41

THE INSIDERS VIEW CONSUMER TRENDS TO BOOST BUSINESS Angela L. Talton Chief Diversity Officer Nielsen Powered by mr. cooper

THE INSIDERS VIEWCONSUMER TRENDS

TO BOOST BUSINESS

Angela L. TaltonChief Diversity Officer

NielsenPowered by mr. cooper

2Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

Angela TaltonChief Diversity Officer | NielsenSeptember 19, 2017

THE IMPACT OF DIVERSITY AMONGST MILLENNIALS ON THE FUTURE OF U.S. HOMEOWNERSHIP

3Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

ABOUT NIELSEN

4Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

THE MOST COMPLETE VIEW OF THE CONSUMER

SURVEYS FROM 500,000+

MOBILE USERS

6.7 BILLIONSTORE TRANSACTIONS PER MONTH

WHAT CONSUMERS BUY

250,000PANEL

HOUSEHOLDS

1.7 MILLIONSTORE VISITS

PER MONTH34 MILLIONRETAIL PRODUCTS

WHAT CONSUMERS WATCH

294 Million U.S. TV

VIEWERS

24X7 MONITORING AT 9,000 STATIONS IN 900 U.S. SITES

1.7 BILLIONVIEWING

RECORDS PER MONTH

We supplement the Watch & Buy consumer picture by measuring consumers’ shopping and viewing habits online and on mobile devices:

CAPTURING ONLINE DATA

MEANINGFUL PARTNERSHIPS

1.6 TRILLIONIMPRESSIONS PER YEAR

CAPTURING MOBILE DATA

SURVEYS FROM 500,000+ MOBILE USERS

7 MILLIONWEB EVENTS DAILY FROM

MOBILE DEVICES

5Copy

right

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

OUR CLIENTS INCLUDE...

6Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

THE CHANGING FACE OF AMERICA’S FUTURE

7Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

AMERICAN DIVERSITY IS DESTINYGROWTH IN POPULATION BY RACE & ETHNICITY

2020 2030 2040 2050

Growth Volume (net new, 000’s) 12,533 12,064 10,354 9,869

92% of the

tota l growth in U.S. popu la tion from 2000 to 2014 cam e from m ulticu ltu ra l consum ers

Source : Nie lsen The Multicu ltu ra l Edge : Supe r Consum ers Rising March 2015 Report

8Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

1 Los Angeles County California Los Angeles, CA2 Cook County Illinois Chicago, IL3 Harris County Texas Houston, TX4 Maricopa County Arizona Phoenix et al, AZ5 San Diego County California San Diego, CA6 Orange County California Los Angeles, CA7 Miami-Dade County Florida Miami-Ft. Lauderdale, FL8 Kings County New York New York, NY9 Dallas County Texas Dallas-Ft. Worth, TX10 Queens County New York New York, NY11 Riverside County California Los Angeles, CA12 San Bernardino County California Los Angeles, CA13 King County Washington Seattle-Tacoma, WA14 Clark County Nevada Las Vegas, NV15 Tarrant County Texas Dallas-Ft. Worth, TX16 Santa Clara County California San Francisco et al, CA17 Broward County Florida Miami-Ft. Lauderdale, FL18 Bexar County Texas San Antonio, TX19 Wayne County Michigan Detroit, MI20 New York County New York New York, NY21 Alameda County California San Francisco et al, CA22 Middlesex County Massachusetts Boston et al, MA-NH23 Philadelphia County Pennsylvania Philadelphia, PA24 Suffolk County New York New York, NY25 Sacramento County California Sacramento et al, CA

THE MULTICULTURAL FUTURE IS NOWRANK NAME STATE NIELSEN DMA

21of 25MOST POPULOUS COUNTIES ARE

MAJORITY MULTICULTURAL

Source: Multicultural Edge: Rising Super Consumers, 2015

9Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

MULTICULTURAL BUYING POWER ENERGIZES THE U.S. ECONOMY

Source: University of Georgia, Selig Center for Economic Growth

$316 billion

$210 billion

$115 billion

$601 billion

$491 billion

$274 billion

$1 trillion

$951 billion

$599 billion

$1.3 trillion

$1.2 trillion

$891 billion

10Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

YEARS OF EFFECTIVE BUYING POWER STRONGEST AMONG MULTICULTURAL CONSUMERS

WHITENON HISPANIC

Source: Nielsen The Multicultural Edge: Super Consumers Rising March 2015 Report

AFRICAN -AMERICAN

ASIAN -AMERICAN

HISPANIC

LIFE EXPECTANCY

YEARS OF EFFECTIVE BUYING POWER

78.7 74.3 87.3 83.5

37 42 52 57

MEDIAN AGE 42 32 35 27

11Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

MILLENNIALS

12Copy

right

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

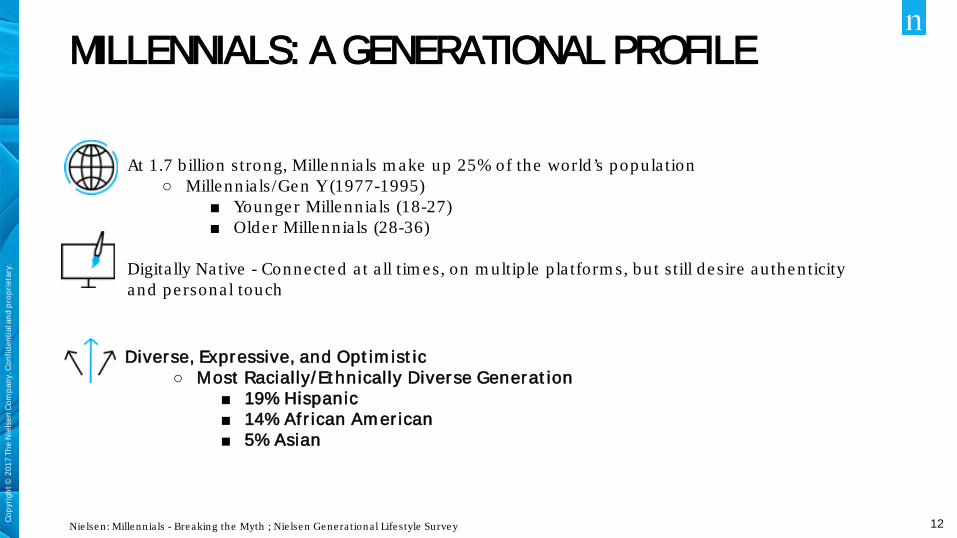

MILLENNIALS: A GENERATIONAL PROFILE

Nie lsen : Millennia ls - Breaking the Myth ; Nie lsen Gene ra tional Life style Survey

At 1.7 b illion strong, Millennia ls m ake up 25% of the world’s popula tion○ Millennia ls/Gen Y (1977-1995)

■ Younger Millennia ls (18-27)■ Olde r Millennia ls (28-36)

Digita lly Native - Connected a t a ll tim es, on m ultip le p la tform s, bu t still de sire au thenticityand pe rsona l touch

Diverse, Expressive, and Opt im ist ic○ Most Racially/Et hnically Diverse Generat ion

■ 19% Hispanic■ 14% Afr ican Am er ican■ 5% Asian

13Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

MILLENNIALS ARE MULTICULTURAL

Source: Nielsen, The Multicultural Edge: Rising Super Consumers, March 2015

Age

Age

Age

Age

Age

Age

Age

Age

Age

Age

GI G

enBo

omer

Gen

-X

Mill

enni

alG

en N

ext

Non Hispanic Whit e, %NHWMult icult ural (al l ot her ), %MC

Am er ican Diversit y by Generat ion

15Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

THE ECONOMIC POWER OF MULTICULTURAL MILLENNIALS

Multicu ltura l Millennia ls in fluence $1 trillion in to ta l fast m oving consum er good and en te rta inm ent spending

Over one -th ird of Multicu ltura l Millennia ls have an ave rage annua l incom e of ove r $50,000

Source : Multicu ltu ra l Millennia ls: The Multip lie r Effect, report 2017

16Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

16

AFRICAN-AMERICAN CONSUMERS

17Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

African-American population is currently

46.3 m il l ion.

Black m illennia ls repre sent 14% of the to ta l m illennia l

popula tion .

POPULATION EDUCATION

21% of Black Millennia ls have earned a t least an

Associa te ’s Degree .

In 2012-13, Black wom en earned 65% of Bache lor’s Degrees awarded to Black

students.

FINANCIAL

The num ber of Black households earn ing $75k to

$100k increased by 35%be tween 2004 & 2014.

African-Am ericans own 2.6 m il l ion businesses with

$150 bil l ion in revenue .

African-Am erican consum ers

con tro l $1.2 Tr i l l ion

in annua l buying power

IMPRESSIVE SOCIOECONOMIC GAINS

18Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

WHERE TO REACH BLACK CONSUMERS

Source : Se lig Cente r for Econom ic Growth , Te rry College of Business, Unive rsity of Georgia , 2015.

• The sta tes with the top Black buying power in 2015 were :

o New York $109 b illion

o Texas $106 b illion

o Californ ia $84 b illion

o Georgia $81 b illion

o Florida $80 b illion

• Sta tes with the h ighest p rojected growth in Black buying power a re in the south , bu t a lso include New York, Ca liforn ia and Illinois

o These sta tes include Black popula tion cente rs New York City, Los Ange les and Chicago

19Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

BLACK CONSUMERS ARE INFLUENTIAL

73% 67%Of Whites Of Hispanics

Believe Black consumers influence mainstream culture

Source: Burrell 40, 2011

20Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

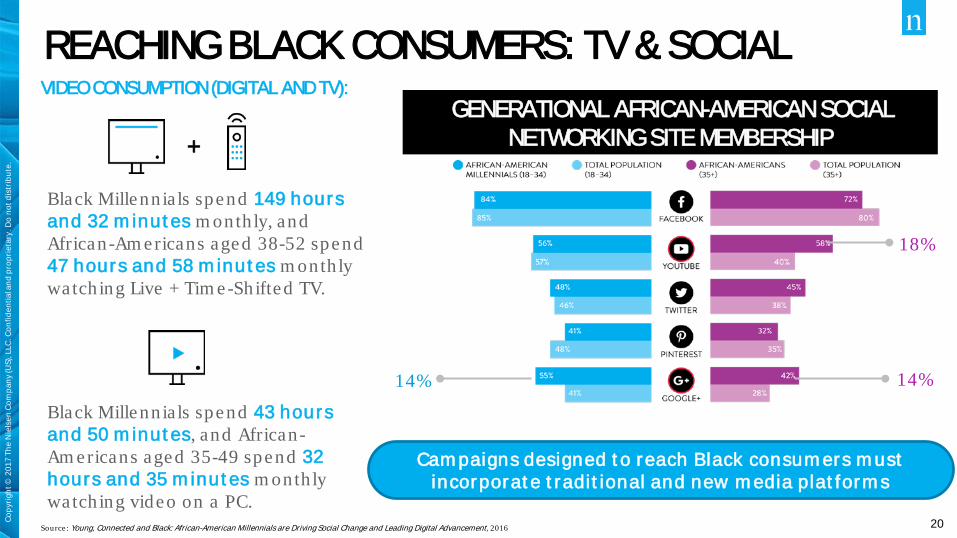

REACHING BLACK CONSUMERS: TV & SOCIALVIDEO CONSUMPTION (DIGITAL AND TV):

Black Millenn ials spend 149 hours and 32 m inut es m onth ly, and African-Am ericans aged 38-52 spend 47 hours and 58 m inut es m onth ly watch ing Live + Tim e-Shifted TV.

Black Millenn ials spend 43 hours and 50 m inut es, and African-Am ericans aged 35-49 spend 32 hours and 35 m inut es m onth ly watch ing video on a PC.

+

Source : Young, Connected and Black: African-American Millennials are Driving Social Change and Leading Digital Advancement, 2016

GENERATIONAL AFRICAN-AMERICAN SOCIAL NETWORKING SITE MEMBERSHIP

18%

14%14%

Cam paigns designed t o reach Black consum ers m ust incorporat e t radit ional and new m edia plat form s

21Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

ASIAN AMERICAN CONSUMERS

22Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Asian American population is currently

21.3 m il l ion.

The Asian Am erican popula tion has increased by

47% in the last 10 years.

POPULATION EDUCATION

Near ly half of Asian Am erican wom en have

earned a Bache lor’s Degree or h ighe r

Both U.S.-born and fore ign-born Asian Am erican

wom en have h ighe r ra te s of educa tion than the ave rage

Am erican wom an.

FINANCIAL

39% of Asian Am ericans have a household incom e

h ighe r than $100,000

Of the 87 U.S. sta rt-ups va lued a t ove r $1 b illion , 19

were sta rted by Asian Am ericans

Asian Am erican consum ers

con tro l $891 Bil l ion

in annua l buying power

FASTEST GROWING MULTICULTURAL GROUP IN THE U.S.

23Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

ASIAN AMERICAN POPULATION CENTERED IN CALIFORNIA POPULATION

BUYING POWER

= 31% = 9% = 7%

= 33% = 8%= 9%

Source: University of Georgia, Selig Center for Economic Growth

24Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

ASIAN AMERICAN CONSUMERS ARE DIVERSE

ANCESTRY OF ASIAN AMERICAN FEMALES 2015 • 19% of recen t im m igrants to the United

Sta te s a re Asian Am erican fem ales, ou tpacing even Hispan ic m ales.

• The m ajority of these recen t im m igrants cam e from India (25%), China (23%) and the Phil ippines (12%).

• Two-t hirds of Asian Am ericans speak a language o the r than English in the hom e

o In to ta l, the re a re 52 languages spoken by Asian Am ericans in the U.S. o the r than English .

Source : Asian Am erican Wom en: Digita lly Fluen t with an In te rcu ltu ra l Mindse t, 2017

25Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

REACH ASIAN AMERICAN CONSUMERS ON DIGITAL PLATFORMS

98% of Asian Am erican adu lts use apps and b rowse the web on sm artphones pe r m onth , 6% highe r than the to ta l popu la tion

Asian Am ericans spend 47 hours and 18 m inut es per m onth watch ing video on PCs, nearly 6 hours m ore than the to ta l popu la tion

10%

of Asian Am erican households a re b roadband on ly, doub le the ra te

of the to ta l popu la tion

81 HOURS, 14 MINUTES

Asian Am ericans, on ave rage , watch 81 hours and 14 m inu te s of TV pe r m onth , the lowest

of any m ulticu ltu ra l group

Asian Am er ican consum ers are digit al pioneers, so cam paigns designed t o reach t hem m ust incorporat e t he lat est t ech and digit al plat form s

26Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

HISPANIC/LATINO CONSUMERS

27Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Hispanic/Latino population is currently57 m il l ion.

The Hispanic popula tion is expected to m ore t han

double by 2060.

POPULATION EDUCATION

Between 2013 and 2015, 74% of Latinas enro lled in co llege im m edia te ly a fte r

graduating h igh school

Be tween 2005 and 2015, the pe rcentage of La tinas with Bache lor’s degrees

increased by 4%

FINANCIAL

There a re currently 1.5 m il l ion Latina-owned businesses in the U.S.,

gene ra ting $78.7 bil l ion in annual sa le s

52% of Latinas say it is the ir goa l to m ake it to the top of

the ir profe ssion

Hispan ic consum ers

con tro l $1.4 Tr i l l ion

in annua l buying power

DRIVERS OF THE U.S. POPULATION

28Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

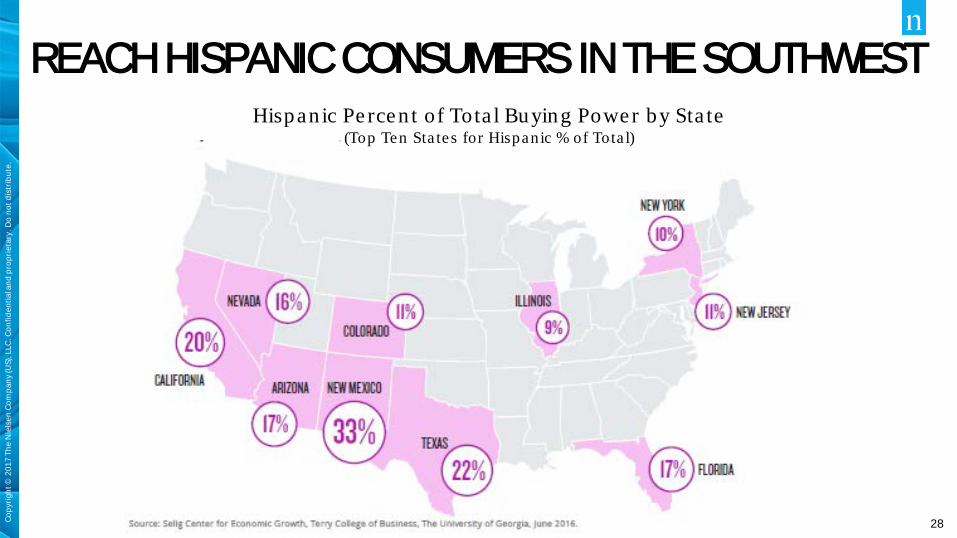

REACH HISPANIC CONSUMERS IN THE SOUTHWESTHispan ic Pe rcen t of Tota l Buying Power by Sta te

(Top Ten Sta tes for Hispanic % of Tota l)

29Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

A BILINGUAL CONSUMER GROUP

• Well over half of La tinos speak Span ish in the hom e , and on ly one -fifth of La tinos speak English on ly in the hom e

• In orde r to reach Hispan ic consum ers, com panies m ust deve lop re levan t m essaging in bot h English and Span ish

30Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

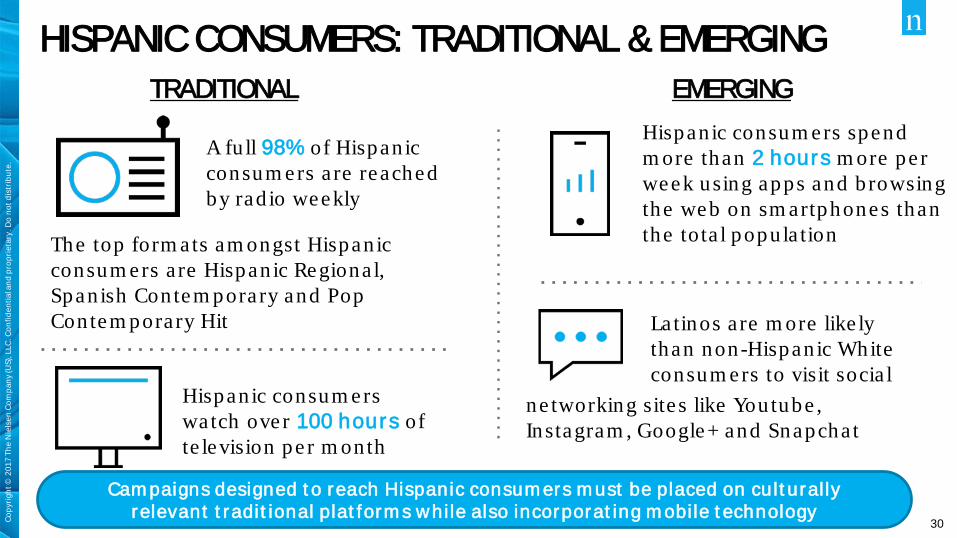

HISPANIC CONSUMERS: TRADITIONAL & EMERGING

A fu ll 98% of Hispan ic consum ers a re reached by rad io weekly

The top form ats am ongst Hispan ic consum ers a re Hispan ic Regiona l, Span ish Contem porary and Pop Contem porary Hit

TRADITIONAL

Hispan ic consum ers watch ove r 100 hours of te levision pe r m onth

EMERGINGHispan ic consum ers spend m ore than 2 hours m ore pe r week using apps and b rowsing the web on sm artphones than the tota l popu la tion

Latinos a re m ore like ly than non-Hispan ic White consum ers to visit socia l

ne tworking site s like Youtube , Instagram , Google+ and Snapcha t

Cam paigns designed t o reach Hispanic consum ers m ust be placed on cult ural ly relevant t radit ional plat form s while also incorporat ing m obile t echnology

31Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

OUR PRESENT –AND OUR FUTURE – IS MULTICULTURAL

Millenn ia ls a re the la rgest and m ost d ive rse genera tion in the U.S.

Multicu ltu ra l consum ers a re se t to m ake up the m ajority of the U.S. popula tion by 2060.

Com panies ab le to m ake m eaningfu l connections with m ulticu ltu ra l consum ers now can see increased fu ture ROI.

32Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

REGARDING HOMEOWNERSHIP –MILLENNIALS HAVE DELAYED ADULTHOOD

Source: American Community Survey

26% 23%

44%37%

25% 25%

40%34%35%

29% 27% 26%

LIVE WITH PARENT IN SCHOOL MARRIED HAVE CHILD

1990 2000 2014

18 TO 34 YEAR OLDS

33Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

HOUSEHOLDS HEADEDBY MILLENNIALS (MILLIONS)*

MILLENNIAL SHARE OF:

MILLENNIAL HOUSING DEMAND IS ON THE RISE. . . AND WILL ACCOUNT FOR A SIGNIFICANT SHARE OF HOUSING SPEND.

Source: Demand Institute estimates based on U.S. Census Bureau Population Projections (2014)*Based on stated intentions from current/existing households.

26.6

39.3

2015 2020

CURRENT HOUSEHOLDS

FUTURE HOME PURCHASES*

FUTURE HOME LEASES*

22%

41%

43%

NEX

T 5 YEA

RS

2015

+48%

34Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

THEY ARE STILL SEEKING THE AMERICAN DREAM. . . AND STILL BELIEVE HOUSING IS AN EXCELLENT INVESTMENT.

Note: Among 18 to 34 year olds.Source: The Demand Institute U.S. Housing & Communities Survey (2015)

75%Believe ownership is an important long-term goal

13%

35%

52%

80%Believe ownership is an excellent investment

PLAN TO PURCHASE

ALREADY OWN

WILL NOT PURCHASE

35Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

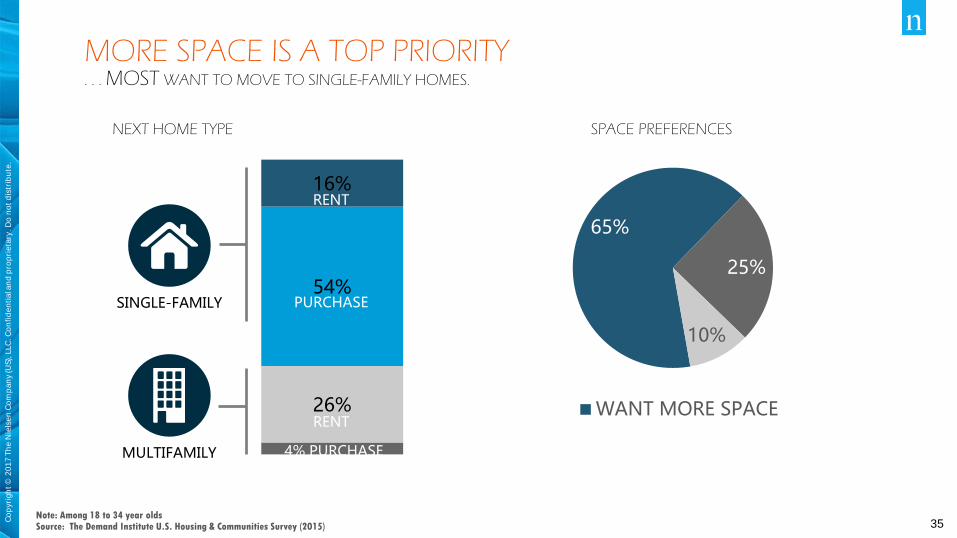

26%

54%

16%

MORE SPACE IS A TOP PRIORITY. . . MOST WANT TO MOVE TO SINGLE-FAMILY HOMES.

Note: Among 18 to 34 year oldsSource: The Demand Institute U.S. Housing & Communities Survey (2015)

Easy

NEXT HOME TYPE

65%

25%

10%

WANT MORE SPACE

RENT

PURCHASE

RENT

4% PURCHASE

SPACE PREFERENCES

SINGLE-FAMILY

MULTIFAMILY

36Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

Note: Among the top 100 Core Based Statistical AreasSource: Nielsen PopFacts (2016)

POPULATION GROWTH WILL BE STRONG IN SOUTH. . . SOME AREAS MAY SEE DECLINES IN YOUNGER HOUSEHOLDS.

CHANGE IN 18 TO 34 POPULATION FOR THE TOP 100 METRO AREAS,2016 TO 2021

37Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

30%

35%

40%

45%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Note: The home ownership rate is based on 3-year moving averages.Source: Current Population Survey March ASEC

HOME OWNERSHIP IS ON THE DECLINE

18 TO 34 HOME OWNERSHIP RATE

. . . EVEN FOR MORE AFFLUENT & MARRIED HOUSEHOLDS.

<$35K-4%

CHANGE IN OWNERSHIP RATE SINCE 2010

$35-74K-8%

$75K+-12%

MARRIED-8%

SINGLE-7%

HO

US

EH

OLD

IN

CO

ME

MA

RITA

L S

TATUS

38Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

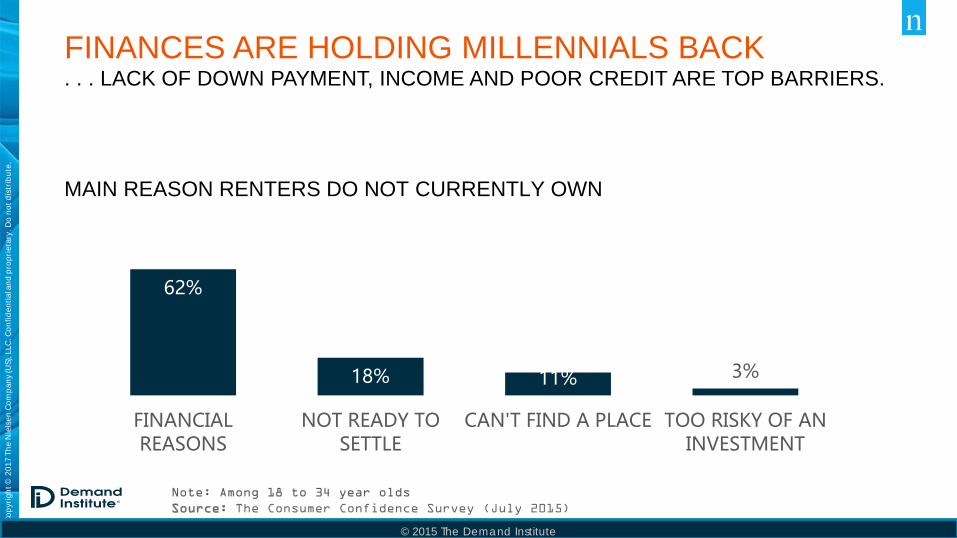

62%

18% 11% 3%

FINANCIALREASONS

NOT READY TOSETTLE

CAN'T FIND A PLACE TOO RISKY OF ANINVESTMENT

FINANCES ARE HOLDING MILLENNIALS BACK

Note: Among 18 to 34 year oldsSource: The Consumer Confidence Survey (July 2015)

MAIN REASON RENTERS DO NOT CURRENTLY OWN

. . . LACK OF DOWN PAYMENT, INCOME AND POOR CREDIT ARE TOP BARRIERS.

39Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

© 2015 The Demand Institute

MILLENNIALS DO FACE FINANCIAL CHALLENGES. . . BUT ARE HOPEFUL THAT THEIR SITUATION WILL IMPROVE.

Note: Assets and debt in 2013 dollars.Source: Federal Reserve Bank Survey of Consumer Finances; The Demand Institute U.S. Housing & Communities Survey (2015)

52%Of renters think it will be difficult to qualify for a mortgage

80%Expect their financial situation to improve in the next few years

DEBT

ASSETS$8.1K

$8.7K

$4.6K

$7.0K

MEDIAN NON-HOUSING ASSETS & DEBT18 TO 34 YEAR OLD HOUSEHOLDS

2001 2013

40Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

40Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

THANK YOU

41Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Nielsen Community

@NielsenKnows

Angela Talt onChie f Dive rsity Office r

Ange la .Ta lton@Nie lsen .com

FOR MORE INFORMATION, PLEASE VISIT NIELSEN.COM

42Copy

right

© 2

017

The

Nie

lsen

Com

pany

(US)

, LLC

. Con

fiden

tial a

nd p

ropr

ieta

ry. D

o no

t dis

trib

ute.

Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.