23

The investment Four attempts to re-build 1 1989

The investment

Four attempts to re-build 1

1989

Today’s investment

Invested $300M to transform the old hangar to an Award Winning Terminal 2

Today

Tomorrow… Our investment

Investing $44M to extend the main terminal building & pier 3

2015

The story so far...

4

• Maintain the momentum and build on our Investment • Today’s presentation will cover:

• What underpins our growth and, • Our service delivery & our planned investment.

• Yes, we have a Commerce Commision report, more about that later…

Value proposition

5 Customer Value Proposition (CVP) = Relative Benefits (RB) / Relative Price (RP)

• The investment / construction cycle. • Comparing airline & airport assets.

• Service delivery & value for money.

• Last 15 years invested over $300M

• 2012 – 2017 increase is 70c per passenger / p.a

Wellington’s catchment market Large, highly mobile, and affluent

• Highest GDP per capita in New Zealand

• New Zealand’s highest wages $1,700 per week

• Lower costs of living resulting in more disposable income for travel

• House prices 25% cheaper than AKL

• 1000 people fly long haul out of WLG per day.

Over 1 million people within the catchment of Wellington Airport

Passenger story – present & future

Competition stimulates growth

The passenger story

• Last two years competition on AKL, CHC, and ZQN -Jetstar has added new growth and stimulated the market.

• JQ’s capacity share has grown to around 20%.

• JQ’s 9th Jet added 500,000 seats to Wellington 10% 15% 20%

Planning for the future – Master Plan

9

“ Next Level”

“Build Growth Pla6orms”

þ þ Work in Progress þ Next Phase

2015 2021

• Main Terminal expansion

• Southern Pier extensions

• Additional retail

• New Fire Appliances

• Multi level car park

• Airport Hotel

• Technology

• Long haul flights

• Runway Extension?

• Terminal & Apron Expansion

• Taxiway separation

• Further retail & transport

• Commercial opportunities

Airports - Good investments but they are capital intensive

Foundation

2013

“Today’s Pla6orm” • Great utilisaton of Terminal &

Aprons

• Experiencing capacity constraints

• Trans-Tasman Airline Duopoly

• Opportunities with land holdings

5.4 Million Passengers

6 Million Passengers

8 Million Passengers

New car park precinct & layout

10 Car park utilisation 80% to 105%

• Currently 2,500 Car parks • Addi5onal 300 car parks • 720,000 car park users p.a • 1:3 outbound passengers park a car • 13% book online • 50% of premium book online

At ground parking versus multi-level

11 Business case still being progressed

• Limited ground space available • Open air parking • Distance from terminal • Lower investment than multi-level

Car parking at ground

• Best utilisation of limited land resource • High build cost ~$40,000 per car park • Got to go down to go up, extensive disruption • Gives a covered product close to the terminal

Multi-level car parking

• 120 beds 4 star • Ties with Trans-Tasman schedule • Convenience • 5.5M passengers – inbound/outbound

Hotel – feasibility study

Property and Retail

• >$10M revenue per annum excluding Duty Free / Forex

• 16 food and beverage outlets and one underway

• Recent developments last 12 months – Witchery, Antipodes, Subway, Burger King, Z

• Full retail park with 19,000 m2 of across 13 tenancies

• Further expansion potential on available commercial land – beachfront café/bar coming soon, additional retail consented and ready to go

Diversified commercial, property and retail revenue at city rates

Expanding the Southern Terminal

The Commerce Commission Review

What they say.... § ... Given us three out of four ticks § The one cross is their claim of ‘forecast excess profits’

What we say... § We disagree on two fundamental aspects ... WACC & land valuation.

15

Ø The Commission’s high level findings:

ü Transparent

ü Innovating appropriately

ü Providing quality services

ü Improved and efficient price structure

o Too early to tell if investment is appropriate

o Too early to tell if efficiencies are being achieved and shared with customers and evidence is mixed

X Information disclosure has not been effective in limiting WIAL’s ability to extract excessive profits

Ø However, the report:

ü Our actual past earnings - the airport was not found to have earned excessive profits

X But on a series of forecast variable and adjusted starting and ending values, profits are deemed to be excessive!

Commission’s s56G Report – key findings

16 Lots of “Ticks” - but ComCom conclude Information Disclosure’s not working!

Commission’s s56G Report – actual & forecast return on MVAU Assets

17 WIAL forecast to earn 8.1% MVEU or 8.9% MVAU (6.57% cash returns) over the pricing period

Actual Forecast

Com Com 75h percentile

WACC 8.04%

18

$456M

$504M

MVAU

MVAU

8.9% MVAU to MVAU

BARNZ Valuation

15.2% IRR BARNZ MVAU to WIAL MVEU (includes terminal value)

12.3% IRR WIAL MVAU to MVEU (includes terminal value)

Commission’s returns are exaggerated based off adjusted WIAL forecasts, amended land valuations and assumptions on future behaviour beyond year 5.

Commission’s s56G Report – Forecast returns

Where we place Australian Productivity Commission Dec 2011

19

WLG AKL CHC

Sydney Adelaide Perth

Pricing is low compared to airports worldwide

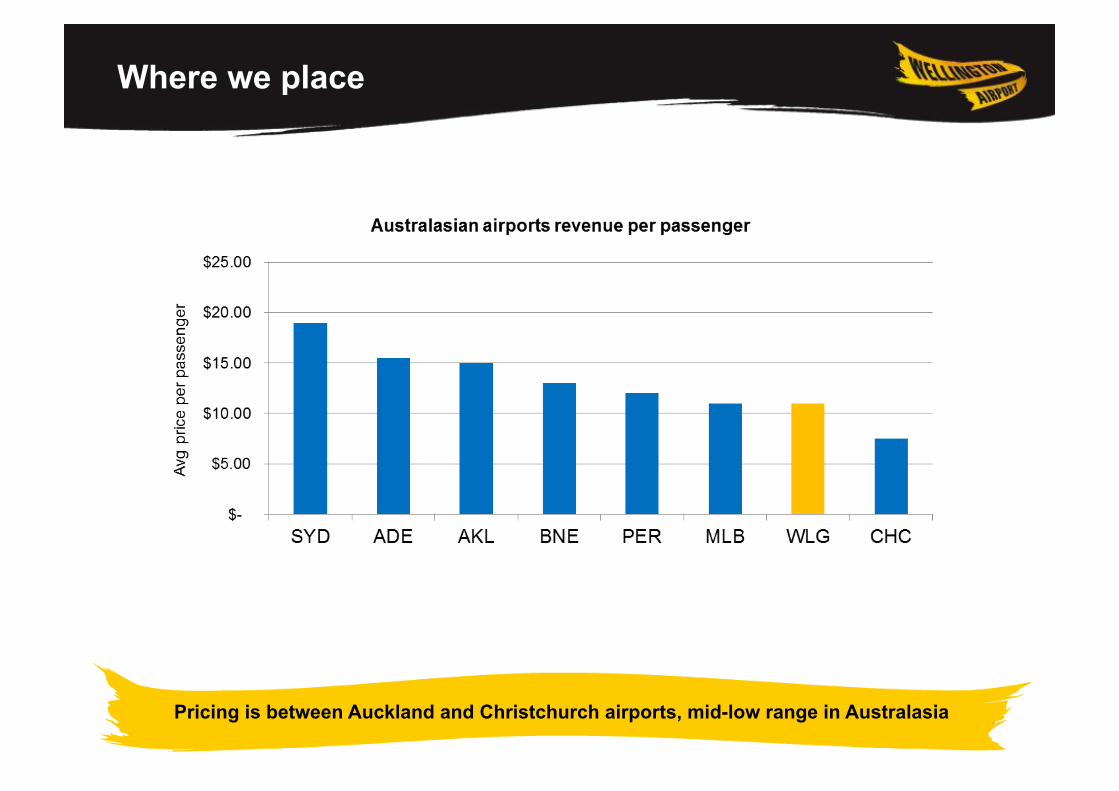

Where we place

20 Pricing is between Auckland and Christchurch airports, mid-low range in Australasia

Where to from here?

21

Now…

• Commerce Commission has completed its review of Wellington Airport

• The 56G report is now with the Ministers (Commerce & Transport)

What Next…

• Com Com have commenced their review of Auckland Airport this will be followed by Christchurch Airport

• WACC and Land Valuation is before the High Court

• Ministers will wait for the 56G reports and High Court decision

Summary

The Customer Value Proposition 22

23

Any questions?