25

STEVE TSHWETE LOCAL MUNICIPALITY SALGA- MUNICIPAL MANAGERS FORUM George Local Municipality 31 AUGUST – 01 SEPTEMBER 2017 THE HOME OF STAINLESS STEEL 1

STEVE TSHWETE LOCAL MUNICIPALITY

SALGA- MUNICIPAL MANAGERS FORUM George Local Municipality

31 AUGUST – 01 SEPTEMBER 2017

THE HOME OF STAINLESS STEEL

1

INSIGHT ON THE 2015/16 AUDIT OUTCOMES

STEVE TSHWETE LOCAL

MUNICIPALITY

2

TABLE OF CONTENT 1. Our Commitment 2. Major Challenges 3. 10 Critical Issues 4. Elements of Clean Audit 5. Overview on causes of financial statement qualifications 6. Core Compliance 7. Financial Management 8. Key control drivers for Clean Administration 9. Preparation of Financial Statements 10. Relationship with Auditor-General 11. Proposed Interventions FORUMS / TASK TEAMS 12. Clean Audits V/S Service Delivery

3

To always treat everyone with

dignity and respect.

To perform duties with integrity,

honesty and diligence.

To diligently apply the principles of Batho Pele in all

dealings.

OUR STANDARD OF GOOD FINANCIAL GOVERNANCE

• Discipline • Accountability Fairness

• Transparency • Responsibility Social Responsibility

There are many faces in the municipality contributing to the clean audit achievement. 4

MAJOR CHALLENGES Ø Internal controls deficiencies Ø Poor reconciliations and misstatement of financial statements Ø Poor credit control – debt collection (affect cash flow) Ø Asset register not compliance to GRAP requirements Ø Increase prohibited expenditure (Unauthorised, irregular, fruitless

and wasteful expenditure) Ø Reconciliation of a Valuation Rolls to a Billing systems Ø Unfunded budget (inflated revenue projections which do not

materialise) Ø Poor reconciliation and cash flow management Ø Ineffective leadership and oversight responsibility (governance

structures) Ø Lack of SCM policy and non compliance Ø Poor relationship between MM and CFO

5

MAJOR CHALLENGES (cont.…..)

Ø Poor quality of AFS – Information submitted for auditing Ø Slow response by management in SCM non compliance Ø Slow response to Audit enquiries raised within prescribed time Ø Slow filling of Key positions and/or with unsuitable candidates Ø Lack of consequences for poor performance and transgression Ø Reliance on consultants to produce AFS and Asset register Ø Ineffective Risk Management Ø Ineffective Billing System Ø Incredible Indigent policy and register Ø Lack of compliance, delegation, contract management and

records system.

6

10 CRITICAL ISSUES Ø Relationships

§ Political and Administration § MM and CFO

Ø Segregation of duties and Delegation register Ø Records Management Ø Legal Compliance and Litigation register Ø Contract Management Ø Monitoring system (Political and Administrative) Ø Institutional Arrangements - Competent and qualified

personnel Ø Billing system Ø Performance Management System (SMART ) Ø Internal control

7

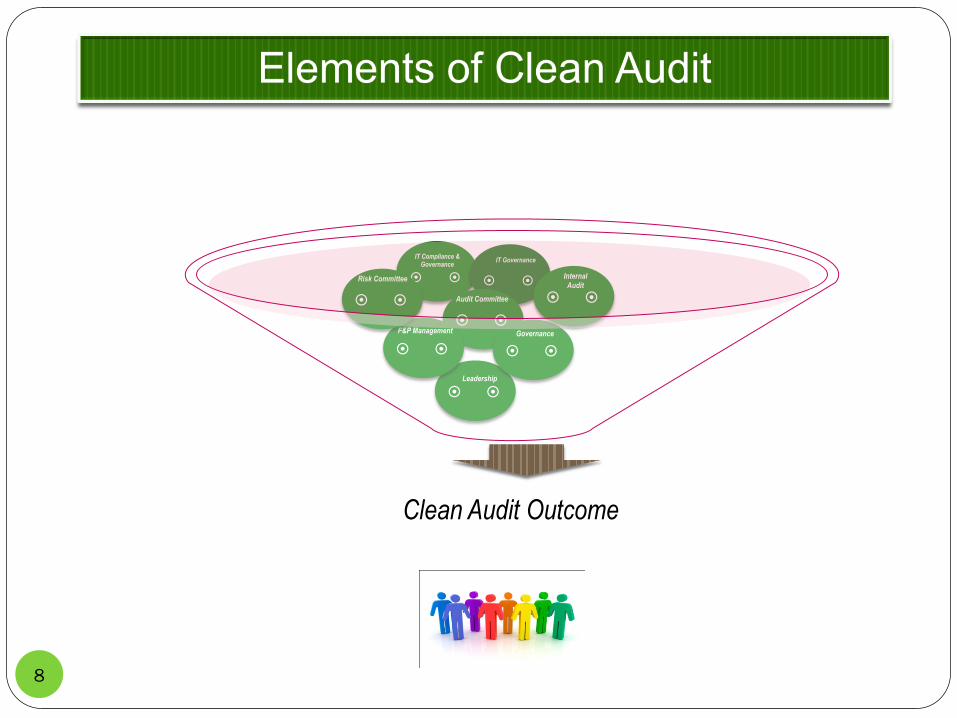

¤ ¤

IT Compliance & Governance

¤ ¤

IT Governance

¤ ¤

Audit Committee

¤ ¤ Leadership

¤ ¤ Governance

¤ ¤ F&P Management

¤ ¤

Risk Committee

¤ ¤

Internal Audit

Clean Audit Outcome

8

OVERVIEW ON CAUSES OF FINANCIAL STATEMENT QUALIFICATIONS

� Property Plant and Equipment (GRAP 17) � Residual values, Useful lives not reviewed � Fixed asset register incomplete and not updated � Reconciliations of registers with GL not performed. � Supporting documentation to support evidence.

� Performance Information and Predetermined Objectives � Performance reports not submitted � Usefulness of reported information measured against relevance

and measurability

� Non-Compliance with Laws and Regulations � Unauthorised, irregular & fruitless and wasteful expenditure � Submitted financial statements required material adjustments � Non functional audit committees & Internal Control

9

OVERVIEW ON CAUSES OF FINANCIAL STATEMENT QUALIFICATIONS

� Critical Supply Chain Management Issues � General non compliance to procurement and contract

management. (Bid committees, Quotations etc) � Awards made to persons in the service of the state. � Competitive bids not invited. � Missing contract documentation

� Governance � Leadership � Performance management � Systems and processes � Lack of proper record keeping

10

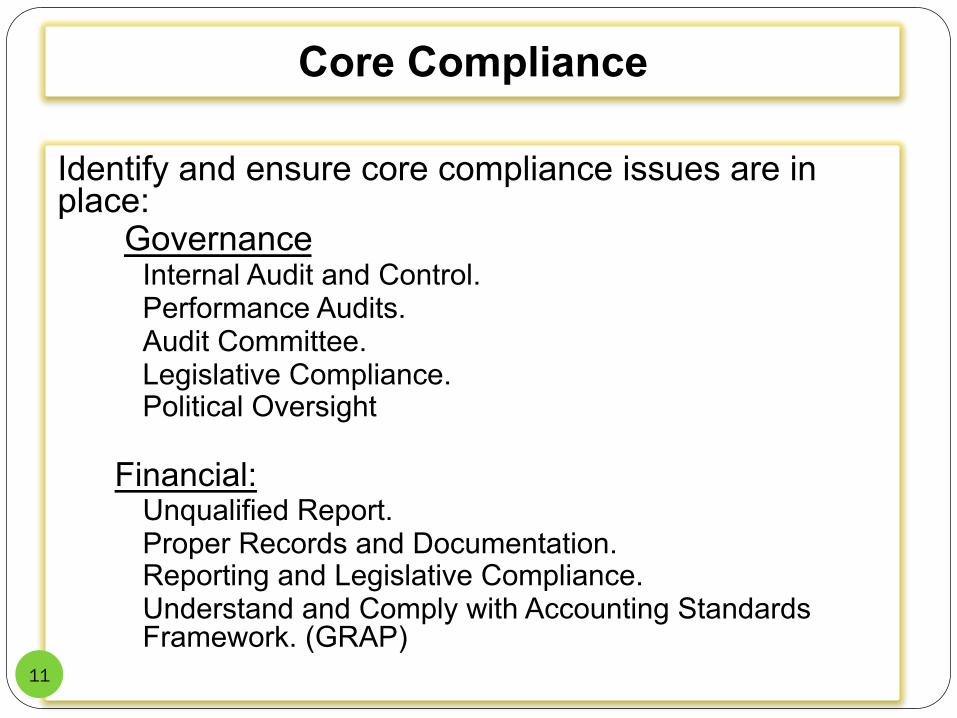

Core Compliance

Identify and ensure core compliance issues are in place:

� Governance � Internal Audit and Control. � Performance Audits. � Audit Committee. � Legislative Compliance. � Political Oversight

� Financial: � Unqualified Report. � Proper Records and Documentation. � Reporting and Legislative Compliance. � Understand and Comply with Accounting Standards

Framework. (GRAP) 11

KEY CONTROL DRIVERS FOR CLEAN ADMINITRATION

12

Leadership Financial and Performance management Governance

Effective leadership culture Proper record keeping Risk management

Oversight responsibility Processing and reconciling controls Internal control

HR management Regular reporting Audit committee Policies and procedures Compliance monitoring

Audit action plans IT system controls IT governance Improved Unchanged Regressed

Improved

Unchanged Regressed

Good

Concerning

Intervention required

Preparation of Financial Statements

� Outsourced versus In-House � Over 60% of municipalities are assisted by

consultants � Consultants were able to correct parts of financial

statements that had been misstated but are unable to ensure that auditees progress towards unqualified reports.

� Disadvantages � Consultants Appointed close to year-end – No real

impact � Deficiencies in record keeping and reconciliations limit

ability to prepare GRAP compliant statements. � Vacancies and capacity of finance department staff.

13

Preparation of Financial Statements

� Prepare Financial statements in-house. � Benefits:

� Build in-house capacity. � Responsibility/Ownership rests with municipality. � Better control over balancing and verification of figures

in general ledger with source documents. � Informed responses to Auditor-General enquiries. � Better understanding of accounting records and

procedures � Defend fairness of enquiries raised. � Accurate and timeously response to AG on queries

raised. 14

Relationship with Auditor-General

� Know the Auditor-General. � Make sure there is a good and positive working

relationship. � Listen to their requirements during Audits. � Respond to informal enquiries quickly and

efficiently. � Provide information as requested and if not

available inform AG accordingly. � Have a open office approach and assist as far as

possible. � Designate an official to be available during audit.

15

PROPOSED INTERVENTIONS FORUMS / TASK TEAMS

18

FORUM / TASK TEAM 1:

QUALITY OF SUBMITTED FINANCIAL STATEMENTS

Development and implementation of Accounting Policies AFS & IFS Committees Development and Implementation of AFS & IFS preparation plans Conduct regular TB, GL and AFS / IFS Reconciliations AFS & IFS Reconciliation Schedules Develop and Implement AFS & IFS checklist Conduct AFS & IFS Review sessions

FORUM /TASK TEAM 2 :

QUALITY OF SUBMITTED PERFORMANCE INFORMATION

Establishment of Planning Unit. Credibility of Municipal Plans Monitoring and Evaluation of implementation plans Performance review sessions Regular reporting as per required legislations

FORUM / TASK TEAM 3:

SUPPLY CHAIN MANAGEMENT

Establishment of SCM Unit SCM Committees Financial Delegations SCM Delegations Appointment of Responsibility Managers Policies and Procedures Compliance Checklists Regular Reporting

FORUM / TASK TEAM 4

INTERNAL CONTROLS

Develop a list of standard policies and procedures Take stock of existing policies and procedures Develop outstanding policies and procedures Assessment of Control Environment Assessment of application Controls

IT Governance and Controls Monitor and enforce implementation of developed policies and procudures

FORUM / TASK TEAM 5

HUMAN RESOURCES MANAGEMENT

Municipal Organogram HR Delegations General HR Matters Competencies

Instability

Vacancies

FORUM / TAK TEAM 6

INFORMATION TECHNOLOGY

ITC Governance Structure establishment Functional ICT Unit within the Municipality

Development ICT Strategy Disaster Recovery Plan User Access control and change management ICT Facilities and environmental control

FORUM / TASK TEAM 7 COMPLIAINCE WITH LAWS AND REGULATIONS

Development and implementation of compliance policy Development and implementation of compliance registers of all applicable laws and regulations Develop and implement monthly compliance checklist Develop operational compliance checklist Establishment of Compliance Units

Establishment of Internal Audit : Compliance Units Monthly compliance reporting arrangements

FORUM / TASK TEAM 8 REVENUE AND CREDIT CONTROL MANAGEMENT

Revenue and Credit Control Management Unit effectiveness

Revenue and Credit Control Policies Revenue Enhancement Strategy Top 100 Users per Revenue Source / Category Government Accounts Reconciliations

Maintenance of accurate Indigent Registers Monthly reporting and monitoring

PROPOSED INTERVENTIONS FORUMS / TASK TEAMS

17

TASK TEAM 9

PROPERTY PLANT AND EQUIPMENTS

Review of Municipal Asset Register (Tangible and Intangible) Physical Verification of Municipal Assets with an objective of ensuring existence, completeness and accuracy.

Compile and maintain GRAP Compliance Municipal Asset Register

Reconcile Asset Register to Municipal Ledger Accounts, Trial Balances and Interim / Annual Financial Statements.

TASK TEAM 10

UNAUTHORISED, IRREGULAR AND FRUITLESS AND WASTEFUL EXPENDITURE

Review Registers for Unauthorised, Irregular and Fruitless and Wasteful Expenditure(UIFW).

Reconcile UIFW Registers to Legers, Trial Balances, Interim/Annual Financial Statements

Monitor the status of UIFW within Municipalities (Investigation processes/ status)

Conduct all outstanding investigations on UIFW within the affected Municipalities

Monitor implementation of Investigations outcome / recommendations where applicable.

Enforce consequence management within the identified or affected Municipalities

TASKS WITH THE POTENTIAL OF BEING OUTSOURCED

INSITUTIONALIZATION OF FORUMS / TASK TEAMS

18

Processing and Reconciliations

Human Resource

Audit Action Plans Record Keeping

SUB-TASK TEAMS RESPONSIBLE FOR PERFORMANCE AND SERVICE DELIVERY

SUB-TASK TEAMS RESPONSIBLE FOR QUALITY OF ANNUAL FINANCIAL STATEMENTS

TASK TEAM / FORUM NO 1 : QUALITY OF

ANNUAL FINANCIAL

STATEMENTS

Record Keeping

TASK TEAM / FORUM NO 2 :

PERFORMANCE AND SERVICE

DELIVERY

Predetermined Objectives and Sector

Specific

Compliance

Internal Controls

Performance Audit

Governance

INSITUTIONALIZATION OF FORUMS / TASK TEAMS

19

Internal Controls

Human Resource Audit Action Plans Record Keeping

SUB-TASK TEAMS RESPONSIBLE FOR INTERNAL CONTROLS

SUB-TASK TEAMS RESPONSIBLE FOR SUPPLY CHAIN MANAGEMENT

TASK TEAM / FORUM NO 3 : SUPPLY CHAIN MANAGEMEN

T

Record Keeping

TASK TEAM / FORUM NO 4 :

INTERNAL CONTROLS

Processing and Reconciliation

Property Plant and Equipment

Information Technology

Compliance

Employee Costs

INSITUTIONALIZATION OF FORUMS / TASK TEAMS

20

Revenue and Receivables

Operating Expenditure

Payables, Commitments,

Provisions and VAT Cash and Bank

SUB-TASK TEAMS RESPONSIBLE FOR HUMAN RESOURCE MANAGEMENT

TASK TEAM / FORUM NO 4 :

INTERNAL CONTROLS

Record Keeping Compliance Provisions Internal Controls

Inventory

Audit Action Plans

SUB-TASK TEAMS RESPONSIBLE FOR INTERNAL CONTROLS

TASK TEAM / FORUM NO 5 :

HUMAN RESOURCE

MANAGEMENT

INSITUTIONALIZATION OF FORUMS / TASK TEAMS

21

Governance Human

Resources Audit Action Plans Internal Controls

SUB-TASK TEAMS RESPONSIBLE FOR PROPERTY PLAN AND EQUIPMENT

TASK TEAM / FORUM NO 6 :

INFORMATION TECHNOLOGY

Record Keeping Compliance Quality of

Annual Financial Statements

Processing and Reconciliations

ICT & Performance

Audits

Audit Action Plans

SUB-TASK TEAMS RESPONSIBLE FOR INFORMATION TECHNOLOGY

TASK TEAM / FORUM NO 7 :

PROPERTY PLANT AND

EQUIPMENTS

INSITUTIONALIZATION OF FORUMS / TASK TEAMS

22

Supply Chain Management

Compliance Audit Action

Plans Internal Controls

TASK TEAM / FORUM NO 8 :

UNAUTHORISED, IRREGULAR AND FRUITLESS AND

WASTEFUL EXPENDITURE

Quality of Annual

Financial Statements

SUB-TASK TEAMS RESPONSIBLE FOR UNAUTHORISED, IRREGULAR AND FRUITLESS AND WASTEFUL EXPENDITURE

SUB-TASK TEAMS RESPONSIBLE FOR UNAUTHORISED, IRREGULAR AND FRUITLESS AND WASTEFUL EXPENDITURE

CLEAN AUDITS V/S SERVICE DELIVERY

� IDP and Budget process � Ward Committees and Community meetings bi-monthly � Monthly Political and Administrative Monitoring

meetings � Involvement of stakeholders in IDP and budget process

� Observation of Batho Pele Principles (Customer Service) • Service standards and Charters • Communication (sms system) • Focus on previously disadvantage areas

� Capital Projects with internal funding � Focus on provision of critical infrastructure � Maintenance of existing infrastructure � Institutional Memeory 23

STLM APPROACH (Cont…)

� KISS CONCEPT � KEEP � IMPROVE � STOP � START

24

THANK YOU

NGIYABONGA DANKIE

NGIYATHOKOZA

25