending depend on tax progressivity

0 10 20 30 40

%

0

0.2

0.4

0.6

0.8

1

Government Spending

0 10 20 30 40

0.085

0.09

0.095

0.1

0.105

0.11

0.115

Progressivity Measure γ

0 10 20 30 40

0.14

0.145

0.15

0.155

0.16

Tax Level 1− λ

= Progressivity

⇑ Progressivity

⇓ Progressivity

Effects of spending depend on tax progressivity

0 10 20 30 40

%

0

0.2

0.4

0.6

0.8

1

Government Spending

0 10 20 30 40

0.085

0.09

0.095

0.1

0.105

0.11

0.115

Progressivity Measure γ

0 10 20 30 40

0.14

0.145

0.15

0.155

0.16

Tax Level 1− λ

= Progressivity

⇑ Progressivity

⇓ Progressivity

0 5 10 15 20 25 30 35 40

%

-0.6

-0.4

-0.2

0

0.2

Output

0 5 10 15 20 25 30 35 40

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

Consumption

Heterogeneous changes in tax rates...

0 10 20 30 40

%

15

15.5

16

16.5

Labor Tax - Total Average

0 10 20 30 40

7

7.5

8

8.5

9

1st Quintile

0 10 20 30 40

14.5

15

15.5

16

2nd Quintile

Quarter0 10 20 30 40

%

17

17.5

18

18.5

3rd Quintile

Quarter0 10 20 30 40

19

19.5

20

20.5

4th Quintile

Quarter0 10 20 30 40

22

22.5

23

23.55th Quintile

... result in heterogenous responses More

0 10 20 30 40

0

0.2

0.4

0.6

0.8

1

%

Government Spending

0 10 20 30 40-0.2

0

0.2

0.4

0.6

0.81st Quintile

hours

consumption

0 10 20 30 40-0.2

0

0.2

0.4

0.6

0.82nd Quintile

0 10 20 30 40

Quarters

-0.2

0

0.2

0.4

0.6

0.8

%

3rd Quintile

0 10 20 30 40

Quarters

-0.2

0

0.2

0.4

0.6

0.84th Quintile

0 10 20 30 40

Quarters

-0.2

0

0.2

0.4

0.6

0.85th Quintile

Intratemporal and intertemporal tax allocation More

How important is debt financing?

Exercise:

+ Same path for {Gt} and {γt} as before.

+ A fraction financed with debt, implies a different path for {λt}.

+ Uhlig (2010): Bt+1 − Bss = (1− ϕ)(ωt − ωss),

WVWXXXXWWwhere ωt = Gt + rtBt − τ k rtAt .

I ϕ = 1: no additional debtI ϕ = 0.05: ≈ 95% of additional spending financed with debt

Intratemporal and intertemporal tax allocation

Micro evidence

State dependent multipliers: local projection

State-dependent local projection method:

o For a vector xt+h =[Yt+h−Yt−1

Yt−1, Gt+h−Gt−1

Yt−1

]xt+h = I (st = P)

{αh,P + Ah,PZt−1 + βh,Pg

∗t

}+ I (st = R)

{αh,R + Ah,RZt−1 + βh,Rg

∗t

}+ trend + εt+h

o Cross-sectional data: TAXSIM

- Pre-tax income of all taxpayers

- 1962-2008; Interpolated (Chow-Lin)

Heterogenous responses across households

Notes: Local projection; data 1962-2006; confidence intervals: 68%; window: 12 quarters.

Solving the puzzle?(preliminary)

Quantitative investigation of the mechanism

+ Data: Typical path for {Gt} and {γt} after a spending shock

- News shock (Ramey), 1960-2006

Quantitative investigation: enough to change signs

Conclusion

+ Tax progressivity is crucial to spending multipliers.

I Heterogeneous responses across households

I Generate changes in signs of multipliers

+ Policy implications: use taxes, not spending More

Conclusion

+ Tax progressivity is crucial to spending multipliers.

I Heterogeneous responses across households

I Generate changes in signs of multipliers

+ Policy implications: use taxes, not spending More

Appendix

Evidence: Output and Consumption Multipliers Return

Output ConsumptionBlanchard and Perotti 0.90 0.5

(0.30) (0.21)

Gali, Lopez-Salido and Valles 0.41 0.1(0.16) (0.10)

Barro and Redlick 0.45 0.005(0.07) (0.09)

Mountford and Uhlig 0.65 0.001(0.39) (0.0003)

Ramey 0.30 0.02(0.10) (0.001)

Note: output/consumption multiplier refers to the increase in output/consumption after a unit increase ingovernment spending.

Why a Puzzle? Return Return

I Assume U(C ,H) = C 1−σ

1−σ − H1+ϕ

1+ϕ and competitive labor markets.

I Then (in logs)

log(1− τt↑) +

mpht

↓

= σct

⇓⇓

+ ϕht

↑

+ Indivisible labor of agents heterogeneous in productivity

+ Distribution of taxes

log(1− ↑↓τ it ) + mpht↓ ≶ σc it + ϕhit↑

+ Progressivity shapes the effects of government spending.

Why a Puzzle? Return Return

I Assume U(C ,H) = C 1−σ

1−σ − H1+ϕ

1+ϕ and competitive labor markets.

I Then (in logs)

log(1− τt↑) +

mpht ↓ = σct⇓

⇓

+ ϕht ↑

+ Indivisible labor of agents heterogeneous in productivity

+ Distribution of taxes

log(1− ↑↓τ it ) + mpht↓ ≶ σc it + ϕhit↑

+ Progressivity shapes the effects of government spending.

Why a Puzzle? Return Return

I Assume U(C ,H) = C 1−σ

1−σ − H1+ϕ

1+ϕ and competitive labor markets.

I Then (in logs)

log(1− τt↑) + mpht ↓ = σct⇓⇓+ ϕht ↑

+ Indivisible labor of agents heterogeneous in productivity

+ Distribution of taxes

log(1− ↑↓τ it ) + mpht↓ ≶ σc it + ϕhit↑

+ Progressivity shapes the effects of government spending.

Why a Puzzle? Return Return

I Assume U(C ,H) = C 1−σ

1−σ − H1+ϕ

1+ϕ and competitive labor markets.

I Then (in logs)

log(1− τt↑) + mpht ↓ = σct⇓⇓+ ϕht ↑

+ Indivisible labor of agents heterogeneous in productivity

+ Distribution of taxes

log(1− ↑↓τ it ) +

mpht↓ ≶ σc it + ϕhit↑

+ Progressivity shapes the effects of government spending.

Why a Puzzle? Return Return

I Assume U(C ,H) = C 1−σ

1−σ − H1+ϕ

1+ϕ and competitive labor markets.

I Then (in logs)

log(1− τt↑) + mpht ↓ = σct⇓⇓+ ϕht ↑

+ Indivisible labor of agents heterogeneous in productivity

+ Distribution of taxes

log(1− ↑↓τ it ) + mpht↓ ≶ σc it + ϕhit↑

+ Progressivity shapes the effects of government spending.

Why a Puzzle? Return Return

I Assume U(C ,H) = C 1−σ

1−σ − H1+ϕ

1+ϕ and competitive labor markets.

I Then (in logs)

log(1− τt↑) + mpht ↓ = σct⇓⇓+ ϕht ↑

+ Indivisible labor of agents heterogeneous in productivity

+ Distribution of taxes

log(1− ↑↓τ it ) + mpht↓ ≶ σc it + ϕhit↑

+ Progressivity shapes the effects of government spending.

A Progressive Taxation Scheme Return

A non-linear labor income tax τ(y) ≡ 1− λy−γ

0 5 10 15 20 25 30−0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

Income

Tax

rat

e

1−λ = 0.12, γ = 0.1

A Progressive Taxation Scheme Return

A non-linear labor income tax τ(y) ≡ 1− λy−γ

0 5 10 15 20 25 30−0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

Income

Tax

rat

e

1−λ = 0.12, γ = 0.11−λ = 0.12, γ = 0.2

A Progressive Taxation Scheme Return

A non-linear labor income tax τ(y) ≡ 1− λy−γ

0 5 10 15 20 25 30−0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

Income

Tax

rat

e

1−λ = 0.12, γ = 0.11−λ = 0.3, γ = 0.1

Heathcote Storesletten Violante (2016) Return

Measurement of τUS

• PSID 2000-06, age of head of hh 25-60, N = 12, 943

• Pre gov. income: income minus deductions (medical expenses,state taxes, mortgage interest and charitable contributions)

• Post-gov income: ... minus taxes (TAXSIM) plus transfers

Share of Wealth- PSID Data −0.00 0.02 0.07 0.15 0.77- Model −0.01 0.04 0.12 0.25 0.61

Participation Rate- PSID Data 0.65 0.75 0.69 0.60 0.57- Model 0.83 0.63 0.57 0.52 0.45

The PSID statistics reflect the family wealth and earnings in the 1984 survey. Thestatistics of ”primary households’ are those for household heads whose education was12 years and whose age is between 35 and 55.

Hours and consumption: households distribution Return

Notes: Income is defined as y(a, x) = wxh(a, x) + (1 + r)a − τ(wxh, ar).

Hours and consumption: households distribution Return

Notes: Income is defined as y(a, x) = wxh(a, x) + (1 + r)a − τ(wxh, ar).

Timing of the change in progressivity Return

How important is the timing of the increase in tax progressivity?

Exercise:

+ Same path for {Gt}.+ {γt} does not react on impact, increases slowly until quarter 5.

+ Debt: Φ = .05

Timing of the change in progressivity Return

0 10 20 30 400

0.2

0.4

0.6

0.8

1

%

Government Spending

0 10 20 30 400.1

0.102

0.104

0.106

0.108

0.11Progressivity Measure γ

0 10 20 30 400.142

0.143

0.144

0.145

0.146

0.147

0.148

0.149Tax Level 1− λ

0 10 20 30 40-0.05

0

0.05

0.1

0.15

0.2

0.25

%

Output

0 10 20 30 40-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

Consumption

0 10 20 30 40-0.05

0

0.05

0.1

0.15

0.2

0.25Government Debt

Use taxes, not spending Return

What is the effect of a temporary increase in progressivity?