39

The International Price System Gita Gopinath Harvard Paper prepared for Jackson Hole Symposium 2015 1 / 27

The International Price System

Gita GopinathHarvard

Paper prepared for Jackson Hole Symposium 2015

1 / 27

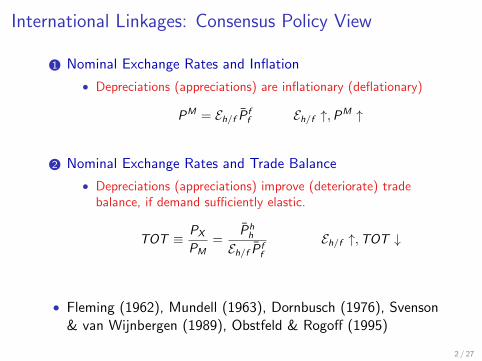

International Linkages: Consensus Policy View

1 Nominal Exchange Rates and Inflation

• Depreciations (appreciations) are inflationary (deflationary)

PM = Eh/f P̄ ff Eh/f ↑,PM ↑

2 Nominal Exchange Rates and Trade Balance

• Depreciations (appreciations) improve (deteriorate) tradebalance, if demand sufficiently elastic.

TOT ≡ PX

PM=

P̄hh

Eh/f P̄ ff

Eh/f ↑,TOT ↓

• Fleming (1962), Mundell (1963), Dornbusch (1976), Svenson& van Wijnbergen (1989), Obstfeld & Rogoff (1995)

2 / 27

International Linkages: Consensus Policy View

1 Nominal Exchange Rates and Inflation

• Depreciations (appreciations) are inflationary (deflationary)

PM = Eh/f P̄ ff Eh/f ↑,PM ↑

2 Nominal Exchange Rates and Trade Balance

• Depreciations (appreciations) improve (deteriorate) tradebalance, if demand sufficiently elastic.

TOT ≡ PX

PM=

P̄hh

Eh/f P̄ ff

Eh/f ↑,TOT ↓

• Fleming (1962), Mundell (1963), Dornbusch (1976), Svenson& van Wijnbergen (1989), Obstfeld & Rogoff (1995)

2 / 27

International Linkages: Consensus Policy View

1 Nominal Exchange Rates and Inflation

• Depreciations (appreciations) are inflationary (deflationary)

PM = Eh/f P̄ ff Eh/f ↑,PM ↑

2 Nominal Exchange Rates and Trade Balance

• Depreciations (appreciations) improve (deteriorate) tradebalance, if demand sufficiently elastic.

TOT ≡ PX

PM=

P̄hh

Eh/f P̄ ff

Eh/f ↑,TOT ↓

• Fleming (1962), Mundell (1963), Dornbusch (1976), Svenson& van Wijnbergen (1989), Obstfeld & Rogoff (1995)

2 / 27

International Linkages: Consensus Policy View

1 Nominal Exchange Rates and Inflation

• Depreciations (appreciations) are inflationary (deflationary)

PM = Eh/f P̄ ff Eh/f ↑,PM ↑

2 Nominal Exchange Rates and Trade Balance

• Depreciations (appreciations) improve (deteriorate) tradebalance, if demand sufficiently elastic.

TOT ≡ PX

PM=

P̄hh

Eh/f P̄ ff

Eh/f ↑,TOT ↓

• Fleming (1962), Mundell (1963), Dornbusch (1976), Svenson& van Wijnbergen (1989), Obstfeld & Rogoff (1995)

2 / 27

3 / 27

Publications using BLS IPP data

1 “The International Price System,” Forthcoming Jackson Hole SymposiumProceedings, 2015.

2 Ariel Burstein and Gita Gopinath. “International Prices and ExchangeRates,” in Gopinath, G., Helpman, E., and Rogoff, K. (Eds.): Handbookof International Economics, Volume 4, 2014. Amsterdam: Elsevier

3 Gita Gopinath, Oleg Itskhoki and Brent Neiman. Trade Prices and theGlobal Trade Collapse of 2008-09,” IMF Economic Review, September2012, Volume 60(12)

4 Gita Gopinath and Oleg Itskhoki. “In Search of Real Rigidities,” NBERMacroeconomics Annual, 2010, Volume 25.

5 Gita Gopinath and Oleg Itskhoki. “Frequency of Price Adjustment andPass- through,?” Quarterly Journal of Economics, May 2010, Volume125(2).

6 Gita Gopinath, Oleg Itskhoki and Roberto Rigobon. “Currency Choiceand Exchange Rate Pass-through,?” American Economic Review, March2010, Vol- ume 100(1).

7 Gita Gopinath and Roberto Rigobon. “Sticky Borders,” Quarterly Journalof Economics, May 2008, Volume 123(2)

4 / 27

International Linkages• The International Price System

1 Dominance of dollar invoicing∗ in world trade.

2 International prices, in their currency of invoicing, are not verysensitive to exchange rates at horizons of up to two years.

• Inflation

PMUS︸︷︷︸

insulated

= P̄$ PMROW︸ ︷︷ ︸

sensitive

= EROW /$P̄$

• Terms of Trade

TOT︸ ︷︷ ︸stable

=P̄$h

P̄$f

• Devereux, Engel & Tille (2003), Corsetti & Pesenti (2005)

*currency in which an invoice for exported or imported goods is denominated. (Non-commodities)

5 / 27

International Linkages• The International Price System

1 Dominance of dollar invoicing∗ in world trade.

2 International prices, in their currency of invoicing, are not verysensitive to exchange rates at horizons of up to two years.

• Inflation

PMUS︸︷︷︸

insulated

= P̄$ PMROW︸ ︷︷ ︸

sensitive

= EROW /$P̄$

• Terms of Trade

TOT︸ ︷︷ ︸stable

=P̄$h

P̄$f

• Devereux, Engel & Tille (2003), Corsetti & Pesenti (2005)

*currency in which an invoice for exported or imported goods is denominated. (Non-commodities)

5 / 27

International Linkages• The International Price System

1 Dominance of dollar invoicing∗ in world trade.

2 International prices, in their currency of invoicing, are not verysensitive to exchange rates at horizons of up to two years.

• Inflation

PMUS︸︷︷︸

insulated

= P̄$ PMROW︸ ︷︷ ︸

sensitive

= EROW /$P̄$

• Terms of Trade

TOT︸ ︷︷ ︸stable

=P̄$h

P̄$f

• Devereux, Engel & Tille (2003), Corsetti & Pesenti (2005)

*currency in which an invoice for exported or imported goods is denominated. (Non-commodities)

5 / 27

International Linkages• The International Price System

1 Dominance of dollar invoicing∗ in world trade.

2 International prices, in their currency of invoicing, are not verysensitive to exchange rates at horizons of up to two years.

• Inflation

PMUS︸︷︷︸

insulated

= P̄$ PMROW︸ ︷︷ ︸

sensitive

= EROW /$P̄$

• Terms of Trade

TOT︸ ︷︷ ︸stable

=P̄$h

P̄$f

• Devereux, Engel & Tille (2003), Corsetti & Pesenti (2005)

*currency in which an invoice for exported or imported goods is denominated. (Non-commodities)

5 / 27

Road Map

• Illustration using three countries

• Empirical evidence for IPS (35 countries)• Dollar dominance• Low sensitivity to ER’s

• Empirical evidence for IPS using BLS IPP data

• Policy Implications

6 / 27

A Tale of Three CountriesER Pass-through into Import Prices

.3.4

.5.6

.7.8

.91

1.1

PAS

S-T

HR

OU

GH

1 2 3 4 5 6 7 8HORIZON (Quarters)

Turkey Japan United States

∆ipin,t = αn +∑T

k=0 βn,k∆en,t−k +∑T

k=0 γn,k∆ppin,t−k + εn,t , T = 8

ERPT Turkey Japan USOne quarter 93% 83% 34%Eight quarter 100% 90% 44%Foreign Invoicing 97% 76% 7%

7 / 27

Road Map

• Illustration using three countries

• Empirical evidence for IPS (35 countries)• Dollar dominance• Low sensitivity to ER’s

• Macro and micro implications of IPS: Casas, Diez, Gopinath,Gourinchas (2015)

8 / 27

Data

• Import Price Index and Producer Price Index data

• Construct trade weighted exchange rates and trade weightedPPI

• Bilateral trade flows: IMF’s Direction of Trade Statistics database

• Currency invoicing• Customs agencies, central banks, other statistical agencies• Kamps (2006), Chinn & Ito (2014)

• BLS confidential import and export price data

• I-O tables to measure import content in consumption

9 / 27

IPS Definition 1: Dominance of dollar invoicing in world trade

• Covers 55% of imports, 57% of exports. Averages post 1999.

• Dollar invoicing share: 4.7 times its share in world imports, 3.1 times itsshare in world exports.

• Euro invoicing share: 1.2 times for imports and exports.

• Goldberg (2013), Goldberg and Tille (2009), Ito and Chinn (2013)

10 / 27

IPS Definition 1: Dominance of dollar invoicing in world trade

Invoicing shares and GDP per capita0

.2.4

.6.8

1Sh

are

AU BE BR CA CO CY CZ DE EE FR GR HU ID IL IN IS IT JP LV

Dollar U.S. Trade

0.2

.4.6

.8Sh

are

CH ES LU MT NL NO PK PL PT RO SE SI TH TR UA UK

Dollar U.S. Trade

Figure : Dollar Dominance in World Trade: By Country

11 / 27

IPS Definition 1: Dominance of dollar invoicing in world trade

Country Imports Exports

United States 0.93 0.97Italy* 0.58 0.61Germany* 0.55 0.62Spain* 0.54 0.58France* 0.45 0.50United Kingdom 0.32 0.51Australia 0.31 0.20Switzerland 0.31 0.35Norway 0.30 0.03Sweden 0.24 0.39Japan 0.23 0.39Canada 0.20 0.23Poland 0.06 0.04Iceland 0.06 0.05Thailand 0.04 0.07Israel 0.03 0.00Turkey 0.03 0.02South Korea 0.02 0.01Brazil 0.01 0.01Indonesia 0.01 0.00India 0.00 0.00 12 / 27

IPS Definition 1: Dominance of dollar invoicing in world trade

Invoicing shares and GDP per capita

AR

AU

BE

BRBG

CA

CO

CY

CZ

EE

FRDE

GR

HU ISIN ID IL

IT

JP

LVLT

LU

MT

NL

NO

PKPL

PT

RO

SKSI

KR

ES

SECH

TH TRUA

UK

US

0.2

.4.6

.81

For

eign

Cur

renc

y In

voic

ing

Sha

re

7 8 9 10 11 12Log GDP Per Capita

(a) Imports

AR

AU

BRBG

CA

COCZ

HU ISIN ID IL

JPNO

PKPL

RO KR

SECH

TH TRUA

UK

US

0.2

.4.6

.81

For

eign

Cur

renc

y In

voic

ing

Sha

re7 8 9 10 11 12

Log GDP Per Capita

(b) Imports, Ex-Euro

13 / 27

IPS Definition 1: Dominance of dollar invoicing in world trade

Invoicing shares and GDP per capita

DZ AR

AU

ATBE

BRBG

CA

CO

CZ

FRDE

GR

HU ISIN ID IL

IT

JP

LVLT

LU

MY

NL

NOPKPL

PT

RO

SKSI

ZA

KR

ES

SECH

THTRUA

UK

US0.2

.4.6

.81

For

eign

Cur

renc

y In

voic

ing

Sha

re

7 8 9 10 11 12Log GDP Per Capita

(c) Exports

DZ AR

AU

BRBG

CA

CO

CZHU IS

IN ID IL

JP

MY NOPKPL

RO

ZA

KR

SECH

THTRUA

UK

US0.2

.4.6

.81

For

eign

Cur

renc

y In

voic

ing

Sha

re7 8 9 10 11 12

Log GDP Per Capita

(d) Exports, Ex-Euro

14 / 27

IPS Definition 1a: Relative Stability of invoicing patterns over time

0.3

.6.9

1995 2000 2005 2010 2015Australia

0.3

.6.9

2000 2005 2010 2015Iceland

0.3

.6.9

1990 1995 2000 2005 2010 2015Indonesia

0.3

.6.9

1970 1980 1990 2000 2010Japan

0.3

.6.9

2000 2005 2010 2015

Norway

0.3

.6.9

1995 2000 2005 2010 2015South Korea

0.3

.6.9

1995 2000 2005 2010 2015United States

0.3

.6.9

1995 2000 2005 2010 2015Thailand

0.3

.6.9

1995 2000 2005 2010 2015Turkey

Figure : Fraction Priced in Foreign Currency

15 / 27

IPS Definition 2a: Countries with high SRPT have high LRPT

• Dynamic Lag Regression

∆ipin,t = αn+T∑

k=0

βn,k∆en,t−k+T∑

k=0

γn,k∆ppin,t−k+εn,t , T = 8

• Cumulative Pass-through, PTn,m ≡∑m

k=0 βn,k

PTn,m = γ + ηPTn,1 + εn,m, m = 4, 8

• Start date 1990, 40 quarters at least, IP excluding petroleumfor U.S.

• VECM, Generated regressor bias

• Burstein and Gopinath (2014)

16 / 27

IPS Definition 2a: Countries with high SRPT have high LRPT (4 quarter)

ARAU

BRCA

COCZ DKEE

FIFR

DE

HK

HU

IE

IL

IT

JP

LV

MX

NL

NZNO

PK

PH

SG

ZA

KR

ES

SE

CH

TH

TR

UK

US

VE

.2.5

.81

.1F

OU

R Q

UA

RT

ER

.2 .5 .8 1.1ONE QUARTER

Four Quarter

Slope InterceptOLS 0.921 0.053

(0.11) (0.07)

Bootstrap

Mean 0.84 0.135th-pctile 0.57 -0.0895th-pctile 1.19 0.32S.D. 0.23 0.15

(R2 = 0.68, N = 35)

∆ipin,t = αn +∑T

k=0 βn,k∆en,t−k +∑T

k=0 γn,k∆ppin,t−k + εn,t , T = 8

PTn,4 = γ + ηPTn,1 + εn,4

17 / 27

IPS Definition 2a: Countries with high SRPT have high LRPT (8 quarter)

ARAU

BRCA

COCZ DK

EE

FIFR

DE

HK

HU

IE

ILIT

JP

LV

MX

NL

NZNO PK

PH

SG

ZA

KR

ES

SE

CH

TH

TR

UK

US

VE

.2.5

.81

.1E

IGH

T Q

UA

RT

ER

.2 .5 .8 1.1ONE QUARTER

Eight Quarter

Slope InterceptOLS 0.871 0.102

(0.14) (0.10)

Bootstrap

Mean 0.708 0.2505th-pctile 0.33 0.0095th-pctile 1.11 0.52S.D. 0.27 0.18

(R2 = 0.53, N = 35)

PTn,8 = γ + ηPTn,1 + εn,8

18 / 27

IPS Definition 2b: Countries with higher shares of imports invoiced in a foreign

currency have higher short-run and long-run pass-through

AR

AUBR

CA

COCZHU

ILJP

NO

PKKR

SE

CH

THTR

UK

US

FR

NL

.2.5

.81

.11 Q

UA

RT

ER

.2 .5 .8 1.1FOREIGN CURRENCY SHARE

1 Quarter

Fracforeign 0.70(0.16)

N 20R2 0.51

19 / 27

IPS Definition 2b: Countries with higher shares of imports invoiced in a foreign

currency have higher short-run and long-run pass-through

ARAU

BR

CA

COCZHU

IL

JP

NO

PKKR

SE

CH

TH

TR

UK

US

FR

NL

.2.5

.81.

14

QU

AR

TER

.2 .5 .8 1.1FOREIGN CURRENCY SHARE

ARAU

BRCA

COCZ

HU

IL

JP

NOPK

KRSE

CH

TH

TR

UK

USFR

NL

.2.5

.81.

18

QU

AR

TER

.2 .5 .8 1.1FOREIGN CURRENCY SHARE

4 Quarter 8 Quarter

Fracforeign 0.57 0.40(0.18) (0.18)

N 20 20R2 0.34 0.17

20 / 27

Detailed Evidence from the U.S.

1 US BLS price surveys, 1994.M1-2014.M6.• Gopinath, Itskhoki, Rigobon (2010)

2 Prices, as opposed to unit values

3 Exclude intra-firm transactions

4 Can condition on a price change

21 / 27

Detailed Evidence from the U.S.US BLS price surveys, 1994.M1-2014.M6, Gopinath, Itskhoki, Rigobon (2010)

0.2

.4.6

.81

1.2

PAS

S-T

HR

OU

GH

1 6 12 18 24HORIZON

DOLLAR NON DOLLAR ALL

Figure : Aggregate ERPT by Currency

22 / 27

0.3

.6.9

1.2

1 5 9 13 17 21 25

Germany

0.3

.6.9

1.2

1 5 9 13 17 21 25

Switzerland

0.3

.6.9

1.2

1 5 9 13 17 21 25

Italy

0.3

.6.9

1.2

1 5 9 13 17 21 25

UK

0.3

.6.9

1.2

1 5 9 13 17 21 25

Japan

0.3

.6.9

1.2

1 5 9 13 17 21 25

France

0.3

.6.9

1.2

1 5 9 13 17 21 25

Spain

0.3

.6.9

1.2

1 5 9 13 17 21 25

Belgium

0.3

.6.9

1.2

1 5 9 13 17 21 25

Netherlands

0.3

.6.9

1.2

1 5 9 13 17 21 25

Sweden

0.3

.6.9

1.2

1 5 9 13 17 21 25

Canada

0.3

.6.9

1.2

1 5 9 13 17 21 25

Austria

Figure : Aggregate ERPT by Currency by Country23 / 27

IPS Definition 2c: Border prices, in whatever currency they are set in, respond

partially to exchange rate shocks even conditional on a price change

go

PT Conditional on Price ChangeD ND

All 0.26 0.85Germany 0.32 0.85Switz. 0.21 0.67Italy 0.24 0.76UK 0.23 0.77France 0.19 0.72Spain 0.21 0.76Diff. 0.21 0.9310 HS 0.27 0.88Sufficient statistic for currency choice

24 / 27

IPS Definition 2c: Border prices, in whatever currency they are set in, respond

partially to exchange rate shocks even conditional on a price change

go

PT Conditional on Price ChangeD ND

All 0.26 0.85Germany 0.32 0.85Switz. 0.21 0.67Italy 0.24 0.76UK 0.23 0.77France 0.19 0.72Spain 0.21 0.76Diff. 0.21 0.9310 HS 0.27 0.88Sufficient statistic for currency choice

Life-long PTD ND

All 0.47 1.01

Diff. 0.39 0.98

24 / 27

International Price Systemgo

Endogenous currency choice: Price in a currency in which ‘desired’prices are most stable

• Strategic complementarity in pricing• Demand systems: Kimball (1995), Melitz and Ottaviano

(2008), Bergin and Feenstra (2001)• GIR(2010): Homogenous (differentiated) goods prices in

dollars (foreign currency)

• Imported input costs• Chung (2014)

• Can explain• Why SR and LRPT are similar

• Link between invoicing choices and PT

• Why dollar dominance hard to break

• Cannot be the full story: fixed costs important

25 / 27

International Price Systemgo

Endogenous currency choice: Price in a currency in which ‘desired’prices are most stable

• Strategic complementarity in pricing• Demand systems: Kimball (1995), Melitz and Ottaviano

(2008), Bergin and Feenstra (2001)• GIR(2010): Homogenous (differentiated) goods prices in

dollars (foreign currency)

• Imported input costs• Chung (2014)

• Can explain• Why SR and LRPT are similar

• Link between invoicing choices and PT

• Why dollar dominance hard to break

• Cannot be the full story: fixed costs important

25 / 27

International Price Systemgo

Endogenous currency choice: Price in a currency in which ‘desired’prices are most stable

• Strategic complementarity in pricing• Demand systems: Kimball (1995), Melitz and Ottaviano

(2008), Bergin and Feenstra (2001)• GIR(2010): Homogenous (differentiated) goods prices in

dollars (foreign currency)

• Imported input costs• Chung (2014)

• Can explain• Why SR and LRPT are similar

• Link between invoicing choices and PT

• Why dollar dominance hard to break

• Cannot be the full story: fixed costs important25 / 27

Policy Implications

1 Inflation Stabilization

InflationCPI = (Import Content) · (Import Pass-through)

• Following a 10% depreciation

Import Content InflationCPI

US 0.12 0.4 – 0.7

Japan 0.12 0.8 – 1.3

Mexico 0.15 1.38 – 1.59

Turkey 0.18 1.65 - 2.03

• Dollar appreciations:• Unlikely major disinflationary concern for US.• More significant inflationary concerns for a country like Turkey.

• Asymmetric monetary policy spillovers (parallel with assetmarkets)

26 / 27

Policy Implications

1 Inflation Stabilization

InflationCPI = (Import Content) · (Import Pass-through)

• Following a 10% depreciation

Import Content InflationCPI

US 0.12 0.4 – 0.7

Japan 0.12 0.8 – 1.3

Mexico 0.15 1.38 – 1.59

Turkey 0.18 1.65 - 2.03

• Dollar appreciations:• Unlikely major disinflationary concern for US.• More significant inflationary concerns for a country like Turkey.

• Asymmetric monetary policy spillovers (parallel with assetmarkets)

26 / 27

Policy Implications

1 Inflation Stabilization

InflationCPI = (Import Content) · (Import Pass-through)

• Following a 10% depreciation

Import Content InflationCPI

US 0.12 0.4 – 0.7

Japan 0.12 0.8 – 1.3

Mexico 0.15 1.38 – 1.59

Turkey 0.18 1.65 - 2.03

• Dollar appreciations:• Unlikely major disinflationary concern for US.• More significant inflationary concerns for a country like Turkey.

• Asymmetric monetary policy spillovers (parallel with assetmarkets)

26 / 27

Policy Implications

1 Inflation Stabilization

InflationCPI = (Import Content) · (Import Pass-through)

• Following a 10% depreciation

Import Content InflationCPI

US 0.12 0.4 – 0.7

Japan 0.12 0.8 – 1.3

Mexico 0.15 1.38 – 1.59

Turkey 0.18 1.65 - 2.03

• Dollar appreciations:• Unlikely major disinflationary concern for US.• More significant inflationary concerns for a country like Turkey.

• Asymmetric monetary policy spillovers (parallel with assetmarkets)

26 / 27

Policy Implications

2 Export Competitiveness: quantities versus mark-ups• Do depreciations (appreciations) make exports cheaper

(expensive)?• For the U.S., Yes• For most others, No: Mainly fluctuations in mark-ups (profits)

• Japan: 33% of exports invoiced in yen.• PT into dollar prices even conditional on a price change for

these goods is 23%

3 Internationalization of Currencies: chinese yuan• Added benefit of insulating domestic inflation from external

shocks.

4 Special Drawing Rights: more symmetry• Bring greater symmetry in policy spillovers.• To be privately optimal, will need a large number of importers

and exporters to price in SDRs.

27 / 27