16

@ 2016 Deloite Financial Advisory 1 The Hotel Property Handbook Investment & Financing Keys Andalusia Snapshot Financial Advisory I Real Estate - Hospitality December 2017

@ 2016 Deloite Financial Advisory 1

The Hotel Property HandbookInvestment & Financing Keys

Andalusia Snapshot

Financial Advisory I Real Estate - Hospitality

December 2017

@ 2016 Deloite Financial Advisory 2

The Hotel Property HandbookAndalusia Snapshot

Javier García-Mateo, MRICS

PartnerFinancial Advisory ‖ Real Estate

[email protected]: +34 659 90 02 15

Leopoldo Parias

PartnerFinancial Advisory [email protected]: +34 629894186

Jose María Espejo

Senior ManagerFinancial Advisory ‖ Real Estate

[email protected]: +34 918 232 692

Jordi Schoenenberger

PartnerHospitality Industry [email protected]: +34 932 543 932

Fernando Baldellou

PartnerHead of Financial Advisory – Hospitality [email protected]: +34 914 432 514

@ 2016 Deloite Financial Advisory 3

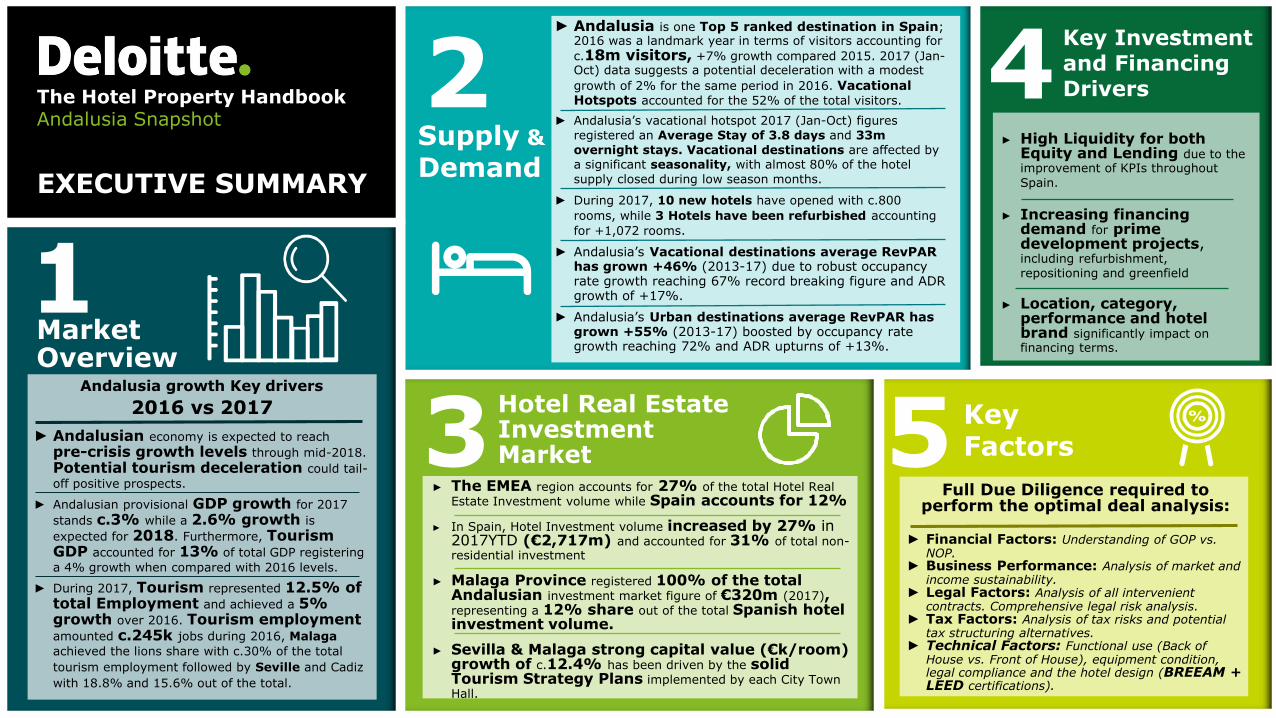

► Andalusia is one Top 5 ranked destination in Spain; 2016 was a landmark year in terms of visitors accounting for

c.18m visitors, +7% growth compared 2015. 2017 (Jan-Oct) data suggests a potential deceleration with a modest

growth of 2% for the same period in 2016. VacationalHotspots accounted for the 52% of the total visitors.

► Andalusia’s vacational hotspot 2017 (Jan-Oct) figures

registered an Average Stay of 3.8 days and 33m

overnight stays. Vacational destinations are affected by a significant seasonality, with almost 80% of the hotel

supply closed during low season months.

► During 2017, 10 new hotels have opened with c.800

rooms, while 3 Hotels have been refurbished accounting

for +1,072 rooms.

► Andalusia’s Vacational destinations average RevPAR has grown +46% (2013-17) due to robust occupancy rate growth reaching 67% record breaking figure and ADR growth of +17%.

► Andalusia’s Urban destinations average RevPAR has grown +55% (2013-17) boosted by occupancy rate growth reaching 72% and ADR upturns of +13%.

5 Key Factors

Full Due Diligence required to perform the optimal deal analysis:

► Financial Factors: Understanding of GOP vs. NOP.

► Business Performance: Analysis of market and income sustainability.

► Legal Factors: Analysis of all intervenient contracts. Comprehensive legal risk analysis.

► Tax Factors: Analysis of tax risks and potential tax structuring alternatives.

► Technical Factors: Functional use (Back of House vs. Front of House), equipment condition, legal compliance and the hotel design (BREEAM + LEED certifications).

Key Investment and Financing Drivers

► High Liquidity for both Equity and Lending due to the improvement of KPIs throughout

Spain.

► Increasing financing demand for prime development projects, including refurbishment, repositioning and greenfield

► Location, category, performance and hotel brand significantly impact on financing terms.

Market Overview

1

► Andalusian economy is expected to reach

pre-crisis growth levels through mid-2018.

Potential tourism deceleration could tail-

off positive prospects.

► Andalusian provisional GDP growth for 2017

stands c.3% while a 2.6% growth is expected for 2018. Furthermore, Tourism GDP accounted for 13% of total GDP registering

a 4% growth when compared with 2016 levels.

► During 2017, Tourism represented 12.5% of total Employment and achieved a 5% growth over 2016. Tourism employment amounted c.245k jobs during 2016, Malaga

achieved the lions share with c.30% of the total

tourism employment followed by Seville and Cadiz

with 18.8% and 15.6% out of the total.

2016 vs 2017

Andalusia growth Key drivers

2Supply &

Demand

4

3Hotel Real Estate Investment Market

The Hotel Property HandbookAndalusia Snapshot

EXECUTIVE SUMMARY

► The EMEA region accounts for 27% of the total Hotel Real Estate Investment volume while Spain accounts for 12%

► In Spain, Hotel Investment volume increased by 27% in 2017YTD (€2,717m) and accounted for 31% of total non-residential investment

► Malaga Province registered 100% of the total Andalusian investment market figure of €320m (2017),representing a 12% share out of the total Spanish hotel investment volume.

► Sevilla & Malaga strong capital value (€k/room) growth of c.12.4% has been driven by the solid Tourism Strategy Plans implemented by each City Town Hall.

@ 2016 Deloite Financial Advisory 4

(8.1%) (13.9%)

(6.2%)

(4.0%)

0.5% 1.7% 6.6% 13.9% (3.7%)

(1.1%)7.9% 11.0%

10.4% 12.4%

9.2% 3.2%

Cap

ital

Val

ues

Gro

wth

(%

)2

01

5-2

01

6

Capital Valu

e p

er

room

(2015-1

6)

€800k

€600k

€400k

€200k

€100k

The Hotel Property HandbookAndalusia Snapshot

EXECUTIVE SUMMARY

Drivers increase in cross-border

investments:

2

3

1

4

Yielding Assets are more attractive than Investment Grade Bonds

Strength of the dollar (For American investors) and weakness of the Euro since 2014

Political and financial uncertainly in certain countries is favouring Spain

Cap

ital

Val

ue

per

ro

om

Tr

end

20

06

-20

16

Max. Min (2006-16) 2015 2016

Source: HSV London

The Hotel Market: Unitary Values Analysis (€/room)

To take away: Malaga and Seville cities

Capital Values (€/room) growth has been gaining momentum through 2015-2016.

2017 growth is expected break record breaking

figures due to the strong effort on asset repositioning and solid Tourism Strategy Plans implemented by each City Town Hall.

Returns expected in Spain through hotel investment are above the European average

10 Year Bond

2016-2017(1 March 2017)

Yield 2016 – Dif. 10 years bond

2,12%▲ 50 bps

1,15%▼65 bps

0,92%▼4 bps

0,23%▼ 34 bps

2,12%▲ 50 bps

2,12%▲ 50 bps

1,67%▼17 bps

1,67%▼17 bps

0,34%▼ 43 bps

-0,22%▼ 22 bps

-0,22%▼ 22 bps

363 bps310 bps408 bps 477 bps388 bps 388 bps433 bps516 bps 538 bps522 bps547 bps 458 bps 458 bps 458 bps458 bps

1,67%▼17 bps

1,67%▼17 bps

1,67%▼17 bps

-

€200k

€400k

€600k

€800k

Pari

s

Lo

nd

on

Zü

ric

h

Ge

nev

a

Ro

me

Flo

ren

ce

Am

ste

rda

m

Ba

rcelo

na

Mila

n

Mu

nic

h

Mad

rid

Eu

rop

e

Sev

illa

Mála

ga

Gra

na

da

Có

rdo

ba

1,67%▼17 bps

4* hotel Category

@ 2016 Deloite Financial Advisory 5

644 687 365 867

2,297

1,894 3,769 2,420

750 576 519 607 932

2,702 2,145

2,717

1,467 591

571

751

2,242

1,263

660

571

1,460

1,056

544

807

2,520

5,313 4,895

1,993

150

279

88

120

596

674 930

1,143

4,470

3,189

2,087

3,151

8,587

11,845 12,398

8,845

-

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017YTD

Top 10 Spanish single asset transactions:

A total pipeline investment volume of €800m is expected to be traded in Spain

Spanish Investment Market

Source: Deloitte

Source: Deloitte

EXECUTIVE SUMMARY

Total Hotel investment volume in Spain as at

2017YTD: €2,717m

Short Term Medium Term Long Term TOTAL

75%100%

17%

8%

In 2017YTD the Hotel investment volume has exceed by 27% the investment volume of 2016. Hotel typology represents 31% of the total investment volume, while Andalusia represents the 12% share.

# Asset UnitsPrice

(€m)Typology

1 Ritz-Carlton Abama 461 183 Vacational

2 Hotel Villaitana 390 101 Vacational

3 Jardin Tropical 390 101 Vacational

4 Sol Príncipe 799 89 Vacational

5 Hotel Silken 240 80 Urban

6 Hilton Diagonal Mar Barcelona (55%)238 80 Urban

7 Ritz-Carlton Abama 50% 461 75 Vacational

8 Sol Palmanova 653 73 Vacational

9 Silken Puerta de América 315 48 Vacational

10 AC Malaga Palacio 214 48 Urban

The Hotel Property HandbookAndalusia Snapshot

Source: Deloitte Data Base and third party sources

For more information see CHAPTER 3 (Investment Market)

31%Hotel

+27%

Hotels

Logistic

Retail High Street

Retail Shopping Centre

Offices

Andalusia

€320m Malaga region

accounted for the 100% of hotel

investment market

@ 2016 Deloite Financial Advisory 6

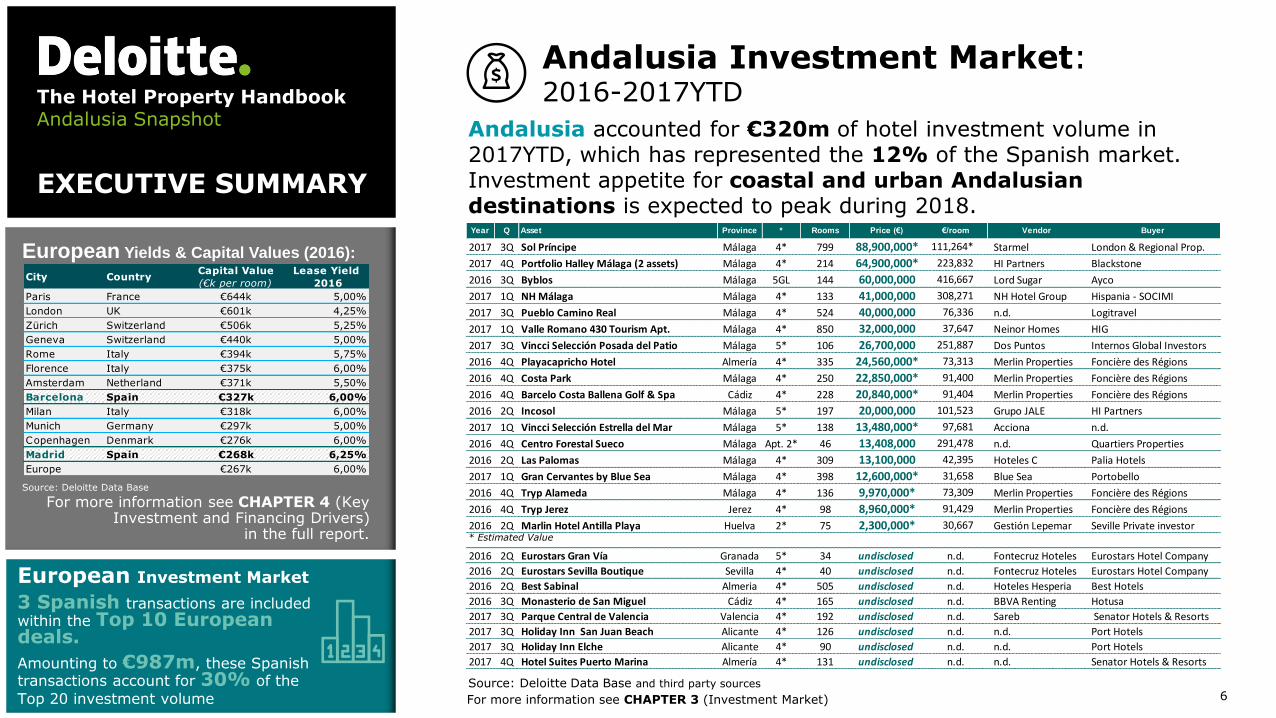

European Yields & Capital Values (2016):

For more information see CHAPTER 4 (Key Investment and Financing Drivers)

in the full report.

Source: Deloitte Data Base

EXECUTIVE SUMMARY

European Investment Market

3 Spanish transactions are includedwithin the Top 10 European deals.

Amounting to €987m, these Spanish transactions account for 30% of the

Top 20 investment volume

Andalusia Investment Market: 2016-2017YTD

Andalusia accounted for €320m of hotel investment volume in 2017YTD, which has represented the 12% of the Spanish market. Investment appetite for coastal and urban Andalusian destinations is expected to peak during 2018.

Source: Deloitte Data Base and third party sources

For more information see CHAPTER 3 (Investment Market)

City CountryCapital Value

(€k per room)

Lease Yield

2016

Paris France €644k 5,00%

London UK €601k 4,25%

Zürich Switzerland €506k 5,25%

Geneva Switzerland €440k 5,00%

Rome Italy €394k 5,75%

Florence Italy €375k 6,00%

Amsterdam Netherland €371k 5,50%

Barcelona Spain €327k 6,00%

Milan Italy €318k 6,00%

Munich Germany €297k 5,00%

Copenhagen Denmark €276k 6,00%

Madrid Spain €268k 6,25%

Europe €267k 6,00%

The Hotel Property HandbookAndalusia Snapshot

Year Q Asset Province * Rooms Price (€) €/room Vendor Buyer

2017 3Q Sol Príncipe Málaga 4* 799 88,900,000* 111,264* Starmel London & Regional Prop.

2017 4Q Portfolio Halley Málaga (2 assets) Málaga 4* 214 64,900,000* 223,832 HI Partners Blackstone

2016 3Q Byblos Málaga 5GL 144 60,000,000 416,667 Lord Sugar Ayco

2017 1Q NH Málaga Málaga 4* 133 41,000,000 308,271 NH Hotel Group Hispania - SOCIMI

2017 3Q Pueblo Camino Real Málaga 4* 524 40,000,000 76,336 n.d. Logitravel

2017 1Q Valle Romano 430 Tourism Apt. Málaga 4* 850 32,000,000 37,647 Neinor Homes HIG

2017 3Q Vincci Selección Posada del Patio Málaga 5* 106 26,700,000 251,887 Dos Puntos Internos Global Investors

2016 4Q Playacapricho Hotel Almería 4* 335 24,560,000* 73,313 Merlin Properties Foncière des Régions

2016 4Q Costa Park Málaga 4* 250 22,850,000* 91,400 Merlin Properties Foncière des Régions

2016 4Q Barcelo Costa Ballena Golf & Spa Cádiz 4* 228 20,840,000* 91,404 Merlin Properties Foncière des Régions

2016 2Q Incosol Málaga 5* 197 20,000,000 101,523 Grupo JALE HI Partners

2017 1Q Vincci Selección Estrella del Mar Málaga 5* 138 13,480,000* 97,681 Acciona n.d.

2016 4Q Centro Forestal Sueco Málaga Apt. 2* 46 13,408,000 291,478 n.d. Quartiers Properties

2016 2Q Las Palomas Málaga 4* 309 13,100,000 42,395 Hoteles C Palia Hotels

2017 1Q Gran Cervantes by Blue Sea Málaga 4* 398 12,600,000* 31,658 Blue Sea Portobello

2016 4Q Tryp Alameda Málaga 4* 136 9,970,000* 73,309 Merlin Properties Foncière des Régions

2016 4Q Tryp Jerez Jerez 4* 98 8,960,000* 91,429 Merlin Properties Foncière des Régions

2016 2Q Marlin Hotel Antilla Playa Huelva 2* 75 2,300,000* 30,667 Gestión Lepemar Seville Private investor

2016 2Q Eurostars Gran Vía Granada 5* 34 undisclosed n.d. Fontecruz Hoteles Eurostars Hotel Company

2016 2Q Eurostars Sevilla Boutique Sevilla 4* 40 undisclosed n.d. Fontecruz Hoteles Eurostars Hotel Company

2016 2Q Best Sabinal Almeria 4* 505 undisclosed n.d. Hoteles Hesperia Best Hotels

2016 3Q Monasterio de San Miguel Cádiz 4* 165 undisclosed n.d. BBVA Renting Hotusa

2017 3Q Parque Central de Valencia Valencia 4* 192 undisclosed n.d. Sareb Senator Hotels & Resorts

2017 3Q Holiday Inn San Juan Beach Alicante 4* 126 undisclosed n.d. n.d. Port Hotels

2017 3Q Holiday Inn Elche Alicante 4* 90 undisclosed n.d. n.d. Port Hotels

2017 4Q Hotel Suites Puerto Marina Almería 4* 131 undisclosed n.d. n.d. Senator Hotels & Resorts

* Estimated Value

@ 2016 Deloite Financial Advisory 7

EXECUTIVE SUMMARY

The Hotel Property HandbookAndalusia Snapshot

GROWTH

EMPLOYMENT

Tourism-related employments

accounts for 12% of Spain’s

employments

In contrast to previous estimates, 12% more UK tourists came to Spain during 2016

BREXIT

Tourism Business Confidence close

to max. levels since 2016

BUSINESS CONFIDENCE

CCI has experienced an

Uptrend since 2012 and is close to

max. levels

CONSUMERCONFIDENCE

The Spanish Tourism Industry is benefiting from the current geopolitical context

GEOPOLITICAL CONTEXT

grew by 3.2% during 2016.

Tourism accounts for 11.3%

of Spain’s GDP

SPAIN’S GDP

75.6 million tourists came to Spain in 2016 spending €77.6k million

RECORD FIGURES 2016

Spanish Tourism industry

acknowledged as the world’s most

competitive

TOURISM COMPETITIVENESS

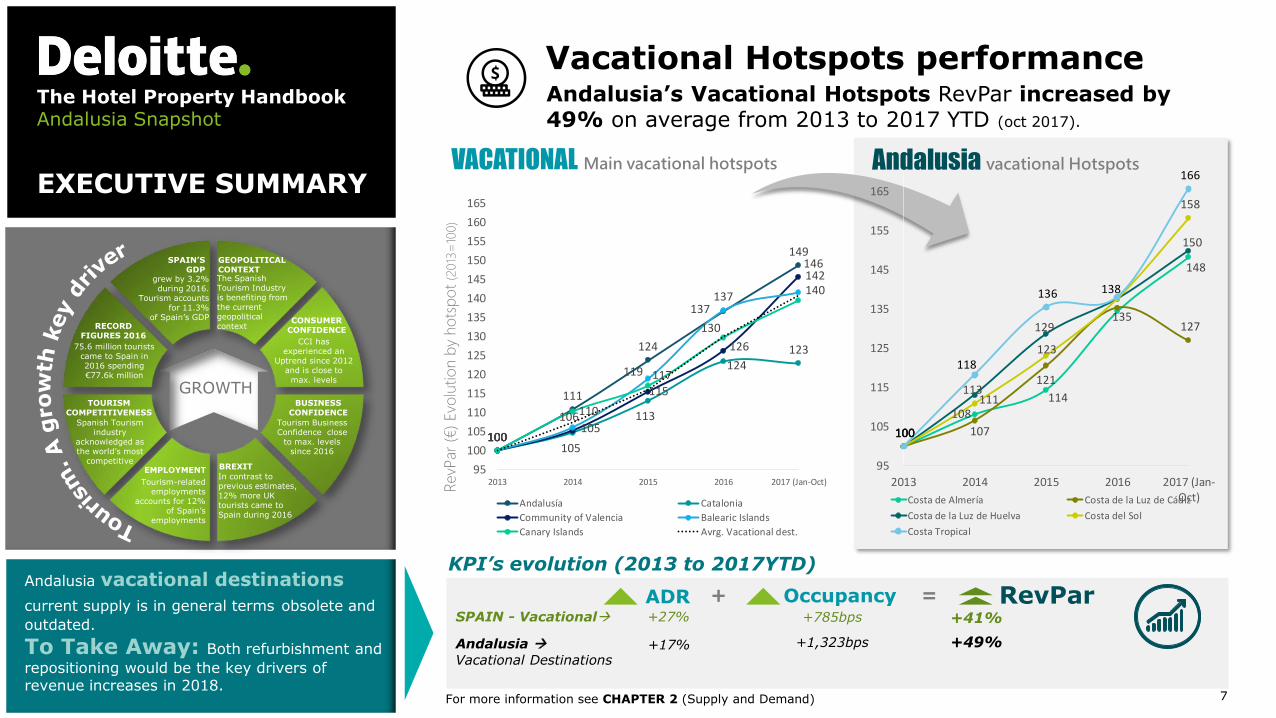

Andalusia vacational Hotspots

RevP

ar(€

) Evo

lutio

n b

y ho

tsp

ot

(2013

=10

0)

VACATIONAL Main vacational hotspots

For more information see CHAPTER 2 (Supply and Demand)

Vacational Hotspots performanceAndalusia’s Vacational Hotspots RevPar increased by 49% on average from 2013 to 2017 YTD (oct 2017).

KPI’s evolution (2013 to 2017YTD)

ADR RevParOccupancy+ =SPAIN - Vacational +27% +785bps +41%

Andalusia

Vacational Destinations

+1,323bps +49%

Andalusia vacational destinations

current supply is in general terms obsolete and

outdated.

To Take Away: Both refurbishment and

repositioning would be the key drivers of revenue increases in 2018.

100

111

124

137

149

100105

113

124123

100105

115

126

146

100

106

119

137

142

100

110

117

130

140

95

100

105

110

115

120

125

130

135

140

145

150

155

160

165

2013 2014 2015 2016 2017 (Jan-Oct)

Andalusía Catalonia

Community of Valencia Balearic Islands

Canary Islands Avrg. Vacational dest.

100

108

114

135

148

100 107

121

127

100

113

129

150

100

111

123

158

100

118

136 138

166

95

105

115

125

135

145

155

165

2013 2014 2015 2016 2017 (Jan-Oct)Costa de Almería Costa de la Luz de Cádiz

Costa de la Luz de Huelva Costa del Sol

Costa Tropical

+17%

@ 2016 Deloite Financial Advisory 8

111

130

147

166

105

116

128

141

100

119

130

144

168

106

121

132

139

95

100

105

110

115

120

125

130

135

140

145

150

155

160

165

170

2013 2014 2015 2016 2017(Jan-Oct)

Sevilla Granada

Malaga Córdoba

Avrg. Urban destinations (Spain)

EXECUTIVE SUMMARY

The Hotel Property HandbookAndalusia Snapshot

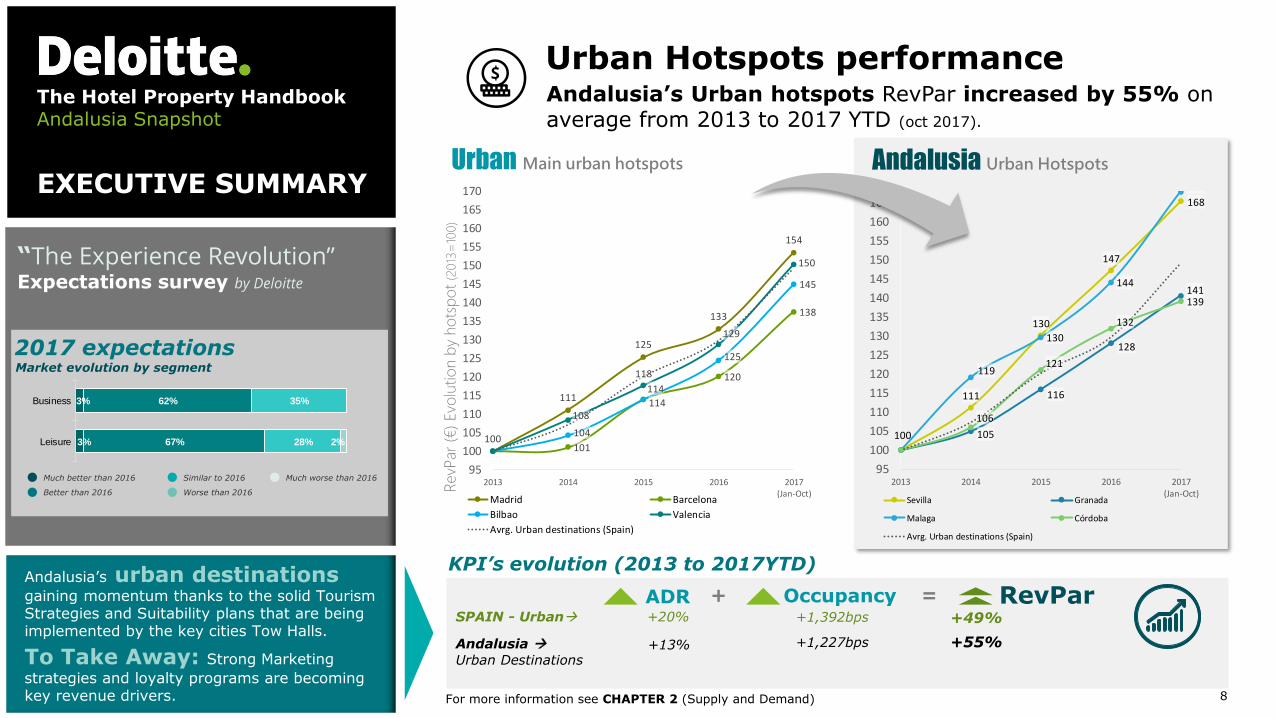

Andalusia Urban Hotspots

RevP

ar(€

) Evo

lutio

n b

y ho

tsp

ot

(2013

=10

0)

Urban Main urban hotspots

For more information see CHAPTER 2 (Supply and Demand)

Urban Hotspots performanceAndalusia’s Urban hotspots RevPar increased by 55% on average from 2013 to 2017 YTD (oct 2017).

Andalusia’s urban destinations gaining momentum thanks to the solid Tourism Strategies and Suitability plans that are being implemented by the key cities Tow Halls.

To Take Away: Strong Marketing

strategies and loyalty programs are becoming key revenue drivers.

KPI’s evolution (2013 to 2017YTD)

ADR RevParOccupancy+ =SPAIN - Urban +20% +1,392bps +49%

Andalusia

Urban Destinations

+1,227bps +55%+13%

“The Experience Revolution” Expectations survey by Deloitte

3%

3%

62%

67%

35%

28% 2%

Business

Leisure

2017 expectations

Better than 2016

Much better than 2016

Worse than 2016

Similar to 2016 Much worse than 2016

Market evolution by segment

100

111

125

133

154

101

114

120

138

104

114

125

145

108

118

129

150

95

100

105

110

115

120

125

130

135

140

145

150

155

160

165

170

2013 2014 2015 2016 2017(Jan-Oct)

Madrid Barcelona

Bilbao Valencia

Avrg. Urban destinations (Spain)

@ 2016 Deloite Financial Advisory 9

New openings22%

Refurbishment7%

Chain/Brand Conversion

67%

Ongoing projects

4%

New openings20%

Refurbishment18%

Chain/Brand Conversion

51%

Ongoing projects

11%

82 62 68 57 56 34 54 50

6.907

5.3965.745

5.120

3.124 2.825

5.6974.973

0

2000

4000

6000

8000

10000

12000

-

20

40

60

80

100

120

140

160

180

200

2010 2011 2012 2013 2014 2015 2016 2017 YTD

New Hotels # rooms

EXECUTIVE SUMMARY

The Hotel Property HandbookAndalusia Snapshot

For more information see CHAPTER 2 (Supply and Demand)

Spanish hotel new openingsSignificant hotel openings during 2017YTD (Dec. 2017)

Hotel openings trend (2010-17 YTD) (number of hotels and rooms)

Source: Censo Alimarket Hoteles

Source: Censo Alimarket Hoteles (2017YTD – Dic. 2017)

New Openings

Refurbishment

Chain/Brand Conversion

Ongoing Projects

10 Hotelsc.818 Rooms

3 Hotels1,072 Rooms

31 Hotels3,840 Rooms

2 Hotels184 Rooms

AndalusiaFigures

Spain Andalusia

2017 YTD openings by type of project:

The main chains’ priorities are asset renovation, brand repositioning, innovation and

sustainability in order to overcome seasonality and foster client loyalty.

@ 2016 Deloite Financial Advisory 10

P&L reconstruction Restructuring of the Financial Sector

Improvement of fundamentals

Alternative to the fixed income / bond yields

Senior Debt: Yielding assets:

gathering momentum

MAIN DRIVERS FOR THE INCREASING LENDING DEMAND

Monetary Policy: QE, low funding costs, etc.

Excess of Liquidity: Increase in transactions

Entry of new sponsors

FINANCIAL SECTOR

REAL ESTATE INVESTMENT MARKET

MACROECONOMIC ENVIRONMENT

Yielding assets: Increasing lending demand due to the outstanding tourism industry performance

Financing MarketThe Hotel Property HandbookAndalusia Snapshot

EXECUTIVE SUMMARY

Source: Deloitte

For more information see CHAPTER 4 (Key Investment and Financing Drivers)

Main

Conditio

ns

LTV (1)

Upfront Fee

Spread

45-50% 45-55%

2015 2016

150-250bps 125-175bps

225-400bps 200-250bps

Framework

Main Players

Balloon (2) 60-80% 65-100%

Credit Access Constraints

Financing Upturn

Institutional Investors / Debt

Funds

Banking / Insurance Companies

2013-14

50-60%

100-150bps

175-225bps

70-100%

Location, category, performance, type of operating contract (and mandatory period duration)and hotel brand significantly affect financing terms.

2017YTD

50-65%

90-135bps

150-225bps

70-100%

(1) Sustainable LTV to deal with the debt service with high funding costs (A higher LTV will result in a greater debt service)(2) A Balloon is required to cover the high funding costs during the loan´s life (a lower balloon will result in a greater annual debt

service). Estimated balloon for a 5-7 years loan.

Development loans: Traditional lenders are

coming back

@ 2016 Deloite Financial Advisory 11

The Most active players are expected

to stay active in 2018:

Main Players:

Equity

Debt

2016 2017THE CORE PROFILE STILL DOMINATES THE MARKET:

Source: Deloitte

The Hotel Property HandbookAndalusia Snapshot

EXECUTIVE SUMMARY

Source: Deloitte

For more information see CHAPTER 4 (Key Investment and Financing Drivers)

Main Chains

NPLs portfolios

Local PlayersMore than 10,000 rooms in Spain

Miguel Sanchez Hoteles

Core

67%

Core+

29%

Value

Added4%

€mCore 1,822

Core+ 790

Value Added 105

Core

79%

Core+

11%

Value

Added10%

€mCore 1,702

Core+ 234

Value Added 209

@ 2016 Deloite Financial Advisory 12

The Hotel Property HandbookAndalusia Snapshot

WHAT IS

NEXT?

@ 2016 Deloite Financial Advisory 13

The Hotel Property HandbookAndalusia Snapshot

EXECUTIVE SUMMARY

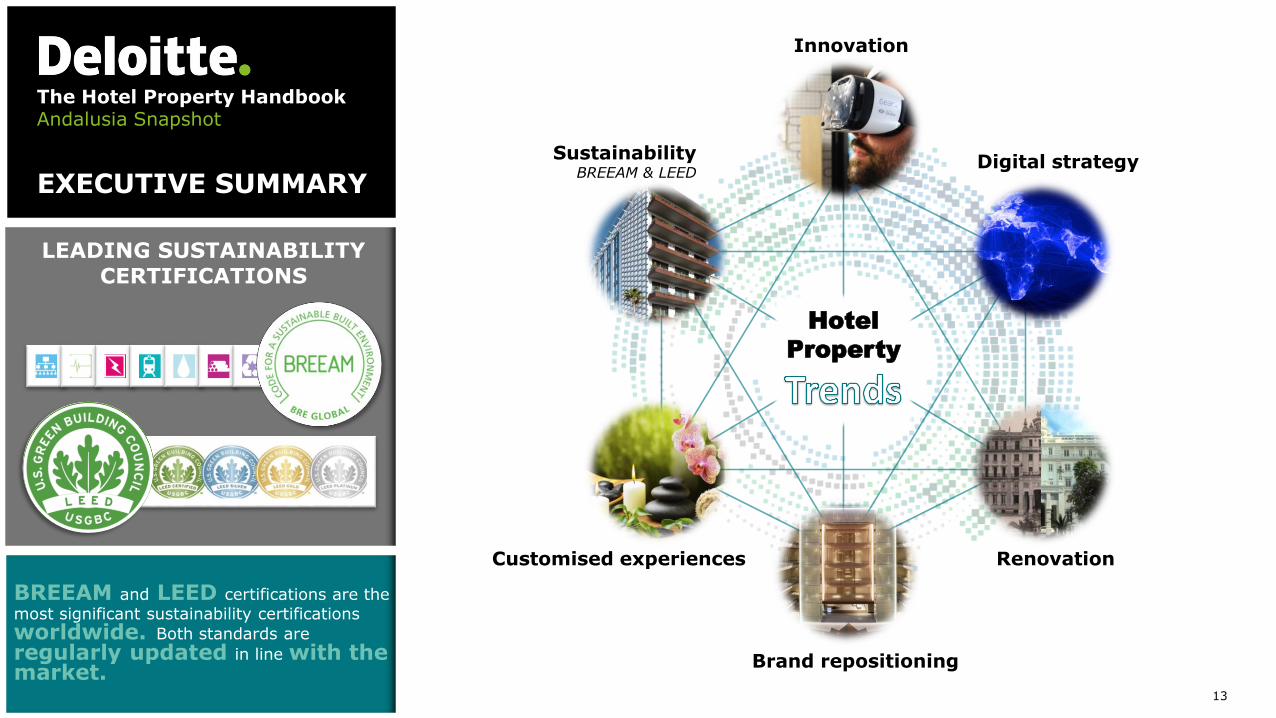

Hotel

Property

Digital strategy

RenovationCustomised experiences

Brand repositioning

Innovation

SustainabilityBREEAM & LEED

BREEAM and LEED certifications are the

most significant sustainability certifications

worldwide. Both standards are

regularly updated in line with the market.

LEADING SUSTAINABILITY CERTIFICATIONS

@ 2016 Deloite Financial Advisory 14

The Hotel Property HandbookAndalusia Snapshot

EXECUTIVE SUMMARY

“Expectativas 2017The Experience Revolution”

Most significant value drivers for CEOs in 2017

Select the two most significant drivers to improve capital and asset efficiency in 2017#1

Incomeincrease

#2Operating margin improvement

#3Talent and brandmanagement

#4Asset and capital efficiency

35%

33%

28%

25%

23%

17%

15%

15%

7%

2%

Investment repositioning

Optimise and invest in asset maintenance

Systems investments

Non-profitable asset sales

Cash Management

Funding sources renegotiation

Accounts receivable and payable management

Acquisitions

Supplier and debtor management

CapEx optimisation

@ 2016 Deloite Financial Advisory 15

The Hotel Property HandbookAndalusia Snapshot

Javier García-Mateo, MRICS

PartnerFinancial Advisory ‖ Real Estate

[email protected]: +34 659 90 02 15

Leopoldo Parias

PartnerFinancial Advisory [email protected]: +34 629894186

Jose María Espejo

Senior ManagerFinancial Advisory ‖ Real Estate

[email protected]: +34 918 232 692

Jordi Schoenenberger

PartnerHospitality Industry [email protected]: +34 932 543 932

Fernando Baldellou

PartnerHead of Financial Advisory – Hospitality [email protected]: +34 914 432 514

@ 2016 Deloite Financial Advisory 16