45

The Italian Asset Management market key figures 16 February 2016 Research Department

The Italian Asset Management marketkey figures

16 February 2016

Research Department

Key figures16 February 2016

The Italian Asset Management market

Research Department

1. The Italian Asset Management market Summary statistics

Open-end funds

Mandates

The recovery, some tentative explanations

2. The European Investment Fund Industry Net assets & sales by fund / fund group domicile

3. Savings & Wealth Household saving rate: trend & int’l comparison

Household financial portfolio & private pension plans

Key figures16 February 2016

The Italian Asset Management market

Research Department

1. The Italian Asset Management market Summary statistics

Open-end funds

Mandates

The recovery, some tentative explanations

2. The European Investment Fund Industry Net assets & sales by fund / fund group domicile

3. Savings & Wealth Household saving rate: trend & int’l comparison

Household financial portfolio & private pension plans

Research Department The Italian Asset Management market Key figures

16 February 2016

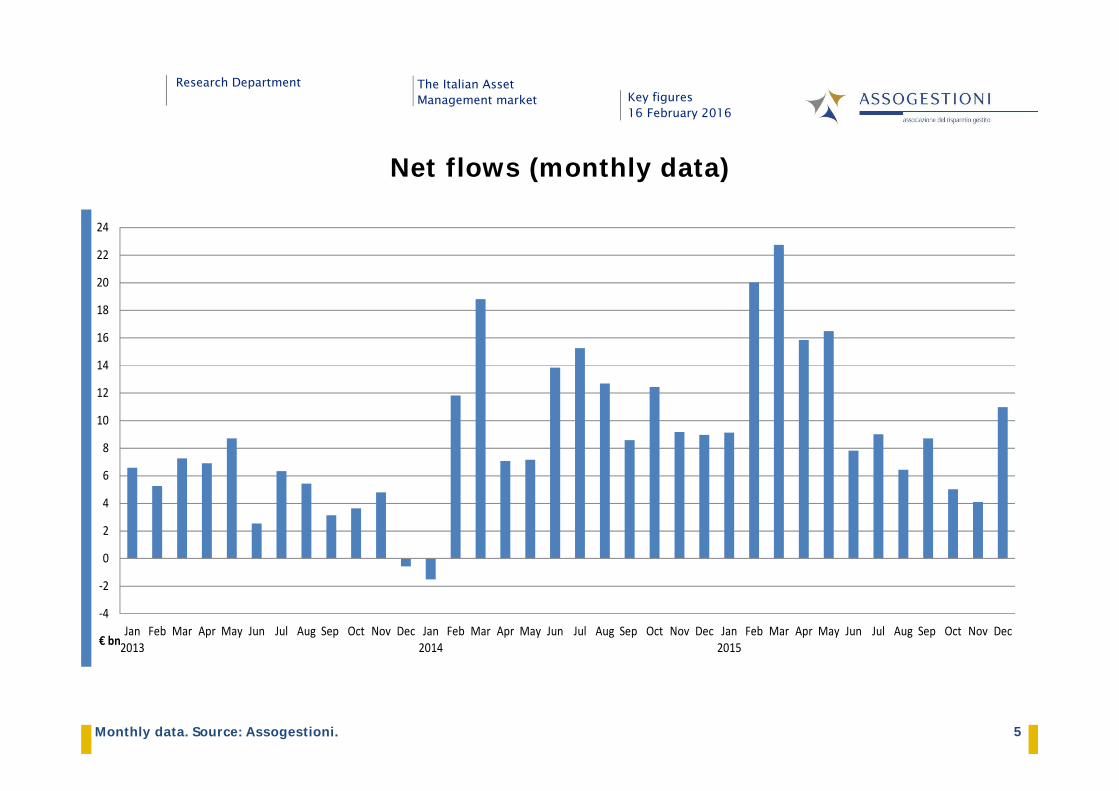

4AuM, net flows & performance, €bn. 4

The Italian AM market (Jan 2015: Dec 2015)

Research Department The Italian Asset Management market Key figures

16 February 2016

5

‐4

‐2

0

2

4

6

8

10

12

14

16

18

20

22

24

Jan2013

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2014

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2015

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec€ bn

Net flows (monthly data)

Monthly data. Source: Assogestioni.

Research Department The Italian Asset Management market Key figures

16 February 2016

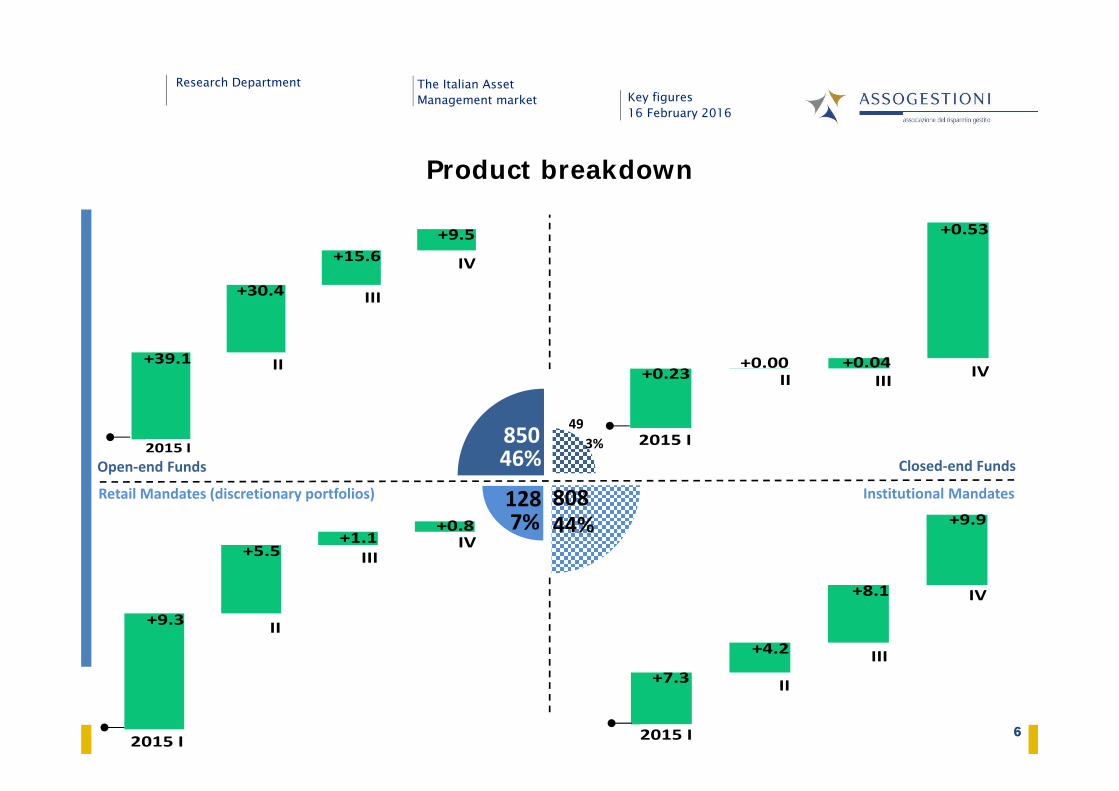

6

+7.3

+4.2

+8.1

+9.9

III

2015 I

II

IV+9.3

+5.5+1.1

+0.8IV

II

2015 I

III

+0.23+0.00 +0.04

+0.53

II III IV

2015 I

+39.1

+30.4

+15.6+9.5

2015 I

IV

II

III

7%128

Product breakdown

6

4%

43

44%808

Open‐end Funds

Retail Mandates (discretionary portfolios)

Closed‐end Funds

Institutional Mandates

85046%

3%49

Research Department The Italian Asset Management market Key figures

16 February 2016

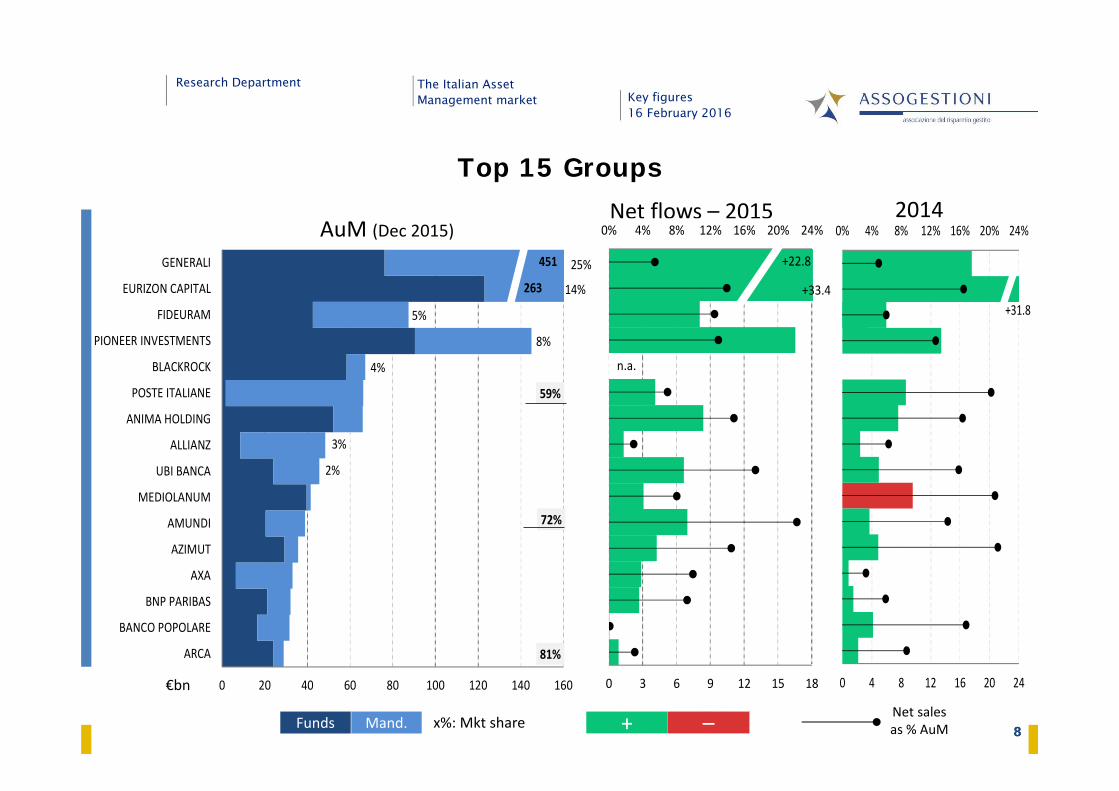

7€bn, yearly data. Source: Assogestioni.

Long term trend

Research Department The Italian Asset Management market Key figures

16 February 2016

8

+31.8

0% 4% 8% 12% 16% 20% 24%

0 4 8 12 16 20 24

81%

72%

59%

14%263

25%

3%

2%

451

4%

8%

5%

0 20 40 60 80 100 120 140 160

ARCA

BANCO POPOLARE

BNP PARIBAS

AXA

AZIMUT

AMUNDI

MEDIOLANUM

UBI BANCA

ALLIANZ

ANIMA HOLDING

POSTE ITALIANE

BLACKROCK

PIONEER INVESTMENTS

FIDEURAM

EURIZON CAPITAL

GENERALI

Net sales as % AuMFunds

€bn

AuM (Dec 2015)Net flows – 2015 2014

Mand. + –x%: Mkt share 8

Top 15 Groups

n.a.

+33.4

+22.8

0% 4% 8% 12% 16% 20% 24%

0 3 6 9 12 15 18

Research Department The Italian Asset Management market Key figures

16 February 2016

9

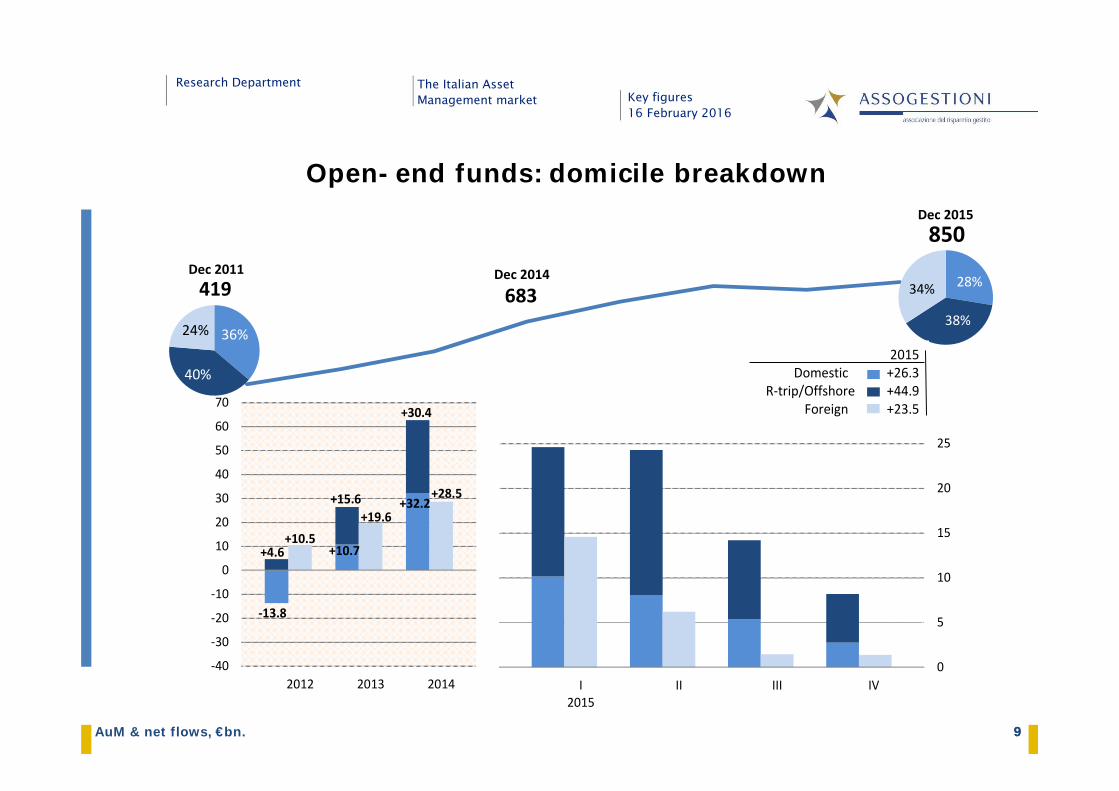

Open-end funds: domicile breakdown

AuM & net flows, €bn. 9

Dec 2015850

Dec 2011419

Dec 2014

683

36%

40%

24%

28%

38%

34%

2015 Domestic +26.3

R‐trip/Offshore +44.9Foreign +23.5

0

5

10

15

20

25

I2015

II III IV

‐13.8

+10.7

+32.2

+4.6

+15.6

+30.4

+10.5+19.6

+28.5

‐40

‐30

‐20

‐10

0

10

20

30

40

50

60

70

2012 2013 2014

Research Department The Italian Asset Management market Key figures

16 February 2016

10

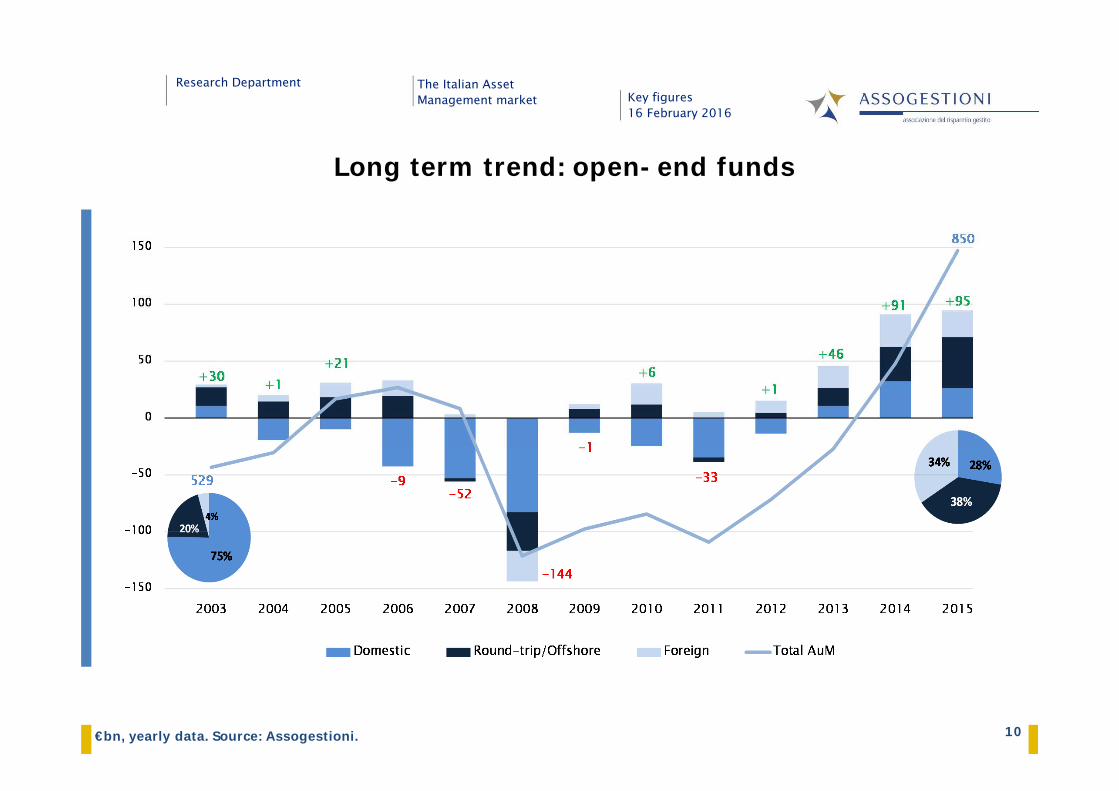

Long term trend: open-end funds

€bn, yearly data. Source: Assogestioni.

Research Department The Italian Asset Management market Key figures

16 February 2016

11

+61%

+55%

0% 10% 20% 30% 40%

0 4 8 12 16

n.a.

+20.2

0% 8% 16% 24% 32% 40%

0 3 6 9 12 15

80%

68%

6%

8%

11%

5%

14%

2%

5%

3%

51%

7%

0 10 20 30 40 50 60 70 80 90 100 110 120 130

PICTET

DEUTSCHE AWM

AMUNDI

INVESCO

FRANKLIN TEMPLETON

JPMORGAN AM

UBI BANCA

ARCA

AZIMUT

MEDIOLANUM

ANIMA HOLDING

BLACKROCK

GENERALI

PIONEER INVESTMENTS

FIDEURAM

EURIZON CAPITAL

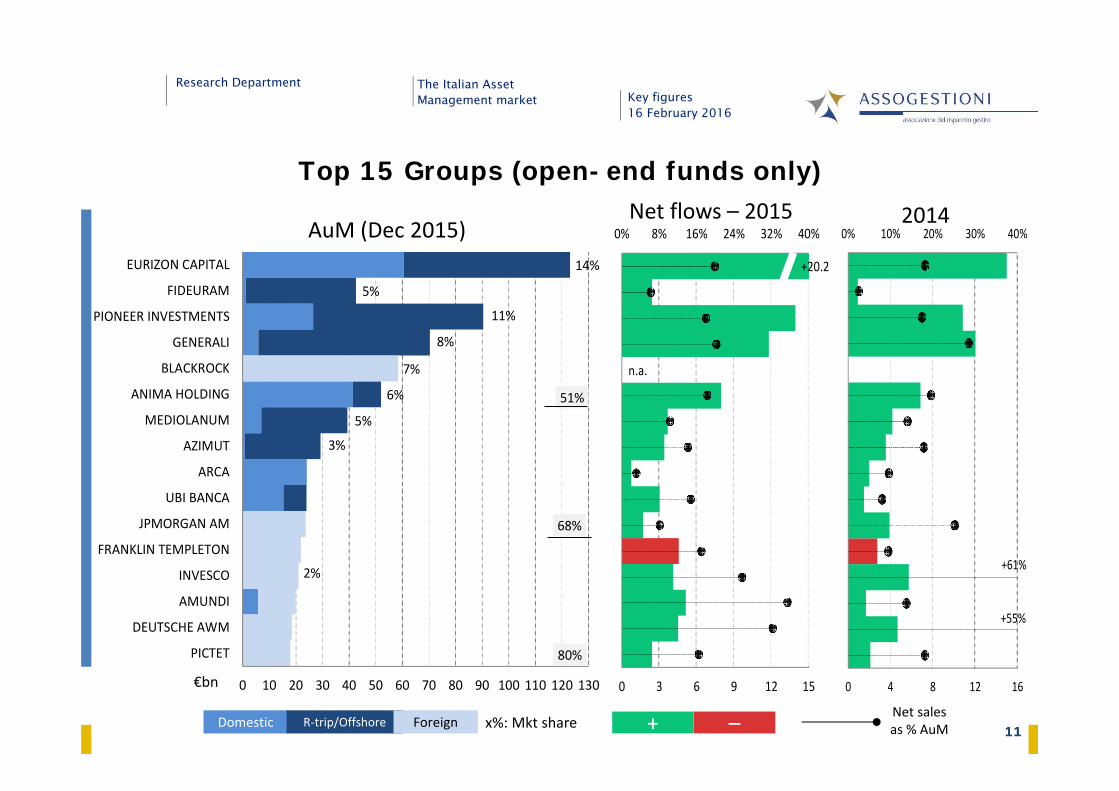

Top 15 Groups (open-end funds only)

11Net sales as % AuMDomestic

€bn

AuM (Dec 2015)Net flows – 2015 2014

R‐trip/Offshore + –x%: Mkt shareForeign

Research Department The Italian Asset Management market Key figures

16 February 2016

12

36%

20%

9%

22% 8%

8%

6%

3%

4%

40%

40%

39%

40%

10%

27%

41%

25%

0% 20% 40% 60% 80% 100%

FOREIGN

R‐TRIP/OFFSHORE

DOMESTIC

TOTAL

Equity Balanced Money Market Bond Flexible Hedge

Asset Class breakdown

12December 2015.

235 bn – 29%

290 bn – 36%

280 bn – 35%

Research Department The Italian Asset Management market Key figures

16 February 2016

13

+12.9

0% 8% 16% 24% 32% 40%

0 2 4 6 8

4%

9%

22%

5%

7%

6%

14%

23%

5%

5%

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70

BALANCED

OTHER

SPECIAL. SECTOR

GLOBAL

SPECIAL. COUNTRY

EMERGING MKTS

PACIFIC AREA

AMERICA

EUROPE

EURO AREA

ITALY

+11.4

0% 10% 20% 30% 40% 50%

0 1 2 3 4 5

Equity & balanced funds

Net sales as % AuMDomestic

€bn

AuM (Dec 2015)Net flows – 2015 2014

R‐trip/Offshore + –x%: Mkt shareForeign 13

Research Department The Italian Asset Management market Key figures

16 February 2016

14

+34%

+23%

+51.6

0% 4% 8% 12% 16% 20%

0 2 4 6 8

1%

202

20%

20%

14%

6%

7%

3%

10%

12%

8%

0 20 40 60 80 100 120 140 160 180

HEDGE

FLEX

FLEX (BOND)

SPECIALIZED

MIXED

EM

GLOBAL

DOLLAR AREA

EURO CORPORATE / HY

EURO GOV. M/L TERM

EURO GOV. SHORT T.

ITALY

MM FUNDS

Net sales as % AuMDomestic

€bn

AuM (Dec 2015)Net flows – 2015 2014

R‐trip/Offshore + –x%: Mkt shareForeign 14

Money mkt, Bond, Flex & Hedge funds

+42.5

0% 12% 24% 36% 48% 60%

0 2 4 6 8 10

Research Department The Italian Asset Management market Key figures

16 February 2016

15

20%

30%

40%

50%

0

20

40

60

80

100

120

140

-20

-10

0

10

20

30

40

Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4

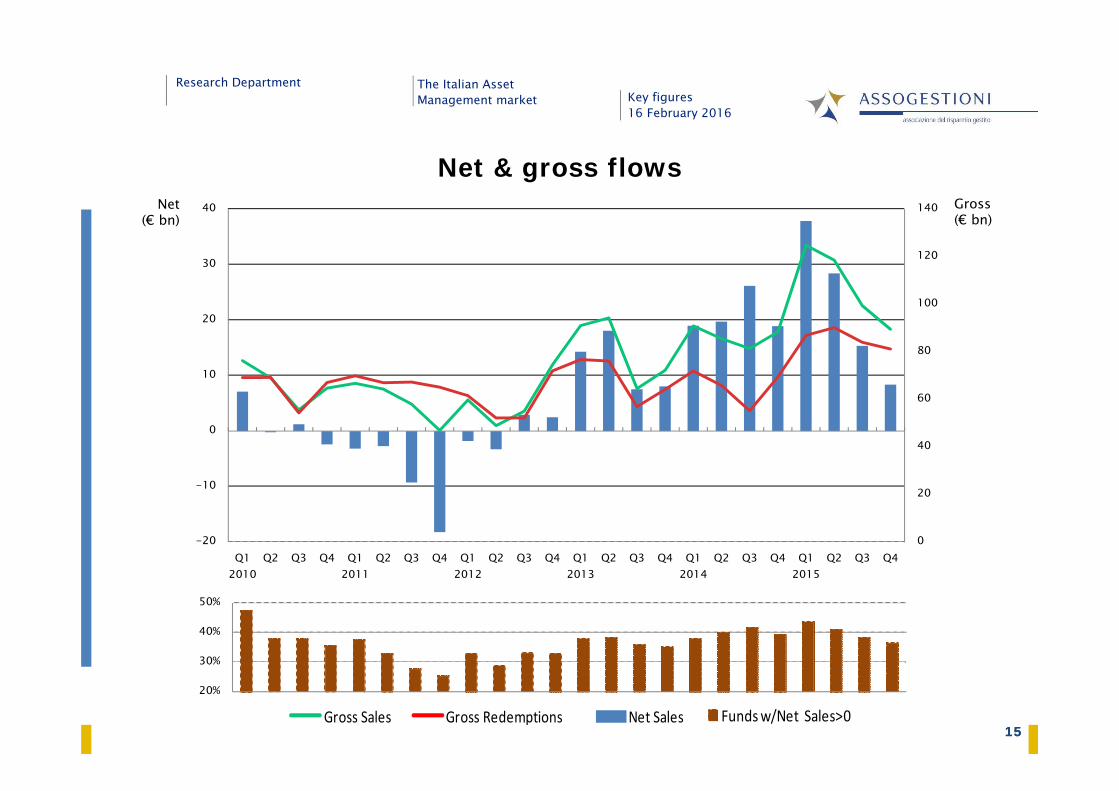

Net & gross flowsNet

(€ bn)Gross(€ bn)

15Gross Sales Gross Redemptions Net Sales Funds w/Net Sales>0

Research Department The Italian Asset Management market Key figures

16 February 2016

16

‐40

‐30

‐20

‐10

0

10

20

30

40

50

60

70

Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4

The blockbuster effect : top quartile funds take all

16Net flows, €bn. I II III IV Top 1% New Stories

Research Department The Italian Asset Management market Key figures

16 February 2016

17

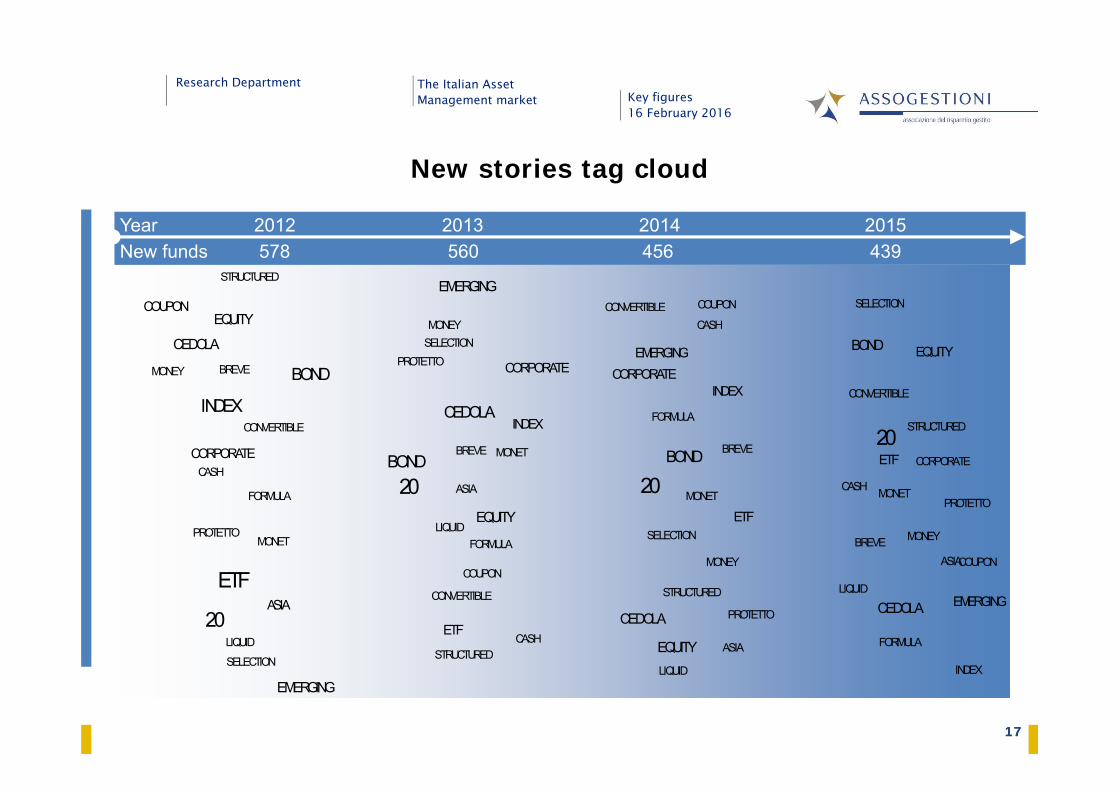

New stories tag cloud

2012 2013 2014 2015New funds 578Year

560 456 439

17

CEDOLA

COUPON

20

INDEX

CORPORATE

EMERGING

ASIAETF

STRUCTURED

FORMULA

SELECTION

CONVERTIBLE

PROTETTOMONET

MONEY

LIQUID

CASH

BREVE BOND

EQUITY

CEDOLA

COUPON

20

INDEX

CORPORATE

EMERGING

ASIA

ETF

STRUCTURED

FORMULA

SELECTION

CONVERTIBLE

PROTETTO

MONET

MONEY

LIQUID

CASH

BREVEBOND

EQUITY

CEDOLA

COUPON

20

INDEXCORPORATE

EMERGING

ASIA

ETF

STRUCTURED

FORMULA

SELECTION

CONVERTIBLE

PROTETTO

MONET

MONEY

LIQUID

CASH

BREVEBOND

EQUITY

CEDOLA

COUPON

20

INDEX

CORPORATE

EMERGING

ASIA

ETF

STRUCTURED

FORMULA

SELECTION

CONVERTIBLE

PROTETTOMONET

MONEY

LIQUID

CASH

BREVE

BOND EQUITY

Research Department The Italian Asset Management market Key figures

16 February 2016

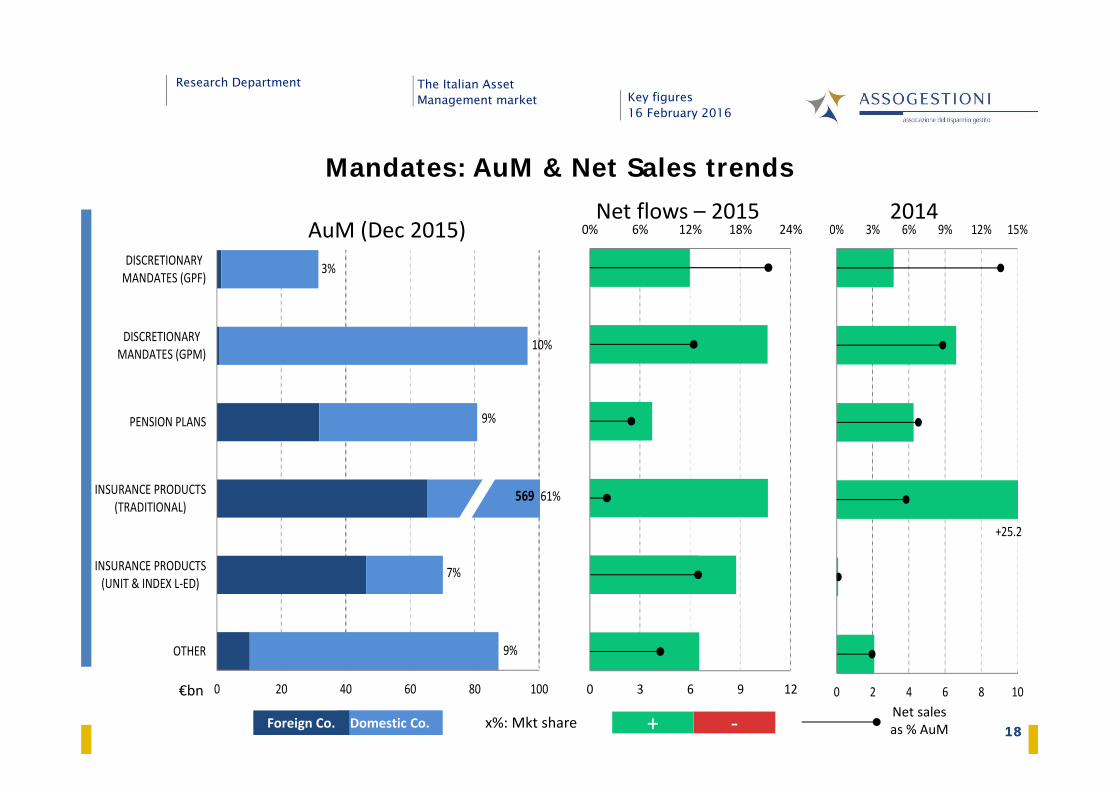

18

0% 6% 12% 18% 24%

0 3 6 9 12

9%

7%

61%

9%

10%

3%

569

0 20 40 60 80 100

OTHER

INSURANCE PRODUCTS(UNIT & INDEX L‐ED)

INSURANCE PRODUCTS(TRADITIONAL)

PENSION PLANS

DISCRETIONARYMANDATES (GPM)

DISCRETIONARYMANDATES (GPF)

+25.2

0% 3% 6% 9% 12% 15%

0 2 4 6 8 10

18Net sales as % AuM

€bn

AuM (Dec 2015)Net flows – 2015 2014

+ ‐x%: Mkt shareDomestic Co.Foreign Co.

Mandates: AuM & Net Sales trends

Research Department The Italian Asset Management market Key figures

16 February 2016

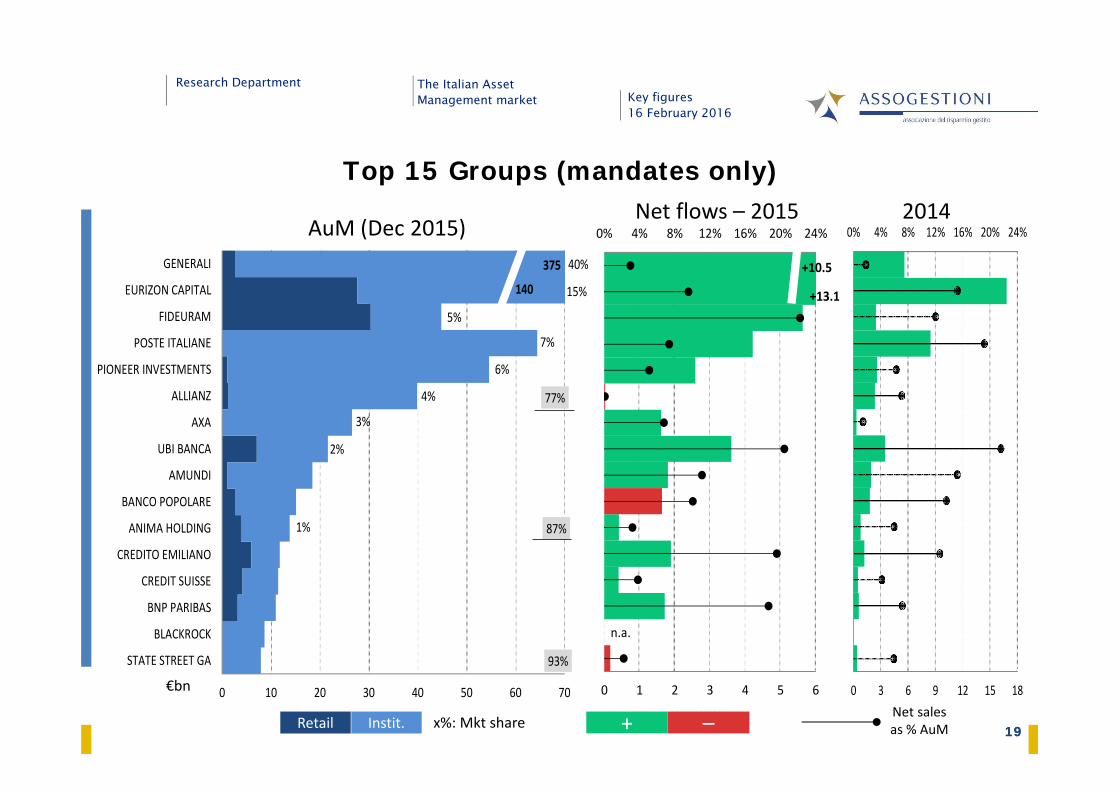

19

n.a.

+13.1

+10.5

0% 4% 8% 12% 16% 20% 24%

0 1 2 3 4 5 6

140

40%

93%

7%

1%

6%

87%

375

2%

3%

77%4%

15%

5%

0 10 20 30 40 50 60 70

STATE STREET GA

BLACKROCK

BNP PARIBAS

CREDIT SUISSE

CREDITO EMILIANO

ANIMA HOLDING

BANCO POPOLARE

AMUNDI

UBI BANCA

AXA

ALLIANZ

PIONEER INVESTMENTS

POSTE ITALIANE

FIDEURAM

EURIZON CAPITAL

GENERALI

0% 4% 8% 12% 16% 20% 24%

0 3 6 9 12 15 18

Top 15 Groups (mandates only)

19Net sales as % AuMRetail

€bn

AuM (Dec 2015)Net flows – 2015 2014

Instit. + –x%: Mkt share

Research Department The Italian Asset Management market Key figures

16 February 2016

20

41%

80%

The market for Institutional Mandates

Household portfolio: share of insurance products & pension funds (2015Q3)IT FRA GER UK USA

20.1% 34.3% 31.2% 59.6% 32.7%

Managedby ManCos

As is ...(2015 Q3)

... and as could become:

Pension funds

201

Insurance products

557

Source: ANIA, Covip, Adepp, Assogestioni, Eurostat, OECD.

As is ...(2015 Q3)

Key figures16 February 2016

The Italian Asset Management market

Research Department

1. The Italian Asset Management market Summary statistics

Open-end funds

Mandates

The recovery, some tentative explanations

2. The European Investment Fund Industry Net assets & sales by fund / fund group domicile

3. Savings & Wealth Household saving rate: trend & int’l comparison

Household financial portfolio & private pension plans

Research Department The Italian Asset Management market Key figures

16 February 2016

22

A pro-cyclical market

€bn, yearly data. Source: Assogestioni, MSCI.

MSCI WORLD (Loc)

Research Department The Italian Asset Management market Key figures

16 February 2016

23

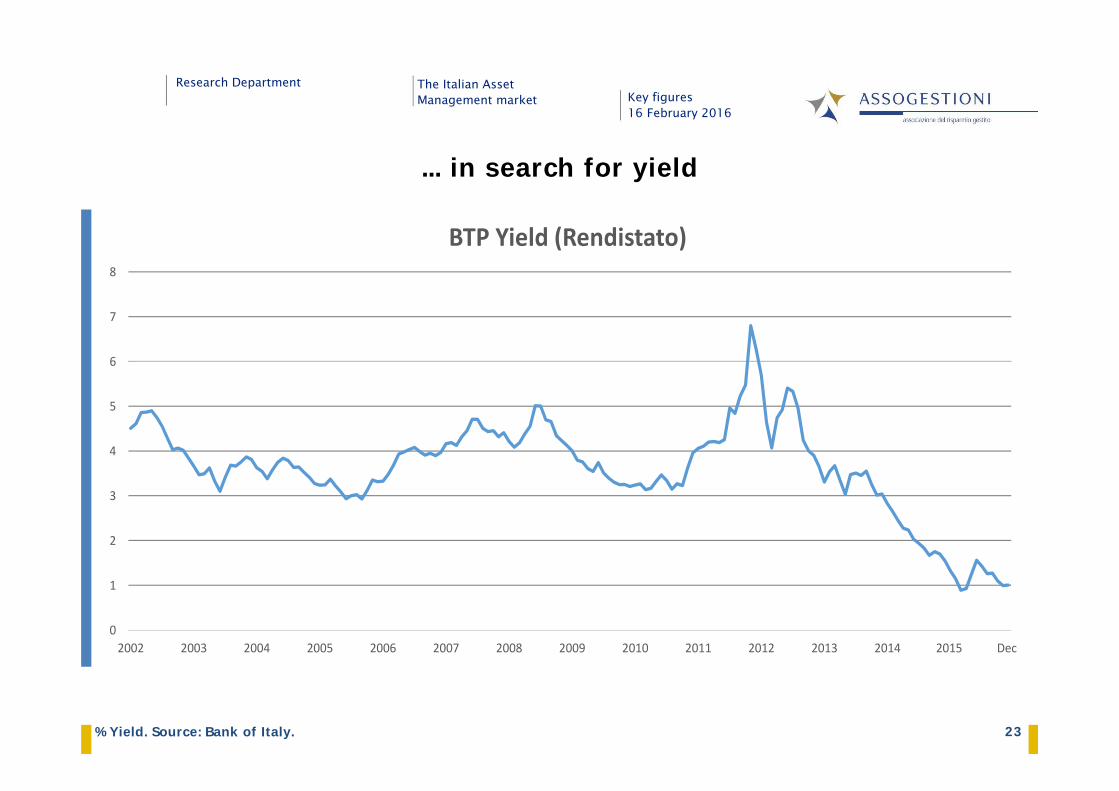

... in search for yield

% Yield. Source: Bank of Italy.

0

1

2

3

4

5

6

7

8

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Dec

BTP Yield (Rendistato)

Research Department The Italian Asset Management market Key figures

16 February 2016

24

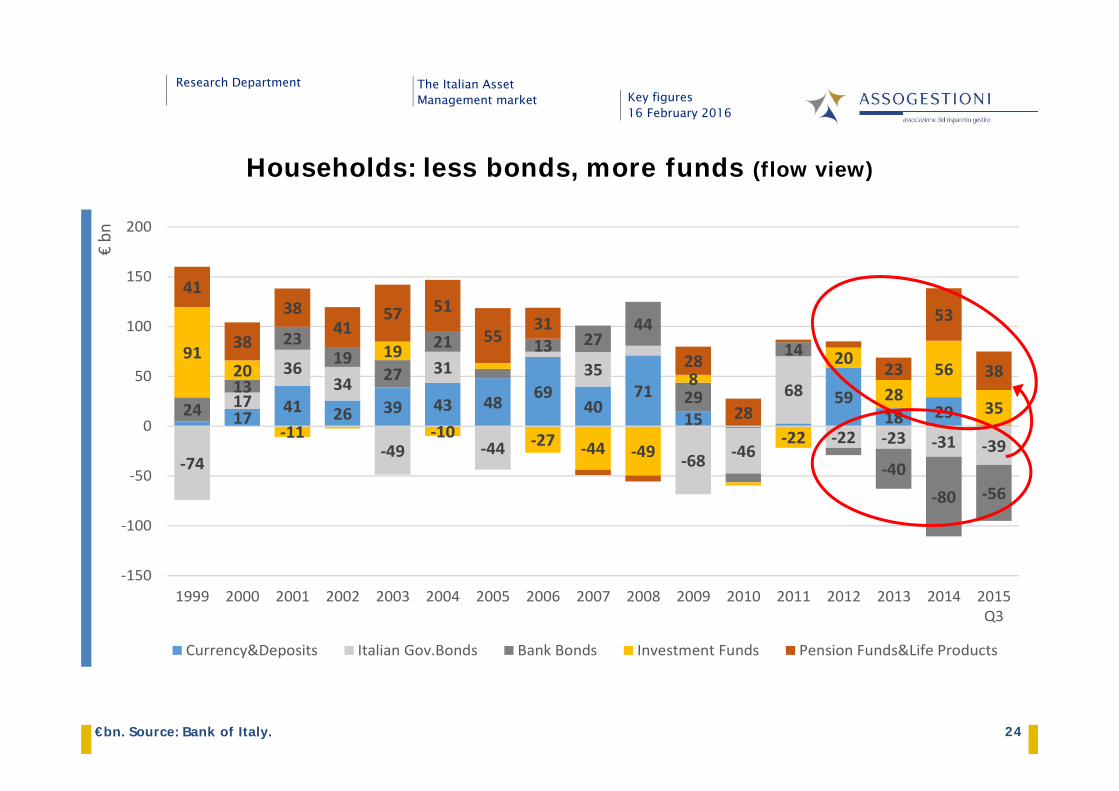

1741 26 39 43 48 69

4071

1559

18 29

‐74

17

3634

‐49

31

‐44

35

‐68 ‐46

68

‐22 ‐23 ‐31 ‐39

2413

2319

27

21 13 2744

29

14

‐40‐80 ‐56

9120

‐11

19

‐10 ‐27 ‐44 ‐49

8

‐22

20

2856

35

41

38

3841

57 51

5531

28

28

23

53

38

‐150

‐100

‐50

0

50

100

150

200

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Q3

€bn

Currency&Deposits Italian Gov.Bonds Bank Bonds Investment Funds Pension Funds&Life Products

Households: less bonds, more funds (flow view)

€bn. Source: Bank of Italy.

Research Department The Italian Asset Management market Key figures

16 February 2016

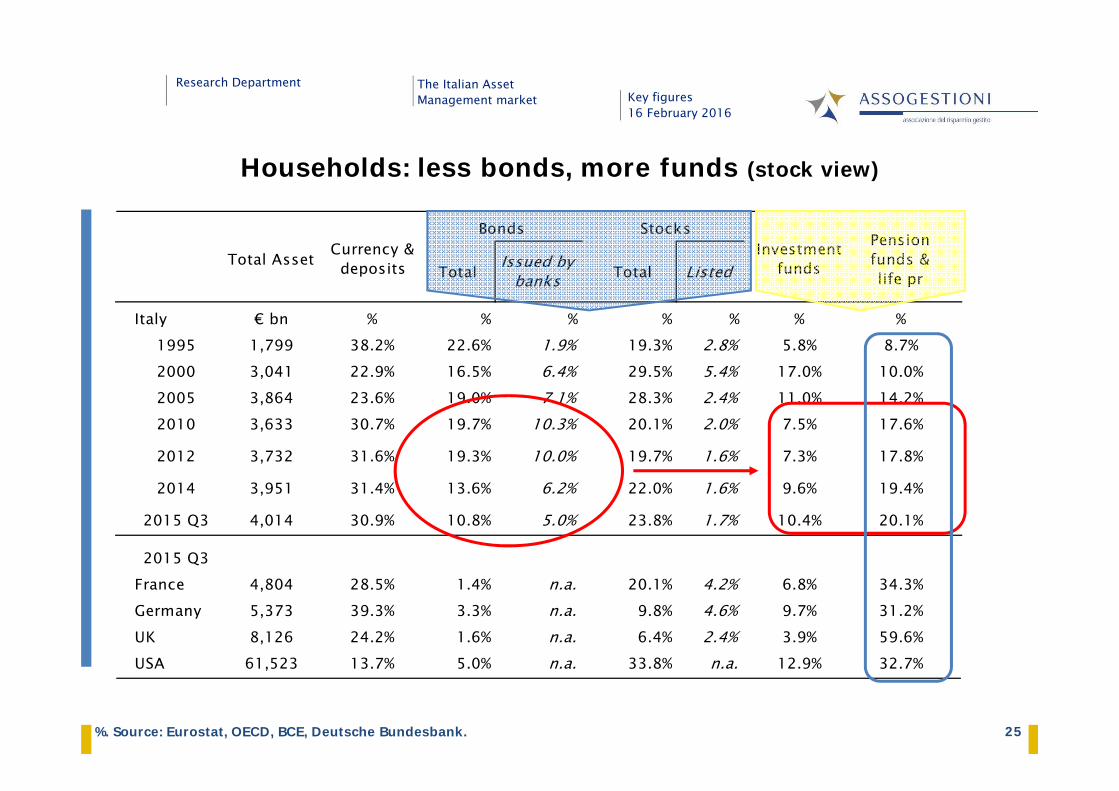

25

Total Issued by banks Total Listed

Italy € bn % % % % % % %1995 1,799 38.2% 22.6% 1.9% 19.3% 2.8% 5.8% 8.7%2000 3,041 22.9% 16.5% 6.4% 29.5% 5.4% 17.0% 10.0%2005 3,864 23.6% 19.0% 7.1% 28.3% 2.4% 11.0% 14.2%2010 3,633 30.7% 19.7% 10.3% 20.1% 2.0% 7.5% 17.6%

2012 3,732 31.6% 19.3% 10.0% 19.7% 1.6% 7.3% 17.8%

2014 3,951 31.4% 13.6% 6.2% 22.0% 1.6% 9.6% 19.4%

2015 Q3 4,014 30.9% 10.8% 5.0% 23.8% 1.7% 10.4% 20.1%

2015 Q3France 4,804 28.5% 1.4% n.a. 20.1% 4.2% 6.8% 34.3%Germany 5,373 39.3% 3.3% n.a. 9.8% 4.6% 9.7% 31.2%UK 8,126 24.2% 1.6% n.a. 6.4% 2.4% 3.9% 59.6%USA 61,523 13.7% 5.0% n.a. 33.8% n.a. 12.9% 32.7%

Total Asset Currency & deposits

Investment funds

Pension funds & life pr

Bonds Stocks

Households: less bonds, more funds (stock view)

%. Source: Eurostat, OECD, BCE, Deutsche Bundesbank.

Research Department The Italian Asset Management market Key figures

16 February 2016

26

0%

5%

10%

15%

20%

25%

0%

5%

10%

15%

20%

25%

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15Q3

EU avg Italy Germany France UK

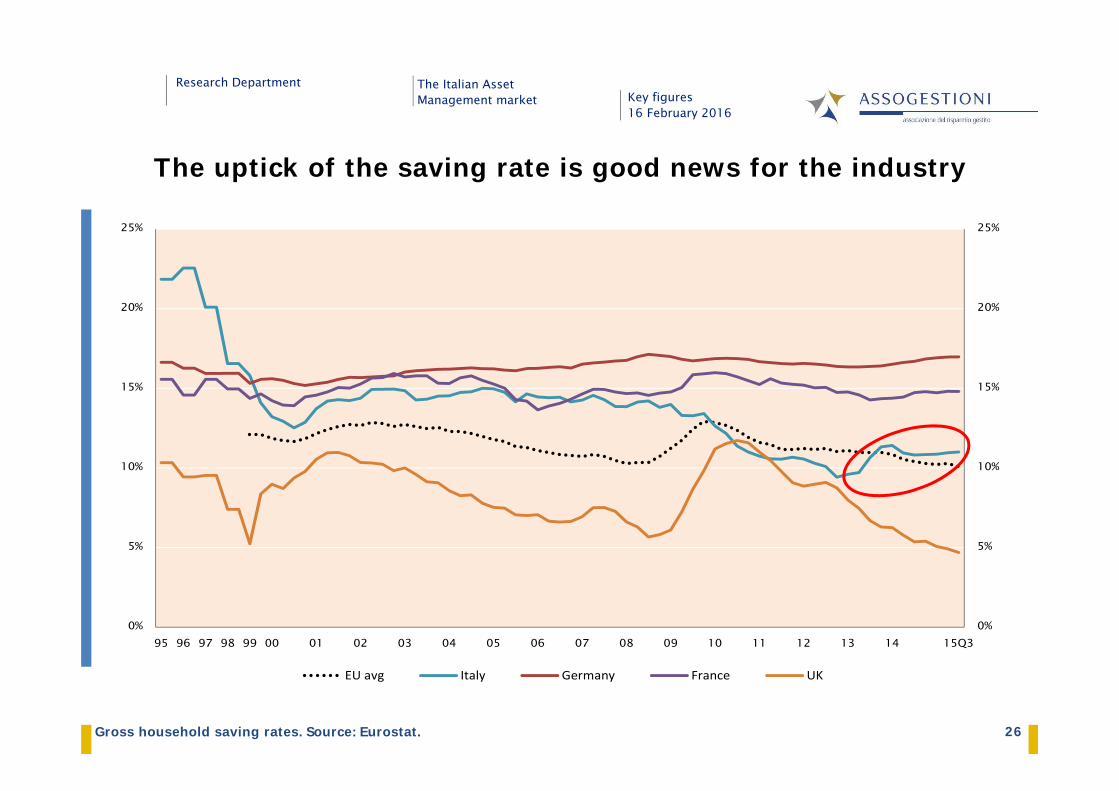

The uptick of the saving rate is good news for the industry

Gross household saving rates. Source: Eurostat.

Research Department The Italian Asset Management market Key figures

16 February 2016

27Quarterly flows, €bn. Source: Assogestioni, Bank of Italy.

Banks: no more dependent on funding from retail investors...

27

‐40

‐30

‐20

‐10

0

10

20

30

Q12007

Q2 Q3 Q4 Q12008

Q2 Q3 Q4 Q12009

Q2 Q3 Q4 Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3

Retail Bank Bonds Domestic and Round‐Trip Funds Foreign Funds

Research Department The Italian Asset Management market Key figures

16 February 2016

28€bn. Source: Assogestioni, bank balance sheets (Top 5 groups). 28

... and urged to sustain profitability throughnon interest-based sources of revenues

6

6.5

7

7.5

8

8.5

9

9.5

10

‐15

‐10

‐5

0

5

10

15

20

25

Q12009

Q3 Q4 Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2 Q3 Q4

Fund flows, captive Man.Cos (l.) Net interest margin (r.)

Research Department The Italian Asset Management market Key figures

16 February 2016

29

+34%

+23%

+51.6

0% 4% 8% 12% 16% 20%

0 2 4 6 8

1%

202

20%

20%

14%

6%

7%

3%

10%

12%

8%

0 20 40 60 80 100 120 140 160 180

HEDGE

FLEX

FLEX (BOND)

SPECIALIZED

MIXED

EM

GLOBAL

DOLLAR AREA

EURO CORPORATE / HY

EURO GOV. M/L TERM

EURO GOV. SHORT T.

ITALY

MM FUNDS

+42.5

0% 12% 24% 36% 48% 60%

0 2 4 6 8 10

AuM (Dec 2015)Net flows – 2015 2014

Net sales as % AuMDomestic

€bn

R‐trip/Offshore + –x%: Mkt shareForeign 29

The success of funds with high margins (target-date funds)

Key figures16 February 2016

The Italian Asset Management market

Research Department

1. The Italian Asset Management market Summary statistics

Open-end funds

Mandates

The recovery, some tentative explanations

2. The European Investment Fund Industry Net assets & sales by fund / fund group domicile

3. Savings & Wealth Household saving rate: trend & int’l comparison

Household financial portfolio & private pension plans

Research Department The Italian Asset Management market Key figures

16 February 2016

31

1,672 1,657

1,403

465275

3,367

1,780

12,113

Germany14%

France14%

UK12%

Switzerland4%

Italy2%

Luxembourg28%

Ireland15%

Europe100%

Ucits

AIF

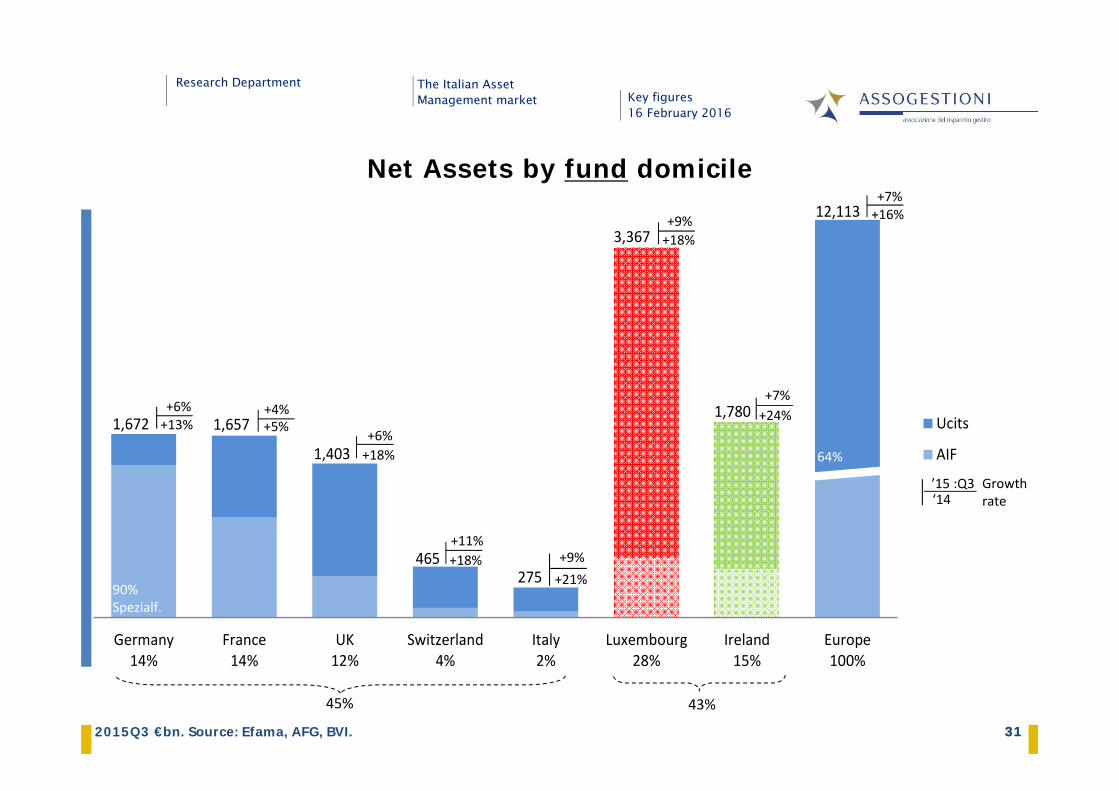

312015Q3 €bn. Source: Efama, AFG, BVI.

Net Assets by fund domicile

+24%+7%

+16%+7%

+18%+9%

+13%+6%

+5%+4%

+18%+6%

+18%+11%

+21%+9%

64%

Growth rate‘14

’15 :Q3

45% 43%

90% Spezialf.

Research Department The Italian Asset Management market Key figures

16 February 2016

32

Net sales by fund domicile

Net sales as a % of AuM. Yearly data in €bn. Source: Efama, BVI.

‐75

‐21

‐7%

+29

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

France

+87

+95

+106

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Germany

201020112012

+27 2013

+34 2014

+13 2015

IIIIIIIVI

IIIIIIV

IIIIII

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

UK

+194

+254

+9%

+261

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Luxembourg

+397

+599

+559

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Europe

201020112012

+11 2013

+34

+24

2014

‐14%

+5.4%2015

‐10%

IIIIIIIVIIIIIIIVIIIIII

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Italy

Research Department The Italian Asset Management market Key figures

16 February 2016

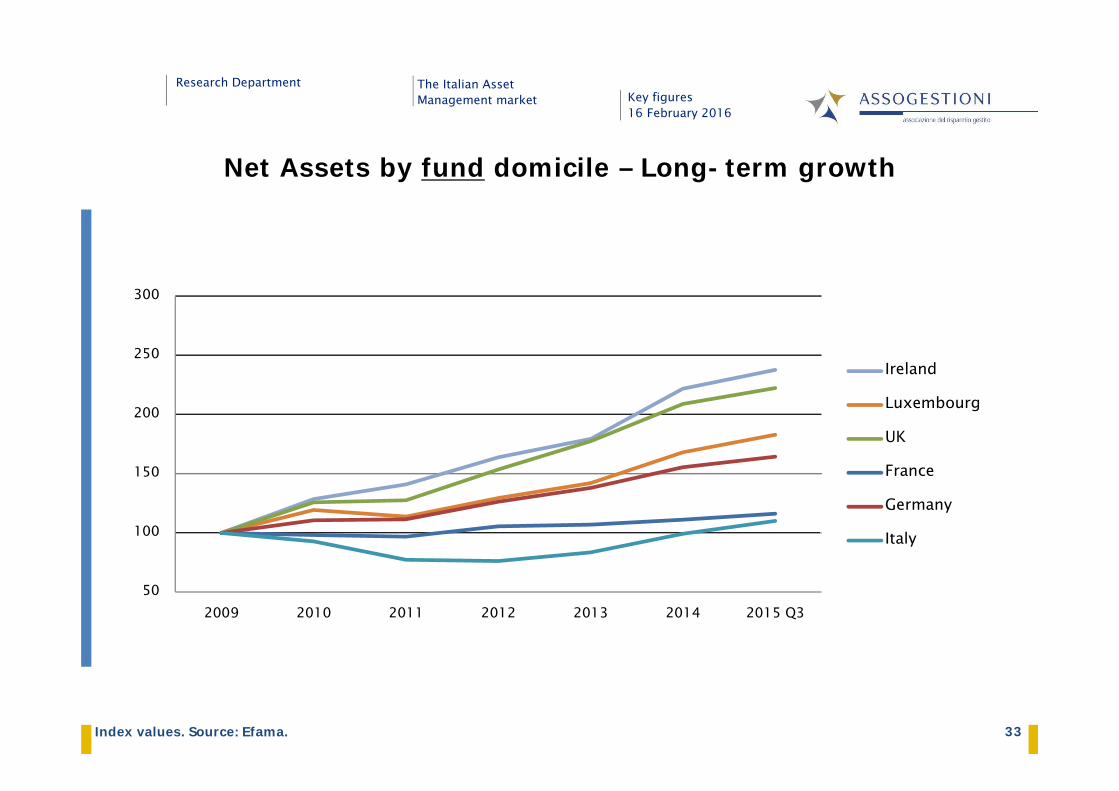

33Index values. Source: Efama.

Net Assets by fund domicile – Long-term growth

50

100

150

200

250

300

2009 2010 2011 2012 2013 2014 2015 Q3

Ireland

Luxembourg

UK

France

Germany

Italy

Research Department The Italian Asset Management market Key figures

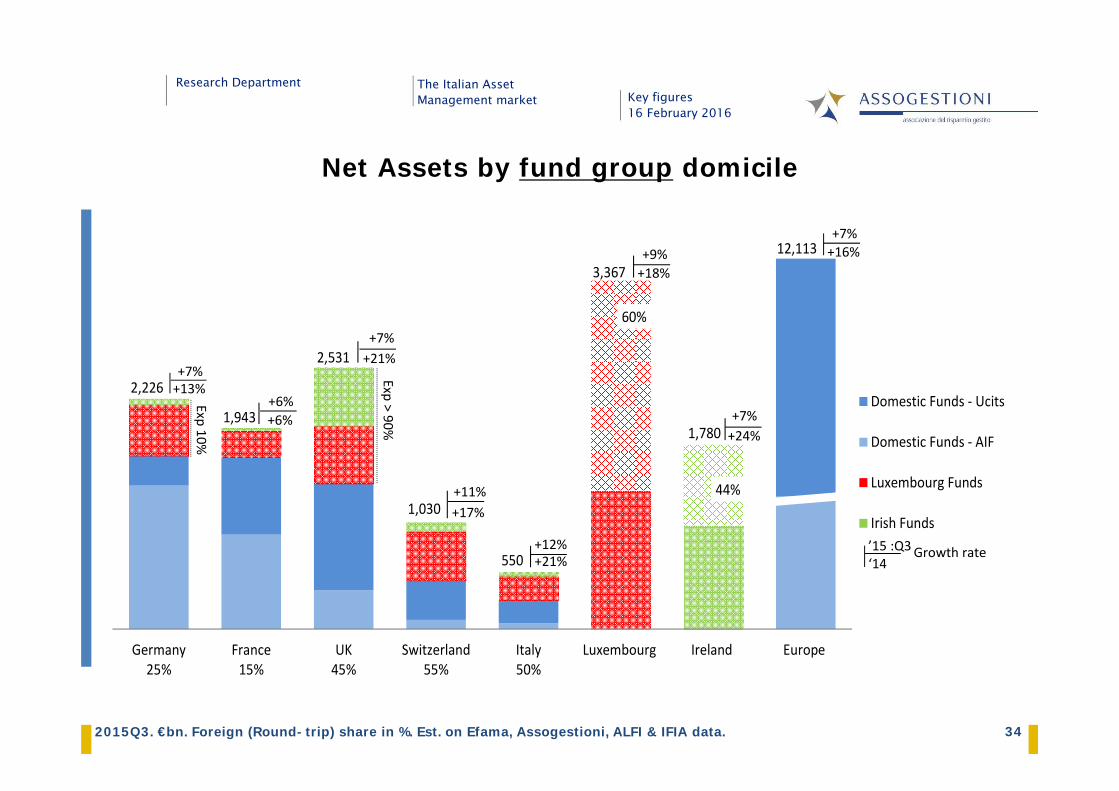

16 February 2016

34

60%

44%

3,367

1,780

12,113

1,030

2,226

1,943

2,531

550

Germany25%

France15%

UK45%

Switzerland55%

Italy50%

Luxembourg Ireland Europe

Domestic Funds ‐ Ucits

Domestic Funds ‐ AIF

Luxembourg Funds

Irish Funds

Net Assets by fund group domicile

2015Q3. €bn. Foreign (Round-trip) share in %. Est. on Efama, Assogestioni, ALFI & IFIA data.Exp > 90%

Exp 10%

+13%+7%

Growth rate‘14’15 :Q3

+21%+7%

+6%+6%

+17%+11%

+21%+12%

+24%+7%

+16%+7%

+18%+9%

Research Department The Italian Asset Management market Key figures

16 February 2016

35

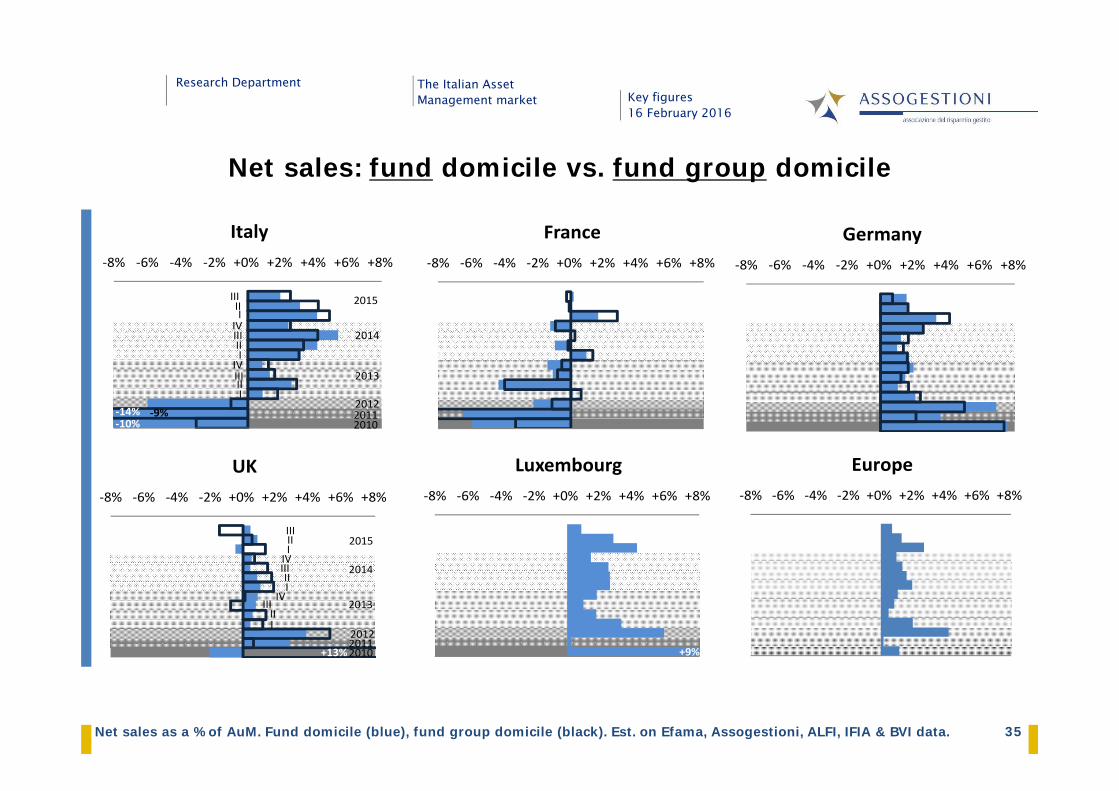

Net sales: fund domicile vs. fund group domicile

Net sales as a % of AuM. Fund domicile (blue), fund group domicile (black). Est. on Efama, Assogestioni, ALFI, IFIA & BVI data.

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Germany

201020112012

2013

2014

2015

III

IIIIVIIIIIIIVIIIIII

+13%

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

UK

+9%

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Luxembourg‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Europe

201020112012

2013

2014

‐9%

IIIIIIIVIIIIIIIVIIIIII

‐10%‐14%

2015

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

Italy

‐6%

‐8% ‐6% ‐4% ‐2% +0% +2% +4% +6% +8%

France

Key figures16 February 2016

The Italian Asset Management market

Research Department

1. The Italian Asset Management market Summary statistics

Open-end funds

Mandates

The recovery, some tentative explanations

2. The European Investment Fund Industry Net assets & sales by fund / fund group domicile

3. Savings & Wealth Household saving rate: trend & int’l comparison

Household financial portfolio & private pension plans

Research Department The Italian Asset Management market Key figures

16 February 2016

37

Household saving rates in Europe

Gross household saving rates. Source: Eurostat.

0%

5%

10%

15%

20%

25%

0%

5%

10%

15%

20%

25%

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15Q3

EU avg Italy Germany France UK

Research Department The Italian Asset Management market Key figures

16 February 2016

38

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0%

∆ c

onsu

mpt

ion

∆ income

How income & consumption Δ% affect saving rates

2008Q4:2015Q3. Source: Eurostat.

13.8%

Italy

11.0%

8%

10%

12%

14%

16%

2009

2010

2011

2012

2013

2014

2015

Q3

Research Department The Italian Asset Management market Key figures

16 February 2016

39

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

-1.0% -0.5% 0.0% 0.5% 1.0% 1.5%

∆ c

onsu

mpt

ion

∆ income

How income & consumption Δ% affect saving rates

2008Q4:2015Q3. Source: Eurostat.

17.1%

Germany 17.0%

10%

12%

14%

16%

18%

14.7%

France 14.8%

10%12%14%16%18%

2009

2010

2011

2012

2013

2014

2015

Q3

Research Department The Italian Asset Management market Key figures

16 February 2016

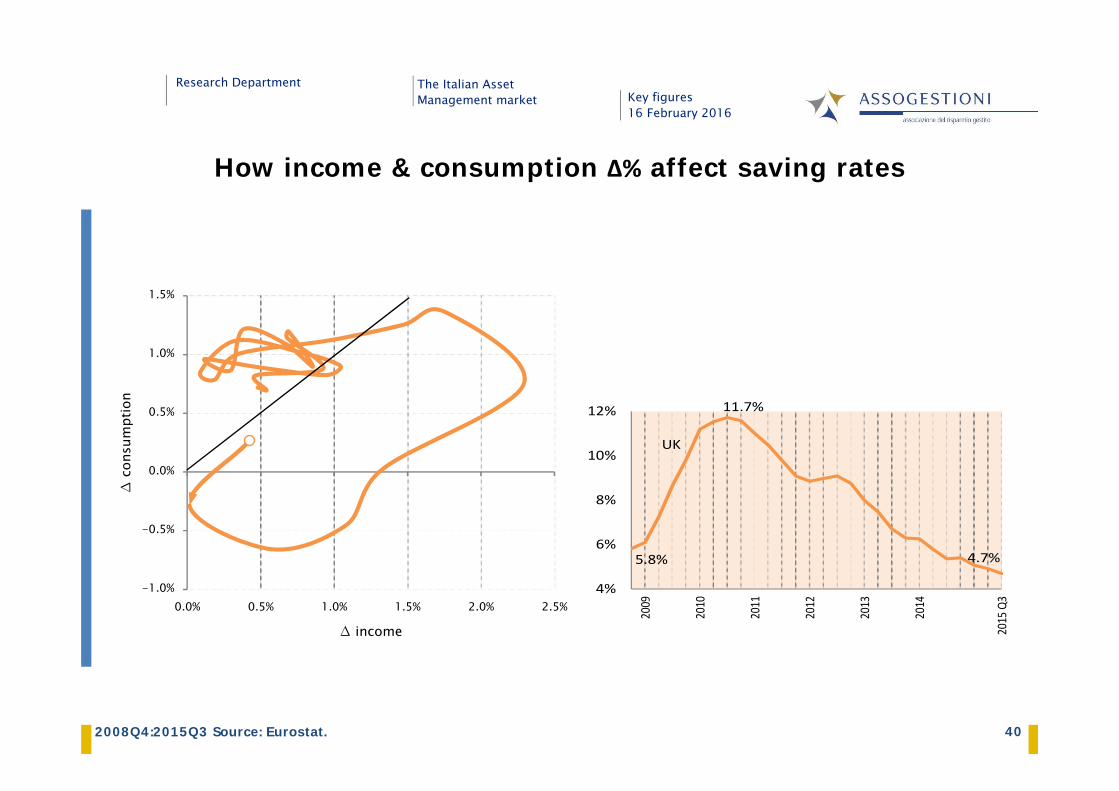

40

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

∆ c

onsu

mpt

ion

∆ income

How income & consumption Δ% affect saving rates

2008Q4:2015Q3 Source: Eurostat.

5.8%

UK

11.7%

4.7%

4%

6%

8%

10%

12%

2009

2010

2011

2012

2013

2014

2015

Q3

Research Department The Italian Asset Management market Key figures

16 February 2016

41

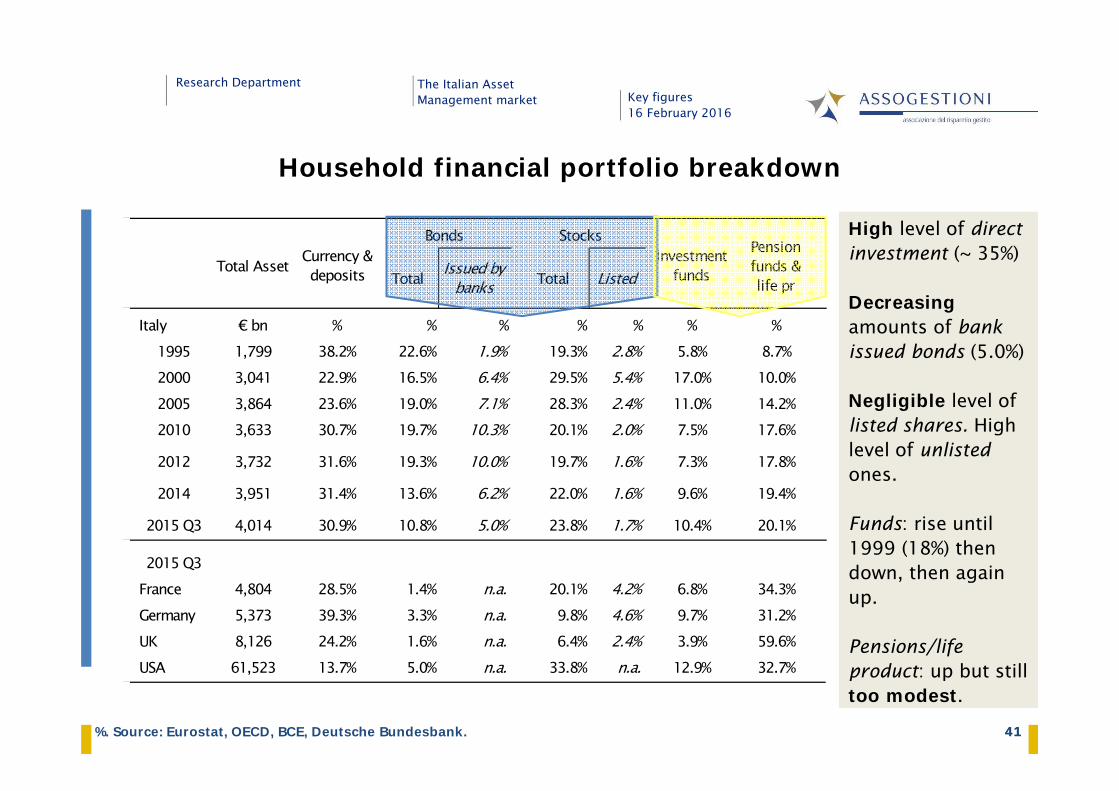

Total Issued by banks Total Listed

Italy € bn % % % % % % %1995 1,799 38.2% 22.6% 1.9% 19.3% 2.8% 5.8% 8.7%2000 3,041 22.9% 16.5% 6.4% 29.5% 5.4% 17.0% 10.0%2005 3,864 23.6% 19.0% 7.1% 28.3% 2.4% 11.0% 14.2%2010 3,633 30.7% 19.7% 10.3% 20.1% 2.0% 7.5% 17.6%

2012 3,732 31.6% 19.3% 10.0% 19.7% 1.6% 7.3% 17.8%

2014 3,951 31.4% 13.6% 6.2% 22.0% 1.6% 9.6% 19.4%

2015 Q3 4,014 30.9% 10.8% 5.0% 23.8% 1.7% 10.4% 20.1%

2015 Q3France 4,804 28.5% 1.4% n.a. 20.1% 4.2% 6.8% 34.3%Germany 5,373 39.3% 3.3% n.a. 9.8% 4.6% 9.7% 31.2%UK 8,126 24.2% 1.6% n.a. 6.4% 2.4% 3.9% 59.6%USA 61,523 13.7% 5.0% n.a. 33.8% n.a. 12.9% 32.7%

Total Asset Currency & deposits

Investment funds

Pension funds & life pr

Bonds Stocks

Household financial portfolio breakdown

High level of directinvestment (~ 35%)

Decreasingamounts of bankissued bonds (5.0%)

Negligible level oflisted shares. High level of unlistedones.

Funds: rise until1999 (18%) thendown, then againup.

Pensions/life product: up but stilltoo modest.

41%. Source: Eurostat, OECD, BCE, Deutsche Bundesbank.

Research Department The Italian Asset Management market Key figures

16 February 2016

42

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15Q3

0%

10%

20%

30%

40%

50%

60%

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15Q3

Managed products in household portfolios

too low?

Italy France Germany United Kingdom USA

Investment funds Pension funds & life products

abnormallyhigh?

42Source: Eurostat, OECD, BCE, Deutsche Bundesbank.

Research Department The Italian Asset Management market Key figures

16 February 2016

43

Public Pensions (1st pillar)

Cost (% GDP) Future substitution ratesOld-age pensions

Source: Ragioneria Generale dello Stato.

Today

1

23

4

ante L 243/2004 ante DL 78/2010

ante DL 98/2011 ante DL 201/2011

1 2

3 4 65

66

67

68

69

70

71

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

2010 2020 2030 2040 2050 2060

Age Private sector employee Self employed

Research Department The Italian Asset Management market Key figures

16 February 2016

44

2008

(,000)

Member breakdown 6,540 21%

Private sector employees 4,528 26%

Public sector employees 173 4%

Self‐employed 1,839 19%

(,000) % '14 ∆ % 6y ∆ % (€ m) % GDP

Vehicle breakdown 6,540 100% +6% +35% 130,941 8.5%

Contractual p.f. 1,944 30% ‐0% ‐5% 39,644

Open p.f. 1,056 16% +7% +24% 13,980

Ind. Insurance Plans (PIP) 2,913 44% +10% +112% 23,219

Ante 1993 p.f. ('pre‐existing') 650 10% ‐0% ‐4% 54,033

2014 Members Assets

13,523 33%

3,335 5%

5,517 33%

2014

Working pop. (est.)

Membership rate

Membership rate

22,375 29%

Private pension plans at a glance (2nd & 3rd pillar)

Source: Covip, Istat, RGS.

The Italian Asset Management marketkey figures

16 February 2016

Research Department