Page 1

© 2015 - Proprietary and Confidential Information of FINCAD

How FINCAD can help navigate Swap Strategies in the new

Regulatory Environment

Subbu Loganathan, Kramerica Consulting

Richard Weeks, Quantitative Analyst, FINCAD

Page 2

© 2015 - Proprietary and Confidential Information of FINCAD

Agenda • Introduction – How it all came to this

– Dodd Frank and EMIR Clearing and Margin – Good intentions, unintended impact

– Basel III Capital Rules and Credit Risk – Consequences for the buy side

– Increase in complexity post financial crisis • Hedging Interest Rate Risk in the new environment

– Using cleared Interest Rate Swaps – Collateralisation considerations – Margin considerations – LCH and CME – too big to fail?

• Managing Complexity using FINCAD F3 – Multiple curves – Risk Reprojection – Demo

• Q&A

2

Page 3

© 2015 - Proprietary and Confidential Information of FINCAD

How it all came to this

• The financial crisis of 2007/08 was in part due to the lack of transparency in the trading and processing of OTC derivatives It highlighted the need for data standards and management of counterparty risk for OTC instruments

“All standardized OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end-2012 at the latest. OTC derivative contracts should be reported to trade repositories. Non-centrally cleared contracts should be subject to higher capital requirements.” September 2009

3

Page 4

© 2015 - Proprietary and Confidential Information of FINCAD

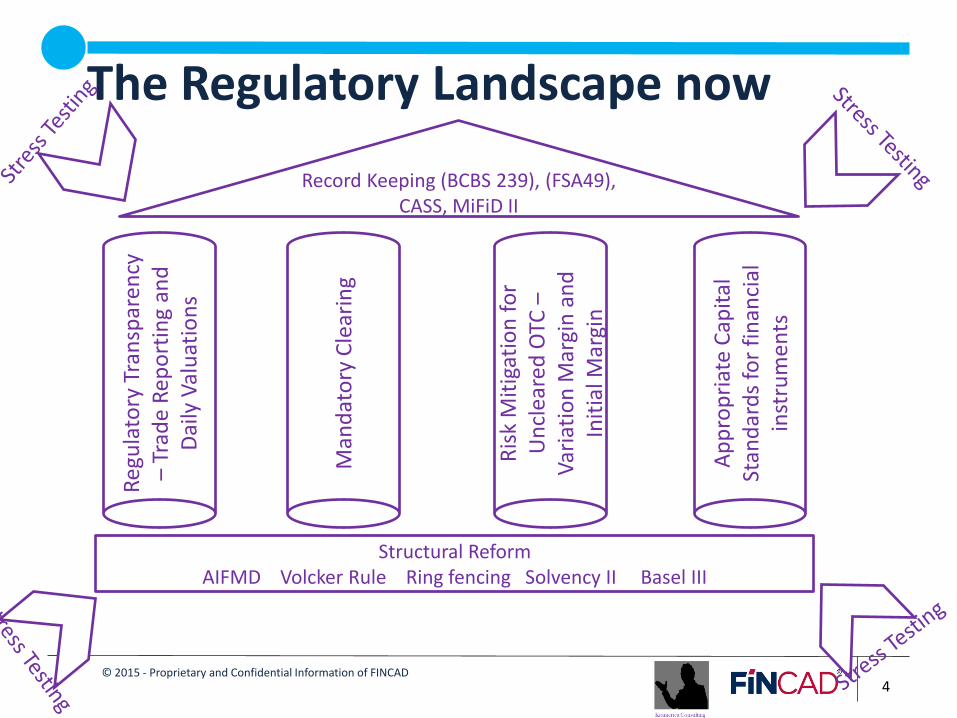

The Regulatory Landscape now

4

Man

dat

ory

Cle

arin

g

Structural Reform AIFMD Volcker Rule Ring fencing Solvency II Basel III

Record Keeping (BCBS 239), (FSA49), CASS, MiFiD II

Ris

k M

itig

atio

n f

or

Un

clea

red

OTC

–

Var

iati

on

Mar

gin

an

d

Init

ial M

argi

n

Ap

pro

pri

ate

Cap

ital

St

and

ard

s fo

r fi

nan

cial

in

stru

me

nts

Reg

ula

tory

Tra

nsp

aren

cy

– Tr

ade

Rep

ort

ing

and

D

aily

Val

uat

ion

s

Page 5

© 2015 - Proprietary and Confidential Information of FINCAD

Evolution of the Market post regulation

Source - http://www.bis.org/publ/qtrpdf/r_qt1312b.pdf

5

Page 6

© 2015 - Proprietary and Confidential Information of FINCAD

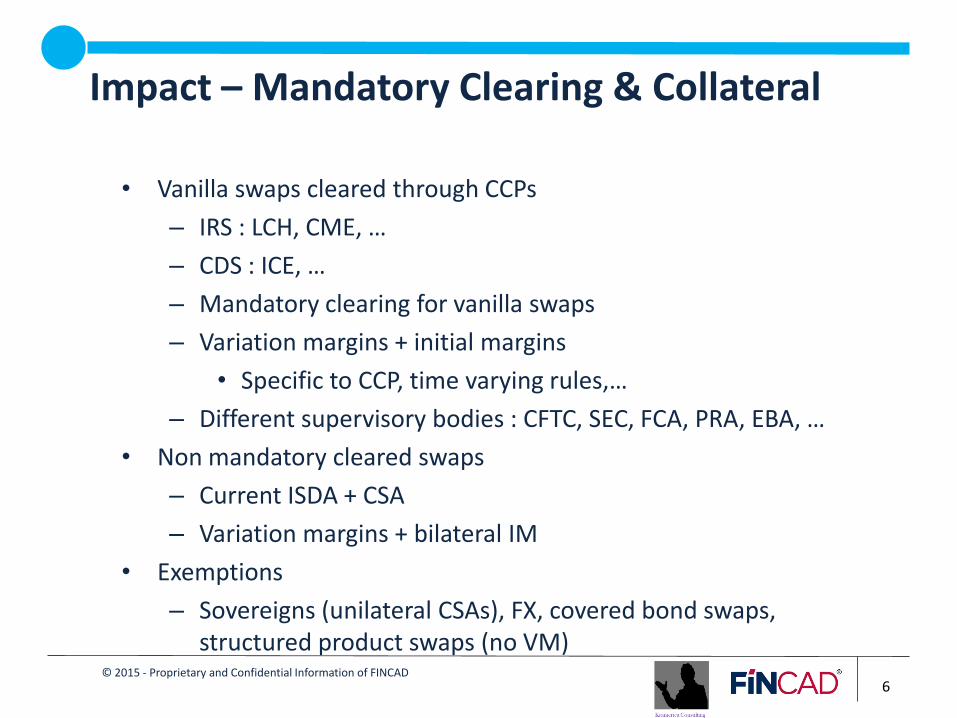

Impact – Mandatory Clearing & Collateral

• Vanilla swaps cleared through CCPs

– IRS : LCH, CME, …

– CDS : ICE, …

– Mandatory clearing for vanilla swaps

– Variation margins + initial margins

• Specific to CCP, time varying rules,…

– Different supervisory bodies : CFTC, SEC, FCA, PRA, EBA, …

• Non mandatory cleared swaps

– Current ISDA + CSA

– Variation margins + bilateral IM

• Exemptions

– Sovereigns (unilateral CSAs), FX, covered bond swaps, structured product swaps (no VM)

6

Page 7

© 2015 - Proprietary and Confidential Information of FINCAD

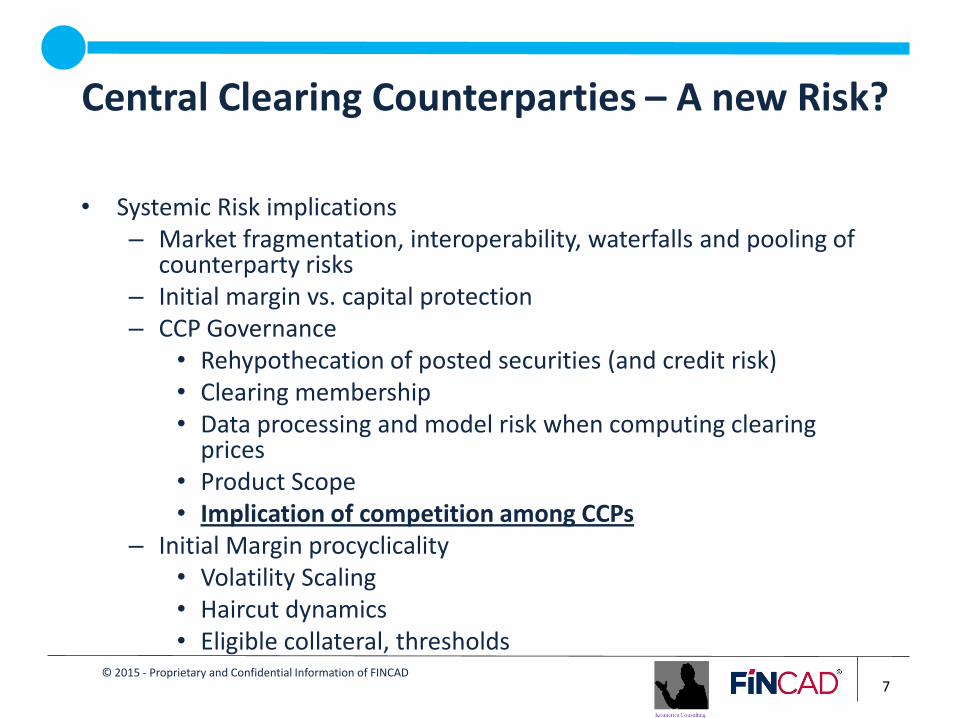

Central Clearing Counterparties – A new Risk?

• Systemic Risk implications – Market fragmentation, interoperability, waterfalls and pooling of

counterparty risks – Initial margin vs. capital protection – CCP Governance

• Rehypothecation of posted securities (and credit risk) • Clearing membership • Data processing and model risk when computing clearing

prices • Product Scope • Implication of competition among CCPs

– Initial Margin procyclicality • Volatility Scaling • Haircut dynamics • Eligible collateral, thresholds

7

Page 8

© 2015 - Proprietary and Confidential Information of FINCAD

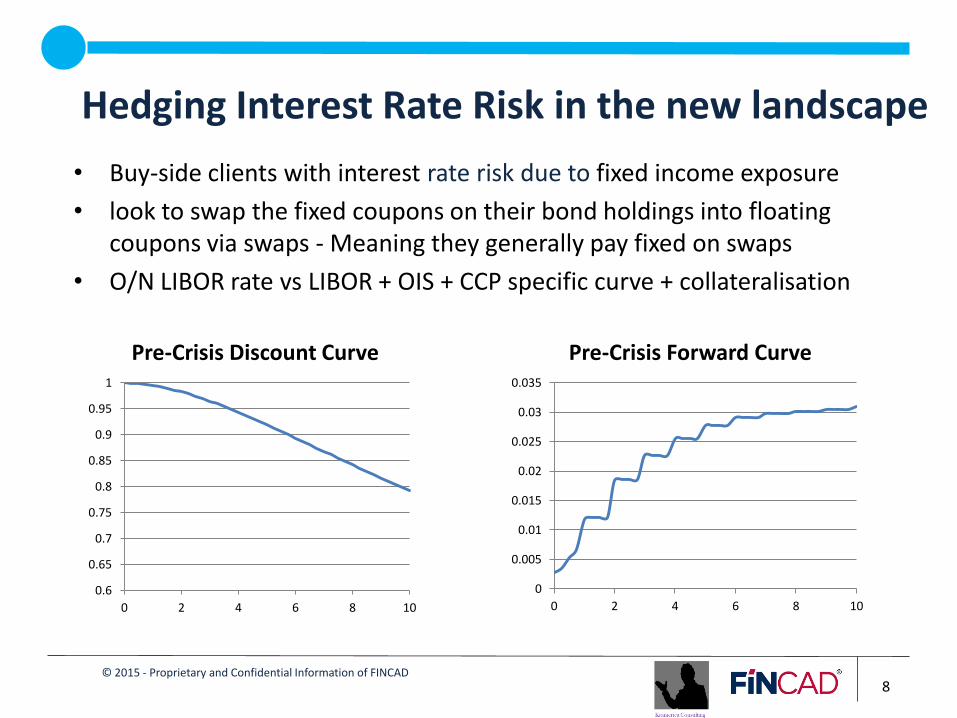

Hedging Interest Rate Risk in the new landscape

• Buy-side clients with interest rate risk due to fixed income exposure

• look to swap the fixed coupons on their bond holdings into floating coupons via swaps - Meaning they generally pay fixed on swaps

• O/N LIBOR rate vs LIBOR + OIS + CCP specific curve + collateralisation

8

0.6

0.65

0.7

0.75

0.8

0.85

0.9

0.95

1

0 2 4 6 8 10

Pre-Crisis Discount Curve

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0 2 4 6 8 10

Pre-Crisis Forward Curve

Page 9

© 2015 - Proprietary and Confidential Information of FINCAD

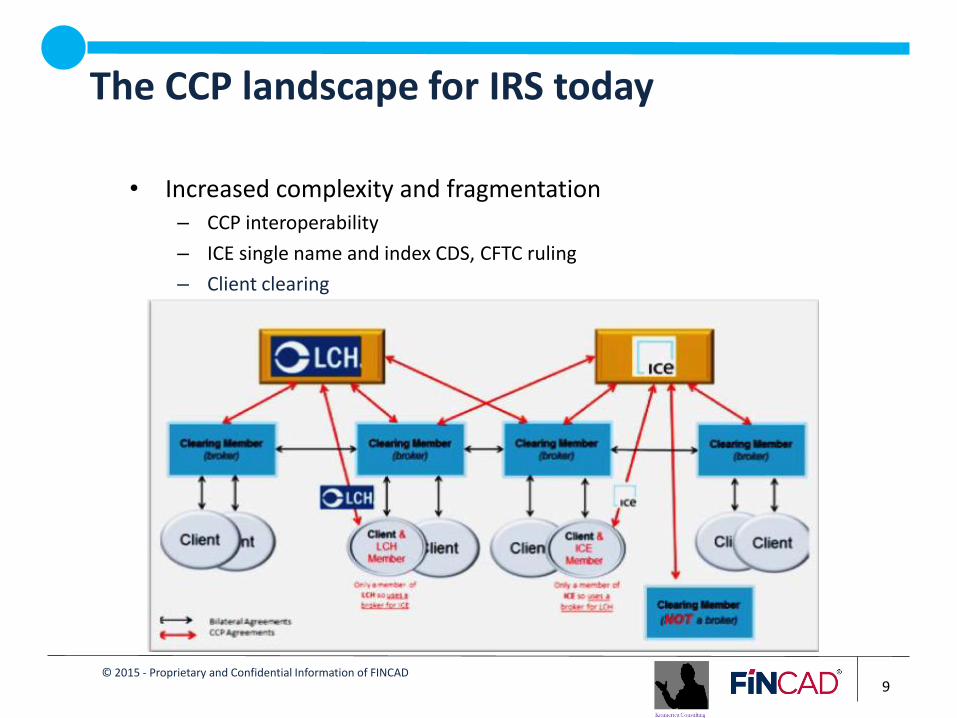

The CCP landscape for IRS today

• Increased complexity and fragmentation – CCP interoperability

– ICE single name and index CDS, CFTC ruling

– Client clearing

9

Page 10

© 2015 - Proprietary and Confidential Information of FINCAD

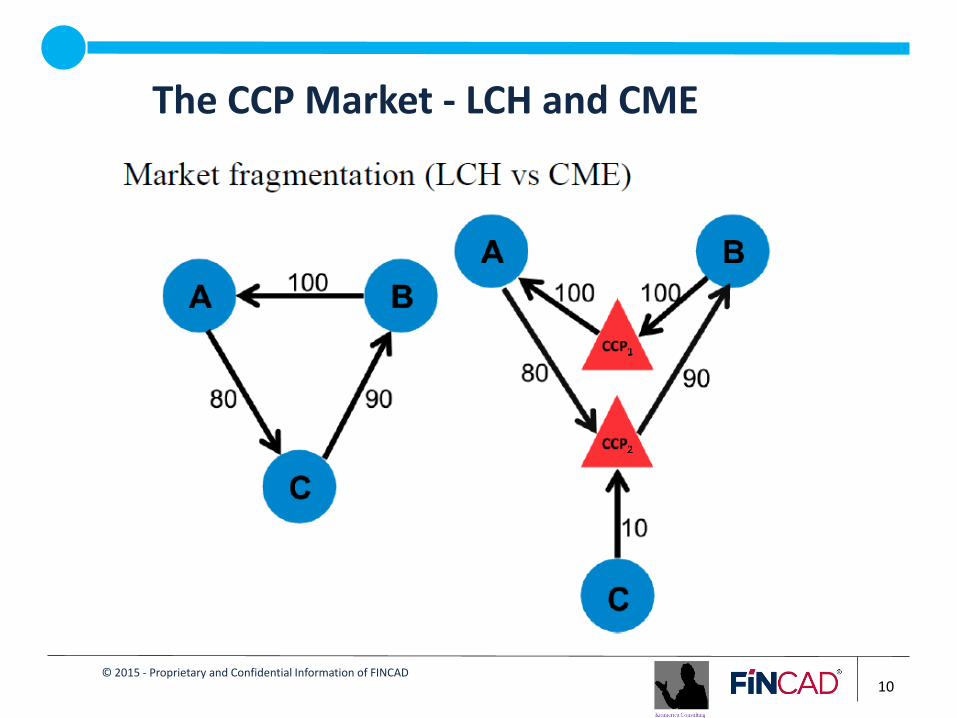

The CCP Market - LCH and CME

10

Page 11

© 2015 - Proprietary and Confidential Information of FINCAD

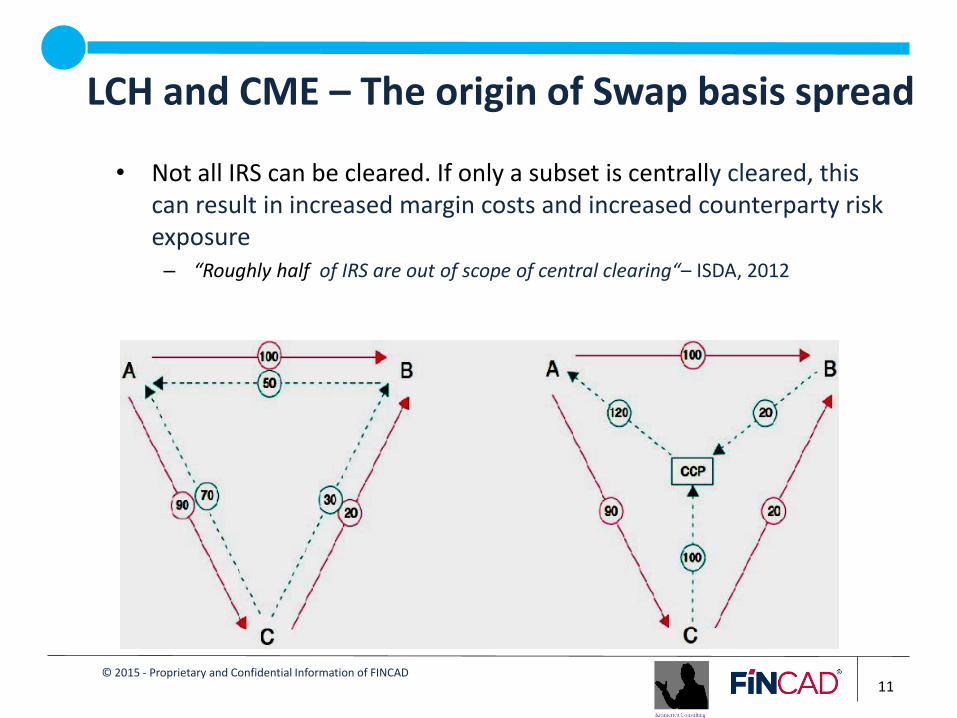

LCH and CME – The origin of Swap basis spread

• Not all IRS can be cleared. If only a subset is centrally cleared, this can result in increased margin costs and increased counterparty risk exposure – “Roughly half of IRS are out of scope of central clearing“– ISDA, 2012

11

Page 12

© 2015 - Proprietary and Confidential Information of FINCAD

The case for FVA

• Funding books of swaps – For fully collateralised contracts

• With no slippage risk at default • Discount rates are tied to the (expected) rate of return of posted

collateral (EONIA or Fed funds rates in the most common cases) • Calibration can be done on market observables with little

adaptation and thus little model risk - Collateralised OIS and Libor swaps, possibly futures’ rates

– Uncollateralised contracts • Generally a funding spread is used but may not be adequate • We miss out-of-the money swap prices to calibrate discount

factors – The funding rate

• Default-free : Funding/Lending rates essentially acts as the usual short-term rate

12

Page 13

© 2015 - Proprietary and Confidential Information of FINCAD

How F3 framework can help

1) Flexible Curve Modeling

1) Curve with OIS discounting

2) Curve with OIS discounting + CCP curves

3) Curve with OIS discounting + CCP curves + collateralisation – CVA/DVA/FVA

2) Risk Reprojection

1) Optimal Hedging of Interest Rate Risk based on Fixed Income Portfolios

2) Accounting for offsetting products like Futures

3) Scenario Analysis – Useful in Stress Testing for AIFMD/ Solvency II/Basel III

13

Page 14

© 2015 - Proprietary and Confidential Information of FINCAD

Flexible Curve Construction

Richard Weeks, Quantitative Analyst, FINCAD

Page 15

© 2015 - Proprietary and Confidential Information of FINCAD 15

Lazy Evaluation

Generic Calibration

Analytic risk

Scenario Analysis

Topical Example

1

2

3

4

5

Page 16

© 2015 - Proprietary and Confidential Information of FINCAD 16

Lazy Evaluation

Generic Calibration

Analytic risk

Scenario Analysis

Topical Example

1

2

3

4

5

Page 17

© 2015 - Proprietary and Confidential Information of FINCAD 17

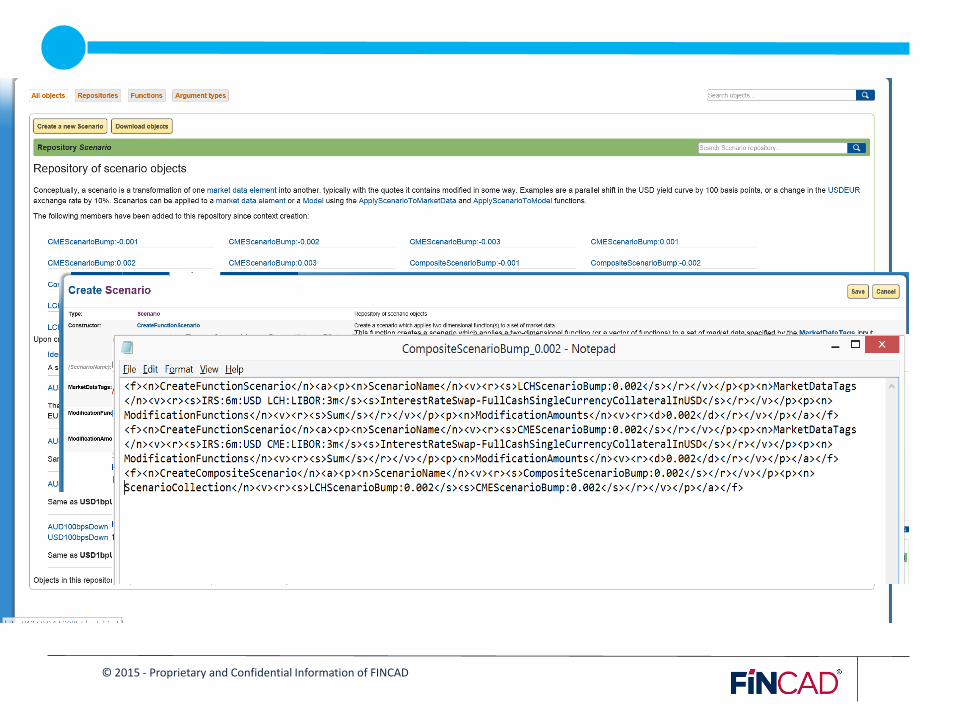

F3 Object Model Overview

Page 18

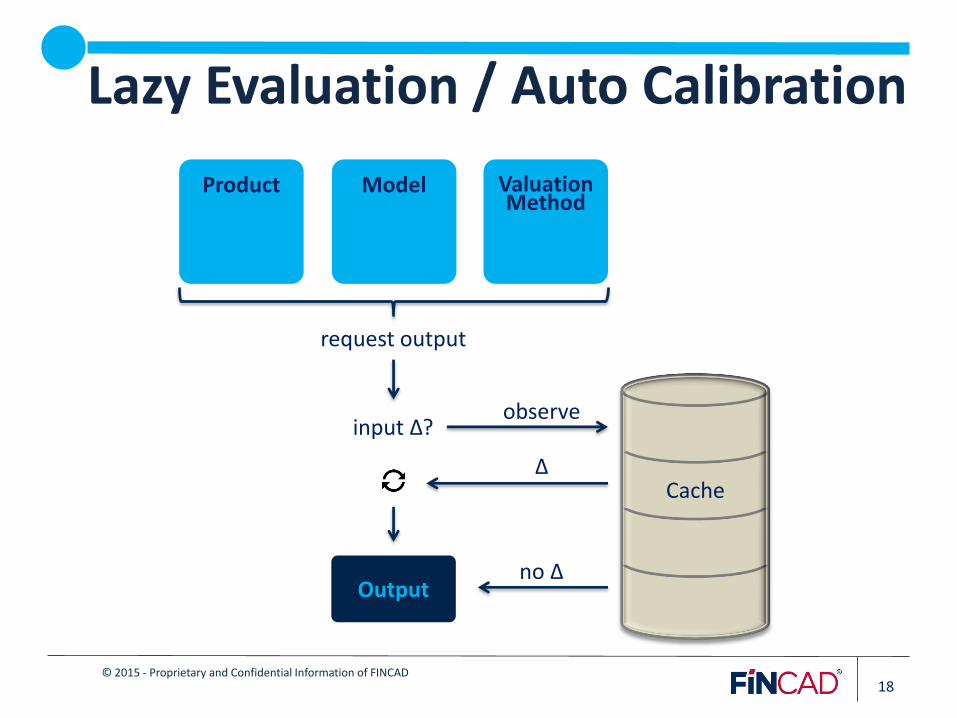

© 2015 - Proprietary and Confidential Information of FINCAD 18

Lazy Evaluation / Auto Calibration

Product Model Valuation Method

input Δ?

request output

observe

Δ

no Δ

Cache

Output

Page 19

© 2015 - Proprietary and Confidential Information of FINCAD 19

Lazy Evaluation

Generic Calibration

Analytic risk

Scenario Analysis

Topical Example

1

2

3

4

5

Page 20

© 2015 - Proprietary and Confidential Information of FINCAD

Model Calibration

Valuation approach

A

Valuation Approach

B

20

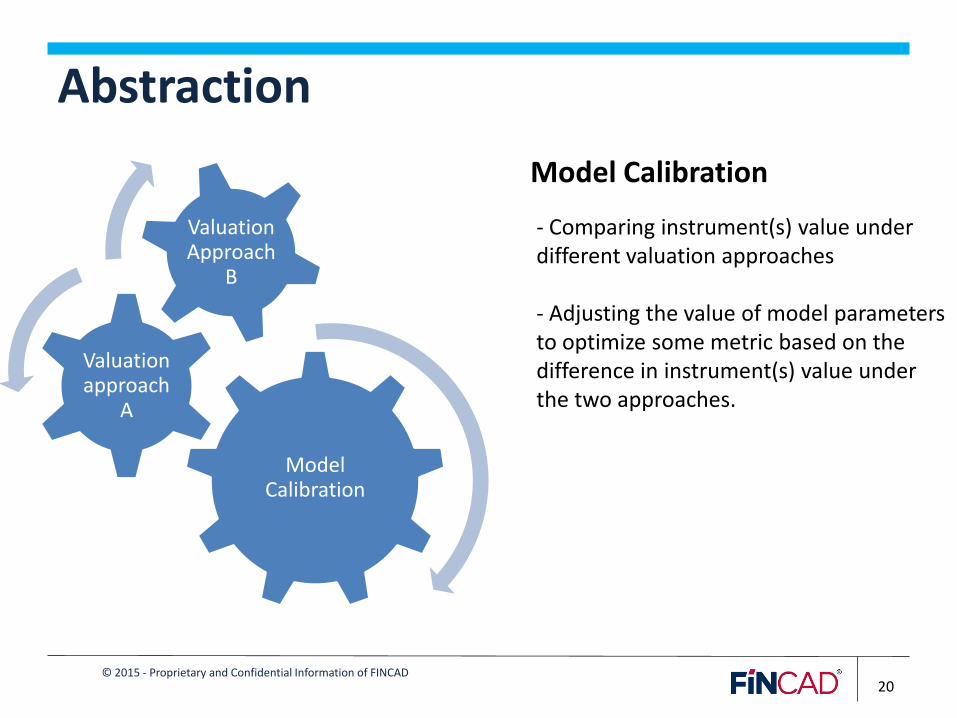

Abstraction

- Comparing instrument(s) value under different valuation approaches - Adjusting the value of model parameters to optimize some metric based on the difference in instrument(s) value under the two approaches.

Model Calibration

Page 21

© 2015 - Proprietary and Confidential Information of FINCAD 21

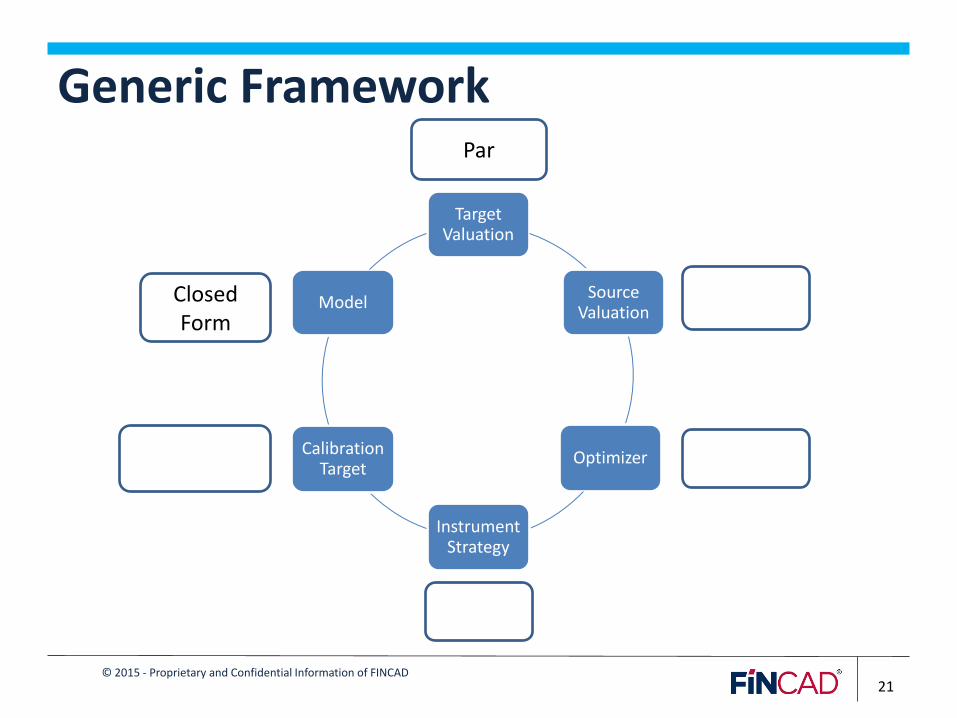

Generic Framework Par

Closed Form

Closed Form Closed Form

Closed Form

Closed Form

Target Valuation

Source Valuation

Optimizer

Instrument Strategy

Calibration Target

Model

Page 22

© 2015 - Proprietary and Confidential Information of FINCAD 22

Hybrid modeling challenges

Generic Calibration

Analytic risk

Scenario Analysis

Conclusion

1

2

3

4

5

Page 23

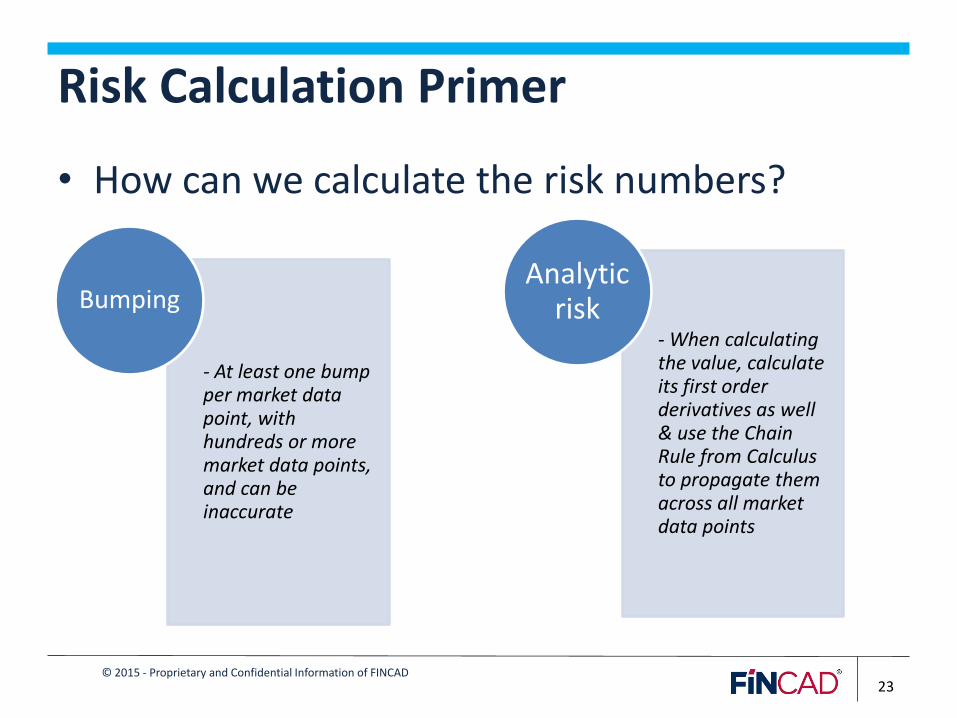

© 2015 - Proprietary and Confidential Information of FINCAD

• How can we calculate the risk numbers?

23

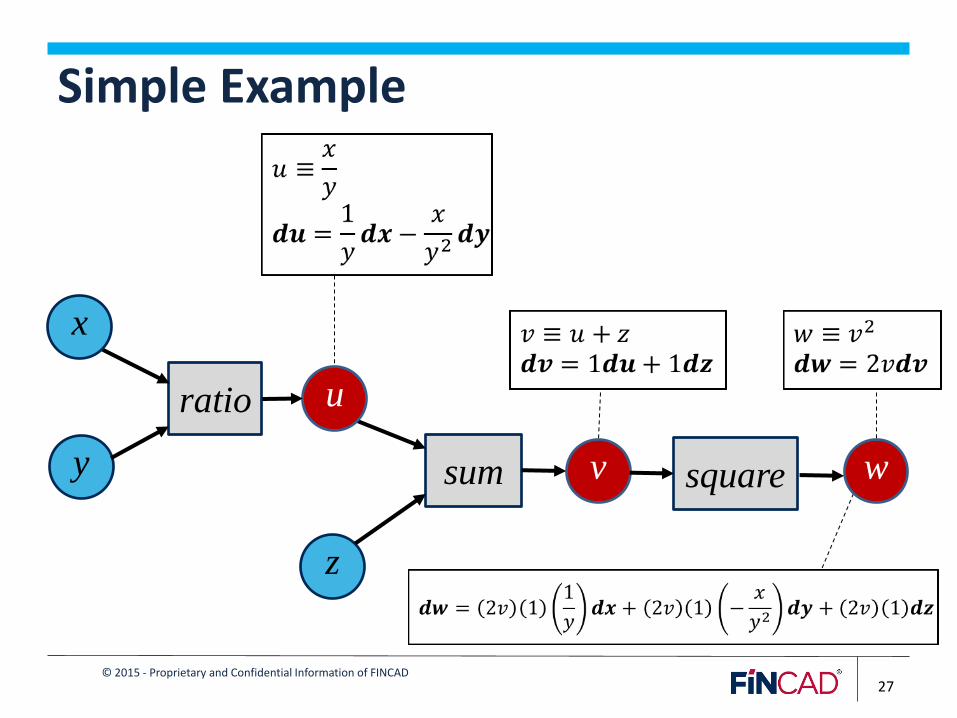

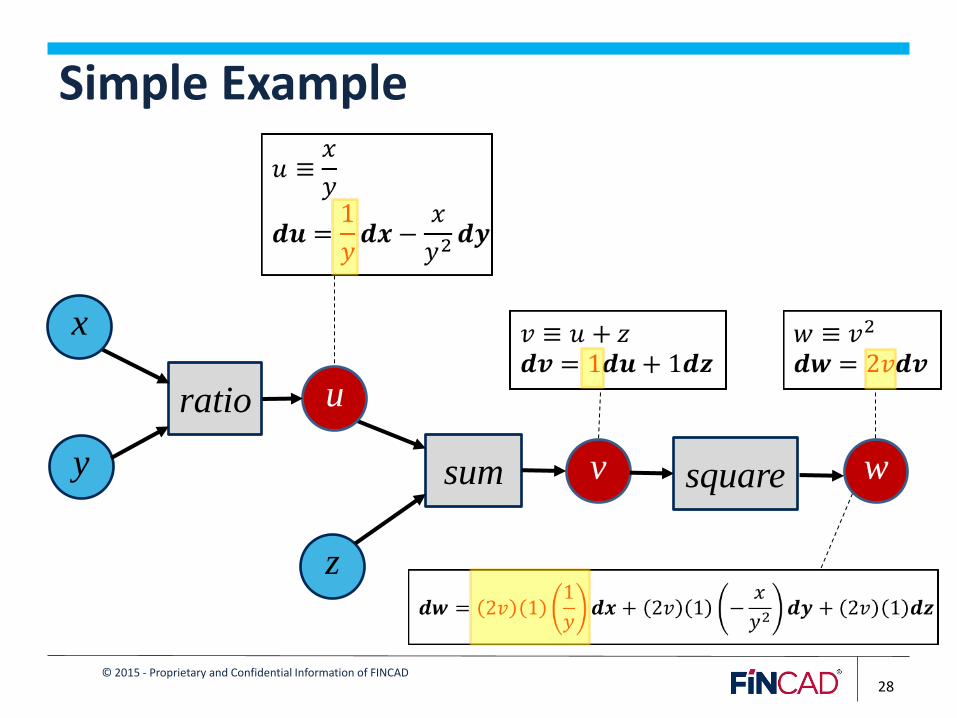

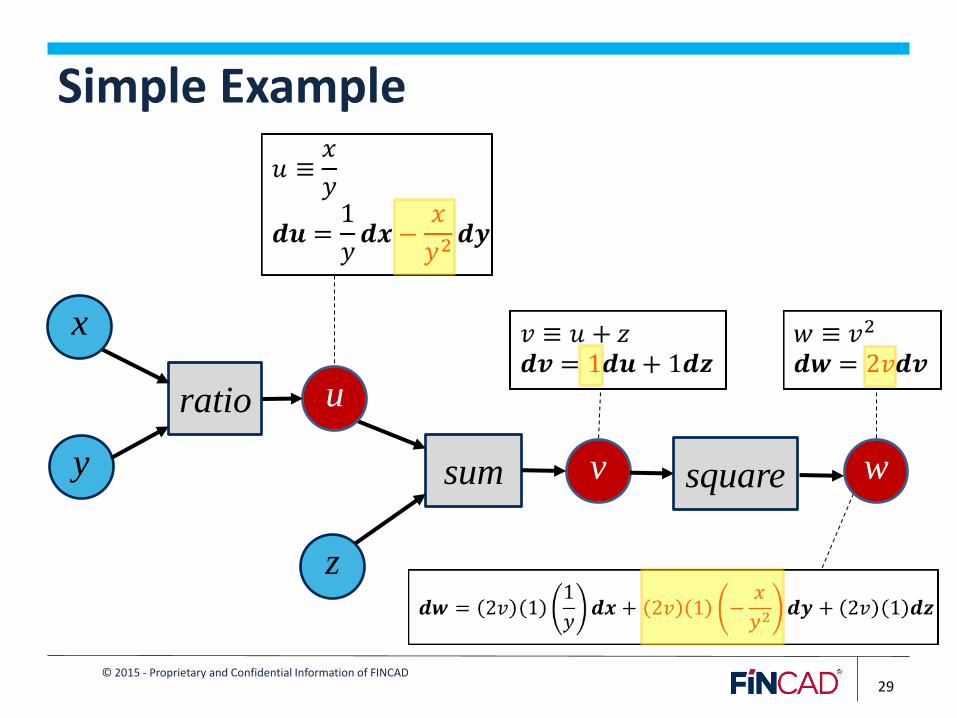

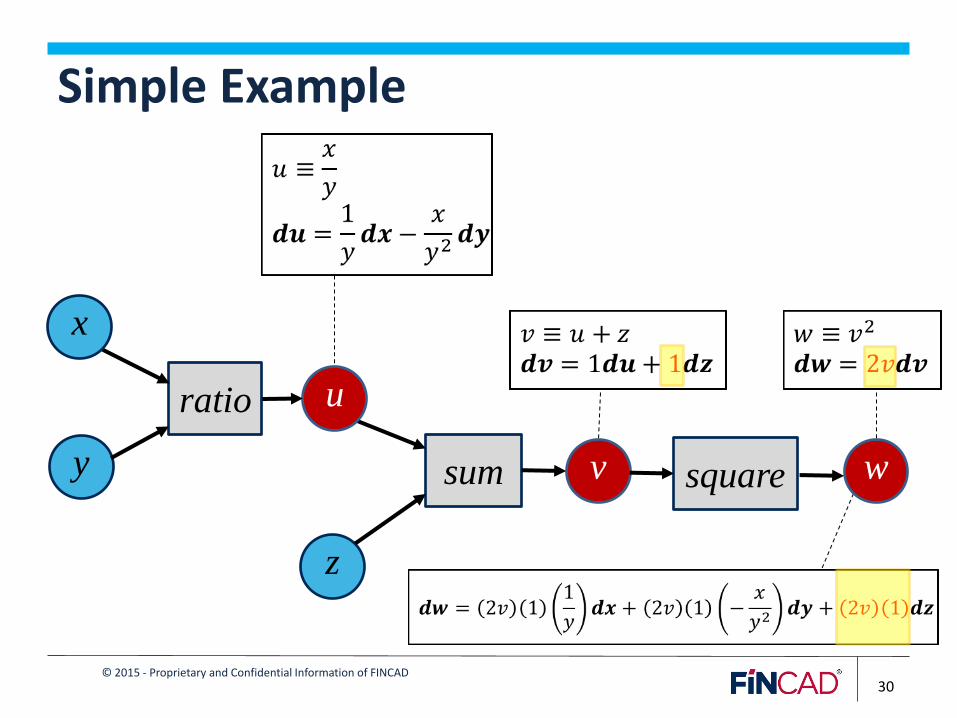

Risk Calculation Primer

- At least one bump per market data point, with hundreds or more market data points, and can be inaccurate

Bumping

- When calculating the value, calculate its first order derivatives as well & use the Chain Rule from Calculus to propagate them across all market data points

Analytic risk

Page 24

© 2015 - Proprietary and Confidential Information of FINCAD 24

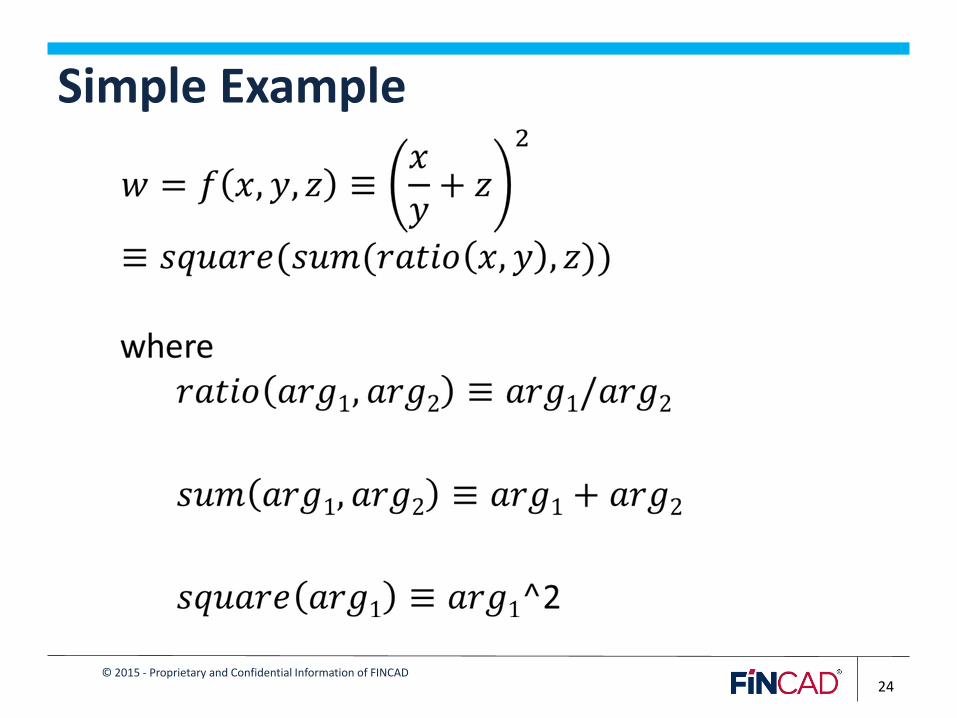

Simple Example

Page 25

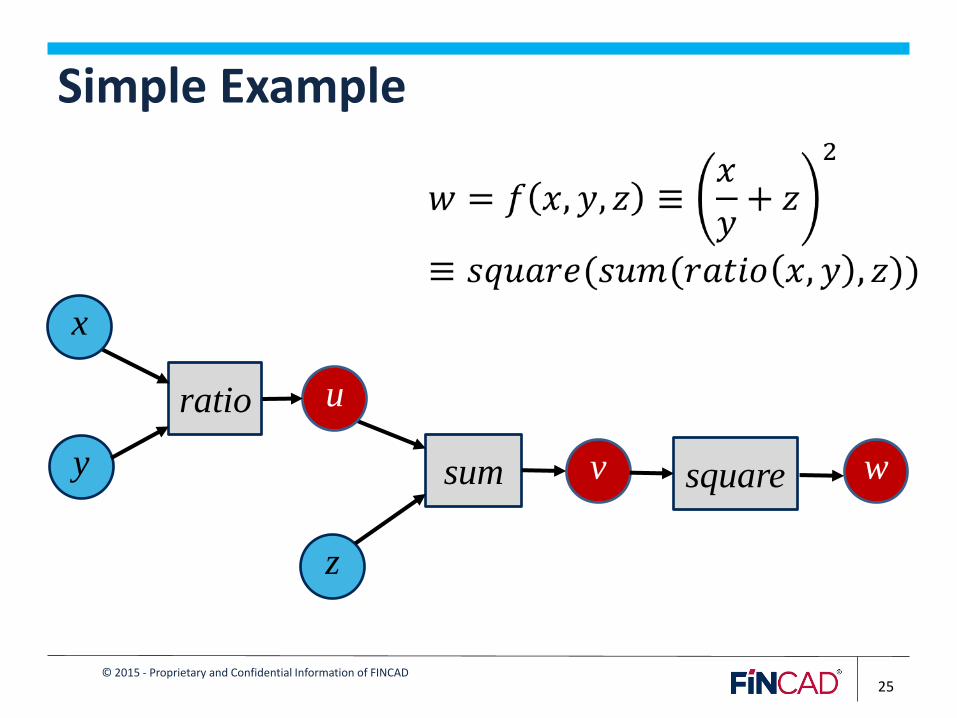

© 2015 - Proprietary and Confidential Information of FINCAD 25

Simple Example

sum w y

ratio

square

z

u

v

x

Page 26

© 2015 - Proprietary and Confidential Information of FINCAD 26

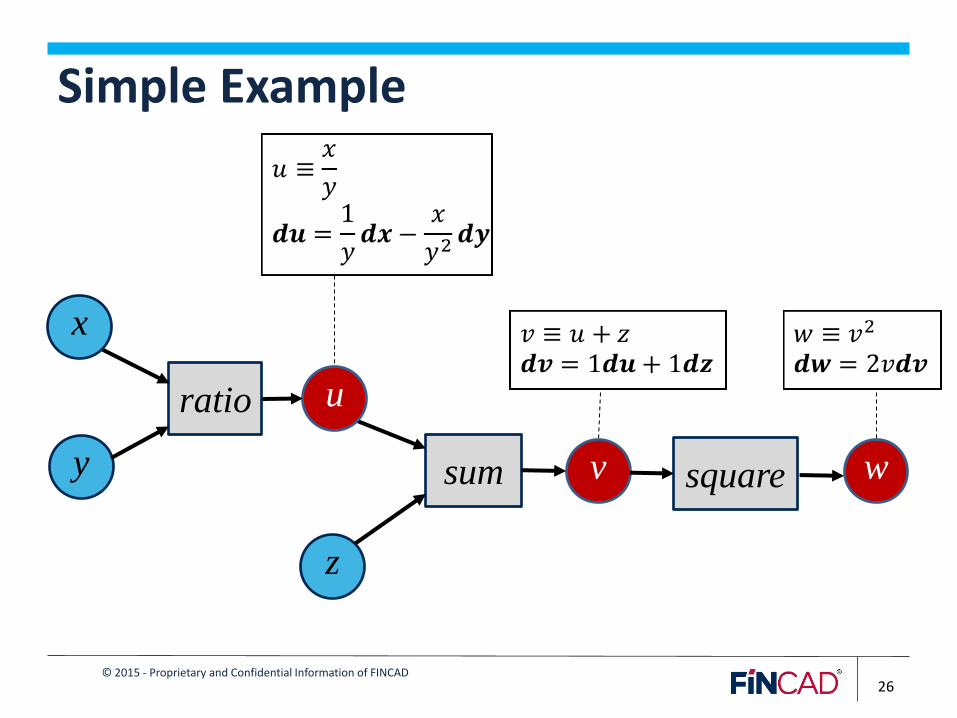

Simple Example

sum w y

ratio

square

z

u

v

x

Page 27

© 2015 - Proprietary and Confidential Information of FINCAD 27

Simple Example

sum w y

ratio

square

z

u

v

x

Page 28

© 2015 - Proprietary and Confidential Information of FINCAD 28

Simple Example

sum w y

ratio

square

z

u

v

x

Page 29

© 2015 - Proprietary and Confidential Information of FINCAD 29

Simple Example

sum w y

ratio

square

z

u

v

x

Page 30

© 2015 - Proprietary and Confidential Information of FINCAD 30

Simple Example

sum w y

ratio

square

z

u

v

x

Page 31

© 2015 - Proprietary and Confidential Information of FINCAD

• Universal Algorithmic Differentiation (UAD) ™ – Automatically calculates the 1st order partial

derivatives without bumping

– Minimal incremental computing cost

– Numerical stability

31

Analytic Risk

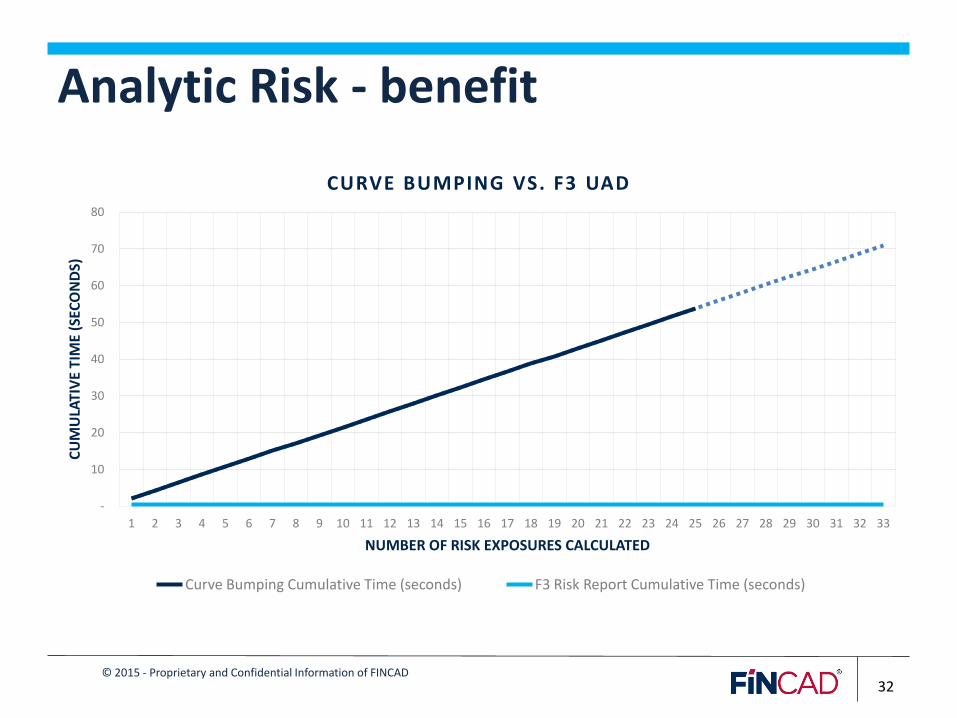

Page 32

© 2015 - Proprietary and Confidential Information of FINCAD

32

Analytic Risk - benefit

-

10

20

30

40

50

60

70

80

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33

CU

MU

LATI

VE

TIM

E (S

ECO

ND

S)

NUMBER OF RISK EXPOSURES CALCULATED

CURVE BUMPING VS. F3 UAD

Curve Bumping Cumulative Time (seconds) F3 Risk Report Cumulative Time (seconds)

Page 33

© 2015 - Proprietary and Confidential Information of FINCAD 33

Lazy Evaluation

Generic Calibration

Analytic risk

Scenario Analysis

Topical Example

1

2

3

4

5

Page 34

© 2015 - Proprietary and Confidential Information of FINCAD

• Generic scenario framework that enables: – Creation of simple and complex hybrid scenarios

– Global scenarios spanning asset classes & stress factors

– Run stress-tests on entire portfolio

• Store definitions and output results – Defensible audit trail & granular risk analysis

34

Scenario Generation

Page 35

© 2015 - Proprietary and Confidential Information of FINCAD

Page 36

© 2015 - Proprietary and Confidential Information of FINCAD

UAD risk computation efficiency with Risk Reprojection. An example, If you want to hedge multiple term-structure exposures using zero-coupon bonds for the respective term structures. • How F3 constructs a reprojected model from the original model,

extracting the risk -report that will give exposures, reprojecting the risk to a new set of instruments that were specified in the reprojected model

• Result No need to re-define market data in this new reprojected

model since it is built from the original model, which contains the market data.

36

F3 Risk Reprojection

Page 37

© 2015 - Proprietary and Confidential Information of FINCAD 37

Lazy Evaluation

Generic Calibration

Analytic risk

Scenario Analysis

Topical Example

1

2

3

4

5

![LCH SA CDS Clearing Rule Book - SECFile No. SR-LCH SA-2017-010 Page 44 of 482 _____ LCH SA © 2017 44 Published on [ ]2017 Table of](https://static.documents.pub/doc/80x56/60a41f885b2c7877a65f67af/lch-sa-cds-clearing-rule-book-sec-file-no-sr-lch-sa-2017-010-page-44-of-482-.jpg)